your financial future a guide to managing your finances

TRANSCRIPT

YOUR FINANCIAL FUTURE

A GUIDE TO MANAGING YOUR FINANCES

LET’S DISCUSS…

• Saving

• Checking/Controlled Spending Accounts

• Budgeting

• Obtaining Credit and Credit Score

• Safeguarding Your Identity

BEFORE WE GET STARTED…

Does anyone know where to go for help with basic financial services?

(ex. savings accounts, checking accounts, loans)

SAVING

• Saving is setting money aside for the future, usually in an account for safekeeping.

• Savings accounts generally earn a small amount of interest, so you can even make money on the money you save.

SAVING

• Saving is like paying yourself – when you pay your bills, think of your savings as another bill!• Saving gives you money for

unexpected expenses, emergencies, future purchases (car or home), etc.

SAVING

CHECKING & CONTROLLED SPENDING ACCOUNTS

CHECKING ACCOUNTS

• Paper checks • Debit card• Register to track credits & debits• Monthly Statement• Beware of NSFs• Overdraft protection available

CONTROLLED SPENDING ACCOUNTS• Debit card – no paper checks• Purchases strictly limited to

funds on the card• No risk of NSFs• No overdraft protection needed• Great for students!

BUDGETING

IMPORTANCE OF BUDGETING• Helps you determine where you

will spend your money. • Allows you to have enough money

to pay your bills each month.• Allows you to save for expensive

items without the use of credit cards or loans.

BUDGET COMPONENTSIncome (Money Coming In)

Expenses (Money Going Out)• Fixed• Variable• Periodic

BUDGETING STEPS

1) Calculate your income (money coming in)

Let’s discuss Gross and Net Pay!

Gross pay is the amount you’re paid before deductions like taxes and Social Security.

Net pay is after the deductions. So….

BUDGETING STEPSIf your salary is $8.00 per hour and you work 10 hours per week, your gross income is $80.00 per week.

But, your take home pay (net) will be less because of deductions!

Base your budget on what you get – net.

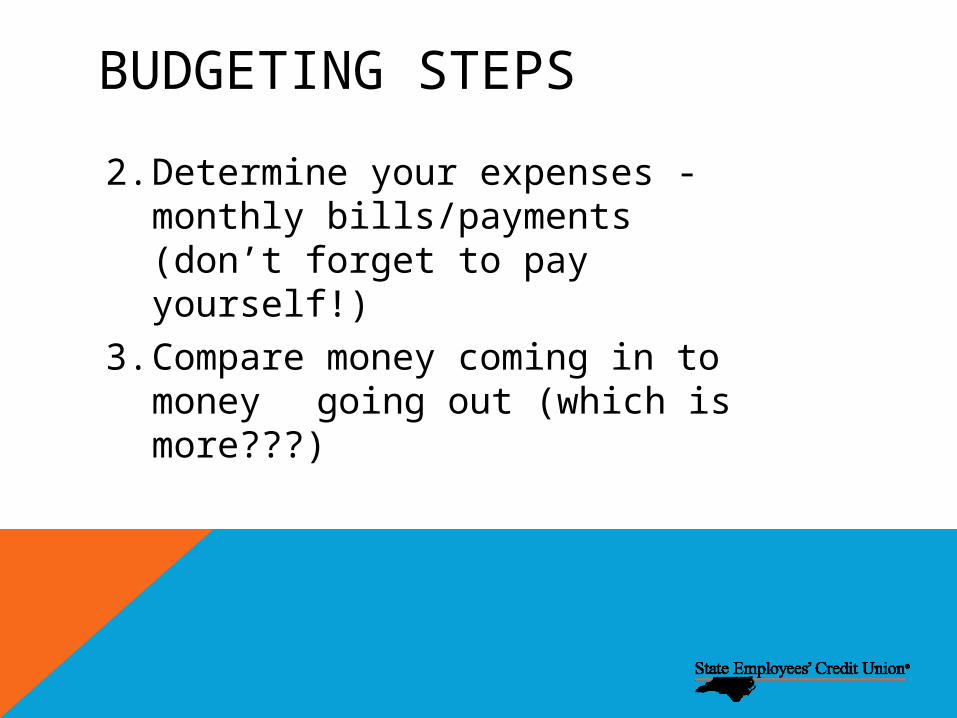

BUDGETING STEPS

2. Determine your expenses - monthly bills/payments (don’t forget to pay yourself!)

3. Compare money coming in to money going out (which is more???)

BUDGETING STEPS

4. Put your budget in print, so you can review it and make adjustments as your income and expenses change.

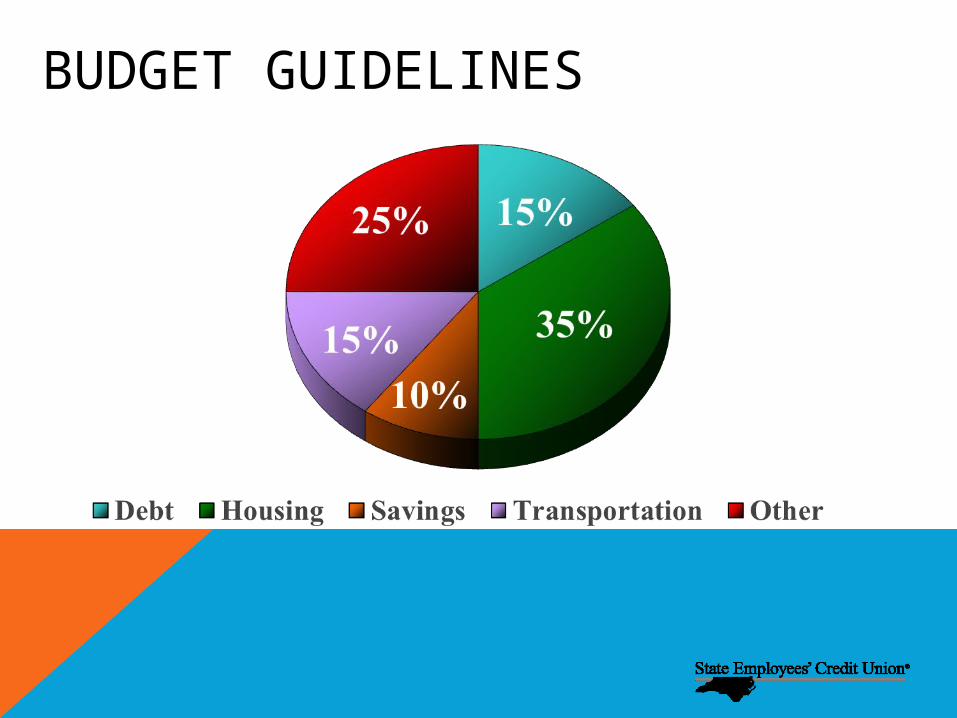

Now let’s look at standard budget guidelines to help with the future…

BUDGET GUIDELINES

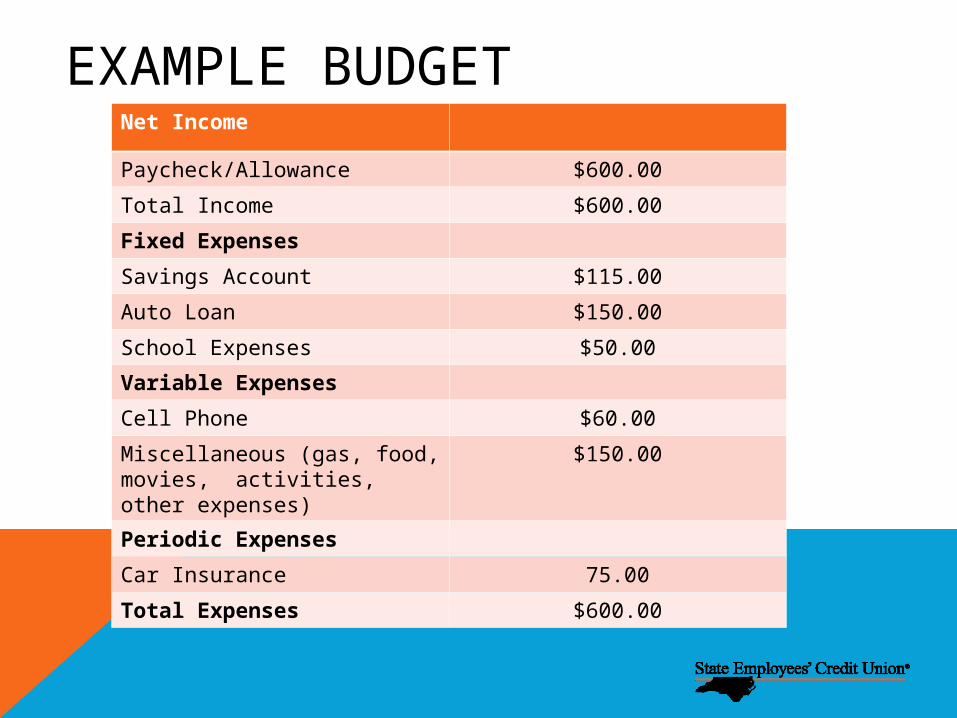

EXAMPLE BUDGETNet Income

Paycheck/Allowance $600.00

Total Income $600.00

Fixed Expenses

Savings Account $115.00

Auto Loan $150.00

School Expenses $50.00

Variable Expenses

Cell Phone $60.00

Miscellaneous (gas, food, movies, activities, other expenses)

$150.00

Periodic Expenses

Car Insurance 75.00

Total Expenses $600.00

BUDGETING RESOURCES

• Money Management Workbooks

• Computer Software

• Cell Phone Applications

CREDIT

WHAT IS CREDIT?• Money loaned, for a fee (interest),

that must be repaid. • Allows you to buy now and pay

later.• Includes credit cards, installment

loans, student loans, and mortgages.

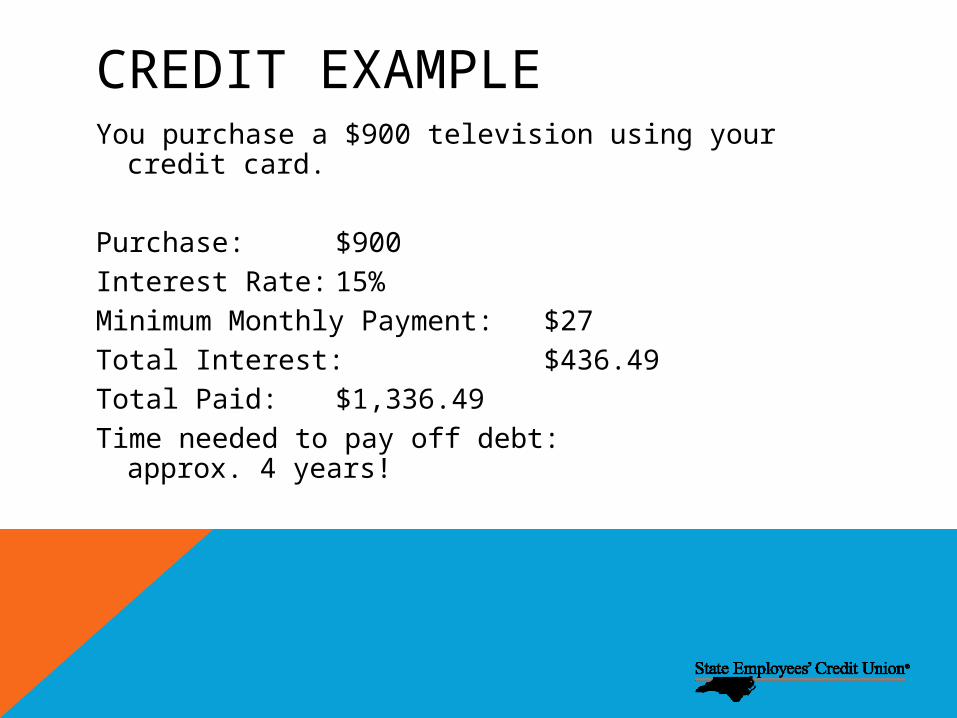

CREDIT EXAMPLEYou purchase a $900 television using your credit

card.

Purchase: $900Interest Rate: 15%Minimum Monthly Payment: $27Total Interest: $436.49Total Paid: $1,336.49Time needed to pay off debt: approx. 4 years!

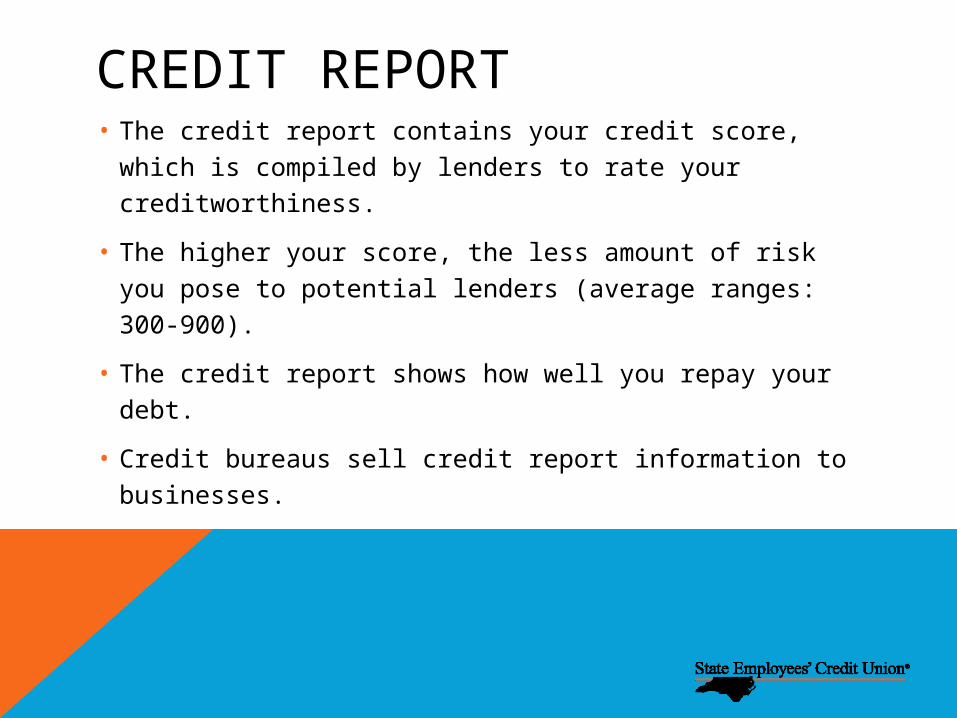

CREDIT REPORT• The credit report contains your credit score, which is

compiled by lenders to rate your creditworthiness.

• The higher your score, the less amount of risk you pose to potential lenders (average ranges: 300-900).

• The credit report shows how well you repay your debt.

• Credit bureaus sell credit report information to businesses.

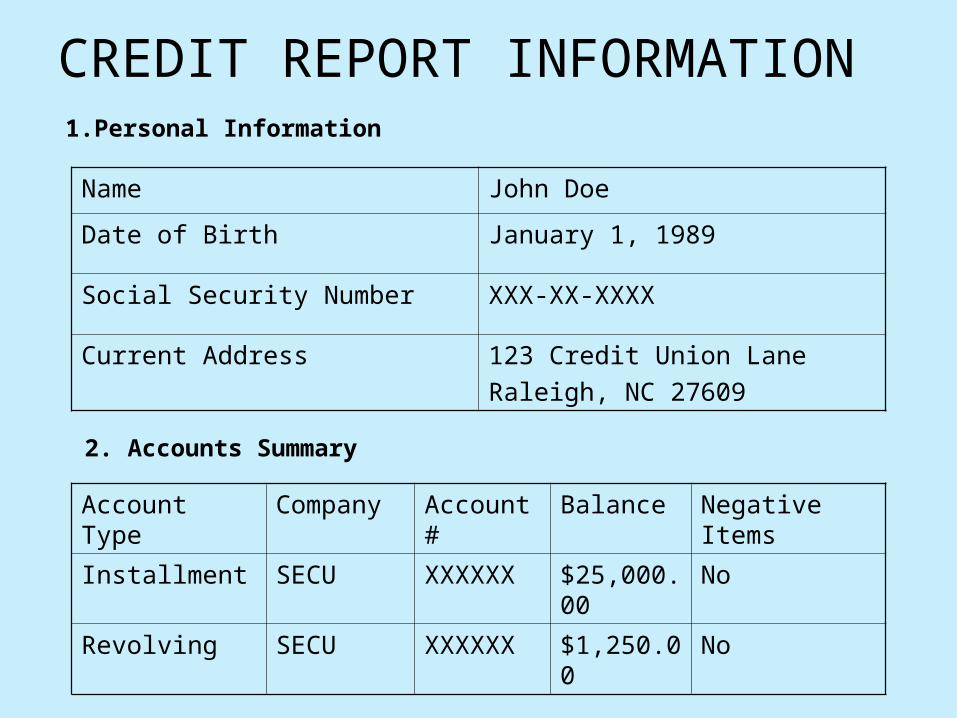

Account Type Company Account #

Balance Negative Items

Installment SECU XXXXXX $25,000.00

No

Revolving SECU XXXXXX $1,250.00

No

Name John Doe

Date of Birth January 1, 1989

Social Security Number XXX-XX-XXXX

Current Address 123 Credit Union LaneRaleigh, NC 27609

CREDIT REPORT INFORMATION

2. Accounts Summary

1.Personal Information

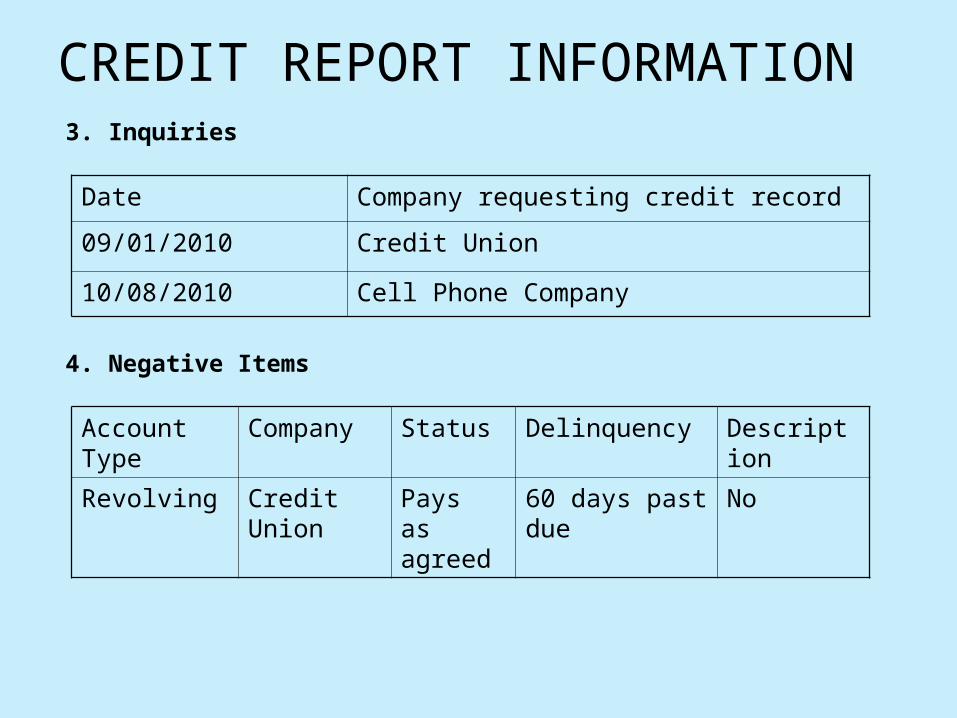

Account Type

Company Status Delinquency Description

Revolving Credit Union

Pays as agreed

60 days past due

No

Date Company requesting credit record

09/01/2010 Credit Union

10/08/2010 Cell Phone Company

CREDIT REPORT INFORMATION

4. Negative Items

3. Inquiries

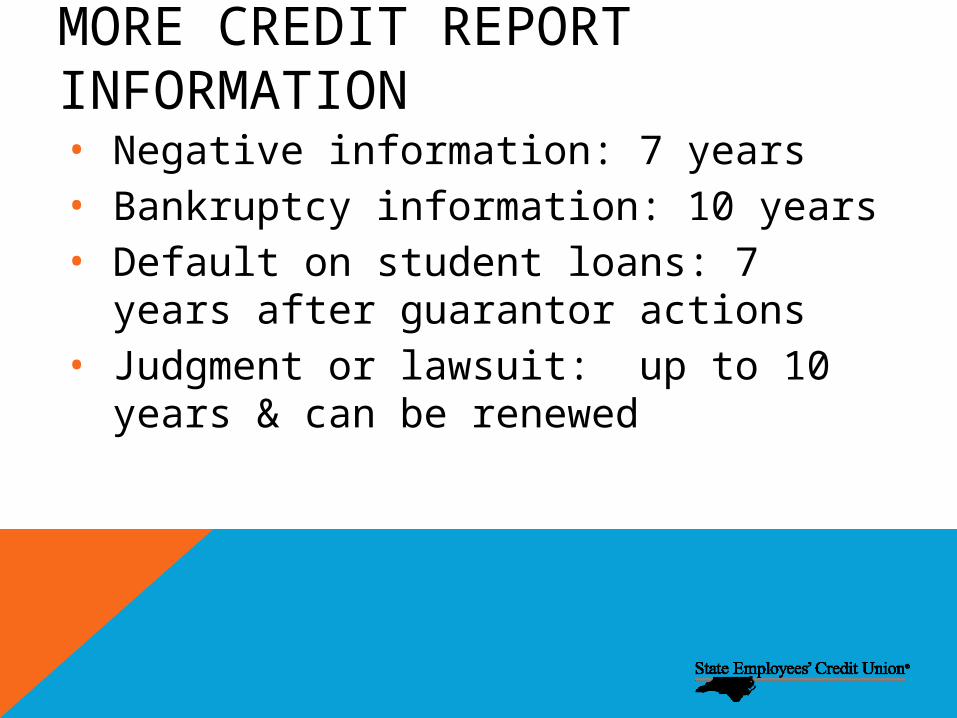

MORE CREDIT REPORT INFORMATION• Negative information: 7 years• Bankruptcy information: 10 years• Default on student loans: 7 years after

guarantor actions• Judgment or lawsuit: up to 10 years &

can be renewed

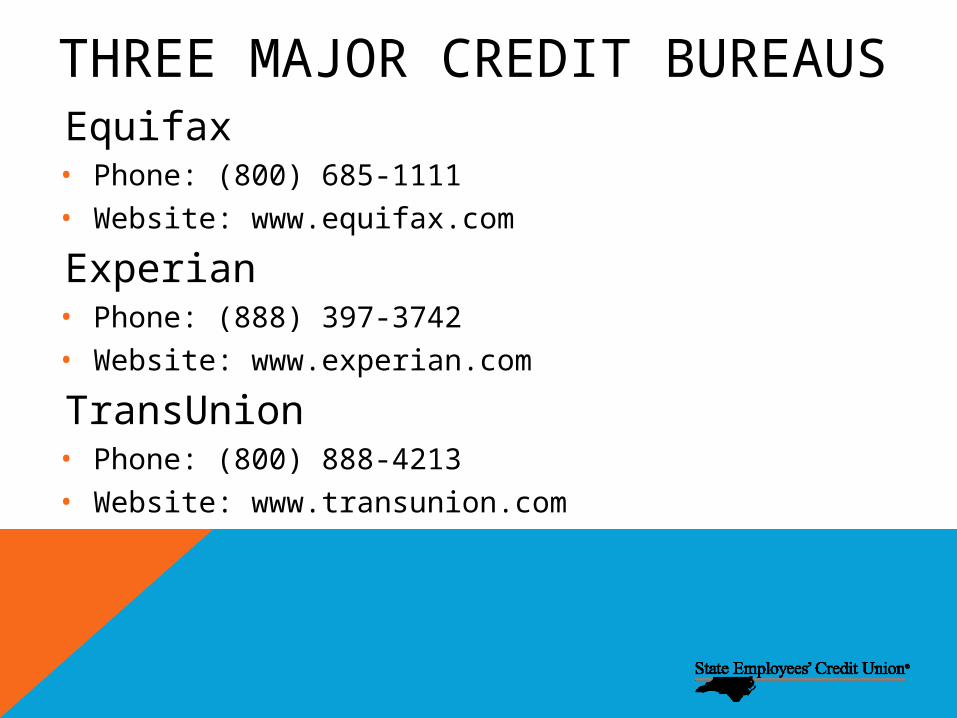

THREE MAJOR CREDIT BUREAUSEquifax• Phone: (800) 685-1111• Website: www.equifax.com

Experian• Phone: (888) 397-3742• Website: www.experian.com

TransUnion• Phone: (800) 888-4213• Website: www.transunion.com

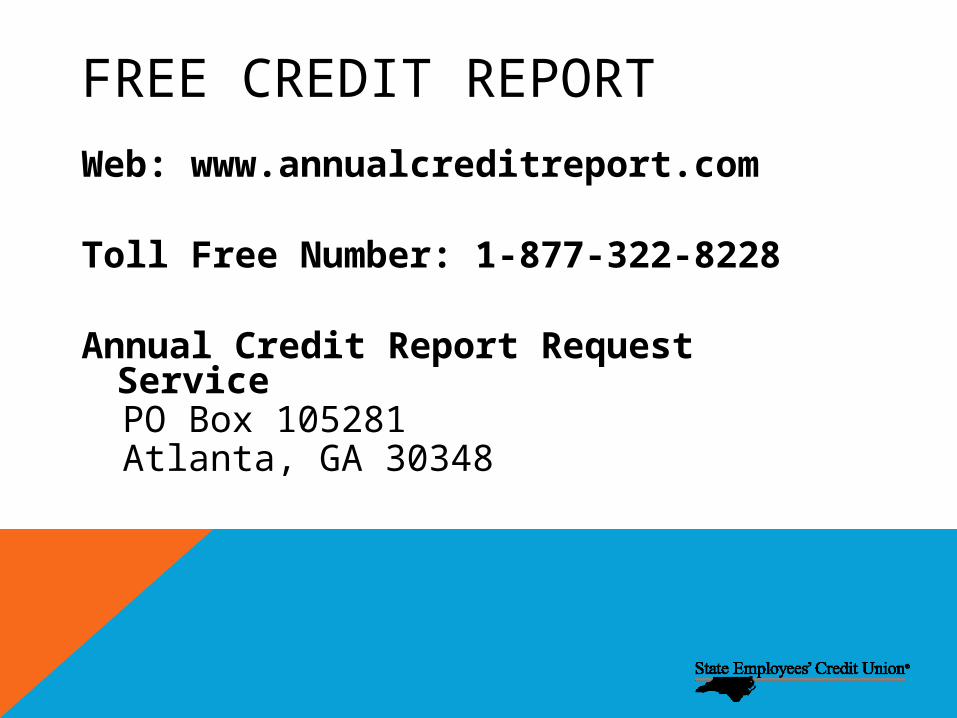

FREE CREDIT REPORT

Web: www.annualcreditreport.com

Toll Free Number: 1-877-322-8228

Annual Credit Report Request Service

PO Box 105281Atlanta, GA 30348

SAFEGUARDING YOUR IDENTITY

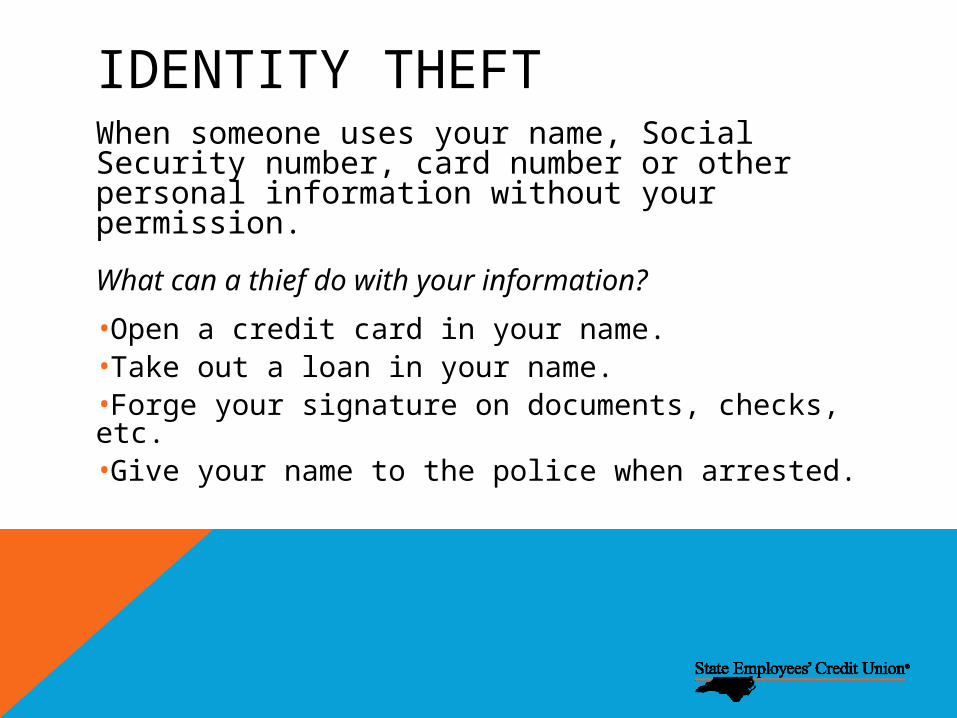

IDENTITY THEFT When someone uses your name, Social Security number, card number or other personal information without your permission.

What can a thief do with your information?

•Open a credit card in your name.•Take out a loan in your name.•Forge your signature on documents, checks, etc.•Give your name to the police when arrested.

POTENTIAL DANGERS OF ID THEFT • Lost and damaged credit.• Difficulty opening a savings account at

some financial institutions.• Difficulty applying for a driver’s license.• Difficulty getting accepted into college.• Inability to secure a job.

SAFE PRACTICESFOR YOUR PERSONAL INFORMATION

• Make sure personal information is secure where you live, at school (and work, if applicable) and do not share your passwords.• You should never share personal

account information.

• When you provide personal information to a company, your information may be shared with others; however, many let you “opt out” of having information shared.

• Insist that creditors safeguard your personal information and do not share with others.

SAFE PRACTICESFOR YOUR PERSONAL INFORMATION

IF YOU ARE A VICTIM…

You Have Rights,

Take Action Immediately!

QUESTIONS?