yapı kredi 9m15 investor presentation resilient commercial

TRANSCRIPT

November 2015

Resilient commercial performance in a challenging environment

Yapı Kredi 9M15 Investor Presentation

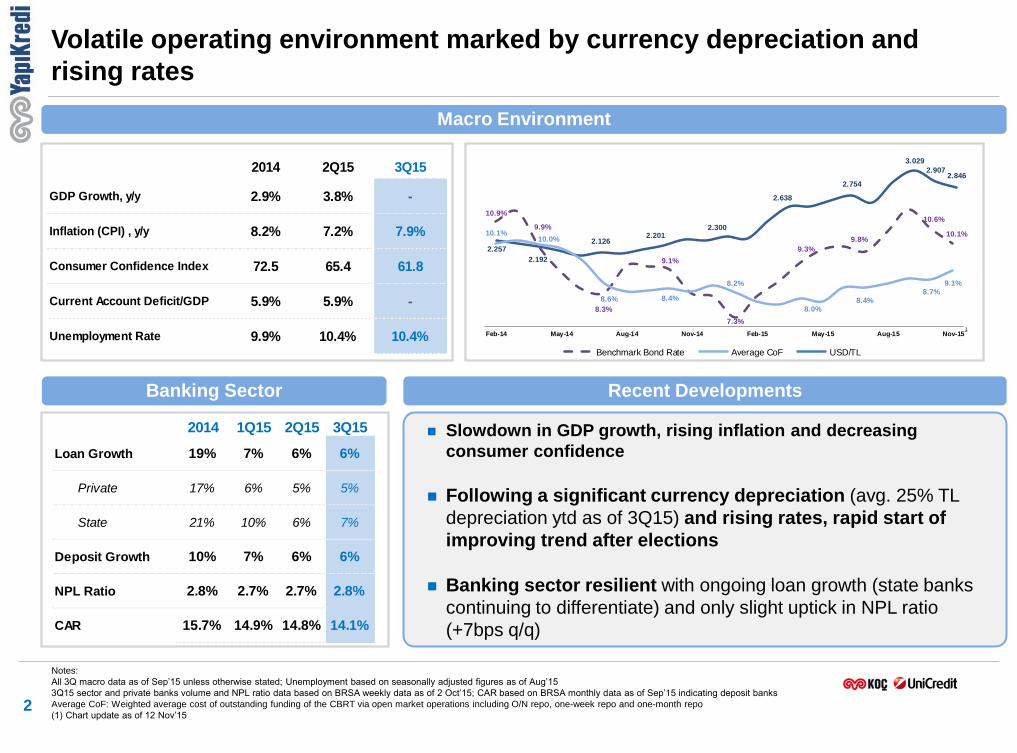

2014 2Q15 3Q15

GDP Growth, y/y 2.9% 3.8% -

Inflation (CPI) , y/y 8.2% 7.2% 7.9%

Consumer Confidence Index 72.5 65.4 61.8

Current Account Deficit/GDP 5.9% 5.9% -

Unemployment Rate 9.9% 10.4% 10.4%

Slowdown in GDP growth, rising inflation and decreasing

consumer confidence

Following a significant currency depreciation (avg. 25% TL

depreciation ytd as of 3Q15) and rising rates, rapid start of

improving trend after elections

Banking sector resilient with ongoing loan growth (state banks

continuing to differentiate) and only slight uptick in NPL ratio

(+7bps q/q)

2

Notes:

All 3Q macro data as of Sep’15 unless otherwise stated; Unemployment based on seasonally adjusted figures as of Aug’15

3Q15 sector and private banks volume and NPL ratio data based on BRSA weekly data as of 2 Oct’15; CAR based on BRSA monthly data as of Sep’15 indicating deposit banks

Average CoF: Weighted average cost of outstanding funding of the CBRT via open market operations including O/N repo, one-week repo and one-month repo

(1) Chart update as of 12 Nov’15

Volatile operating environment marked by currency depreciation and

rising rates

Banking Sector

Macro Environment

Recent Developments

2014 1Q15 2Q15 3Q15

Loan Growth 19% 7% 6% 6%

Private 17% 6% 5% 5%

State 21% 10% 6% 7%

Deposit Growth 10% 7% 6% 6%

NPL Ratio 2.8% 2.7% 2.7% 2.8%

CAR 15.7% 14.9% 14.8% 14.1%

2.257

2.192

2.1262.201

2.300

2.638

2.754

3.029

2.9072.846

10.9%

9.9%

8.3%

9.1%

7.3%

9.3%

9.8%

10.6%

10.1%10.1%10.0%

8.6% 8.4%

8.2%

8.0%8.4%

8.7%

9.1%

Feb-14 May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15

Benchmark Bond Rate Average CoF USD/TL

1

3

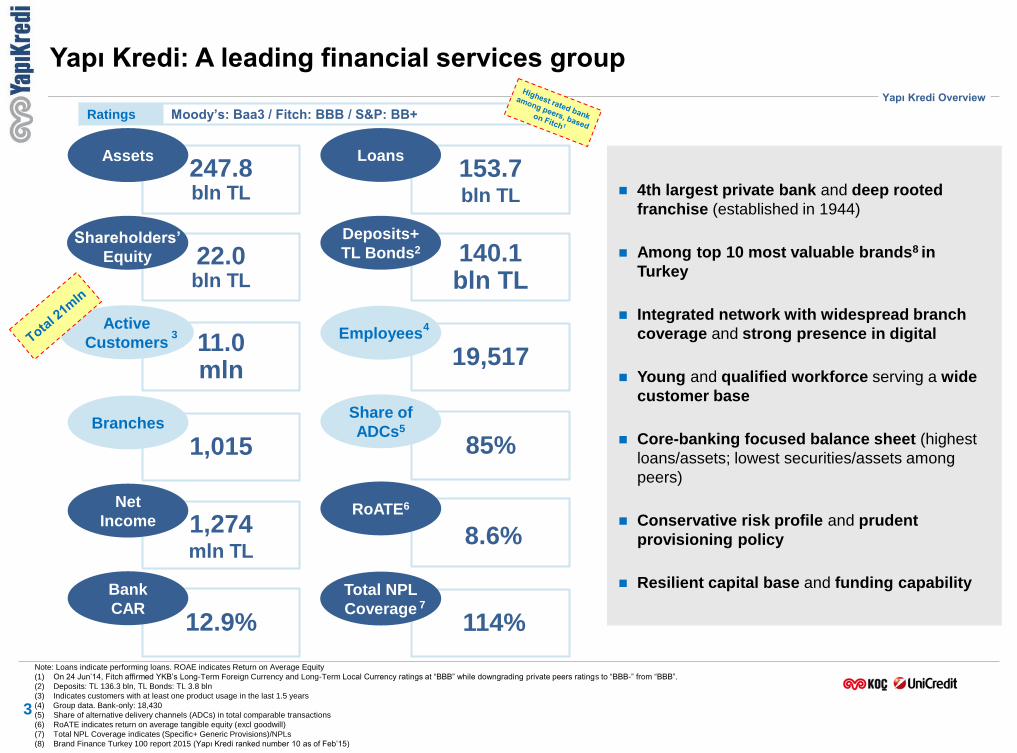

Yapı Kredi: A leading financial services group

247.8 bln TL

Assets 153.7 bln TL

Loans

140.1 bln TL

Deposits+

TL Bonds2

1,274 mln TL

Net

Income

22.0 bln TL

12.9%

Bank

CAR

11.0 mln

Active

Customers

1,015 Branches

85%

Share of

ADCs5

19,517 Employees

RoATE6

114%

Total NPL

Coverage

Ratings Moody’s: Baa3 / Fitch: BBB / S&P: BB+

4th largest private bank and deep rooted

franchise (established in 1944)

Among top 10 most valuable brands8 in

Turkey

Integrated network with widespread branch

coverage and strong presence in digital

Young and qualified workforce serving a wide

customer base

Core-banking focused balance sheet (highest

loans/assets; lowest securities/assets among

peers)

Conservative risk profile and prudent

provisioning policy

Resilient capital base and funding capability

Shareholders’

Equity

Yapı Kredi Overview

8.6%

Note: Loans indicate performing loans. ROAE indicates Return on Average Equity

(1) On 24 Jun’14, Fitch affirmed YKB’s Long-Term Foreign Currency and Long-Term Local Currency ratings at “BBB” while downgrading private peers ratings to “BBB-” from “BBB”.

(2) Deposits: TL 136.3 bln, TL Bonds: TL 3.8 bln

(3) Indicates customers with at least one product usage in the last 1.5 years

(4) Group data. Bank-only: 18,430

(5) Share of alternative delivery channels (ADCs) in total comparable transactions

(6) RoATE indicates return on average tangible equity (excl goodwill)

(7) Total NPL Coverage indicates (Specific+ Generic Provisions)/NPLs

(8) Brand Finance Turkey 100 report 2015 (Yapı Kredi ranked number 10 as of Feb’15)

3 4

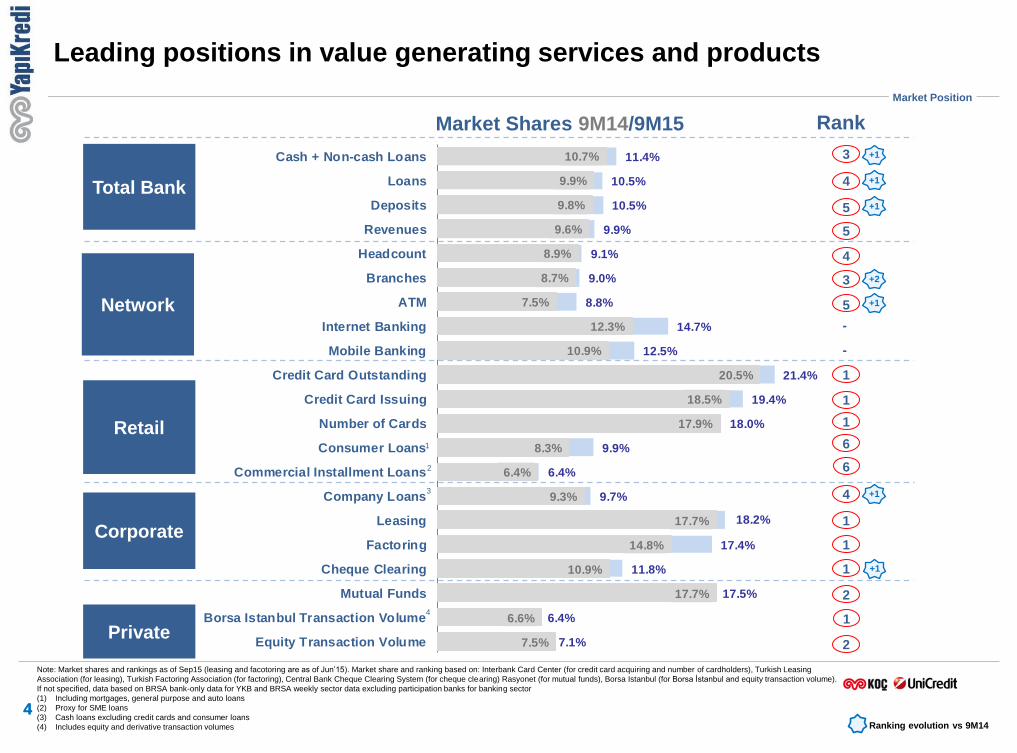

7

11.4%

10.5%

10.5%

9.9%

9.1%

9.0%

8.8%

14.7%

12.5%

21.4%

19.4%

18.0%

9.9%

6.4%

9.7%

18.2%

17.4%

11.8%

17.5%

6.4%

7.1%

Cash + Non-cash Loans

Loans

Deposits

Revenues

Headcount

Branches

ATM

Internet Banking

Mobile Banking

Credit Card Outstanding

Credit Card Issuing

Number of Cards

Consumer Loans

Commercial Installment Loans

Company Loans

Leasing

Factoring

Cheque Clearing

Mutual Funds

Borsa Istanbul Transaction Volume

Equity Transaction Volume

10.7%

9.9%

9.8%

9.6%

8.9%

8.7%

7.5%

12.3%

10.9%

20.5%

18.5%

17.9%

8.3%

6.4%

9.3%

17.7%

14.8%

10.9%

17.7%

6.6%

7.5%

4 4

Note: Market shares and rankings as of Sep15 (leasing and facotoring are as of Jun’15). Market share and ranking based on: Interbank Card Center (for credit card acquiring and number of cardholders), Turkish Leasing

Association (for leasing), Turkish Factoring Association (for factoring), Central Bank Cheque Clearing System (for cheque clearing) Rasyonet (for mutual funds), Borsa Istanbul (for Borsa İstanbul and equity transaction volume).

If not specified, data based on BRSA bank-only data for YKB and BRSA weekly sector data excluding participation banks for banking sector

(1) Including mortgages, general purpose and auto loans

(2) Proxy for SME loans

(3) Cash loans excluding credit cards and consumer loans

(4) Includes equity and derivative transaction volumes

Total Bank

Retail

Private

Corporate

Rank Market Shares

Leading positions in value generating services and products

Market Position

Network

Ranking evolution vs 9M14

2

1

9M14/9M15

4

3

5

4

5 +1

+2

-

-

1

1

1

6

6

1

1

1

2

2

3 +1

4 +1

+1

5

3

+1

+1

1 4

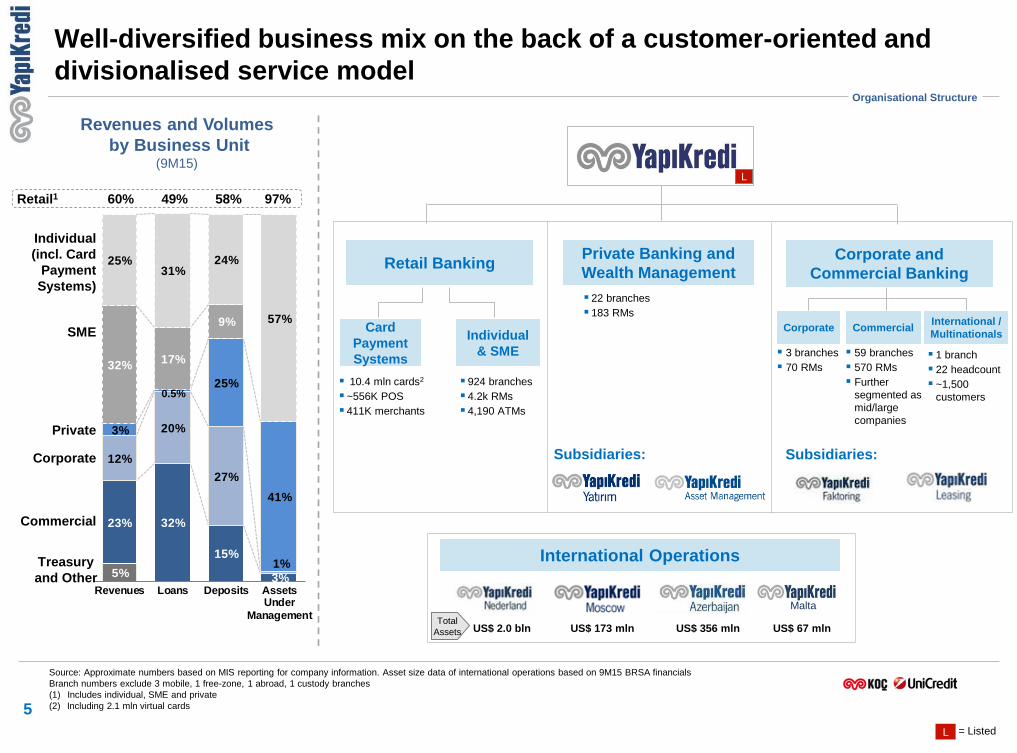

5%

23% 32%

15%

3%

12%

20%

27%

1%

3%

25%

41%

32%17%

9%

25%31%

24%

57%

Revenues Loans Deposits AssetsUnder

Management

Well-diversified business mix on the back of a customer-oriented and

divisionalised service model

5

Revenues and Volumes

by Business Unit

(9M15)

SME

Private

Corporate

Commercial

Treasury

and Other

Individual

(incl. Card

Payment

Systems)

Retail1 60% 49%

Private Banking and

Wealth Management

Subsidiaries:

International Operations

Corporate and

Commercial Banking

Commercial Corporate

Retail Banking

Individual

& SME

Card

Payment

Systems

US$ 356 mln US$ 173 mln US$ 2.0 bln

10.4 mln cards2

~556K POS

411K merchants

924 branches

4.2k RMs

4,190 ATMs

3 branches

70 RMs

59 branches

570 RMs

Further

segmented as

mid/large

companies

22 branches

183 RMs

Total

Assets

International /

Multinationals

Source: Approximate numbers based on MIS reporting for company information. Asset size data of international operations based on 9M15 BRSA financials

Branch numbers exclude 3 mobile, 1 free-zone, 1 abroad, 1 custody branches

(1) Includes individual, SME and private

(2) Including 2.1 mln virtual cards

1 branch

22 headcount

~1,500

customers

58%

Organisational Structure

97%

Subsidiaries:

Malta

US$ 67 mln

L

L = Listed

0.5%

d

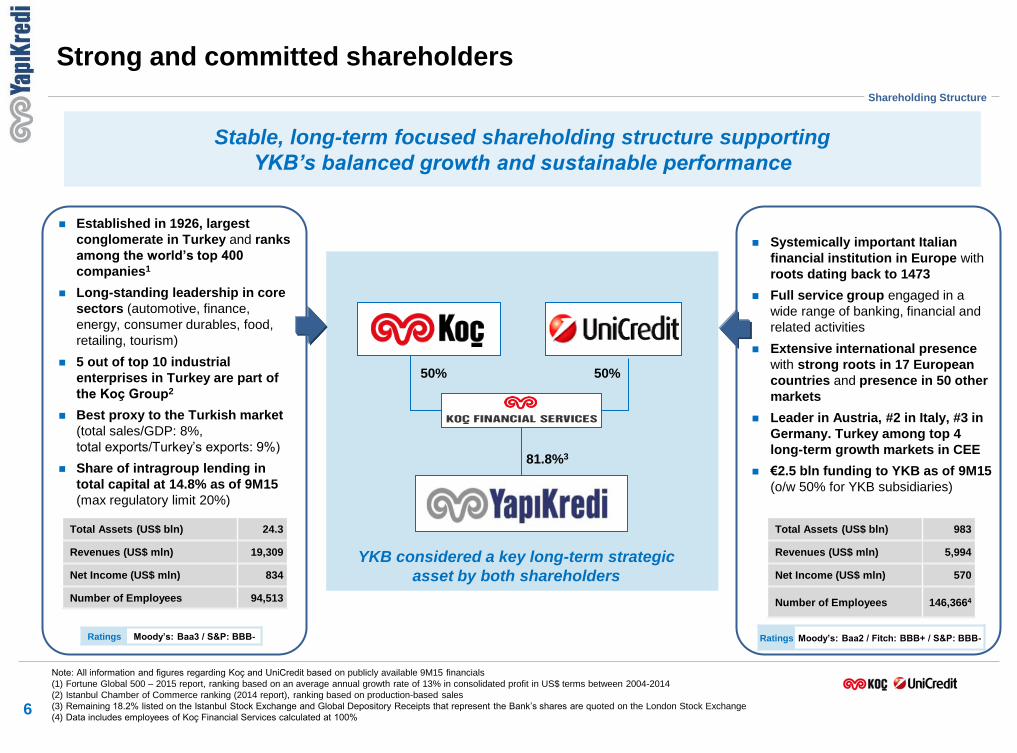

Strong and committed shareholders

50% 50%

81.8%3

Note: All information and figures regarding Koç and UniCredit based on publicly available 9M15 financials

(1) Fortune Global 500 – 2015 report, ranking based on an average annual growth rate of 13% in consolidated profit in US$ terms between 2004-2014

(2) Istanbul Chamber of Commerce ranking (2014 report), ranking based on production-based sales

(3) Remaining 18.2% listed on the Istanbul Stock Exchange and Global Depository Receipts that represent the Bank’s shares are quoted on the London Stock Exchange

(4) Data includes employees of Koç Financial Services calculated at 100% 6

Established in 1926, largest

conglomerate in Turkey and ranks

among the world’s top 400

companies1

Long-standing leadership in core

sectors (automotive, finance,

energy, consumer durables, food,

retailing, tourism)

5 out of top 10 industrial

enterprises in Turkey are part of

the Koç Group2

Best proxy to the Turkish market

(total sales/GDP: 8%,

total exports/Turkey’s exports: 9%)

Share of intragroup lending in

total capital at 14.8% as of 9M15

(max regulatory limit 20%)

Stable, long-term focused shareholding structure supporting

YKB’s balanced growth and sustainable performance

Systemically important Italian

financial institution in Europe with

roots dating back to 1473

Full service group engaged in a

wide range of banking, financial and

related activities

Extensive international presence

with strong roots in 17 European

countries and presence in 50 other

markets

Leader in Austria, #2 in Italy, #3 in

Germany. Turkey among top 4

long-term growth markets in CEE

€2.5 bln funding to YKB as of 9M15

(o/w 50% for YKB subsidiaries)

YKB considered a key long-term strategic

asset by both shareholders

Total Assets (US$ bln) 24.3

Revenues (US$ mln) 19,309

Net Income (US$ mln) 834

Number of Employees 94,513

Shareholding Structure

Ratings Moody’s: Baa3 / S&P: BBB- Ratings Moody’s: Baa2 / Fitch: BBB+ / S&P: BBB-

Total Assets (US$ bln) 983

Revenues (US$ mln) 5,994

Net Income (US$ mln) 570

Number of Employees 146,3664

7

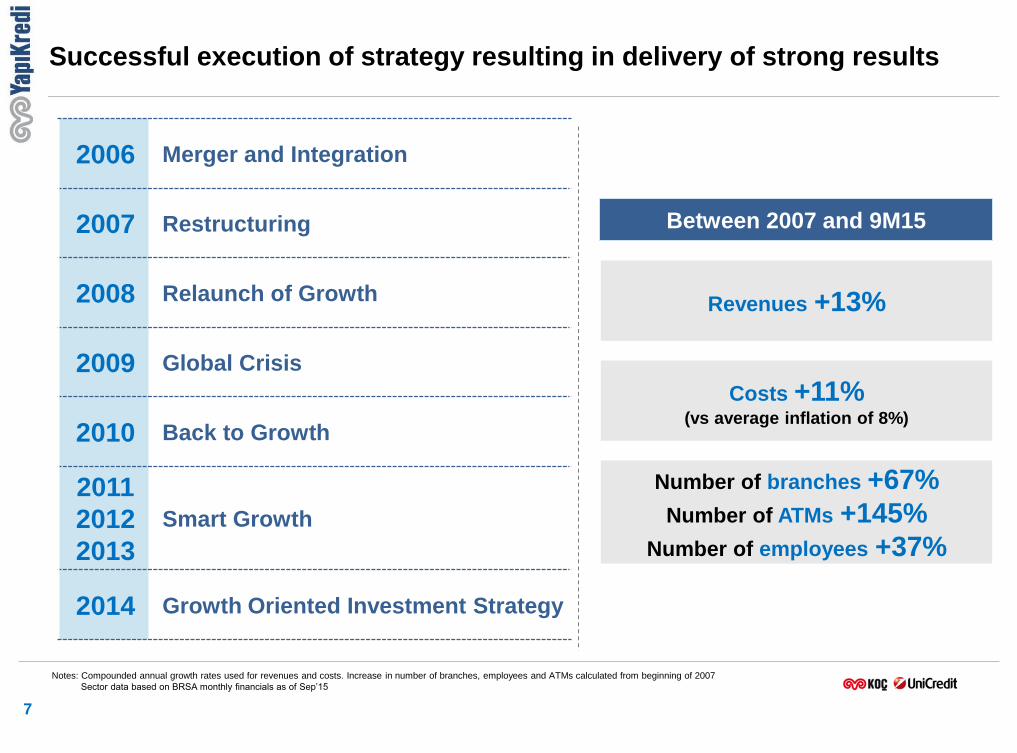

Successful execution of strategy resulting in delivery of strong results

Between 2007 and 9M15

Revenues +13%

Costs +11% (vs average inflation of 8%)

Number of branches +67%

Number of ATMs +145%

Number of employees +37%

Notes: Compounded annual growth rates used for revenues and costs. Increase in number of branches, employees and ATMs calculated from beginning of 2007

Sector data based on BRSA monthly financials as of Sep’15

2006 Merger and Integration

2007 Restructuring

2008 Relaunch of Growth

2009 Global Crisis

2010 Back to Growth

2011

2012

2013

Smart Growth

2014 Growth Oriented Investment Strategy

112%

108%110% 109%109%

109%111%

109%

2014 1Q15 1H15 9M15

11.7%10.6%

11.2%8.6%

9M14 9M15

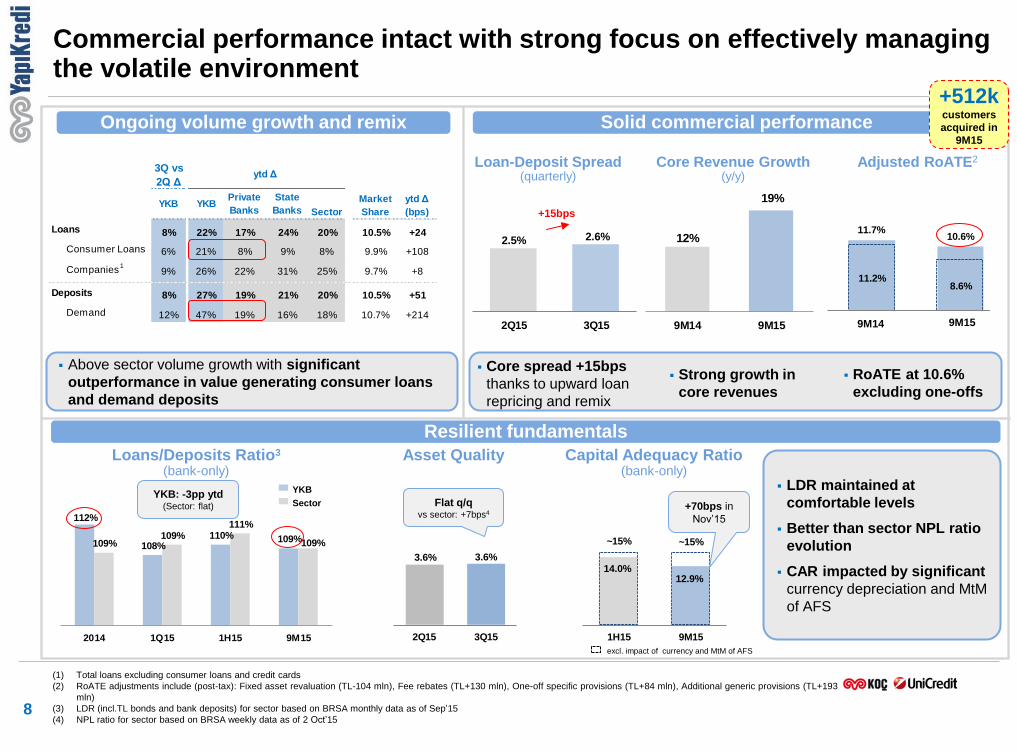

3Q vs

2Q Δ

YKB YKBPrivate

Banks

State

Banks Sector

Loans 8% 22% 17% 24% 20% 10.5% +24

Consumer Loans 6% 21% 8% 9% 8% 9.9% +108

Companies1

9% 26% 22% 31% 25% 9.7% +8

Deposits 8% 27% 19% 21% 20% 10.5% +51

Demand 12% 47% 19% 16% 18% 10.7% +214

Market

Share

ytd Δ

(bps)

ytd Δ

2.5% 2.6%

2Q15 3Q15

3.6% 3.6%

2Q15 3Q15

12%

19%

9M14 9M15

Above sector volume growth with significant

outperformance in value generating consumer loans

and demand deposits

Capital Adequacy Ratio (bank-only)

Loans/Deposits Ratio3

(bank-only)

8

Ongoing volume growth and remix

Resilient fundamentals

Solid commercial performance

Loan-Deposit Spread (quarterly)

Commercial performance intact with strong focus on effectively managing the volatile environment

(1) Total loans excluding consumer loans and credit cards

(2) RoATE adjustments include (post-tax): Fixed asset revaluation (TL-104 mln), Fee rebates (TL+130 mln), One-off specific provisions (TL+84 mln), Additional generic provisions (TL+193

mln)

(3) LDR (incl.TL bonds and bank deposits) for sector based on BRSA monthly data as of Sep’15

(4) NPL ratio for sector based on BRSA weekly data as of 2 Oct’15

Core spread +15bps

thanks to upward loan

repricing and remix

Strong growth in

core revenues

RoATE at 10.6%

excluding one-offs

Core Revenue Growth (y/y)

Adjusted RoATE2

Asset Quality

LDR maintained at

comfortable levels

Better than sector NPL ratio

evolution

CAR impacted by significant

currency depreciation and MtM

of AFS

+15bps

9M14 9M15

Flat q/q vs sector: +7bps4

YKB

Sector

14.0%12.9%

1H15 9M15

~15% ~15%

excl. impact of currency and MtM of AFS

YKB: -3pp ytd (Sector: flat)

+512k customers

acquired in

9M15

+70bps in

Nov’15

Headcount and branch investments finalized; ATM network continues to expand

9

4,217

Market Share +130 bps y/y to 8.8%

2014: +600

9M15: +584

1,015

Market Share +26bps y/y to 9.0%

2014: +60 new (1)

9M15: +12 new(1)

Headcount

19,517

Market Share +23 bps y/y to 9.1%

2014: +1,850

9M15: +983

(1) Net increase

Branches ATMs

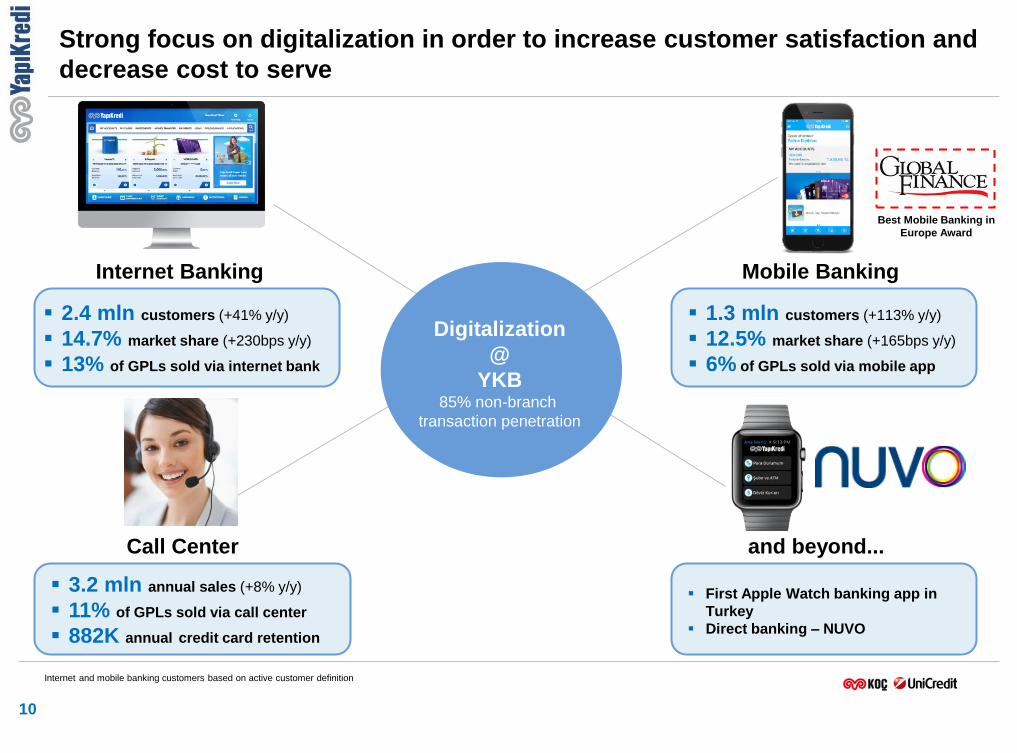

Strong focus on digitalization in order to increase customer satisfaction and

decrease cost to serve

1.3 mln customers (+113% y/y)

12.5% market share (+165bps y/y)

6% of GPLs sold via mobile app

3.2 mln annual sales (+8% y/y)

11% of GPLs sold via call center

882K annual credit card retention

2.4 mln customers (+41% y/y)

14.7% market share (+230bps y/y)

13% of GPLs sold via internet bank

First Apple Watch banking app in

Turkey

Direct banking – NUVO

10

Internet Banking Mobile Banking

Call Center and beyond...

Digitalization

@

YKB 85% non-branch

transaction penetration

Best Mobile Banking in

Europe Award

Internet and mobile banking customers based on active customer definition

38%

32%

29%

1%

54%

46%Corp/

Comm

1Q vs

2014 Δ

2Q vs

1Q Δ

3Q vs

2Q Δ

TL bln9M15 YKB

Private

BanksSector

Total Loans1 153.7 8% 5% 8% 22% 17% 20% 10.5%

TL 97.1 7% 5% 4% 16% 11% 13% 10.4%

FC ($) 18.6 -2% 3% 2% 3% -1% 3% 10.7%

Consumer Loans 28.8 6% 8% 6% 21% 8% 8% 9.9%

Mortgages 12.6 5% 7% 3% 15% 12% 14% 9.7%

General Purpose 15.8 9% 9% 9% 30% 5% 5% 10.1%

Credit Cards 19.4 2% 3% 4% 9% 6% 6% 21.4%

Companies2 105.5 10% 5% 9% 26% 22% 25% 9.7%

TL 48.9 9% 4% 2% 16% 15% 17% 8.8%

FC ($) 18.6 -2% 3% 2% 3% -1% 3% 10.7%

SME3 49.3 10% 15% 9% 37% 17% 16% 13.9%

Comm. Install. 12.0 9% 4% 1% 14% 17% 19% 6.4%

YKB

ytd ΔMarket

Share

11

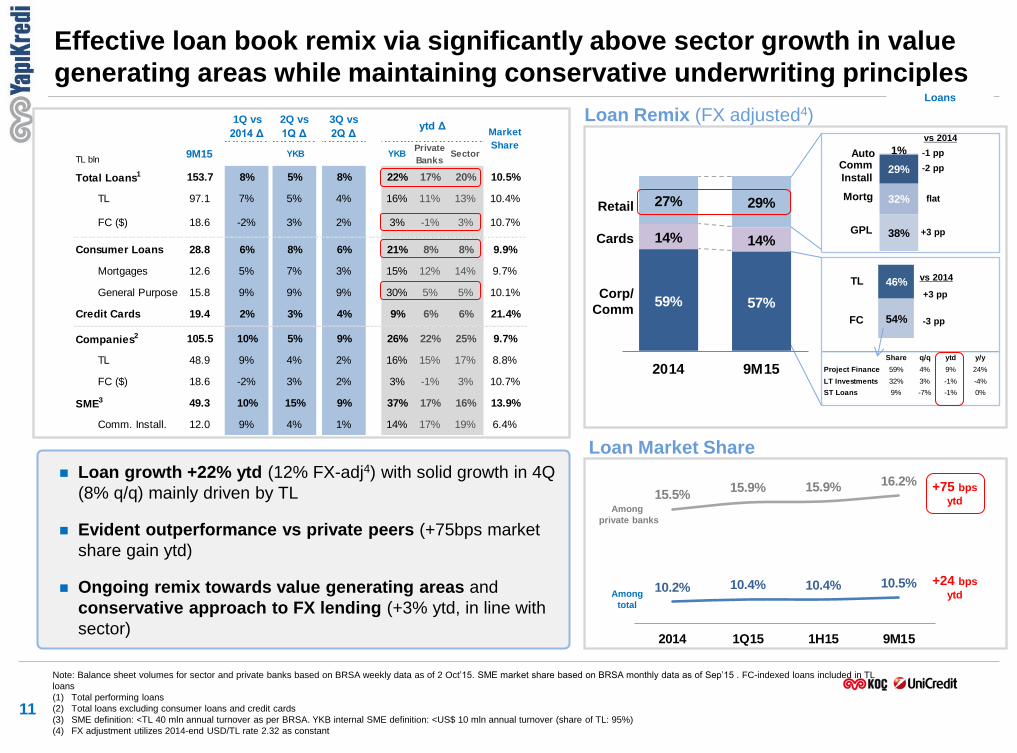

Effective loan book remix via significantly above sector growth in value

generating areas while maintaining conservative underwriting principles

Loan growth +22% ytd (12% FX-adj4) with solid growth in 4Q

(8% q/q) mainly driven by TL

Evident outperformance vs private peers (+75bps market

share gain ytd)

Ongoing remix towards value generating areas and

conservative approach to FX lending (+3% ytd, in line with

sector)

Note: Balance sheet volumes for sector and private banks based on BRSA weekly data as of 2 Oct’15. SME market share based on BRSA monthly data as of Sep’15 . FC-indexed loans included in TL

loans

(1) Total performing loans

(2) Total loans excluding consumer loans and credit cards

(3) SME definition: <TL 40 mln annual turnover as per BRSA. YKB internal SME definition: <US$ 10 mln annual turnover (share of TL: 95%)

(4) FX adjustment utilizes 2014-end USD/TL rate 2.32 as constant

Retail

Cards

Loan Market Share

FC

TL vs 2014

+3 pp

-3 pp

Loan Remix (FX adjusted4)

10.2% 10.4% 10.4% 10.5%

15.5%15.9% 15.9% 16.2%

2014 1Q15 1H15 9M15

Among

total

Among

private banks

+75 bps

ytd

+24 bps

ytd

GPL

Mortg

Comm

Install

Auto

Share q/q ytd y/y

Project Finance 59% 4% 9% 24%

LT Investments 32% 3% -1% -4%

ST Loans 9% -7% -1% 0%

vs 2014

+3 pp

59% 57%

14% 14%

27% 29%

2014 9M15

-2 pp

-1 pp

flat

Loans

9M151Q vs

2014 Δ

2Q vs

1Q Δ

3Q vs

2Q ΔYKB Private Sector

Total Deposits 136.3 11% 5% 8% 27% 19% 20% 10.5%

TL 65.4 2% -3% 4% 4% 0% 5% 9.7%

FC ($) 23.3 10% 11% -1% 21% 11% 10% 11.5%

Customer1 132.4 9% 6% 8% 26% 20% 20% 11.0%

Demand 24.4 14% 15% 12% 47% 19% 18% 10.7%

TL Bonds 3.8 9% 2% 5% 17% -6% -4% 13.4%

Repos 10.6 9% 0% 58% 71% 17% 15% 7.0%

Borrowings 52.8 12% -2% 15% 27% 23% 27%

ytd ΔMarket

Share

9M15 (ytd)

Corp/Comm 21%

TL -26%

FC ($) 32%

Individual 26%

TL 20%

FC ($) 9%

SME 19%

TL 8%

FC ($) 10%

Private 29%

TL 0%

FC ($) 31%

15%16%

17%18%

2014 1Q15 1H15 9M15

12

Deposits

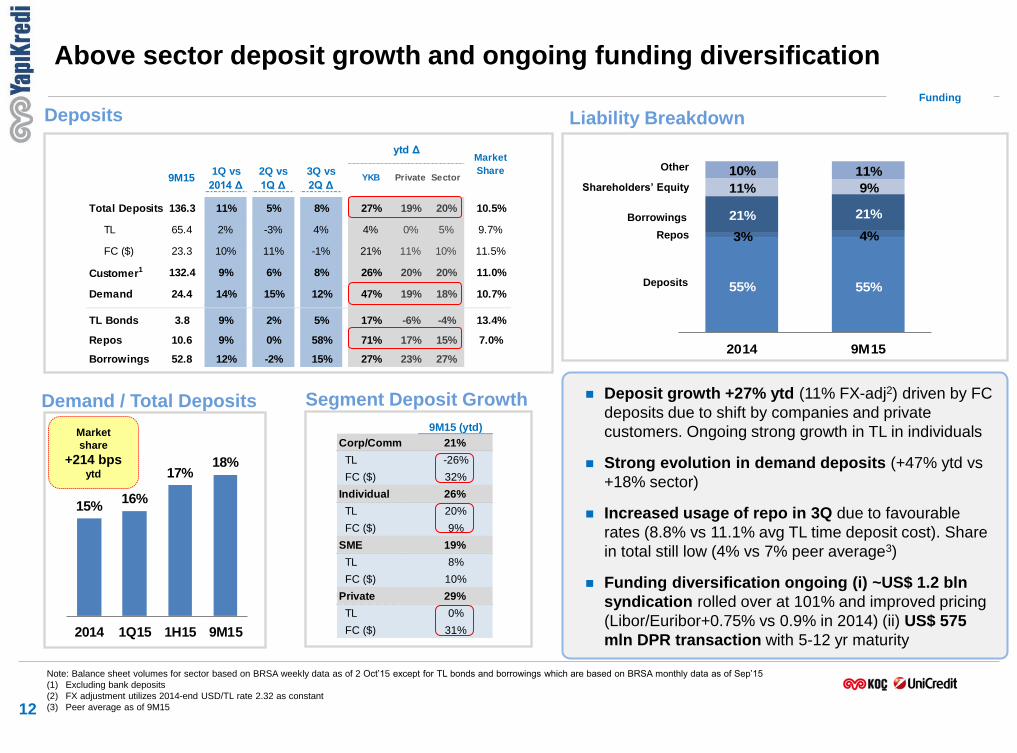

Above sector deposit growth and ongoing funding diversification

Liability Breakdown

Note: Balance sheet volumes for sector based on BRSA weekly data as of 2 Oct’15 except for TL bonds and borrowings which are based on BRSA monthly data as of Sep’15

(1) Excluding bank deposits

(2) FX adjustment utilizes 2014-end USD/TL rate 2.32 as constant

(3) Peer average as of 9M15

Borrowings

Deposits

Other

Repos

Shareholders’ Equity

Deposit growth +27% ytd (11% FX-adj2) driven by FC

deposits due to shift by companies and private

customers. Ongoing strong growth in TL in individuals

Strong evolution in demand deposits (+47% ytd vs

+18% sector)

Increased usage of repo in 3Q due to favourable

rates (8.8% vs 11.1% avg TL time deposit cost). Share

in total still low (4% vs 7% peer average3)

Funding diversification ongoing (i) ~US$ 1.2 bln

syndication rolled over at 101% and improved pricing

(Libor/Euribor+0.75% vs 0.9% in 2014) (ii) US$ 575

mln DPR transaction with 5-12 yr maturity

55% 55%

3% 4%

21% 21%

11% 9%

10% 11%

2014 9M15

Funding

Demand / Total Deposits

Market

share

+214 bps ytd

Segment Deposit Growth

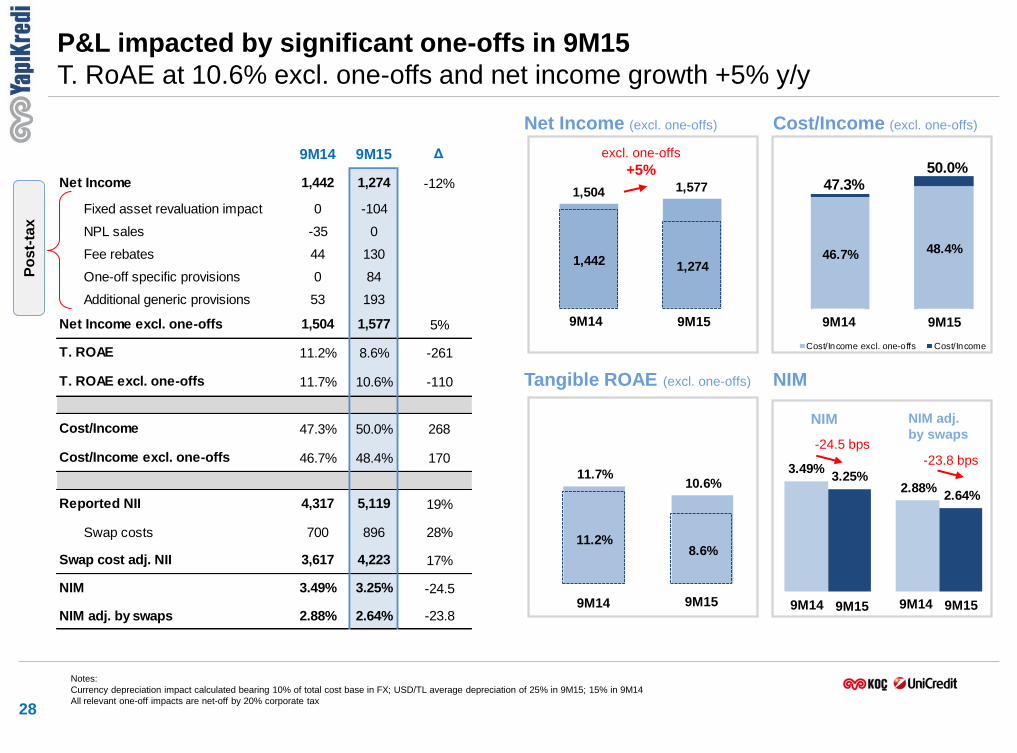

1,504 1,577

1,442 1,274

13

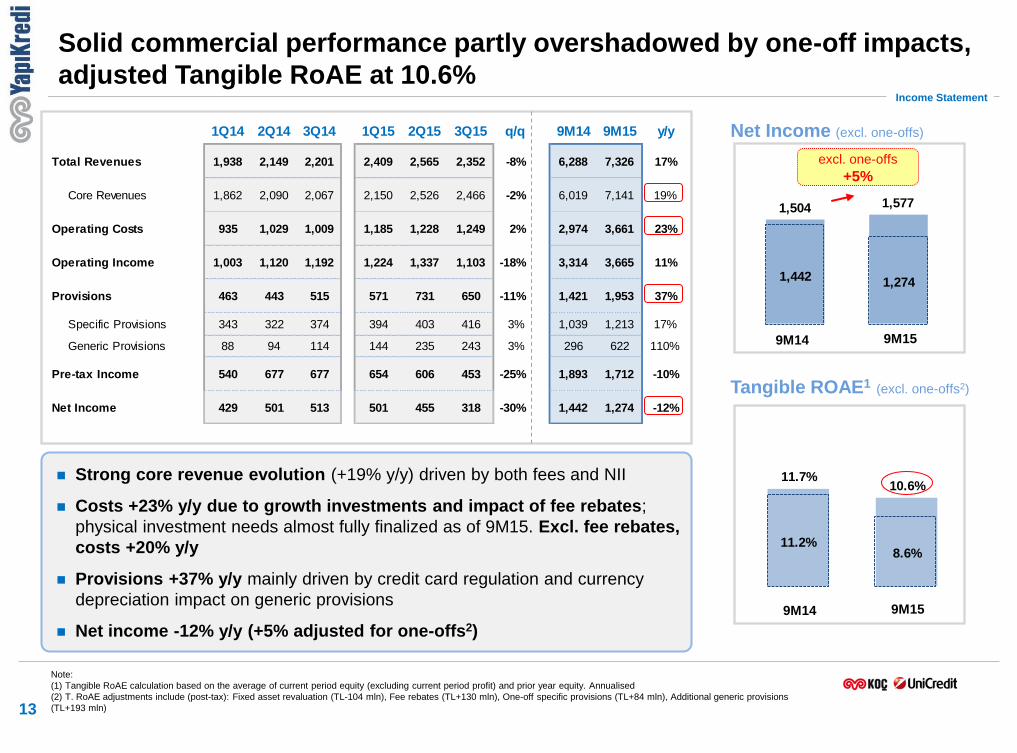

Income Statement

Solid commercial performance partly overshadowed by one-off impacts,

adjusted Tangible RoAE at 10.6%

Note:

(1) Tangible RoAE calculation based on the average of current period equity (excluding current period profit) and prior year equity. Annualised

(2) T. RoAE adjustments include (post-tax): Fixed asset revaluation (TL-104 mln), Fee rebates (TL+130 mln), One-off specific provisions (TL+84 mln), Additional generic provisions

(TL+193 mln)

Strong core revenue evolution (+19% y/y) driven by both fees and NII

Costs +23% y/y due to growth investments and impact of fee rebates;

physical investment needs almost fully finalized as of 9M15. Excl. fee rebates,

costs +20% y/y

Provisions +37% y/y mainly driven by credit card regulation and currency

depreciation impact on generic provisions

Net income -12% y/y (+5% adjusted for one-offs2)

1Q14 2Q14 3Q14 1Q15 2Q15 3Q15 q/q 9M14 9M15 y/y

Total Revenues 1,938 2,149 2,201 2,409 2,565 2,352 -8% 6,288 7,326 17%

Core Revenues 1,862 2,090 2,067 2,150 2,526 2,466 -2% 6,019 7,141 19%

Operating Costs 935 1,029 1,009 1,185 1,228 1,249 2% 2,974 3,661 23%

Operating Income 1,003 1,120 1,192 1,224 1,337 1,103 -18% 3,314 3,665 11%

Provisions 463 443 515 571 731 650 -11% 1,421 1,953 37%

Specific Provisions 343 322 374 394 403 416 3% 1,039 1,213 17%

Generic Provisions 88 94 114 144 235 243 3% 296 622 110%

Pre-tax Income 540 677 677 654 606 453 -25% 1,893 1,712 -10%

Net Income 429 501 513 501 455 318 -30% 1,442 1,274 -12%

Tangible ROAE1 (excl. one-offs2)

Net Income (excl. one-offs)

9M14 9M15

9M14 9M15

excl. one-offs

+5%

11.7%10.6%

11.2%8.6%

16%

18%19%

15%

16%

15%

1Q15 1H15 9M15

9%4% 2%

26%27% 28%

65% 69%

70%

9M13 9M14 9M15

14

6,288

NII

Fees

Other

+6%

+17% 7,326

5,931

Core

Revenues 5,379 6,019 7,141

(1) Core revenues indicate Net Interest Income + Fees & Commissions

(2) Private banks based on BRSA monthly data as of Sep’15

Core revenue evolution above private banks with a growing spread

Revenues (TL mln)

Revenues

Core revenues +19% y/y with significant

outperformance vs private banks (15% y/y)2

Total revenue growth lagging core revenue

growth (17% y/y) due to pressure from swap

costs and lower collections 1

19%

Core

revenues

y/y

Core revenue evolution vs private banks

Private banks YKB

2

10.9%11.1%

11.4%

11.4% 11.4% 11.6%

4.9% 4.7%5.0%

5.4%5.0%

5.5%

3Q14 4Q14 1Q15 2Q15 3Q15

2.6%2.3%

2.5% 2.6%

4Q14 1Q15 2Q15 3Q15

3.6%3.1%

3.6%3.1%

4Q14 1Q15 2Q15 3Q15

7.6%

8.1%8.6%

7.4%

7.8%8.2%

1.7% 1.5% 1.5%

1.7% 1.6% 1.5%

3Q14 4Q14 1Q15 2Q15 3Q15

8.1%

9.1%

7.0%

10.4%

6.4%

5.4% 5.4% 5.6%5.9%

5.7%

3Q14 4Q14 1Q15 2Q15 3Q15

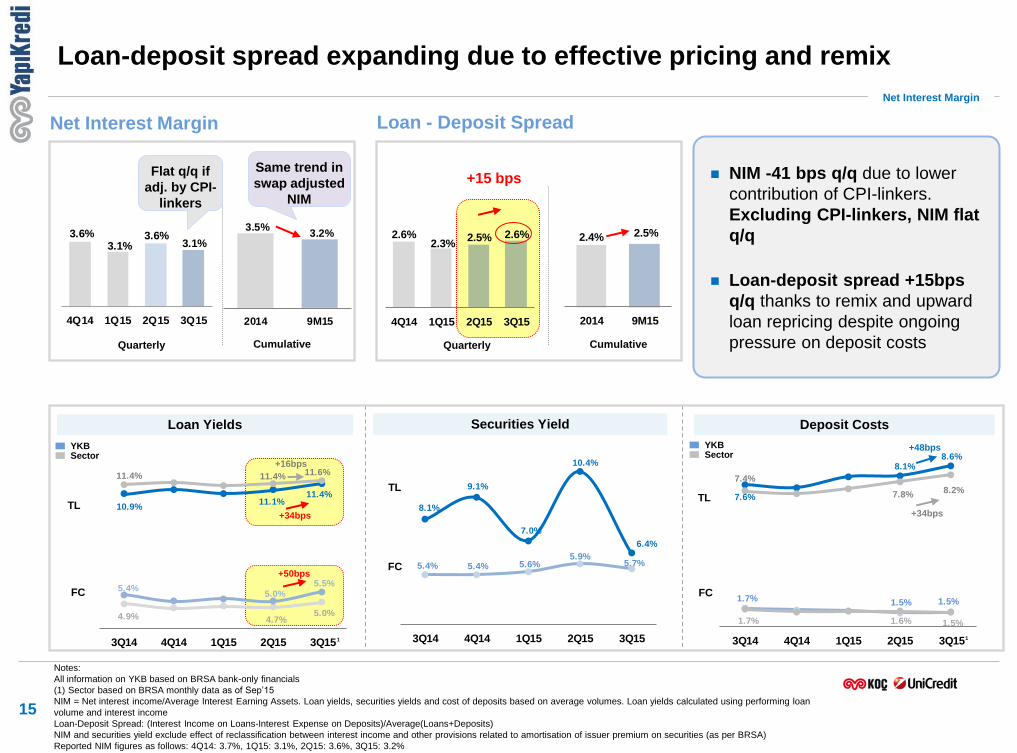

Loan-deposit spread expanding due to effective pricing and remix

15

Net Interest Margin

Notes:

All information on YKB based on BRSA bank-only financials

(1) Sector based on BRSA monthly data as of Sep’15

NIM = Net interest income/Average Interest Earning Assets. Loan yields, securities yields and cost of deposits based on average volumes. Loan yields calculated using performing loan

volume and interest income

Loan-Deposit Spread: (Interest Income on Loans-Interest Expense on Deposits)/Average(Loans+Deposits)

NIM and securities yield exclude effect of reclassification between interest income and other provisions related to amortisation of issuer premium on securities (as per BRSA)

Reported NIM figures as follows: 4Q14: 3.7%, 1Q15: 3.1%, 2Q15: 3.6%, 3Q15: 3.2%

Loan Yields Securities Yield Deposit Costs

Net Interest Margin

YKB Sector

TL

FC

TL

FC

TL

FC

NIM -41 bps q/q due to lower

contribution of CPI-linkers.

Excluding CPI-linkers, NIM flat

q/q

Loan-deposit spread +15bps

q/q thanks to remix and upward

loan repricing despite ongoing

pressure on deposit costs

Loan - Deposit Spread

+15 bps

Quarterly Cumulative Quarterly Cumulative

+16bps

+34bps

+48bps

+34bps

YKB Sector

3.5%3.2%

2014 9M15

2.4% 2.5%

2014 9M15

Same trend in

swap adjusted

NIM

+50bps

Flat q/q if

adj. by CPI-

linkers

1 1

1Q15 2Q15 3Q15 9M14 9M15

Total Other

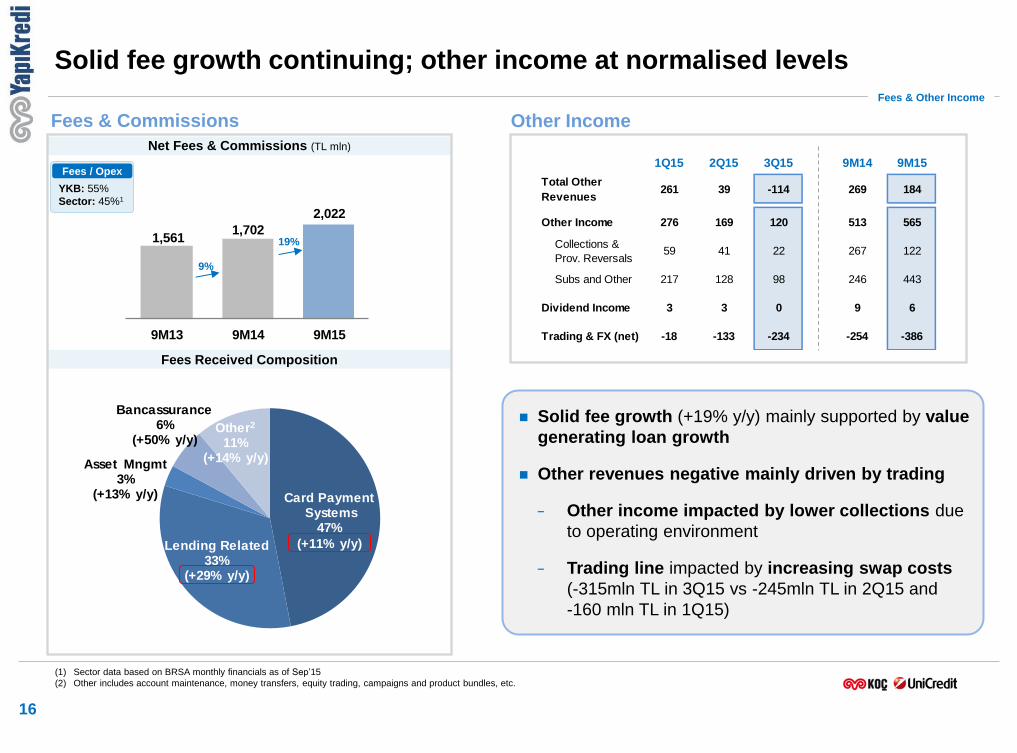

Revenues261 39 -114 269 184

Other Income 276 169 120 513 565

Collections &

Prov. Reversals59 41 22 267 122

Subs and Other 217 128 98 246 443

Dividend Income 3 3 0 9 6

Trading & FX (net) -18 -133 -234 -254 -386

Card PaymentSystems

47%

(+11% y/y)Lending Related 33%

(+29% y/y)

Asset Mngmt 3%

(+13% y/y)

Bancassurance 6%

(+50% y/y)Other2

11%(+14% y/y)

1,5611,702

2,022

9M13 9M14 9M15

Solid fee growth continuing; other income at normalised levels

16

Fees & Commissions

Fees Received Composition

Net Fees & Commissions (TL mln)

Other Income

Fees & Other Income

(1) Sector data based on BRSA monthly financials as of Sep’15

(2) Other includes account maintenance, money transfers, equity trading, campaigns and product bundles, etc.

Solid fee growth (+19% y/y) mainly supported by value

generating loan growth

Other revenues negative mainly driven by trading

− Other income impacted by lower collections due

to operating environment

− Trading line impacted by increasing swap costs

(-315mln TL in 3Q15 vs -245mln TL in 2Q15 and

-160 mln TL in 1Q15)

9%

19%

YKB: 55%

Sector: 45%1

Fees / Opex

17

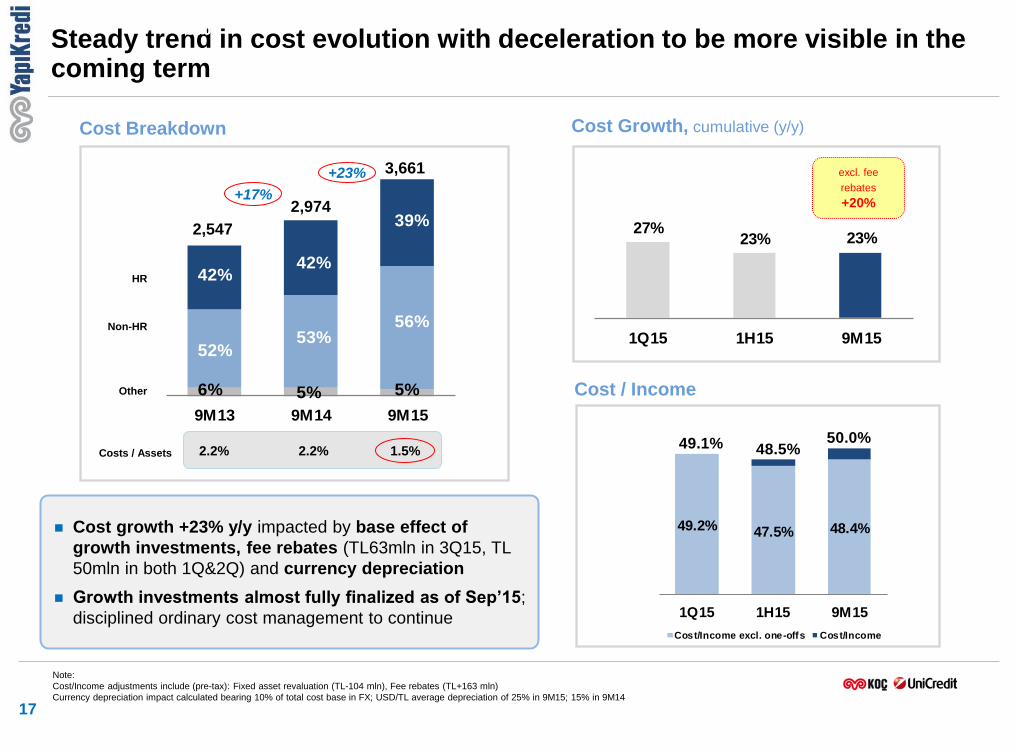

Cost Breakdown

Steady trend in cost evolution with deceleration to be more visible in the coming term

9M13 9M14 9M15

39%

39%

56%53%

56%

42%

56%

52%

56%

42%

6% 5% 5%

2,974 +17%

+23% 3,661

2,547

HR

Non-HR

Other

Cost growth +23% y/y impacted by base effect of

growth investments, fee rebates (TL63mln in 3Q15, TL

50mln in both 1Q&2Q) and currency depreciation

Growth investments almost fully finalized as of Sep’15;

disciplined ordinary cost management to continue

Cost Growth, cumulative (y/y)

Costs / Assets 2.2% 2.2% 1.5%

27%23% 23%

1Q15 1H15 9M15

Cost / Income

Note:

Cost/Income adjustments include (pre-tax): Fixed asset revaluation (TL-104 mln), Fee rebates (TL+163 mln)

Currency depreciation impact calculated bearing 10% of total cost base in FX; USD/TL average depreciation of 25% in 9M15; 15% in 9M14

49.2% 47.5% 48.4%

1Q15 1H15 9M15

Cost/Income excl. one-offs Cost/Income

49.1% 50.0%48.5%

excl. fee

rebates

+20%

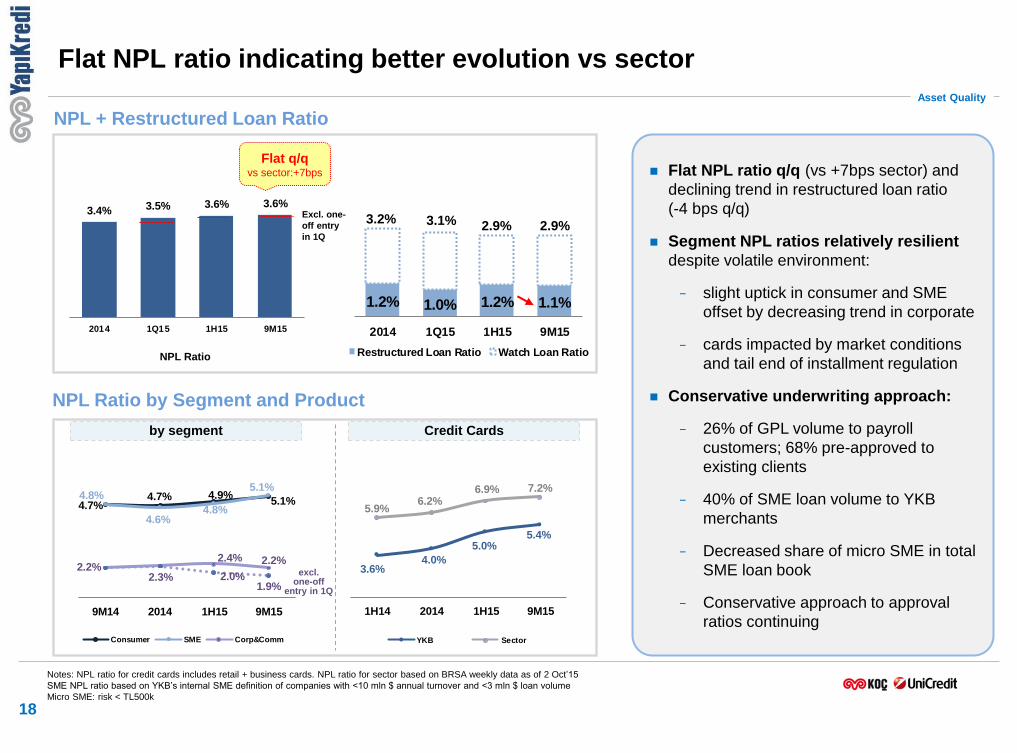

1.2% 1.0% 1.2% 1.1%

2014 1Q15 1H15 9M15

Restructured Loan Ratio Watch Loan Ratio

3.4% 3.5% 3.6% 3.6%

2014 1Q15 1H15 9M15

18

Flat NPL ratio indicating better evolution vs sector

NPL Ratio by Segment and Product

Asset Quality

Notes: NPL ratio for credit cards includes retail + business cards. NPL ratio for sector based on BRSA weekly data as of 2 Oct’15

SME NPL ratio based on YKB’s internal SME definition of companies with <10 mln $ annual turnover and <3 mln $ loan volume

Micro SME: risk < TL500k

by segment Credit Cards

Flat NPL ratio q/q (vs +7bps sector) and

declining trend in restructured loan ratio

(-4 bps q/q)

Segment NPL ratios relatively resilient

despite volatile environment:

− slight uptick in consumer and SME

offset by decreasing trend in corporate

− cards impacted by market conditions

and tail end of installment regulation

Conservative underwriting approach:

− 26% of GPL volume to payroll

customers; 68% pre-approved to

existing clients

− 40% of SME loan volume to YKB

merchants

− Decreased share of micro SME in total

SME loan book

− Conservative approach to approval

ratios continuing

4.7%4.7% 4.9%

5.1%4.8%

4.6%4.8%

5.1%

2.2%2.3%

2.4% 2.2%

2.0%1.9%

9M14 2014 1H15 9M15

Consumer SME Corp&Comm

3.6%4.0%

5.0%5.4%

5.9%6.2%

6.9% 7.2%

1H14 2014 1H15 9M15

YKB Sector

excl. one-off

entry in 1Q

NPL + Restructured Loan Ratio

NPL Ratio

3.2% 3.1% 2.9% Excl. one-

off entry

in 1Q 2.9%

Flat q/q vs sector:+7bps

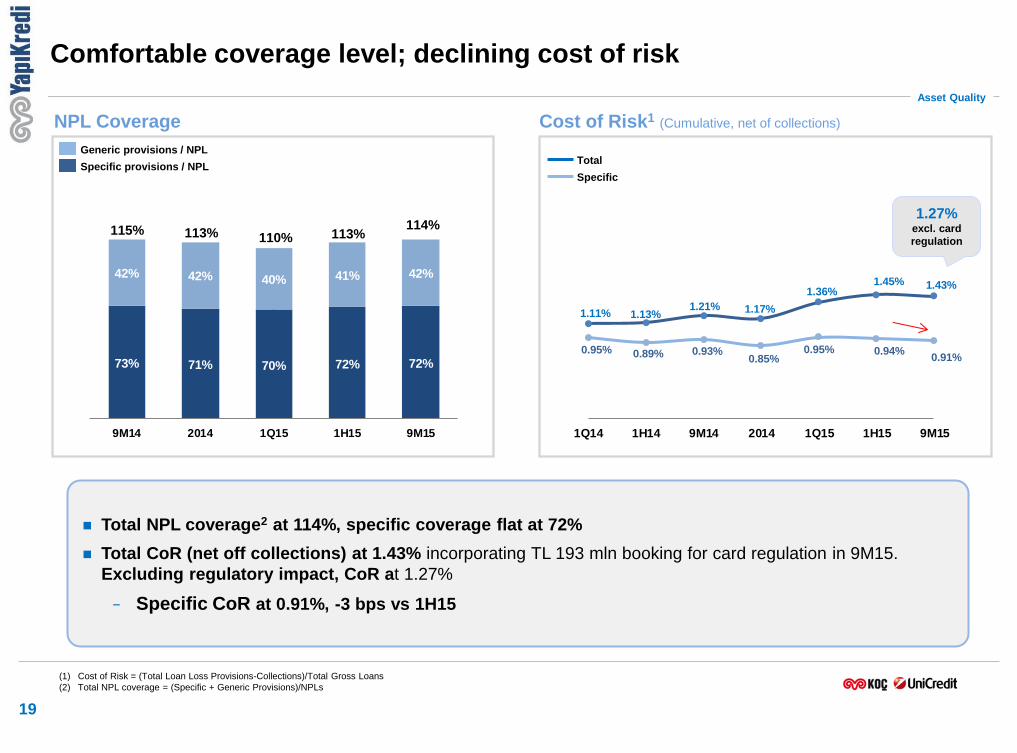

1.11% 1.13%1.21% 1.17%

1.36%1.45% 1.43%

0.95% 0.89% 0.93%0.85%

0.95% 0.94%0.91%

1Q14 1H14 9M14 2014 1Q15 1H15 9M15

42% 42% 40% 41% 42%

73% 71% 70% 72% 72%

9M14 2014 1Q15 1H15 9M15

Comfortable coverage level; declining cost of risk

19

NPL Coverage

Specific provisions / NPL

Generic provisions / NPL

Cost of Risk1 (Cumulative, net of collections)

Total

(1) Cost of Risk = (Total Loan Loss Provisions-Collections)/Total Gross Loans

(2) Total NPL coverage = (Specific + Generic Provisions)/NPLs

Asset Quality

Specific

115% 113%

Total NPL coverage2 at 114%, specific coverage flat at 72%

Total CoR (net off collections) at 1.43% incorporating TL 193 mln booking for card regulation in 9M15.

Excluding regulatory impact, CoR at 1.27%

− Specific CoR at 0.91%, -3 bps vs 1H15

110% 113%

1.27% excl. card

regulation

114%

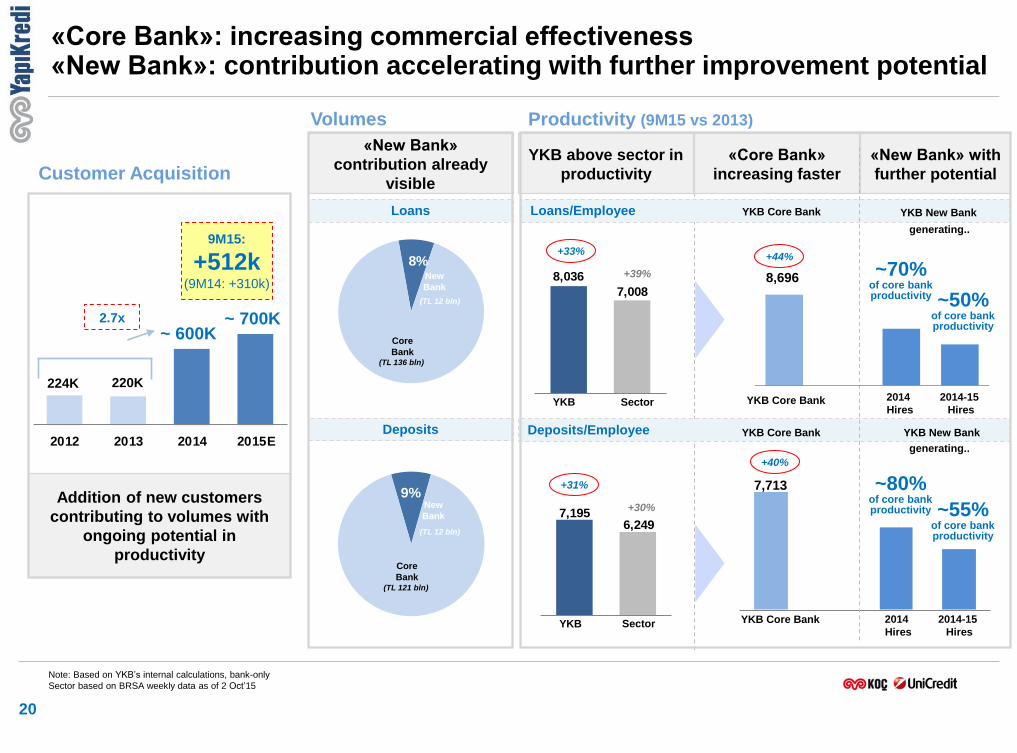

9%

8%

7,1956,249

8,036

7,008

2012 2013 2014 2015E

Loans/Employee

20

Customer Acquisition

«Core Bank»: increasing commercial effectiveness «New Bank»: contribution accelerating with further improvement potential

Volumes

Note: Based on YKB’s internal calculations, bank-only

Sector based on BRSA weekly data as of 2 Oct’15

220K

~ 600K

Addition of new customers

contributing to volumes with

ongoing potential in

productivity

224K

2.7x

«New Bank»

contribution already

visible

Core

Bank

Loans

Deposits

Productivity (9M15 vs 2013)

YKB Sector

YKB Sector

+39%

YKB Core Bank

+30%

YKB Core Bank

«Core Bank»

increasing faster

«New Bank» with

further potential

YKB above sector in

productivity

Deposits/Employee

New

Bank

New

Bank

+33%

(TL 12 bln)

(TL 12 bln)

(TL 136 bln)

Core

Bank (TL 121 bln)

+44%

YKB New Bank

+31%

~ 700K

YKB Core Bank YKB New Bank

9M15:

+512k (9M14: +310k)

~70% of core bank productivity ~50%

of core bank productivity

2014

Hires

2014-15

Hires YKB Core Bank

~80% of core bank productivity ~55%

of core bank productivity

+40%

2014

Hires

2014-15

Hires

generating..

generating..

8,696

7,713

10.5%9.4%

1H15 9M15

~11% ~11%

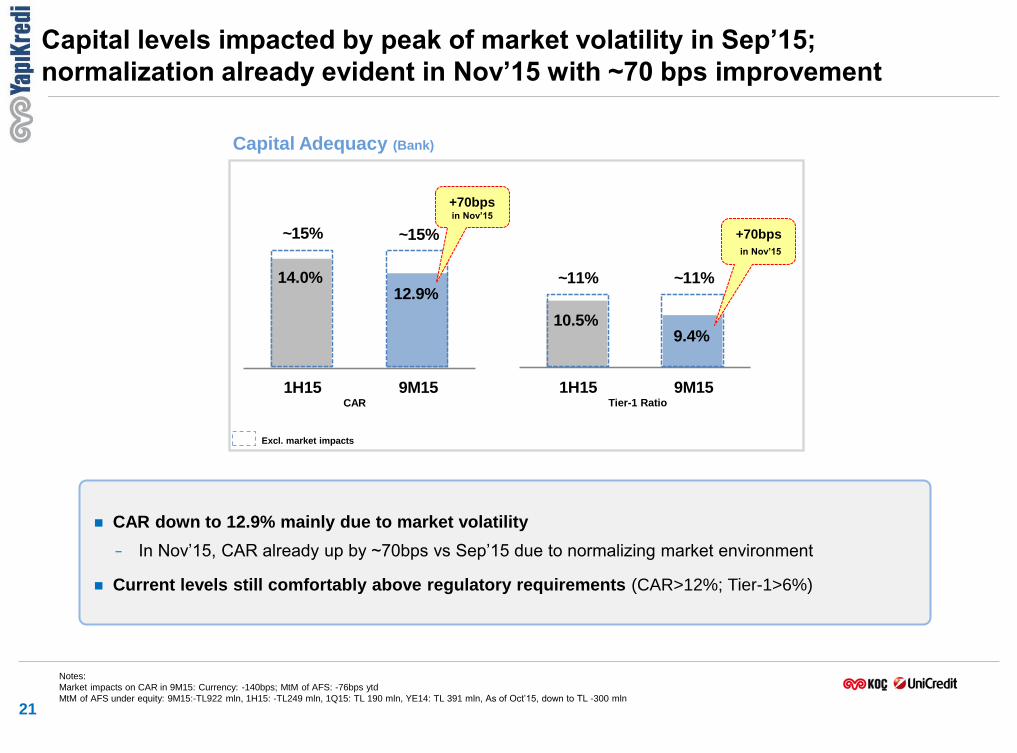

21

Capital Adequacy (Bank)

CAR down to 12.9% mainly due to market volatility

− In Nov’15, CAR already up by ~70bps vs Sep’15 due to normalizing market environment

Current levels still comfortably above regulatory requirements (CAR>12%; Tier-1>6%)

Capital levels impacted by peak of market volatility in Sep’15;

normalization already evident in Nov’15 with ~70 bps improvement

Notes:

Market impacts on CAR in 9M15: Currency: -140bps; MtM of AFS: -76bps ytd

MtM of AFS under equity: 9M15:-TL922 mln, 1H15: -TL249 mln, 1Q15: TL 190 mln, YE14: TL 391 mln, As of Oct’15, down to TL -300 mln

14.0%12.9%

1H15 9M15

~15% ~15% +70bps

in Nov’15

+70bps in Nov’15

CAR Tier-1 Ratio

Excl. market impacts

22

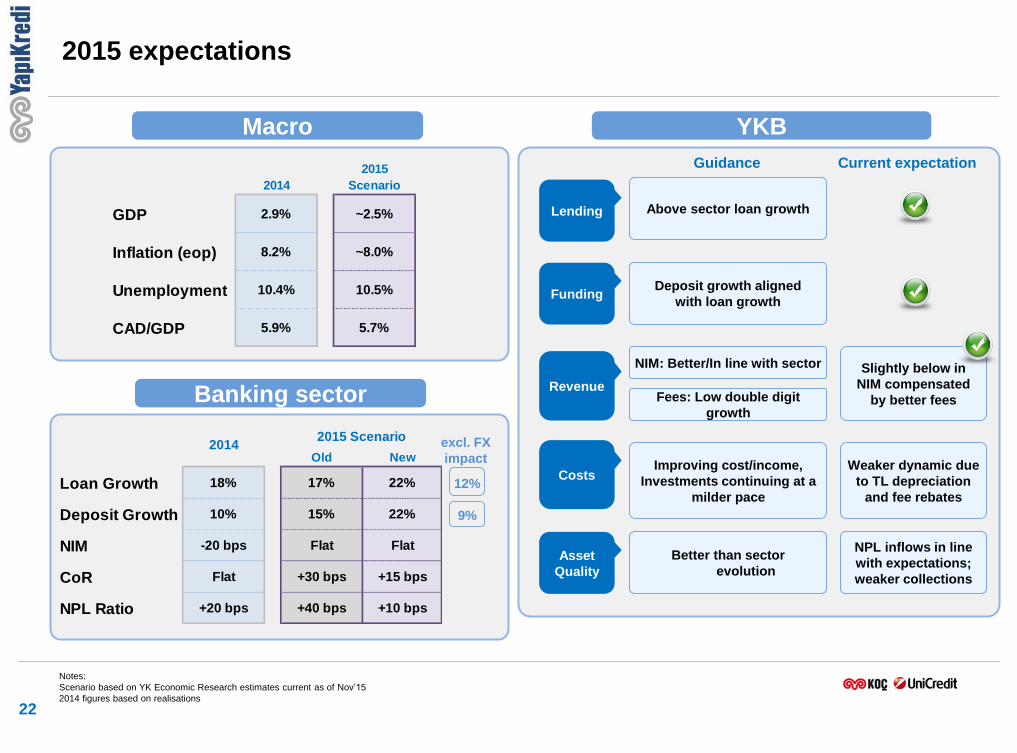

2015 expectations

Notes:

Scenario based on YK Economic Research estimates current as of Nov’15

2014 figures based on realisations

2014

2015

Scenario

GDP 2.9% ~2.5%

Inflation (eop) 8.2% ~8.0%

Unemployment 10.4% 10.5%

CAD/GDP 5.9% 5.7%

Old New

Loan Growth 18% 17% 22%

Deposit Growth 10% 15% 22%

NIM -20 bps Flat Flat

CoR Flat +30 bps +15 bps

NPL Ratio +20 bps +40 bps +10 bps

2015 Scenario2014

Macro

Banking sector

Lending

Funding

Revenue

Costs

Asset

Quality

Deposit growth aligned

with loan growth

NIM: Better/In line with sector

Better than sector

evolution

Guidance

Fees: Low double digit

growth

Improving cost/income,

Investments continuing at a

milder pace

YKB

Current expectation

Above sector loan growth

Slightly below in

NIM compensated

by better fees

Weaker dynamic due

to TL depreciation

and fee rebates

NPL inflows in line

with expectations;

weaker collections

excl. FX

impact

12%

9%

23

Annex

Agenda

Borrowings 21%

Repos 4%

Deposits 55%

Other 11%

Shareholders' Equity

9%

Loans 62%

Securities 13%

Other IEAs 20%

Other Assets

5%

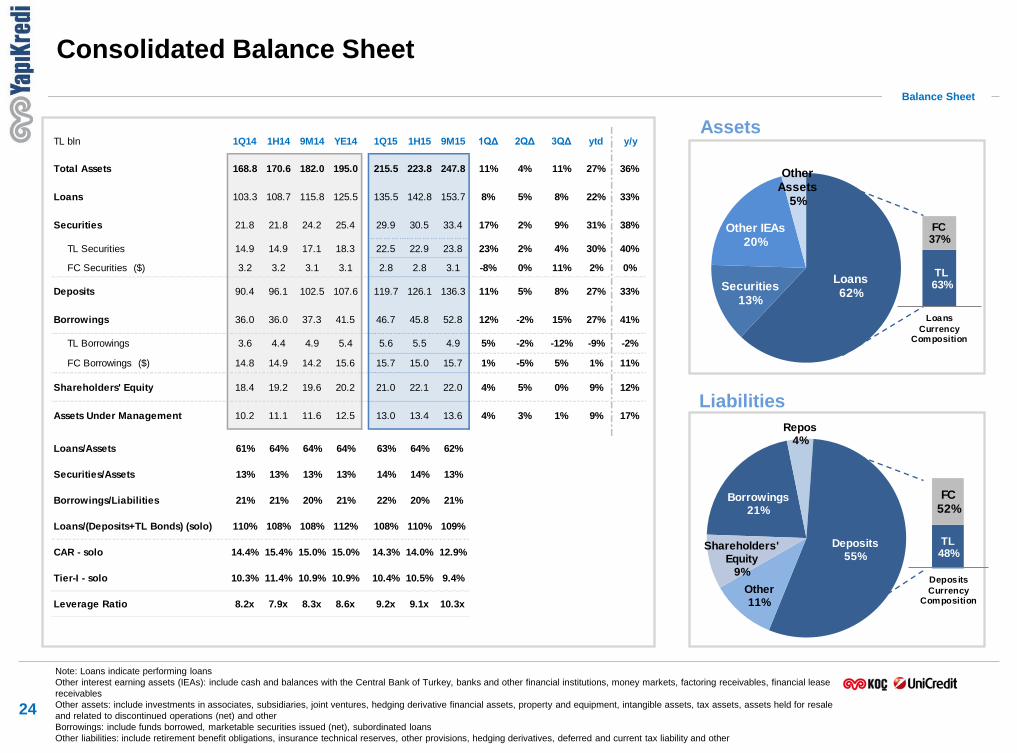

24

Balance Sheet

Assets

Liabilities

Consolidated Balance Sheet

TL63%

FC37%

Loans

CurrencyComposition

TL48%

FC52%

Deposits

CurrencyComposition

Note: Loans indicate performing loans

Other interest earning assets (IEAs): include cash and balances with the Central Bank of Turkey, banks and other financial institutions, money markets, factoring receivables, financial lease

receivables

Other assets: include investments in associates, subsidiaries, joint ventures, hedging derivative financial assets, property and equipment, intangible assets, tax assets, assets held for resale

and related to discontinued operations (net) and other

Borrowings: include funds borrowed, marketable securities issued (net), subordinated loans

Other liabilities: include retirement benefit obligations, insurance technical reserves, other provisions, hedging derivatives, deferred and current tax liability and other

TL bln 1Q14 1H14 9M14 YE14 1Q15 1H15 9M15 1QΔ 2QΔ 3QΔ ytd y/y

Total Assets 168.8 170.6 182.0 195.0 215.5 223.8 247.8 11% 4% 11% 27% 36%

Loans 103.3 108.7 115.8 125.5 135.5 142.8 153.7 8% 5% 8% 22% 33%

Securities 21.8 21.8 24.2 25.4 29.9 30.5 33.4 17% 2% 9% 31% 38%

TL Securities 14.9 14.9 17.1 18.3 22.5 22.9 23.8 23% 2% 4% 30% 40%

FC Securities ($) 3.2 3.2 3.1 3.1 2.8 2.8 3.1 -8% 0% 11% 2% 0%

Deposits 90.4 96.1 102.5 107.6 119.7 126.1 136.3 11% 5% 8% 27% 33%

Borrowings 36.0 36.0 37.3 41.5 46.7 45.8 52.8 12% -2% 15% 27% 41%

TL Borrowings 3.6 4.4 4.9 5.4 5.6 5.5 4.9 5% -2% -12% -9% -2%

FC Borrowings ($) 14.8 14.9 14.2 15.6 15.7 15.0 15.7 1% -5% 5% 1% 11%

Shareholders' Equity 18.4 19.2 19.6 20.2 21.0 22.1 22.0 4% 5% 0% 9% 12%

Assets Under Management 10.2 11.1 11.6 12.5 13.0 13.4 13.6 4% 3% 1% 9% 17%

Loans/Assets 61% 64% 64% 64% 63% 64% 62%

Securities/Assets 13% 13% 13% 13% 14% 14% 13%

Borrowings/Liabilities 21% 21% 20% 21% 22% 20% 21%

Loans/(Deposits+TL Bonds) (solo) 110% 108% 108% 112% 108% 110% 109%

CAR - solo 14.4% 15.4% 15.0% 15.0% 14.3% 14.0% 12.9%

Tier-I - solo 10.3% 11.4% 10.9% 10.9% 10.4% 10.5% 9.4%

Leverage Ratio 8.2x 7.9x 8.3x 8.6x 9.2x 9.1x 10.3x

25

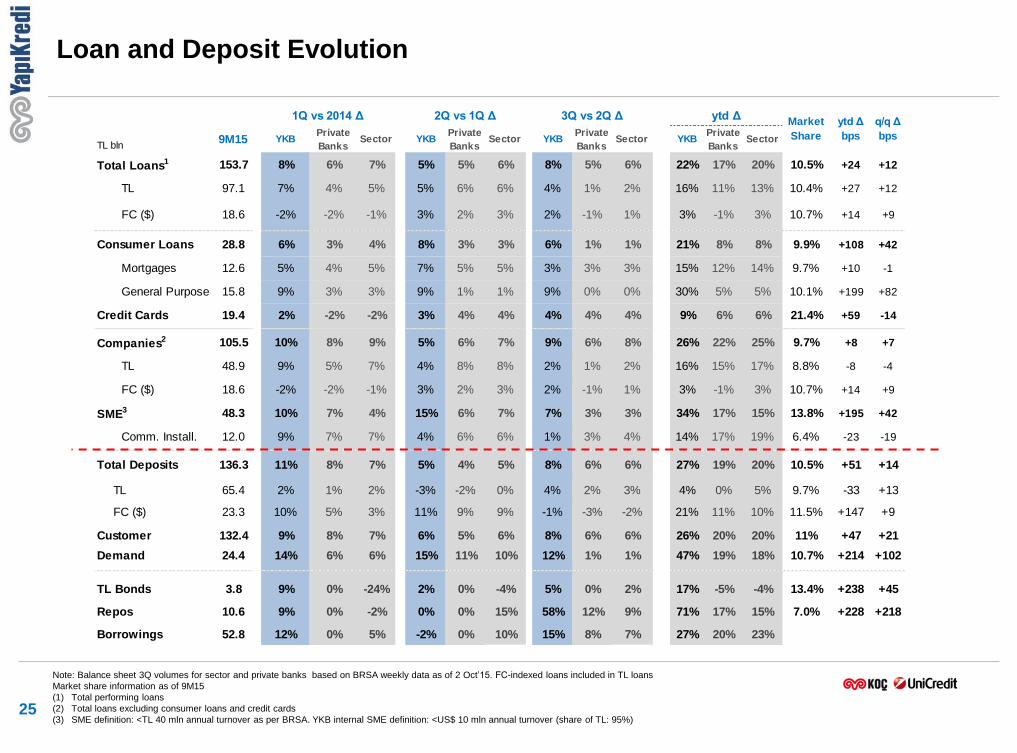

TL bln9M15 YKB

Private

BanksSector YKB

Private

BanksSector YKB

Private

BanksSector YKB

Private

BanksSector

Total Loans1 153.7 8% 6% 7% 5% 5% 6% 8% 5% 6% 22% 17% 20% 10.5% +24 +12

TL 97.1 7% 4% 5% 5% 6% 6% 4% 1% 2% 16% 11% 13% 10.4% +27 +12

FC ($) 18.6 -2% -2% -1% 3% 2% 3% 2% -1% 1% 3% -1% 3% 10.7% +14 +9

Consumer Loans 28.8 6% 3% 4% 8% 3% 3% 6% 1% 1% 21% 8% 8% 9.9% +108 +42

Mortgages 12.6 5% 4% 5% 7% 5% 5% 3% 3% 3% 15% 12% 14% 9.7% +10 -1

General Purpose 15.8 9% 3% 3% 9% 1% 1% 9% 0% 0% 30% 5% 5% 10.1% +199 +82

Credit Cards 19.4 2% -2% -2% 3% 4% 4% 4% 4% 4% 9% 6% 6% 21.4% +59 -14

Companies2 105.5 10% 8% 9% 5% 6% 7% 9% 6% 8% 26% 22% 25% 9.7% +8 +7

TL 48.9 9% 5% 7% 4% 8% 8% 2% 1% 2% 16% 15% 17% 8.8% -8 -4

FC ($) 18.6 -2% -2% -1% 3% 2% 3% 2% -1% 1% 3% -1% 3% 10.7% +14 +9

SME3 48.3 10% 7% 4% 15% 6% 7% 7% 3% 3% 34% 17% 15% 13.8% +195 +42

Comm. Install. 12.0 9% 7% 7% 4% 6% 6% 1% 3% 4% 14% 17% 19% 6.4% -23 -19

Total Deposits 136.3 11% 8% 7% 5% 4% 5% 8% 6% 6% 27% 19% 20% 10.5% +51 +14

TL 65.4 2% 1% 2% -3% -2% 0% 4% 2% 3% 4% 0% 5% 9.7% -33 +13

FC ($) 23.3 10% 5% 3% 11% 9% 9% -1% -3% -2% 21% 11% 10% 11.5% +147 +9

Customer 132.4 9% 8% 7% 6% 5% 6% 8% 6% 6% 26% 20% 20% 11% +47 +21

Demand 24.4 14% 6% 6% 15% 11% 10% 12% 1% 1% 47% 19% 18% 10.7% +214 +102

TL Bonds 3.8 9% 0% -24% 2% 0% -4% 5% 0% 2% 17% -5% -4% 13.4% +238 +45

Repos 10.6 9% 0% -2% 0% 0% 15% 58% 12% 9% 71% 17% 15% 7.0% +228 +218

Borrowings 52.8 12% 0% 5% -2% 0% 10% 15% 8% 7% 27% 20% 23%

q/q Δ

bps

1Q vs 2014 Δ 2Q vs 1Q Δ 3Q vs 2Q Δ ytd ΔMarket

Share

ytd Δ

bps

Loan and Deposit Evolution

Note: Balance sheet 3Q volumes for sector and private banks based on BRSA weekly data as of 2 Oct’15. FC-indexed loans included in TL loans

Market share information as of 9M15

(1) Total performing loans

(2) Total loans excluding consumer loans and credit cards

(3) SME definition: <TL 40 mln annual turnover as per BRSA. YKB internal SME definition: <US$ 10 mln annual turnover (share of TL: 95%)

26

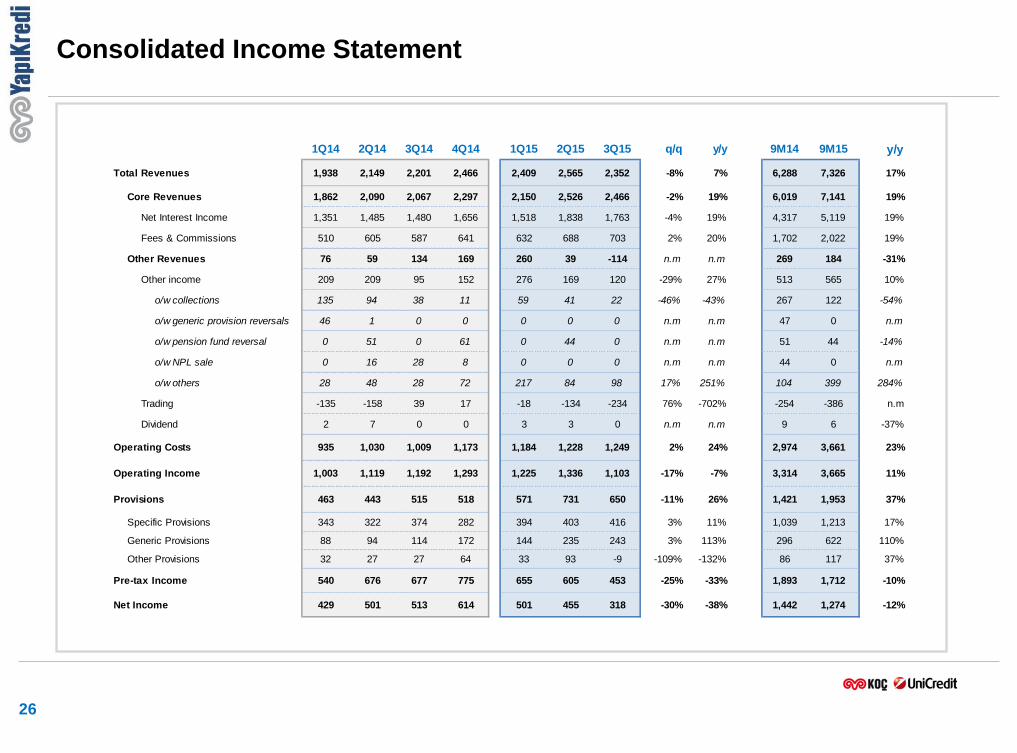

Consolidated Income Statement

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 q/q y/y 9M14 9M15 y/y

Total Revenues 1,938 2,149 2,201 2,466 2,409 2,565 2,352 -8% 7% 6,288 7,326 17%

Core Revenues 1,862 2,090 2,067 2,297 2,150 2,526 2,466 -2% 19% 6,019 7,141 19%

Net Interest Income 1,351 1,485 1,480 1,656 1,518 1,838 1,763 -4% 19% 4,317 5,119 19%

Fees & Commissions 510 605 587 641 632 688 703 2% 20% 1,702 2,022 19%

Other Revenues 76 59 134 169 260 39 -114 n.m n.m 269 184 -31%

Other income 209 209 95 152 276 169 120 -29% 27% 513 565 10%

o/w collections 135 94 38 11 59 41 22 -46% -43% 267 122 -54%

o/w generic provision reversals 46 1 0 0 0 0 0 n.m n.m 47 0 n.m

o/w pension fund reversal 0 51 0 61 0 44 0 n.m n.m 51 44 -14%

o/w NPL sale 0 16 28 8 0 0 0 n.m n.m 44 0 n.m

o/w others 28 48 28 72 217 84 98 17% 251% 104 399 284%

Trading -135 -158 39 17 -18 -134 -234 76% -702% -254 -386 n.m

Dividend 2 7 0 0 3 3 0 n.m n.m 9 6 -37%

Operating Costs 935 1,030 1,009 1,173 1,184 1,228 1,249 2% 24% 2,974 3,661 23%

Operating Income 1,003 1,119 1,192 1,293 1,225 1,336 1,103 -17% -7% 3,314 3,665 11%

Provisions 463 443 515 518 571 731 650 -11% 26% 1,421 1,953 37%

Specific Provisions 343 322 374 282 394 403 416 3% 11% 1,039 1,213 17%

Generic Provisions 88 94 114 172 144 235 243 3% 113% 296 622 110%

Other Provisions 32 27 27 64 33 93 -9 -109% -132% 86 117 37%

Pre-tax Income 540 676 677 775 655 605 453 -25% -33% 1,893 1,712 -10%

Net Income 429 501 513 614 501 455 318 -30% -38% 1,442 1,274 -12%

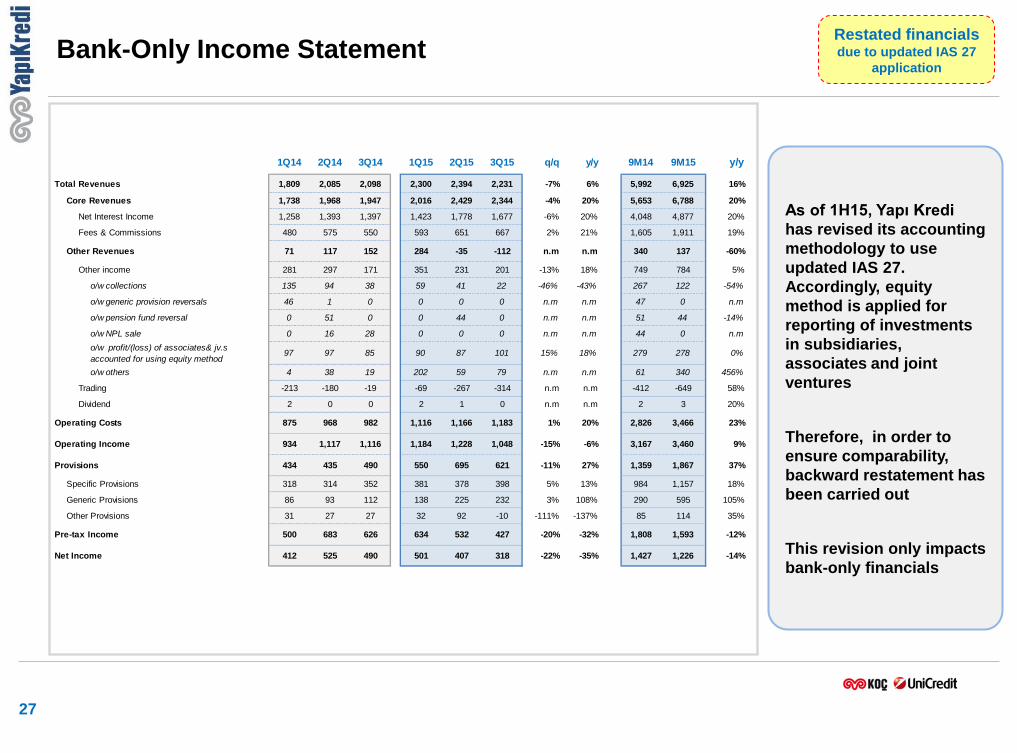

Bank-Only Income Statement

27

As of 1H15, Yapı Kredi

has revised its accounting

methodology to use

updated IAS 27.

Accordingly, equity

method is applied for

reporting of investments

in subsidiaries,

associates and joint

ventures

Therefore, in order to

ensure comparability,

backward restatement has

been carried out

This revision only impacts

bank-only financials

Restated financials due to updated IAS 27

application

1Q14 2Q14 3Q14 1Q15 2Q15 3Q15 q/q y/y 9M14 9M15 y/y

Total Revenues 1,809 2,085 2,098 2,300 2,394 2,231 -7% 6% 5,992 6,925 16%

Core Revenues 1,738 1,968 1,947 2,016 2,429 2,344 -4% 20% 5,653 6,788 20%

Net Interest Income 1,258 1,393 1,397 1,423 1,778 1,677 -6% 20% 4,048 4,877 20%

Fees & Commissions 480 575 550 593 651 667 2% 21% 1,605 1,911 19%

Other Revenues 71 117 152 284 -35 -112 n.m n.m 340 137 -60%

Other income 281 297 171 351 231 201 -13% 18% 749 784 5%

o/w collections 135 94 38 59 41 22 -46% -43% 267 122 -54%

o/w generic provision reversals 46 1 0 0 0 0 n.m n.m 47 0 n.m

o/w pension fund reversal 0 51 0 0 44 0 n.m n.m 51 44 -14%

o/w NPL sale 0 16 28 0 0 0 n.m n.m 44 0 n.m

o/w profit/(loss) of associates& jv.s

accounted for using equity method 97 97 85 90 87 101 15% 18% 279 278 0%

o/w others 4 38 19 202 59 79 n.m n.m 61 340 456%

Trading -213 -180 -19 -69 -267 -314 n.m n.m -412 -649 58%

Dividend 2 0 0 2 1 0 n.m n.m 2 3 20%

Operating Costs 875 968 982 1,116 1,166 1,183 1% 20% 2,826 3,466 23%

Operating Income 934 1,117 1,116 1,184 1,228 1,048 -15% -6% 3,167 3,460 9%

Provisions 434 435 490 550 695 621 -11% 27% 1,359 1,867 37%

Specific Provisions 318 314 352 381 378 398 5% 13% 984 1,157 18%

Generic Provisions 86 93 112 138 225 232 3% 108% 290 595 105%

Other Provisions 31 27 27 32 92 -10 -111% -137% 85 114 35%

Pre-tax Income 500 683 626 634 532 427 -20% -32% 1,808 1,593 -12%

Net Income 412 525 490 501 407 318 -22% -35% 1,427 1,226 -14%

3.49%3.25%

2.88%2.64%

46.7% 48.4%

Cost/Income excl. one-offs Cost/Income

47.3%50.0%

1,504 1,577

1,442 1,274

28

Notes:

Currency depreciation impact calculated bearing 10% of total cost base in FX; USD/TL average depreciation of 25% in 9M15; 15% in 9M14

All relevant one-off impacts are net-off by 20% corporate tax

Cost/Income (excl. one-offs)

NIM

P&L impacted by significant one-offs in 9M15

T. RoAE at 10.6% excl. one-offs and net income growth +5% y/y

9M14 9M15

9M14 9M15 Δ

Net Income 1,442 1,274 -12%

Fixed asset revaluation impact 0 -104

NPL sales -35 0

Fee rebates 44 130

One-off specific provisions 0 84

Additional generic provisions 53 193

Net Income excl. one-offs 1,504 1,577 5%

T. ROAE 11.2% 8.6% -261

T. ROAE excl. one-offs 11.7% 10.6% -110

Cost/Income 47.3% 50.0% 268

Cost/Income excl. one-offs 46.7% 48.4% 170

Reported NII 4,317 5,119 19%

Swap costs 700 896 28%

Swap cost adj. NII 3,617 4,223 17%

NIM 3.49% 3.25% -24.5

NIM adj. by swaps 2.88% 2.64% -23.8

Tangible ROAE (excl. one-offs)

Net Income (excl. one-offs)

9M14 9M15

9M14 9M15 9M14 9M15

excl. one-offs

+5%

Po

st-

tax

11.7%10.6%

11.2%8.6%

-24.5 bps

-23.8 bps

9M14 9M15

NIM NIM adj.

by swaps

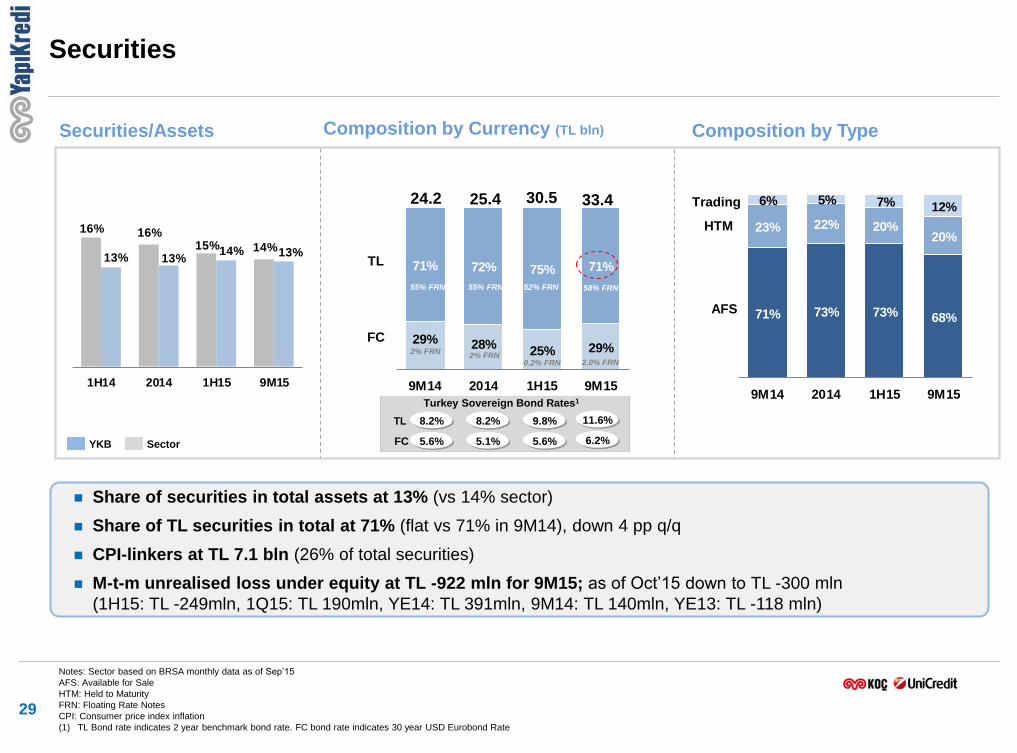

29% 28%25% 29%

71% 72% 75% 71%

9M14 2014 1H15 9M15

29

Notes: Sector based on BRSA monthly data as of Sep’15

AFS: Available for Sale

HTM: Held to Maturity

FRN: Floating Rate Notes

CPI: Consumer price index inflation

(1) TL Bond rate indicates 2 year benchmark bond rate. FC bond rate indicates 30 year USD Eurobond Rate

Share of securities in total assets at 13% (vs 14% sector)

Share of TL securities in total at 71% (flat vs 71% in 9M14), down 4 pp q/q

CPI-linkers at TL 7.1 bln (26% of total securities)

M-t-m unrealised loss under equity at TL -922 mln for 9M15; as of Oct’15 down to TL -300 mln

(1H15: TL -249mln, 1Q15: TL 190mln, YE14: TL 391mln, 9M14: TL 140mln, YE13: TL -118 mln)

Trading

AFS

HTM

Securities/Assets Composition by Currency (TL bln) Composition by Type

Sector YKB

Turkey Sovereign Bond Rates1

TL

FC

30.5

8.2%

5.6%

9.8%

5.6%

Securities

8.2%

5.1%

TL

FC

25.4 24.2

2% FRN

55% FRN

2% FRN

55% FRN

0.2% FRN

52% FRN

16% 16%15% 14%

13% 13%14% 13%

1H14 2014 1H15 9M15

33.4

58% FRN

2.0% FRN

11.6%

6.2%

71% 73% 73% 68%

23% 22% 20%20%

6% 5% 7% 12%

9M14 2014 1H15 9M15

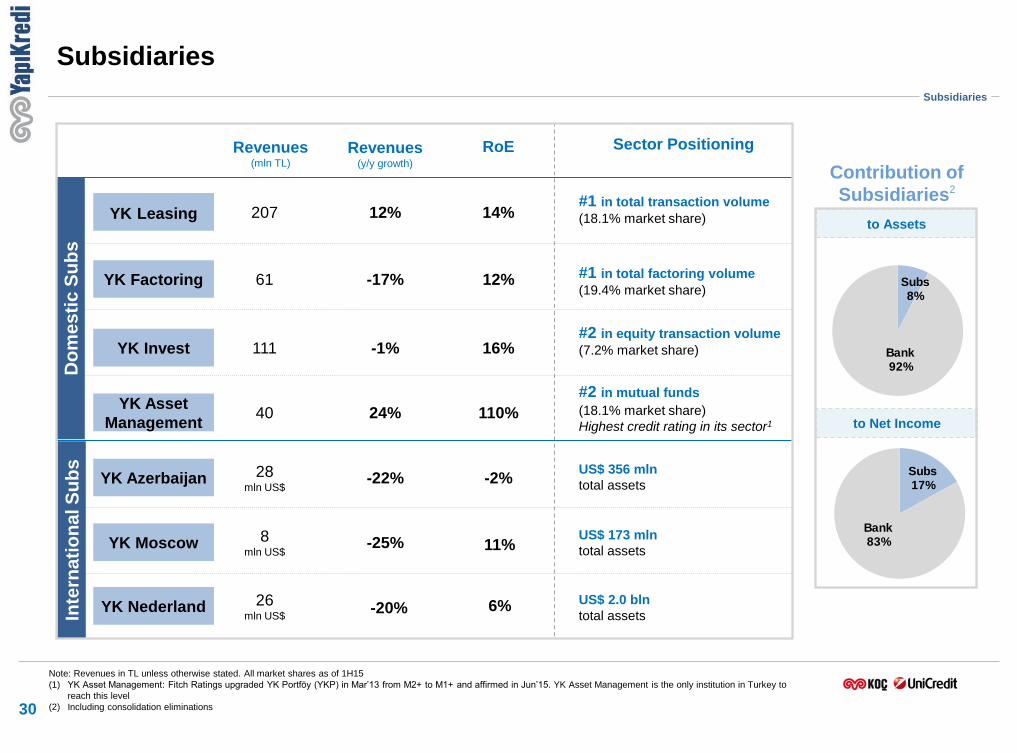

Subsidiaries

30

Revenues (y/y growth)

Sector Positioning

-22%

-25%

Note: Revenues in TL unless otherwise stated. All market shares as of 1H15

(1) YK Asset Management: Fitch Ratings upgraded YK Portföy (YKP) in Mar’13 from M2+ to M1+ and affirmed in Jun’15. YK Asset Management is the only institution in Turkey to

reach this level

(2) Including consolidation eliminations

-17%

12% #1 in total transaction volume

(18.1% market share)

#1 in total factoring volume

(19.4% market share)

-1%

#2 in equity transaction volume

(7.2% market share)

24%

#2 in mutual funds

(18.1% market share)

Highest credit rating in its sector1

US$ 356 mln

total assets

US$ 173 mln

total assets

US$ 2.0 bln

total assets Inte

rna

tio

na

l S

ub

s

Subsidiaries

to Net Income

Contribution of

Subsidiaries2

to Assets

RoE

-2%

12%

14%

16%

110%

YK Leasing

YK Factoring

YK Invest

YK Asset

Management

YK Moscow

YK Nederland

YK Azerbaijan

Revenues (mln TL)

207

61

28 mln US$

111

40

8 mln US$

26 mln US$

Do

me

sti

c S

ub

s

11%

6%

-20%

Subs17%

Bank83%

Subs8%

Bank92%

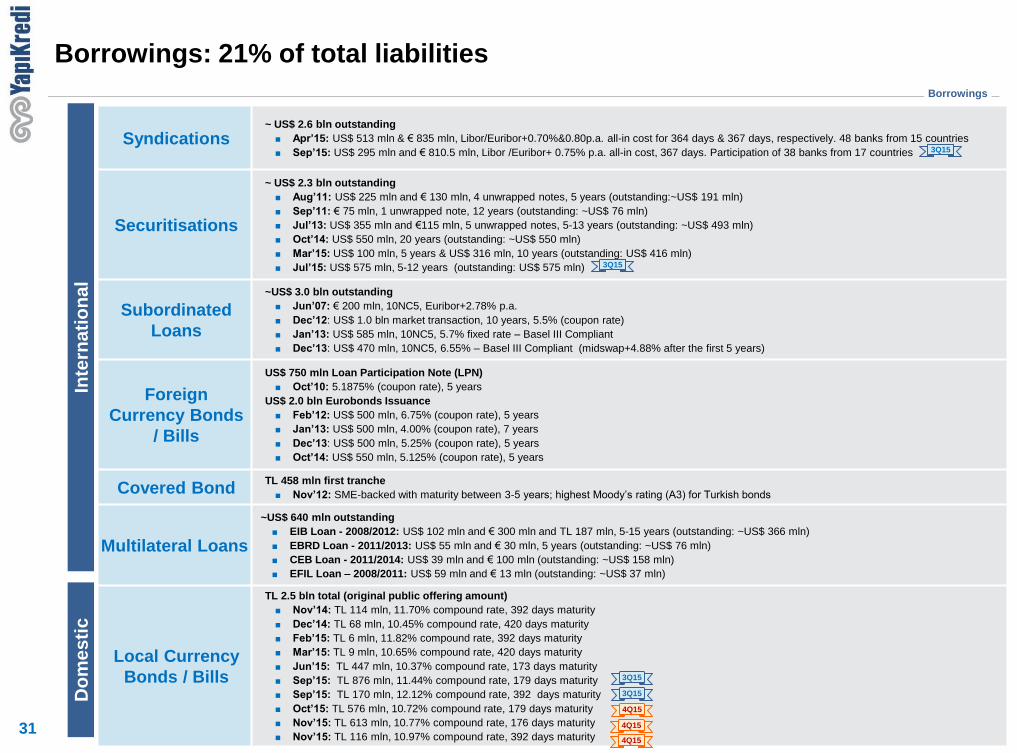

Borrowings

Borrowings: 21% of total liabilities In

tern

ati

on

al

Do

me

sti

c

31

Syndications ~ US$ 2.6 bln outstanding

Apr’15: US$ 513 mln & € 835 mln, Libor/Euribor+0.70%&0.80p.a. all-in cost for 364 days & 367 days, respectively. 48 banks from 15 countries

Sep’15: US$ 295 mln and € 810.5 mln, Libor /Euribor+ 0.75% p.a. all-in cost, 367 days. Participation of 38 banks from 17 countries

Securitisations

~ US$ 2.3 bln outstanding

Aug’11: US$ 225 mln and € 130 mln, 4 unwrapped notes, 5 years (outstanding:~US$ 191 mln)

Sep’11: € 75 mln, 1 unwrapped note, 12 years (outstanding: ~US$ 76 mln)

Jul’13: US$ 355 mln and €115 mln, 5 unwrapped notes, 5-13 years (outstanding: ~US$ 493 mln)

Oct’14: US$ 550 mln, 20 years (outstanding: ~US$ 550 mln)

Mar’15: US$ 100 mln, 5 years & US$ 316 mln, 10 years (outstanding: US$ 416 mln)

Jul’15: US$ 575 mln, 5-12 years (outstanding: US$ 575 mln)

Subordinated

Loans

~US$ 3.0 bln outstanding

Jun’07: € 200 mln, 10NC5, Euribor+2.78% p.a.

Dec’12: US$ 1.0 bln market transaction, 10 years, 5.5% (coupon rate)

Jan’13: US$ 585 mln, 10NC5, 5.7% fixed rate – Basel III Compliant

Dec’13: US$ 470 mln, 10NC5, 6.55% – Basel III Compliant (midswap+4.88% after the first 5 years)

Foreign

Currency Bonds

/ Bills

US$ 750 mln Loan Participation Note (LPN)

Oct’10: 5.1875% (coupon rate), 5 years

US$ 2.0 bln Eurobonds Issuance

Feb’12: US$ 500 mln, 6.75% (coupon rate), 5 years

Jan’13: US$ 500 mln, 4.00% (coupon rate), 7 years

Dec’13: US$ 500 mln, 5.25% (coupon rate), 5 years

Oct’14: US$ 550 mln, 5.125% (coupon rate), 5 years

Covered Bond TL 458 mln first tranche

Nov’12: SME-backed with maturity between 3-5 years; highest Moody’s rating (A3) for Turkish bonds

Multilateral Loans

~US$ 640 mln outstanding

EIB Loan - 2008/2012: US$ 102 mln and € 300 mln and TL 187 mln, 5-15 years (outstanding: ~US$ 366 mln)

EBRD Loan - 2011/2013: US$ 55 mln and € 30 mln, 5 years (outstanding: ~US$ 76 mln)

CEB Loan - 2011/2014: US$ 39 mln and € 100 mln (outstanding: ~US$ 158 mln)

EFIL Loan – 2008/2011: US$ 59 mln and € 13 mln (outstanding: ~US$ 37 mln)

Local Currency

Bonds / Bills

TL 2.5 bln total (original public offering amount)

Nov’14: TL 114 mln, 11.70% compound rate, 392 days maturity

Dec’14: TL 68 mln, 10.45% compound rate, 420 days maturity

Feb’15: TL 6 mln, 11.82% compound rate, 392 days maturity

Mar’15: TL 9 mln, 10.65% compound rate, 420 days maturity

Jun’15: TL 447 mln, 10.37% compound rate, 173 days maturity

Sep’15: TL 876 mln, 11.44% compound rate, 179 days maturity

Sep’15: TL 170 mln, 12.12% compound rate, 392 days maturity

Oct’15: TL 576 mln, 10.72% compound rate, 179 days maturity

Nov’15: TL 613 mln, 10.77% compound rate, 176 days maturity

Nov’15: TL 116 mln, 10.97% compound rate, 392 days maturity

3Q15

3Q15

3Q15

3Q15

4Q15

4Q15

4Q15

32

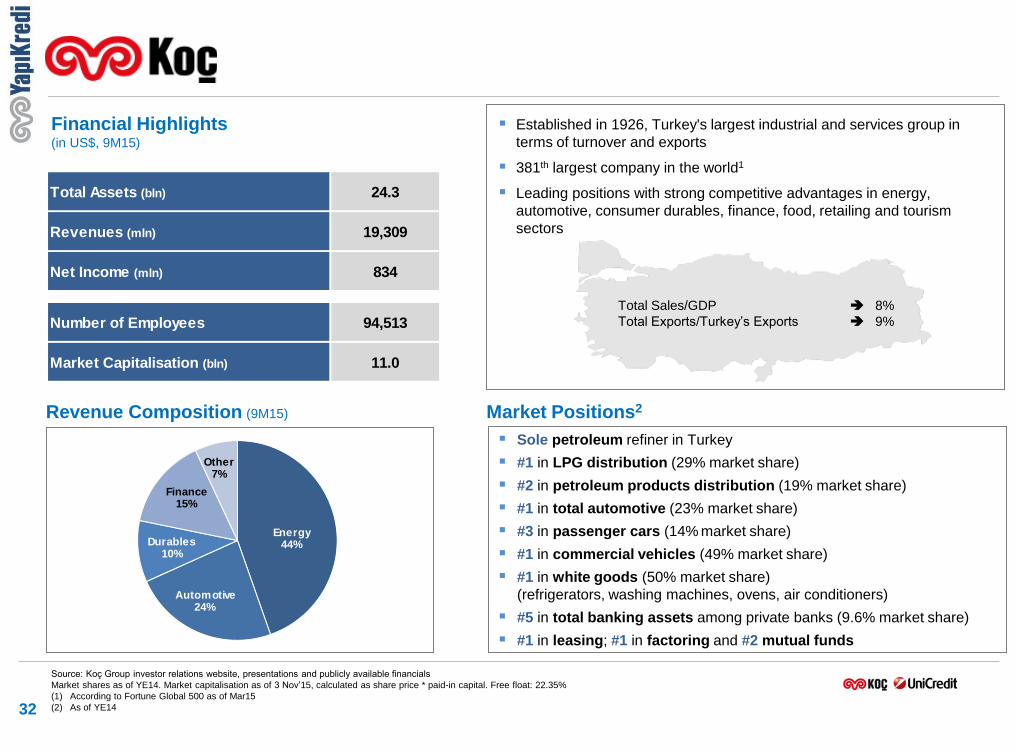

Sole petroleum refiner in Turkey

#1 in LPG distribution (29% market share)

#2 in petroleum products distribution (19% market share)

#1 in total automotive (23% market share)

#3 in passenger cars (14% market share)

#1 in commercial vehicles (49% market share)

#1 in white goods (50% market share)

(refrigerators, washing machines, ovens, air conditioners)

#5 in total banking assets among private banks (9.6% market share)

#1 in leasing; #1 in factoring and #2 mutual funds

Established in 1926, Turkey's largest industrial and services group in

terms of turnover and exports

381th largest company in the world1

Leading positions with strong competitive advantages in energy,

automotive, consumer durables, finance, food, retailing and tourism

sectors

Total Sales/GDP

Total Exports/Turkey’s Exports

8%

9%

Source: Koç Group investor relations website, presentations and publicly available financials

Market shares as of YE14. Market capitalisation as of 3 Nov’15, calculated as share price * paid-in capital. Free float: 22.35%

(1) According to Fortune Global 500 as of Mar15

(2) As of YE14

Revenue Composition (9M15) Market Positions2

Financial Highlights (in US$, 9M15)

Energy44%

Automotive24%

Durables10%

Finance15%

Other7%

Total Assets (bln) 24.3

Revenues (mln) 19,309

Net Income (mln) 834

Number of Employees 94,513

Market Capitalisation (bln) 11.0

Italy50%

CEE16%

Poland7%

Germany18%

Austria9%

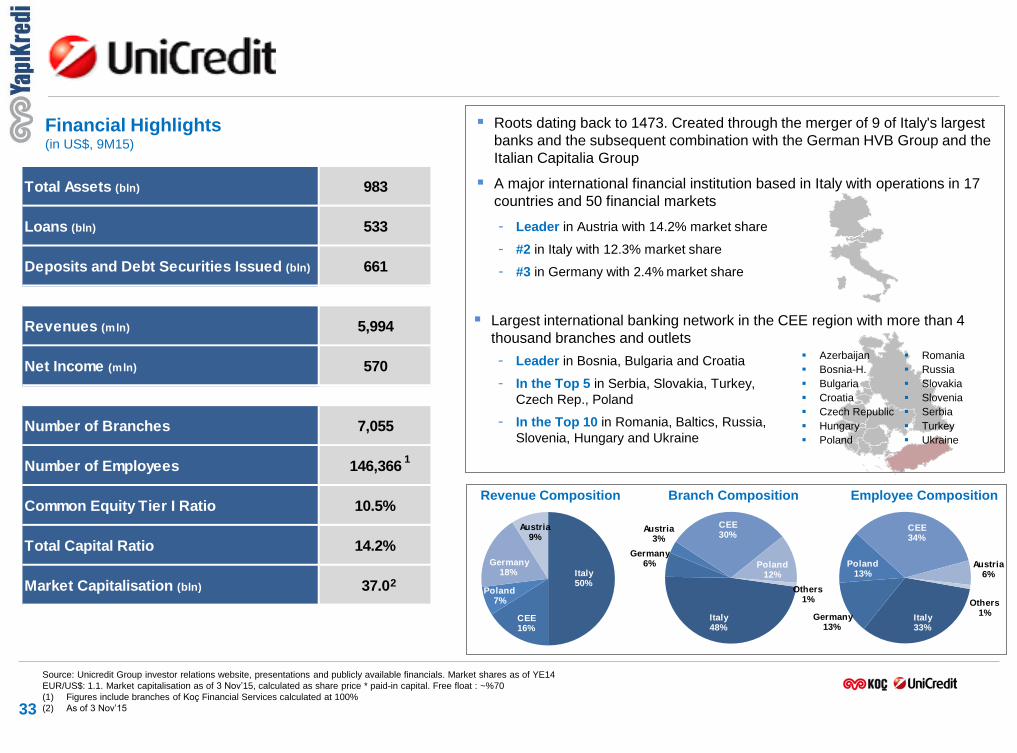

Total Assets (bln) 983

Loans (bln) 533

Deposits and Debt Securities Issued (bln) 661

Revenues (mln) 5,994

Net Income (mln) 570

Number of Branches 7,055

Number of Employees 146,366

Common Equity Tier I Ratio 10.5%

Total Capital Ratio 14.2%

Market Capitalisation (bln) 37.0

Italy48%

Germany6%

Austria3%

CEE30%

Poland12%

Others1%

- Leader in Austria with 14.2% market share

- #2 in Italy with 12.3% market share

- #3 in Germany with 2.4% market share

33

Azerbaijan

Bosnia-H.

Bulgaria

Croatia

Czech Republic

Hungary

Poland

Roots dating back to 1473. Created through the merger of 9 of Italy's largest

banks and the subsequent combination with the German HVB Group and the

Italian Capitalia Group

A major international financial institution based in Italy with operations in 17

countries and 50 financial markets

- Leader in Bosnia, Bulgaria and Croatia

- In the Top 5 in Serbia, Slovakia, Turkey,

Czech Rep., Poland

- In the Top 10 in Romania, Baltics, Russia,

Slovenia, Hungary and Ukraine

Largest international banking network in the CEE region with more than 4

thousand branches and outlets

Revenue Composition Employee Composition Branch Composition

Financial Highlights (in US$, 9M15)

Source: Unicredit Group investor relations website, presentations and publicly available financials. Market shares as of YE14

EUR/US$: 1.1. Market capitalisation as of 3 Nov’15, calculated as share price * paid-in capital. Free float : ~%70

(1) Figures include branches of Koç Financial Services calculated at 100%

(2) As of 3 Nov’15

Romania

Russia

Slovakia

Slovenia

Serbia

Turkey

Ukraine

1

2

Italy 33%

Germany13%

Poland13%

CEE34%

Austria6%

Others1%

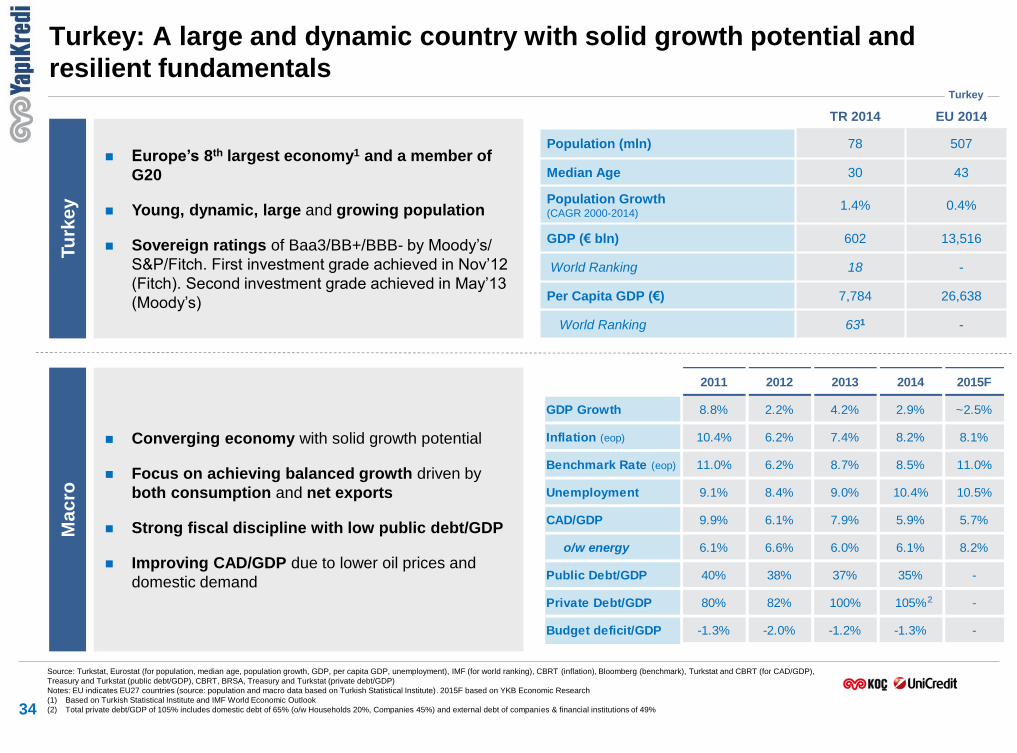

2011 2012 2013 2014 2015F

GDP Growth 8.8% 2.2% 4.2% 2.9% ~2.5%

Inflation (eop) 10.4% 6.2% 7.4% 8.2% 8.1%

Benchmark Rate (eop) 11.0% 6.2% 8.7% 8.5% 11.0%

Unemployment 9.1% 8.4% 9.0% 10.4% 10.5%

CAD/GDP 9.9% 6.1% 7.9% 5.9% 5.7%

o/w energy 6.1% 6.6% 6.0% 6.1% 8.2%

Public Debt/GDP 40% 38% 37% 35% -

Private Debt/GDP 80% 82% 100% 105% -

Budget deficit/GDP -1.3% -2.0% -1.2% -1.3% -

Turkey: A large and dynamic country with solid growth potential and

resilient fundamentals

34

Europe’s 8th largest economy1 and a member of

G20

Young, dynamic, large and growing population

Sovereign ratings of Baa3/BB+/BBB- by Moody’s/

S&P/Fitch. First investment grade achieved in Nov’12

(Fitch). Second investment grade achieved in May’13

(Moody’s)

Tu

rke

y

Converging economy with solid growth potential

Focus on achieving balanced growth driven by

both consumption and net exports

Strong fiscal discipline with low public debt/GDP

Improving CAD/GDP due to lower oil prices and

domestic demand

Source: Turkstat, Eurostat (for population, median age, population growth, GDP, per capita GDP, unemployment), IMF (for world ranking), CBRT (inflation), Bloomberg (benchmark), Turkstat and CBRT (for CAD/GDP),

Treasury and Turkstat (public debt/GDP), CBRT, BRSA, Treasury and Turkstat (private debt/GDP)

Notes: EU indicates EU27 countries (source: population and macro data based on Turkish Statistical Institute). 2015F based on YKB Economic Research

(1) Based on Turkish Statistical Institute and IMF World Economic Outlook

(2) Total private debt/GDP of 105% includes domestic debt of 65% (o/w Households 20%, Companies 45%) and external debt of companies & financial institutions of 49%

Ma

cro

TR 2014 EU 2014

Population (mln) 78 507

Median Age 30 43

Population Growth (CAGR 2000-2014)

1.4% 0.4%

GDP (€ bln) 602 13,516

World Ranking 18 -

Per Capita GDP (€) 7,784 26,638

World Ranking 631 -

2

Turkey

20%

7%

42%

23%

7%

8%

2007 2008 2009 2010 2011 2012 2013 2014

59%

67%

118%

82%

55%

59%

2007 2008 2009 2010 2011 2012 2013 2014

402

145

EU-27 Turkey

225%

137%

EU-27 Turkey

Branches Per

Million Inhabitants

(1H15)

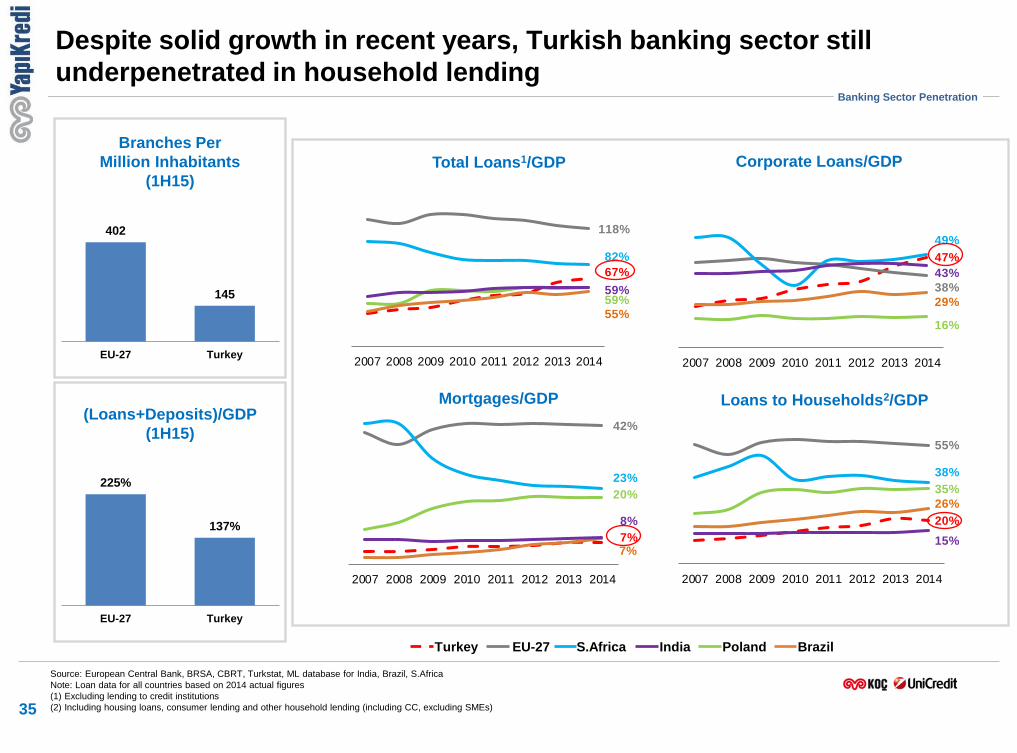

Despite solid growth in recent years, Turkish banking sector still

underpenetrated in household lending

(Loans+Deposits)/GDP

(1H15)

Source: European Central Bank, BRSA, CBRT, Turkstat, ML database for India, Brazil, S.Africa

Note: Loan data for all countries based on 2014 actual figures

(1) Excluding lending to credit institutions

(2) Including housing loans, consumer lending and other household lending (including CC, excluding SMEs)

Corporate Loans/GDP

Mortgages/GDP

Total Loans1/GDP

35

Banking Sector Penetration

16%

47%

38%

49%

29%

43%

2007 2008 2009 2010 2011 2012 2013 2014

35%

20%

55%

38%

26%

15%

2007 2008 2009 2010 2011 2012 2013 2014

Loans to Households2/GDP

Turkey EU-27 S.Africa India Poland Brazil

2007 2012 2013 2014 1H15 9M15 2015F

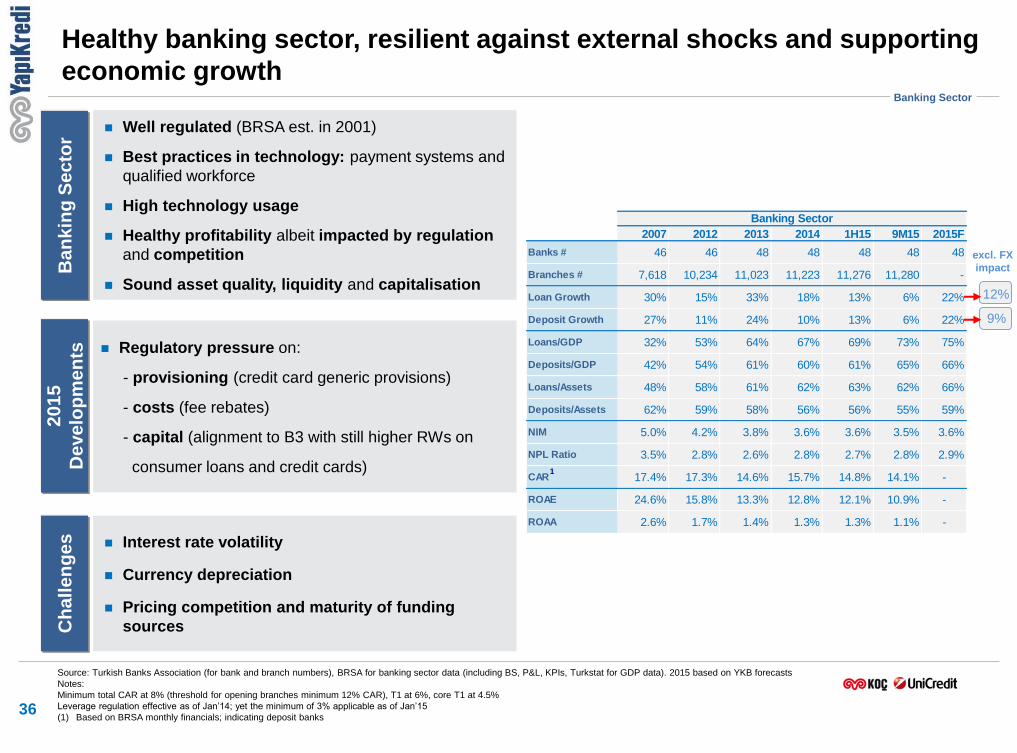

Banks # 46 46 48 48 48 48 48

Branches # 7,618 10,234 11,023 11,223 11,276 11,280 -

Loan Growth 30% 15% 33% 18% 13% 6% 22%

Deposit Growth 27% 11% 24% 10% 13% 6% 22%

Loans/GDP 32% 53% 64% 67% 69% 73% 75%

Deposits/GDP 42% 54% 61% 60% 61% 65% 66%

Loans/Assets 48% 58% 61% 62% 63% 62% 66%

Deposits/Assets 62% 59% 58% 56% 56% 55% 59%

NIM 5.0% 4.2% 3.8% 3.6% 3.6% 3.5% 3.6%

NPL Ratio 3.5% 2.8% 2.6% 2.8% 2.7% 2.8% 2.9%

CAR 17.4% 17.3% 14.6% 15.7% 14.8% 14.1% -

ROAE 24.6% 15.8% 13.3% 12.8% 12.1% 10.9% -

ROAA 2.6% 1.7% 1.4% 1.3% 1.3% 1.1% -

Banking Sector

Well regulated (BRSA est. in 2001)

Best practices in technology: payment systems and

qualified workforce

High technology usage

Healthy profitability albeit impacted by regulation

and competition

Sound asset quality, liquidity and capitalisation

Ba

nk

ing

Se

cto

r

36

Healthy banking sector, resilient against external shocks and supporting

economic growth 2

01

5

De

ve

lop

me

nts

Regulatory pressure on:

- provisioning (credit card generic provisions)

- costs (fee rebates)

- capital (alignment to B3 with still higher RWs on

consumer loans and credit cards)

Interest rate volatility

Currency depreciation

Pricing competition and maturity of funding

sources

Banking Sector

Source: Turkish Banks Association (for bank and branch numbers), BRSA for banking sector data (including BS, P&L, KPIs, Turkstat for GDP data). 2015 based on YKB forecasts

Notes:

Minimum total CAR at 8% (threshold for opening branches minimum 12% CAR), T1 at 6%, core T1 at 4.5%

Leverage regulation effective as of Jan’14; yet the minimum of 3% applicable as of Jan’15

(1) Based on BRSA monthly financials; indicating deposit banks

Ch

all

en

ge

s

1

excl. FX

impact

12%

9%

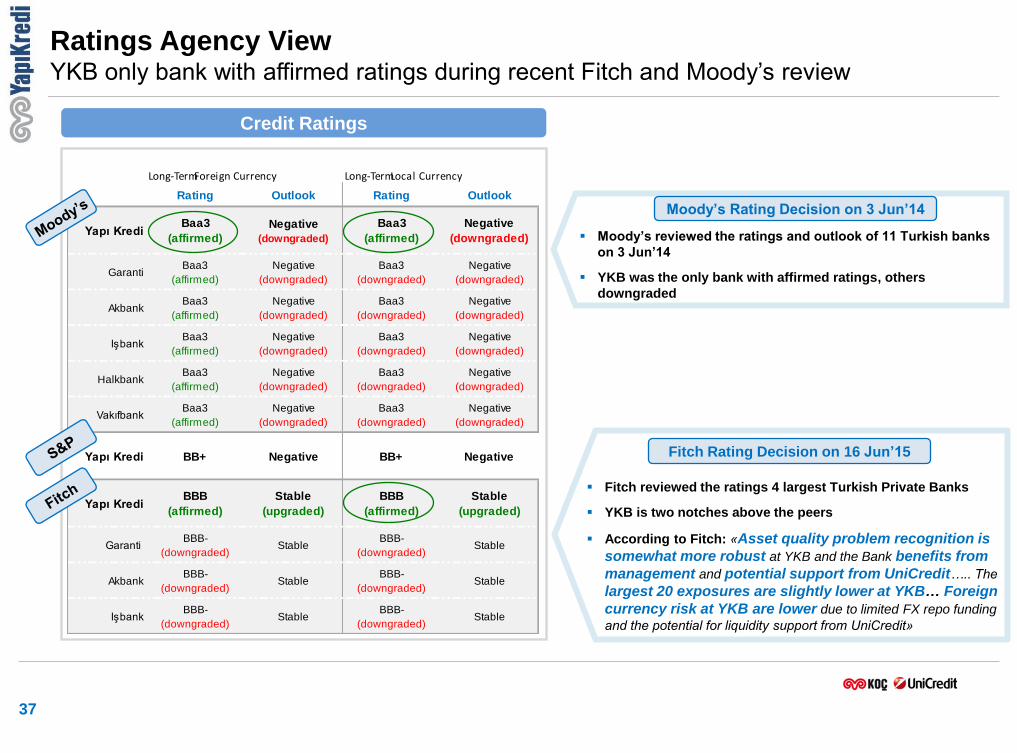

Rating Outlook Rating Outlook

Yapı KrediBaa3

(affirmed)

Negative

(downgraded)

Baa3

(affirmed)

Negative

(downgraded)

GarantiBaa3

(affirmed)

Negative

(downgraded)

Baa3

(downgraded)

Negative

(downgraded)

AkbankBaa3

(affirmed)

Negative

(downgraded)

Baa3

(downgraded)

Negative

(downgraded)

IşbankBaa3

(affirmed)

Negative

(downgraded)

Baa3

(downgraded)

Negative

(downgraded)

HalkbankBaa3

(affirmed)

Negative

(downgraded)

Baa3

(downgraded)

Negative

(downgraded)

VakıfbankBaa3

(affirmed)

Negative

(downgraded)

Baa3

(downgraded)

Negative

(downgraded)

Yapı Kredi BB+ Negative BB+ Negative

Yapı KrediBBB

(affirmed)

Stable

(upgraded)

BBB

(affirmed)

Stable

(upgraded)

Garanti BBB-

(downgraded)Stable

BBB-

(downgraded)Stable

Akbank BBB-

(downgraded)Stable

BBB-

(downgraded)Stable

IşbankBBB-

(downgraded)Stable

BBB-

(downgraded)Stable

Long-Term Foreign Currency Long-Term Local Currency

37

Credit Ratings

Ratings Agency View YKB only bank with affirmed ratings during recent Fitch and Moody’s review

Moody’s reviewed the ratings and outlook of 11 Turkish banks

on 3 Jun’14

YKB was the only bank with affirmed ratings, others

downgraded

Moody’s Rating Decision on 3 Jun’14

Fitch Rating Decision on 16 Jun’15

Fitch reviewed the ratings 4 largest Turkish Private Banks

YKB is two notches above the peers

According to Fitch: «Asset quality problem recognition is

somewhat more robust at YKB and the Bank benefits from

management and potential support from UniCredit….. The

largest 20 exposures are slightly lower at YKB… Foreign

currency risk at YKB are lower due to limited FX repo funding

and the potential for liquidity support from UniCredit»

Yapı Kredi Head Office

Yapı Kredi Plaza D Blok

Levent 34330 Istanbul - TURKEY

Tel: +90 (212) 339 73 23

Email: [email protected]

Web: http://www.yapikredi.com.tr/en/investor-relations

Contact Investor Relations

Strong Analyst Coverage

35 Equity Analysts

10 Fixed Income Analysts

> 800 fixed income meetings

> 2,400 equity meetings

and participation in >130 conferences /

roadshows in US, UK, Europe, Middle-East

and Asia over the past ~4 years

38