world economy year 2100

TRANSCRIPT

The US-Australia Alliance in the Twenty First Century

Emerging Asia stream

The world economy in 2100

Five alternative visions of the future and the development of the Alliance

Huw McKay

Westpac Bank1

Abstract

There is a considerable degree of uncertainty – and thus disagreement – about the future course of the world economy. This paper seeks to offer some empirical guidance for the debate by presenting a suite of high level long run economic growth scenarios for the major actors, with an emphasis on developments in emerging Asia. These projections, which are based on a variety of assumptions on the rate and degree of ‘convergence’, aim to cover most of the major stylised positions on Asia’s economic future. The aim is to provide a catalogue of five scenarios from which non-economists can select ‘economic anchor assumptions’ for their deliberations in other fields. Having set out these alternative visions of the future of the global economy, they will then be discussed in the context of the prospective development of the Australia-US Alliance.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!!!1!The!views!expressed!in!this!paper!are!the!author’s!personal!opinions!and!should!not!be!ascribed!to!the!companies!of!the!Westpac!Group.!

There is a considerable degree of uncertainty – and thus major disagreement – about the future course of the world economy. Over the sort of time horizons relevant to the choice and assessment of alliance partnerships – when a decade or two can appear trivial - even small disagreements on the future trajectory of economic growth become substantial disagreements on the future relative scale of nations. Indeed, when one’s view extends over a century, alternate expectations of relative economic growth can imply visions of the future that are so far apart that debate on the non-economic aspects of security questions are almost pointless in their presence.

This paper seeks to offer some empirical guidance for the debate by presenting a suite of high level, long run, global economic growth scenarios with an emphasis on developments in emerging Asia. These projections, which are based on a set of assumptions on the rate and degree of ‘convergence’, aim to cover most of the major stylised positions on Asia’s economic future. The aim is to provide a catalogue of five scenarios from which non-economists can select ‘economic anchor assumptions’ for their deliberations in other fields. Having set out these alternative potential futures for the global economy, the implications of the results will be discussed in the context of the prospective development of the Australia-US Alliance.

The paper will proceed as follows. The initial task is to describe the jumping off point for the scenarios, which is the International Monetary Fund’s (IMF) baseline forecast for the world economy out to 2017, as outlined in its semi-annual World Economic Outlook of April 2012. The second is to outline and discuss the five long run scenarios in narrative form. The third is to present the resulting profiles for world growth, the distribution of output and relative living standards at various points between the present and 2100. The fourth is to draw out implications of these scenarios for the development of the US-Australia Alliance over the course of the twenty-first century.

The most important points arising from the scenario work are arguably

1. China will be the world’s largest economy for most of the time between its IMF forecast takeover of the USA in 2016 and mid century in every scenario, even the most pessimistic. However, it

finishes the century at number one just once in the five scenarios, reaching 2100 in fourth place twice and second place twice.

2. India is the largest economy in the world in 2100 in three of the five scenarios and is a close second in another two. In four out of five scenarios India spends at least some time as the world’s largest economy.

3. The scenario that produces a world economic structure most consistent with a balance of power scenario (between the USA, Developed Europe, China and India) is one where emerging Asian economies collectively stall around the middle income level. This is also the scenario where the USA rallies back to number one by century’s end after falling behind in its middle decades.

4. Developed Europe finishes the century as the world’s third or fourth largest economy in each scenario, indicating that it will remain economically relevant even in the face of the Asian ascent.

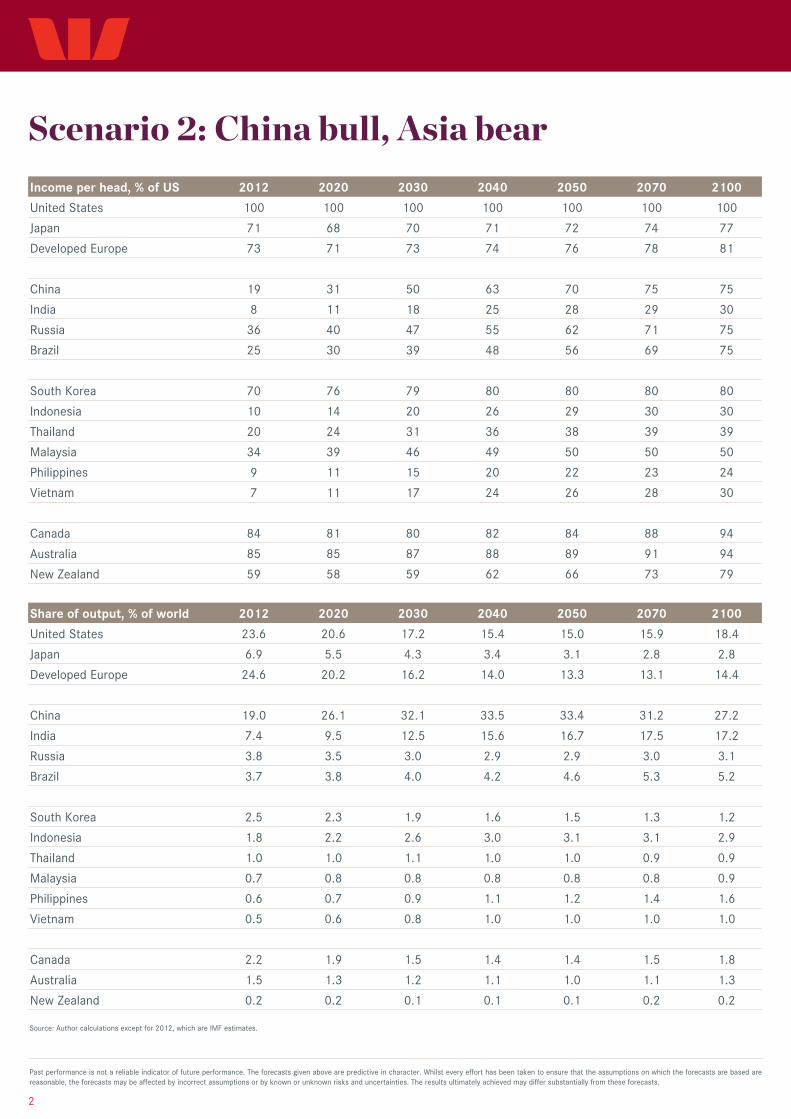

5. While the Japanese will remain a wealthy people, the economy’s size will be surpassed in all scenarios by Indonesia, in most scenarios by Brazil and Russia, and on a single occasion each by Canada and the Philippines.

6. No economy outside the top four will comprise more than 6.1% of world output (a relative position equivalent to China circa 1996) in any scenario. What is highly notable outside the top four is that Indonesia finishes the century as number five in every scenario but one. That implies very strongly that the widely used BRIC grouping of countries is not a particularly useful one for long run analysis. These scenarios highlight that not only are China and India in a very different league to Brazil and Russia, but also that Indonesia will be a bigger long run economic factor than either of the latter two powers. That is of course a particularly relevant point for any considered discussion of the Australia-US Alliance.

7. The scenarios draw out the stark differences in the long run demographic profiles of the major economies (as projected by the United Nations). Societies that are already old (Japan, South Korea, Developed Europe) with contracting working age populations will fall away appreciably in relative economic scale in the first half of this century. Younger societies (India, Indonesia, the Philippines) with growing working age populations in the second half of the century forge ahead. Those in the middle – including the Alliance

partners – show some resilience in defending global market share. China’s unique combination of modest income levels and an ageing population makes its share of global activity highly vulnerable to the future maturation of its catch-up growth phase.

8. Weak growth in the advanced countries, particular for the frontier defining US, would be very damaging for absolute global living standards in the long run. Weak growth in the emerging world would keep the West “in the game” from a scale perspective throughout the century, but the trade off is a major loss of global prosperity.

Where we are: the distribution of global economic activity in the second decade of the twenty first century.2

The world economy is still suffering from the legacies of the unsustainable debt accumulation that took place in advanced countries in the decade leading up to the Great Recession of 2008/09. This recession was precipitated by a resounding housing market crash and an intense financial crisis in the United States. It was propagated broadly through financial and real economy channels. In the time since, outside of the immediate rebound phase where large fiscal and monetary stimulus policies were able to pull confidence out of its spectacular downdraft, the world economy has been kept off balance by rolling financial and sovereign debt crises in Europe. Against this backdrop emerging markets, including those in Asia, have seen their growth rates lowered. The first challenge for these countries in the recovery phase was to look inwards for a higher proportion of activity. The second was to wean themselves off the stimulus policies enacted in self defence in 2008/09. In the face of these challenges, the economic performance of the major emerging economies has been respectable in

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!!!2!From!here!forward,!unless!specified!otherwise!the!term!“world!economy”!is!defined!as!the!combined!activity!of!a!subset!of!major!Asian!economies,!plus!the!USA,!Australia,!Canada,!New!Zealand,!Developed!Europe,!Russia!and!Brazil.!All!shares!reported!in!the!text!are!to!be!understood!as!a!proportion!of!this!subset,!not!of!the!full!sample!of!countries!in!the!IMF!database.!This!subset!represented!approximately!80%!of!total!activity!in!2012.!While!it!is!tempting!to!widen!this!subset!to!include!more!economies,!with!Singapore,!Pakistan,!Myanmar,!Bangladesh,!Mongolia,!Afghanistan,!Sri!Lanka!and!the!DPRK!among!those!considered!but!ultimately!excluded!to!keep!the!discussion!manageable.!

absolute terms, and highly creditworthy in relative terms, ensuring that a strong rate of “catch-up” has been maintained.

As of 2012, the IMF estimates that in purchasing power parity (PPP) terms the USA and the combined economies of Developed Europe are a similar size, each representing roughly one quarter of activity in our sample. China is about one fifth of the total. Japan and India each represent around 7% while Russia and Brazil are each about 4%. The combined weight of the major ASEAN economies sums to something close to 5%, almost 2 percentage points of which is represented by Indonesia; South Korea and Canada are a little over 2% each, with the former having a slight edge; while Australia comes in at 1.5%.

By 2017, which is the end point of the IMF projection, China has surpassed both the USA and Developed Europe, India has left Japan far behind and Korea is edging away from Canada, who has been surpassed by Indonesia in the meantime. So, the short period between this year and the end of the IMF projections, which we take as the jumping off point for our scenarios, is expected to see some important changes in relative rankings at the top and in the middle ranks.

The IMF estimates are taken as a neutral jumping off point for the scenarios to take any of the author’s own biases out of the equation. However, the author and many others have described the IMF forecasts, particularly in the shorter term regarding Europe, as tilted towards the optimistic end of the plausible range. That may be a function of the organisation’s conservative bias, and the indirect influence of the governments that comprise its stakeholders, which tends to produce trend-like, uncontroversial forecasts that are not too far from the assumptions embedded in national budget documents. Of course, the IMF does critique its own forecasts in a detailed semi-annual narrative. This discussion of the potential risks that may intercede and prevent trend-like growth from eventuating is a valuable check on the raw numbers. At present, the IMF clearly sees the balance of risks for world growth as skewed to the downside, which is entirely appropriate.

The scenarios: compilation and description

The method used to compile the scenarios is extremely simple. First, the United Nations’ medium fertility demographic projections are taken as given. Second, each scenario is underpinned by a projection of US economic growth, which defines the per capita frontier. Third, convergence assumptions for all other economies are chosen consistent with the tone of each scenario. In other words, each economy is assigned an ultimate target level of GDP per capita relative to the US, which may be reached before, after or at 2100 depending upon its historical performance level and the IMF defined starting point. Fourth, the size of national economies and the annual rate of growth are defined by back solving from the known variables (or more correctly, hard keyed assumptions) of population and the GDP per capita level relative to the frontier.

The five scenarios prepared have both a number and a name. They are

1. Blue Sky. In this scenario the economies of emerging Asia smoothly converge towards the living standards of a still expanding West, without interruption, over the full course of the twenty-first century.

2. China bull, Asia bear. In this scenario, China smoothly converges towards the living standards of a still expanding West, without interruption, over the course of the twenty-first century. However, the other economies of emerging Asia, including India, stall at middle income levels.

3. China bear, Asia bull. In this scenario, China stalls at middle income level, while the rest of emerging Asia, including India, smoothly converges towards the living standards of a still expanding West, without interruption, over the full course of the twenty-first century.

4. Emerging Asia bear. In this scenario, emerging Asia stalls at a middle income level en masse. There are no exceptions. The West expands on the trajectory defined for it in the Blue Sky scenario.

5. Grey skies for the West. In this scenario the economies of emerging Asia smoothly converge towards the living standards of a struggling West. In other words, emerging Asia catches up in a relative sense, but the bar is substantially lower than in the first four scenarios.

The Blue Sky scenario is the province of the optimist. Here emerging Asia transits the middle income phase of their development without disruption, inexorably closing in on a living standard three quarters of that enjoyed by the USA. Once that point is reached in each jurisdiction, their catch-up

phase concludes and they move forward at the same rate as the global frontier can be pushed out. Under these very generous assumptions, many of the major economies of emerging Asia will reach 75% of US income per capita before the end of this century (China in 2068; South Korea in 2019; Indonesia and Malaysia in 2100) while many others (India, Vietnam and Thailand) have that target within their grasp in the early part of the twenty-second century.

The China bull, Asia bear scenario describes a world where the most myopic Sinophiles are justified in their present optimism. The Chinese economy follows the same path mapped out for it in the Blue Sky scenario, whereas its regional neighbours find themselves unable to advance beyond middle income levels. Under these parameters, China is the largest economy in the world from 2016 onwards. Its share of activity will peak around one third at mid century and it will still comprise around 27% at 2100, despite its demographic challenges. The USA finishes the century with a slightly larger economy than India under these conditions. It is also worthy of note that the action of restraining growth in emerging Asia (but not in the non-Asian emerging markets) pushes Indonesia outside the top five economies in 2100. This is the only scenario in this study where that is the case.

0.0

0.1

0.2

0.3

0.4

0.0

0.1

0.2

0.3

0.4

1994 2004 2014 2024 2034 2044 2054 2064 2074 2084 2094

% of output % of outputJapan AU/CA/NZ Russia

Brazil South Korea Other ASEAN

Indonesia

Sources: IMF, author calcu la tions.

China

Developed Europe

USA

India

Scenario 1: blue sky

The China bear, Asia bull scenario is one for the myopic China sceptics and the demographically inclined bulls. China is prevented from ascending beyond middle income levels in this scenario, with its catch-up impetus halted around two-fifths of US levels, which means it will cease to grow faster than the US from approximately 2030. The other emerging Asian economies are left free to trace the paths laid out in the Blue Sky scenario.!

0.0

0.1

0.2

0.3

0.4

0.0

0.1

0.2

0.3

0.4

1994 2004 2014 2024 2034 2044 2054 2064 2074 2084 2094

% of output % of outputJapan AU/CA/NZ Russia

Brazil South Korea Other ASEAN

Indonesia

Sources: IMF, author calculations.

China

Developed Europe

USA

India

Scenario 2: China bull, Asia bear

0.0

0.1

0.2

0.3

0.4

0.0

0.1

0.2

0.3

0.4

1994 2004 2014 2024 2034 2044 2054 2064 2074 2084 2094

% of output % of outputJapan AU/CA/NZ Russia

Brazil South Korea Other ASEAN

Indonesia

Sources: IMF, author calculations.

China

Developed Europe

USA India

Scenario 3: China bear, Asia bull

The scale arithmetic here is simple and is particularly potent in the third quarter of the century: emerging Asia ex China grows swiftly in per capita terms while still enjoying a growing population. Simultaneously, China grows like a mature economy while absorbing the negative scale factor of a declining population of working age. That means a massive shift in the share of global activity that is conducted in these jurisdictions. Earth-shattering fact: under this set of conditions, India’s economy would be three times as large as China’s in 2100.

The emerging Asia bear scenario takes the trajectory for Chinese economic growth from scenario 3 (China bear) and the trajectory for other emerging Asian economies from scenario 2 (Asia bear). All emerging Asian economies will see their catch-up efforts stall at living standards between one quarter and one half of that enjoyed by the USA in 2100. The US’ share of global activity traces a flattened ‘U’ shape over the course of the century, bottoming in the 2040s and rebounding close to its current share by 2100. China’s abruptly halted catch-up allows the “tortoise” of Developed Europe to pass the Chinese “hare” in the last decade of the century. So a poor performance by the East would be sufficient to allow the West to rebound to a reasonably close facsimile of its current relative position in the long run.

The Grey Skies for the West scenario holds back the growth in developed country living standards while simultaneously allowing Emerging Asia to

0.0

0.1

0.2

0.3

0.4

0.0

0.1

0.2

0.3

0.4

1994 2004 2014 2024 2034 2044 2054 2064 2074 2084 2094

% of output % of outputJapan AU/CA/NZ Russia

Brazil South Korea Other ASEAN

Indonesia

Sources: IMF, author calculations.

China

Developed Europe

USAIndia

Scenario 4: Emerging Asia bear

catch up on a relative trajectory not far removed from the Blue Sky scenario. This is of course a lesser feat than if the West was flourishing and is thus associated with lower absolute living standards for all. This scenario is probably most attractive to those who see the present problems of private and public indebtedness in the West as a major impediment to future prosperity. Those who see an end to the “exorbitant privilege” associated with the US’ role as the provider of the global reserve currency and the benchmark ‘risk free’ asset; and a messy outcome (from an economic perspective at least) for the “European project”, should take particular note of the outcomes of this scenario. It is far from a worst possible case of course, but it does represent a century of diminishing expectations for those who did so well in the three that preceded it.

Of course, theoretically the analysis need not end with the discrete outcomes outlined above. By assigning probabilities to each of the basic scenarios, any number of composite scenarios can be calculated from the ‘raw materials’ as a weighted average. However, the scenarios have not been designed with a view to their being manipulated in this fashion. At this point in time the author would not recommend going too far down that path, although it may yet be a possible future avenue for developing the concept from the general to the bespoke.

0.0

0.1

0.2

0.3

0.4

0.0

0.1

0.2

0.3

0.4

1994 2004 2014 2024 2034 2044 2054 2064 2074 2084 2094

% of output % of outputJapan AU/CA/NZ Russia

Brazil South Korea Other ASEAN

Indonesia

Sources: IMF, author calculations.

China

Developed Europe

USA

India

Scenario 5: Grey skies for the West

Assessing the scenarios in the context of the US-Australia Alliance.

The most important themes and observations arising from the scenario work from the perspective of the US-Australia Alliance are arguably the following.

1. China will be the world’s largest economy for most of the time between 2016 and mid century in every scenario, even the most pessimistic. However, it finishes the century at number one in just one of the five scenarios (China bull, Asia bear), reaching 2100 in fourth place twice and second place twice. So China’s time in the sun is not very distant, and its ascent to the number one position in economic scale is unstoppable, but in the second half of the century it will be losing ground to others under most sets of conditions that do not include stagnation elsewhere in Asia. China’s moment as a dominant power without a near challenger in economic scale will reach its zenith circa 2040.

2. India is the largest economy in the world in 2100 in three of the five scenarios and is a close second in another two. In four out of five scenarios India spends at least some time as the world’s largest economy. India’s demographic profile is starkly different to China’s. This creates an enormous edge for India in terms of the growth of market size once the second half of the century gets under way. Any vision of the world economy in the long run, and of the security architecture that will evolve in the region, needs to have a very well defined position on India’s preferences in the matter.

3. The scenario that produces a world economic structure most consistent with a balance of power scenario (between the USA, Developed Europe, China and India) is one where all the major emerging Asian economies stall around middle income levels. This is also the scenario where the USA rallies back to number one by century’s end after falling behind in its middle decades. This potential future offers up some fascinating areas of speculation on the global financial architecture, socio-political developments in China and the relevance of middle powers in a century of delicate economic equipoise. It is also probably the one that would present the fewest challenges to the status quo position regarding the US-Australia Alliance. This scenario also highlights that for purposes of internal

consistency one should not be bullish on emerging Asian economic growth in the long run and simultaneously a believer that an evenly balanced multi-polar structure will emerge.

4. Developed Europe finishes the century as the world’s third or fourth largest economy in each scenario, indicating that it will remain economically relevant even in the face of the Asian ascent. The challenges presently facing the European economy are gigantic. But so is the region’s current global footprint, and even consistent growth under-performance relative to the US in the coming decades will add considerable increments to global output each and every year. And the demographics of the total region3 make interesting reading, with the drag on the working age population from ageing beginning to moderate from mid century, and turning back to growth by century’s end. Many may wish to simplify matters in the “Asian Century” by writing off the European economy as a unit of relevance. The data says that would be a dangerous abstraction. For instance, based on the scenarios presented here, it is the Japanese yen and the Great British Pound that will be removed from the IMF’s SDR (“special drawing rights”) currency basket4 to eventually make way for the Chinese yuan and the Indian rupee – not the euro. Nor would the euro be asked to give way to the Russian rouble5, the Indonesian rupiah or the Brazilian real.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! !!!!!!!!!!!!!!!!!!!!!3!For!the!purposes!of!this!study,!the!UN’s!demographic!projections!for!the!sum!of!Western,!Northern!and!Southern!Europe!have!been!used!to!proxy!“Developed!Europe”.!4!The!IMF!“special!drawing!rights”!currency!basket!is!an!accounting!unit!composed!of!the!four!currencies!that!are!perceived!to!play!the!most!important!roles!in!the!global!system,!based!on!factors!such!as!usage!in!international!trade!and!shares!of!global!reserve!holdings.!The!present!weights!and!composition,!which!have!prevailed!since!January!1,!2011,!are!the!US!dollar!(41.9%)!the!euro!(37.4%)!the!Japanese!yen!(9.4%)!and!the!Great!British!Pound!(11.3%).!The!next!re_weighting!is!due!in!2015.!5!Russia’s!national!currency!tends!to!be!spelt!“ruble”!in!the!United!States!and!“rouble”!elsewhere.!The!Oxford!English!Dictionary!agrees!with!the!latter!spelling.!China’s!national!currency!is!the!renmimbi!(“People’s!currency”.!abbreviation!RMB)!the!basic!unit!of!which!is!the!yuan!(abbreviation!CNY).!In!practice,!the!terms!are!interchangeable,!and!monetary!amounts!may!be!rendered!as!either!RMB!or!CNY,!although!the!formal!bilateral!currency!code!is!always!quoted!USD/CNY.!To!confuse!matters!further,!official!economic!data!is!generally!presented!by!the!National!Bureau!of!Statistics!in!units!of!RMB.!!

5. While the Japanese will remain a wealthy people, their economy’s size is surpassed in all scenarios by Indonesia, in most scenarios by Brazil and Russia, and on a single occasion each by Canada and the Philippines. The Japanese economy surpassed West Germany in the late 1960s and the USSR in the 1980s to become the world’s second largest national economy. It ceded that mantle to China in the first decade of the twenty first century, and it ceded the number three position to India soon after. It will not re-ascend such heights again.

6. No economy outside the top four will comprise more than 6.1% of world output (a relative position equivalent to China circa 1996) in any scenario. What is notable outside the top four is that Indonesia finishes the century as number five in every scenario but one, arguing that the widely used BRIC grouping of countries is not a particularly useful unit for long run analysis. Its window of relevance will prove quite short. These scenarios highlight that not only are China and India in a very different league to Brazil and Russia, but also that Indonesia will be a bigger economic factor than either of the latter two powers. Given Indonesia’s proximity to Australia, and its guarded relationship with both the US and China, this is of course a particularly relevant point for any considered discussion of the Alliance.

7. The scenarios draw out the stark differences in demographics profiles – as projected by the United Nations - across the major economies. Older societies (Japan, South Korea, Developed Europe, Russia, China) with contracting working age populations in the second half of the century fall away appreciably in relative economic scale. Young societies (India, Indonesia, the Philippines) with growing working age populations in the second half of the century forge ahead. Demographics are not destiny of course and overt reliance on them to drive dynamic analyses is a dangerous occupation. However, in a century where the demographic trajectories of groups of major powers are going to be opposite in sign, the implications for economic scale should not be under-estimated.

8. Weak growth in the advanced countries, particular for the frontier defining US, would be very damaging for absolute global living standards in the long run. Weak growth in the emerging world would keep the West “in the game” from a scale perspective throughout the century, but the trade off is a major loss of global prosperity. That

could serve to destabilise nations internally, precipitating unpredictable political responses. As a wealthy economy, Australia has a larger vested interest in the global productivity frontier being extended continually than an emerging economy with decades of ‘catch-up’ ahead of it. In terms of absolute global living standards, scenarios 4 and 5 produce similar low lying outcomes. Relative to the blue sky scenario, some $240 trillion of potential purchasing power is foregone at the global level in 2100 (circa 60% of scenario 4 and 5 average 2100 GDP), which equates to a loss of $22,000 per head.

Narrowing these results down still further, the major Alliance relevant outcomes are

1. India is the most likely nation to conclude the century as the unchallenged number one in terms of economic scale. If India is not #1, that position will be taken by either China or the US, an inconveniently ambiguous result.

2. The first half of the century is China’s: the second half is most unlikely to be China’s, although it is not impossible.

3. The US is not going to fade into obscurity as populous Asian economies rise in scale. Neither is Europe. But it will take a wholesale stagnation in Asia – a ubiquitous inability to avoid the middle income trap - for the US to be in position to re-assert its economic primacy.

4. Indonesia – Australia’s near neighbour – is inarguably the third most important emerging market behind India and China in terms of its projected long run strategic economic weight. Put another way, Indonesia may be the one country in the region able to graduate from middle power status.

5. If emerging Asian economies stall en masse at the middle income level, then a four way balance of global economic power is the likely outcome, with the North Atlantic on the ascent at century’s end. This point follows 3, developing the import of the Asian bear scenario further. It is vital to reiterate the opposite side of this observation: concepts of a multi-polar balance of power and bullish long run views on growth in emerging Asia are not compatible with each other over the full course of the century.

6. Japan is going to lag considerably behind both its advanced peers and its emerging neighbours. Its long run destiny may be that it becomes another middle power, joining current examples Australia, Canada

and South Korea, and future examples the Philippines and Vietnam. Proponents of a Chinese containment strategy would do well to think hard whether (or for how long) Japan would remain an effective vertex in such an alignment.

7. Energy spent considering the rise of Russia and Brazil should not come at the expense of time considering the top five economies in the sample. Those studying the Alliance should ignore the BRIC categorisation as a useful analytical grouping.

A risk averse reading of these results from the Australian side would argue for a consolidation of its Alliance structure, as the US will remain a major force irrespective of developments elsewhere. However, moving beyond this point, clarity on which of the five scenarios is going to be closer to the truth will take a considerable time to emerge: certainly “clarity” on the shape of the world economy in the second half of this century will post date the working careers of mid-level diplomats and security analysts – let alone the current leading thinkers and decision makers. Even if Australia were to prepare now to move away from the status quo, which is clearly not its preference, it would still not know exactly where to align itself even if the criteria for a change of alignment were to be carefully defined in economic terms. All that can be said with certainty is that India will have to be a central element in future strategic calculus; Indonesia will become even more important; the Chinese sun will dominate the heavens in the first half of this century and it will be very difficult not to be dazzled, projected second half decline notwithstanding; Japan’s strategic decline appears terminal; while European decline may have been greatly exaggerated.

Considering these results from the US side, the scenarios have put forward a useful rule of thumb on relative economic weight. If either of China or India navigates the middle income phase of its development successfully, they will surpass the US in size and will retain that advantage in scale. If they fall into the middle income trap, the US will retain a size advantage. This is an example where a little bit of knowledge might be construed as dangerous.

Armed with this information, should the US actively work to inhibit Chinese and Indian economic growth to retain its relative position? Armed with this information, how are the Chinese and Indian authorities to overcome their suspicion of Western advice; their perceptions of discrimination; their fear of technological and energy blockades? One hopes that the vast amount of foregone wealth indicated by the difference between projected world

economic activity in 2100 under the Blue Sky scenario and in the more pessimistic scenarios 4 and 5 is a sufficiently valuable hostage to prevent negative outcomes brought about by a naïve reading of the results.

!

Appendix one: individual scenario details

The two measures that command principal attention are relative living standards – assumptions on the progress of which define the scenarios - and relative economic scale, which is our ultimate interest in terms of assessing longer run security questions. These two measures are presented in table form for each nation/region for which individual trajectories have been defined, at various time stamps between 2012 and 2100. The upper panel is for living standards (assumptions) and the lower panel is for relative shares of activity (outcomes).

!

1

Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are

reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Income per head, % of US 2012 2020 2030 2040 2050 2070 2100

United States 100 100 100 100 100 100 100

Japan 71 68 68 69 70 72 75

Developed Europe 73 71 71 72 74 76 79

China 19 31 52 68 73 75 75

India 8 11 19 29 41 64 75

Russia 36 40 50 60 67 73 75

Brazil 25 30 41 52 62 72 75

South Korea 70 76 84 85 85 85 85

Indonesia 10 14 21 30 39 58 71

Thailand 20 24 33 40 47 62 73

Malaysia 34 39 49 54 60 71 75

Philippines 9 11 16 23 30 45 56

Vietnam 7 11 18 27 38 59 71

Canada 84 81 80 82 84 88 94

Australia 85 85 87 88 89 91 94

New Zealand 59 58 59 62 66 73 79

Share of output, % of world 2012 2020 2030 2040 2050 2070 2100

United States 23.6 20.6 17.2 15.2 14.0 13.1 13.7

Japan 6.9 5.5 4.3 3.4 2.9 2.3 2.1

Developed Europe 24.6 20.2 16.2 13.9 12.5 10.8 10.7

China 19.0 26.1 32.1 33.1 31.3 25.7 20.3

India 7.4 9.5 12.5 16.2 20.6 28.2 31.2

Russia 3.8 3.5 3.0 2.8 2.7 2.5 2.3

Brazil 3.7 3.8 4.0 4.1 4.3 4.3 3.9

0.0 0.0 0.0 0.0 0.0 0.0 0.0

South Korea 2.5 2.3 1.9 1.6 1.4 1.1 0.9

Indonesia 1.8 2.2 2.6 3.0 3.4 4.2 5.5

Thailand 1.0 1.0 1.1 1.0 1.0 1.1 1.2

Malaysia 0.7 0.8 0.8 0.8 0.8 0.9 1.0

Philippines 0.6 0.7 0.9 1.1 1.4 1.9 2.9

Vietnam 0.5 0.6 0.8 1.0 1.2 1.5 1.7

Canada 2.2 1.9 1.5 1.4 1.3 1.2 1.3

Australia 1.5 1.3 1.2 1.0 1.0 0.9 1.0

New Zealand 0.2 0.2 0.1 0.1 0.1 0.1 0.1

Scenario 1: Blue sky

Source: Author calculations except for 2012, which are IMF estimates.

2

Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are

reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Income per head, % of US 2012 2020 2030 2040 2050 2070 2100

United States 100 100 100 100 100 100 100

Japan 71 68 70 71 72 74 77

Developed Europe 73 71 73 74 76 78 81

China 19 31 50 63 70 75 75

India 8 11 18 25 28 29 30

Russia 36 40 47 55 62 71 75

Brazil 25 30 39 48 56 69 75

South Korea 70 76 79 80 80 80 80

Indonesia 10 14 20 26 29 30 30

Thailand 20 24 31 36 38 39 39

Malaysia 34 39 46 49 50 50 50

Philippines 9 11 15 20 22 23 24

Vietnam 7 11 17 24 26 28 30

Canada 84 81 80 82 84 88 94

Australia 85 85 87 88 89 91 94

New Zealand 59 58 59 62 66 73 79

Share of output, % of world 2012 2020 2030 2040 2050 2070 2100

United States 23.6 20.6 17.2 15.4 15.0 15.9 18.4

Japan 6.9 5.5 4.3 3.4 3.1 2.8 2.8

Developed Europe 24.6 20.2 16.2 14.0 13.3 13.1 14.4

China 19.0 26.1 32.1 33.5 33.4 31.2 27.2

India 7.4 9.5 12.5 15.6 16.7 17.5 17.2

Russia 3.8 3.5 3.0 2.9 2.9 3.0 3.1

Brazil 3.7 3.8 4.0 4.2 4.6 5.3 5.2

South Korea 2.5 2.3 1.9 1.6 1.5 1.3 1.2

Indonesia 1.8 2.2 2.6 3.0 3.1 3.1 2.9

Thailand 1.0 1.0 1.1 1.0 1.0 0.9 0.9

Malaysia 0.7 0.8 0.8 0.8 0.8 0.8 0.9

Philippines 0.6 0.7 0.9 1.1 1.2 1.4 1.6

Vietnam 0.5 0.6 0.8 1.0 1.0 1.0 1.0

Canada 2.2 1.9 1.5 1.4 1.4 1.5 1.8

Australia 1.5 1.3 1.2 1.1 1.0 1.1 1.3

New Zealand 0.2 0.2 0.1 0.1 0.1 0.2 0.2

Scenario 2: China bull, Asia bear

Source: Author calculations except for 2012, which are IMF estimates.

3

Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are

reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Income per head, % of US 2012 2020 2030 2040 2050 2070 2100

United States 100 100 100 100 100 100 100

Japan 71 68 70 71 72 74 77

Developed Europe 73 71 73 74 76 78 81

China 19 29 38 38 38 38 38

India 8 11 18 26 37 57 72

Russia 36 40 47 55 62 71 75

Brazil 25 30 39 48 56 69 75

South Korea 70 76 79 82 83 85 84

Indonesia 10 14 20 27 35 50 75

Thailand 20 24 31 37 42 55 75

Malaysia 34 39 46 51 55 65 74

Philippines 9 11 15 21 27 39 59

Vietnam 7 10 15 23 31 49 69

Canada 84 81 80 82 84 88 94

Australia 85 85 87 88 89 91 94

New Zealand 59 58 59 62 66 73 79

Share of output, % of world 2012 2020 2030 2040 2050 2070 2100

United States 23.6 21.1 18.6 17.5 16.4 15.0 15.2

Japan 6.9 5.6 4.6 3.9 3.4 2.7 2.3

Developed Europe 24.6 20.7 17.6 15.9 14.6 12.4 11.9

China 19.0 24.4 26.5 23.2 20.0 15.0 11.5

India 7.4 9.7 13.5 18.7 24.0 32.3 34.7

Russia 3.8 3.5 3.3 3.3 3.1 2.8 2.6

Brazil 3.7 3.8 4.3 4.8 5.0 5.0 4.3

South Korea 2.5 2.4 2.1 1.9 1.7 1.3 1.0

Indonesia 1.8 2.2 2.8 3.5 4.0 4.8 6.1

Thailand 1.0 1.1 1.1 1.2 1.2 1.2 1.4

Malaysia 0.7 0.8 0.9 0.9 0.9 1.0 1.1

Philippines 0.6 0.7 0.9 1.3 1.6 2.2 3.2

Vietnam 0.5 0.6 0.7 1.0 1.3 1.7 1.9

Canada 2.2 1.9 1.7 1.6 1.5 1.4 1.5

Australia 1.5 1.3 1.3 1.2 1.1 1.1 1.1

New Zealand 0.2 0.2 0.2 0.2 0.2 0.2 0.2

Scenario 3: China bear, Asia bull

Source: Author calculations except for 2012, which are IMF estimates.

4

Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are

reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Income per head, % of US 2012 2020 2030 2040 2050 2070 2100

United States 100 100 100 100 100 100 100

Japan 71 68 70 71 72 74 77

Developed Europe 73 71 73 74 76 78 81

China 19 29 38 38 38 38 38

India 8 11 18 25 28 29 30

Russia 36 40 47 48 48 48 48

Brazil 25 30 39 40 40 40 40

South Korea 70 76 79 80 80 80 80

Indonesia 10 14 20 26 29 30 30

Thailand 20 24 31 36 38 39 39

Malaysia 34 39 46 49 50 50 50

Philippines 9 11 15 20 22 23 24

Vietnam 7 10 15 21 24 26 27

Canada 84 81 80 82 84 88 94

Australia 85 85 87 88 89 91 94

New Zealand 59 58 59 62 66 73 79

Share of output, % of world 2012 2020 2030 2040 2050 2070 2100

United States 23.6 21.1 18.6 18.0 18.1 19.5 22.1

Japan 6.9 5.6 4.6 4.0 3.7 3.5 3.4

Developed Europe 24.6 20.7 17.6 16.4 16.1 16.1 17.3

China 19.0 24.4 26.5 23.8 22.1 19.4 16.7

India 7.4 9.7 13.5 18.2 20.2 21.5 20.8

Russia 3.8 3.5 3.3 2.9 2.7 2.5 2.4

Brazil 3.7 3.8 4.3 4.1 3.9 3.7 3.3

South Korea 2.5 2.4 2.1 1.9 1.8 1.6 1.4

Indonesia 1.8 2.2 2.8 3.4 3.7 3.7 3.5

Thailand 1.0 1.1 1.1 1.2 1.2 1.1 1.0

Malaysia 0.7 0.8 0.9 0.9 0.9 1.0 1.1

Philippines 0.6 0.7 0.9 1.3 1.4 1.7 1.9

Vietnam 0.5 0.6 0.7 1.0 1.1 1.1 1.1

Canada 2.2 1.9 1.7 1.6 1.7 1.8 2.1

Australia 1.5 1.3 1.3 1.2 1.3 1.4 1.6

New Zealand 0.2 0.2 0.2 0.2 0.2 0.2 0.2

Scenario 4: Asia bear

Source: Author calculations except for 2012, which are IMF estimates.

5

Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are

reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Income per head, % of US 2012 2020 2030 2040 2050 2070 2100

United States 100 100 100 100 100 100 100

Japan 71 68 68 69 70 72 75

Developed Europe 73 71 71 72 74 76 79

China 19 31 52 68 73 75 75

India 8 11 19 29 41 64 75

Russia 36 40 50 60 67 73 75

Brazil 25 30 41 52 62 72 75

South Korea 70 76 84 85 85 85 85

Indonesia 10 14 21 30 39 58 71

Thailand 20 24 33 40 47 62 73

Malaysia 34 39 49 54 60 71 75

Philippines 9 11 16 23 30 45 56

Vietnam 7 11 18 27 38 59 71

Canada 84 81 80 82 84 88 94

Australia 85 85 87 88 89 91 94

New Zealand 59 58 59 62 66 73 79

Share of output, % of world 2012 2020 2030 2040 2050 2070 2100

United States 23.6 20.6 16.7 14.5 13.3 12.5 13.6

Japan 6.9 5.5 4.1 3.2 2.7 2.2 2.0

Developed Europe 24.6 20.1 15.4 12.8 11.6 10.1 10.4

China 19.0 26.1 32.9 34.0 31.2 24.6 20.2

India 7.4 9.5 12.8 17.0 22.0 30.0 32.4

Russia 3.8 3.5 3.1 2.9 2.7 2.4 2.3

Brazil 3.7 3.8 4.1 4.3 4.5 4.3 3.9

South Korea 2.5 2.3 1.9 1.6 1.4 1.1 0.9

Indonesia 1.8 2.2 2.7 3.2 3.7 4.7 5.2

Thailand 1.0 1.0 1.1 1.1 1.1 1.2 1.2

Malaysia 0.7 0.8 0.8 0.8 0.8 0.9 1.0

Philippines 0.6 0.7 0.9 1.2 1.5 2.1 2.8

Vietnam 0.5 0.6 0.8 1.0 1.3 1.7 1.7

Canada 2.2 1.9 1.5 1.3 1.2 1.2 1.3

Australia 1.5 1.3 1.1 1.0 0.9 0.9 1.0

New Zealand 0.2 0.2 0.1 0.1 0.1 0.1 0.1

Scenario 5: Grey skies for the West

Source: Author calculations except for 2012, which are IMF estimates.