zce january 14,715 +10 cnce january 14,689 +74 101.03 100 ... · zce january 14,715 +10 101.03...

TRANSCRIPT

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Beijing Report January 2, 2018

Roadmap for rural revitalisation unveiled The central government has outlined major tasks and targets for a rural revitalisation strategy as it seeks to address issues related to agriculture, rural areas and the rural population. By 2020, the revitalisation strategy should have achieved important progress, and an institutional framework and policy system should have been basically formed, according to a statement released last Friday after the annual central rural work conference. By 2035, the aim is for ‘decisive’ progress in implementing the plan for basic modernisation of agriculture and rural areas. By 2050, rural areas should see all-around revitalisation, featuring strong agriculture, a beautiful countryside and well-off farmers, the statement said.

Xinjiang report Nearly 4.7 million tonnes of lint pressed The average daily pressing rate in Xinjiang during the past few days has fallen below 20,000 tonnes but the total by yesterday had risen to 4,668,898 tonnes, consisting of 3,200,341 tonnes by the local cooperative system and 1,468,556 by the PCC (army group). Hence, as recently anticipated, an upward revision in the estimate of Xinjiang’s final output from the 4,700,000

tonnes indicated by BCO in December seems now inevitable. Cultivated area in southern Xinjiang’s Bayingol Mongolian Autonomous Prefecture this year was estimated at 3,593,900 mu (239,593 ha), up 10.9 percent from a year ago. Output was 516,500 tonnes, up 15 percent, year-on-year. Xinjiang long staple prices have maintained a steady tendency during the past week. Type 137 lint is still quoted at 25,200 yuan per tonne, equivalent to roughly 173 US cents per lb.

Cotton movement slows Data show that 53,400 tonnes of Xinjiang cotton were transported by road to ‘mainland’ warehouses last week, 3,100 tonnes less than in the previous week, and 37,200 tonnes (minus 41 percent) less than during the same week last year. The average freight cost by road to ‘mainland’ destinations declined slightly, to around 700/800 yuan per tonne.

2018 State Reserve sales preparation works begin The China National Cotton Reserve Corporation and the China Fibre Inspection Bureau have recently started crop inspection and warehouse clearance work for the 2018 State Reserve sales programme, so as to ensure the smooth development and timely delivery of sales in mid-March.

National Xinjiang

Lint forecast 5,480,000 4,700,000

Lint pressed* 4,815,151 4,668,898

%age of forecast 87.87% 99.34%

Lint inspected* 4,638,968 4,486,083

%age of forecast 84.65% 95.45%

Crop data as at January 1, 2018

*National totals under-record figures for

'mainland'

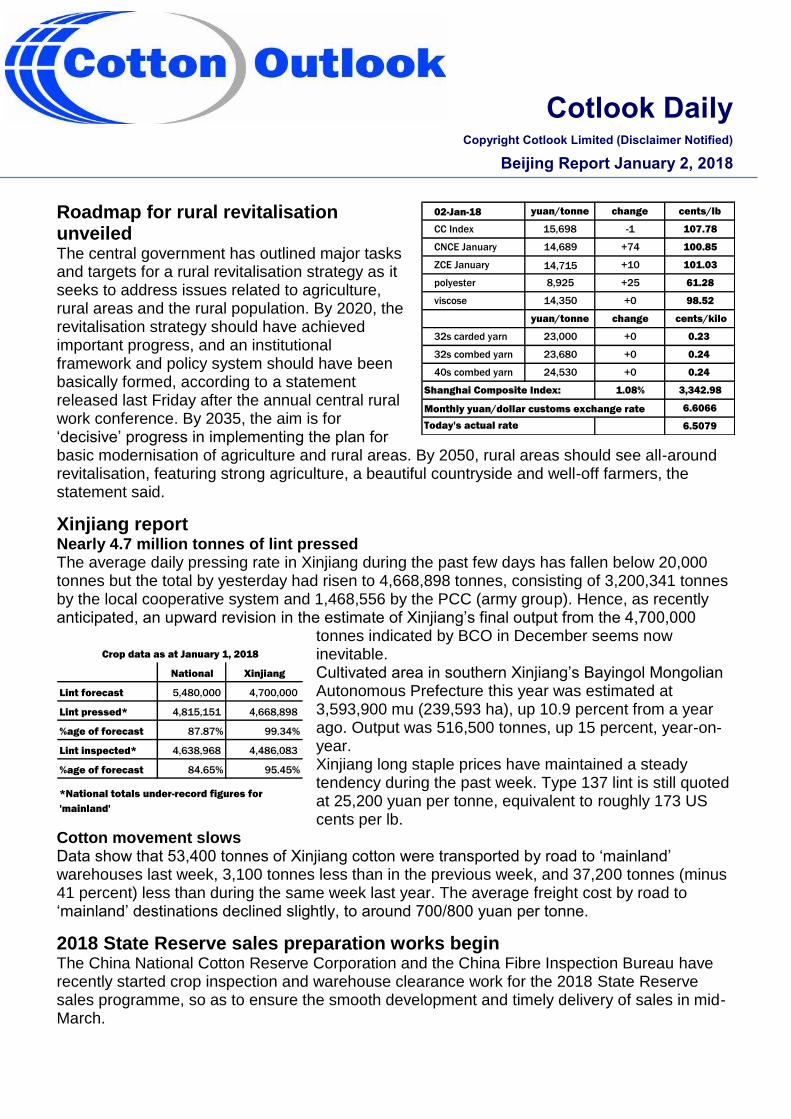

02-Jan-18 yuan/tonne change cents/lb

CC Index 15,698 -1 107.78

CNCE January 14,689 +74 100.85

ZCE January 14,715 +10 101.03

polyester 8,925 +25 61.28

viscose 14,350 +0 98.52

yuan/tonne change cents/kilo

32s carded yarn 23,000 +0 0.23

32s combed yarn 23,680 +0 0.24

40s combed yarn 24,530 +0 0.24

Shanghai Composite Index: 1.08% 3,342.98

Monthly yuan/dollar customs exchange rate 6.6066

6.5079Today's actual rate

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Beijing Report January 2, 2018

Market prices Traders and ginners have been under pressure in view of the stagnant market. Spinners insist on a ‘hand-to-mouth’ buying style. Cotton futures on the Zhengzhou Commodity Exchange recorded gains of between ten and one hundred yuan per tonne, reversing the weak trend evident on the previous trading day. May increased by 15 yuan, while January rose by ten yuan, so the spread between the two months widened by five yuan, to 295 yuan (May premium). Turnover dropped by 101,116, to 75,000 contracts, counting both the sale and the purchase. Open interest decreased by 5,042, to 353,140. At the close of business, the top 20 brokers were holding 114,899 long positions (1,917) and 141,453 short positions (-1,261). The certified stock increased by 105 lots, to 3,348.

On the China National Cotton Exchange’s e-platform, the spot month rose sharply, while the remaining contracts were barely changed. Turnover declined by 3,370, to 10,140 tonnes.

The China Cotton Index (basis Type 3128B) decreased by one yuan to 15,698 yuan per tonne, equivalent to 107.80 US cents per lb. Type 2227B dropped by one yuan to 14,662 yuan, equivalent to 100.65 US cents per lb, and Type 2129B declined by six yuan to 16,217 yuan per tonne, equivalent to 111.35 US cents per lb.

PMI drops slightly NBS data show that the country’s manufacturing purchasing managers’ index (PMI) came in at 51.6 in December, down from 51.8 in November but still running above the level that distinguishes expansion from contraction. The non-manufacturing PMI rose by 0.2 percentage points, to 55 during the month.

Prev

Settle Open High Low Close

Settle-

ment

Net

change Volume

Open

Interest

Jan 14,705 14,650 14,740 14,650 14,710 14,715 +10 1,048 26,832

Mar 14,725 14,795 14,800 14,795 14,795 14,795 +70 56 576

May 14,995 14,910 15,045 14,910 15,040 15,010 +15 69,604 287,494

Jly 15,010 0 0 0 0 15,110 +100 0 116

Sep 15,340 15,240 15,420 15,240 15,405 15,385 +45 4,292 38,088

Nov 15,500 0 0 0 0 15,500 +0 0 34

75,000 353,140

ZCE

02 January 2018

Certified Stocks: 3,348 lots (185 bales each, ±5)

DeliveryTurnover

in tonnes

Average

price in

yuan per

tonne

Change

versus

previous

day's

average

US cents

per lb

equivalent

Type 328 (domestic 'MA')

JAN18 10 14,689 +74 100.55

FEB18 160 14,730 +8 100.83

MAR18 970 14,874 +7 101.82

APR18 5,550 14,885 -6 101.89

MAY18 4,520 14,910 -1 102.06

JUN18 2,300 14,932 +8 102.21

CNCE

January 2, 2018

47.0

48.0

49.0

50.0

51.0

52.0

53.0Manufacturing PMI

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Liverpool Report January 2, 2018

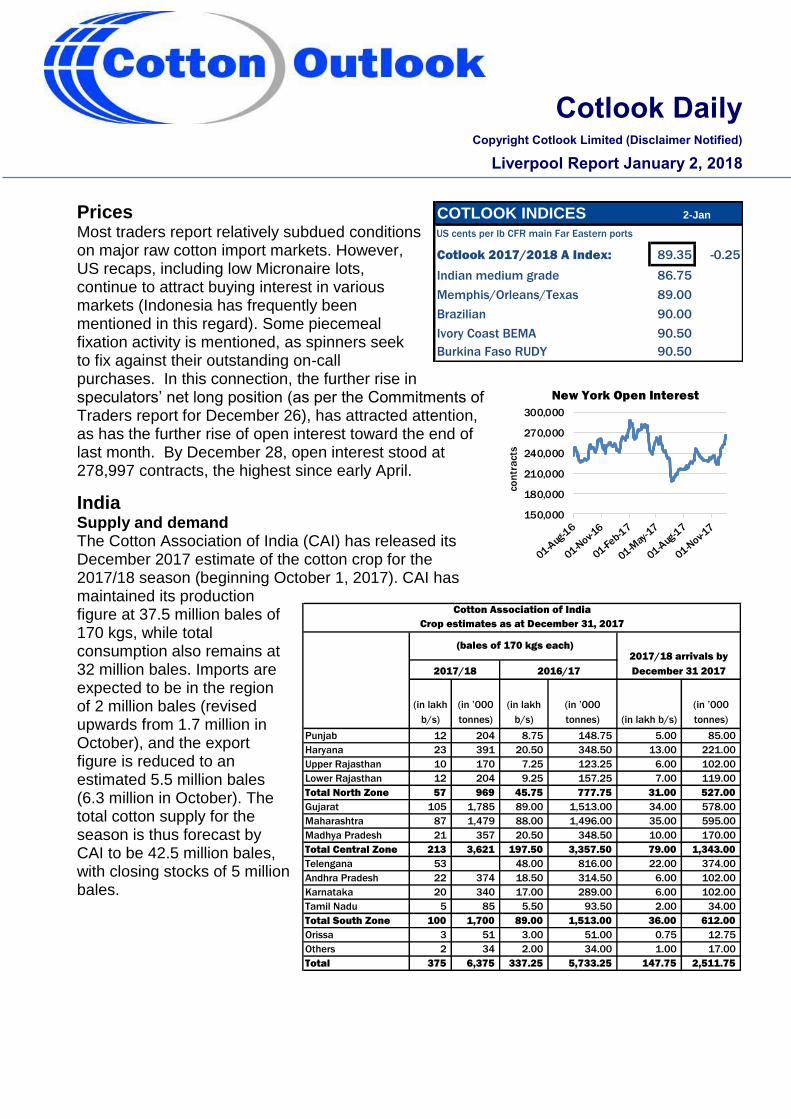

Prices Most traders report relatively subdued conditions on major raw cotton import markets. However, US recaps, including low Micronaire lots, continue to attract buying interest in various markets (Indonesia has frequently been mentioned in this regard). Some piecemeal fixation activity is mentioned, as spinners seek to fix against their outstanding on-call purchases. In this connection, the further rise in speculators’ net long position (as per the Commitments of Traders report for December 26), has attracted attention, as has the further rise of open interest toward the end of last month. By December 28, open interest stood at 278,997 contracts, the highest since early April.

India

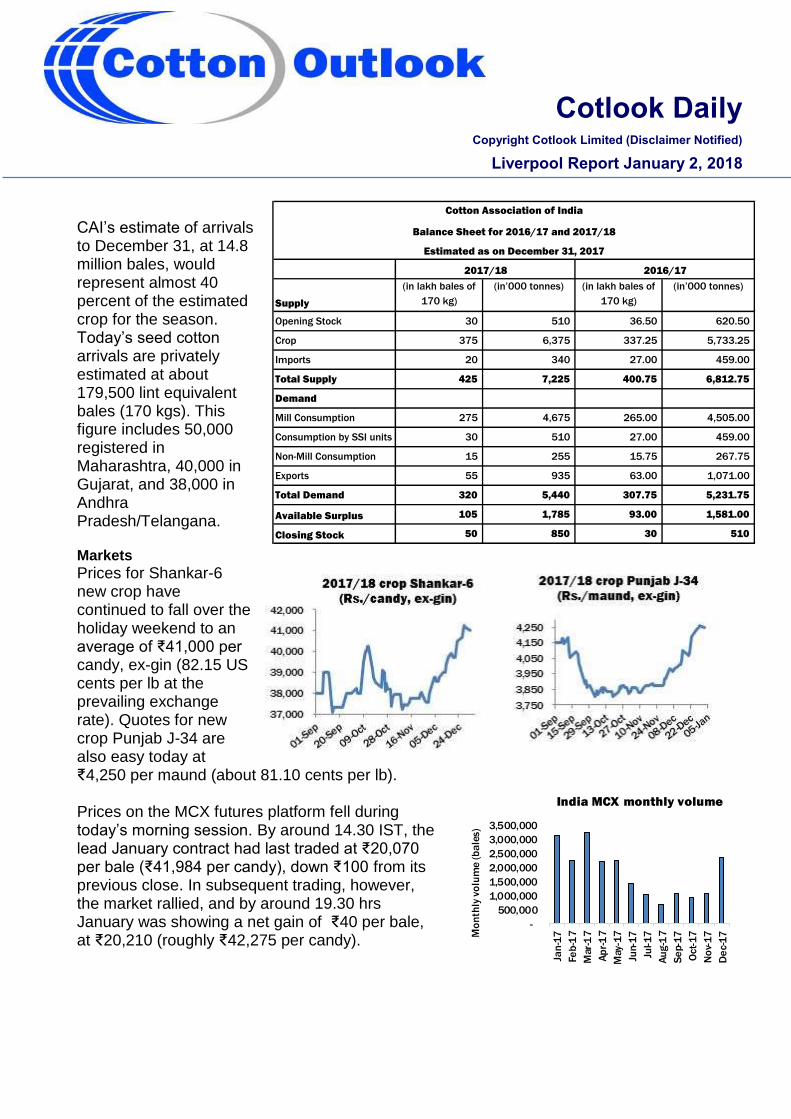

Supply and demand The Cotton Association of India (CAI) has released its December 2017 estimate of the cotton crop for the 2017/18 season (beginning October 1, 2017). CAI has maintained its production figure at 37.5 million bales of 170 kgs, while total consumption also remains at 32 million bales. Imports are expected to be in the region of 2 million bales (revised upwards from 1.7 million in October), and the export figure is reduced to an estimated 5.5 million bales (6.3 million in October). The total cotton supply for the season is thus forecast by CAI to be 42.5 million bales, with closing stocks of 5 million bales.

150,000

180,000

210,000

240,000

270,000

300,000

co

ntr

acts

New York Open Interest

(in lakh

b/s)

(in ’000

tonnes)

(in lakh

b/s)

(in ’000

tonnes) (in lakh b/s)

(in ’000

tonnes)

Punjab 12 204 8.75 148.75 5.00 85.00

Haryana 23 391 20.50 348.50 13.00 221.00

Upper Rajasthan 10 170 7.25 123.25 6.00 102.00

Lower Rajasthan 12 204 9.25 157.25 7.00 119.00

Total North Zone 57 969 45.75 777.75 31.00 527.00

Gujarat 105 1,785 89.00 1,513.00 34.00 578.00

Maharashtra 87 1,479 88.00 1,496.00 35.00 595.00

Madhya Pradesh 21 357 20.50 348.50 10.00 170.00

Total Central Zone 213 3,621 197.50 3,357.50 79.00 1,343.00

Telengana 53 48.00 816.00 22.00 374.00

Andhra Pradesh 22 374 18.50 314.50 6.00 102.00

Karnataka 20 340 17.00 289.00 6.00 102.00

Tamil Nadu 5 85 5.50 93.50 2.00 34.00

Total South Zone 100 1,700 89.00 1,513.00 36.00 612.00

Orissa 3 51 3.00 51.00 0.75 12.75

Others 2 34 2.00 34.00 1.00 17.00

Total 375 6,375 337.25 5,733.25 147.75 2,511.75

2017/18 2016/17

Cotton Association of India

Crop estimates as at December 31, 2017

(bales of 170 kgs each)2017/18 arrivals by

December 31 2017

COTLOOK INDICESUS cents per lb CFR main Far Eastern ports

Cotlook 2017/2018 A Index: 89.35 -0.25

Indian medium grade 86.75 86.75

Memphis/Orleans/Texas 89 89.00

Brazilian 90 90.00

Ivory Coast BEMA 90.5 90.50

Burkina Faso RUDY 90.5 90.50

2-Jan

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Liverpool Report January 2, 2018

CAI’s estimate of arrivals to December 31, at 14.8 million bales, would represent almost 40 percent of the estimated crop for the season. Today’s seed cotton arrivals are privately estimated at about 179,500 lint equivalent bales (170 kgs). This figure includes 50,000 registered in Maharashtra, 40,000 in Gujarat, and 38,000 in Andhra Pradesh/Telangana. Markets

Prices for Shankar-6 new crop have continued to fall over the holiday weekend to an average of ₹41,000 per candy, ex-gin (82.15 US cents per lb at the prevailing exchange rate). Quotes for new crop Punjab J-34 are also easy today at ₹4,250 per maund (about 81.10 cents per lb). Prices on the MCX futures platform fell during today’s morning session. By around 14.30 IST, the lead January contract had last traded at ₹20,070 per bale (₹41,984 per candy), down ₹100 from its previous close. In subsequent trading, however, the market rallied, and by around 19.30 hrs January was showing a net gain of ₹40 per bale, at ₹20,210 (roughly ₹42,275 per candy).

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Jan

-17

Fe

b-1

7

Mar-

17

Ap

r-1

7

May-1

7

Jun-1

7

Jul-1

7

Au

g-1

7

Se

p-1

7

Oct-

17

No

v-1

7

De

c-1

7Mo

nth

ly v

olu

me

(b

ale

s)

India MCX monthly volume

Supply

(in lakh bales of

170 kg)

(in’000 tonnes) (in lakh bales of

170 kg)

(in’000 tonnes)

Opening Stock 30 510 36.50 620.50

Crop 375 6,375 337.25 5,733.25

Imports 20 340 27.00 459.00

Total Supply 425 7,225 400.75 6,812.75

Demand

Mill Consumption 275 4,675 265.00 4,505.00

Consumption by SSI units 30 510 27.00 459.00

Non-Mill Consumption 15 255 15.75 267.75

Exports 55 935 63.00 1,071.00

Total Demand 320 5,440 307.75 5,231.75

Available Surplus 105 1,785 93.00 1,581.00

Closing Stock 50 850 30 510

Cotton Association of India

Balance Sheet for 2016/17 and 2017/18

Estimated as on December 31, 2017

2017/18 2016/17

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Liverpool Report January 2, 2018

On Friday, prices fell substantially for December on its last day of trading and ended the day more moderately lower for January to March. In yesterday’s half-day trading session, prices fell by ₹100 per bale each for January and February, while no business was recorded for contracts further ahead.

Turnover on Friday was 5,111 lots (127,775 bales), and 1,885 lots (47,125 bales) on Monday. Total turnover for December was 2,346,725 bales, making December the busiest trading month since March.

Pakistan Conditions in the raw cotton market have reflected a bullish mood over the past few days. The harvest is drawing to a close, and local cotton stocks remain in very tight hands. Since no lower-priced foreign cottons are available, mills with requirements to meet have been forced to chase prices higher in order to secure supplies. Some of the ginners holding better grades produced earlier in the season are still holding out for higher prices. Although the bulk of turnover has reflected hand-to-mouth spinners covering their pressing needs, some larger textile groups have also extended their coverage, which has provided an additional element of support to the market. Business in better quality cotton has been reported between Rs. 7,600/8,000 per maund (roughly 83.50/88.00 US cents per lb), ex-gin.

Previous

close Open High Low Close Change Volume

Open

Interest

29-Dec-17 20,140 20,100 20,430 20,040 19,710 -430 293 1,240

31-Jan-18 20,350 20,340 20,450 20,160 20,270 -80 4,011 8,644

28-Feb-18 20,560 20,550 20,610 20,340 20,460 -100 800 1,887

31-Mar-18 20,780 20,680 20,780 20,610 20,730 -50 7 29

30-Apr-18 20,180 - - - 20,180 0 0 1

31-May-18 20,100 - - - 20,100 0 0 0

MCX December 29, 2017

rupees per 170 kilo bale (lots of 25 bales)

Previous

close Open High Low Close Change Volume

Open

Interest

31-Jan-18 20,270 20,240 20,240 20,080 20,170 -100 1,537 8,841

28-Feb-18 20,460 20,430 20,460 20,270 20,360 -100 348 1,916

31-Mar-18 20,730 - - - 20,730 0 0 29

30-Apr-18 20,180 - - - 20,180 0 0 1

31-May-18 20,100 - - - 20,100 0 0 0

29-Jun-18 - - - - 20,800 20,800 0 0

MCX January 1, 2018

rupees per 170 kilo bale (lots of 25 bales)

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Liverpool Report January 2, 2018

Turkey Raw cotton imports in November amounted to 67,742 tonnes, up from 50,589 the previous month, and also higher than the 59,627 tonnes recorded during the same month a year earlier.

At 282,858 tonnes, the cumulative total for the first four months of the international cotton season is appreciably higher than the corresponding figure (187,090) for last season.

Greece was by far the largest supplier in November, accounting for 28,750 tonnes (over 42 percent) of the total, followed by Brazil with 13,796 tonnes (20 percent). More modest quantities were sourced from Central Asia (5,942 tonnes), West Africa (5,742), the United States (5,720), Syria (3,129) and Australia (2,151).

Egypt A further 1,085.5 tonnes were registered for export by Alcotexa (the exporters’ association) during the week ended December 30 (week 17 of the current marketing season), bringing the running total for shipment this season to 41,199.03 tonnes. This is the highest figure by the corresponding week during any season since 2010/11.

Of the quantity registered, actual shipments amounted to 11,259.58 tonnes.

The latest registrations comprised 100 tonnes of Giza 88 at 152.00 US cents per lb FOB, 533 tonnes of Giza 86 at an average price of 146.00 cents, 361.5 tonnes of Giza 94 at an average of 138.00 cents and 91 tonnes of Giza 95 at 125.00 cents.

0

20,000

40,000

60,000

80,000

100,000

120,000

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r

May

Jun

Jly

ton

ne

s

Turkish raw cotton imports

2015/16 2016/17 2017/18

-10,000

10,000

30,000

50,000

1 6 11

16

21

26

31

36

41

46

51

Week No. September through August

Egyptian export sales by

December 30 (Week 17)(tonnes)

2016/172017/18

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Memphis Report January 2, 2018

Nearby cotton contracts ended the session on

heavy losses between 69 and 119 points low-er. The March ’18 contract opened near un-changed and moved to negative ground early in the session. Buyers lifted the spot month to gains, reaching an intraday high of 79.29 cents/lb around 1200 GMT. Once the nearby March contract reached its high, resistance was met and the most active contract fell back to negative territory, eventually falling to triple point losses. Buyers remained on the sidelines over the remainder of the day and the March ’18 contract settled on steep losses at 77.50 cents/lb (-113).

For the month of December, the March ’18 contract gained 582-points and for the 2017 year, gained 916 points.

US recaps, including Low Micronaire lots, continue to attract interest in multiple markets.

The latest CFTC On-Call Cotton report for the week ended December 22 showed a new record of unfixed on-call sales amounting to a total of 153,225 contracts. March ’18 unfixed on-call sales were reported at 53,130 contracts.

ICE estimated volume at 34,100 contracts, higher than Friday’s 23,804. At the time cotton settled, the US dollar was trading lower while corn, soybeans and wheat were all trading higher.

Total open interest increased by 3,692 contracts to 282,689. March ’18 interest increased by 690 contracts to 175,374 and May ’18 interest increased by 1,510 contracts to 54,078. Certificated stocks were last reported at 47,601 bales.

Blustery conditions were reported across West Texas over the holiday weekend, with overnight lows ranging from -4° (F) to the upper teens, and wind chill read-

ings dipping into the single digits or below zero. Wind chill advisories, therefore, remain in effect for most of the region this morning. A wintry mix fell over the weekend, but no significant snow accumulations were recorded. Fields are frozen today, and outside activities are at a standstill. Much warmer weather is expected to return tomorrow, with daytime highs climbing into the 40°s and 50°s (F). Gins are resuming pressing operations, fol-lowing a brief shut down for the New Year holiday. Wintry conditions also were reported elsewhere in the state over the three-day holiday weekend. Scattered showers fell in South Texas, but amounts were nearly immeasurable. Below-average temperatures remain in

(Continued on page 2)

ICE Futures

Crop Developments

ICE No. 2 Cotton

Open High Low Settle Change

Mar '18 78.64 79.29 77.30 77.50 -113

May '18 78.92 79.40 77.60 77.77 -119

July '18 79.19 79.52 77.95 78.14 -110

Oct '18 - - - 74.77 -69

Dec '18 74.45 74.69 73.75 74.13 -38

Mar '19 73.90 74.24 73.68 74.22 +35

May '19 73.55 73.55 73.54 74.03 +69

July '19 73.23 73.75 73.23 73.73 +73

Oct '19 - - - 72.36 +47

Dec '19 71.02 71.13 70.94 70.93 +12

ICE estimated futures volume: 34,100

*Data includes implied trades which are not posted on ICE end of day report

Cotlook Daily Copyright Cotlook Limited (Disclaimer Notified)

Memphis Report January 2, 2018

the week’s forecast, with highs only reaching the 60°s (F) by Friday. Most fields have already been prepared for winter, and producers are making plans for the

upcoming season. Soils are being sampled, and the application of fertilizers is expected to increase this month. Slow-soaking rains, though, would be welcome through February to enhance groundwater table sup-plies. Frigid weather rules in the Memphis Territory today as an Arctic air mass hovers across the Delta. Many north-ern areas dipped into the single digits overnight, and wind chill readings were reported from below zero to the low teens. Highs for most locales will range from the mid-20°s to the low 30°s (F) today. Slightly warmer condi-tions are expected tomorrow, but temperatures will remain some 20° below normal for this time of year through Friday. Outside activities, therefore, will be limited. The Arctic front entered the Southeast late in the holiday weekend, and unseasonably cold weather remains in the near-term forecast. Soils are frozen in many cotton producing areas, hindering winter field preparations. Although a few of the smaller pressing plants have closed for the season, most of the larger gins are still work-ing through backlogs of seed cotton supplies on their yards. Meanwhile, mostly cloudy, warmer-than-normal conditions have been reported in the Far West. Daytime highs will climb into the 70°s (F) in California’s San Joaquin Valley today. The month of December was unseasona-bly dry, and as a result, it was ranked as the 5th lowest on record by the National Weather Service. According to the California Department of Water Resources, lack of wintry precipitation in the Sierra Nevada Mountains during the last quarter of 2017 resulted in an unusually low snowpack of 23 percent of normal in the southern Sierra as of December 31. This compares with the 95 percent reported at the same time in 2016 and 86 percent in 2015. Thus, a prolonged snowy period is needed in the upcoming months to help boost the win-ter snowpack in the Sierra Nevada Mountains.

Crop Developments