your finances and all that matters to you … finances and all that matters to you ... 56000...

TRANSCRIPT

YOUR FINANCES AND ALL THAT MATTERS TO YOU

JUNE 2011ISSUE 9KDN : PP16208/06/2011(029654)

by

Feature Story

YOUR CHILD’SEDUCATION FUND:Will you pass with flying colours? Pg 2

Money Matters

Is there a bubble in commodities?Based on views by Schroders Investment Limited Pg 8

Personal Finance

Say hello toMobile Banking Pg 12

Need cash on the go?Get convenient access to your HSBC account via MEPS’ Shared ATM Network Pg 16

Takaful Education PlanFinancial flexibility to create his future

Notes:* The investment returns will fluctuate (i.e. rise or fall) based on actual performance of the investment-linked funds. ^ The payout amount depends on the performance of the funds selected and is not guaranteed. The regular payout option is only available if a covered

person‘s (child’s) entry age is from 1 month to 12 years. Issued by HSBC Bank Malaysia Berhad (Company No. 127776-V) (”HSBC”) and HSBC Amanah Malaysia Berhad (Company No. 807705-X) (”HSBC Amanah”). Takaful Education Plan is managed by HSBC Amanah Takaful (Malaysia) Sdn. Bhd. (Company No. 731530-M). HSBC and HSBC Amanah are the distributors for this plan. Terms and Conditions apply.

Prepare to give your child one of life's most precious gifts – an education of his choice with our Takaful Education Plan.

The Takaful Education Plan offers: Flexibility to help you build an education fund through an investment-linked Takaful

plan that may offer potentially higher returns* as compared to deposit accounts. Payout^ when your child is ready for university. Takaful protection for both you and your child.

Start planning today for your child's education tomorrow.

Call 1 300 88 0181 (HSBC) or 1 300 80 2428 (HSBC Amanah) Click hsbc.com.my or hsbcamanah.com.my

hope

HSBC Bank Malaysia Berhad June 2011 1

PublisherHSBC Bank Malaysia Berhad(Company No. 127776-V)

editorialLo Wei TeingWoo Chui ChuiJeff OngYap Mei Mei

Printed byPercetakan Lai Sdn. Bhd.No. 1, Persiaran 2/118CKawasan PerindustrianDesa Tun Razak56000 Cheras, Kuala LumpurWilayah Persekutuan

For more information on HSBC products and services, please feel free to contact us.• Call 1 300 88 0181• Click www.hsbc.com.my• Visit your nearest HSBC branch

© Copyright. hsbC bank Malaysia berhad (Company no.127776-V) 2011. all right reserved.

This publication is for private circulation to selected customers of HSBC Bank Malaysia Berhad (”HSBC”), and may not be

redistributed, reproduced, copied or published, in whole or in part, for any purpose. This publication is solely for general information and does not constitute any advice, recommendation or offer by HSBC.

The opinions, statements and information contained in this publication are based on available data delivered to be reliable. HSBC does not warrant the accuracy, completeness of fairness of such opinions, statements and information and reliance thereon shall give rise to any claim whatsoever against HSBC.

Issued by HSBC Bank Malaysia Berhad (Company No. 127776-V) You may, at any time, choose not to receive direct marketing literature/information about our products and services. Please write to Direct Mailing Exclusion Coordinator at P.O. Box 13688, 50818 Kuala Lumpur, Malaysia with your request and we will delete your name from our direct mailing lists without charge.

off the cuff

Phot

o by

Rel

ucen

t Pho

togr

aphy

A plan today, a degree tomorrowWelcome to another issue of Liquid. Our feature for this issue is a topic close to the heart of parents – the education of their children.

An education is one of life's most precious gifts that parents can provide to their children. It not only prepares them for their future but it also gives them a vital head start in life. Nevertheless, life is unpredictable and has its own twist and turns which may serve as road bumps on a child's educational journey. But no matter where life takes us, there are strategies that parents may use to ensure that their children get the education they deserve. Read on for some tips on education planning.

Commodities had a good run in 2010. For 2011, some investors are concerned that a bubble may be developing in this asset class. Schroders Investment Limited, one of the world's leading asset management companies, shares its views on commodities and the factors that could drive prices up or down.

We will also be highlighting the growing trend of mobile banking. Perhaps you are one of our customers who frequent HSBC's website via our mobile banking application. You will appreciate the security measures we have in place as well as the various quick and easy services available on this platform.

Lastly, we would like to thank you for letting us walk with you through life's journey as your financial partner. Do enjoy this issue of Liquid.

Best regards,

lim eng seongGeneral Manager Personal Financial Services

2 HSBC Bank Malaysia Berhad June 2011

feature

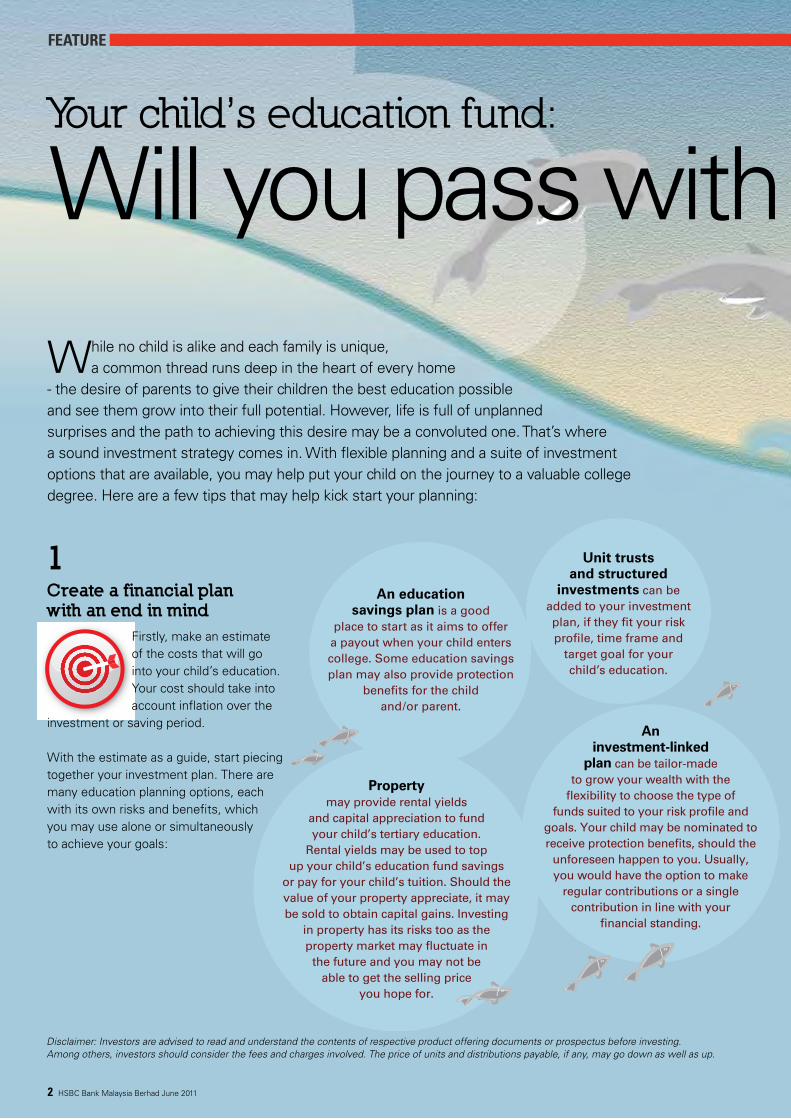

1Create a financial plan with an end in mind

Firstly, make an estimate of the costs that will go into your child’s education. Your cost should take into account inflation over the

investment or saving period.

With the estimate as a guide, start piecing together your investment plan. There are many education planning options, each with its own risks and benefits, which you may use alone or simultaneously to achieve your goals:

Disclaimer: Investors are advised to read and understand the contents of respective product offering documents or prospectus before investing. Among others, investors should consider the fees and charges involved. The price of units and distributions payable, if any, may go down as well as up.

While no child is alike and each family is unique, a common thread runs deep in the heart of every home

- the desire of parents to give their children the best education possible and see them grow into their full potential. However, life is full of unplanned surprises and the path to achieving this desire may be a convoluted one. That’s where a sound investment strategy comes in. With flexible planning and a suite of investment options that are available, you may help put your child on the journey to a valuable college degree. Here are a few tips that may help kick start your planning:

Your child’s education fund:

Will you pass with flying colours?

An educationsavings plan is a good

place to start as it aims to offera payout when your child enters college. Some education savings plan may also provide protection

benefits for the child and/or parent.

Property may provide rental yields

and capital appreciation to fund your child’s tertiary education.

Rental yields may be used to top up your child’s education fund savings

or pay for your child’s tuition. Should the value of your property appreciate, it may be sold to obtain capital gains. Investing

in property has its risks too as the property market may fluctuate in

the future and you may not be able to get the selling price

you hope for.

Unit trusts and structured

investments can be added to your investment plan, if they fit your risk profile, time frame and

target goal for your child’s education.

An investment-linked

plan can be tailor-made to grow your wealth with the

flexibility to choose the type of funds suited to your risk profile and

goals. Your child may be nominated to receive protection benefits, should the

unforeseen happen to you. Usually, you would have the option to make

regular contributions or a single contribution in line with your

financial standing.

HSBC Bank Malaysia Berhad June 2011 3

feature

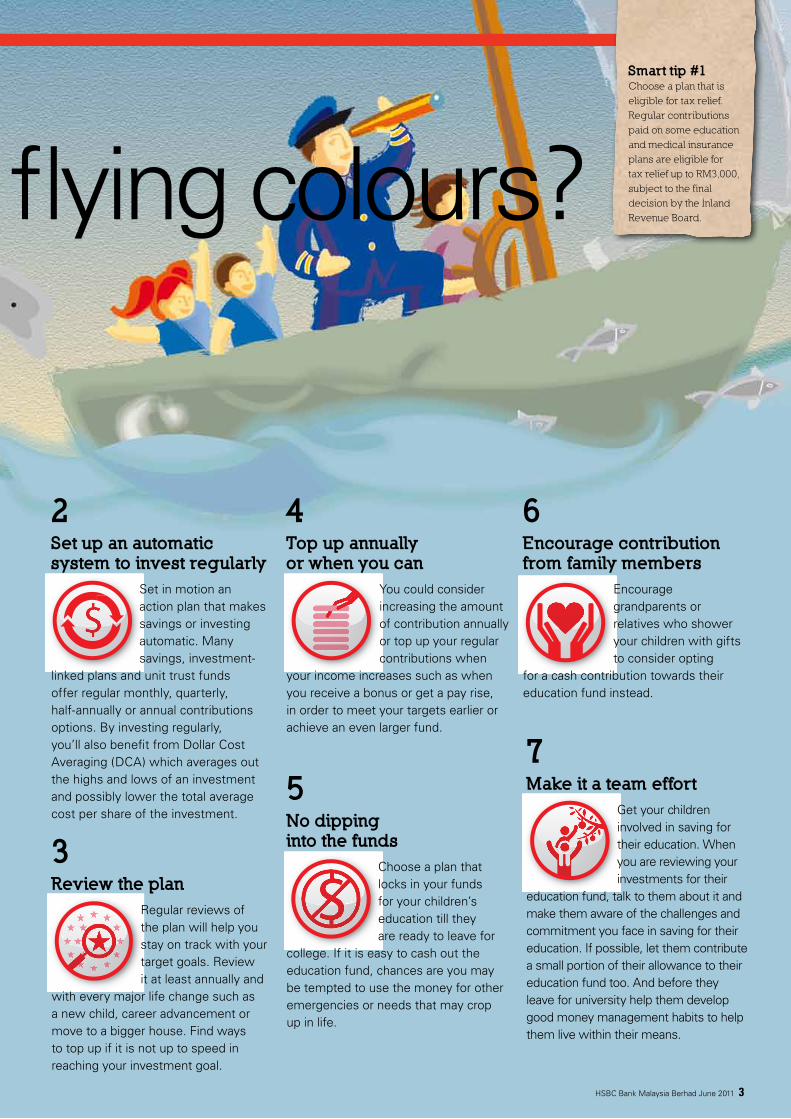

2Set up an automatic system to invest regularly

Set in motion an action plan that makes savings or investing automatic. Many savings, investment-

linked plans and unit trust funds offer regular monthly, quarterly, half-annually or annual contributions options. By investing regularly, you’ll also benefit from Dollar Cost Averaging (DCA) which averages out the highs and lows of an investment and possibly lower the total average cost per share of the investment.

3Review the plan

Regular reviews of the plan will help you stay on track with your target goals. Review it at least annually and

with every major life change such as a new child, career advancement or move to a bigger house. Find ways to top up if it is not up to speed in reaching your investment goal.

4Top up annually or when you can

You could consider increasing the amount of contribution annually or top up your regular contributions when

your income increases such as when you receive a bonus or get a pay rise, in order to meet your targets earlier or achieve an even larger fund.

5No dipping into the funds

Choose a plan that locks in your funds for your children’s education till they are ready to leave for

college. If it is easy to cash out the education fund, chances are you may be tempted to use the money for other emergencies or needs that may crop up in life.

6Encourage contribution from family members

Encourage grandparents or relatives who shower your children with gifts to consider opting

for a cash contribution towards their education fund instead.

7Make it a team effort

Get your children involved in saving for their education. When you are reviewing your investments for their

education fund, talk to them about it and make them aware of the challenges and commitment you face in saving for their education. If possible, let them contribute a small portion of their allowance to their education fund too. And before they leave for university help them develop good money management habits to help them live within their means.

Smart tip #1Choose a plan that is eligible for tax relief. Regular contributions paid on some education and medical insurance plans are eligible for tax relief up to RM3,000, subject to the final decision by the Inland Revenue Board.Will you pass with flying colours?

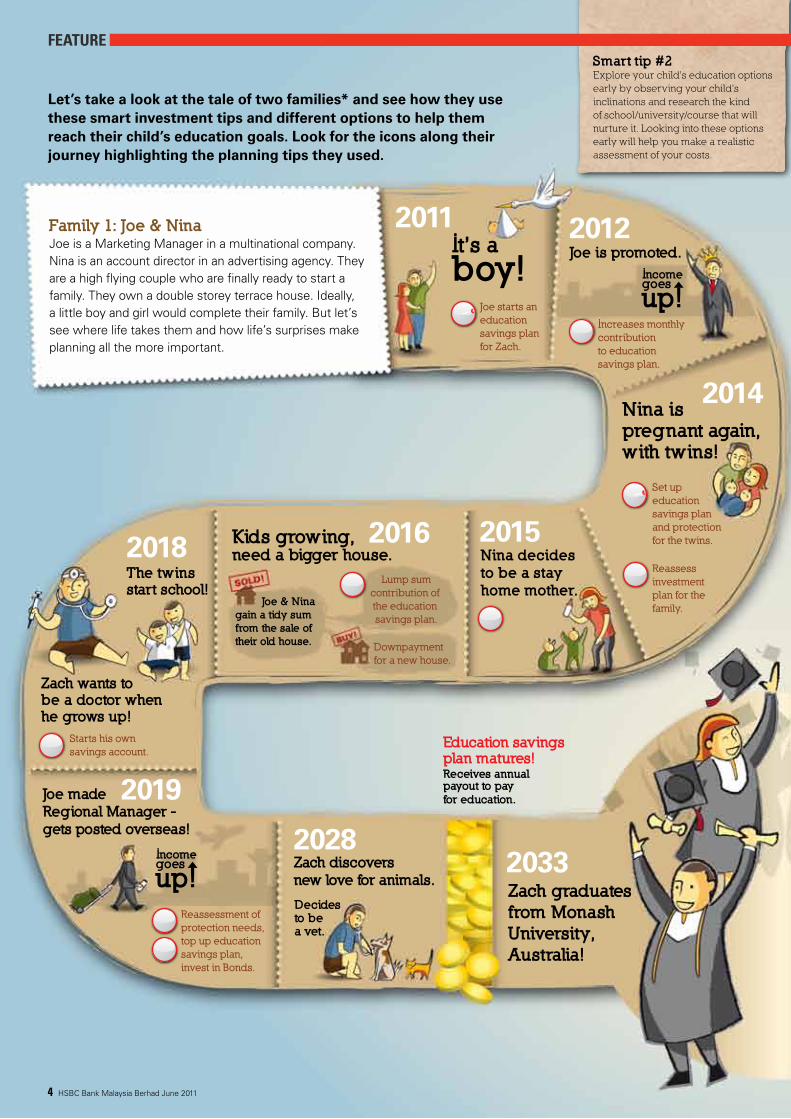

Family 1: Joe & Nina Joe is a Marketing Manager in a multinational company. Nina is an account director in an advertising agency. They are a high flying couple who are finally ready to start a family. They own a double storey terrace house. Ideally, a little boy and girl would complete their family. But let’s see where life takes them and how life’s surprises make planning all the more important.

It’s aboy!

Joe is promoted.

Joe madeRegional Manager -gets posted overseas!

Zach graduatesfrom MonashUniversity,Australia!

Nina ispregnant again,with twins!

Nina decidesto be a stayhome mother.

Kids growing,need a bigger house.

Zach wants tobe a doctor when he grows up!

The twinsstart school!

2011 2012

2014

201520162018

2019

20282033

Increases monthlycontributionto education savings plan.

Joe starts aneducation savings planfor Zach.

Set up educationsavings planand protectionfor the twins.

Reassessment of protection needs,top up education savings plan, invest in Bonds.

Education savings plan matures!Receives annual payout to pay for education.

Lump sumcontribution of the education savings plan.

Downpayment for a new house.

Zach discoversnew love for animals.

Starts his own savings account.

Decidesto be a vet.

Reassess investmentplan for the family.

Let’s take a look at the tale of two families* and see how they use these smart investment tips and different options to help them reach their child’s education goals. Look for the icons along their journey highlighting the planning tips they used.

* All characters appearing in this article are fictitious. Any resemblance to real persons, living or dead, is purely coincidental.

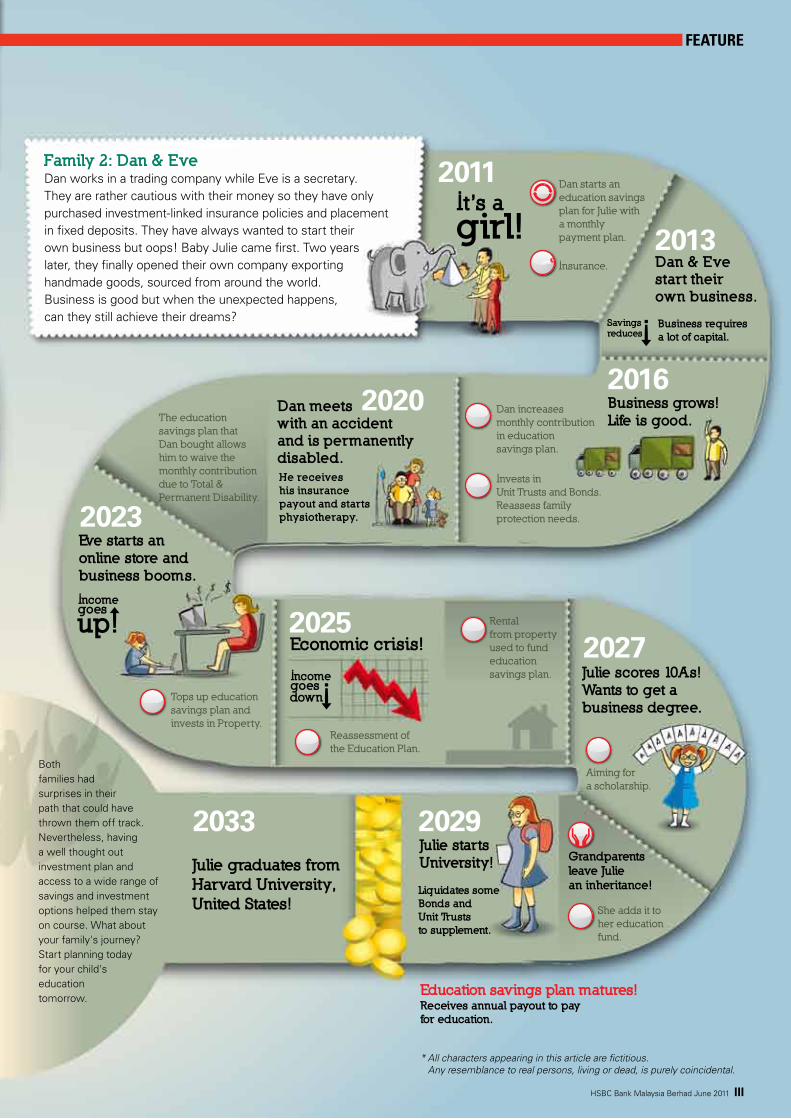

It’s agirl!

Dan & Evestart theirown business.

Business grows!Life is good.

Dan meetswith an accidentand is permanentlydisabled.

Eve starts anonline store and business booms.

Economic crisis!Julie scores 10As!Wants to get abusiness degree.

Julie graduates from Harvard University,United Kingdom!

2011

2013

20162020

2023

20252027

2033

Business requiresa lot of capital.

Insurance.

Dan starts an education savings plan for Julie witha monthlypayment plan.

Dan increasesmonthly contributionin educationsavings plan.

He receiveshis insurancepayout and startsphysiotherapy.

The education savings plan that Dan bought allows him to waive themonthly contribution due to Total & Permanent Disability.

Tops up education savings plan and invests in Property.

Reassessment ofthe Education Plan.

Grandparents leave Juliean inheritance!

Julie startsUniversity!

2029

Liquidates someBonds and Unit Truststo supplement.

Education savings plan matures!Receives annual payout to pay for education.

Joe & Ninagain a tidy sumfrom the sale oftheir old house.

Invests inUnit Trusts and Bonds.Reassess familyprotection needs.

Aiming for a scholarship.

She adds it toher educationfund.

Rentalfrom property used to fund education savings plan.

Savingsreduces

Both families had surprises in their path that could have thrown them off track. Nevertheless, having a well thought out investment plan and access to a wide range of savings and investment options helped them stay on course. What about your family's journey? Start planning today for your child's education tomorrow.

Family 2: Dan & EveDan works in a trading company while Eve is a secretary. They are rather cautious with their money so they have only purchased investment-linked insurance policies and placement in fixed deposits. They have always wanted to start their own business but oops! Baby Julie came first. Two years later, they finally opened their own company exporting handmade goods, sourced from around the world. Business is good but when the unexpected happens, can they still achieve their dreams?

4 HSBC Bank Malaysia Berhad June 2011

featureSmart tip #2Explore your child’s education options early by observing your child’s inclinations and research the kind of school/university/course that will nurture it. Looking into these options early will help you make a realistic assessment of your costs.

Family 1: Joe & Nina Joe is a Marketing Manager in a multinational company. Nina is an account director in an advertising agency. They are a high flying couple who are finally ready to start a family. They own a double storey terrace house. Ideally, a little boy and girl would complete their family. But let’s see where life takes them and how life’s surprises make planning all the more important.

It’s aboy!

Joe is promoted.

Joe madeRegional Manager -gets posted overseas!

Zach graduatesfrom MonashUniversity,Australia!

Nina ispregnant again,with twins!

Nina decidesto be a stayhome mother.

Kids growing,need a bigger house.

Zach wants tobe a doctor when he grows up!

The twinsstart school!

2011 2012

2014

201520162018

2019

20282033

Increases monthlycontributionto education savings plan.

Joe starts aneducation savings planfor Zach.

Set up educationsavings planand protectionfor the twins.

Reassessment of protection needs,top up education savings plan, invest in Bonds.

Education savings plan matures!Receives annual payout to pay for education.

Lump sumcontribution of the education savings plan.

Downpayment for a new house.

Zach discoversnew love for animals.

Starts his own savings account.

Decidesto be a vet.

Reassess investmentplan for the family.

Let’s take a look at the tale of two families* and see how they use these smart investment tips and different options to help them reach their child’s education goals. Look for the icons along their journey highlighting the planning tips they used.

* All characters appearing in this article are fictitious. Any resemblance to real persons, living or dead, is purely coincidental.

It’s agirl!

Dan & Evestart theirown business.

Business grows!Life is good.

Dan meetswith an accidentand is permanentlydisabled.

Eve starts anonline store and business booms.

Economic crisis!Julie scores 10As!Wants to get abusiness degree.

2011

2013

20162020

2023

20252027

2033

Business requiresa lot of capital.

Insurance.

Dan starts an education savings plan for Julie witha monthlypayment plan.

Dan increasesmonthly contributionin educationsavings plan.

He receiveshis insurancepayout and startsphysiotherapy.

The education savings plan that Dan bought allows him to waive themonthly contribution due to Total & Permanent Disability.

Tops up education savings plan and invests in Property.

Reassessment ofthe Education Plan.

Grandparents leave Juliean inheritance!

Julie startsUniversity!

2029

Liquidates someBonds and Unit Truststo supplement.

Education savings plan matures!Receives annual payout to pay for education.

Joe & Ninagain a tidy sumfrom the sale oftheir old house.

Invests inUnit Trusts and Bonds.Reassess familyprotection needs.

Aiming for a scholarship.

She adds it toher educationfund.

Rentalfrom property used to fund education savings plan.

Savingsreduces

Both families had surprises in their path that could have thrown them off track. Nevertheless, having a well thought out investment plan and access to a wide range of savings and investment options helped them stay on course. What about your family's journey? Start planning today for your child's education tomorrow.

Family 2: Dan & EveDan works in a trading company while Eve is a secretary. They are rather cautious with their money so they have only purchased investment-linked insurance policies and placement in fixed deposits. They have always wanted to start their own business but oops! Baby Julie came first. Two years later, they finally opened their own company exporting handmade goods, sourced from around the world. Business is good but when the unexpected happens, can they still achieve their dreams?

Julie graduates from Harvard University,United States!

HSBC Bank Malaysia Berhad June 2011 III

feature

6 HSBC Bank Malaysia Berhad June 2011

featurefeature

75% of affluent Malaysians have plans to send their children to study overseas, the HSBC Affluent Asian Tracker Survey 2009 conducted by Nielsen for HSBC Group reported. They estimated that each child would require an average of US$100,000.

Besides the salary gap, an overseas degree may offer international recognition and an opportunity to experience life abroad. An international student will also enjoy cross cultural exposure, possibly pick up a new language as well as learn valuable lessons in independence and adapting to new surroundings. With the international head start, it may open doors to careers with global prospects.

Is an overseas education worth it?

Estimated budget for each child's total educational expenses(Average: US$103,281)

Smart tip #4Do not forget to consider insurance/Takaful protection for your child. With insurance/Takaful protection, it may help to provide for your child’s education needs should the unfortunate happen to you.

Smart tip #3Get your Will written to ensure that your assets are distributed among family, dependents and other beneficiaries according to your wishes, should the unfortunate happen to you. With a Will, it may help you to continue to provide for, as well as assign support and guardianship to your young children.

* For this research, the term "overseas" refers to the top three most popular overseas destinations for tertiary studies - Australia, Great Britain and United States - and includes twinning programmes.

Source: Jobstreet.com, "Graduates of overseas universities fare better than local grads in salary scale", 15 April 2008.

3 out of 4 aff luent Malaysians think soPlans to send childrenoverseas to study

Build your child's education fund with our new Takaful Education Plan or our wide range of investment and protection plans. Talk to your Relationship Manager if you are interested in creating an investment portfolio for your children's education.

Source: The Edge Malaysia, “Affluent Malaysians increase investments despite financial storm” 6 July, 2009.

start Planning today for your Child's eduCation toMorrow.

Jobstreet.com, one of the leading recruitment agencies in Malaysia conducted a study* of more than 100,000 JobStreet.com members in Malaysia who held a Bachelor degree and are currently working in the country. From the study, JobStreet.com discovered that graduates from overseas* universities on average earn about 12 percent more than local graduates. "The salary gap is most apparent among those with up to five years of work experience. Overseas graduates are earning a significant 20 percent more than their local counterparts. Even after 10 years or more of work experience, the gap is still more than 10 percent," the report states.

No Yes25% 75% 10%

23%

3%

29%

21%

15%

Less thanUS$10K

US$10K - <US$30K

US$30K - <US$50K

US$50K - <US$100K

US$100K - <US$200K

US$200K or above

THE ALL NEW EXCLUSIVEHSBC VISA SIGNATURE

JUST ONE CREDIT CARD FOR THE BEST PRIVILEGES WORLDWIDE

SIGN UP TODAY!Call 03-2059 9333Click www.hsbc.com.mySMS type HSBC and SMS to 33213

HotelsUp to 75% discounton 55,000 hotelsworldwide

AirlinesUp to 70% discount onCathay and MASBusiness Class tickets

For more details on privileges, visit www.hsbc.com.my

Home & Away PrivilegesUp to 50% discount onmerchants in more than160 countries

Issued by HSBC Bank Malaysia Berhad (Company No. 127776-V). *HSBC Visa Signature 5X Rewards Programme Terms and Conditions apply. The HSBC Visa Signature 5X Reward Points is applicable only to spends made at the following merchants: Shopping (Malls; Mid Valley Megamall & The Gardens Mall KL, KSL City Mall JB, Gurney Plaza Penang and Departmental Stores; Tangs, Parkson & Isetan), Groceries (Mercato, Village Grocer, Cold Storage) and Overseas Spend (all Dining spend and Hotel charges). There is a capping on the 5X RP that an Eligible Cardholder stands to receive on the eligible spend per Participating Month. The Reward Points will be credited into the primary Eligible Cardholder's HSBC Visa Signature Credit Card account and can only be redeemed and used by the primary Eligible Cardholder. SmartPrivileges Terms and Conditions apply to the merchant offers shown.

8 HSBC Bank Malaysia Berhad June 2011

Money Matters

Is there a bubble in commodities?Based on views by Schroders Investment Limited

First of all, we need to understand that like investments in any asset class, commodity prices are driven over the long-term by the rules of supply and demand. And like many asset classes, the long term is made up of a series of medium-term cycles, in which prices move up and down as supply and demand fall into and out of alignment with each other.

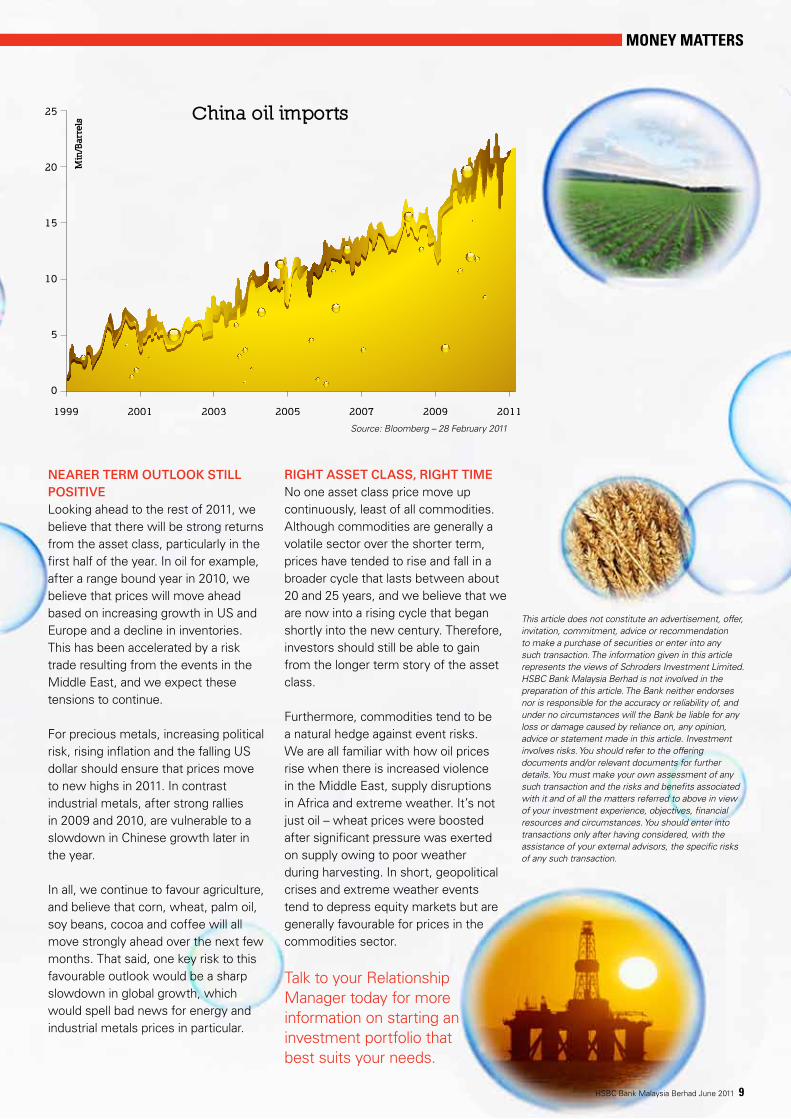

Long term dynamicS oF demand and SUppLy behind cUrrent priceSIn all three groups, agriculture, energy and metals, the needs of a growing population and a developing world economy show no signs of slowing down. The graph on the next page shows one small facet of this immensely powerful global trend – the growth in Chinese crude oil imports. There are thousands of other examples – some representing long-established markets, others new and emerging ones. In agriculture,

for example, it is clear that the surge of interest in the concept of bio-fuels is leading to strong and steady growth in demand for crops like corn (which is used to make ethanol).

The supply of many of the most important commodities is increasingly constrained by a combination of factors. The world’s available area of agricultural land, for example, is now shrinking, partly because of climate change. Some metals and some fossil fuels are becoming much more difficult, and expensive, to extract. Regulations resulting from environmental concerns are slowing the pace of development in other areas.

The outcome of this complex combination of factors is, simply, that providers have not been able to meet the growth in demand. This is an important reason to anticipate rising commodity prices – which in turn spell good news for investors.

commodities have seen a good run over 2010, and indeed, in recent months as well. This has raised concerns among investors, on whether the asset class is seeing a bubble?

HSBC Bank Malaysia Berhad June 2011 9

Money Matters

nearer term oUtLook StiLL poSitiveLooking ahead to the rest of 2011, we believe that there will be strong returns from the asset class, particularly in the first half of the year. In oil for example, after a range bound year in 2010, we believe that prices will move ahead based on increasing growth in US and Europe and a decline in inventories. This has been accelerated by a risk trade resulting from the events in the Middle East, and we expect these tensions to continue.

For precious metals, increasing political risk, rising inflation and the falling US dollar should ensure that prices move to new highs in 2011. In contrast industrial metals, after strong rallies in 2009 and 2010, are vulnerable to a slowdown in Chinese growth later in the year.

In all, we continue to favour agriculture, and believe that corn, wheat, palm oil, soy beans, cocoa and coffee will all move strongly ahead over the next few months. That said, one key risk to this favourable outlook would be a sharp slowdown in global growth, which would spell bad news for energy and industrial metals prices in particular.

right aSSet cLaSS, right timeNo one asset class price move up continuously, least of all commodities. Although commodities are generally a volatile sector over the shorter term, prices have tended to rise and fall in a broader cycle that lasts between about 20 and 25 years, and we believe that we are now into a rising cycle that began shortly into the new century. Therefore, investors should still be able to gain from the longer term story of the asset class.

Furthermore, commodities tend to be a natural hedge against event risks. We are all familiar with how oil prices rise when there is increased violence in the Middle East, supply disruptions in Africa and extreme weather. It’s not just oil – wheat prices were boosted after significant pressure was exerted on supply owing to poor weather during harvesting. In short, geopolitical crises and extreme weather events tend to depress equity markets but are generally favourable for prices in the commodities sector.

Talk to your Relationship Manager today for more information on starting an investment portfolio that best suits your needs.

This article does not constitute an advertisement, offer, invitation, commitment, advice or recommendation to make a purchase of securities or enter into any such transaction. The information given in this article represents the views of Schroders Investment Limited. HSBC Bank Malaysia Berhad is not involved in the preparation of this article. The Bank neither endorses nor is responsible for the accuracy or reliability of, and under no circumstances will the Bank be liable for any loss or damage caused by reliance on, any opinion, advice or statement made in this article. Investment involves risks. You should refer to the offering documents and/or relevant documents for further details. You must make your own assessment of any such transaction and the risks and benefits associated with it and of all the matters referred to above in view of your investment experience, objectives, financial resources and circumstances. You should enter into transactions only after having considered, with the assistance of your external advisors, the specific risks of any such transaction.

China oil imports

Source: Bloomberg – 28 February 2011

Min

/Bar

rels

Short Term Fund Performance

AdventurousHigh risk appetite, consider products which have the potential to earn returns substantially better than inflation. Capital values can fluctuate and may fall substantially below your original investment.

SpeculativeHigher risk appetite, consider products which have the potential to earn high returns. Capital values can fluctuate and may fall substantially below your original investment.

CautiousLow risk appetite, consider products which have the potential to outperform deposits over the medium term (3 years) and protect your capital against the effects of inflation.

Medium risk appetite, consider products which have the potential to outperform deposits over the medium to long term (5 years) and protect your capital against the effects of inflation.

Balanced

Talk to your Relationship Manager for more information on the above funds.

Top Performing Unit Trusts Funds distributed by HSBC (ranked by 1 Year Performance Growth %). Data is sourced from Lipper, as of 31st March 2011.

1 MONTH30 DAYS

ASSET TYPE*NAME 28/02/2011 to 31/03/2011

%

3 MONTHS91 DAYS

31/12/2010 to 31/03/2011

%

6 MONTHS182 DAYS

30/09/2010 to 31/03/2011

%

9 MONTHS270 DAYS

30/06/2010 to 31/03/2011

%

1 YEAR365 DAYS

31/03/2010 to 31/03/2011

%

Denotes Commodities Fund *Asset Type is based on Lipper Investment Management classification.

PRUdana al-ilham

CIMB-Principal Balanced

CIMB-Principal Equity Aggressive 3

Pacific Dana Aman

HwangDBS AIIMAN Growth

PRUequity income

Alliance Tactical Growth

AmPrecious Metals

Pacific Pearl

AmIttikal

CIMB-Principal Income Plus Balanced

RHB Mudharabah

HwangDBS Select Opportunity

OSK-UOB KLCI Tracker

PRUgrowth

OSK-UOB Smart Treasure

OSK-UOB Asean

OSK-UOB Energy

OSK-UOB Gold and General

Pacific Recovery

Equity

Mixed Assets

Equity

Equity

Equity

Equity

Equity

Equity

Equity

Equity

Mixed Assets

Mixed Assets

Equity

Equity

Equity

Equity

Equity

Bond

Equity

Equity

4.63

3.89

4.11

2.28

4.68

3.53

4.22

-0.64

5.25

4.11

2.49

3.51

4.83

3.71

5.30

5.66

6.30

3.69

0.35

3.47

4.29

3.10

2.42

1.83

4.71

3.54

1.56

-6.01

2.34

4.54

1.91

2.10

4.33

1.94

3.65

4.38

-0.21

16.66

-2.35

2.09

10.99

9.74

11.36

10.15

15.32

8.93

7.39

-2.16

8.74

12.83

5.90

8.92

16.06

6.11

12.64

13.80

9.53

28.66

10.68

11.46

21.62

20.60

22.17

19.16

24.51

19.72

19.09

6.90

18.00

18.63

13.65

14.35

24.29

18.76

26.46

26.07

24.52

37.47

19.29

21.79

20.23

19.80

19.59

19.30

18.59

18.57

17.57

17.11

16.82

16.15

14.20

13.78

18.09

18.19

25.13

23.75

23.43

22.45

22.35

20.92

HSBC Fund Selection

Investors are advised to read and understand the contents of the respective product offering documents or prospectus before investing. Among others, investors should consider the fees and charges involved. The price of units and distributions payable, if any, may go down as well as up.

10 HSBC Bank Malaysia Berhad June 2011

funD PerforMance

Are your investments dancing to Brazil's economic Samba?

Discover new investment opportunities in Brazil, South America's bustling economic powerhouse through AmAdvantage Brazil2. Its Target Fund, HSBC Global Investment Funds Brazil Equity, is the largest Brazil equity fund in Hong Kong with Assets Under Management of USD2.7 billion3. It was also recognised as a strong performing Brazil equity fund in Hong Kong with an annual return of 16.2%p.a.4.

Brazil has proven its resilience by being one of the first emerging markets to begin recovery from the economic crisis5. Major events to be hosted by Brazil, the 2014 FIFA World Cup and 2016 Summer Olympics are also key drivers in boosting infrastructure spending and expansion, with investments projected to hit USD169 billion in 2010-136. Brazil's GDP for 2011 is forecast at 4.4% with robust domestic consumption driving economic growth7.

Now, you can uncover new investment opportunities through HSBC’s global expertise, which is supported by over 217 investment experts and USD443.5 billion in Assets Under Management worldwide8. Let your investments benefit from our global experience today.

Find out more about AmAdvantage Brazil2. Live life without boundaries.

Visit your nearest HSBC branchCall 1300 88 9393Log on to hsbcpremier.com.my

Issued by HSBC Bank Malaysia Berhad (Company No.127776-V) ("HSBC Bank"). 1 As of 9 May 2011, there are no other Brazil equity unit trust funds offered in Malaysia as reflected in Lipper Malaysia's list of unit trust funds, available at TheEdge Malaysia. 2 A product of AmInvestment Services Berhad, exclusively distributed by HSBC Bank. 3 Derived from data produced by Morningstar Inc at www.hk.morningstar.com, retrieved as at 10 May 2011 and HSBC Global Investment Funds Brazil Equity Fund Factsheet dated April 2011 issued by HSBC Global Asset Management (Hong Kong) Limited, available at www.assetmanagement.hsbc.com/hk. 4 Derived from data produced by Morningstar Inc at www.sg.morningstar.com, as at 31 March 2011. The Target Fund’s growth rate in US dollar terms based on class AD in Hong Kong over the past one year (31 March 2010 - 31 March 2011). 5 International Monetary Fund Survey Magazine, Emerging Market Economies, BRICs Drive Global Economic Recovery, 22 July 2009 6 Morgan Stanley Blue Paper "Brazil Infrastructure - Paving the Way", 5 May 2010. Based on the exchange rate quoted by Banco Central do Brasil at the offer rate of USD1 = BRL1.6207 for 12 May 2011, available at www.bcb.gov.br. 7 World Bank Global Economic Prospects, published 12 January 2011. 8 HSBC Global Asset Management, 31 December 2010, available at www.assetmanagement.hsbc.com. We recommend that you read and understand the contents of AmMutual Prospectus for AmAdvantage Brazil dated 5 May 2011 that is registered with the Securities Commission (“Prospectus”), who takes no responsibility for its contents, before investing. For copies of the Prospectus, please visit HSBC Bank Malaysia Berhad’s branches or AmInvestment Services Berhad’s website at www.ammutual.com.my. Any issue of units to which the prospectus relates will only be made on receipt of an application form referred to and accompanying a copy of the prospectus. You should be aware that investments in unit trust funds carry risks. An outline of some of the risks is contained in the Prospectus. The specific risks associated to the fund includes currency risk, risk of a passive strategy and investment manager risk as contained in the Prospectus. Unit prices and income distribution, if any, may rise or fall. Past performance of a fund is not indicative of future performance. Please consider the fees and charges involved before investing. Neither HSBC Bank nor AmInvestment Services Berhad guarantees any returns on the investments.

AmAdvantage Brazil is a product of AmInvestment Services Berhad, exclusively distributed by HSBC Bank Malaysia Berhad.

First Brazil equity fund in Malaysia1.

Exclusively at HSBC.

22°S – Rio de Janeiro, Brazil

12 HSBC Bank Malaysia Berhad June 2011

Personal finance

Take a look around you. How many people do you see with their noses buried in their mobile phones? People are more glued to their mobile phones than ever, thanks to the arrival of smartphones.

Say Helloto

mobile banking

HSBC Bank Malaysia Berhad June 2011 13

Personal finance

Furthermore, an article by GigaOM.com reported that signs are pointing towards smartphones overtaking personal computers (PC) as the preferred internet device. GigaOM.com, a leading business and technology online news portal reports that mobile Internet usage is ramping up substantially faster than desktop Internet usage. This is derived from the observation by Mary Meeker, Managing Director at Morgan Stanley and head of the global technology research team in her latest report “State of the Internet” on the adoption rates of iPhone/iPod touch as compared to that of internet services provider, AOL (formerly known as America Online) and browser, Netscape in the early 1990s. The adoption of the Apple devices is taking place more than 11 times faster than that of AOL, and several times as fast as that of Netscape.2

Rising along with this trend is mobile banking. According to Bank Negara’s

Financial Stability and Payment Systems Report 2008, mobile banking subscribers nearly doubled from 0.3 million as at end of 2007 to 0.5 million as at end of 2008, while its transaction value rose from RM21.2mil in 2007 to RM71.5mil in 2008.3

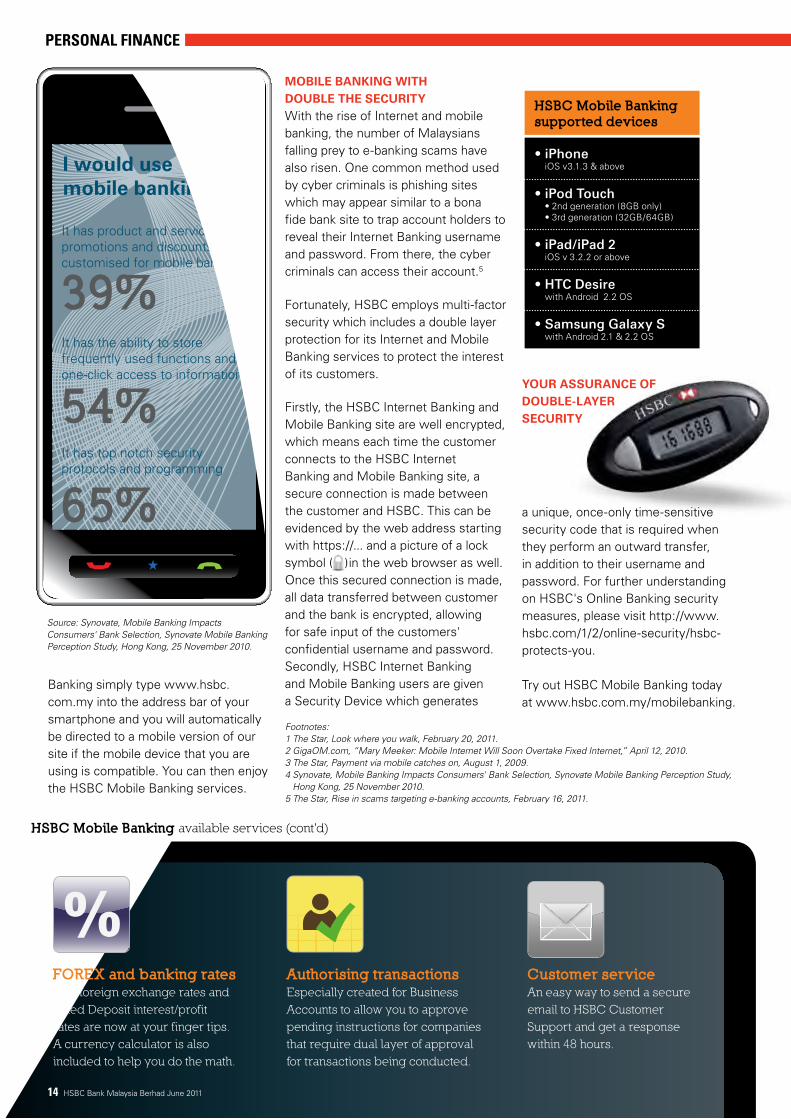

The convenience and ease of use are among reasons smartphone users have taken to mobile banking. Synovate, in its study of mobile banking trends in Hong Kong have found that among early adopters of mobile banking, close to half (49%) have used it in the past 12 months to buy and sell stocks, one in three (32%) has bought and sold foreign currencies, and one in four (23%) has purchased other banking

HSBC Mobile Banking available services

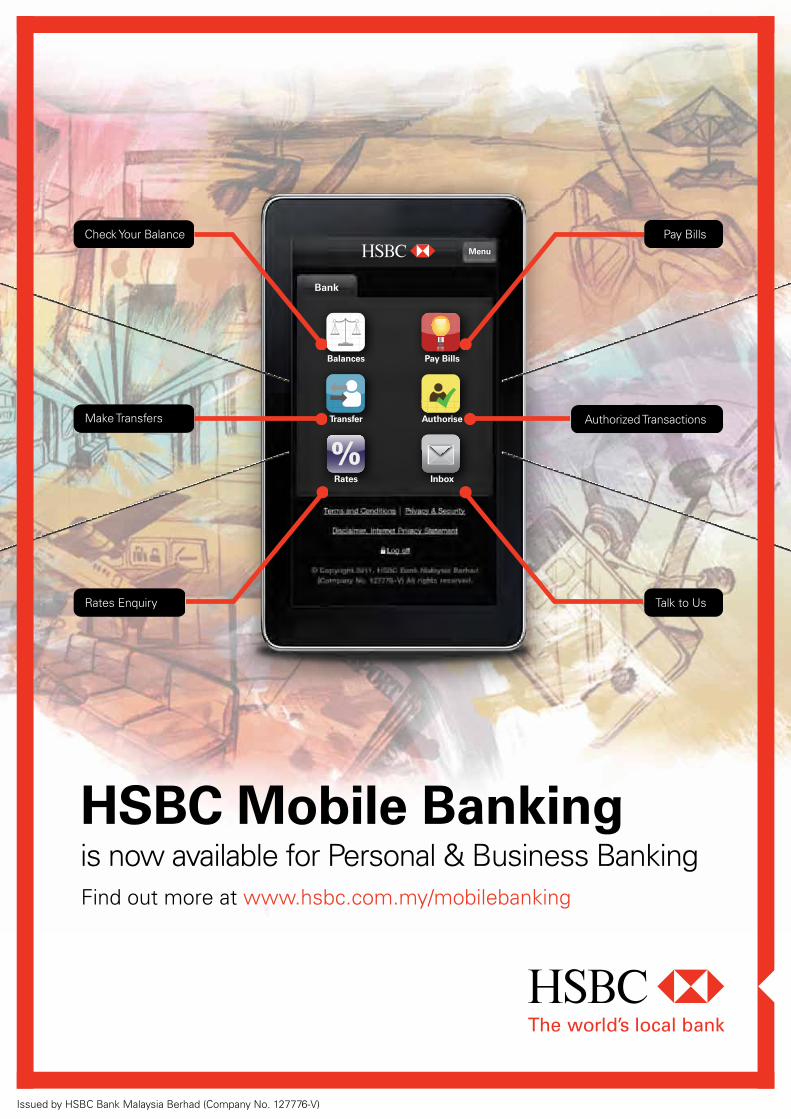

Checking of balancesQuick access to all your HSBC accounts, your transaction history and account details.

Payment of bills Conveniently pay bills using this service on your smartphone wherever you are.

Transferring fundsMake interbank transfers easily, even when you are out of the country. You'll also get instant confirmation and acknowledgment of transfers made.

…close to half (49%) have used mobile banking in the past 12 months to buy and sell stocks…

The trend can only go up as two in five (38%) mobile phones sold in Malaysia

in 2010 were smartphones, according to a retail study by research company,

GfK Malaysia which was reported in The Star. The study also revealed that

consumers snapped up over 24% more mobile phones in 2010 compared with 2009

and that sales of smartphones have consistently increased every month.1

products through mobile banking. In communicating with bank customers, mobile phones have proven effective, with over 40% of mobile banking users surveyed having looked up banking-related promotions and discounts through this channel.4 exPerienCe banking on the MoVe with hsbC Mobile banking The convenience and ease of banking via your mobile phone is now available with HSBC Mobile Banking. The first step is to ensure that you have registered for Internet Banking at www.hsbc.com.my through your PC and accepted the Internet Banking Product Terms and Conditions. After you have registered for Internet

14 HSBC Bank Malaysia Berhad June 2011

Personal finance

Banking simply type www.hsbc.com.my into the address bar of your smartphone and you will automatically be directed to a mobile version of our site if the mobile device that you are using is compatible. You can then enjoy the HSBC Mobile Banking services.

Footnotes:1 The Star, Look where you walk, February 20, 2011. 2 GigaOM.com, “Mary Meeker: Mobile Internet Will Soon Overtake Fixed Internet,” April 12, 2010.3 The Star, Payment via mobile catches on, August 1, 2009. 4 Synovate, Mobile Banking Impacts Consumers' Bank Selection, Synovate Mobile Banking Perception Study,

Hong Kong, 25 November 2010.5 The Star, Rise in scams targeting e-banking accounts, February 16, 2011.

Mobile banking with double the seCurity With the rise of Internet and mobile banking, the number of Malaysians falling prey to e-banking scams have also risen. One common method used by cyber criminals is phishing sites which may appear similar to a bona fide bank site to trap account holders to reveal their Internet Banking username and password. From there, the cyber criminals can access their account.5

Fortunately, HSBC employs multi-factor security which includes a double layer protection for its Internet and Mobile Banking services to protect the interest of its customers.

Firstly, the HSBC Internet Banking and Mobile Banking site are well encrypted, which means each time the customer connects to the HSBC Internet Banking and Mobile Banking site, a secure connection is made between the customer and HSBC. This can be evidenced by the web address starting with https://... and a picture of a lock symbol ( )in the web browser as well. Once this secured connection is made, all data transferred between customer and the bank is encrypted, allowing for safe input of the customers' confidential username and password. Secondly, HSBC Internet Banking and Mobile Banking users are given a Security Device which generates

Source: Synovate, Mobile Banking Impacts Consumers' Bank Selection, Synovate Mobile Banking Perception Study, Hong Kong, 25 November 2010.

FOREX and banking ratesLive foreign exchange rates and Fixed Deposit interest/profit rates are now at your finger tips. A currency calculator is also included to help you do the math.

Authorising transactions Especially created for Business Accounts to allow you to approve pending instructions for companies that require dual layer of approval for transactions being conducted.

Customer service An easy way to send a secure email to HSBC Customer Support and get a response within 48 hours.

HSBC Mobile Banking available services (cont'd)

HSBC Mobile Banking supported devices

•iPhone iOS v3.1.3 & above

•iPodTouch • 2nd generation (8GB only) • 3rd generation (32GB/64GB)

•iPad/iPad2 iOS v 3.2.2 or above

•HTCDesire with Android 2.2 OS

•SamsungGalaxyS with Android 2.1 & 2.2 OS

I would usemobile banking if...

It has product and servicepromotions and discountscustomised for mobile banking

It has the ability to store frequently used functions and one-click access to information

It has top notch securityprotocols and programming

39%

54%

65% a unique, once-only time-sensitive security code that is required when they perform an outward transfer, in addition to their username and password. For further understanding on HSBC's Online Banking security measures, please visit http://www.hsbc.com/1/2/online-security/hsbc-protects-you.

Try out HSBC Mobile Banking today at www.hsbc.com.my/mobilebanking.

your assuranCe of double-layer seCurity

Balances Pay Bills

Transfer Authorise

Rates Inbox

Menu

BankBank

Make Transfers

Rates Enquiry

Pay Bills

Authorized Transactions

Talk to Us

Check Your Balance

Issued by HSBC Bank Malaysia Berhad (Company No. 127776-V)

HSBC Mobile Bankingis now available for Personal & Business BankingFind out more at www.hsbc.com.my/mobilebanking

Personal finance

16 HSBC Bank Malaysia Berhad June 2011

Every mention of “HSBC” refers to HSBC Bank Malaysia Berhad and HSBC Amanah Malaysia

Berhad collectively. Individually, HSBC Bank Malaysia Berhad (Company No. 127776-V) will be

referred to as “HSBC Bank” and HSBC Amanah Malaysia Berhad (Company No. 807705-X)

will be referred to as “HSBC Amanah”.

Get convenient access to your HSBC account via MEPS’ Shared ATM Network

1 You may transfer up to RM5,000 per day to any HSBC banking account. However, for Credit Cards with secondary account(s) encoded into the same card, the limit for transfers between accounts [credit card account and secondary account(s)] on the same card is RM20,000.

2 The SMS alert service is provided on a best effort basis and is subject to telco service provider’s coverage and availability. Terms and conditions and Tariff and Charges apply, and are available at www.hsbc.com.my.

3 Tariff & Charges apply and are available at www.hsbc.com.my (HSBC Premier customers enjoy a waiver on any fees or charges for any cash withdrawals at any HSBC Group ATMs overseas).

for an account holder, an Automated Teller Machine (ATM) is indispensable. Just slot in the ATM card, punch in your password and the ATM transforms into a mini-bank – where you can check

your balances, withdraw cash, apply for a cheque book, transfer funds and much more.

Take advantage of the convenience of your HSBC ATM card locally and around the world with the services listed on your right.

Need cashon the go?

IN MALAYSIAYour HSBC ATM card can be used at HSBC ATMs, HOUSe ATM Network and now also available at MEPS' Shared ATM Network anywhere in Malaysia.

Over 10,000MEPS SharedATMs nationwideServices include: Interbank cash withdrawal (at a transaction cost of RM 4 per transaction)

Balance Inquiry

HSBC ATMs Services include: Cash Withdrawal (up to RM5,000 per day)

Credit Card Cash Advance Funds Transfer1

Cheque Book Request Statement Request New Share (IPO) Application (not available for HSBC Amanah)

Multiple Account Access with the same HSBC ATM Card (up to 3 accounts may be linked under 1 HSBC

ATM Card)

PIN Change Account Activity Enquiry Language Selection (English, Bahasa Malaysia or Mandarin)

HOUSeServices include: Interbank cash withdrawal (at a transaction fee of RM1 per transaction)

Balance Inquiry

OVERSEAS Security measure for your peace of mindAn instant SMS notification2 will be sent to your locally registered Malaysian mobile number when a cash withdrawal transaction is performed with your HSBC ATM card overseas.

Cash withdrawals3 are also available at any of the following networks.

IN MALAYSIAYour HSBC ATM card can be used at HSBC ATMs, HOUSe ATM Network and now also available at MEPS' Shared ATM Network anywhere in Malaysia.

Over 10,000MEPS SharedATMs nationwideServices include: Interbank cash withdrawal (at a transaction cost of RM 4 per transaction)

Balance Inquiry

HSBC ATMs Services include: Cash Withdrawal (up to RM5,000 per day)

Credit Card Cash Advance Funds Transfer1

Cheque Book Request Statement Request New Share (IPO) Application (not available for HSBC Amanah)

Multiple Account Access with the same HSBC ATM Card (up to 3 accounts may be linked under 1 HSBC

ATM Card)

PIN Change Account Activity Enquiry Language Selection (English, Bahasa Malaysia or Mandarin)

HOUSeServices include: Interbank cash withdrawal (at a transaction fee of RM1 per transaction)

Balance Inquiry

OVERSEAS Security measure for your peace of mindAn instant SMS notification2 will be sent to your locally registered Malaysian mobile number when a cash withdrawal transaction is performed with your HSBC ATM card overseas.

Cash withdrawals3 are also available at any of the following networks.

Issued by HSBC Bank Malaysia Berhad (Company No. 127776-V)

Get convenient access to your funds anywhere in Malaysia with MEPS.

Now available for your banking needs.With over 10,000 MEPS’ Shared ATM Network nationwide, you can choose to make interbank cash

withdrawals (at a Transaction Fee of RM4 per transaction) or balance inquiries at any MEPS participating banks. HSBC Premier and HSBC Advance Account Holders can enjoy a cash rebate promotion on

MEPS Withdrawals for a limited period until 14 July 2011.*

* Details on the cash rebate promotion are as follow:

HSBC Premier Account Holder

First 3 successful MEPS Withdrawals are entitled to cash rebate of the Transaction Fee 4th and subsequent successful MEPS

Withdrawal: a Transaction Fee of RM4 will be charged per MEPS Withdrawal.

Cash Withdrawal via MEPS

HSBC Advance Account Holder

First 2 successful MEPS Withdrawals are entitled to cash rebate of the Transaction Fee 3rd and subsequent successful MEPS

Withdrawal: a Transaction Fee of RM4 will be charged per MEPS Withdrawal.

Log-on to www.hsbc.com.my for MEPS Promotion Campaign Terms & Conditions.

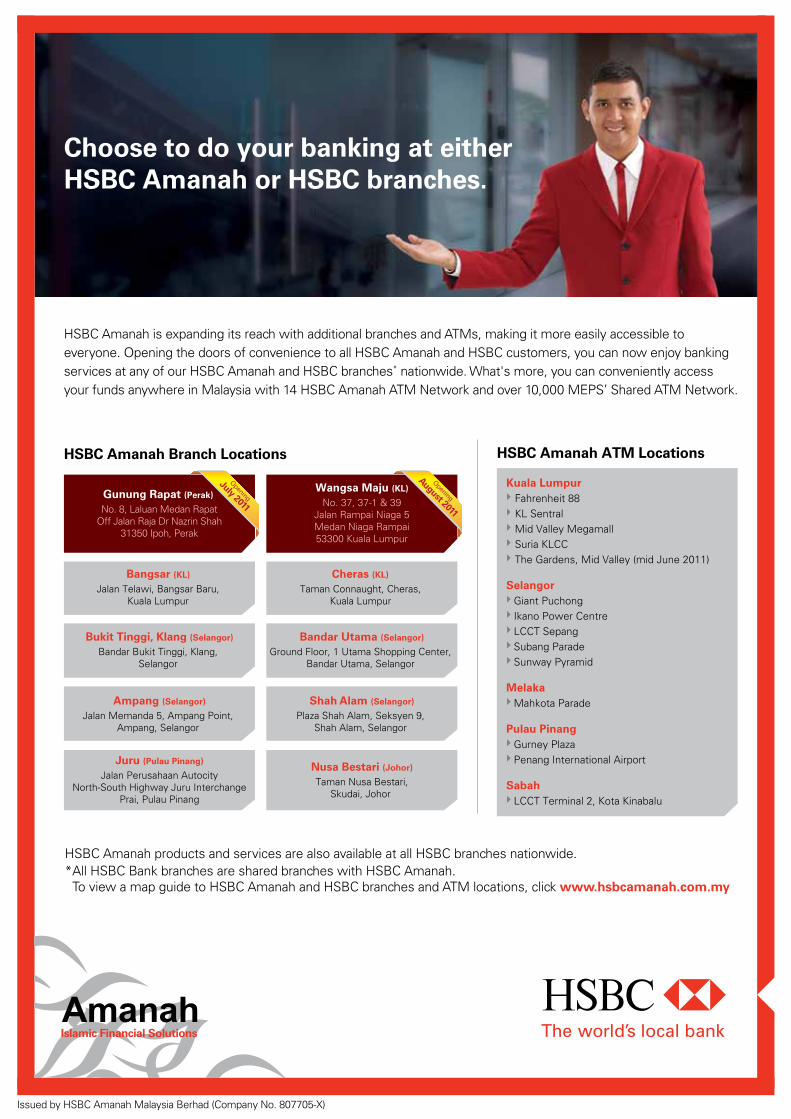

Choose to do your banking at either HSBC Amanah or HSBC branches.

Issued by HSBC Amanah Malaysia Berhad (Company No. 807705-X)

HSBC Amanah Branch Locations HSBC Amanah ATM Locations

Bangsar (KL)

Jalan Telawi, Bangsar Baru, Kuala Lumpur

Nusa Bestari (Johor)

Taman Nusa Bestari, Skudai, Johor

Cheras (KL) Taman Connaught, Cheras,

Kuala Lumpur

Gunung Rapat (Perak)

No. 8, Laluan Medan RapatOff Jalan Raja Dr Nazrin Shah

31350 Ipoh, Perak

Bandar Utama (Selangor)

Ground Floor, 1 Utama Shopping Center, Bandar Utama, Selangor

Ampang (Selangor)

Jalan Memanda 5, Ampang Point, Ampang, Selangor

Shah Alam (Selangor)

Plaza Shah Alam, Seksyen 9, Shah Alam, Selangor

Juru (Pulau Pinang)

Jalan Perusahaan AutocityNorth-South Highway Juru Interchange

Prai, Pulau Pinang

Bukit Tinggi, Klang (Selangor)

Bandar Bukit Tinggi, Klang, Selangor

Wangsa Maju (KL)

No. 37, 37-1 & 39Jalan Rampai Niaga 5Medan Niaga Rampai53300 Kuala Lumpur

Opening

July 2011

Opening

August 2011

HSBC Amanah products and services are also available at all HSBC branches nationwide. * All HSBC Bank branches are shared branches with HSBC Amanah.

To view a map guide to HSBC Amanah and HSBC branches and ATM locations, click www.hsbcamanah.com.my

HSBC Amanah is expanding its reach with additional branches and ATMs, making it more easily accessible to everyone. Opening the doors of convenience to all HSBC Amanah and HSBC customers, you can now enjoy banking services at any of our HSBC Amanah and HSBC branches* nationwide. What's more, you can conveniently access your funds anywhere in Malaysia with 14 HSBC Amanah ATM Network and over 10,000 MEPS’ Shared ATM Network.

Kuala Lumpur Fahrenheit 88 KL Sentral Mid Valley Megamall Suria KLCC The Gardens, Mid Valley (mid June 2011)

Selangor Giant Puchong Ikano Power Centre LCCT Sepang Subang Parade Sunway Pyramid

Melaka Mahkota Parade

Pulau Pinang Gurney Plaza Penang International Airport

Sabah LCCT Terminal 2, Kota Kinabalu