ys;j;alu - clcclc.lk/m/reports/clc_ar_201415.pdf · ys;j;alu “hithawathkama” ... to soar into...

TRANSCRIPT

ys;j;alu“ H i t h a w a t h k a m a ”

Commercial Leasing & Finance PLC | Annual Report 2014/15

Com

mercial L

easing & F

inance PL

C | A

nnual Report 2014/15

Building relationships, building lives.

Contents

For a more interactive report, go online at

http://www.clc.lk

Who We are / 2Highlights of 2014/15 / 4Financial Highlights / 6Chariman’s Message / 10Director’s Review / 12CEO’s Message / 14The Board of Directors / 18Management Team / 23Regional Management Team / 26Management Discussion & Analysis / 30Branch Network / 35Financial Review / 36Sustainability Report / 40Corporate Governance / 43Risk Management / 70Directors Report / 76Audit Committee Report / 80Integrated Risk Management Committee Report / 81Remuneration Committee Report / 82Nomination Committee Report / 83Related Party Transaction Review Committee Report / 84Directors’ Statement on Internal Control over Financial Reporting / 85Chief Executive Officer’s and Chief Financial Officer’s Responsibility Statement / 86Independent Auditors’ Report / 87Statement of Profit or Loss and Other Comprehensive Income / 88Statement of Financial Position / 89Statement of Changes in Equity / 90Statement of Cash Flows / 92Notes to the Financial Statements / 94Shareholder Information / 169Summarised Quarterly Statistics / 171Ten Year Summary / 172Sources and Distribution of Income / 173Statement of Value Added / 174Glossary Terms / 175Notice of Meeting / 179Notes / 180Form of Proxy / 183Corporate Information / IBC

ys;j;alu“ H i t h a w a t h k a m a ”

Building relationships, building lives.

We don’t see ourselves as just another finance company. Instead, our business is designed to build better lives, by offering myriad financial products and services that empower all Sri Lankan communities. Today, we are proud to have established solid relationships with our customers across the island through our corporate philosophy of “Hithawathkama”. We believe that we understand Sri Lankan’s needs better than most and we’ve used our unique insights to shape many lifestyles, understand people’s dreams, goals and aspirations for the future.

Building on 27 years of expertise and sound strategy, Commercial Leasing & Finance PLC (CLC) now boasts strong fundamentals in finance and corporate governance, backed by the strength of the LOLC Group. Today, we are committed to the integration of long-term sustainability and good governance in order to improve individual livelihoods and drive national development.

And that is how we will foster the spirit of “Hithawathkama”, as we continue to build strong relationships and better lives for the thousands of Sri Lankans we pledge to serve.

“Hithavathkama”

At CLC we have adopted the word Hithavathkama to sum up our corporate philosophy; a word that describes how we create value for our customers and partners, helping them grow by enhancing their wealth.

In this context, hitha signifies the warmth, trust and confidence of our stakeholder relationships, while wathkama indicates the financial returns and value we create for them each day.

2Commercial Leasing & Finance PLC

ys;j;alu

Commercial Leasing & Finance PLC (CLC) is one of Sri Lanka’s leading Non Banking Financial Service Providers offering solutions ranging from leasing, fixed deposits, savings, loans, flexi cash to factoring. With 58 customer touch points spread across the country, CLC has become a trusted brand, synonymous with stability and dependability, playing an invaluable role as a key catalyst in financial empowerment.

CLC will continue to grow and expand with its unique operating philosophy “Hithawathkama” which encapsulates how the trust and progress of all our stakeholders will continue to be the priority in our hearts and minds.

About Us

WhoWe are

3Annual Report 2014/15

To soar into the future, giving wings to the dreams, hopes and aspirations of our people and everyone who has a stake in the success of our enterprise.

To forge ahead to reach new frontiers, to touch new horizons, seeking new challenges and exploring new opportunities.

Together with our people with diverse strengths, committed to achieving personnel excellence and the continuous growth of our enterprise.

In order to make our vision a reality, we always strive:

To provide innovative financial solutions of highest possible quality at an optimum value.

To ensure utmost customer focus and dedication to superior customer service.

To provide best returns to our stakeholders through the strength of our customer, strategic partner and employee satisfaction.

To serve our customers with utmost care.

To serve our customers professionally.

To do work with utmost integrity.

Be performance driven.

To work as a team and treat fellow colleagues as one family.

Core Values

Vision

Mission

4Commercial Leasing & Finance PLC

ys;j;alu

Highlights of 2014/15

ATM Launch

Facebook Launch

Winner of the Silver Award at the SLITAD People’s Development Awards 2014.

Gampola Branch Opening

Grandpass Branch Opening Dehiwala Branch Opening

5Annual Report 2014/15

Minuwangoda Branch Opening

Long Service Awards

3W Consultancy Training held at Thulhiriya

Wattala Branch Opening

Branch Performance Awards

Sports Day

6Commercial Leasing & Finance PLC

ys;j;alu

Financial Highlights

Company

For the year ended 31st March 2011 2012 2013 2014 2015

Performance indicators (Rs. Mn)Interest income 3,402 5,317 5,996 7,514 7,590 Interest expense 1,309 2,167 2,515 3,039 2,406 Net interest income 2,093 3,150 3,481 4,475 5,184 Profit before tax 741 3,245 1,603 1,289 1,728 Profit after tax 664 2,964 1,168 936 1,426

Executions (leases and loans) 12,926 15,262 11,232 18,593 22,762 Factoring funds in use 2,954 3,005 2,859 2,231 2,778

Financial position(Rs. Mn)Total assets 21,351 26,398 27,229 32,934 42,385Net lending portfolio 18,339 24,101 24,985 27,570 32,982Outstanding borrowings 14,880 16,974 14,660 14,369 20,095Deposits from customers - 385 2,962 7,534 9,381 Shareholders funds 3,695 6,763 7,837 8,856 10,115

Key indicatorsEarnings per share(Adjusted)(Rs. per share) 0.10 0.46 0.18 0.15 0.22 Net asset value per share(Adjusted)(Rs. per share) 0.58 1.06 1.23 1.39 1.59

Interest cover(times) 1.57 2.49 1.63 1.42 1.72Debt to equity ratio (times) 4.03 2.57 2.25 2.47 2.91 Return on equity (%) 23.20 56.69 16.01 11.21 15.03Return on average total assets (%) 3.92 12.42 4.36 3.11 3.79Non performing ratio (%) 0.76 2.80 2.98 2.44 1.96

Capital adequacyCore capital ratio (%) - 25.01 29.53 27.63 28.27Total risk weighted capital ratio (%) - 25.01 29.53 27.63 25.57

7Annual Report 2014/15

Total Assets to ROA

0

10,000

20,000

30,000

40,000

50,000

0

2

4

6

8

10

12

14

Total assetsReturn on average total assets

2011 2012 2013 2014 2015

Rs. Mn %

Shareholders' Funds and ROE

0

2,000

4,000

6,000

8,000

10,000

12,000

0

10

20

30

40

50

60

Shareholders fundsReturn on equi�

2011 2012 2013 2014 2015

Rs. Mn %

Deposits from customers

0

2,000

4,000

6,000

8,000

10,000

2012 2013 2014 2015

Rs. Mn

Interest income to interest expense

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Rs. Mn

Interest incomeInterest expense

2010/11 2011/12 2012/13 2013/14 2014/15

Net lending portfolio

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2011 2012 2013 2014 2015

Rs. Mn

Executions

0

5,000

10,000

15,000

20,000

25,000

2010/11 2011/12 2012/13 2013/14 2014/15

Rs. Mn

8

HowWe buildBetter Lives

Management ReviewsChairman’s Message | Director’s Review | CEO’s Message | The Board of Directors | Management Team | Regional Management Team

Backed by strong financial capabilities, we build better lives...We are helping to create better lifestyles by generating wealth, which in turn drive national development.

With a solid growth strategy and strong operating performance, we’re driving national development, generating wealth and creating better lifestyles.

ys;j;alu“ H i t h a w a t h k a m a ”

Annual Report 2014/15

10Commercial Leasing & Finance PLC

ys;j;alu

Ishara NanayakkaraChairman

Chairman’s Message

11Annual Report 2014/15

It is my pleasure to welcome you to the 23rd Annual General meeting of Commercial Leasing & Finance PLC (CLC) and to present to you the Annual Report and Audited Financial Statements for the year ended 31st March 2015. In the year under review, the Company achieved an excellent performance and surpassed last year’s, to record its best results to date.

CLC’s revenue reached Rs. 8 Billion contributing a significant 18% to LOLC Group’s revenues whilst Profit Before Tax grew by 34% to Rs. 1.7 Billion. Profit After Tax reached Rs. 1.4 Billion growing by 52% over the previous year. It is noteworthy that our performance primarily represents the performance of the second half of the year due to a lacklustre industry performance in the first half.

The year was a momentous one for another reason. Under the Central Bank directed consolidation programme for the NBFI sector, CLC acquired BRAC Lanka Finance PLC, a microfinance entity which caters to the lowest income segments in the country at the grassroots level. In December 2013, LOLC parented with BRAC Bangladesh, the largest NGO of the world to acquire Nanda Investments Finance PLC. which was then renamed as BRAC Lanka Finance PLC. Although now a 94.35% owned subsidiary of CLC, BRAC will stand alone as an entity which caters to the lower end of the micro finance segment with a unique model of its own. With women empowerment as one of its primary objectives, BRAC Lanka focuses on lending exclusively to women entrepreneurs with 95% of its workforce comprising women. In addition to directly empowering via employment, having a female workforce also facilitates better communication and understanding and hence more enduring partnerships with its key stakeholder group.

Becoming a member of the LOLC Group has had an inspiring impact on BRAC’s performance, within a mere span of 6 months. The Company was able to achieve a remarkable turnaround, to record a Profit Before Tax of Rs. 195.7 Million from a profit of Rs. 21.7 Million during the previous year, thus recording a profit growth of 799%. BRAC’s total portfolio also grew considerably by 180% to Rs. 3 Billion whilst the total disbursement during the year was Rs. 4.8 Billion compared with Rs. 1 Billion in the previous year. The establishment and implementation of our inhouse IT systems, standards and management practices, and the transfer of expertise and knowledge of LOLC’s experience in the Microfinance sector, combined with the access to new funding lines, which saw a decline in the cost of funds; were key factors which supported this turnaround during the year and will place BRAC on a sound platform to reach greater heights.

CLC’s financial products have primarily benefited the micro sector of the economy. We have thus been the incubator for many micro enterprises and progressively, the facilitator of their progression to small to medium scale (SME) enterprises. Moreover, Brand CLC has become a household name in the multitude of rural and semi urban locations we operate in. This has enabled CLC to become an integral part of the empowerment and enrichment of these communities. The new entrant BRAC Lanka currently has 82 customer centres and a customer base of 70,000. Thus the inclusion of BRAC has added a grassroots level market segment to CLC’s portfolio, offering many synergies and providing an ideal opportunity to widen our growth prospects in the years ahead.

CLC’s success has been based on a win-win model -of facilitating economic development in Sri Lanka. It will continue to expand in the micro and SME sectors in the next few years and capitalize on the numerous opportunities that still remain untapped. The Company also plans to become a ‘One stop shop’ for financing requirements of all our customers such as Capital revenue, Working Capital revenue, and Leasing products.

CLC is one of the few Sri Lankan finance companies to be funded by leading international funding agencies such as FMO, the Development bank of Netherlands, Proparco the French Development Agency and DEG a subsidiary of the German Development Bank KFW. These agencies together account for 22 % of your Company’s funding and the partnerships are a valuable endorsement of the role we play in Sri Lanka’s economic progress. Furthermore, these partnerships also stand as testimony to the high standards of governance and management we strive for at CLC. We also appreciate the opportunity these relationships offer to continuously raise the bar for ourselves- whether it be in technical know how or governance or by being abreast of the latest in best practices. CLC will continue to strengthen the current relationships and also look to establish new sources of funding.

Acknowledgements :I would like to convey my sincere appreciation to the Board for their guidance, and continual support and to the team at CLC whose unreserved commitment, tireless effort and talents have been the cornerstone of the Company’s success. My sincere gratitude also extends to our customers, funding partners, Business Introducers, shareholders, and all other stakeholders for their constant support as we look to the year ahead with renewed vigour..

Ishara NanayakkaraChairman

21st May, 2015

12Commercial Leasing & Finance PLC

ys;j;alu

Director’s ReviewKapila JayawardenaDirector

13Annual Report 2014/15

The Economic Environment :

Demonstrating resilience in the face of domestic as well as external challenges, the Sir Lankan economy continued on the momentum we’ve experienced since 2013; to grow at a robust 7.4%, compared with a growth of 7.2% in 2013 and 6.3% in 2012. Accordingly, GDP Per Capita increased to US Dollars 3,625 in 2014 from US Dollars 3,280 in the previous year. The economy was driven by domestic consumption expenditure that constitutes the largest share of aggregate demand, while investments, particularly on construction, also provided an impetus to the economic expansion during the year. Sri Lankan government policy to a large extent remained stable, and the low inflation levels and a low interest rate regime in 2014 were largely conducive to business. Moreover the exchange rate also remained stable to support growth in our business. Strong macro economic growth is expected to continue in 2015; which as per the IMF’s projections is to average 6.5% per year until 2020.

Performance :

The Company’s record performance was reflective of all indicators; with profits reaching the highest, the balance sheet growing to the largest ever and customer base and products reaching the highest. Several internal measures contributed to this growth during the year. For one, significant investments in training and development of our people with a focus on soft skills development was a key factor. Moreover, the Company also introduced branch performance awards to reward the best performing teams, which helped enhance performance whilst further encouraging the team spirit which is valued at CLC.

CLC’s acquisition of BRAC Lanka Finance during the year was another significant milestone which would create many synergies for CLC and BRAC and enable the Company to enhance the value we create for all our stake holders. The

LOLC Group’s shared services model, a key component of its agile business model, also continued to be a key strength which CLC will continue to leverage on, to provide customised state of the art IT solutions for a competitive advantage.

CLC thus looks to the next year and beyond with much optimism, and I am confident that year 2015/16 will see us surpass this year’s achievements and be another record breaking year. CLC will look to create and meet new opportunities to keep expanding its potential as a financial services provider. Towards this end, the development of new products and new distribution channel, will take priority in the year ahead.

Appreciation :

I would like to convey my sincere appreciation to my colleagues on the Board for their support and guidance. My congratulations and appreciation to the entire team at CLC, for their unreserved effort and commitment which propel the company to keep surpassing their own achievements and to constantly raise the bar for themselves and the Company. My sincere appreciation also to our customers, funding partners, shareholders, business introducers and other stakeholders for their constant support and confidence in brand CLC and its potential to create value for all its stakeholders.

Kapila JayawardenaDirector

21st May, 2015

Dear Shareholder, The year has been a momentous one with a remarkable performance by CLC and one which was well supported by a conducive economic environment. The economic environment is discussed at length in the MD&A that follows later on in this report, and let me hence provide a brief overview of a few salient points.

14Commercial Leasing & Finance PLC

ys;j;alu

Krishan ThilakaratneDirector/Chief Executive Officer

CEO’s Message

15Annual Report 2014/15

Dear Stakeholder, It is my pleasure and privilege to share with you the performance and outlook of Commercial Leasing & Finance PLC (CLC) as it ends an year with another remarkable performance which has surpassed previous year’s, to be its highest ever.

Performance highlights :The year under review was record breaking in many ways. Our portfolio grew by 20% to reach Rs. 33 Billion during the year, whilst revenue reached Rs. 8 Billion contributing 18% to LOLC Group’s revenues and 21% of the Group’s PBT. Profit Before Tax grew by 34% to Rs. 1.7 Billion and Profit After Tax reached Rs. 1.4 Billion representing an increase of 52%. CLC’s capital surpassed Rs. 10 Billion during the year. Our NPA ratio also continued to be exceptional at 1.96% as at 31st March 2015, compared with the industry average of 6.7%.

Furthermore, the Company was able to maintain gearing well below industry averages and norms at 2.9 times, vis a vis an industry average which is over 7 times.

The Company’s public deposits amounted to Rs. 9.4 Billion during the year accounting for 32% of its funding. Moreover, we also continued to have a healthy mix in our funding portfolio with bank borrowings constituting 46% and overseas borrowings making up another 22%, a fact which underpins our stability and growth potential.

Another key highlight of the year was CLC’s acquisition of BRAC Lanka Finance to become a 94.35% owned subsidiary of CLC. Although this initiative took place under the Central Bank’s directive for consolidation in the MBFI sector, CLC recognised it to be rife with opportunities to harness as well create many synergies with CLC. For us it was thus more than mere consolidation of two entities but an opportunity for CLC to expand its portfolio to include a new income category.

Our Factoring arm, Commercial Factors also performed well during the year achieving a portfolio growth of 33.8% to reach 2.4 Billion in 2014/15 from Rs. 1.8 Billion in the previous year. The contribution from the branches to the Factoring portfolio grew by a significant 136% to Rs 985 Million whilst the number of clients utilising the Factoring portfolio at branches increased by 73% to 218 as at 31st March 2015, compared with a portfolio of Rs. 417 Million and 126 clients as at 31, March 2014. Our strategy of

pioneering Factoring into outstation areas to reach a market which was hitherto been neglected, has proven to be a success and Commercial Factors will continue to expand the factoring business in the regions.

Context of performance : CLC’s performance during the year was enabled by many factors. An environment of low interest rates and inflation and a stable exchange rate combined with favourable weather patterns during the second half of the year which facilitated agricultural growth, were key environmental factors which supported our performance during the year. The favourable macro economic conditions contributed to the high liquidity in the banking industry, which in turn saw a high credit demand encouraged by low interest rates.

A Brand Value - That Creates Value Our internal strength of being the preferred brand in the market segment, due to the quality of our service and the value we provide, was a key factor which enabled us to capitalize on the numerous opportunities in this conducive environment. The Company has now extended its footprint to 58 branches with 5 new branches being opened during the year. CLC continues to be a very strong brand, and particularly so in the outstation market. We see much potential to further grow our brand in the metropolitan areas and in partnership with key businesses such as leading automobile vendors.

CLC’s business activities have been based on its philosophy that lending should primarily be for economic value creation rather than to finance consumption. Hence, our marketing activities engage customers and prospective customers who would seek our products for a purpose such as to upgrade their business or create a source of income generation.

It is noteworthy that our lending portfolio is well diversified into many different asset classes, many different industries, customer segments, demographics and geographic regions. We are thus proud to have been able to add value to many different sectors in the country and particularly in to segments which are neglected by the larger financial

16Commercial Leasing & Finance PLC

ys;j;alu

institutions. CLC has thus, emerged as one of the leading financial institutions in the country, by making a real impact on the real livelihoods and real economy of the country.

Our focus on ensuring that our Information Technology is state of the art and the best combined with the shared services of LOLC Group will continue. During the year under review, CLC signed up with HNB –which has one of the largest ATM networks in the country, to facilitate our deposit customers to transact using HNB’s island wide ATM network from 2015. The year ahead will also see us offer our customers internet based online transactions including opportunity for utility bill payments; taking us closer to our objective to be the financial service provider offering the most convenience.

We are proud to note that the Company enjoys a staff retention ratio of over 90% which is well above industry average and is a preferred employer in the industry. The commitment, loyalty and talents of our people will continue to be the key factor in propelling the company forward.

Future outlook In addition to the offer of advanced solutions and convenience, our deposit clients benefit from a good return and the unmatched safety of their investments. As CLC is today one of the strongest and safest brands, with an equity of Rs. 10 Billion, an A- ICRA Lanka rating and a well diversified asset portfolio.

The low interest environment is expected to continue during the remainder of 2015, thus auguring well for a continued growth in credit demand and capital investments in the country.

CLC will continue to innovate and introduce new products and expand its footprint, whilst investing in new channels of distribution and establishing new business partnerships to create value to all our stakeholders.

CEO’s Message

CLC’s business activities have been based on its philosophy that lending should primarily be for economic value creation rather than to finance consumption. Hence, our marketing activities engage customers and prospective customers who would seek our products for a purpose such as to upgrade their business or create a source of income generation.

17Annual Report 2014/15

The synergies that we enjoy from being a member of the LOLC Group, and the trust earned by brand CLC as the first choice in the micro and SME market in Sri Lanka, will continue to be key strengths which we will leverage on.

AcknowledgementI would like to convey my sincere appreciation to the Board of Directors for their guidance and the trust and confidence placed in CLC and its people. My appreciation also extends to the entire team that makes up CLC, all our business partners, funding agencies, banks and other Financial institutions and the regulators for their continuous support and our customers for the continuous loyalty and patronage.

Our journey has been one made possible, in unison with all our stakeholders and one that will continue to be driven by the goal of benefiting all our stakeholders and adding value to the lives of all Sri Lankans.

Krishan ThilakaratneDirector/Chief Executive Officer

21st May, 2015

18Commercial Leasing & Finance PLC

ys;j;alu

The Board of Directors

Mr. Ishara Nanayakkara Chairman

Mrs. Kalsha Amarasinghe Non Executive Director

Mr. Kapila Jayawardena Non Executive Director

Mr. Priyantha Fernando Senior Independent Non Executive Director

19Annual Report 2014/15

Miss. Chrishanthi EmmanuelDirector, LOLC Corporate Services (Pvt) Ltd, Secretaries

Dr. Harsha Cabral, PC Independent Non Executive Director

Mr. Krishan Thilakaratne Director/CEO

20Commercial Leasing & Finance PLC

ys;j;alu

Mr. I C NanayakkaraNon-Executive Director / Chairman

Mr. Ishara Nanayakkara joined the Board of Commercial Leasing & Finance PLC in June 2008. He is an astute businessman who holds directorial positions in many corporates and conglomerates in Sri Lanka. He joined the Board of Lanka ORIX Leasing Company PLC in January 2002 and presently holds the position of Deputy Chairman. He is also the Deputy Chairman of Lanka ORIX Finance PLC.

He chairs the Board of LOLC Micro Credit Limited and BRAC Lanka Finance PLC backed by the professional expertise in the industry for over a decade. He also serves on the Board of PRASAC Micro Finance Institution; Cambodia’s largest Micro Finance Institution. His expertise in micro finance in the region is evident in the recent investment in Thaneakea Phum Cambodia Ltd (TPC Micro Finance), the 5th largest microfinance company in Cambodia along with the green field operations in Myanmar via Myanmar Micro Finance Company Ltd of which he is the founding Chairman.

Mr. Nanayakkara is the Deputy Chairman of Seylan Bank PLC, a premier commercial bank in the country. His exposure in general and life insurance through LOLC Insurance Company Ltd, stock brokering through LOLC Securities Ltd, factoring through LOLC Factors Ltd, micro financing and Islamic finance, manifests his vision of catering the entire value chain of the finance sector.

His Business philosophy based on sustainable development has made LOLC enter into many new business ventures with high potential for growth in all three spheres, economic, social and environmental.

Accordingly he serves the Board of Sierra Constructions Ltd, AgStar PLC, Lanka Century Investment PLC and Associated Battery Manufacturers (Cey) Ltd in line with the Group’s vision to expand into strategic investments such as Agriculture & Plantation, Trading & Manufacturing, Leisure and Construction.

His need to diversify LOLC group into a key conglomerate that operates in the growth sectors of the economy is further reflected through the vital role played by him in Brown & Company PLC and Browns Investments PLC as the Executive Chairman. Browns Group is a renowned

conglomerate with leading market position in trade, leisure, manufacturing, consumer appliances and agriculture equipment.

Mr. Nanayakkara was appointed as the Chairman of FLC Holdings PLC, FLC Hydro Power PLC, and as a Director in Pussellawa Plantations Ltd, Ceylon Estate Teas (Pvt) Ltd and FLMC Plantations (Pvt) Ltd subsequent to the recent acquisition.

He holds a diploma in Business Accounting from Australia.

Mr. W D K Jayawardena Non-Executive DirectorMr. Kapila Jayawardena counts over thirty years’ experience in Banking, Financial Management and Corporate Management. He joined the Board of Commercial Leasing & Finance PLC in June 2008. Mr. Jayawardena was appointed as the Group Managing Director/CEO of Lanka ORIX Leasing Co., PLC in 2007. He was the former CEO/Country Head of Citibank Sri Lanka & Maldives.

Mr. Jayawardena has played a pivotal role in the banking sector contributing to the financial market reforms development and regularly advising regulators on prudential requirements and has widespread experience in introducing innovative financial service products to the market.

LOLC Group is one of the largest conglomerates in Sri Lanka with presence in diversified industries such as Financial Services, Trading, Manufacturing, Construction, Leisure and Renewable Energy.

As an individual with extensive international and domestic financial experience, Mr. Jayawardena was a key member of the following committees:

• ChairmanSriLankaBank’sAssociation(SLBA)2003/2004

• MemberoftheFinancialServicesReformsCommittee(FSRC) 2003/ 2004

• DirectorofLankaClearandwasinstrumentalincompleting the automated clearing project for the Sri Lankan banking industry 2004

• PresidentoftheAmericanChamberofCommerceSriLanka 2006/2007

• MemberoftheinauguralSovereignratingsteamforSriLanka

• MemberoftheNationalCouncilofEconomicDevelopment (NCED)

The Board of Directors

21Annual Report 2014/15

• BoardMemberoftheUnitedStates-SriLankaFulbrightCommission

Presently, Mr. Jayawardena holds Chairmanship/directorship in the following companies:

• LankaORIXLeasingCompanyPLC–GroupManagingDirector/CEO

• LankaORIXFinancePLC-Chairman

• LOLCInsuranceCompanyLimited-Chairman

• LOLCSecuritiesLimited-Chairman

• EdenHotelsLankaPLC-Chairman

• PalmGardenHotelsPLC-Chairman

• LOLCGeneralInsuranceLtd-Chairman

• LOLCMicroCreditLtd-Director

• CommercialLeasing&FinancePLC-Director

• Brown&Co.,PLC-Director

• BrownsInvestmentsPLC-Director

• SeylanBankPLC-Director

• BRACLankaFinancePLC-Director

• RiverinaResorts(Pvt)Ltd-Director

• FLCHoldingsPLC-Director

• PussellawaPlantationsLimited-Director

• FLCHydroPowerPLC-Director

• FLMCPlantations(Pvt)Ltd-Director

Qualifications : Master of Business Administration, American University of Asia, Fellow of the Institute of Bankers, Sri Lanka, Associate of the Institute of Cost and Executive Accountants, London.

Mrs. K U Amarasinghe Non-Executive Director

Mrs. Kalsha Amarasinghe was appointed to the Board in June 2008. She holds an Honours Degree in Economics.

She serves on the Boards of Lanka ORIX Leasing Company PLC, LOLC Micro Credit Ltd, LOLC Insurance Co. Ltd, Palm Garden Hotels PLC and Eden Hotel Lanka PLC. She also serves as a Director on the Boards of Lanka ORIX Finance PLC, Brown & Company PLC, Browns Investments PLC, Riverina Resorts (Pvt) Ltd, FLC Hydro Power PLC, FLC Holdings PLC, Pussellawa Plantations Ltd, Melfort Green Teas (Private) Ltd and FLMC Plantations (Pvt) Ltd

Mr. P D J Fernando Senior Independent Non-Executive Director

Mr Priyantha Fernando was appointed to the Board of CLC in March 2012.

Mr Fernando has more than 35 years of experience at the Central Bank where he rose to the position of the Deputy Governor. He was the Deputy Governor of the Central Bank in 2010/2011, in charge of the Financial System Stability and the Corporate Services clusters. Mr Fernando has extensive experience and expertise in the fields of Banking and Financial Sector particularly at the policy making levels in financial regulation and supervision, Information technology, national accounting, macro-economic analysis and statistics, finance and fund management. At the Central Bank he was the chairman of the Financial Stability Committee, member of the Monetary policy Committee, member of the Risk Management Committee and Chairman of the National Payment Council. He also functioned as the secretary to the Monetary Board during 2009/2010.

He was an ex-officio board member in several regulatory organizations namely the Securities Exchange Commission, the Insurance Board of Sri Lanka, the Chairman of the Credit Information Bureau, Institute of Bankers –Sri Lanka and have also served as a Board Member at Employers Trust Fund, Lanka Clear (Pvt) Ltd and Lanka Financial Services Bureau.

During his career, he has initiated and spearheaded several key projects of national importance, especially in the area of developing the infrastructure for the national payments and settlement system.

Mr. Fernando has served a number of committees at national level covering a range of subjects representing the Central Bank.

He has been appointed the Chairman of Golden Key Credit Card Company and currently serves in the boards of the Union Bank of Sri Lanka PLC, Hambana Petro Chemicals (Pvt) Ltd, Taprobane Holdings Ltd, Ceylon Leather Products PLC, Commercial Insurance Brokers (Pvt) Ltd and Thomas Cook Travels Sri Lanka.

22Commercial Leasing & Finance PLC

ys;j;alu

Dr. H Cabral, PC Independent Non-Executive Director

Dr Harsha Cabral was appointed to the Board as an Independent Non Executive Director in December 2011. He is a President’s Counsel and holds a PhD in Corporate Law (University of Canberra) Australia. Dr Cabral is a Senior Counsel in Corporate Law with 28 years of experience, specialising in Company Law, Intellectual Property Law, Commercial Law, International Trade Law & Commercial Arbitration.

He serves as a Commissioner, Law Commission of Sri Lanka. He is a Member of the Advisory Commission in Company Law, Sri Lanka (key member in drafting the new Companies Act No. 07 of 2007), member of the Ministerial Committee appointed to reform the Law on Commercial Arbitration. He is a Council member of the University of Colombo, member of the Council of Legal Education in Sri Lanka, member of the Academic Board of Studies of the Institute of Chartered Accountants of Sri Lanka and a member of the Corporate Governance Committee of the Institute of Chartered Accountants of Sri Lanka.

He is currently serving on the Boards of Diesel & Motor Engineering PLC (DIMO), Richard Pieris & Co. Distributors Ltd., Tokyo Cement Company (Lanka) PLC, Tokyo Super Cement Co (Private) Ltd., Tokyo Cement Power (Lanka) Ltd, Hayleys PLC. Hambana Petrochemicals Ltd, Lanka ORIX Finance PLC, Tokyo Eastern Cement Company Ltd, Browns Investments PLC, Just in Time Consultancy (Pvt ) Ltd, Imperial Institute of Higher Education (Pvt) Ltd and Alumex PLC. He is also the Chairman of Tokyo Cement Group.

Dr Cabral is a lecturer and examiner of the University of Colombo, Council member and faculty member of Institute for the Development of Commercial Law & Practice, and the Vice President of Business Recovery & Insolvency Practitioners Association of Sri Lanka.

He is the author of several books on Company Law & Intellectual Property Law.

Mr. D M D K Thilakaratne Director/Chief Executive Officer

Mr Krishan Thilakaratne is the Director/ CEO of Commercial Leasing & Finance PLC, General Manager of LOLC Al-Falaah - Islamic Business Unit of LOLC Group and also the Head of the Valuation Unit of LOLC under LOLC Motors Ltd. He also serves on the Board of Commercial Insurance Brokers (Pvt) Ltd., the largest Insurance Broker in Sri Lanka which is an associate Company of Commercial Leasing & Finance PLC.

He previously held the positions of CEO, Lanka ORIX Factors Ltd, and CEO, Auto Finance of LOLC. He is an Associate Member of the Institute of Bankers of Sri Lanka and joined the LOLC Group in 1995.

Miss. Chrishanthi EmmanuelDirector, LOLC Corporate Services (Pvt) Ltd, Secretaries

Miss Chrishanthi Emmanuel is a Fellow of the Institute of Chartered Secretaries and Administrators - UK and a Fellow of the Institute of Chartered Corporate Secretaries (Sri Lanka).

The Board of Directors

23Annual Report 2014/15

Management Team

Mr. Krishan Thilakaratne - Director/Chief Executive OfficerMr. Jude Anthony - Deputy General Manager - Branch NetworkMr. Nihal Weerapana - Deputy General Manager - RecoveriesMrs. Deepmalie Abhayawardane - Assistant General Manager - FactoringMr. Tharanga Indrapala - Assistant General Manager - OperationsMrs. Nishanthi Kariyawasam - Head of Finance

24Commercial Leasing & Finance PLC

ys;j;alu

Mr. Lasantha Peiris - Head of IT OperationsMr. Upul Samarasinghe - Assistant General Manager - CreditMr. Lal Abeyrathne - Head of Marketing - FactoringMr. Prasanna Dayarathna - Chief Manager - Operations (Factoring)Mr. Prasanna Karandagolla - Chief Manager - Polonnaruwa RegionMr. Terrence Kaushalya - Chief Manager - Saving & Deposits

Management Team

25Annual Report 2014/15

Mr. Pradeep Madurasinghe - Chief Manager - Negombo RegionMr. Dishan Obeysinghe - Chief Manager - Asset Backed FinanceMr. Ruwan Wickremeratne - Chief Manager - RecoveriesMr. Jagath Jayasekara - Manager - Human ResourcesMr. Rasika Alwis - Head of AdministrationMr. Hasitha Hemasiri - Assistant Manager - Customer ServicesMr. Prasad Perera - Assistant Manager - Marketing Communications

26Commercial Leasing & Finance PLC

ys;j;alu

Regional Management Team

Mr. Samitha Aruggoda - Chief Manager - Gampaha RegionMr. Sarath Gamage - Chief Manager - Anuradhapura RegionMr. Prasanna Goonethilleke - Chief Manager - Kurunegala RegionMr. Suneetha Samarawickrama - Chief Manager - Colombo RegionMr. Sunil Shantha - Chief Manager - Galle RegionMr. Sarath Wijenayake - Chief Manager - Ratnapura Region

27Annual Report 2014/15

Mr. Sampath Palliyaguru - Manager - Matara RegionMr. Janaka Karunaratne - Manager - Kandy RegionMr. Harsha Kumarage - Assistant Regional Manager - Anuradhapura Region

Needs

Operational ReviewsManagement Discussion & Analysis | Branch Network | Financial Review | Sustainability Report | Corporate Governance | Risk Management

Our corporate philosophy “Hithawathkama” helps us to understand the needs of Sri Lankans. Our portfolio of financial products and services helps them grow their wealth.

UnderstandingSri Lankan

ys;j;alu“ H i t h a w a t h k a m a ”

30Commercial Leasing & Finance PLC

ys;j;alu

Commercial Leasing & Finance PLC (CLC) recorded an exceptional 2014/15 financial year in both financial and operational terms. Apart from creating greater value for our shareholders, we were able to improve several operational aspects which supported the strong growth experienced by CLC during the year. Furthermore, we continued our quest to improve and streamline our processes to provide efficient service for our customers while maintaining strict internal controls. CLC is among the largest non-banking financial institutions in Sri Lanka with 27 years’ experience in the financial sector.

A key process improvement undertaken during the period was the redesigning of documentation for our loan and lease products, which now offers customers greater ease in doing transactions due to minimal documentation requirements. We have also taken the initiative to ensure that customers reap the benefits of technological advancements such as SLIPS, Online transacting and our ATM network, by connecting with the customers and vendors in real-time.

Business ChannelsThe sector performed well during the period under review due to reduction of tax rates on importing vehicles, reduction in fuel prices and the low interest regime that prevailed through the year. In addition, CLC’s ability to source low cost funds has helped in offering competitive lending rates to target customers.

The deep domain experience and the strength of the sales and marketing team were key factors in achieving set targets during the year. The introduction of new products along with CLC’s exclusive business model fuelled further growth. Our employees are encouraged to pursue excellence and are supported with comprehensive training programmes to enhance their skills.

During the year, 5 new branches were opened in strategic locations to enhance our reach to offer greater customer convenience. The introduction of branch performance awards by dividing branches into three categories has helped drive higher productivity and resulted in stronger results for the company.

Management Discussion & Analysis

Going ahead, we will endeavour to expand our portfolio of products and services, while ensuring geographical expansion across the length and breadth of the country. The severe competition and price wars in the industry in which we operate requires us to create a distinctive positioning for our company and product portfolio in such a manner that customers opt for CLC products for its outstanding service levels and innovative products. Our success in this segment can be attributed to one of the strongest marketing teams in the industry, which has the capability to drive growth and achieve corporate objectives.

Leasing & LoansThe leasing sector experienced a YoY growth of 18.63%. The Net advances portfolio of CLC, which primarily consists of leases, loans and flexi cash, increased from Rs. 25.7 Billion in March 2014 to Rs. 30.5 Billion in March 2015. In a sectoral analysis, advances to the Services sector (Rs. 8.4 Billion) and Trade sector (Rs. 7.9 Billion) accounted for the highest increase in advances.

Since industry focus was on financial sector consolidation in the first half of the year, the usual heightened competition was absent. However, there was a visible shift by the banking sector to stake a share in traditional NBFI products, as they were in a position to offer more competitive rates.

In the leasing industry, a favourable import duty structure for Hybrid and Light Commercial Vehicles (LCVs) was announced by the government. In post budget 2014, there was a shift in duty concessions from Hybrids to motor cars below 1000cc. Infrastructure development projects across Sri Lanka rendered lending for construction vehicles and equipment a lucrative business avenue for the company.

During the year, net interest income from the portfolio improved due to decrease in interest expenses.

During the year under review, we expanded the number of products in our portfolio and stepped up promotional efforts to attract a greater number of customers while leveraging on new partnerships. Two new advanced products Flexi cash, an innovative working capital solution for businesses; and Flexi loan, a product with variable interest rates were introduced

31Annual Report 2014/15

during the year. The company undertook three major marketing campaigns for Flexi cash, Alto and Hybrid vehicles, in addition to many regional promotional activities. In the first year of its launch, the net value of the Flexi cash portfolio rose from Rs. 333 Million to Rs. 2.06 Billion, amassing a total number of 1,300 contracts, which demonstrates the dynamism of CLC in the industry. We forged new partnerships with two prominent vehicle importing companies, in addition to our other existing partnerships.

CLC continued to consolidate its position as the single largest player in the market for financing Light Commercial Vehicles (LCVs). Currently, 17% of all LCVs sold in the country are financed by CLC. The company enjoys a strong presence in the agricultural sector and is one of the largest players in tractor financing.

We believe that product innovation and the adoption of new technology in tandem with increased product marketing activities will define the future growth of CLC’s advances portfolio. Looking ahead, our focus will be on growing the corporate lending sector, as we have recently set up a corporate lending unit under the Asset Backed Finance Business unit. In the meantime, we will continue to break new ground in personal lending, while leveraging on synergies with the Savings & Deposits arms to drive greater product innovation.

DepositsCLC’s deposits arm continued its strong growth trajectory by reaching Rs. 9.4 Billion in deposits in the financial year under review, compared to Rs. 7.5 Billion in the previous year. The period witnessed a 24% growth in fixed deposits, which reflects the public trust towards the company. We also continued to strengthen our customer service levels which helped to boost the deposit base of the company further. Customers are becoming increasingly cautious about the security of their investments and are seeking companies that have built a strong legacy of trust. In this context, CLC is emerging as the preferred choice for clients who understand the value of our heritage. CLC’s strengths and group synergies with parent company LOLC helps us retain shareholder wealth and grow customer confidence.

We continued to encourage healthy competition between branches to recognise the best performing ones. Bambalapitiya branch was selected as the best deposit mobilization branch of the year. Moreover, we continued to add value to our existing product portfolio by introducing new value-added features and by focusing on enhancing service quality to exceed customers’ expectations. Our technologically advanced products and service standards offer us a unique positioning and we will continue to fine-tune our delivery further.

Deposits and savings products are one of the key funding sources for CLC. Customers have the option of selecting investment instruments according to their need. We continue to forge ahead in new product development by using cutting-edge technology to add more value to the existing product range. One of our primary goals is to inculcate savings habits among people by reaching the unbanked segment of the society by promoting savings products.

FactoringThe pace of competition in the arena of factoring has been rising steadily, as companies engaged in Factoring rose to 10 in number during the year from 7 in the previous year. In addition, many other finance companies and banks have begun offering similar products such as Cheque Discounting, Speed draft and so on, enabling entrepreneurs to fulfil their working capital requirements without pledging their receivables.

Some of the other challenges faced by the company during the year were high level of excess liquidity in the banking sector and low demand for credit due to slow growth in existing businesses experienced throughout the year. CLC’s Factoring arm was buoyed by its strong business model while operating against this challenging backdrop in 2014/15. However, we were quick to leverage on the stable economic and political environment that prevailed during the year and expect this to lead to growth of trading and service business sectors which, in turn, will open up avenues for us to seize opportunities in lending and providing working capital solutions.

32Commercial Leasing & Finance PLC

ys;j;alu

The Factoring portfolio increased from Rs. 1.8 Billion in 2013/14 to Rs. 2.4 Billion in 2014/15, which reflects a sharp growth of 33.8%. The factoring arm contributes 7% to the company’s total portfolio and 7% to its income. The active client base grew from 290 clients in 2013/14 to 398 in 2014/15. During the year under review, we persisted with the previous year’s strategy to diversify our market segment from Corporate to SMEs through branch factoring programmes. We leveraged on offering more flexible and customized solutions to suit working capital related requirements, and expanded service standards through SLIP transfers and Fax transfers. All these improvements helped us achieve our targets for the year. The branch Factoring portfolio which stood at Rs. 417 Mn and 126 clients as at 31st March 2014 grew to 218 clients contributing Rs. 985 mn to the total Factoring portfolio of Rs. 2,413 mn as at 31st March 2015, which is a 73% increase in number of clients and a 136% increase in the branch factoring portfolio.

Factoring fits well into the overall company’s basket of products as it is the only product that can be offered without collateral but against receivables. The robust performance of the Factoring unit in the year under review and our dynamic strategies for the future will no doubt consolidate and improve Commercial Factors’ position as one of the largest factoring related solutions providers in the country.

Building Human CapitalCLC has built up a strong reputation for professionally trained and courteous staff that are well-versed in all aspects of the company and who engage closely with customers to customize financial solutions for them. The company continues to invest in its people through talent acquisition, talent development and talent retention, and by offering its employees a superior work culture with numerous opportunities for career progression. Building competencies through formal training and development programmes has helped us attract and retain the best and brightest talent. In turn, we have reached out to share and impart our knowledge with academia wherever possible, so as to share our best practices with the rest of the industry. Not only is CLC perceived as possessing a competitive talent acquisition team, it is also known for its pioneering thought leadership in the industry.

Management Discussion & Analysis

The CLC team consists of young and dynamic professionals, with 77% belonging to the 18-35 age groups, which signifies a strong potential for developing this talent for the sustainable future of the company. The company enjoys an average monthly retention rate of 98% and above industry average year-to-date retention rate of 85% largely due to the myriad opportunities for professional growth and dynamic and pleasant work culture. We are focused on creating an internal pipeline of leadership, having introduced a comprehensive development program facilitated by 3W Consulting for Branch and Regional Managers, which is considered a significant milestone in developing leadership skills and competencies.

CLC has adopted a lateral hiring strategy, which is, hiring candidates with industry experience and then steeping them in our culture, mainly due to the fact that they are able to achieve set budgets within a short time span, as against the industry norm of hiring fresh school leavers. As a result, we have built up a strong talent pool built around the concept of ‘Hithavathkama’. The Human Resources team won the Silver award at the SLITAD awards in December 2014.

Looking ahead, the objective of the HR team is to introduce management training programmes while stepping up recruitment initiatives. Greater Environment, Health & Safety (EHS) and efforts at reducing carbon footprint are being initiated along with an increased focus on training frontline employees. CLC’s success can be strongly attributed to its professional team of employees and in the year ahead, every effort will be made to consolidate and build on this reputation further.

Customer ServiceCustomer service is a hub which interconnects all other departments and we will continue to strengthen this function. The professionalism of our service is directly reflected in our high customer retention levels. The Customer Service Hotline continues to be a key touch point between staff and customers. The Marketing Call Centre set up last year, which is dedicated to handle all inbound calls on advertisements, product promotions and marketing campaigns, performs a useful role in streamlining the company’s connection with customers and other

33Annual Report 2014/15

stakeholders. We have also made efforts to constantly enhance service levels through new technology and the year ahead will see CLC offering superior mobile banking facilities to customers.

Our staff is also equipped to handle customer inquiries relating to the entire product range. Teamwork and high communication skills were factors that played a major role in our enhanced performance during the year. The work culture and ambience was improved during the year with extensive refurbishment which enhanced comfort levels and a spacious feeling for both staff and customers. Some key processes were analysed and paradigm shifts made so that maximum efficiency could be achieved. Continuous training and updating of frontline staff was also accomplished.

Going ahead, continuous training of human resources will be a key focus area, while we will ramp up our adoption of technology by upgrading processes and procedures so that they meet the evolving expectations of our customers.

CreditDuring the year under review, the company focused on improving systems and processes in the Credit division, to minimize delivery time to customers which would ultimately result in improved customer satisfaction. We were able to strategically strengthen the structure of our collection division, improve credit policies and infuse greater controls of procedures, which together improved efficiencies in the Credit function. A strong risk framework is in place and underpinned our success during the year.

Moreover, a concentrated effort was made to empower Branch Managers and Regional Managers by decentralizing decision-making process, so that they are fully equipped to approve files at regional level. This, along with other process developments and improvements, enhanced our credit division out put. Continuous internal credit training programmes were conducted with a view to enhance the credit knowledge of the frontline staff. Furthermore, marketing staff in the company underwent external credit training and risk evaluation programmes, to ensure that they have a 360-degree understanding of the business.

Our astute portfolio management guided by our robust risk and governance policies has resulted in low Non Performing Loan (NPL) ratios. We pride ourselves on our diversified

portfolio that strikes the right balance between assessed risks and secure options through portfolio diversification. Recoveries were closely monitored to ensure that stability was maintained throughout the year.

RecoveriesAdverse weather conditions in the first half of the 2014/15 financial year resulted in a low growth in the leasing segment, especially in the north and north-east. However, improved weather conditions in the second half of the year coupled with a low interest and inflation regime reflected a strong pick-up in growth across all the regions. The Recoveries division ended the year on a high, recording positive results.

Cognizant of the hardships our customers had to endure due to unfavourable weather, we extended them the fullest support in the first part of the year; offering grace periods and restructuring loans and leases, so that customers engaged in agriculture and agri related businesses could tide over a difficult period. CLC’s Recoveries Team is focused and mindful of its social responsibility to provide support to our customer base.

This resilient performance by the recoveries team was achieved owing to the extensive training that has been given to our staff for them to deal with extraordinary situations such as the one we faced during the first half of the year, and they are now equipped to react and adapt to situations as they develop. The activities of the collection team is monitored on a daily basis and they have been empowered with relevant data to carry out their functions smoothly. In order to streamline the system further, delinquency meetings were carried out at all branches to address relevant issues in a timely manner. Going forward, we plan to centralize call centre activities to maximize productivity and provide training to staff in handling of new products.

Marketing CommunicationsBrand CLC grew from strength to strength in the year under review. CLC was listed 44th out of top 100 brands in Sri Lanka by LMD Brands Annual Magazine in 2014/15. The brand was further nominated for SLIM- Nielsen’s ‘People’s Financial Service Provider of the Year’ award in 2015. These accolades are the result of close customer engagement and acting on customer feedback to better meet and surpass their expectations. During the year, CLC’s official Facebook

34Commercial Leasing & Finance PLC

ys;j;alu

Management Discussion & Analysis

page was launched, which opened a new interface for the company to interact with its customers and step up to its digital media presence. The CLC Facebook page has witnessed a significant growth in fans since its launch in January 2015. However, majority of our customer segment hails from rural and developing areas, therefore, we will continue to maintain our presence in traditional media as well.

We are focused on enhancing brand equity and brand engagement online, so that the division is in a better position to offer recommendations to enhance business through insights into competition and market trends. The popularity of the CLC brand has been proved by being a nominee of a SLIM-Nielsen Award. The company’s unique operating philosophy of ‘Hithavathkama’ is cascaded across all its communications and underpins the company’s corporate culture.

Future OutlookCLC stands on a strong footing today as one of the most prominent and trusted financial services brands, reflecting an equity capital of Rs. 10 Billion and an A- ICRA rating. The company is innovating its portfolio of products and services to better benefit from forecasted growth in credit demand and capital investments in the country. CLC staff drives its success quotient. Therefore, existing and potential customers can expect even greater levels of personalized service across the company’s extensive branch network. The company plans to leverage on its strength and group synergies as a member of the LOLC Group to achieve even greater financial and operational results in the upcoming financial year.

35Annual Report 2014/15

Branch Network

Nelliady

Jaffna

Killinochchi

Mannar Parakramapura

Kebitigollewa

Trincomalee

Serunuwara

Batticaloa

Kalmunai

Ampara

Monaragala

BadullaNuwara Eliya

Welimada

RatnapuraMaharagama

Kalutara

NugegodaBambalapitiya

Pettah

KiribathgodaKaduwela

Avissawella

Kalawana

Tissamaharama

Embilipitiya

UdugamaAmbalangoda

Pitigala

Baduraliya

GalleMatara

Anuradhapura

Nochchiyagama

Dambulla

Polonnaruwa

Bakamuna

Puttalam

ChilawKurunegala

Matale

Mahiyanganaya

KandyWarakapola

Gampaha

Kuliyapitiya

Negombo

Wennappuwa

Medawachchiya

Vavuniya

CLC Branches

Post Office Services Centers

Specialised Factoring Branches

Dehiwala

Grandpass

Minuwangoda

Wattala

Gampola

Nawala

36Commercial Leasing & Finance PLC

ys;j;alu

Financial Review

OverviewThe Company closed the financial year ending 31st March 2015, recording strong performance with a profit before income tax reaching Rs. 1,728Mn, reporting a growth of 34% over the previous year. The Company maintained the growth momentum to achieve an after tax profit growth of 52% moving to 1,426Mn from Rs.936Mn whilst the earnings per share rose to Rs.0.22 from Rs.0.15 during the year. This strong growth in profitability was achieved amidst lower margins experienced during the year as a result of the drop in lending rates.

In September 2014, the Company acquired 59.33% of the voting rights of BRAC Lanka Finance PLC(BRAC) whose principal activity is the provision of micro financial services. In the mandatory offer made subsequently, an additional stake of 35.02% was acquired in November 2014, increasing its ownership to 94.35%. Group figures in the profit or loss statement reflects seven months performance of BRAC Lanka Finance PLC (BRAC) together with 12 months performance of the Company. BRAC contributed Rs.157Mn to the bottom line of the Group while the contribution from its associate company with 40% ownership, Commercial Insurance Brokers Ltd., was marginal.

Interest IncomeThe primary source of income of the Company increased marginally over the previous year to Rs.7,590Mn from Rs.7,514Mn due to thinning margins with the relatively low lending rate regime prevailing across the industry.

In Rs.Mn

Interest incomeFY

2014/2015FY

2013/2014Variance

%

Leasing 2,821 3,163 (11)

Loans & advances 3,451 2,646 30

Hire purchase 122 495 (75)

Factoring 521 695 ( 25)

Overdue interest 536 446 20

Other 139 69 99

Total 7,590 7,514 1

2014/15

2013/14

LeasingLoans & advances Hire purchaseFactoringOverdue interestOther

37%

7%7%

45%

42%

35%

9%6%

1%

7%

2%

2%

Components of interest income

Interest income on leasing and hire purchase declined from Rs.3,163 Mn to Rs.2,821 Mn and Rs.495 Mn To Rs.122 Mn respectively mainly due to the shift in the product mix. Interest income on loans reached to Rs.3,451 Mn from Rs.2,646 Mn. Leasing and loan interest income represents 82% of the total interest income compared to 77% over the corresponding last year. Factoring income stood at Rs.521 Mn, with a decrease of 25% from Rs.695 Mn. The overdue interest income grew by 20% to reach Rs.536 Mn compared with Rs.446 Mn in the previous year.

Interest ExpenseInterest expense reduced by 21% to Rs.2,406 Mn from Rs.3,039Mn mainly due to the low interest regime prevalent market-wide, strong fund management strategies and conscious efforts made to tap low cost funding. This is a significant performance considering the higher level of borrowings sourced by the company by way of deposits and borrowings to support the aggressive business growth.

37Annual Report 2014/15

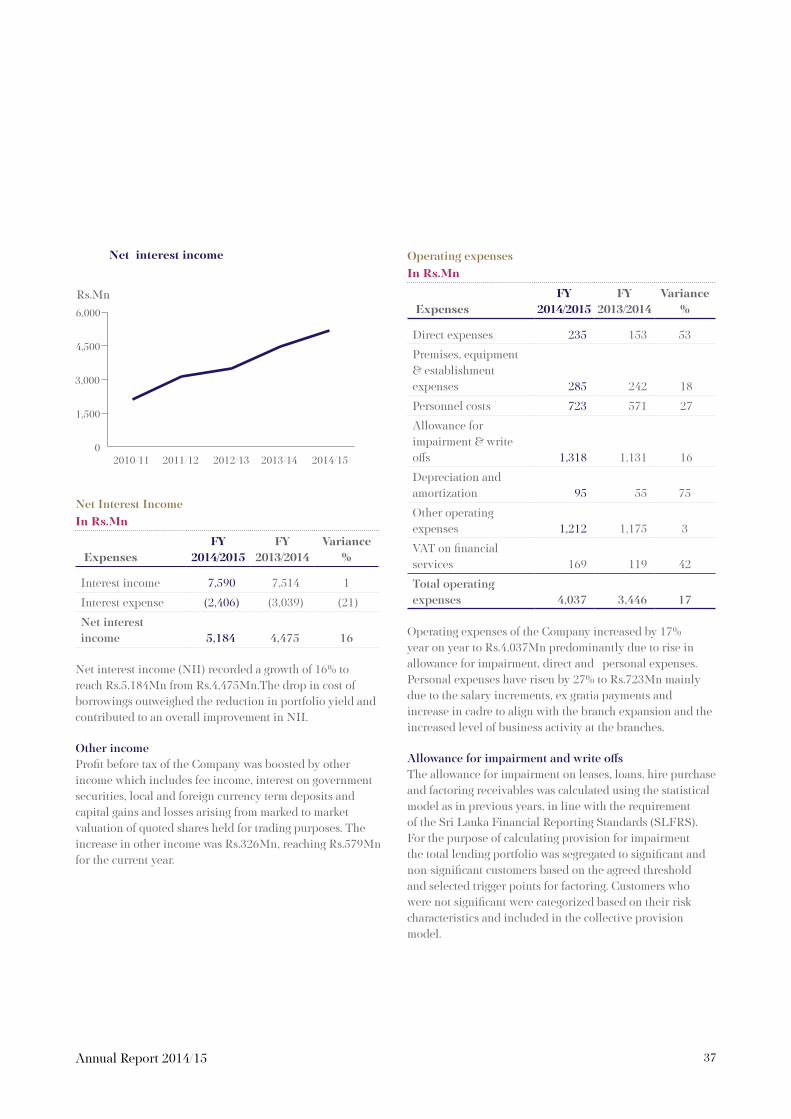

Net Interest IncomeIn Rs.Mn

ExpensesFY

2014/2015FY

2013/2014Variance

%

Interest income 7,590 7,514 1

Interest expense (2,406) (3,039) (21)

Net interest income 5,184 4,475 16

Net interest income (NII) recorded a growth of 16% to reach Rs.5,184Mn from Rs.4,475Mn.The drop in cost of borrowings outweighed the reduction in portfolio yield and contributed to an overall improvement in NII.

Other incomeProfit before tax of the Company was boosted by other income which includes fee income, interest on government securities, local and foreign currency term deposits and capital gains and losses arising from marked to market valuation of quoted shares held for trading purposes. The increase in other income was Rs.326Mn, reaching Rs.579Mn for the current year.

Operating expensesIn Rs.Mn

ExpensesFY

2014/2015FY

2013/2014Variance

%

Direct expenses 235 153 53

Premises, equipment & establishment expenses 285 242 18

Personnel costs 723 571 27

Allowance for impairment & write offs 1,318 1,131 16

Depreciation and amortization 95 55 75

Other operating expenses 1,212 1,175 3

VAT on financial services 169 119 42

Total operating expenses 4,037 3,446 17

Operating expenses of the Company increased by 17% year on year to Rs.4,037Mn predominantly due to rise in allowance for impairment, direct and personal expenses. Personal expenses have risen by 27% to Rs.723Mn mainly due to the salary increments, ex-gratia payments and increase in cadre to align with the branch expansion and the increased level of business activity at the branches.

Allowance for impairment and write offsThe allowance for impairment on leases, loans, hire purchase and factoring receivables was calculated using the statistical model as in previous years, in line with the requirement of the Sri Lanka Financial Reporting Standards (SLFRS). For the purpose of calculating provision for impairment the total lending portfolio was segregated to significant and non-significant customers based on the agreed threshold and selected trigger points for factoring. Customers who were not significant were categorized based on their risk characteristics and included in the collective provision model.

Net interest income

0

1,500

3,000

4,500

6,000

2010/11 2011/12 2012/13 2013/14 2014/15

Rs.Mn

38Commercial Leasing & Finance PLC

ys;j;alu

Impairment loss for the year increased from Rs.1,131Mn to Rs.1,318Mn. This was due to an additional provisioning being made on identified facilities in arrears including few factoring facilities under litigation. The Company’s impairment balances remain healthy and conservative and well over the stipulated regulatory levels at the year end.

In Rs Mn

FY2014/2015

FY2013/2014

Individual impairment charge 758 855

Collective impairment charge 560 276

Total impairment charge 1,318 1,131

Individual impairment loss recorded a marginal decrease compared to the previous year but the collective impairment provision showed an increase in line with the prudent provisioning policy adopted by the Company.

Financial Review

Rs.353Mn to Rs.302Mn due to part reversal of deferred tax asset in the year under review. The Company paid Rs.204Mn as VAT on financial services, NBT on financial services and Crop insurance levy which is included in direct expenses.

Asset growthThe Company’s balance sheet strengthened, supported by the aggressive growth in the lending portfolio increasing total assets to Rs. 42,385 Mn from Rs.32,934 Mn, 29% higher than the previous year. During the year, the company grew its net lending portfolio including factoring from Rs.27,570 Mn to Rs.32,982 Mn recording a rupee growth of Rs.5,412Mn. The net lending portfolio accounts for 78% of the total assets, a reduction of 6% from 84% in the previous year. The ratio dipped with the investment of Rs.968Mn in the subsidiary company, BRAC. The growth of the assets was also supported by the increase in financial investment mainly in foreign currency term deposits.

Total assets to net lending portfolio

0

10,000

20,000

30,000

40,000

50,000

Total assets

Net lending portfolio

2011 2012 2013 2014 2015

Rs. Mn.

NPL ratio

0

1

2

3

4

2011 2012 2013 2014 2015

%

The Company strengthened the recovery efforts to create stability of the lending portfolio. The non-performing loan ratio, the measure of the quality of the lending portfolio has improved from 2.44% to 1.96% since 31st March 2014.This is well below the industry peers.

TaxationThe current year’s profit after tax reached Rs.1,426Mn after providing Rs.302Mn for taxation. Rs.443Mn has been provided as income taxes and Rs.141Mn has been reversed as deferred tax. The Company’s tax expense dipped by 14%, from

The asset base of the Group stood at Rs.45,429Mn mainly supported by the growth of the loan book of the Company and BRAC. During the year, the Group disbursed Rs.27,530Mn in leases, loans and hire purchase.

Net asset per share of the company was Rs.1.59, up from Rs. 1.39 since 31st March 2014. Further, the Return on Average Assets(ROAA) has improved to 3.79% from 3.11% reflecting the company’s efficiency in asset and liability management.

39Annual Report 2014/15

Deposits from customersThe customer deposit base grew from Rs 7,534Mn to Rs.9,381 Mn, a growth of 25% over last year despite fluctuating interest rates. This accounted for 32% of the funding mix. The growth was largely driven by the concentrated efforts made on fund mobilization, supported by the strong brand image. Launching of CLC ATM/Debit card in April 2015 will help the Company to improve its savings deposit base further.

FundingTotal sources of funding of the Company increased from Rs.21,989Mn to 29,551Mn.During the period under review, the Company received long term loans amounting to Rs.2.4Bn and short term borrowings equivalent to Rs.7.7Bn out of which Rs.3.8Bn was borrowed against foreign currency fixed deposit.

Foreign funding agenciesSecuritizationOther long termShort termCustomer depositsOthers

22%

9%

34%

1%

3%

32%

Funding mix as at 31-3-2015

30%

8%8%

19%

1%

34%

Funding mix as at 31-3-2014

CapitalizationThe equity of the Company reached Rs.10,115Mn, an increase from Rs.8,856Mn with the earnings from operations. The Company’s rich repository of capital continued to energize and strengthen the company’s growth prospects. Return on Average Equity (ROAE) increased to 15.03% from 11.21% over previous year.

Core capital and total risk weighted capital ratio, Capital Adequacy Ratios (CAR) stood at 28.27% and 25.57% respectively as at financial year end 31st March 2015, well above the stipulated regulatory minimum of 5% and 10% each. The regulatory capital computation excludes Rs.968Mn invested in subsidiary company.

The market capitalization of the Company exceeded Rs.25Bn as at 31st March 2015 with a closing share price of Rs.4.00,which resulted in a Price Earning(PE) ratio of eighteen (times).

The strong performance of the Company during the year and the strong balance sheet, positions the Company to derive stronger performance in the coming years.

The Company is planning to raise Rs.5Bn through a 5 year listed senior debenture with the objective of growing the portfolio and minimising maturity mismatches in assets and liabilities.

Capital adequacy - core capital ratio

22

23

25

26

28

30

2012 2013 2014 2015

%

40Commercial Leasing & Finance PLC

ys;j;alu

Sustainability Report

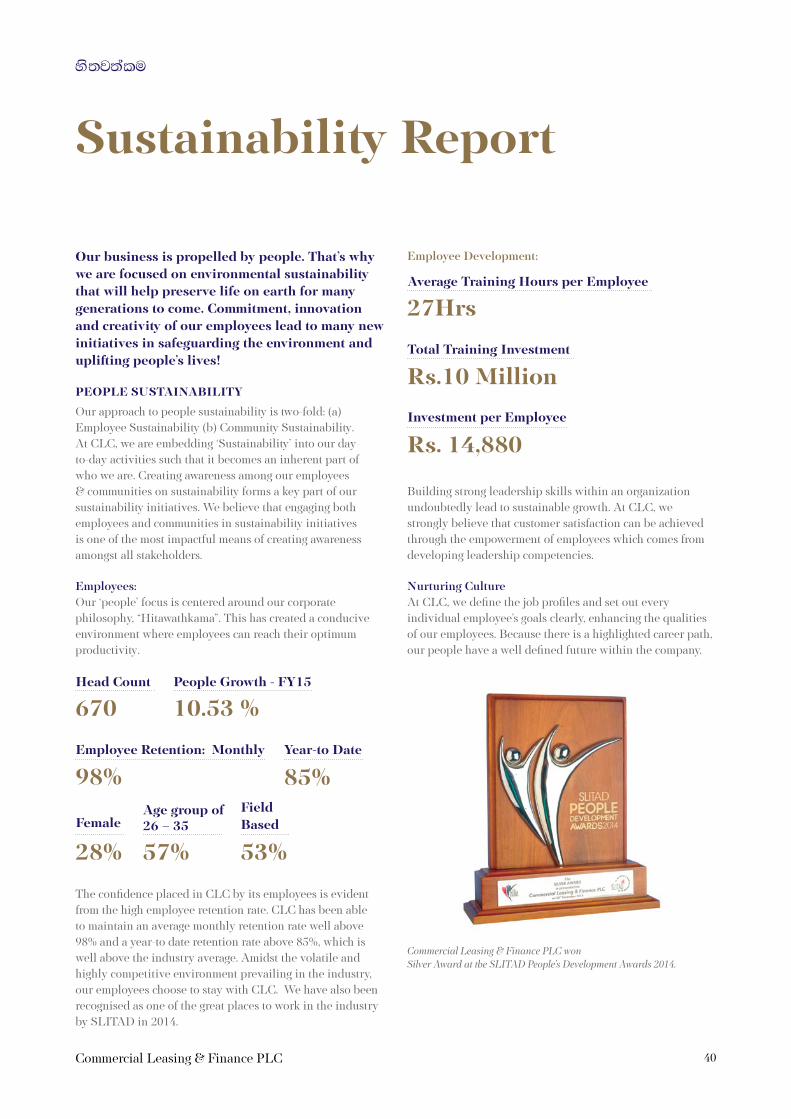

Our business is propelled by people. That’s why we are focused on environmental sustainability that will help preserve life on earth for many generations to come. Commitment, innovation and creativity of our employees lead to many new initiatives in safeguarding the environment and uplifting people’s lives!

PEOPLE SUSTAINABILITY

Our approach to people sustainability is two-fold: (a) Employee Sustainability (b) Community Sustainability. At CLC, we are embedding ‘Sustainability’ into our day-to-day activities such that it becomes an inherent part of who we are. Creating awareness among our employees & communities on sustainability forms a key part of our sustainability initiatives. We believe that engaging both employees and communities in sustainability initiatives is one of the most impactful means of creating awareness amongst all stakeholders.

Employees:Our ‘people’ focus is centered around our corporate philosophy, “Hitawathkama”. This has created a conducive environment where employees can reach their optimum productivity.

27Hrs

Rs. 14,880

Rs.10 Million

Average Training Hours per Employee

Investment per Employee

Total Training Investment

The confidence placed in CLC by its employees is evident from the high employee retention rate. CLC has been able to maintain an average monthly retention rate well above 98% and a year-to date retention rate above 85%, which is well above the industry average. Amidst the volatile and highly competitive environment prevailing in the industry, our employees choose to stay with CLC. We have also been recognised as one of the great places to work in the industry by SLITAD in 2014.

Employee Development:

670

85%

57%

98%

10.53 %

28% 53%

Head Count

Year-to Date

Age group of 26 – 35

Employee Retention: Monthly

People Growth - FY15

FemaleField Based

Building strong leadership skills within an organization undoubtedly lead to sustainable growth. At CLC, we strongly believe that customer satisfaction can be achieved through the empowerment of employees which comes from developing leadership competencies.

Nurturing CultureAt CLC, we define the job profiles and set out every individual employee’s goals clearly, enhancing the qualities of our employees. Because there is a highlighted career path, our people have a well defined future within the company.

Commercial Leasing & Finance PLC won Silver Award at the SLITAD People’s Development Awards 2014.

41Annual Report 2014/15

and they strive hard to reach their goals. The company provides them with ample support in the form of training and development programmes, workshops and an open door policy to discuss any issues with senior management. A strong sense of teamwork and cooperation abounds in our work culture, engendering a sense of a shared vision. Employees undergo a 360-degree review process, whereby their strengths and weaknesses are identified and they are given the necessary tools to strengthen weaker areas, so that they can realize their full potential. The company constantly develops pipelines of leadership to take it on its sustainable journey.

We are focused on creating an internal pipeline of leadership, having introduced a comprehensive development programme facilitated by 3W Consulting for Branch and Regional Managers, which is considered a significant milestone in developing leadership skills and competencies

Leadership teams at CLC are familiarized with the various aspects of ‘Sustainability’ to safeguard the environment and act promptly and responsibly to arrest and curtail factors that may endanger health and safety, or the environment.

Developing a Customer-centric MindsetAt CLC, our employees work consistently on providing customers with superior service, with each area of the business ensuring consistency during each interaction with the customer. Delivering consistency across all customer touch points is our chief endeavour as we believe it drives customer loyalty. By delivering consistent customer care excellence, we not only create a loyal customer base, but we also encourage and motivate our employees to persist in raising the bar when it comes to delivering excellence. This is achieved through training and communicating clear deliverables. CLC engages closely with customer to gain feedback and identify weak areas that can be strengthened further.

Maintaining Work-Life BalanceAT CLC, we cherish and uphold the concept of work-life balance. Alongside encouraging employees to deliver high productivity, we simultaneously encourage their participation in other initiatives outside of their job roles to remain engaged with the company and to maintain an ideal work-life balance. The annual dinner dance, sports day and

the annual trip are eagerly-awaited events in the company’s calendar and witness active participation by employees. Our staff also takes part in mercantile competitions. These social activities have proven to be beneficial for employees’ well being and communicate the company’s ‘Hitawathkama’ philosophy across the enterprise.

Community Engagement

“Water is the foundation of life!

On 22nd of September 2014, 77families in Udayarkaddu village in Mullativu District was given access to tube well water”

Our idea of community sustainability is based on the belief that communities are made up of social, economic, and environmental aspects that are inalienable from each other and if, as a company, we can balance all these aspects, we will be leaving behind a legacy of sustainability. By sharing our resources with the community, we not only forge closer ties, but we also strengthen the capability of the under-served to hope for a brighter tomorrow.

Employees at CLC – Killinochchi branch witnessed the hardship that local villagers faced to fetch drinking water for their daily survival. There are 77 families in the village of Udayarkaddu, who had to travel more than 4 kilometres by foot to fetch water for their daily chores. During the heavy drought period, villagers needed to walk even further to source water.

42Commercial Leasing & Finance PLC

ys;j;alu

Sustainability Report

ENVIRONMENT

“Think, Act, Save”Reduction of purchasing new envelopes |

Switch-off not Stand-by | Healthy lifestyle by walking

Environmental sustainability allows for the needs of mankind to be fulfilled without having e a harmful impact on the ability of future generations to meet their needs. The social, environmental, and economic consequences of rapid population growth, climate change, global warming, unbridled economic growth and over-consumption of our natural resources are being felt globally. We believe it behoves each one of us to arrest this unsustainable approach and stop and think about how we can make a positive difference in our immediate environment. At CLC, we value employees who care for the environment and we encourage our people to act responsibly in order to nurture the planet’s valuable natural resources.

CLC launched an internal sustainability initiative “Think, Act, Save” where employees are encouraged to suggest new ideas to save resources which will result in the reduction of the company’s carbon footprint.

Employee driven initiatives to save planet!Recycling of envelopes – At CLC, we use envelopes for inter-department, intern-company document transfers on a day-to-day basis. Employees suggested reuse of envelopes as many times as possible before being disposed. This resulted in 40% reduction of purchase of new envelopes.

Switching off Lights and Equipment – Awareness was created among employees to switch-off lights, and to use daylight whenever possible to illuminate the work environment by opening blinds. Furthermore, employees were educated to shut down PCs and other electronic devices without keeping them on sleep mode.

Use of elevators – Posters were displayed near the elevators to encourage employees to use the stair case and gain health benefits. This helped CLC reduce power consumption as well as instil a sustainable healthy lifestyle for the CLC employees.

CLC employees came together and helped to provide a long-lasting solution for the drought-affected village by installing a tube well water pump in Udayarkaddu, in Mullaitivu District. The CLC Killinochchi branch took the ownership of maintaining the tube well water pump so as to sustain this facility into the future and to provide villagers access to water.