world bank documentdocuments.worldbank.org/curated/en/... · finance and private sector development...

TRANSCRIPT

Document ofThe World Bank

FOR OFFICIAL USE ONLY

Report No: 19104

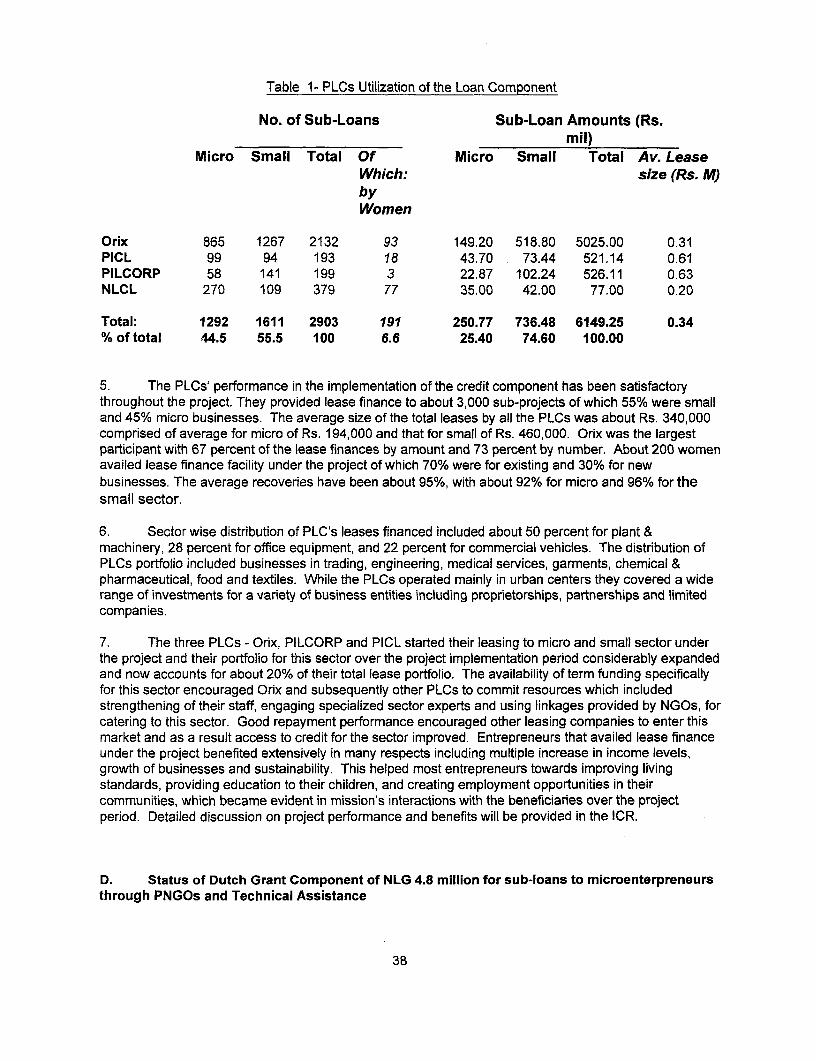

IMPLEMENTATION COMPLETION REPORT

ISLAMIC REPUBLIC OF PAKISTAN

MICROENTERPRISE PROJECT

(LOAN 3318 -PAK)

March 10, 1999

Finance and Private Sector DevelopmentSouth Asian Region

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosedwithout World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTCurrency Unit - Pakistan Rupee (Rs)

(annual average)

Rs. Per US $1.00 US $ Per Rs. 1.001987 17.399 0.05741988 18.003 0.05551989 20.541 0.04861990 21.707 0.0460

1991 23.801 0.0420

1992 25.083 0.03901993 28.107 0.03551994 30.567 0.03271995 31.430 0.03161996 '36.09 0.02771997 38.89 0.02571998 45.38 0.0220

ABBREVIATIONS

ABL Allied Bank LimitedADI AlFalah Development InstituteADB Asian Development BankAKRSP Agha Khan Rural Support ProgramBEL Bankers EquityBUSTI Basic Urban Services for Katchi Abadies

BRSP Balochistan Rural Support Program

FSAL Financial Sector Adjustment Loan

FSDIP Financial Sector Deepening & Intermediation Project

GON Government of NetherlandsGOP Government of PakistanHBL Habib Bank LimitedIBRD International Bank for Reconstruction and Development

NCB Nationalized Commercial Bank

NLC Network Leasing CompanyNLG Netherlands GuilderNGO Non Governmental OrganizationOLP Orix Leasing PakistanOPP Orangi Pilot ProjectPNGO Participating NGOPLC Participating Leasing CompanyPILCORP Pakistan Industrial Leasing CorporationPICL Pakistan Industrial and Commercial Leasing

PFI Participating Financial InstitutionSBP State Bank of PakistanTA Technical Assistance

FISCAL YEARS

GOP and BEL = July I to June 30

OLP, PILCORP, PICL and NLC -January 1 to December 31

Vice President: Ms. Mieko Nishimizu

Country Director: Mr. Sadiq Ahmed

Sector Manager: Ms. Marilou Uy

Team Leader: Mr. Joseph Pernia

Task Manager: Mr. Mudassir Khan

FOR OFFICIAL USE ONLY

IMPLEMENTATION COMPLETION REPORTISLAMIC REPUBLIC OF PAKISTAN

MIROENTERPRISE PROJECT(LOAN 3318-PAK)

Page No.

PREFACE TABLE OF CONTENTS

EVALUATION SUMMARY i

PART I: PROJECT IMPLEMENTATION ASSESSMENT

A Introduction 1B Statement/Evaluation of Objectives 1C Achievement Of Objectives 3D Major Factors Affecting The Project 8E Project Sustainability 8F Bank's Performance 9G Borrower's Performance 9H Assessment of Outcome 10I Follow-up Operations 10J Main Lessons Learned 11

PART Il: STATISTICAL TABLES

Table 1 Summary Of Assessments 13Table 2 Related Bank Loans/Credits 14Table 3 Project Timetable 15Table 4 Loan/Grant Disbursements: Cumulative Estimated And Actual 16Table 5 Key Indicators For Project Implementation 17Table 6 Key Indicators For Project Operation 18Table 7 Studies Included in Project 19Table 8A Project Costs 20Table 8B Project Financing 20Table 9 Economic Costs and Benefits 21Table 10 Status of Main Legal Covenants 21Table 11 Compliance With Operational Manual Statements .22Table 12 Bank Resources: Staff Input 22Table 13 Bank Resources: Missions 23

This document has a restricted distribution and may be used by recipients only inthe performance of their official duties. Its contents may not otherwise bedisclosed without world Bank authorization.

ANNEXES

Annex I Lease Disbursement 24Annex li Lease Characteristics 25Annex IlIl Geographical & Sub-sectoral Distribution of leases financed 26Annex IV Type of assets leased 27Annex V Lease Disbursement to Women Sponsors 28Annex VI PLC's Recovery Performance 29Annex VII PLC's cost of leasing operation as percentage of amount disbursed 29Annex VIII Dutch Grant: Sub-loan disbursement 30Annex IX Dutch Grant: Sub-sectoral Distribution 31Annex X Dutch Grant: Recovery Performance 32Annex XI Dutch Grant: Women sponsors financed 32Annex XII Dutch Grant: Disbursement Summary 33Annex XIII Dutch Grant: Sub-loan terms 34Annex XIV Examples of project impact on microenterprises 35Annex XV Project's impact on PLC's portfolio 36

APPENDIX

Appendix A ICR Mission Aide-Memoire 37Appendix B Project Review From Borrowers Perspective 41

PROJECT IMPLEMENTATION COMPLETION REPORT

ISLAMIC REPUBLIC OF PAKISTAN

Microenterprise Project(Ln 3318-PAK)

PREFACE

This is the Implementation Completion Report (ICR) for the Microenterprise Project(Ln.3318) in the amount of US $ 26 million IBRD Loan and DFL 4.8 million Dutch Grant forsub projects and technical assistance approved on April 23, 1991 and made effective on April 30,1992. The project closed as originally scheduled on June 30,1998. Final transaction under theLoan took place on October 31, 1998 with total disbursement of US$25.97 million andcancellation of US$0.03 million. Final transaction under the Dutch Grant took place on May 5,1998, with total disbursement of DFL 4.8 million utilizing the Grant fully.

The ICR was prepared by Mudassir Khan (Task Leader), Shideh Hadian ( OperationsOfficer) and Ainul Hassan Qureshi (Consultant), and reviewed by Joseph Pernia (Team Leader),Finance and Private Sector Development, Abid Hasan, Principal Operations Officer, IslamabadOffice, Rie Hiraoka (SASHP) and peer reviewers Joselito Gallardo (FSD) and Carlos Cuevas(AFTP1).

Preparation of this ICR was begun after the Bank's final supervision/completion missionin May, 1998 by collecting data from the concerned institutions. It is based on Staff AppraisalReport, Loan Agreement, Supervision Reports and other material in the project files. Theborrower contributed to the preparation of the ICR by preparing the data on different componentsof the project, commenting on the draft ICR and preparing independent evaluation which isincluded as Appendix to the ICR. Co-financier -Netherlands Government, also, contributed byreviewing and commenting on the draft ICR.

IMPLEMENTATION COMPLETION REPORTISLAMIC REPUBLIC OF PAKISTAN

MICROENTEREPRISE PROJECT(LOAN 3318-PAK)

EVALUATION SUMMARY'

Introduction

1. The Bank's earlier projects in small, medium and large scale industry had assisted Pakistanthrough loans and credits for the development of industrial and services sectors. These projects,however, did not address the needs of the growing microenterprise sub-sector. The MicroenterpriseProject was, therefore, designed as a pilot to provide support and focused on critical constraintsbeing faced by this sub-sector. The Project attempted to build experience by associating with theprivate sector institutions already having direct business relations with microenterprises includingNGOs and leasing companies for strengthening their business capacity and for reaching a largerconstituency in the sub-sector (para 1).

Project Objectives

2. The Microenterprise Project was designed to provide credit, through formal financial sector,to the micro and small scale entrepreneurs for their capital investment and to assist this sector, inparticular women entrepreneurs to improve their living conditions by engaging in income generatingactivities. The specific project objectives were: a) to strengthen the capacity of participatinginstitutions in delivering financial and technical/social services to microenterprises; b) to assist theseinstitutions to deliver their services to a larger constituency of microenterprises; c) to broaden themenu of financial instruments available for microenterprises in the upper stratum, by promoting theinitiative to market leasing to sub-contractors of small-scale businesses; d) to catalyze NGOs'financial, technical and social support services for microenterprises in the lower stratum; e) todemonstrate the replicability of the NGOs and leasing initiatives to others, including the commercialbanks who could potentially see microenterprises in the middle to upper stratum as a promisingmarket niche; f) to demonstrate the creditworthiness of microenterprises, including and particularlywomen, at market prices and practices; and g) to promote the development of businesses owned andoperated by women.

3. Under the project, US$ 26.0 million equivalent, was on-lent by GOP, administered byBankers Equity Limited (BEL) as the apex institution, to the Participating Leasing Companies(PLCs), at a variable interest rate including foreign exchange risk cover fee and GOP'sadministrative charges. The PLCs financed productive assets, at prevailing market rates, ofestablished and profitable micro and small enterprises (MSEs); however, for women entrepreneurs,start-up projects were also eligible to encourage their participation in development activities. TheBank Loan was co-financed by Government of Netherlands (GON) for a total of NLG 4.8 million(US$ 2.8 million equivalent) grant. The grant was allocated for: (i) NGOs as seed capital for theirrevolving credit operations (NLG 2.8 million or US$ 1.6 million equivalent): and (ii) institutional

Provides cross reference to paragraphs from Part I of ICR.

i

capacity building of NGOs through staff training and adapting and upgrading their credit proceduresand supervision information system (NLG 2.0 million or US$ 1.2 million equivalent).

Implementation Experience

4. The project was approved by the Board in April 1991 and became effective almost a yearlater. The delay was due to lack of familiarity of participating institutions with GOP and Bankprocedures and additionally GOP had to devise new procedures for participation by the privatesector, particularly NGOs.

5. Initially, the loan was made to one leasing company Orix Leasing Pakistan (OLP). In 1995two more leasing companies, Pakistan Industrial Leasing Corporation (PILCORP) and PakistanIndustrial and Commercial Leasing (PICL), which had also started leasing to micro-enterprises wereappraised by the Bank and started participation under the project. In May 1997, Network LeasingCorporation Limited (NLCL) was also appraised and selected to participate in the project. With fourPLCs participating in the project, the Loan was fully disbursed (para 8).

6. Performance of BEL as administrator of the project was satisfactory, except that they did notperform some of the responsibilities originally assigned (para 10). BEL carried out a check oneligibility criteria on refinance applications forwarded by the PLCs to the Bank for clearance andreimbursement. It maintained the Special Account and handled disbursements to the PLCs inaddition to collecting repayments from PLCs for the GOP account. BEL, also, helped the Bank inmonitoring continued eligibility for participation of the PLCs in the Project. Finally, BEL providedthird party guarantees to GOP for repayment of the Loan funds on lent to PLCs in accordance withparticipation agreements.

7. The PLCs' performance during project implementation remained satisfactory. Loan recoveryby PLCs, on average, was 95 percent (para 7 & 11), which is highly satisfactory. The PLCs tookconcrete measures to build their institutional capacity to meet the needs of the MSEs and the Bank'srequirements (para 11), financing about 2900 leases (para 9). It is estimated that nearly 2 jobs werecreated per lease on average resulting in investment per job of about US$ 5,000. In case of NLCLwhich caters mainly to the microenterprise sector, investment per job was only about US$ 1,000. Inthe process PLC's also strengthened their capacity for lending to MSEs and their portfolio in microand small scale sector considerably expanded during the project implementation and now accountsfor about 20% of their total lease portfolio.

8. Implementation of Dutch Grant Component - NLG 2.8 million of the Dutch Grant wasoriginally allocated to four NGOs as revolving fund for their credit operations to remain financiallyself-sustaining. The participating NGOs (PNGOs) comprising Agha Khan Rural Support Program(AKRSP), Orangi Pilot Project (OPP), Basic Urban Services for Katchi Abadies (BUSTI) andAlFlah Development Institute (ADI) made short/medium term loans to micro and smallestablishments at prevailing market rates for income generating activities. In 1994, ADI wasdisqualified due to non compliance with minimum participation criteria (para 13). In 1995,Balochistan Rural Support Program (BRSP) was appraised and found eligible to participate in theproject (para 13). Due to higher demand for sub-loans, the Grant was reallocated increasing thesub-loan component to NLG 4.25 million and reducing the TA to 0.55 million (para 13). The

ii

PNGOs utilized the entire allocation on first come first served basis and provided sub-loans to about7,000 micro entrepreneurs, and creating estimated 10,000 new jobs. The recoveries were 90-94%except BRSP (para 13, 14). The TA was utilized for capacity building of BUSTI and two studiescomprising a sector study and evaluation of participating institutions performance (para 16). Finally,based on satisfactory experience under the project, the Bank has decided to continue association withNGOs on a larger scale by participating in the upcoming Pakistan Poverty Alleviation Fund.

Results and Performance

9. The project outcome is satisfactory. All objectives (para 2) have been achieved bysuccessful participation of leasing companies and NGOs in providing access to credit to the MSEsector, particularly, microenterprises as described below:

Objective (a): The PLCs strengthened their capacity for delivering the required financialservices by adopting measures which included (i) creating a cell to carry out research in themicroenterprise sector through collaboration with NGOs, (ii) established of new microenterprisedepartments, (iii) translation of lease documents and materials into local language - Urdu, (iv)development of credit appraisal and monitoring systems for micro and small enterprises, (v)development of marketing strategy and techniques for better servicing of the sector and expandingtheir outreach, and (vi) staff training. The capacity for delivering technical/social advisory servicesto microenterprises was strengthened by engaging consultants for field work, and associating theirown staff for training. Under the project, services for development of marketing, accounting andmanagement skills were also provided to the enterprises (para 11). Increased lending to MSEstogether with satisfactory repayment performance confirms successful delivery of the extensionservices envisaged under the project objectives.

Objective (b): Before participation in the project, the PLCs were catering to the needs ofmicroenterprises to a very modest extent. The Bank Loan assisted the participating institutions toreach a much larger constituency of microenterprises which financed 1275 leases amounting to 44%of the total under the Loan (para 9). PICL and PILCORP started leasing to the microenterprisesector based on demonstrated success of OLP under the project and NLCL was set up primarily tocatering to this sector and financed two and a half times more micro leases compared with SSIs.Also, the Loan has been advanced to the PLCs for 10 years while the average lease life is threeyears, permitting roll over of these funds and project impact by more than three times (para 9).

Objective (c): The consultants engaged by the PLCs helped in identification of sub-contractors of small scale businesses and explained the advantages of lease financing. Leasingproved to be a viable financing mechanism increasing access to capital assets for this sector.Achievement of the project objective is confirmed by the PLCs' financing not only about 2900 leasesunder the project but increasing their overall MSE lease portfolio by about 100% in amount. In caseof three of the PLCs, their overall MSE lease portfolio increased by about four times in number (para11).

Objective (d): PNGOs considerably increased their outreach and catered to the financingneeds of about 7,000 sub-borrowers under the project. In addition, PNGOs further played a catalystrole by associating with and training other NGOs and CDOs (Community Development

111

Organizations), including funding, technical and other support services to microenterprises (para 15).The PNGO, also, utilized services of agents and technical experts for support services. Finally, thesub-loans provided by the PNGOs were instrumental in extending highly significant benefits to thelower stratum communities (para 17).

Objective (e): Based on the experience of OLP, three more leasing companies joined asPLCs during project implementation, one of which - NLCL was established primarily for leasing tomicroenterprises. As a result, PLC's outreach significantly increased in this sector. Based ondemonstrated credit worthiness of microenterprises at market rates and practices (para 9,11,12) asenvisaged under the project objectives, some commercial banks have not only expressed interest inparticipation in future projects but have started lending to microenterprises on a pilot scale.Furthermore, TA provided to BUSTI helped establish it as a successful lender to microenterprises.Based on demonstration of lending to micro- enterprises as promising, many other NGOs startedmicrocredit operations, Kashf being notable among them was setup solely for this purpose.

Objective a): Utilization of a substantial share of the Loan and full utilization of the sub-loancomponent of the Grant funds by microenterprises, including women entrepreneurs at market pricesand practices, together with satisfactory repayment performance demonstrates their credit worthiness(para 9, 11, 12). Performance of women entrepreneurs who established new businesses under theproject was, also, satisfactory indicating achievement of the project objective.

Objective (g): About 7% of the total lease contracts were for women entrepreneurs. In fact,three of the PLCs increased their lending to women entrepreneurs three times under the project,while, the fourth only started lending to them to a significant extent under the project (para 9). ThePNGOs also, lent about a quarter of the sub-loan funds to women entrepreneurs of which 309 werenew enterprises (para 14). The project objective is considered to have been met, particularly, inview of conditions prevailing in Pakistan.

10. Based on successful outcome of the pilot project, GOP has requested the Bank for a followup project with a larger allocation for broader geographical coverage (Appendix A para 15 andAppendix B). The Bank is considering a follow up project for MSEs based on the lessons learnedunder the pilot project (para 25).

Borrower and Bank Performance

11. Performance of GOP and the Bank was satisfactory in identification, design, appraisal andimplementation of the project. Although there had been three Bank supported Small Scale Industriesprojects in Pakistan, it was the first effort to reach microenterprises. As a pilot project, it wasdecided to cater only to successful ongoing businesses and select intermediaries which already hadsome exposure to microenterprises. Similar eligibility criteria were applied to selection of NGOs forparticipation. The pilot was successful as evident from the benefits to MSE sector under the projectand of the intermediaries. Allowing new women entrepreneurs to be eligible under the project alsoproved successful and demonstrated viability of women entrepreneurs. Finally, the Bank could havesupervised the project more frequently during mid phase of the project when there was a slow down(para 7, 22).

iv

12. GOP's readiness to on-lend to private sector intermediaries directly for the first time madethe project possible. GOP procedures, nevertheless, caused a delay of about one year in the Loanbecoming effective after Board approval (para 23). Its requirement of a third party guarantee frompublic sector financial institutions for the PLCs could have been relaxed which would have allowedinduction of additional PLCs earlier in the project. Financial covenants were met generally on time.The study on performance evaluation of the PLCs required under the project was delayed by abouttwo years, and therefore, its recommendations could not be used for possible restructuring of theproject at mid-term. However, these recommendations would be beneficial for future activities inthe sector (para 25).

Lessons Learned

13. Main lessons learned from implementation of the Project are as follows:

- The project has demonstrated that financing of microenterprises is sustainable.

- MSE sector can be developed successfully by providing financing at market rates andwithout subsidies.

- MSE entrepreneurs performance concerning repayment of loans is satisfactory and betterthan recoveries from medium-large scale industry.

- Leasing is a viable option for medium-termn credit. Leasing companies, however, areconstrained by availability of term funds. This underlines the need for developing medium -long term fixed income securities market.

- NGOs have played an effective role in meeting funding needs of microenterprises. Tofurther improve they should develop suitable credit programs that meet the differing needs ofvarious MSE sectors.

- Women can play their due role in development of MSEs provided credit is made available.

- Private sector financial institutions have proved to be effective intermediaries indevelopment of the MSE sector.

- Prudent selection of financial intermediaries is key to project success.

- Clear identification of the target sector's characteristics, including information on businessesand their operations, employment and funding needs along with linkages with other sectorsshould be part of design of future proJects.

- Poverty reduction is vital for eradication of child labor and a practical concerted role can beplayed by NGOs. Microenterprise projects have a great potential for poverty alleviation,however, use of child labor at the expense of their education needs to be specificallydiscouraged and adequate precautionary measures taken in future.

v

IMPLEMENTATION COMPLETION REPORT

ISLAMIC REPUBLIC OF PAKISTAN

MIROENTERPRISE PROJECT(LOAN 3318-PAK)

PART I: PROJECT IMPLEMENTATION ASSESSMENT

A. Introduction

1. The project was the first assistance by the Bank to microenterprises in Pakistan. It wasdesigned to focus on critical constraints being faced by the sector and as a pilot project attempted tobuild experience by associating with institutions in Pakistan already having some direct businessrelations with the microenterprise sub-sector. As a start an emerging leasing company was selectedfor the upper stratum i.e. the group composed mostly of profitable and technologically moresophisticated businesses and NGOs for the lower stratum i.e. group comprising mainly thedisadvantaged having compelling social as well as financial needs. It also, complemented GOP'sreforms and liberalization efforts and recognized the fact that the earlier small scale industriesprojects had failed to reach the microenterprise sub-sector. Attempts to include commercial banksfor the upper stratum were abandoned during appraisal due to their lack of experience of catering tothis sub-sector which was judged inappropriate for a pilot project. Nevertheless, it was envisagedthat the project would induce some business interest in lending to this sub-sector in the bankingsystem by way of demonstrated replicability and hence promoting closer integration between formaland informal financial markets.

B. Statement I Evaluation Of Objectives

2. Project Objectives - Microenterprise project was designed to provide credit, through formalfinancial sector, to the micro and small scale entrepreneurs for their capital investment and to assistthis sector, in particular, women entrepreneurs to improve their living conditions by engaging inincome generating activities. The specific project objectives were to:

a) strengthen the capacity of participating institutions in delivering financial andtechnical/social services to microenterprises;

b) assist these institutions to deliver their services to a larger constituency ofmicroenterprises;

c) broaden the menu of financial instruments available for microenterprises in the upperstratum, by promoting the initiative to market leasing to sub-contractors of small-scalebusinesses;

d) catalyze NGOs' financial, technical and social support services for microenterprises in thelower stratum;

e) demonstrate the replicability of the NGOs and leasing initiatives to others, including thecommercial banks who could potentially see microenterprises in the middle to upperstratum as a promising market niche;

1

f)demonstrate the creditworthiness of microenterprises, including and particularly women, atmarket prices and practices; and

g) promote the development of businesses owned and operated by women.

3. Microenterprise project of US$ 26.0 million was on-lent by GOP, administered by BankersEquity Limited (BEL) as the apex institution, to the Participating Leasing Companies (PLCs) at avariable interest rate including foreign exchange risk cover fee and GOP's administrative charges.The PLCs financed, at prevailing market lease rates, the lease contracts of established andoperational micro and small enterprises (MSEs). To encourage women's participation indevelopment activities, start up firms were financed for eligible women entrepreneurs. The Bankloan was co-financed by Government of Netherlands (GON) for a total of NLG 4.8 million (US$ 2.8million equivalent) grant. The GON grant was allocated for: (i) NGOs as seed capital for theirrevolving credit operations (NLG 2.8 million or US$ 1.6 million equivalent): and (ii) institutionalcapacity building of NGOs through staff training and adapting and upgrading their credit proceduresand supervision information system (NLG 2.0 million or US$ 1.2 million equivalent).

4. Evaluation of Objectives - The Microenterprise Project, which was the first assistance to theinformal or unregulated sector by the Bank for Pakistan, was a pilot effort and aimed at addressingthe needs of the microenterprise sub-sector. The previous Bank lending to small scale industries(Table 2) had assisted the industrial and services units in the formal sector and did not address theneeds of the growing microenterprise sub-sector. A microenterprise, under the project, was definedas a manufacturing, commercial or service enterprise employing less than 10 workerss without anydefinite limiting asset size. This sub-sector was somewhat neglected and had very little or no accessto the formal financial sector. Preparation of Microenterprise project was in line with theGovernment of Pakistan's (GOP) socio-economic development policy and was an integral part of theBank's assistance strategy for the country. It coincided with the GOP's reforms in the financialsector at the time and the Bank's support through the Financial Sector Adjustment Loan (FSAL,prepared in 1989). The financial sector liberalization was also not sufficient to address the needs ofmicro sub-sector for investment funds. The project, therefore, proposed innovative lendingtechniques and instruments which facilitated access of the microenterprises to the short/mediumterm funds, through NGOs and leasing companies. The choice of leasing for opening up access ofMSEs to medium term financing for equipment from the formal financial sector was made as MSEswere considered having financially viable and high cash flow oriented operations but lacked formalfinancial records and adequate collateral requirements. Furthermore, in case of leasing ownershipof the asset remains with the PLC and as a result lower equity investment is required by the lessee.

5. Participation of NGOs and private leasing companies (emerging sector) as financialintermediaries in the project ensured access of microenterpreneurs in lower and upper stratum tofinancial, technical and social support in accordance with GOP's objective of promoting the privatesector participation in development activities and poverty alleviation initiatives in the country.Microenterprise project also promoted women's involvement in social and economic development byallowing them to borrow for start up firms not otherwise allowed under the project. Bankinvolvement was important and instrumental in: (i) providing funds for capital investment otherwiseunavailable through formal financial sector; (ii) ensuring sustainable development of newinstruments, approaches, and transfer of the best international practices/experiences inmicroenterprise lending; and (iii) stimulating other donors in supporting microentrprise sector.

2

C. Achievement of Objectives

6. The project objectives were achieved satisfactorily. The direct benefit of the project hasbeen poverty alleviation, sustained income generation, reduced under-employment and increasedproductive opportunities, particularly for women. Successful participation of leasing companiesprovided access to credit to the micro and small enterprise (MSE) sector.

7. Implementation of the Bank Loan Component - The loan component was implementedsatisfactorily and achieved its development objectives. The project made significant contribution topromoting leasing as an alternative to capital investment in the MSE sector, generating employment,and supporting income generating activities for large number of microentrepreneurs. Initially, theloan was on-lent to one private leasing company- Orix Leasing Pakistan (OLP) which was the onlyeligible institution at appraisal in 1990. Until March 1996, only US$ 9.2 million of the total loanamount was utilized since the effectiveness of the project in April 1992. While OLP performed wellin expanding the leasing facility to microenterprises, due to escalation of law and order problem in1995-1996, the loan utilization was not as projected at appraisal. In 1995 two more leasingcompanies, namely Pakistan Industrial Leasing Corporation (PILCORP) and Pakistan Industrial andCommercial Leasing (PICL) expressed interest to participate in the project based on demonstratedsuccess of lease financing to the MSE sector by OLP. Although they were appraised by the Bankand found eligible to participate in the project, PILCORP and PICL started utilizing the loan funds inJune and August 1996, respectively. The delay in their participation was mainly due to cumbersomeprocedures imposed on them by BEL for providing third party guarantee to GOP (para 10). As aresult of participation of these two leasing companies, disbursements increased substantially and byApril 1997, reached US$ 16.4 million, an increase of US$ 7.2 million (78%) over a period of 13months.

8. In May 1997, Network Leasing Corporation Limited (NLCL) was also appraised andselected to participate in the project. With four PLCs participating in the project and improvedpolitical and economic conditions, the utilization of the Loan component substantially improved. Inview of turnaround of project implementation the Bank, based on the request of BEL and PLCs,extended the original deadline for submission of lease finance applications to the Bank from June 30,1997 to March 31, 1998. The project closing date of June 30, 1998 remained unchanged based onthe fact that lease finance applications were for reimbursement of expenditures already incurred bythe PLCs, thus allowing sufficient time for disbursement by the Bank. The US$ 26 million Loan wasfully committed by March 31, 1998 and subsequently disbursed with cancellation of US$ 30,000 dueto exchange rate fluctuation.

9. The Bank Loan financed about 2,900 leases. Of these, about 44 % by number and 25% byamount were for capital formation of microenterprises and 56 % and 75% respectively for smallscale industrial units (Annex I). Although, more funds were disbursed to SSIs compared withmicroenterprises, project's outcome is satisfactory as three of the PLCs which were lending tomicroenterprise only on nominal basis earlier, established themselves as lenders to microenterprisesunder the project (para 11). The fourth PLC (NLCL), which was set up primarily for catering to theneeds of MSEs based on the demonstrated success of OLP under the project, financed two and a half

3

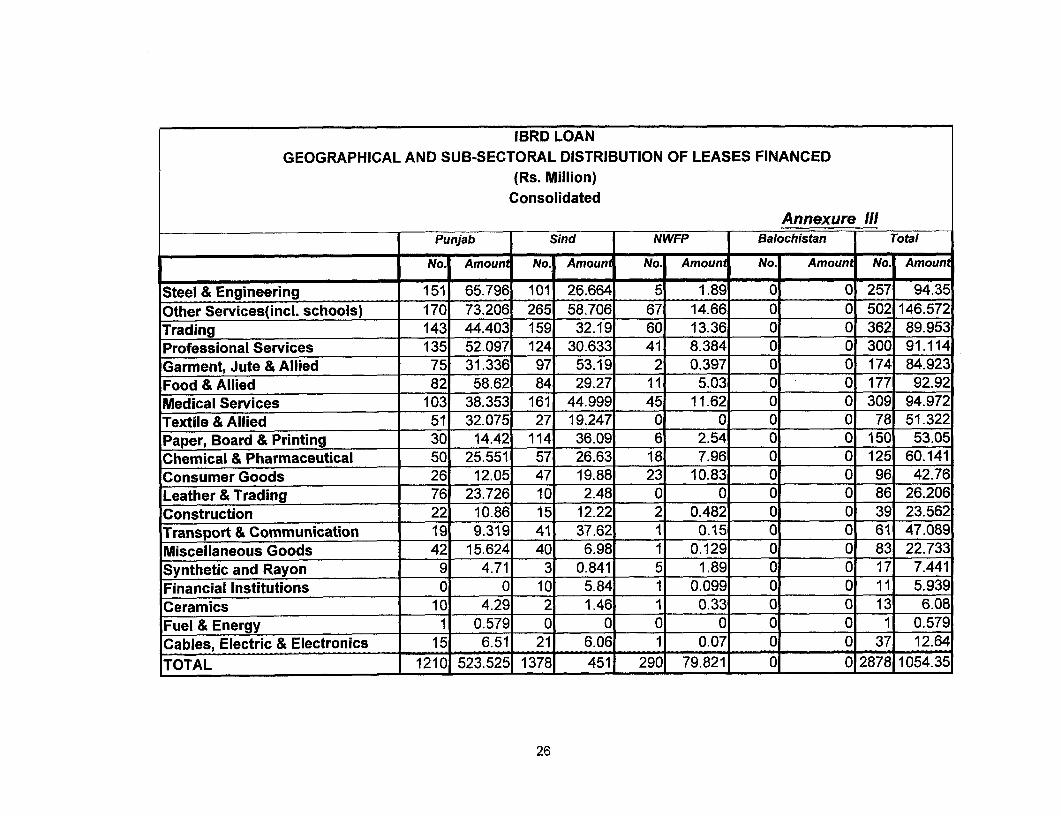

times more microenterprise leases compared with SSIs. Also, the Loan has been advanced to thePLCs for 10 years while lease maturity has been about three years, permitting roll over of thesefunds and increasing project impact more than three times. OLP, the first and the largest PLC in theproject, financed 73 percent of leases by number and 70 percent of those by amount. The averagelease comprised Rs 370,000, being about Rs. 180,000 in micro sub-sector and Rs. 440,000 in smallscale sub-sector. It is estimated that nearly 2 jobs were created per lease on average resulting ininvestment per job of about US$ 5,000 (Annex II). In case of NLCL which caters mainly to themicroenterprise sub-sector, investment per job was only about US$ 1,000. About 50% leases werefor sole proprietorships and 30% for private limited companies and of the total 45% were for plantand machinery, 31% for office equipment and 23% for commercial vehicles (Annex IV).Geographical distribution of leases financed included about 48% in the province of Sind, 42% inPunjab and the remainder in NWFP (Annex III). None were financed in Balochistan due to lack ofdemand and also, there being no branch office of any of the PLCs located in the province. PLC'sproactively provided financing to women entrepreneurs including new/startup businesses which wasearlier not their usual lending practice. Promotion of businesses owned and operated by women wasspecifically included in project design. About 7% of the total leases financed benefited womenentrepreneurs (Annex V). The project objective in this regard is considered to have been achieved asNLCL and PICL increased their lending to women MSEs by about three times, while, PILCORPonly started to lend them to a significant extent under the project (Annex XV). OLP, also, based ontheir experience under the project, doubled their lending to women enterpreneurs during the projectcycle. Lease finance facility to MSE entrepreneurs had an immense impact on businesses and livesof the sub-borrowers under the project and some real life examples reflecting contribution of theproject towards achievement of its objectives, are provided in Annex XIV.

10. BEL's performance as administrator of the project, was generally satisfactory. Although, afew tasks originally assigned to BEL, including monitoring of technical assistance component andsubmission of routine progress reports on project implementation were not performed. PLC'sapplications for refinance were routed to the Bank through BEL which carried out a check oneligibility. BEL maintained the Special Account, handled disbursements to the PLCs and collectedrepayments from PLCs for crediting to the GOP account and for record keeping established acomputerised data base. BEL also helped the Bank in monitoring continued eligibility forparticipation of the PLCs in the Project. Furthermore, BEL provided third party guarantees to GOPfor repayment of the Loan funds. Finally, according to GOP, BEL has not deposited in GOPaccount, the repayments it collected from PLCs.

11. The PLCs' Performance in implementation of the Loan component has been satisfactorythroughout the project. Their procurement and disbursement procedures were satisfactory. Loanrecovery rate for micro and small scale sub-leases, on average, was 95%, which is highly satisfactory(Annex VI) considering they were on lent to the PLCs by GOP under participation agreements witheach of the PLCs as well as the law and order situation in the country since 1995. It is significantthat almost 90% of the remaining 5% is, also, not lost by the leasing companies and is recoveredwith some delay. The assets being in the name of the PLC are recovered more easily, generally,without recourse to the courts and are also insured. Furthermore, PLCs, also, offer insurance whichin case of lessee's death not only ensure PLC's repayments but enable lessee's family to retain theasset. Orix Leasing Corporation, the first PLC, participating in the project started leasing in

4

September 1992 and took several measures to build its institutional capacity to meet the needs of theMSEs and the Bank's requirements under this project. These measures included (i) creating a specialcell to carry out research in informal sector through collaboration with the NGOs; (ii) creating a newmicroenterprise department in Karachi; (iii) translating lease documents and materials into Urdu,Pakistan's national language; (iv) developing a separate credit system for microenterprises and smallscale clients which usually lack accurate financial accounts for ensuring proper appraisal, monitoringand recoveries; and (v) improving marketing techniques to better serving this sector and expandingthe outreach. PLCs joining the project later also took similar measures. The technical advisoryservices to microenterprises were delivered through engaging consultants for field work foridentifying potentially promising enterprises and helping them to improve their marketing,accounting and management skills. PLC's own specialized staff also worked closely with the sub-borrowers and their increased lending to micro and small enterprises togetherwith satisfactoryrepayment performance confirms successful delivery of the extension services envisaged under theproject objectives. In the process PLC's also strengthened their capacity for lending to MSEs andtheir portfolio in micro and small scale sector considerably expanded during the projectimplementation and now accounts for about 20% of their total lease portfolio. Considering thatNLCL was established exclusively for leasing to micro and small enterprises followed by itsparticipation in the project significantly increased PLCs outreach in the MSE sector as envisagedunder the project objectives. PLC's overall MSE portfolio increased by an average of about fourtimes in number except OLP where it was about 50%, and by about 100% for all in amount duringproject implementation (Annex XV).

12. Pakistan Industrial Leasing Corporation (PILCORP) and Pakistan Industrial andCommercial Leasing (PICL) also performed satisfactorily and took measures similar to OLP forcatering to the MSE sector. PILCORP opened a branch in Peshawar and setup a representativeoffice in Quetta to study the market and estimate possible demand prior to starting operations there.PICL was the second largest user of funds and had the advantage of their commercial bank branchesin various parts of the country for their outreach. NLCL, joined towards the tail end of the project,but performed very well for the micro sub-sector as they had been setup with a charter to caterprimarily to microenterprises.

13. Implementation of Dutch Grant Component: NLG 2.8 million under the Dutch Grant sub-loan component was initially allocated to four NGOs as grant for their revolving fund creditoperation, to become financially self-sustaining. The participating NGOs (PNGOs) comprisingAgha Khan Rural Support Program (AKRSP), Orangi Pilot Project (OPP), Basic Urban Services forKatchi Abadies (BUSTI) and AlFlah Development Institute (ADI) were to make short term loans tomicro and small enterprises of the lower stratum at the prevailing market rates and bear the creditrisk. In 1994 ADI, after utilising a small amount, failed organizationally due to inadequate attentionby its board of directors and was disqualified from further participation for non compliance with theminimum participation criteria. In 1995, Balochistan Rural Support Program (BRSP) was appraisedand found eligible to participate in the project. However, the formalities for participation took abouta year and BRSP started its grant utilization in 1996. The reasons for delay included unfamiliarity ofBRSP with GOP's procedures for participation in projects and difficulties arising out of distantlocation of BRSP headquarters (Quetta). By end of 1995, the allocation for sub-loans were fullycommitted with over-commitment of NLG 0.2 while only 30 percent of TA component of NLG 2.0million was utilized. The 1996 review mission, after consulting with the PNGOs and the GON,

5

concluded that demand for sub-loan was much higher than for TA and recommended that unutilizedTA allocation be reallocated to the sub-loan component. Thus , the allocation for sub-loans toPNGOs was increased to NLG 4.25 million and the entire Grant was fully utilized (Annex XII).

14. The PNGOs utilized the sub-loan component for on-lending to about 7,000 micro-entrepreneurs for income generating activities of which about 1,500 were women - 309 being newstart-up projects. This represented about a quarter of total lending which is considered satisfactoryin meeting project objectives of promoting women entrepreneurs (para 9). Employment generatedunder the component is estimated at about 10,000. About 55% of the sub-loans were utilized fortrading and 16% for livestock (Annex IX). As against the SAR requirement of at least 60% forfinancing sub-projects below $700, the project achieved a much higher proportion of about 90% forsub-loans under Rs.25,000 (Annex XIII). The recoveries were 85-100, while most of the remainderis also being recovered with some delay, except BRSP which faced deterioration due to internalchanges after withdrawal of their main sponsor-GTZ of Germany. Its collection ratio dropped toonly about 42%. The Netherlands Government, while, commenting on the draft ICR, expressedconcern over BRSP's situation. BRSP, have now advised that poor recoveries are due to droughtand crop diseases and while their recovery ratio has improved to 47%, they are making concertedefforts to recover the remaining overdues and will even resort to legal action if necessary. Finally,satisfactory repayment performance of most of the sub-loans to lower stratum indicates achievementof the project objective of demonstrating credit worthiness of microenterprises at market prices andpractices (Annex X).

15. AKRSP had the major share utilizing about 38% of the Grant for about 4,800 sub-loans inthe northern areas (Annex VIII). These sub-loans amounting to NLG 1.8 million were channeled tothe rural community for purposes of agriculture, live stock and trading. AKRSP's credit programtraditionally was based on village/women's (v/wo) organizations allowing autonomy in financialmanagement. Under the terms v/wo members are required to contribute to the collective savingsaccording to their financial capacity. This pool of savings serves as collateral for obtaining credit forthe members and has brought about a change in culture in the area and financial independence forthe people. OPP utilized NLG 0.56 million for sub-loans primarily in Orangi, Karachi, however,their operations over the years also expanded to other provinces. OPP through its innovativeapproach considerably increased its outreach in a cost effective and efficient manner by associatingwith 41 NGOs / Community Development Organizations (CDOs) and 53 groups formed by itsagents, which are now replicating OPP's program. The catalyst role played by OPP, not only forincreasing its outreach in quantum but also in extending technical and other support services to thelower stratum of microenterprises by training other NGOs met project objectives highlysatisfactorily. BUSTI utilized NLG 1.5 million for sub-loans to sub-borrowers in both rural andurban Sind advancing loans to about 1,100 borrowers with a split of 80/20 between rural and urbancommunities, with 55% of the loans to female entrepreneurs. In this process BUSTI spread itselfsomewhat thin in capacity to efficiently monitor distant rural areas and there is need to buildadditional capacity for the expanded operations. BUSTI has additionally contributed to the societyby employing qualified and dedicated female staff which have provided effective assistance in thedevelopment of women entrepreneurs in the field through technical and marketing advice asenvisaged under the project objectives, and by providing training to the upcoming young universitystudents in this field. BRSP became a PNGO in late 1996 and was only able to utilize NLG 0.28million under the project. BRSP follows almost a similar program as AKRSP i.e. credit through self

6

help organizations comprising of village/women organizations and village specialist associations, amodel which is based on savings of the communities and tied to the credit program. BRSP,however, faced substantial problems and deterioration of its portfolio after withdrawal of GTZ in1997, which happened subsequent to Bank having disbursed the Dutch Grant. It is imperative forBRSP's survival and recovery of its outstanding loans that its management be strengthened andsupport is provided to fill the gap created by GTZ's withdrawal.

16. A total of NLG 0.55 million were utilized for TA, of which NLG 0.36 million was utilizedfor an assessment study of microenterprise sub-sector and for evaluation study of participatinginstitutions performance, NLG 0.04 million by AKRSP for apricots preservation research and NLG0.16 million by BUSTI for institutional development and MIS (Annex XII). The sector assessmentwas somewhat delayed and was completed in 1995, its outcome was disseminated to GOP forpurposes of guidance in sectoral polices concerning growth of the microenterprise sub-sector andmaking adjustments in policies and practices of the formal financial sector as well as in preparationof trade and industry policy reforms. The performance evaluation required to be conducted at mid-term for possible restructuring and incorporating the lessons learnt to improve project design wasdelayed by two years and was carried out about eight months before closing. Therefore, therecommendations could not be used to restructure the project as envisaged and it is expected thatthey would be utilized for future activities in this sector. BUSTI benefited greatly from consultancyassistance under the TA and introduced sub-project appraisal and account keeping techniquestransforming it from a welfare organization to an active lender to microenterprises for productivepurposes with satisfactory recovery performance. The consultant who helped BUSTI, was notsuccessful in introducing an MIS at BEL for monitoring PNGO's lending operations as providedunder the project due to coordination problems between BEL and the PNGOs and lack of funding forequipment.

17. PNGOs carried out extremely valuable work in their areas (both rural and urban) in terms ofproviding credit to the microenterpreneurs, promoting self reliance, bringing awareness andproviding the necessary linkages and their sub-borrowers benefited significantly under the project.The PNGOs also derived considerable benefits in improving and developing their institutionalstructure, operations, outreach and enhanced their capacity to deliver microcredit. For AKRSP, OPPand BRSP, which were already established, the project provided additionality, while for BUSTI,which was not involved in microenterprise lending earlier, increased its outreach in the micro sectorsignificantly. Some examples of project impact which were observed by Bank missions during fieldvisits to sub-borrowers are provided in Annex XIV. PNGOs have played an important role inreducing poverty in their respective communities which has also helped in reducing incidence ofchild labor. Families living below subsistence level resort to getting help from their children in theirefforts to earn a living. NGOs role needs to be enhanced at a broader level in eradicating child laborfrom the country. It is important for the NGOs as they have close relationship with communities inthe lower stratum where child labor still continues. Encouraging development of microenterprisesopened greater avenues for employment thus improving incomes and lesser dependence on children.

7

D. Major Factors Affecting the Project

18. The project was implemented satisfactorily without any major problem.An important feature of project design comprised clear identification of the target sector'scharacteristics, including information on businesses and their operations, employment and fundingneeds alongwith linkages with other sectors which was a key to achieving project objectives. Therewere, however some factors (para 7, 13 and 23) that delayed the utilization of the Bank's loancomponent and the institutional development component under the Dutch Grant and are analysed inthe following para.

19 (a). Factors Not Generally Under Implementing Agencies Control: As mentioned in para.7,OLP was the only leasing company participating in the project from the project effectiveness (April1992) until mid-1996. In addition, the law and order situation that deteriorated in the country inearly 1995, slowed down the business activities and therefore utilization of the loan funds.

(b) Factors Subject to ImplementingAgencies Control: The project was the Bank's firstoperation catering to microenterprises and as a pilot was based on selected existing leasinginstitutions and NGOs as financial intermediaries for channeling funds to the MSE sector.Administrative arrangements and building the capacity of these institutions to meet the MSEs'demand was more of a learning process for the Bank and the concerned institutions (PLCs, PNGOs,and BEL as Apex). Therefore, the procedures and formalities for appraising and finalizing theparticipation agreements of NGOs (BRSP) and leasing companies (PICL and PILCORP) that joinedthe project in 1996 took longer than expected (para 7, 13). Disqualification of ADI in 1994 due tonon-compliance with the participation criteria (para. 13) also affected the utilization of the Grantcomponent. In addition, the fact that second hand/used equipment were not allowed to be financedunder the project limited the use of the loan component to those entrepreneurs who could afford newmachinery and equipment. This was, also, the major concern of the PLCs, because micro and smallscale businesses generally preferred and at times could only afford second hand/reconditionedmachinery available at substantially lower cost.

E. Project Sustainability

20 Micro and Small Scale Financing: Development of the micro and small scale enterprises isan integral part of the GOP's private sector development strategy and its trade policy. Theexperience of the Micro project and previous SME projects in Pakistan shows that these sectors canplay vital role in enhancing exports, developing the economy through employment generation andimproving the income status of population at large. In a recent plan to boost exports, the GOP is tolaunch a comprehensive program for the SME sector by providing special facilities to them andenhancing the incentive system in order to improve and increase the production and exports fromthis sector. The government's commitment to further integrate these two sectors into the economy aswell as the growing interest in the leasing industry to build up their capacity to finance the mediumterm investment projects in the micro and small scale sector suggest that the impact of theMicroenterprise Project would be sustainable (para 9, 11).

8

21. Participating Institutions: The Microenterprise project had significant impact on facilitatingthe access of the MSEs to investment funds through introduction of new financing instruments inthe formal financial sector. The project was successful in improving the operations of the PLCs andPNGOs, strengthening their financing activities/credit operations, and adding focus on the emergingMSE sector. These participating institutions took several important measures to improve theiroperations and portfolio in this sector (para 11). These benefits are likely to be sustained in the longterm as the PLCs have experienced that financing the MSE sector is in fact a profitable businessactivity and could be their market niche. The financial performance (profitability and loancollection performance) of the PLCs and the PNGOs and their increased lending activities in thissector during the life of the project were instrumental to the successful implementation of theproject. The PLCs substantially broadened their geographical coverage and outreach during the lifeof the project and new leasing institutions, such as Network Leasing Corporation, were establishedin past few years which primarily cater to the micro and small enterprise sector.

F. Bank's Performance

22 Bank's performance has been satisfactory. Although the Bank had three Small ScaleIndustries projects in Pakistan, it was the first effort to reach microenterprises. As a pilot project, itwas decided at appraisal to cater only to successful ongoing businesses and select intermediarieswhich already had some, even though limited exposure to microenterprises. The participatinginstitutions were also required to have, as a corporate policy, lending to microenterprises andprovided for expansion into this market in their business plans. Therefore, the project started withparticipation of only one leasing company. Additional leasing companies joined during projectimplementation having met the conditions of participation. Similar eligibility criteria were appliedto selection of NGOs for participation. This strategy paid off as evident from the benefits to MSEsector under the project and of the intermediaries which operated successfully with high recoveryratios. Also, allowing new women entrepreneurs to be eligible under the project has been successfulin demonstrating viability of their business efforts. Finally, the Bank could have supervised theproject more frequently during mid phase of the project when there was a slow down and, also, couldhave arranged for speedier appraisal of potential leasing companies for participation.

G. Borrower's Performance

23. Borrower's performance has also been satisfactory. Its readiness to on-lend to private sectorintermediaries directly for the first time made the project possible. The formalities, nevertheless,caused a delay of about one year in the Loan becoming effective. GOP, therefore, needs tostreamline its procedures to avoid delays in project effectiveness and implementation. Itsrequirement of third party guarantee from a public sector financial institution for the PLCs wasunnecessary. Financial covenants were met, generally on time. GOP, also, carried out reforms ofthe financial system covering the legal, tax ,accounting and regulatory environment includingspecific actions to help the leasing sector by allowing them access to Banking Tribunals for loanrecovery and avoidance of double taxation concerning sales tax. Evaluation study on performanceof the PLCs was delayed by about two years, and, therefore, its recommendations to restructure theproject for improving project design at mid-term as envisaged could not be achieved. BEL's

9

performance as an administrator and Apex under the project on behalf of the Government wasgenerally satisfactory although a few tasks assigned to BEL were not performed (para 10).

H. Assessment of Outcome

24. The project is rated high with regard to outcome. Project objectives were achieved eventhough it was the bank's first intervention in the microenterprise sector on pilot basis. Thebeneficiaries and the intermediaries performed well in contrast to the experience under the SSIprojects. MSE has been demonstrated to be a viable sector for financing by formal sector financialinstitutions. This includes women sponsors of MSEs and, particularly, microenterprises for whichno specific targets were laid under the project. However, in view of socioeconomic conditions in thecountry, over 20% of total lending under the Dutch Grant going to women entrepreneurs (Annex XI)is viewed as satisfactory for meeting project objectives. This, together with arrangement of thetechnical and other advisory services extended by the PNGOs and the PLCs to their sub- borrowersis considered a satisfactory outcome of the project with regard to strengthening their capacity andoutreach (para 9, 14, 15). Thus, avenues for financing at a lower cost as compared with the informalsources of finance have opened up. There are now four leasing companies catering to this sector formeeting their medium term needs for capital, while, at the start of the project there was only onewhich had just started to entertain microenterprises. The PLCs having built up their capacity forlending to the MSEs and expanded their outreach (para 11) under the project intend to continue tocater to this sector even though the volumes are likely to be reduced due to constraints in termfinance available to the leasing companies. In view of the achievements the project performance isconsidered satisfactory.

I. Follow up Operations

25. Based on success of the pilot microenterprise project, GOP, PLCs, PNGOs, MSEbeneficiaries and, also, some other financial institutions have requested for a follow up project.MSE sector is important for socio-economic reasons and accounts for about 38% of the employmentin the country and 13% of manufacturing value added. It has extensive linkages with larger industrythrough sub-contracting. The scope for growth is therefore substantial. The pilot projectdemonstrated that such assistance to MSEs does not require subsidies. The sector growth, however,is constrained due to limited access to credit for capital investment, including permanent workingcapital. The reasons are collateral requirements and small size of their operations. Leasingcompanies are the only financial institutions providing significant medium term lending to this setorfor fixed investment. Furthermore, under the project the PLCs have developed expertise forproviding financing to MSEs, however, the resource constraints remain. While, intermediaries andthe beneficiaries performed well under the pilot project, any follow up project would need to addressthe resource constraints faced by the leasing companies catering to this sector on a longer term basis.Based on successful outcome of the pilot project, GOP has requested the Bank for a follow upproject with a larger allocation for broader geographical coverage (Appendix A para 15 andAppendix B). The Bank is considering a follow up project for MSEs which will be based on thelessons learned under the pilot project. The project will address the need of medium/ long termfunds for the MSEs through expansion of private financial intermediaries for development of the

10

sector. With regard to NGOs, the Bank's association under the pilot project has helped inunderstanding their methodology for sub-project appraisal, loan sanctioning, monitoring andsupervision. Based on satisfactory experience under the project, the Bank has decided to continuethis association on a larger scale by participating in the upcoming Poverty Alleviation Fund.

J. Main Lessons Learned

26. The project has demonstrated that financing of microenterprises is sustainable as theyexpanded their operations and increased their incomes through leasing of equipment under theproject. This is, also, evident from their timely repayment of the installments to the leasingcompanies and the fact that about 300 lessees were repeat. This contrasts with repaymentperformance of large industries where recoveries are often a problem. Similar was the performnanceof the PNGO's sub-borrowers. They expanded their businesses, improved their turnover and repaidtheir loans to the PNGOs and in the process generated employment. This as a result improved theirquality of life which evidently they would make all efforts to sustain.

27. The PLCs, also, found that lending to the MSEs was viable. They have made suitablechanges in their procedures for making it easier to deal with MSEs whose financial statementsusually fall short of the standard requirements for industries. Additionally, PLCs utilised consultantservices to provide technical and management advice to microenterpreneurs. In fact, their portfolionow comprises of microenterprises to the extent of 20% and they have indicated that financing tothis sub-sector will continue indicating sustainability of funding for the MSEs. This, also,represents significant increase in their outreach in the MSE sector under the project in accordancewith the project objectives, which with the exception of NLCL, was only modest when they joinedas PLCs. The PLCs intention to continue financing MSEs is, however, likely to be on a smallerscale as they are constrained by availability of medium term funds from the market. Therefore, thereis a need to develop a market for medium term funds which would support accelerated developmentof the MSE sub-sector and may be addressed through a follow up project.

28. NGOs play a useful role in meeting funding requirements of microenterprises. Theiroperations are sustainable as their recoveries were about 90%. The Government and the banks,however, need to encourage their intermediary role for MSEs. It has, also, been demonstrated thatNGOs focusing on welfare activities could play a significant role in alleviating poverty bydeveloping their credit operations. As PNGOs, they increased their outreach to microenterprise sub-sector substantially, compared with limited lending before their participation and thus meeting theproject objectives.

29. MSEs sponsored by women operated successfully under the project. Both PLCs and PNGOshad satisfactory recoveries even from their start-up projects. Women entrepreneurs under the projectproved to be a credible risk which can play a significant development role as the PLCs and PNGOssuccess in promoting women microenterprises would encourage other lending institutions todisregard any reservation they may have had in dealing with them.

11

30. Careful selection of financial intermediaries is key to project success. Private sectorfinancial institutions can be relied upon to perform intermediaries role satisfactorily as a betteralternative to public sector institutions.

31. Clear identification of the target sector's characteristics, including information on businessesand their operations, employment and funding needs alongwith linkages with other sectors at theappraisal stage is of great importance for achieving project objectives.

32. Child labor should be discouraged and phased out, however, the underlying causes need tobe addressed as families living below subsistence level resort to getting help from their children intheir efforts to earn a living. Microenterprise projects have a great potential for poverty alleviation,however, use of child labour at the expense of their education needs to be specifically discouragedand adequate precautionary measures taken in future. NGOs, based on their closer relationship withcommunities can play an effective role in poverty reduction and eradication of child labor.

12

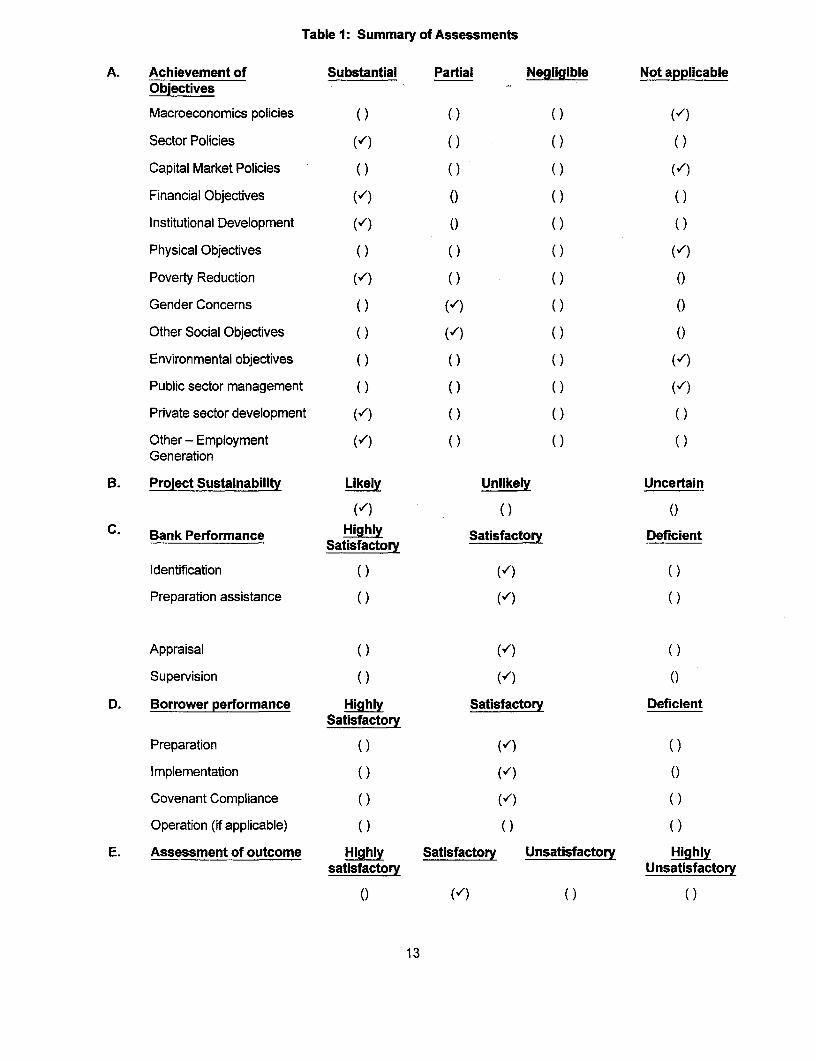

Table 1: Summary of Assessments

A. Achievement of Substantial Partial Negligible Not applicableObjectives

Macroeconomics policies () () () (1)

Sector Policies (/) () () ()

Capital Market Policies () () () (X)

Financial Objectives (v) 0 () ()

Institutional Development (v) 0 () ()

Physical Objectives () () ()

Poverty Reduction (X) () () (

Gender Concerns () (/) () 0

Other Social Objectives () (v) () 0

Environmental objectives () () () (/)

Public sector management () () () (1)

Private sector development (X) () () ()

Other - Employment (/) () () ()Generation

B. Project Sustainability Likely Unlikely Uncertain

(v") () ()

Bank Performance Satisfactory Satisfactory Deficient

Identification () (1) ()

Preparation assistance () (v) ()

Appraisal () (/) ()

Supervision () (/) 0

D. Borrower performance Highly Satisfactory DeficientSatisfactory

Preparation () (v) ( )

Implementation () (1) 0

Covenant Compliance () (I) ( )

Operation (if applicable) () () ()

E. Assessment of outcome Highly Satisfactory Unsatisfactory Highlysatisfactory Unsatisfactory

0) (1) ( ) ( )

13

Table 2: Related Bank Loans/Credits

Loan/credit title Purpose Year of StatusApproval

Preceding Operations

1. First Industrial To help GOP improve the credit delivery system 2/84 ClosedInvestment Credit and focus on the institutional restructuring of on(I IC-I) Loan 2830/ PICIC and IDBP. 12/31/90Credit 1439-Pak)

2. Second Industrial To assist GOP develop the capital market, 1/86 ClosedInvestment Credit improve credit delivery for industrial finance and on(IIC-II) Loan 2648/ continue institution building for PFIs. 12/31/92Credit 1646-PAK) . l

3. Second Small To promote investments in promising SSI sub- 6/84 ClosedScale Industry sectors and improve productivity of existing SSI onProject (SSI-Il) units. 6/30/92Credit 1499-Pak

4. Third Small To build on the first two SSI projects and 6/87 ClosedIndustries Project. continue supporting the objectives of increasing onLoan 2839-PAK the contribution of SSls to employment

generation, production and exports, while, 12/31/95providing funds for technology and productivityupgradation of SSls.

5. Third Industrial To assist in meeting the objectives of increasing 1/89 ClosedInvestment Project the role of private sector and accelerating the on(IIC-III) Loan growth of capital markets, through institution 6/30/95

building and policy changes

6. Financial Sector To assist the GOP in financial sector reforms: 3/89 ClosedAdjustment Loan gearing credit allocation to market signals, on(FSAL) Loan 3029- improving health and efficiency of banking 6/30/92Pak system, and creating more efficient Government

debt system.

Following Operations To provide term finance for all economic 11/94 Closing1. Financial Sector activities; to continue and expand the reform date is

1. Financial Sector process started under FSAL; and to support 12/31/99Deepening and GOP's strategy for macroeconomic and financialIntermediation setrefmlProject (FSDIP) sector reform.Loan 3808-PAK

2. Banking Sector To assist GOP in banking sector reforms: Legal 12/98 ClosedAdjustment Loan reforms for loan recovery, SBP's autonomy and 3/ 31/98

improving banking supervision, market reformsand privatisation of financial institutions.

14

Table 3: Project Timetable

Steps in project cycle Date planned Date actual/latest estimate

Identification 1988 July 1988

Preparation March 1989 October 1989

Appraisal June 1990 June 1990

Negotiations Nov. 1990 February 4, 1991

Letter of development policy (if applicable) NA NA

Board presentation January 1991 April 23, 1991

Signing June 1991 June 28, 1991

Effectiveness September 1991 April 30, 1992

First tranche release (if applicable) NA NA

Midterm review (if applicable) NA NA

Second (and third) tranche release (if NA NAapplicable)

Project completion June 30, 1997 March 31, 1998

Loan/Credit closing June 30. 1998 June 30, 1998

15

Table 4: Loan/Grant Disbursements: Cumulative Estimated and Actual

US$ Million

FY93 FY94 FY95 FY96 FY97 FY98

Appraisal 0.8 6.2 16.4 22.1 24.9 26.0estimate I/

Actual " 2.0 6.0 7.9 12.6 17.8 25.97

Actual as % of 250 97 48 57 71 99.88estimate

Grant-Actual 2' 0.4 1.0 1.7 3.1 4.7 4.8

NLG Million

" Loan component.21 Netherlands Grant component. Disbursements were not estimated at Appraisal.Date of final disbursement: Loan: October 31, 1998

Grant: May 5,1998

16

Table 5: Key Indicators for Project Implementation

I. Key implementationindicators inSAR/President's Report Estimated Actual

1. Development of PLCs Utilization of a total of US$ 100% of the Loancapacity for lending to 26.0 million for increasing disbursed (see table 4);.microenterprises investment in

microenterprise sector

2. PLCs satisfactory financial Average collectionperformance including Collection ratio to remain achieved 94%compliance with the satisfactory (above 90%)eligibility criteria under theproject.

3. Demonstrate credit Profitable utilisation of the . Most beneficiaries utilisedworthiness of credit and expansion of the credit well, increasedmicroenterpreneurs their businesses. their incomes and

expanded theirbusinesses. Theirrepayment of loans wastimely

4. Demonstrate replicability of More FIs starting to lend to Other leasing companieslending to microenterprises microenterprises started lending toto others microenterprises and the

PLCs increased from oneat start to four

II. Modified indicators NA NA

Ill. Other indicators (if NA NAapplicable) I

17

Table 6: Key Indicators for Project Operation

Key operating indicators in Estimated ActualSAR/President's Report l

1. NGOs performance on Managing revolving Three of the NGOs have beencapacity building funds managing well, while, one NGO

due to set back explained in thetext, is now taking steps toimprove its operations.

Improving NGO Lending operations improved,lending operations particularly, of the NGO which

received major technicalassistance

Advanced NGOs to One advanced PNGO assisted nonassist other PNGOs participating NGOs nationwide to

improve their operations. Suchassistance could not, however, bearranged for the PNGOs

II. Modified indicators (if NA NAapplicable) l

Ill. Modified indicators for NA NAfuture operation (ifapplicable).

18

Table 7: Studies Included in Project

Study Purpose Status Impact1. Small and Update and analyze changes in The study was carried out Findings of the study will be

Microenterprises the sector policy environment satisfactorily discussed with GOP duringSector Assessment and microenterprises preparation of follow up project in anStudy performance. Based on effort to improve microenterprise

findings of the study, GOP and sector policy environment.the Bank to take actions asappropriate.

2. Performance Evaluate performance of the The study was delayed and Due to the delay, its conclusionsEvaluation Study PCIs and project completed about a year became available too late in the

accomplishments in the light of before project closing, project cycle. The recommendations,project objectives two years therefore, could not be used forafter project effectiveness. amending the project mid term asAdjust project design based on envisaged at appraisal. However,the recommendations of the these are now being used forstudy preparing follow up project.

19

Table 8A: Project Costs

Appraisal estimate (US$ M) Actualllatest estimate (US$ M)

Item Local Foreign Local ForeignCosts Costs Total Costs Costs Total

1. Lease Investment 7.8 26.0 33.8 3.5 26.0 29.52. Sub-loans (Dutch 1.7 1.7 - 2.47 2.47Grant)

3. Technical Assistance - 1.1 1.1 - 0.33 0.33

TOTAL 7.8 28.8 36.6 3.5 28.8 32.3

Note: Actual Rupee costs converted to US$ based on average exchange rate during the utilizationperiod

Table 8B: Project Financing

._____________________ Appraisal estimate (US$ M) Actual/latest estimate (US$ M)

Source Local Foreign Local ForeignCosts Costs Total Costs Costs Total

IBRD Loan 0.0 26.0 26.0 26.0 26.0Netherlands Govt. 2.8 2.8 - 2.8 2.8

Private Sector 7.8 - 7.8 3.5 - 3.5

TOTAL 7.8 28.8 36.6 3.5 28.8 32.3

20

Table 9. Economic Costs and Benefits

Expost data regarding FRR and ERR are not available for the sub-projects

Table 10: Status of Main Legal Covenants

Agree Section Covenant Presen Original Revised Description of covenant Commentment type t fulfillment fulfillment s

status date date

Loan 4.01(a) Accounting C Througho PLCs, and BEL to maintainut the procedures and recordsproject life adequate to monitor the

operations and expendituresof the project

Loan 4.01(b) Accounting C 6 months PLCs to have the records of ThereAudit after each financial statements and BEL were

FY for special account in someaccordance with sound minoraccounting practice applied delaysby independent auditors;

Loan 4.02 Financial C Through PLCs Debt/ Equity ratio not tothe project exceed 10 to 1life

Loan 4.03 Financial C AnnuallyPLCs Debt Service Coveragenot to fall below 1.25

C = Complied with CD = Complied with after delay CP = Complied with partially

21

Table 11: Compliance with Operational Manual Statements

There was no incidence of non compliance with Operational Manual Statements

Table 12: Bank Resources: Staff Inputs

Stage of Project Cycle Actual staff Weeks1. Through appraisal 1422. Appraisal - Board 453. Supervision 1274. ICR 11

Total 325

22

Table 13: Bank Resources: Missions "'

Stages of Month/ No. of Days Specialized Types ofProject Cycle Year Persons in staff skills Performance Problems

Field represented l

Implementation DevelopmentStatus Impact

Identification and 10/89 10 30 Financial Project briefpreparation Economist prepared

Informalsector/NGOspecialist l

Appraisal 4/91 4 20 Financial, Project Appraised HBL wasthrough Board Economist, appraised as aapproval Informal participating

sector /NGO bank.specialist However, it

withdrew justbeforeconclusion ofprojectAppraisal

Board approval 4/92 2 5 Project declaredthrough effectiveeffectiveness

Supervision 1/92 4 8 The entire loan of The01/93 2 7 US$ 26 million development

utilised objectives met8/94 2 8

02/95 4 20

6/96 2 17

5/97 3 22

12/97 2 12

Completion 5/98 4 17 Satisfactory Satisfactory

1/ The Microenterprise missions were, during the first three years, combined with those of other Bank'sintermediation operations. No record is available as how the time/number of staff was split between the projects.Therefore, time for supervision missions spent on Microenterprise project has been estimated.

23

IBRD LoanLease Disbursement

Annex - IIBRD Refinance No. Of Leases Amount - Rs. Million Amount in US$

Micro % of Small % of Sub- % of Micro % of Small % of Sub- % of millionsub total Scale sub total total Total sub total Scale sub total total Total

Orix Leasing Pakistan Ltd. 859 40.77 1248 59.23 2107 73.2 147.52 22.82 499.00 77.18 646.52 70.0 18.19

(OLP)Pakistan Ind. Leasing 58 29.15 141 70.85 199 6.9 21.878 18.28 97.78 81.72 119.66 11.0 2.86

(PILCORP)

Pak. Ind.& Comm. Leasing 105 49.07 109 50.93 214 7.4 45.79 33.69 90.11 66.31 135.90 13.0 3.37

(PICL)Network Leasing 253 70.67 105 29.33 358 12.5 32.40 46.29 37.60 53.71 70.00 6.0 1.55

(NLCL) I_I

TOTAL 1275 44.30 1603 55.70 2878 100.00 247.59 25.4 724.5 74.53 972.08 100.00 25.97

24

IBRD LOANLEASE CHARACTERSTICS

Annex - II

OLP PILCORP PICL NLCL TOTALParticulars Numbers Rupees Numbers Rupees Numbers Rupees Numbers Rupees Numbers Rupees

(Million) (Million) (Million) (Million) (Million)

Lease Financed by IBRD 2107 646.52 199 119.656 214 135.900 358 70.000 2878 972.076

Total Amount Advanced by 2107 713.55 132.916 138.030 72.000 1056.496

PLCs .. .

Total Investment (including 2107 713.55 145.153 151.150 77.800 1087.653

down payment)Average Size of Lease 2107 0.339 0.668 0.700, 0.201 2107 0.477

Average Size of refinanace 2107 0.307 0.601 0.635 0.196 2107 0.435

No. of Jobs created 3000 271 275 1902 5450

Average No. of jobs per lease 1.362 1.29 5.313 1.9

Investment per_job 0.24 0.536 0.550 0.041 _ 0.2

Leases in Arrears 215 12.79 12 2.32 17 2.680 3 0.030 247 17.820

Leases under litigation 39 12.18 1 1.270 Nil Nil 40 13.45

Leases repossessed 10__ 3.60 1 0.15_ 1 0.240 Nil Nil 12 3.990

Leases re-scheduled 2 1.80 Nil NilL Nil Nil 2 1.80

Leases for new projects - 93 31.80 Nil Nil 5 3.300 16 3.110 114 38.210

womenLeases for existing projects - 13 6.469 16 16.870 61 12.040 90 35.379

women _

Note: Jobs created under OLP leases are ICR mission's best estimates

25

IBRD LOAN

GEOGRAPHICAL AND SUB-SECTORAL DISTRIBUTION OF LEASES FINANCED

(Rs. Million)Consolidated

Annexure IIIPunjab Sind NWFP Balochistan Total

No. Amoun No. Amount No. Amoun No. Amount No. Amount

Steel & Engineering 151 65.796 101 26.664 5 1.89 0 0 257 94.35

Other Services(incl. schools) 170 73.206 265 58.706 67 14.66 0 0 502 146.572

Trading 143 44.403 159 32.19 60 13.36 0 0 362 89.953

Professional Services 135 52.097 124 30.633 41 8.384 0 0 300 91.114

Garment, Jute & Allied 75 31.336 97 53.19 2 0.397 0 0 174 84.923

Food & Allied 82 58.62 84 29.27 11 5.03 0 0 177 92.92

Medical Services 103 38.353 161 44.999 45 11.62 0 0 309 94.972

Textile & Allied 51 32.075 27 19.247 0 0 0 0 78 51.322

Paper, Board & Printing 30 14.42 114 36.09 6 2.54 0 0 150 53.05

Chemical & Pharmaceutical 50 25.551 57 26.63 18 7.96 0 0 125 60.141

Consumer Goods 26 12.05 47 19.88 23 10.83 0 0 96 42.76

Leather & Trading 76 23.726 10 2.48 0 0 0 0 86 26.206

Construction 22 10.86 15 12.22 2 0.482 0 0 39 23.562

Transport & Communication 19 9.319 41 37.62 1 0.15 0 0 61 47.089

Miscellaneous Goods 42 15.624 40 6.98 1 0.129 0 0 83 22.733

Synthetic and Rayon 9 4.71 3 0.841 5 1.89 0 0 17 7.441

Financial Institutions 0 0 10 5.84 1 0.099 0 0 11 5.939

Ceramics 10 4.29 2 1.46 1 0.33 0 0 13 6.08

Fuel & Energy 1 0.579 0 0 0 0 0 0 1 0.579

Cables, Electric & Electronics 15 6.51 21 6.06 1 .007 0 0 37 12.64

TOTAL 1210 523.525 1378 451 290 79.821 0 0 2878 1054.35

26

IBRD LOANTYPE OF ASSETS LEASED

Annexure IVORIX PILCORP PICL NLCL Consolidated

Category No. of Amount in No. of Amount in No. of Amount in No. of Amount in No. of Amount in

Leases Rs. million Leases Rs. Million Leases Rs. million Leases Rs. million Leases Rs. million

Machinery & 861 368.67 63 61.667 62 65.01 302 58.09 1288 553.437

PlantCommercial 501 198.68 77 33.72 53 42.84 35 10.28 666 285.52

VehicleOffice 745 146.2 59 24.268 90 32.6 11 1.06 905 204.128

EquipmentOthers 9 10.7 10 0.57 19 11.27

TOTAL 2107 713.55 199 119.655 205 151.15 358 70 2869 1054.355

27

IBRD LOANLEASE REFINANCE TO WOMEN SPONSORS

Annexure VIBRD Refinance No. Of Leases Amount Rs million

Micro Small Sub-total Micro Small Sub-total