world investment report - unctadunctad.org/en/docs/wir2005ch3_en.pdf · technology transfer can...

TRANSCRIPT

United Nations Conference on Trade and Development

WorldInvestmentReport

United NationsNew York and Geneva, 2005

2005 Transnational Corporations andthe Internationalization of R&D

INTRODUCTION

Bridging the technology gap betweencountries is necessary to foster sustainableeconomic development. Technology is advancingfaster than ever before. Developing countries thatfail to build capabilit ies enabling them toparticipate in the evolving global networks ofknowledge creation risk falling further behindin terms of competitiveness as well as economicand social development. While internationaltechnology transfer can bring importantknowledge to an economy, that alone is notenough. Using new technologies efficientlyrequires creating additional absorptive capacity,while a continuous effort has to be made to keepup with technical change. This is particularly truegiven the fact that wages tend to rise as a countrydevelops, facilitating the entry of lower costcompetitors in the market. While actions of bothdomestic enterprises and the government areessential to build technology capabilities indeveloping countries, TNCs can also play a role.

One of the main reasons why developingcountries promote inward FDI is indeed to linkup to the global technology and innovationnetworks led by these firms. In terms of creatingnew technology and diffusing it internationally,TNCs are world leaders in many industries. Theyaccount for the bulk of global businessexpenditures on R&D. They dominate newpatents and often lead innovation in managementand organization. Establishing links with theirinnovation and production networks can helpcountries enhance their technological capabilitiesand enable them to compete better in internationalmarkets.

Technological capabilities are difficult toacquire. The rapid pace of technical change andthe growing importance of science-basedtechnologies in many industries call for moreadvanced and diverse skills and intense technicaleffort. These require better infrastructure, not the

least in information and communicationstechnologies. They also require strong supportinginstitutions as well as stable and efficient legaland governance systems. Moreover, they requireaccess to the international knowledge base,combined with a strategy to leverage this accessfor the benefit of local innovation systems. Thecumulative forces that are increasing the gapbetween countries with respect to innovationperformance make the role of policy increasinglyimportant at all levels – national and international.

The manner in which TNCs allocate theirR&D activities internationally is significant inthis context. R&D is among the leastinternationalized functions of TNCs.Traditionally, when R&D internationalizationtook place, both home and host countries werefound in the developed world. To the extent thatTNCs undertook R&D in developing countries,they did so almost exclusively to adapt productsand processes to local conditions. These stylizedfacts have begun to change.

These changes manifest themselves inseveral ways. First , the degree of R&Dinternationalization by firms is rising in all keyhome countries as part of the overall trendtowards the offshoring of services (WIR04).German TNCs, for example, set up more foreignR&D units during the 1990s than they did duringthe preceding 50 years (Ambos 2005). Second,R&D internationalization is now growing fastestin some host developing countries, notably inAsia. Third, the drivers of R&Dinternationalization are changing. The processis no longer driven only by the need for localadaptation or to tap into established knowledgecentres. In response to increasing competition,TNCs now relocate segments of R&D so as toaccess foreign pools of research talent, reduceR&D costs and speed up the process oftechnology development. Fourth, R&D in some

developing countries now goes well beyond localadaptation and involves complex stages of R&Don a par with work undertaken in the developedeconomies. Fifth, developing-country firms arealso setting up R&D units abroad. These trendshave become apparent only in the past few yearsand are likely to continue.

This new phenomenon is partly expectedand partly unexpected. It is expected in two ways.First, in most cases R&D undertaken abroadsupports production. As TNCs increaseproduction in developing countries, some R&D(of the adaptive kind) can be expected to follow.Second, R&D is a form of service activity. Manyother services are fragmenting in a processwhereby certain segments are located in countrieswith lower wages and appropriate skills. It is notsurprising that R&D is following suit. Indeed,the survey of Europe’s largest firms conductedin 2004 by UNCTAD and Roland Berger showedthat all service functions – including R&D – arenow candidates for offshoring (WIR04). It isunexpected in that R&D is a service activity withvery demanding skill, knowledge and supportneeds — traditionally only met in developedcountries with strong national innovationsystems. Moreover, R&D is taken to be the least“fragmentable” of economic activities becauseit involves knowledge that is strategic to firms,and because it often requires dense knowledgeexchange (much of it tacit) between users andproducers within localized clusters. A home-country bias in R&D activities “reflects thelinguistic and geographic constraints imposed byperson-embodied exchanges and transfers of tacitknowledge” (Patel and Pavitt 2000, p 218).

The extent to which developing countriesconnect with the internationalizing R&Dnetworks of TNCs depends in particular on thestrength of their national innovation systems. Thisin turn is dependent on policies, the quality ofinstitutions (including both organizations and therules governing innovation activities), the qualityof human resources and the production andinnovative capabilities of enterprises. Innovation

reflects an intense interaction between firms andother actors in the public and private sectors.Innovation in developing countries is often carriedout on the shop floor, in process or productengineering, quality control, procurement,distribution and overall management. However,a significant part also involves technical effortin R&D laboratories separated from production.R&D-based innovation is greater the moreadvanced, fast changing and large-scale thetechnology involved, but it is needed even if itdoes not aim to push forward frontiers ofknowledge.

Part Two of WIR05 reviews recent trendsin the internationalization of R&D by TNCs. Itbegins in chapter III by looking at the linksbetween R&D, innovation and development, andconsiders the levels of innovative capabilitiesamong countries around the world. Large gapsin this area prevail between countries — gapsthat limit the ability of many of them to take partin the global networks of knowledge creation anddiffusion. Addressing these gaps is a majordevelopment challenge; it is also essential toensure that the internationalization of R&D byTNCs benefits larger parts of the world.

Chapter IV identifies the main players(firms and countries) in the R&Dinternationalization process. The analysis isconfined to R&D due to data constraints, but,where available, other qualitative informationrelated to innovation, notably in services, is alsoconsidered. Chapter V discusses the changingdrivers and determinants of R&Dinternationalization. Chapter VI reviews theimplications of R&D internationalization for hostand home economies, recognizing the difficultiesinvolved in assessing the impact of thisphenomenon. The last two chapters (VII andVIII) focus on policy implications at the nationaland international levels. They place particularemphasis on the need to promote interactionbetween TNCs and domestic players (firms andinstitutions) in national innovation systems.

100 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

A. Innovation matters forall countries

Innovative activity and capabilities areessential for economic growth and development.A recent report identifies science, technology andinnovation as essential to achieving theMillennium Development Goals (UN MillenniumProject 2005, Sachs and McArthur 2005). Thisis true for the industrialized countries that areat the technology frontiers, as well as fordeveloping countries that need to catch up interms of technology.

Given the large gap between the developedand developing countries in terms oftechnological advancement, the latter continueto rely heavily on technology transfer from theformer in their development process. However,sustainable economic development requires thatcountries do more than simply “open up” andpassively wait for new technologies to flow in.It demands active, continuous technological effortby enterprises, along with government policiesthat help firms attract technologies, use themeffectively and innovate. Technology requiresefforts to absorb and adapt; it has strong “tacit”elements that cannot be embodied in equipmentor codified in instructions or blueprints. Tacitknowledge can only be transferred effectivelyif the recipient develops capabilities to learn andincorporate the knowledge. It must seek newinformation, experiment with the technology, findnew ways of organizing production and train itsemployees in new skills. It involves not just theenterprise itself but also interaction with otherfirms and institutions.

The development of technologicalcapabilities has always been necessary for theeffective use of new technologies; all the moreso today. Greater openness to trade and capital

��������

INNOVATION, R&D AND DEVELOPMENTflows does not reduce the need for localtechnological effort – on the contrary.Technologies are changing more rapidly, fallingtransport costs and liberalization are intensifyingcompetition, and TNCs are seeking locations withstrong capabilit ies to produce efficiently.Moreover, i t is not just export-orientedmanufacturing that needs to be competitive;manufacturers selling to domestic markets haveto compete against imports. Export-orientedservices and primary activities need to use newtechnologies to remain competitive in worldmarkets. The development of new capabilitiesapplies to both technical functions andmanagerial ones: organizational and marketinginnovation is as important as technical innovationto growth and competitiveness (Teece 2000).

Technological innovation means theintroduction of new products, processes orservices into the market.1 Innovation does notnecessarily mean pushing the frontiers ofknowledge, particularly in a developing-countrycontext. Rather, innovations can be new to theuser but not necessarily new to the world.2 Thenature of innovation – and of required capabilities– varies greatly between activities according totheir technological complexity, the creation ofnew technology being at one extreme and the useof existing technologies at the other.3 Figure III.1shows an illustrative pyramid, with the leastcomplex technological functions (in terms ofinnovative efforts) at the base, and the mostdemanding ones at the top.4 While thesecategories are generic activities in all threesectors – primary, manufacturing and services– they can be adapted to different technologiesto take account of particular machinery, process,product and organizational characteristics.

• The starting point is the acquisition of basicproduction capabilities to absorb and useexisting technology. This sounds easy but

102 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

it is not, at least in order for capabilities tomatch relevant global best practice and foractivity that goes beyond simple assembly.Reaching internationally acceptable levels ofproduction efficiency and quality in complexactivities is very demanding. Manyenterprises fail to do this, even after yearsof operation, unless they invest sufficientlyin collecting information, creating new skillsand developing appropriate managementstructures.

• Absorption and adaptation of technology areparticularly challenging if conditions aresignificantly different from those at the originof the technology, and if local support andsupply structures are weak.

• Adaptation, in turn, can grow into significanttechnological improvement and technologicallearning, with systematic efforts made toimprove product and process performance.At this stage, many firms start monitoringinternational technological trends andselecting those technologies that can feed intotheir own efforts.

• Finally there is the frontier innovation stage,when firms design, develop and test entirelynew products and processes.

Research and development (R&D) is onesource of innovation (box III.1). In the early stagesof technological activity, enterprises need not setup formal R&D departments. As they mature,however, it becomes increasingly desirable tomonitor, import and implement technologies. R&Das a distinct activity may appear as early as thesecond level of complexity, where multifacetedtechnologies are involved or if local conditionsdemand significant adaptation. In a developingcountry, such R&D is feasible once the operationis fairly large scale and the necessary technicalskills are available. The role of formal R&D thengrows as the firm attempts significanttechnological improvements to introduce newproducts or processes. Firms that reach the highestlevel in the pyramid need not, however, be frontierinnovators (technological “leaders”) – their R&Dmay build on or improve upon innovations doneelsewhere (technological “followers”). Aspecialized unit not involved in routine technicalor production work is needed to monitor newdevelopments outside the firm or country, assesstheir significance for the firm and master, adaptand improve on existing technologies.5 FormalR&D becomes an essential part of the

Figure III.1. Stages of technology development by innovation effort

Source: UNCTAD.

FRONTIERINNOVATION

Create new technologies:as leader or follower

TECHNOLOGYIMPROVEMENT &

MONITORING

Change products and processes, plant layout, productivitymanagement and quality systems, procurement methods andlogistics to adapt technology to local or export-market needs.

This is based on in-house experimentation and R&D as well ason search and interactions with other firms and institutions

SIGNIFICANT ADAPTATION

BASIC PRODUCTION

Train workers in essential production and technical skills; reach plant design capacityand performance levels; configure products and processes; set up essential quality

management systems; institute supervisory, procurement and inventory managementsystems; establish in-bound and out-bound logistics

Improve products, processes and skills toraise productivity and competitiveness,

based on own R&D, licensing, interactionswith other firms or institutions

103CHAPTER III

technological learning process, especially forcomplex and fast moving technologies.

Empirical studies suggest a directrelationship between R&D and growth.6 Thelong-term impacts on economic growth of publicR&D and business R&D have been found to bestrong and significant (Guellec and vanPottelsberghe 2004a). Business R&D undertakenin other countries also plays an important role.Moreover, increased domestic business R&Daccentuates the positive impact of both publicand foreign business R&D. In other words,business R&D (either domestic or foreign-funded) has both a direct impact on a country’seconomic growth and an indirect one throughimproved absorption of the results of public R&Dand R&D performed in other countries.

Enterprises are the principal agents ofinnovation today, but they do not innovate andlearn in isolation. They rely on intricate (formaland informal) links with other firms and withpublic research institutions, universities and other

knowledge creating bodies like standards andmetrology institutes. In undertaking innovation,they react to government policies on trade,competition, investment and innovation. Theyseek human resources for innovation from theeducation and training system, and they drawupon the financial system for funding innovativeefforts. The complex web within whichinnovation occurs is commonly referred to as the“national innovation system” or NIS (Nelson1993, Lundvall 1992b).

Most of the NIS li terature focuses onfrontier invention in industrialized countries,rather than on mastery and adaptation oftechnology that take place in developingcountries. However, the innovation systemconcept is just as relevant for the latter (UNIDO2003, Edquist and McKelvey 2001). Mostlearning, mastery and adaptive activity requiresclose and continuous interaction with otherenterprises l ike suppliers, subcontractors,competitors and consultants, as well as with otheractors such as public R&D institutes, universities,

R&D is only one component of innovationactivities, but it represents the most developed,widely available, and internationally comparablestatistical indicator of industrial innovationactivities.

According to international guidelines, R&D(also called research and experimentaldevelopment) comprises creative work“undertaken on a systematic basis in order toincrease the stock of knowledge, includingknowledge of man, culture and society, and theuse of this stock of knowledge to devise newapplications” (OECD 2002b, p. 30).

R&D involves novelty and the resolutionof scientific and technological uncertainty. Itincludes basic and applied research along withdevelopment (United States, NSB 2004):

• Basic research. The objective of basic researchis to gain a more comprehensive knowledgeor understanding of the subject under studywithout specific applications in mind. Inindustry, basic research is defined as researchthat advances scientific knowledge but doesnot have specific immediate commercialobjectives.

• Applied research. The objective of appliedresearch is to gain the knowledge orunderstanding to meet a specific, recognizedneed. In industry, applied research includesinvestigations to discover new scientificknowledge that has specific commercialobjectives with respect to products, processes,or services.

• Development. Development is the systematicuse of the knowledge or understanding gainedfrom research directed towards the productionof useful materials, devices, systems ormethods, including the design and developmentof prototypes and processes.

For data collection purposes, the boundarybetween R&D and other technological innovationactivities can be found in pre-productiondevelopment activities (OECD 2002b). Inpractice, however, it is difficult to make thedistinction. In technology-intensive industriesdistinguishing between “research” and“development” is especially difficult since muchof the R&D work conducted involves closeinteraction between researchers in both the privateand public sectors, often also including closecollaboration with customers and suppliers (BIAC2005, Amsden and Tschang 2003).

Box III.1. Definition of R&D

Source: UNCTAD and Moris 2005b.

104 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

the metrology, standards, testing and quality(MSTQ) system, small and medium-sizedenterprise (SME) extension services, venturecapital funds and export marketing or traininginstitutions. A good supportive institutionalinfrastructure is therefore important for effectiveinnovation. Incentive structures that fosterentrepreneurship, risk-taking and innovation atthe firm, industry and university level are alsoimportant.

As the internationalization of productiondeepens and communication costs decline, eachNIS increasingly draws on knowledge createdin other systems. Rapid technical progress andthe rising costs and risks of innovation forceinnovators to seek centres of scientific excellenceinternationally. Global production networks – inwhich TNCs play the leading role – link togetherthe productive activities that underly innovation.Parent companies are instrumental in suchnetworks, providing the initial technology to theiraffiliates and helping them absorb, adapt andsubsequently upgrade it . As a result , theinnovation systems of more and more countriesare becoming interlinked in a global network in

which technological activity is international andinformation networks span the world.

From an economic developmentperspective it is becoming increasingly importantto take part in this international exchange. Thosecountries that are in a position to do so stand abetter chance of accessing new technologies atan early stage, as well as commercializinginnovations developed in their own NIS. However,the capabilities needed for participating areunequally distributed among countries (seebelow), which increases the risk of a furtherwidening of already large development gaps.

While there are different ways for countriesto participate in the international exchange ofinnovation (box III.2), WIR05 focuses on the roleof TNCs in this process, with special emphasison the internationalization of R&D. As notedabove, R&D is not always necessary forinnovation. Due to data limitations, however, theanalysis in Part Two is confined to this particulartype of innovative activity. The next two sectionsdescribe the global allocation of R&D and ofinnovative capabilities. Subsequent chapters

Box III.2. Different ways of internationalizing innovation

There are three main categories ofinnovation internationalization (box table III.2.1).In the first category, national enterprises and TNCsas well as individuals are engaged in theinternational commercialization of technologydeveloped at home. The second category relatesto domestic and international technical and

scientific collaborations among private and publicinstitutions, including domestic firms and TNCs,universities and research centres. Internationalinnovation by TNCs is the third category. TheTNC is the only institution that, by definition,can control and carry out within its boundariesthe process of innovation across the globe.

Source: UNCTAD.

Box table III.2.1. Taxonomy of internationalization of innovation

Category Actors Forms

International exploitation Profit-seeking (national and • Exports of innovative productsof nationally produced transnational) firms and • Cession of licenses and patentsinnovations individuals • Foreign production of innovative goods internally

designed and developed

International techno- Universities and public • Joint scientific projectsscientific collaborations research centres • Scientific exchanges, sabbaticals

• International flows of studentsNational and transnational • Joint ventures for specific projectsfirms • Production agreements with exchange of technical

information and/or equipment

International generation TNCs • R&D and other innovative activities both in homeof innovations and host countries

• Acquisitions of existing R&D units or greenfieldR&D investment in host countries

Source: adapted from Archibugi and Michie 1995, Narula and Zanfei 2004.

105CHAPTER III

focus on the internationalization of R&D, thetrend towards increased R&D by TNCs indeveloping countries, the driving forces behindthis phenomenon, potential impacts and policyimplications.

B. Global R&D trends

1. R&D is geographicallyconcentrated

Between 1991 and 1996, global R&Dspending increased from $438 billion to $576billion (an average annual growth of 4.4%; annex

table A.III.2). The momentum of R&D spendingcontinued throughout the late 1990s and thebeginning of the new millennium. By 2002 it hadrisen to $677 bill ion,7 corresponding to anaverage annual growth rate of 2.8% since 1996.

R&D expenditure is geographicallyconcentrated. In 1996 and 2002, the ten largestspenders accounted for more than 86% of theworld total, with their share marginally increasingover that period (table III.1). Eight of them aredeveloped countries, of which the United Statesreported by far the largest amounts in both years.Only two developing countries are among the topten: China and the Republic of Korea.

Table III.1. The 10 leading economies in R&D and business R&D spending,1996 and 2002

(Ranked by their 2002 values, billions of dollars)

Total R&D Business R&D

Rank Economy 1996 2002 Rank Economy 1996 2002

World 575.6 676.5 World 376.3 449.81 United States 197.3 276.2 1 United States 142.4 194.42 Japan 138.6 133.0 2 Japan 92.5 92.33 Germany 52.3 50.2 3 Germany 34.6 34.84 France 35.3 32.5 4 France 21.8 20.65 United Kingdom 22.4 29.3 5 United Kingdom 14.5 19.66 China 4.9 15.6 6 Korea, Republic of 9.9 10.47 Korea, Republic of 13.5 13.8 7 China .. 9.58 Canada 10.1 13.8 8 Canada 5.9 7.99 Italy 12.6 13.7 9 Sweden 6.6 a 7.3 b

10 Sweden 8.8 a 9.4 b 10 Italy 6.7 6.6Total 495.8 587.6 Total 334.7 c 403.4Share in world (%) 86.1 86.9 Share in world (%) 88.9 89.7

Developing economies, Developing economies,South-East Europe and CIS 44.5 57.1 South-East Europe and CIS 20.4 31.9

1 China 4.9 15.6 1 Korea, Republic of 9.9 10.42 Korea, Republic of 13.5 13.8 2 China .. 9.53 Taiwan Province of China 5.0 6.5 3 Taiwan Province of China 2.9 4.04 Brazil 6.0 4.6 e 4 Russian Federation 2.6 3.05 Russian Federation 3.8 4.3 5 Brazil 2.7 1.9 e

6 India 2.1 3.7 b 6 Singapore 0.8 1.27 Mexico 1.0 2.7 7 Mexico 0.2 0.8 b

8 Singapore 1.3 1.9 8 Turkey 0.2 0.49 Turkey 0.8 1.2 9 Hong Kong, China 0.2 d 0.3

10 Hong Kong, China 0.7 d 1.0 10 Chile 0.1 0.2Total 39.1 55.4 Total 19.7 31.5Share in developing economies, Share in developing economies,South-East Europe and CIS (%) 88.0 97.0 South-East Europe and CIS (%) 96.4 98.7

Source: UNCTAD, based on annex table A.III.2.a 1995.b 2001.c In 1996, Switzerland was the 10th largest spender on business R&D ($5.7 billion). Thus, the total of the top ten in

that year was $340.4 billion.d 1998.e 2003.

106 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

The growth in global R&D is partly dueto increased expenditures by the largest spenders.Between 1996 and 2002, the growth in the R&Dexpenditure of the United States (5.8% per year)was twice as high as the world average. Canadaand the United Kingdom also showed fastexpansion during that period. The expendituresof China rose at an average annual rate of morethan 20% during the same period. This dynamismcontrasts sharply with the trends of France,Germany and Japan, where R&D expendituresactually contracted in dollar terms.8

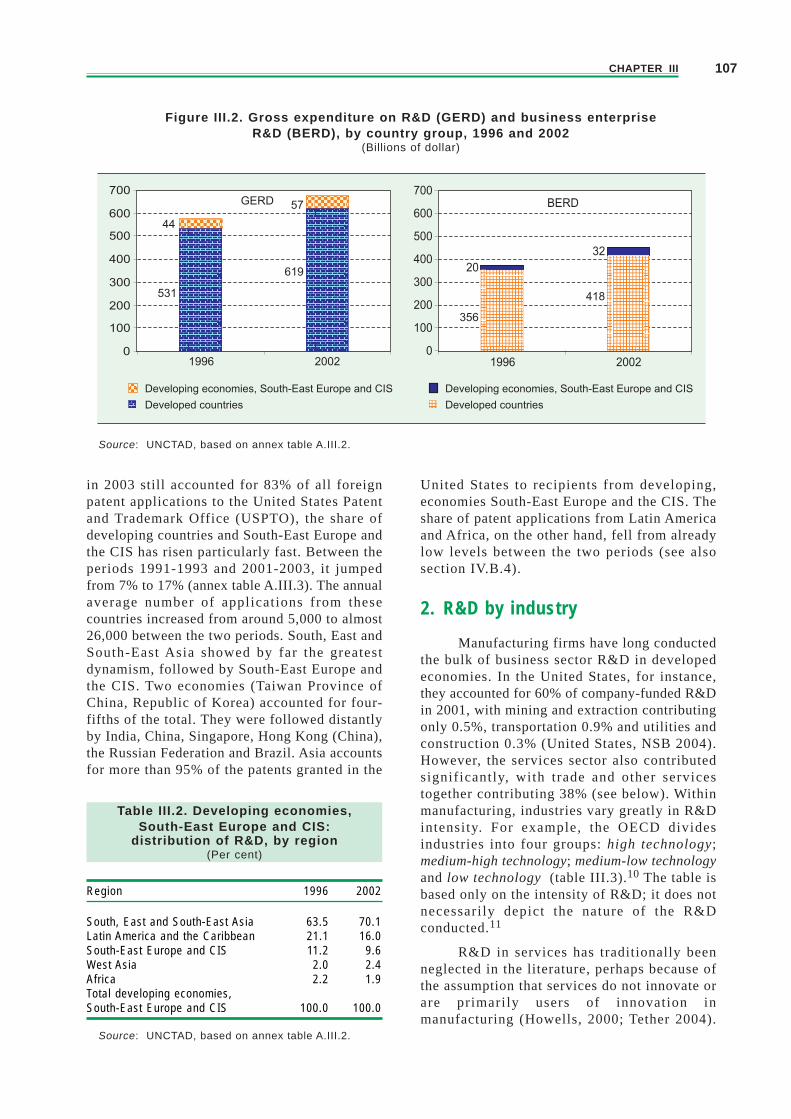

The combined share of developingeconomies, South-East Europe and the CIS inglobal R&D spending is on the rise, althoughfrom a very low level. In 1991 they accountedfor only 2.5% of the world total (annex tableA.III.2). By 1996 their share had reached 7.7%,and by 2002 it had increased further to 8.4%(figure III.2). This increase was concentratedmainly in South, East and South-East Asia (tableIII.2), which accounted for a dominant andgrowing share in R&D expenditure outsidedeveloped countries (more than two-thirds in2002). With the exception of West Asia, the shareof all other subregions in the grouping droppedbetween 1996 and 2002. The decline was the mostpronounced in Latin America and the Caribbean,the share of which shrunk from 21% to 16% ofthe total for the countries included in table III.2.Africa’s share also declined from 2.2% to 1.9%.

The concentration of R&D expendituresoutside developed countries is high and rising.The ten largest R&D spenders of the developingeconomies, South-East Europe and the CIS in2002 accounted for 97% of all R&D in theseeconomies (table III.1). Reflecting the dynamicsof South, East and South-East Asia, six of thetop ten are from these subregions. In the majorityof these economies, R&D expenditure grew fastduring the period. Double-digit annual growthrates were recorded for China, India and Mexico.R&D expenditures contracted in dollar terms onlyin Brazil.

In today’s world economy, enterprises(private and State-owned) account for the lion’sshare of global R&D. In 1991, they spent $292billion on R&D (annex table A.III.2). Thatamount increased to $376 billion in 1996 and$450 billion in 2002 (figure III.2). In other words,in each of these years enterprises wereresponsible for two-thirds of global R&Dspending; the remaining one-third was accounted

for by governments, higher education institutionsand non-profit private entities.

While the overall share was stable at theglobal level, the share of business enterprises intotal R&D expenditure varied considerably byregion and country (figure III.3). In the Triad– Japan, the United States and the EU – the shareof enterprises was above 60% in 2002. Between1996 and 2002 this share rose in Japan and theEU but not in the United States. In developingAsia, the share of enterprises rose rapidly overthat period, reaching a level similar to that ofthe EU by 2002 (62%). Conversely, the share ofenterprises in Latin America and the Caribbeanwas low and even declined in 1996-2002 (from37% to 33%).9

Reflecting the dominant role of enterpriseR&D in global R&D, the geographical patternsof the former show various similarities with thoseof the latter. R&D in the business sector isconcentrated, just like total R&D. Both in 1996and in 2002, the ten largest spenders on businessR&D accounted for about 90% of the world total,their share marginally increasing over that period(table III.1). The list of the largest business R&Dspenders is identical with that of the largest totalR&D spenders; only the rankings vary. In a slightcontrast to the global picture of total R&D, inbusiness R&D only the spending of France, Italyand Japan declined in dollar terms in 1996-2002.

The share of developing economies, South-East Europe and the CIS in global business R&Dspending is lower than in total R&D spending,reflecting a greater reliance on government R&Din these economies. Their share in the formerreached only 5.4% in 1996 and 7.1% in 2002(figure III.2). The top ten positions in terms ofbusiness R&D among the developing economies,South-East Europe and the CIS differ from thosefor total R&D only because data are not availablefrom India, and the tenth place is thus taken byChile (table III.1). Six of the ten economies arefrom South, East and South-East Asia. Anotherfeature of the list of the largest businessenterprise R&D spenders among the developingcountries is i ts very high geographicalconcentration (the share of the largest ten is 99%of the group total in 2002), reflecting in part alack of data reporting on business R&D in themajority of developing economies.

An output-based assessment of globalinnovation activities confirms the patternsobserved above. Whereas developed countries

107CHAPTER III

Figure III.2. Gross expenditure on R&D (GERD) and business enterpriseR&D (BERD), by country group, 1996 and 2002

(Billions of dollar)

Source: UNCTAD, based on annex table A.III.2.

Table III.2. Developing economies,South-East Europe and CIS:

distribution of R&D, by region(Per cent)

Region 1996 2002

South, East and South-East Asia 63.5 70.1Latin America and the Caribbean 21.1 16.0South-East Europe and CIS 11.2 9.6West Asia 2.0 2.4Africa 2.2 1.9Total developing economies,South-East Europe and CIS 100.0 100.0

Source: UNCTAD, based on annex table A.III.2.

in 2003 still accounted for 83% of all foreignpatent applications to the United States Patentand Trademark Office (USPTO), the share ofdeveloping countries and South-East Europe andthe CIS has risen particularly fast. Between theperiods 1991-1993 and 2001-2003, it jumpedfrom 7% to 17% (annex table A.III.3). The annualaverage number of applications from thesecountries increased from around 5,000 to almost26,000 between the two periods. South, East andSouth-East Asia showed by far the greatestdynamism, followed by South-East Europe andthe CIS. Two economies (Taiwan Province ofChina, Republic of Korea) accounted for four-fifths of the total. They were followed distantlyby India, China, Singapore, Hong Kong (China),the Russian Federation and Brazil. Asia accountsfor more than 95% of the patents granted in the

United States to recipients from developing,economies South-East Europe and the CIS. Theshare of patent applications from Latin Americaand Africa, on the other hand, fell from alreadylow levels between the two periods (see alsosection IV.B.4).

2. R&D by industry

Manufacturing firms have long conductedthe bulk of business sector R&D in developedeconomies. In the United States, for instance,they accounted for 60% of company-funded R&Din 2001, with mining and extraction contributingonly 0.5%, transportation 0.9% and utilities andconstruction 0.3% (United States, NSB 2004).However, the services sector also contributedsignificantly, with trade and other servicestogether contributing 38% (see below). Withinmanufacturing, industries vary greatly in R&Dintensity. For example, the OECD dividesindustries into four groups: high technology;medium-high technology; medium-low technologyand low technology (table III.3).10 The table isbased only on the intensity of R&D; it does notnecessarily depict the nature of the R&Dconducted.11

R&D in services has traditionally beenneglected in the literature, perhaps because ofthe assumption that services do not innovate orare primarily users of innovation inmanufacturing (Howells, 2000; Tether 2004).

GERD

531619

0

100

200

300

400

500

600

700

1996 2002

Developing economies, South-East Europe and CIS

Developed countries

BERD

418356

0

100

200

300

400

500

600

700

1996 2002

Developing economies, South-East Europe and CIS

Developed countries

44

531

57

619 20

356

32

418

108 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

Services do innovate in the broader sense in bothprocesses (organizational change) and products(new services), but much of this innovation doesnot involve formal R&D. Data on this aretherefore scarce, which makes empirical analysisdifficult. This may be changing, however, as aresult of new information and communicationtechnologies (ICTs) and their growing role inservice industries. The telecommunications andcomputer service industries have been investingin R&D for some time, and a new industry is nowemerging that provides R&D services tomanufacturers on a contractual basis (Tether2002).

Data on services R&D are patchy.Published sources cover only a few industrialized

Figure III.3. Share of enterprise R&D in total R&D by country/region, 1996 and 2002(Per cent)

Source: UNCTAD, based on annex table A.III.2.

Table III.3. Classification of manufacturing industries by R&D intensity

Industry category R&D intensity Industries

High technology >5% Aircraft and spacecraft; pharmaceuticals; office, accounting and computing equipment;radio, television and communications equipment; medical, precision and optical instruments

Medium-high 1.5-5% Electrical machinery and apparatus not elsewhere classified; motor vehicles, trailerstechnology and semi-trailers; chemicals excluding pharmaceuticals; railroad equipment and transport

equipment not elsewhere classified; machinery and equipment not elsewhere classifiedMedium-low 0.7-1.5% Coke, refined petroleum products and nuclear fuel; rubber and plastic products; othertechnology non-metallic mineral products; building and repair of ships and boats; basic metals;

fabricated metal products, except machinery and equipmentLow technology <0.7% Manufacturing, not elsewhere classified, and recycling; wood, pulp, paper, paper

products, printing and publishing; food products, beverages and tobacco; textiles,textile products, leather and footwear

Source: United States, NSB 2004, Table 6-1.

Note: R&D intensity is direct R&D expenditures as a percentage of production (gross output).

countries up to 2000. However, they suggest thatservices R&D is rising in most economies, butthat its share in total R&D varies greatly. Severalcountries showed substantial increases in servicesR&D from the early 1980s to the late 1990s; forinstance, the shares of services in company-funded R&D increased by about 5 percentagepoints in France and Italy and 13 percentagepoints in Canada and the United Kingdom(United States, NSB 2004). The United Statesled the industrialized economies in terms ofservices R&D (box III.3). Interestingly, the R&Dintensity of services (R&D as a percentage ofsales) was higher than for manufacturing, thoughit also varied greatly by activity.

0

20

40

60

80

Japan United States European

Union

Developing

Asia

South-East

Europe and

CIS

Latin America

and the

Caribbean

1996 2002

109CHAPTER III

3. Capability needs and benefitsdiffer across activities

The efforts and capabilities required tomaster, adapt and create technologies, and thusto undertake R&D, differ. At the industry level,clothing manufacture is usually less complex inthe range and depth of technical skills orinformation needed than making semiconductors.Within complex industries, technical processesmay differ according to the speed of change andin the effort needed to create new generationsof technology: steel technology today is morestable and less demanding in product innovationthan electronics. Within any industry there canbe differences according to product: in textiles,for instance, yarn spinning, a capital- and scale-intensive activity, requires more advancedtechnical skills than clothing manufacture.Finally, there are differences by function for anygiven product. In clothing, sewing is easier thandesigning new fashion products or managing aninternational supply chain.

There is a similar hierarchy of technicalcomplexity in services, though it may be moredifficult to define than in manufacturing. As notedin box III.2, some services now performconsiderable R&D (indeed, the only output ofcontract research firms is research anddevelopment). Others do not conduct muchformal R&D but innovate in terms of productdevelopment (e.g. new financial services bybanks or new packages by tour operators) andmanagement practices. In broad terms, serviceactivities and functions can be ranked by the levelof skills required – formal (education levels) orinformal (employee training). In export-orientedservices, for instance, the bottom end may includesome call centres while the top end representsadvanced R&D (WIR04).

Different types of R&D also yield differentbenefits in terms of adding value, learning, skillcreation, productivity improvement, marketgrowth and spillovers to other activities (chapterVI). Complex R&D activities generally call for,and so create, more advanced skills andknowledge than simple ones; they also yieldhigher value added. Activities associated withrapid technical progress offer better prospectsfor future productivity increase and enjoy fastergrowth than other activities.12 Within atechnology, advanced functions like design anddevelopment (as compared to basic production)provide higher value added and so higher wages.As innovation moves into higher functions, the

NIS itself grows stronger and permits greaterinnovation in a more diverse range of activities.

The deepening of the industrial structurefrom simple to complex activities, and ofinnovative activities from simple to advancedfunctions, is a natural result of economicdevelopment, but accelerating and facilitatingthe process often requires active policies.13 Thisapplies not only to manufacturing but also toprimary production (with the advent ofbiotechnology and genetic modification inagriculture), infrastructure and services(particularly those IT-based ones that areundergoing rapid offshoring, analysed in WIR04).

The R&D hierarchy for the manufacturingsector depicted above is actually a goodrepresentation of the industrialization process.Most developing economies start modernmanufacturing with the simplest (low R&D)technologies: textiles, clothing, food-processingand wood products. Some move up the scale intoheavy process industries (metals, petroleumrefining) and metal products, providing basicintermediates. A few go on to become efficientusers of “medium-high” technologies, makingmore advanced intermediate and capital goods(chemicals, automobiles, and industrialmachinery). Even fewer develop competitivecapabilities in high-technology industries likeaerospace, micro-electronics or pharmaceuticals.

There is an important exception to thisdepiction, of special interest to this analysis. The“fragmentation” of production (i.e. the relocationof processes or functions across countries byTNCs to take advantage of differences inproduction and communication costs and skills)allows some countries without a strong R&D baseto leapfrog to production in high-technologyindustries l ike electronics (Arndt andKierzkowski 2001, Lall and Zhang 2004).14

While developing countries generally start at thelowest level of technical complexity – finalassembly – it is possible for them to move upthe innovation ladder in electronics, taking onmore demanding functions, handling moreadvanced equipment and making the morecomplex products.15 For such science-basedindustries as biotechnology and some ICT-relatedindustries, there may be limited need to locatethe R&D activity in close proximity toproduction. As noted by one observer (Reddy2000, p. 174): “because of their science base eventheoretically trained personnel, with little or noindustrial experience, can be employed for R&Dfunctions in new technologies.”

110 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

Service enterprises in the United Statessharply increased their R&D spending and theirshare of total industrial R&D after the mid-1980s.Before 1983, service industries accounted for lessthan 5% of total industrial R&D; by 2002, theirshare reached 43%. The total value of R&D byservices was $82 billion compared to $109 billionfor manufacturing in 2002.

The amount of R&D by firms in serviceactivities varied greatly (box table III.3.1). Theleading performers were trade, scientific R&Dservices, software and computer systems design.With a combined R&D of $63 billion, theyaccounted for 77% of R&D by service firms.

The R&D intensity of service firms (R&Das a percentage of sales) is higher than that formanufacturing firms, though it also varies greatlyby activity (box table III.3.2).

However, the classification of firms underservice categories has to be treated with care.Companies are classified under various serviceactivities on the basis of payroll, and theclassification may be misleading as a result. Thisis particularly true of “trade”. Thus, firms with ahigh payroll in sales and marketing are classifiedunder “trade”, and may include manufacturers withhigh marketing payrolls or diversified industrialconglomerates. One example of misclassification(noted by NSF) is that over $1 billion of biotechR&D in 2001 appears to have been performed by

Box III.3. Services sector R&D in the United States

trading companies, when it is likely to have beenperformed by manufacturing companies.

Firms in software and computer systemsdesign and related services jointly spent $21billion on R&D in 2002, raising their share oftotal United States company-funded R&D from4% in 1987 to 12% in 2002.

Scientific R&D services, the leaders in R&Dintensity in 2001, are provided by companies thatperform R&D for other firms on a contractualbasis, mainly in manufacturing. R&D by thesefirms more than doubled during 1997-2001,showing both the rising pace of innovation andthe growing willingness of manufacturers tooutsource R&D previously kept in-house(Jankowski, 2001).

Health-care services are tightly linked tothe high-technology pharmaceutical industry.Firms in these services have traditionally donerelatively little R&D, but there was a sharpincrease in 2002. The financial services andinsurance industry, along with broadcasting andtelecommunications, does very little. However,formal R&D may not be the best way to measureinnovation in these industries, as they areconstantly designing and introducing newproducts and processes.

Box table III.3.1. R&D spending bynon-manufacturing activities in the

United States, 2002(Millions of dollars)

Total non-manufacturing 81 824

Mining, extraction and support activities app. 700Utilities app. 100Construction 164Trade app. 25 000Information 17 870Transportation and warehousing app. 300Newspapers, periodicals, books and databases 614Software 12 927Broadcasting and telecommunications app. 1 600Other information services app. 2 600Finance, insurance and real estate 1 903Architecture, engineering, related services 4 159Computer systems design, related services 11 983Scientific R&D services 13 034Other professional and scientific services 1 182Management of companies and enterprises 148Health-care services app. 4 200Other app. 900

Source: United States, NSF (forthcoming), tables A-2, A-3.Note: Approximate (app.) figures are based onR&D funded by industry; data on federal fundingof R&D are suppressed for confidentiality reasons,so that total R&D spending is also suppressed.

Box table III.3.2. R&D intensity: companyand other (non-federal) R&D funds as % of

net sales in R&D-performing firms

2001 2002All industries 3.8 3.6

Manufacturing 3.6 3.2Non-manufacturing 4.0 4.1Scientific R&D services 36.5 17.6Software 19.3 21.4Computer systems design, related services 16.5 14.3Management of companies 7.8 7.6Trade 6.2 5.0Architectural, engineering, related services 5.2 5.3Health-care services 4.1 15.1Newspapers, periodicals, books, databases 2.7 2.8Transportation and warehousing 2.4 0.5Construction 1.4 0.6Mining, extraction and support 1.3 3.2Finance, insurance and real estate 0.7 0.6Broadcasting and telecommunications 0.5 0.7Information 4.4 4.0

Source: United States, NSF (forthcoming), table A-27.

Source: UNCTAD, based on information provided by NSF.

111CHAPTER III

Some countries (Singapore amongdeveloping countries, Ireland among developedones) have managed such upgrading rapidly;China appears set to follow suit. In other words,provided they have the absorptive capacity andappropriate policies and institutions in place,developing countries can take advantage offragmentation to move up the technology ladder,both across activities and within them. Thefragmentation of functions is proceeding evenmore rapidly in some services, as communicationcosts fall dramatically due to new informationand communications technologies (WIR04) .However, taking advantage of the potential offragmentation requires countries to createknowledge and build local capabilities. As shownin the next section, the gap between theinnovative capabilities of countries is very wide.

C. The innovationcapability gap

1. Measuring innovationcapabilities

In order for countries to connect withglobal networks of knowledge creation as wellas to attract and benefit from R&D by TNCs, acertain basic level of innovative capabilities isneeded. However, countries vary greatly in thisrespect, and in many cases the gaps betweencountries have been growing over time. In orderto il lustrate the current situation, WIR05introduces a new measure of national innovationcapabilities: the UNCTAD Innovation CapabilityIndex (UNICI). The UNICI measures two criticaldimensions: (i) innovative activity (theTechnological Activity Index) and (ii) the skillsavailability for such activity (the Human CapitalIndex). As it is not possible to measure nationaltechnological activity or skills directly, theindices use proxies. Since the data available evenfor the proxies are not complete (caveats arenoted below) the indices should be interpretedwith caution and seen mainly as broad indicators(box III.4).16

National innovative activity can bemeasured by its inputs or outputs. On the “input”side, the usual measures are R&D expendituresand/or employment. R&D is a narrow measureof innovation effort in that it does not captureinformal technological effort; at the same timeit is rather broad in that it includes defence and

basic research that may not be relevant to thetypes of company R&D important for the presentanalysis.17 Still, R&D data are the only onesavailable on a comparable basis across countries,and they provide an indicator of technical effortin complex activities (where the absorption oftechnologies requires formal R&D). As R&Dexpenditure data are more limited than R&Dmanpower data for a given year, only the latterappear in the index.

Innovation “outputs” are often proxied bypatents (national or international) and scientificpublications.18 Data on patents taken out in theUnited States are singled out as they indicate thatthe innovation has reached a comparable levelof novelty and is commercially valuable.19

Patents are a better indicator of invention thanof innovation, since they do not capture thecommercial utility of the discovery; scientificpublications are further removed from the market,though they do show the knowledge base onwhich technological activities depend.

The human resource base for technologicalactivity is generally measured by educationalenrolment. Enrolment data do not capturedifferences in the quality and relevance of theeducation; neither do they reflect skilldevelopment by learning on the job or otherforms of employee training. Moreover, theavailable enrolment data are patchy and, in somecountries, out of date. Again, they are the onlydata available for benchmarking skills and theydo indicate differences in the education base onwhich technological capabilities are built.

These measures have to be normalized byeconomic size (say, population) to make themcomparable across countries. However, where theabsolute size of technological effort or skilledresearchers matters (i.e. where there are minimumcritical mass effects), it is also important tocompare total values for economies. This isparticularly relevant for the cross-border locationof R&D (chapter V).

The components and variables of theUNICI are shown in table III .4. The threecomponents of the Technological Activity Indexare weighted equally while those making up theHuman Capital Index are assigned differentweights to capture the greater importance of high-level skills for innovation. The UNICI iscalculated for 117 countries for the years 1995and 2001. The starting year, 1995, was selectedso as to include a large number of economies inSouth East Europe and the CIS.

112 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

The Technological Activity Index is shownin annex table A.III.4, with countries divided intofour roughly equal groups. Its ranks were stablebetween 1995 and 2001 (with a correlationcoefficient of 0.955). However, some countrieschanged ranks significantly. At the lower levelsthe changes generally arose from small shifts inone component, and so are difficult to interpret.At the higher levels they appear to be moreclearly related to changes in technological effort.It should be noted that the Index does not capturethe absolute size of the technological activities

in each country, thus biasing the Index againstcountries like China or India with large ruralpopulations, combined with large values for R&Dspending. To the extent that the internationalizationof R&D is affected by the absolute size oftechnological activity rather than its innovationintensity per capita, it is important to look at thisfactor as well (chapter V).

The Human Capital Index could becalculated for 119 countries.20 The countries aregrouped into three sets (annex table A.III.5). Most

Various attempts have been made tobenchmark national competitiveness andinnovation, separately or together (all analystsaccept innovation to be a vital ingredient ofcompetitiveness).a A recent survey of many of themain indices found that they have several elementsin common (Archibugi and Coco 2005).b All havevariables for innovation inputs (R&D effort,measured by R&D spending or personnel), outputs(patents, nationally or in the United States) andhuman capital (different measures of educationenrolment). Some also use scientific and technicaljournal articles, and some include variables forinfrastructure (power and ICT). UNDP uses theseinfrastructure variables to capture technologydiffusion (power for traditional technology andICT for modern technology). The Rand indexincludes GDP per capita along with the numberof universities and R&D institutions per capita.Some of these variables, like infrastructure, appearto be only remotely related to innovation; others,like GDP per capita, appear too broad to capturedifferences in technological capability.

The index which is probably closest to theUNICI is the Knowledge Index used by the WorldBank (www.worldbank.org/kam). However, whilethe Knowledge Index encompasses 14 dimensionsof knowledge capacities, the UNICI focuses oninnovation capacity, drawing on a smaller set ofvariables. The UNICI weightings (especially withregard to human capital) are also different.

Broader competitiveness indices like theone calculated by the World Economic Forum(published in its annual Global CompetitivenessReport) include subjective perceptions on thequality of innovation institutions, the strengthof intellectual property protection, theaggressiveness of local enterprises in absorbingtechnology and the uniqueness of local productinnovations.c These qualitative variables are notalways reliable, however, as respondents fromdifferent countries may use different standardsto answer the questions.

A merit of the UNICI is that it is basedentirely on quantitative variables, and uses onlythose that are direct measures of technologicalactivity and technical human capital. Thetechnological activity component of the indexuses R&D manpower,d patents taken out in theUnited States and scientific and technicalpublications (all deflated by population). TheHuman Capital Index uses literacy rates as thebroadest indicator of skills, secondary enrolmentsas an indicator of workforce skills and tertiaryenrolments as an indicator of high level skills.The components of the Technology Activity Indexare not weighted, but those of the Human CapitalIndex are: higher levels of education are assignedhigher weights because they are considered moreimportant for technical and managerialinnovation.e

Source: UNCTAD.

a See Archibugi and Coco 2004, IMD various years, Lall 2003, United States, NSB 2004, Porter and Stern 2001,UNIDO 2003, UNDP 2001, WEF various years.

b They discuss the UNDP index, their own ArCo index, the index developed by Lall and Albaladejo, 2002 and theRand index (Wagner et al. 2001).

c For a detailed critique see Lall 2001b.d The R&D manpower data were available for a larger number of countries than data for R&D spending.e A simple weighting scheme of 1 for literacy, 2 for secondary enrolment and 3 for tertiary enrolment is used.

Box III.4. Comparing the UNCTAD Innovation Capability Index with other indices

113CHAPTER III

developed and some transition economies are inthe leading group; this group also has fourdeveloping economies: the Republic of Korea,Taiwan Province of China, Argentina andUruguay in that order. As with the TechnologicalActivity Index, the Human Capital Index is stableover time, with a correlation coefficient of 0.973between 1995 and 2001. Again, the absolute sizeof the skills availability is not captured by theindex but is of importance for the internationalallocation of R&D internationalization (chapterV). The technology and skill indices are highlycorrelated (coefficients of 0.910 in 1995 and0.889 in 2001), though technological effort andskill formation do not always go together.

2. The UNCTAD InnovationCapability Index

The UNCTAD Innovation Capability Index(UNICI) consists of the unweighted averages ofthe two indices mentioned above. Countries aredivided into three groups: high, medium and low(table III.5). The high capability group in theUNICI comprises all developed countries(including the new EU members) as well as fourdeveloping and four South-East European andCIS countries (all from Europe). Three of the fourdeveloping economies are from South-East andEast Asia; the fourth (Argentina) is from LatinAmerica. The Asian ones combine strongtechnological and skill performance, whileArgentina is weak in technology but somewhatstronger in skills. The economies in transitionare in the top group mainly because of their skillbase – their technological performance isrelatively weak, with only one (the RussianFederation) in the high innovation group.

Table III.4. Components of the UNCTAD Innovation Capability Index

Indices Components Weights attached

Technological Activity Index R&D personnel per mill ion population All 3 components have equal weightsUnited States patents granted per mill ion populationScientific publications per mill ion population

Human Capital Index Literacy rate as % of population Weight of 1Secondary school enrolment as % age group Weight of 2Tertiary enrolment as % of age group Weight of 3

UNCTAD Innovation Technological Activity Index Both indices have equal weightsCapability Index Human Capital Index

Source: UNCTAD.

The “medium” capability group containsother South-East European and CIS economiesas well as most resource-rich and newlyindustrializing economies (including China andtwo sub-Saharan African economies, South Africaand Mauritius). The “low” capability group hasall the South Asian economies, one from South-East Asia (Indonesia), most sub-Saharan Africaneconomies and the remaining countries of LatinAmerica, West Asia and North Africa. Therankings are in line with received knowledgeabout national capabilities. If some economies(like India) seem misplaced, the explanation liesin the use of total population as the deflator;while this is the correct way to construct theindex, i t can be misleading when minimumcritical mass is important.

The unweighted regional averages for theUNICI are shown in table III.6. The developedcountries are well in the lead, albeit with a slightdecline in the average score. This does not meanthat they are investing less in skills or innovation,but rather, that other countries are spendingrelatively more. The new EU members improvedtheir scores during the period studied,approaching the levels of developed countries.The South-East and East Asia subregions are theclear leaders among developing regions, and theiraverage score combined has improved over time.The West Asia and North African subregions alsoimproved their performance, and overtook LatinAmerica and the Caribbean, which had adeteriorating score between 1995 and 2001. SouthAsia also shows a lower score over time, mainlybecause of weaker technological performance byPakistan and declining human capitalperformance by Sri Lanka. Sub-Saharan Africaimproves its average score marginally but stilllags behind all other regions.

114 World Investment Report 2005: Transnational Corporations and the Internationalization of R&DT

ab

le I

II.5

. T

he

UN

CT

AD

In

no

va

tio

n C

ap

ab

ilit

y I

nd

ex

Hig

hM

ediu

m

Low

199

5

20

01

1

995

2

001

19

95

2

001

1Sw

eden

0.

957

Swed

en

0.97

940

Uzb

ekis

tan

0.60

5Jo

rdan

0.

595

79M

ongo

lia0.

321

Sri L

anka

0.

317

2Fi

nlan

d 0.

947

Finl

and

0.97

741

Hon

g K

ong

(Chi

na)

0.59

3G

eorg

ia0.

593

80Tu

nisi

a0.

302

Bot

swan

a0.

315

3C

anad

a 0.

947

Uni

ted

Stat

es

0.92

742

Cyp

rus

0.58

1C

hile

0.

576

81In

dia

0.28

7A

lger

ia0.

312

4U

nite

d St

ates

0.

946

Den

mar

k 0.

926

43C

hile

0.

581

Cyp

rus

0.56

682

Bol

ivia

0.28

3Vi

et N

am0.

295

5A

ustr

alia

0.94

4N

orw

ay

0.92

344

Slo

vaki

a0.

580

Uzb

ekis

tan

0.56

483

Hon

dura

s0.

279

Indi

a 0.

285

6D

enm

ark

0.93

4A

ustr

alia

0.92

045

Sou

th A

fric

a0.

579

Hon

g K

ong

(Chi

na)

0.56

384

Ecu

ador

0.27

9El

Sal

vado

r 0.

279

7N

orw

ay

0.92

9C

anad

a 0.

907

46A

rmen

ia0.

574

Leba

non

0.55

585

El S

alva

dor

0.27

6Zi

mba

bwe

0.27

88

Uni

ted

King

dom

0.

914

Uni

ted

King

dom

0.9

0647

Cos

ta R

ica

0.55

5R

oman

ia0.

554

86In

done

sia

0.27

6M

oroc

co0.

277

9N

ethe

rland

s 0.

912

Bel

gium

0.89

448

Latv

ia

0.55

4S

outh

Afr

ica

0.54

887

Bot

swan

a0.

264

Indo

nesi

a 0.

261

10B

elgi

um0.

911

Net

herla

nds

0.88

849

Rom

ania

0.55

4B

razi

l0.

529

88N

amib

ia0.

261

Ken

ya0.

260

11Ja

pan

0.90

6Ja

pan

0.88

550

Leba

non

0.53

8A

rmen

ia0.

526

89A

lger

ia0.

257

Syr

ian

Ara

b R

ep.

0.24

612

Fran

ce

0.90

2N

ew Z

eala

nd0.

879

51K

azak

hsta

n0.

521

Kaz

akhs

tan

0.52

590

Om

an0.

234

Om

an0.

232

13G

erm

any

0.88

9S

witz

erla

nd0.

877

52K

uwai

t0.

515

Uru

guay

0.50

691

Par

agua

y0.

233

Dom

inic

an R

epub

lic0.

221

14N

ew Z

eala

nd0.

874

Icel

and

0.87

653

Vene

zuel

a0.

504

Kyr

gyzs

tan

0.50

092

Syr

ian

Ara

b R

ep.

0.22

5N

amib

ia0.

218

15S

witz

erla

nd0.

871

Taiw

an P

OC

0.86

554

Mol

dova

, R

ep.

of0.

497

Thai

land

0.

488

93Vi

et N

am0.

218

Par

agua

y0.

213

16A

ustr

ia0.

852

Fran

ce

0.86

355

Sau

di A

rabi

a0.

496

Sau

di A

rabi

a0.

476

94N

icar

agua

0.21

2N

icar

agua

0.17

917

Taiw

an P

OC

0.85

2A

ustr

ia0.

852

56B

ahra

in0.

485

Egyp

t 0.

474

95K

enya

0.17

3H

ondu

ras

0.17

418

Icel

and

0.83

5G

erm

any

0.85

057

Qat

ar0.

471

Kuw

ait

0.47

396

Gua

tem

ala

0.16

5N

iger

ia0.

157

19Ire

land

0.

829

Kore

a, R

ep. o

f 0.

839

58Ta

jikis

tan

0.45

4C

osta

Ric

a0.

472

97Pa

kist

an

0.16

0Ta

nzan

ia, U

nite

d R

ep. o

f0.

145

20Ko

rea,

Rep

. of

0.82

1Sp

ain

0.81

959

Mex

ico

0.45

4M

exic

o0.

469

98Za

mbi

a0.

150

Gha

na0.

143

21Sp

ain

0.81

4Ire

land

0.

814

60Ph

ilipp

ines

0.

452

Mal

aysi

a 0.

467

99N

iger

ia0.

137

Uga

nda

0.14

022

Isra

el0.

808

Isra

el0.

804

61Eg

ypt

0.44

9B

ahra

in0.

466

100

Cam

eroo

n0.

133

Paki

stan

0.

137

23R

ussi

an F

ed.

0.79

7S

love

nia

0.80

162

Per

u0.

448

Vene

zuel

a0.

460

101

Gha

na0.

131

Gua

tem

ala

0.13

524

Italy

0.78

1R

ussi

an F

ed.

0.78

863

Turk

ey

0.43

0P

eru

0.42

510

2C

ôte

d’Iv

oire

0.12

9C

amer

oon

0.13

425

Esto

nia

0.77

4Es

toni

a 0.

775

64B

razi

l0.

421

Phili

ppin

es

0.42

310

3B

enin

0.11

8M

adag

asca

r0.

133

26Be

laru

s 0.

770

Sing

apor

e 0.

748

65Th

aila

nd

0.41

3M

oldo

va,

Rep

. of

0.41

310

4M

alaw

i0.

109

Yem

en0.

130

27S

love

nia

0.76

3Ita

ly 0.

746

66Ja

mai

ca0.

394

Qat

ar0.

403

105

Ban

glad

esh

0.10

9C

ôte

d’Iv

oire

0.12

728

Gre

ece

0.73

3P

ortu

gal

0.74

667

Mal

aysi

a 0.

393

Jam

aica

0.39

510

6S

eneg

al0.

105

Ban

glad

esh

0.12

129

Ukr

aine

0.72

8Li

thua

nia

0.74

268

Mau

ritiu

s0.

390

Col

ombi

a 0.

393

107

Uga

nda

0.08

1Za

mbi

a0.

115

30Si

ngap

ore

0.71

9G

reec

e0.

737

69K

yrgy

zsta

n0.

370

Mon

golia

0.39

110

8Ta

nzan

ia, U

nite

d R

ep. o

f0.

080

Ben

in0.

106

31Po

land

0.

717

Pola

nd

0.73

270

Col

ombi

a 0.

367

Turk

ey

0.39

010

9Ye

men

0.07

9M

alaw

i0.

105

32H

unga

ry

0.70

5H

unga

ry

0.72

571

Dom

inic

an R

ep.

0.35

7B

oliv

ia0.

367

110

Mau

ritan

ia0.

070

Sen

egal

0.10

133

Por

tuga

l0.

704

Ukr

aine

0.70

572

Chi

na

0.35

4Tu

nisi

a0.

365

111

Mad

agas

car

0.06

5M

aurit

ania

0.06

834

Geo

rgia

0.68

3La

tvia

0.

705

73Zi

mba

bwe

0.35

1Ta

jikis

tan

0.36

211

2D

jibou

ti0.

057

Erit

rea

0.05

435

Bul

garia

0.67

1Be

laru

s 0.

697

74Ir

an, I

slam

ic R

ep. o

f0.

349

Chi

na

0.35

811

3H

aiti

0.05

5E

thio

pia

0.05

136

Lith

uani

a 0.

665

Cze

ch R

ep.

0.69

075

Uni

ted

Ara

b E

mira

tes

0.34

6Ir

an, I

slam

ic R

ep. o

f0.

346

114

Erit

rea

0.04

7H

aiti

0.04

637

Cze

ch R

ep.

0.64

8A

rgen

tina

0.68

576

Jord

an

0.33

9U

nite

d A

rab

Em

irate

s0.

326

115

Eth

iopi

a0.

046

Moz

ambi

que

0.03

038

Arg

entin

a0.

640

Bul

garia

0.66

577

Sri L

anka

0.

336

Mau

ritiu

s0.

323

116

Ang

ola

0.02

2D

jibou

ti0.

028

39U

rugu

ay0.

617

Slo

vaki

a0.

626

78M

oroc

co0.

324

Ecu

ador

0.31

911

7M

ozam

biqu

e0.

018

Ang

ola

0.01

9

So

urc

e:

UN

CT

AD

.N

ote

:T

he

co

mb

ine

d i

nd

ex

is a

n u

nw

eig

hte

d a

vera

ge

of

the

Te

chn

olo

gic

al A

ctiv

ity

Ind

ex

an

d t

he

Hu

ma

n C

ap

ita

l In

de

x.

115CHAPTER III

Table III.6. Regional unweightedaverages for the UNCTAD

Innovation Capability Index

Region 1995 2001

Developed countries (excl. thenew EU members) 0.876 0.869The new EU members 0.665 0.707South-East Europe and CIS 0.602 0.584South-East and East Asia 0.492 0.518West Asia and North Africa 0.348 0.361Latin America and the Caribbean 0.375 0.360South Asia 0.223 0.215Sub-Saharan Africa 0.157 0.160

Source: UNCTAD.

Each of these three indices is highlycorrelated with income. In a regression analysis,the log of per capita income “explains” 75% ofthe variation in the Technology Activity Indexin 2001, 66% of the variation in the HumanCapital Index and 74% of the variation in theUNICI. As expected, technological activity, skillsand incomes reinforce each other. The causalconnections between the three are highlycomplex, and there are many possible feedbackloops. For example, more technological activityleads to higher incomes, and higher incomesallow countries to invest more in innovation.However, it can be argued that the main causallink is likely to run from innovative activity and

skills to incomes, and that innovative activityrequires more advanced skills.21

Still, the indices do not rise uniformly withincome levels. As the scatter diagram shows,there is a large variation around the regressionline for the UNCTAD Innovation Capability Index(figure III.4).22 Countries above the line havehigher incomes than predicted by their innovationindex value (i.e. scoring lower on the index thanpredicted by their incomes); those below the linescore higher on the index than predicted by theirincomes. Hong Kong (China) has the lowestcomposite innovation score in relation to its percapita income (presumably earning high incomefrom service activities that do not requiresignificant technological effort), followed bysome small resource-rich economies. At the otherend of the spectrum, various economies intransition have high composite scores relativeto income, a result, as noted above, of theirrelatively strong performance in skill creation.

To sum up, there are large gaps betweencountries in terms of technological activity andhuman capital. The gap is not just between thedeveloped and developing countries, but alsowithin the developing and transition economies.In the developing world, innovative capabilitiesare highly skewed, with South-East and East Asiaat the high end and sub-Saharan Africa at the lowend of the spectrum. Within South-East and East

Figure III.4. Relationship between the UNCTAD Innovation Capability Index andlog per capita GDP, 2001

Source: UNCTAD.

2

3

4

5

6

7

8

9

10

11

12

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Innovation capability index

EthiopiaMalawi

Kenya MongoliaKyrgyzstan

Georgia

UzbekistanUkraine

BelarusLithunia

Djibouti

Guatemala

NamibiaMauritius

Botswana

Bahrain

Kuwait

Hong Kong,China

Cyprus

Italy

Singapore Ireland

Switzerland

Viet Nam

China

India Tajikistan

Bulgaria

RussianFederation

Japan

Sweden

Norway United States

Multiple R: 0.86R Square: 0.74Adjusted R Square: 0.74n= 113

Pe

rca

pita

GD

P(in

log

s)

116 World Investment Report 2005: Transnational Corporations and the Internationalization of R&D

Asia, the three leaders (the Republic of Korea,Taiwan Province of China, Singapore) are wellahead of the other economies. Transitioneconomies have large reservoirs of skills inrelation to their income levels but seem to lagin technological effort.

While the Index suffers from the inevitableproblems of finding the appropriate measures fortechnological effort and human capital, its useof hard statistics provides intuitively plausibleresults:

• Innovative capabilities differ greatly acrosscountries, and the ranks are quite stable overthe period considered. It is proving difficultfor countries at the bottom to improve theirposition over time; there are cumulativeforces at work that seem to reinforce theadvantages of the leaders. It also suggeststhat significant change takes time to achieve.

• However, some countries have improvedtheir ranking. Thus, while developedcountries dominate the “high” group in theUNICI, that group also includes fourdeveloping economies and four economiesin transition.

• The three leading developing economieshave participated vigorously in the globalproduction and innovation system, but eachdid so using different means to accesstechnologies and build domesticcapabilities.23 Each invested heavily ineducation and skills development, sincesustained progress in either strategy requireshighly skilled human capital. Mostfundamentally, in each case access to globaltechnologies and to foreign markets wascritical to sustained growth and upgrading.

• The main strength of the economies intransition, particularly those in Europe, liesin their human capital, rather than intechnological activity, suggesting that thereis scope for using the former to enhance thelatter.

• South Asia and sub-Saharan Africa lagbehind the other regions in innovation and,more particularly, in human capital creation.

What are the implications of theseobservations? The first , of course, is thatinnovative capabilities affect countries’ abilityto develop and raise l iving standards. In aglobalizing world with rapid technical change,strong and growing innovative capabilities are

essential to economic progress. This is as trueof resource-based economies as of others, andit applies as much to services and agriculture asit does to manufacturing. As technologicalprogress proceeds at an accelerating pace, andas the competitive pressure on firms intensifies,the demands made on countries’ capabilities rise.This makes it more important than ever beforeto seek ways to bridge the gaps that exist.

Second, innovative capabilities are directlyrelevant to the location of internationally mobileR&D – the theme of WIR05. TNCs seeking R&Dsites overseas look for adequate supplies ofqualified technical manpower and innovativeactivity (chapter V). This is not to say that theseare the only factors at work in their choices.Attracting global R&D, whether conducted in-house by TNCs or outsourced to local serviceproviders, also needs such conditions as a stableand conducive investment climate, capable localfirms, adequate ICT and other infrastructure, andintellectual property protection. But innovationcapabilities – of the right quality and at the rightcost – are clearly the conditio sine qua non.

Third, innovative capabilities also affectthe scope for host-country benefits frominternationalized R&D (chapter VI). The qualityof R&D that is internationalized depends on localcapabilities. The same applies to the resultingexternalities, in terms of how much local firmsand institutions are able to absorb and learn fromexposure to best practice R&D techniques andskills. Whether or not R&D deepens over time,and how far it spreads over different activities,are almost entirely a function of the strength ofthe local skill and innovation system.

Finally, a word of caution. Nationalinnovative capabilities as measured above canbe misleading where minimum critical massconsiderations apply. While deflatingtechnological effort and skill formation by thesize of the economy is the right way to calculatea capability index, it skews the result againstcountries that have a large pool of employableskilled manpower with diverse skills, even withlow rates of skill creation at the national level.Thus the absolute size of the stock of educatedpeople has to be taken into account whenconsidering the determinants of R&D location.This explains the relatively modest positions inthe UICI rankings of China and India, twosignificant players in the recent increase in R&Dinternationalization by TNCs (chapter IV).

117CHAPTER III

D. Conclusion