zeel company presentationakamai.vidz.zeecdn.com/zeetele/pdfs/presentationdec2010... ·...

TRANSCRIPT

1

COMPANY OVERVIEW

DECEMBER 2010

2

DISCLAIMER

Some of the statements made in this presentation are forward-looking statements andare based on the current beliefs, assumptions, expectations, estimates, objectives andprojections of the directors and management of Zee Entertainment EnterprisesLimited (ZEEL) about its business and the industry and markets in which it operates.

These forward-looking statements include, without limitation, statements relating torevenues and earnings. The words“believe”, “anticipate”, “expect”, “estimate”, “intend”, “project” and similar expressionsare also intended to identify forward looking statements.

These statements are not guarantees of future performance and are subject torisks, uncertainties and other factors, some of which are beyond the control of theCompany and are difficult to predict. Consequently, actual results could differmaterially from those expressed or forecast in the forward-looking statements as aresult of, among other factors, changes in economic and market conditions, changes inthe regulatory environment and other business and operational risks. ZEEL does notundertake to update these forward-looking statements to reflect events orcircumstances that may arise after publication.

ZEE ENTERTAINMENT

Hindi

Entertainment

Sports Channels

Regional

Entertainment

English

Entertainment

Music & Lifestyle

Largest Indian TV Network in the World

3

Leading Hindi Entertainment Network

4

Leading Sports Network

5

Leading Regional Entertainment Network

6

English Entertainment

7

8

Indian Music and Lifestyle Network

9

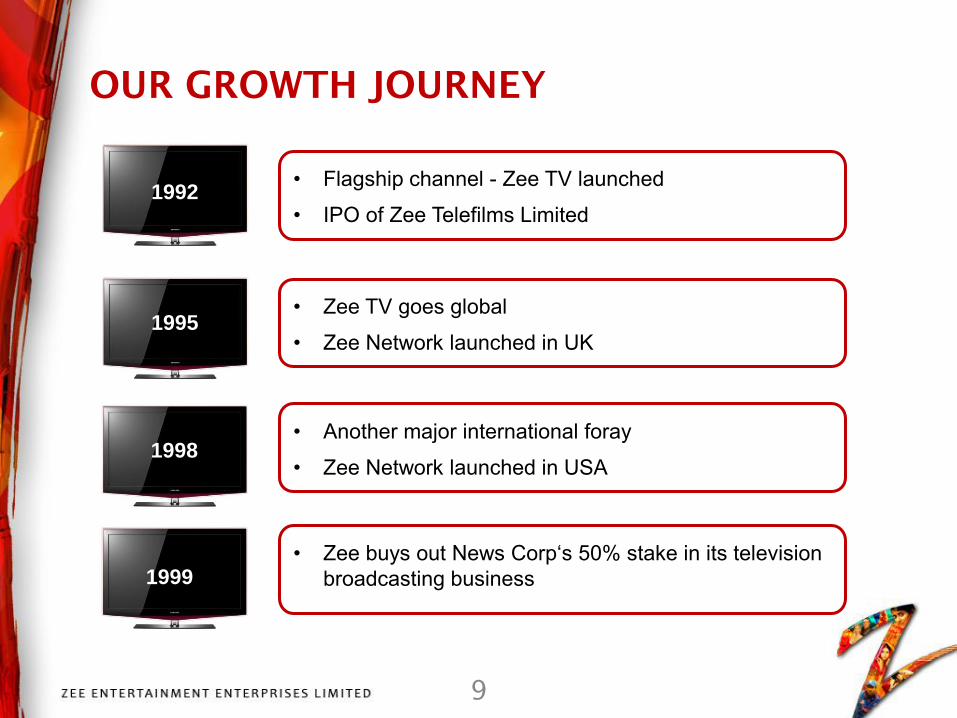

OUR GROWTH JOURNEY

1992

1995

1998

1999

• Flagship channel - Zee TV launched

• IPO of Zee Telefilms Limited

• Zee TV goes global

• Zee Network launched in UK

• Another major international foray

• Zee Network launched in USA

• Zee buys out News Corp‘s 50% stake in its television broadcasting business

10

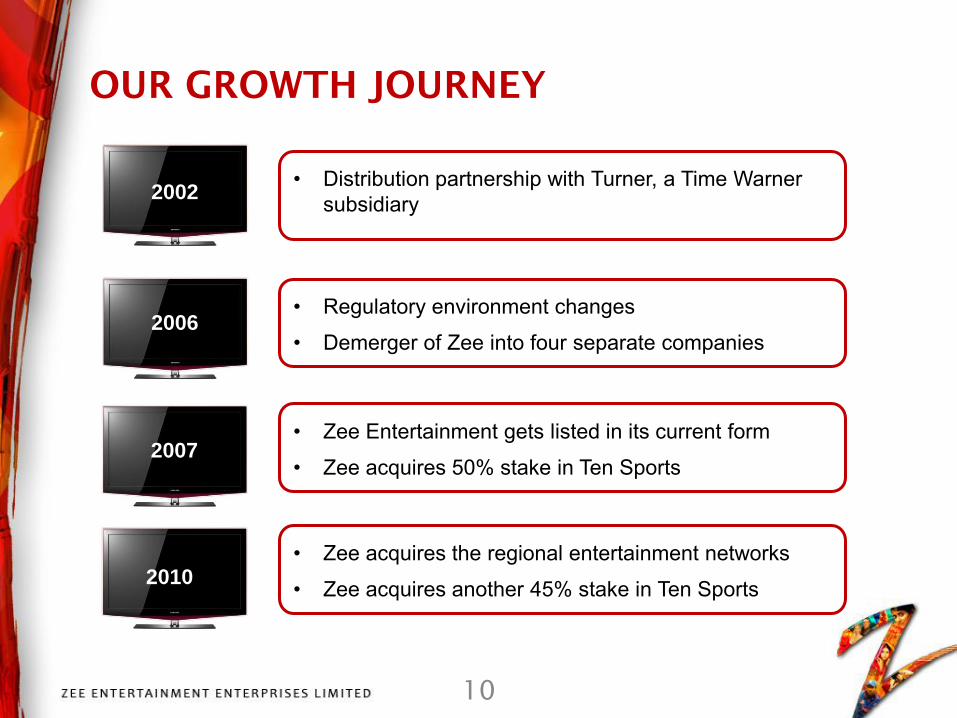

OUR GROWTH JOURNEY

2002

2006

2007

2010

• Distribution partnership with Turner, a Time Warner subsidiary

• Regulatory environment changes

• Demerger of Zee into four separate companies

• Zee Entertainment gets listed in its current form

• Zee acquires 50% stake in Ten Sports

• Zee acquires the regional entertainment networks

• Zee acquires another 45% stake in Ten Sports

BACKDROP: BUOYANT INDIAN ECONOMY

Source: Central Statistical Organization (CSO), National Council of Applied Economic Research (NCAER)

India less impacted by meltdown; Recovery faster than rest of the world

GDP is expected to grow at 8.4% this fiscal year

Infrastructure spending expected to double in the 12th Five-Year Plan to $1

trillion from $500 billion in the 11th Five-Year Plan ending 2011-12

4.4%5.8%

3.8%

8.5%7.5%

9.5% 9.7% 9.2%

6.7%7.4%

8.4%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E

YoY Growth in India's real GDP, March fiscal-year ends, 2001-2011E

-0.2%

6.3%

-7.2%

10.0%

0.0%

5.2%3.7%

4.7%

1.6% 0.2%

6.6%6.4%

2.4%

6.8% 6.0%

8.5% 8.1%

13.6%

9.3%

3.1%

10.4%8.8%

5.7%

6.9% 7.5% 8.8%

9.9%11.3%

10.2%10.4%

9.3%

8.3%8.7%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E

India's Real GDP Growth by Sectors, 2001-2010

Agriculture & Allied Activities Industry Services Sector

11

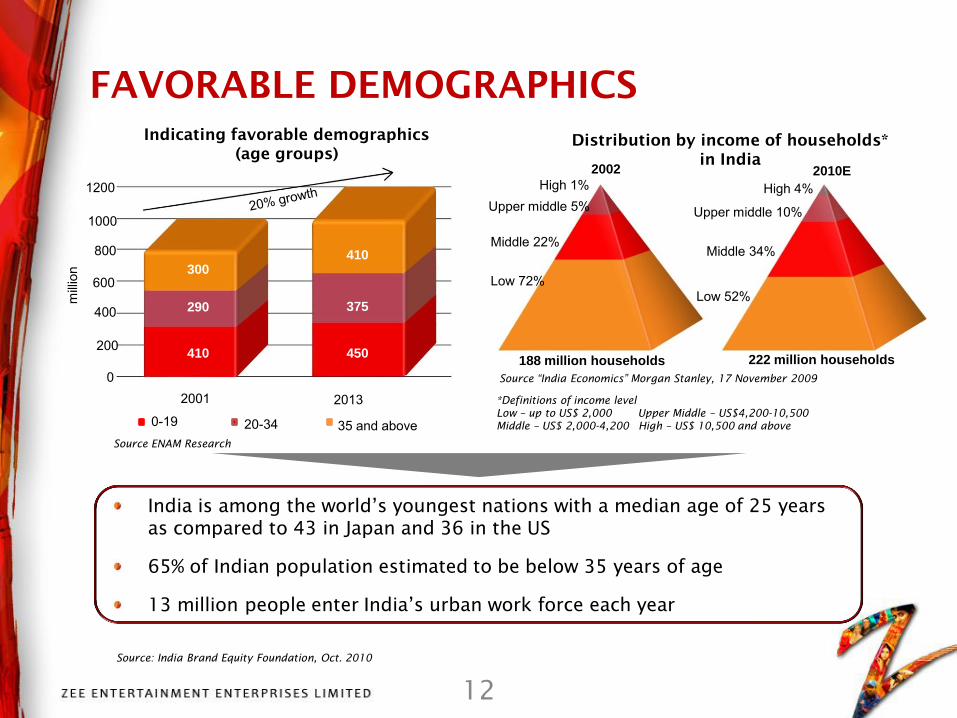

FAVORABLE DEMOGRAPHICS

India is among the world’s youngest nations with a median age of 25 years

as compared to 43 in Japan and 36 in the US

65% of Indian population estimated to be below 35 years of age

13 million people enter India’s urban work force each year

Source ENAM Research

Distribution by income of households*

in India

2002 2010EHigh 1%Upper middle 5%

Middle 22%

Low 72%

High 4%

Upper middle 10%

Middle 34%

Low 52%

188 million households 222 million households

Source “India Economics” Morgan Stanley, 17 November 2009

*Definitions of income level

Low – up to US$ 2,000 Upper Middle – US$4,200-10,500

Middle – US$ 2,000-4,200 High – US$ 10,500 and above

400

600

800

1000

1200

0

Indicating favorable demographics

(age groups)

milli

on

20132001

410

290

300410

375

450200

Source: India Brand Equity Foundation, Oct. 2010

2002 2010E

12

0-19 20-34 35 and above

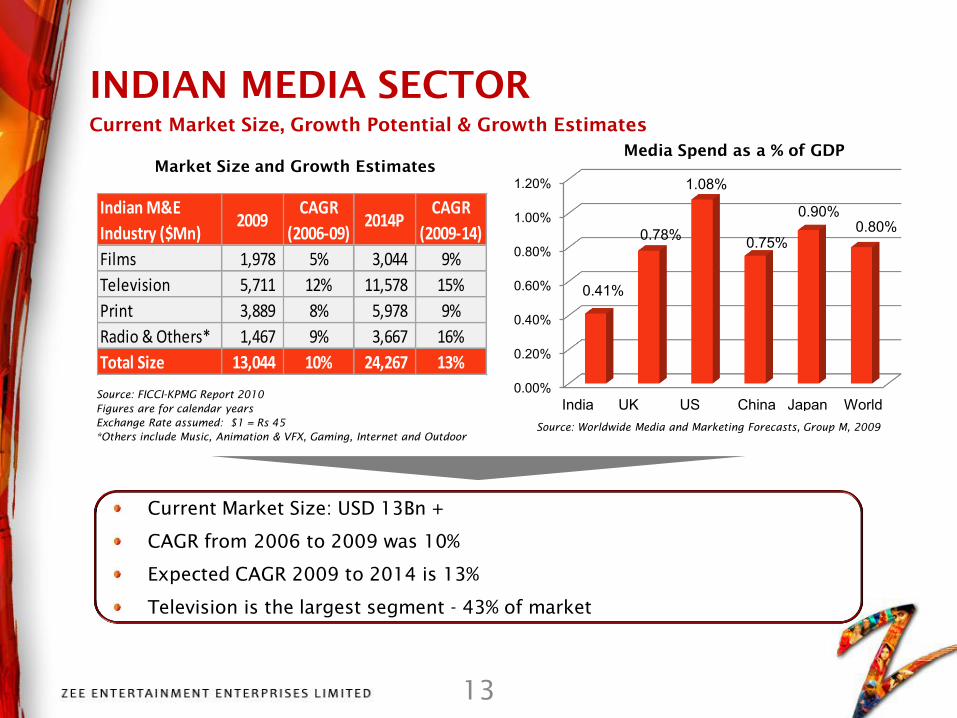

INDIAN MEDIA SECTOR

Source: FICCI-KPMG Report 2010

Figures are for calendar years

Exchange Rate assumed: $1 = Rs 45

*Others include Music, Animation & VFX, Gaming, Internet and Outdoor

Source: Worldwide Media and Marketing Forecasts, Group M, 2009

Current Market Size, Growth Potential & Growth Estimates

Indian M&E

Industry ($Mn)2009

CAGR

(2006-09)2014P

CAGR

(2009-14)

Films 1,978 5% 3,044 9%

Television 5,711 12% 11,578 15%

Print 3,889 8% 5,978 9%

Radio & Others* 1,467 9% 3,667 16%

Total Size 13,044 10% 24,267 13%0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

India UK US China Japan World

0.41%

0.78%

1.08%

0.75%

0.90%0.80%

Media Spend as a % of GDP

Market Size and Growth Estimates

Current Market Size: USD 13Bn +

CAGR from 2006 to 2009 was 10%

Expected CAGR 2009 to 2014 is 13%

Television is the largest segment - 43% of market

13

14

Reach of almost 500 million TV viewers

Number of channels: 450+

Average time spent on watching television: Approx 2.5 hrs per day

Intensive Competition in the Distribution space:

Six private DTH players

More than 5,000 MSOs

More than 60,000 LCOs

INDIA - TELEVISION LANDSCAPE

Source: FICCI-KPMG Report 2010; Figures as on end of calendar year 2009

69, 77%

4 5%

16 .

18%

0 , 0%

Pay TV Subscriber Base

(Mn Subs)

Analog Cable Digital Cable

DTH IPTV

95 , 74%

34, 26%

No. of Cable and Satellite (C&S)

HHs (Mn Subs)

C&S HHs Non-C&S HHs

129, 58%

93, 42%

No. of TV Households

(HHs) (in Mn Subs)

TV HHs Non-TV HHs

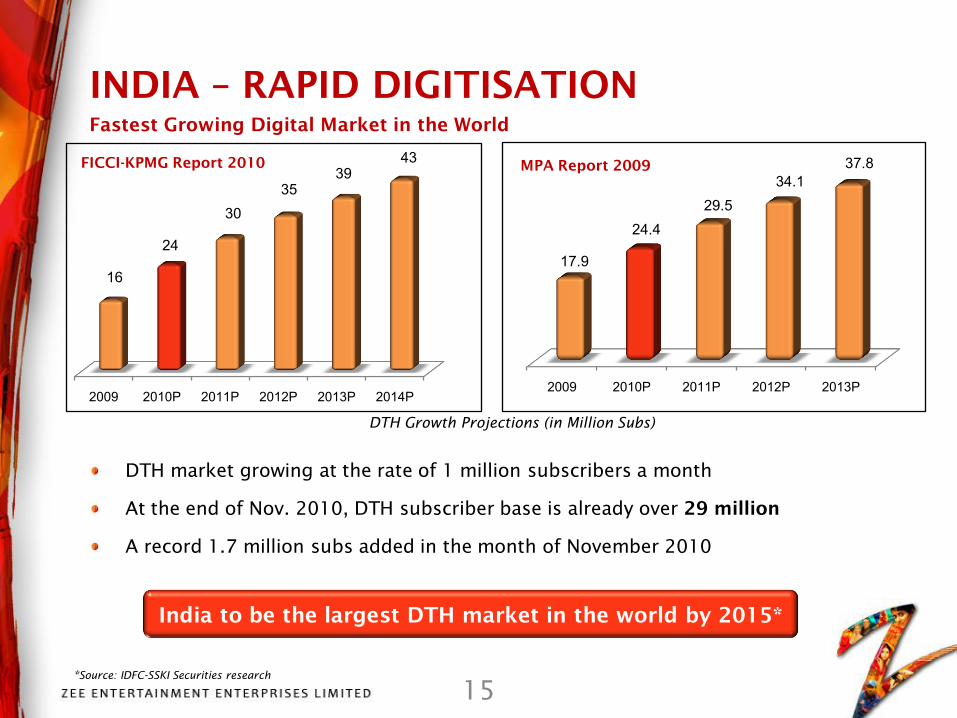

INDIA – RAPID DIGITISATION

Fastest Growing Digital Market in the World

DTH market growing at the rate of 1 million subscribers a month

At the end of Nov. 2010, DTH subscriber base is already over 29 million

A record 1.7 million subs added in the month of November 2010

India to be the largest DTH market in the world by 2015*

*Source: IDFC-SSKI Securities research

DTH Growth Projections (in Million Subs)

2009 2010P 2011P 2012P 2013P 2014P

FICCI-KPMG Report 2010

16

24

3035

3943

2009 2010P 2011P 2012P 2013P

MPA Report 2009

17.9

24.429.5

34.137.8

15

16

17

HINDI ENTERTAINMENT

HINDI MOVIES

ENGLISH ENTERTAINMENT & MOVIES

* 9X – Acquisition subject to Court approvals

PRODUCT OFFERING

18

REGIONAL LANGUAGE ENTERTAINMENT (R-GEC)

SPORTS

INTERNATIONAL

MUSIC/ LIFESTYLE/ NICHE

PRODUCT OFFERING

19

NETWORK VIEWERSHIP TRENDS%

V

iew

ership Share

Source: TAM Media Research, All Universe, All Markets of India, Total Network Cumulative Average Weekly Channel Shares, Calendar year

numbers

Zee

Star

Sun

Sony

Sony

Sun

Zee

Star

20

Advertising Subscription Other Sales

FY2010 Revenues: Rs 21,966 million

REVENUE CONTRIBUTION

21

BUSINESS PERFORMANCE

22

HINDI ENTERTAINMENT CHANNELS

Zee TV is the largest Hindi entertainment channel of the world

Source: TAM Media Research, Period: Q2FY11; Zee’s Cinema Channels- Zee Cinema, Zee

Premier, Zee Action, Zee Classic; TG: CS 4+, HSM; MAX ratings- non-cricket

Zee Cinema - The leading Hindi movies channel in India

Star Gold 21%

Filmy 5%

Zee Cinema 30%UTV 15%

Max 26%

HINDI MOVIE CHANNELS

23

STRONG MOVIE LIBRARY

The Largest Hindi Movie Library in the World

24

SPORTS CHANNELS

25

26

SPORTS CHANNELS - KEY PROPERTIES

27

Source: TAM Media Research, Period: Q2 FY2011; Zee’s Sports Channels- Ten Sports & Zee Sports: CS Male 15+, All India

Ten Sports, Zee Sports & Ten Cricket- The leading

sports network of the country

Key properties in FY2011- West Indies vs South

Africa Series, Zimbabwe - India - Sri Lanka

Triangular Series, UEFA Champions League, Europa

League, WWE, India South Africa series, Asian

Games, Ryder Cup in Golf

CRICKET, SOCCER, TENNIS & MORE

Zee sports 50%

28

Tie-ups with leading studios from across the world

ENGLISH LANGUAGE CHANNELS

29

Zee Marathi – No. 1 channel in the

marathi language

Other regional offerrings - Zee Bangla,

Zee Telegu, Zee Kannada

Zee’s regional networks have a library

of over 32,000 hours of content and

rights to over 1,750 movie titles.

REGIONAL CONTENT - HIGHLIGHTS

Source: TAM Media Research, Period: Q2FY11, CS 4+, All

Maharashtra

30

INTERNATIONAL OPERATIONS

Presence across 5 continents through

over 15 channels

Catering to both South Asian as well

as non South Asian communities

Recent local language launches in

Russia, South East Asia, Saudi Arabia

International subscription contributed

19% of company top line in FY10

Renewed focus on advertising as a

source of revenues

31

1H FY 2011 RESULTS

APRIL 2010 – SEPTEMBER 2010

32

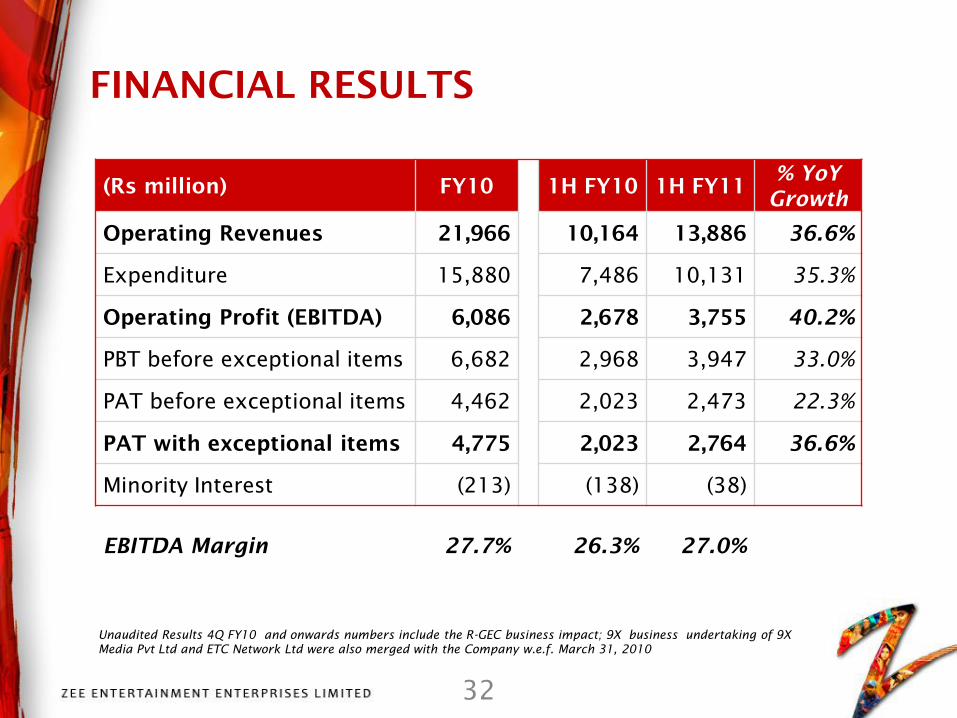

FINANCIAL RESULTS

Unaudited Results 4Q FY10 and onwards numbers include the R-GEC business impact; 9X business undertaking of 9X

Media Pvt Ltd and ETC Network Ltd were also merged with the Company w.e.f. March 31, 2010

(Rs million) FY10 1H FY10 1H FY11% YoY

Growth

Operating Revenues 21,966 10,164 13,886 36.6%

Expenditure 15,880 7,486 10,131 35.3%

Operating Profit (EBITDA) 6,086 2,678 3,755 40.2%

PBT before exceptional items 6,682 2,968 3,947 33.0%

PAT before exceptional items 4,462 2,023 2,473 22.3%

PAT with exceptional items 4,775 2,023 2,764 36.6%

Minority Interest (213) (138) (38)

EBITDA Margin 27.7% 26.3% 27.0%

33

DTH

rev. as a %

of C

able rev.

Domestic Cable Domestic DTH

Subscription Revenue (Rs. m

illion)

GROWING DIGITAL REVENUES

Y1 Axis Figures: INR million; Y2 Axis Figures: DTH as % of Cable; Domestic DTH Q3FY10 and Q4FY10 include a non recurring

amount of Rs 49.8 million and Rs 30 million respectively; 4Q FY 10 and onwards, numbers include R-GEC business revenues;

9X business undertaking of 9X Media Pvt Ltd and ETC Network Ltd were also merged with the Company w.e.f. March

31, 2010

DTH as a % of Cable

804840 845 849 851 864

821 822

894

961

249271 283

381

467514

632683

710

787

31% 32%

33%

45%

55%

59%

77% 83%79%

82%

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1000

1200

Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Q1 FY11 Q2 FY11

34

BALANCE SHEET

Lower debt

Higher cash &

cash-equivalents

Significant level

of net cash in

balance sheet

FY2010 numbers include the R-GEC business impact w.e.f Jan 1, 2010; 9X business undertaking of 9X Media Pvt Ltd

and ETC Network Ltd were also merged with the Company w.e.f. March 31, 2010

2007 2008 2009 2010

15,159

18,354

21,773 21,998

3,204

5,423 5,480 6,135

Y-o-Y Growth in Revenues and Operating Profit (Rs Mn)

Revenue Operating profit

CONSISTENT PROFITABLE GROWTH

35

Consistent dividend payout since 1994

36

Revenues

Digitization: Big

pay opportunity

Advertising:

Continued growth

New streams:

Digital

media, syndication

OUTLOOK AND STRATEGY

Content

Innovation &

quality

Regional

revolution

Niche content

Broadcast to

narrowcast

Our Strategy

Enhance our leadership position in the genres we compete

Continue to run our business as best in class

Deploy strong cash flows to improve returns to shareholders

Returns

Consolidation

Collaboration

Disciplined

investments

37

QUESTIONS & ANSWERS

Consistent performer since inception; Shareholder value CAGR of >30% between 1992 to 2010