“zero emission” power generation from coal - …bcura.org/csl07.pdf“zero emission” power...

TRANSCRIPT

POWER

Nick Otter

8th October 2007

“Zero Emission” Power Generation from Coal

- what is being done and what needs to be done

BCURA 2007 ROBENS COAL SCIENCE LECTUREThe Institute of Physics, 76 Portland Place, London

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 2

Agenda

1st topic Why is the topic so important?

2nd topic What is it all about?

3rd topic What is happening?

4th topic What is the way forward?

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 3

Early days of coal fired power generation

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 4

Agenda

1st topic Why is the topic so important?

2nd topic What is it all about?

3rd topic What is happening?

4th topic What is the way forward?

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 5

Market Driver : GDP GrowthIncreasing demand for electricity

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 6

Note: 180 GW missing due to unknown commission year,mainly Conventional ST, Hydro & OthersSource: Alstom, UDI

Market Driver : Ageing Fleet29 % of installed capacity older than 30 years

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 7

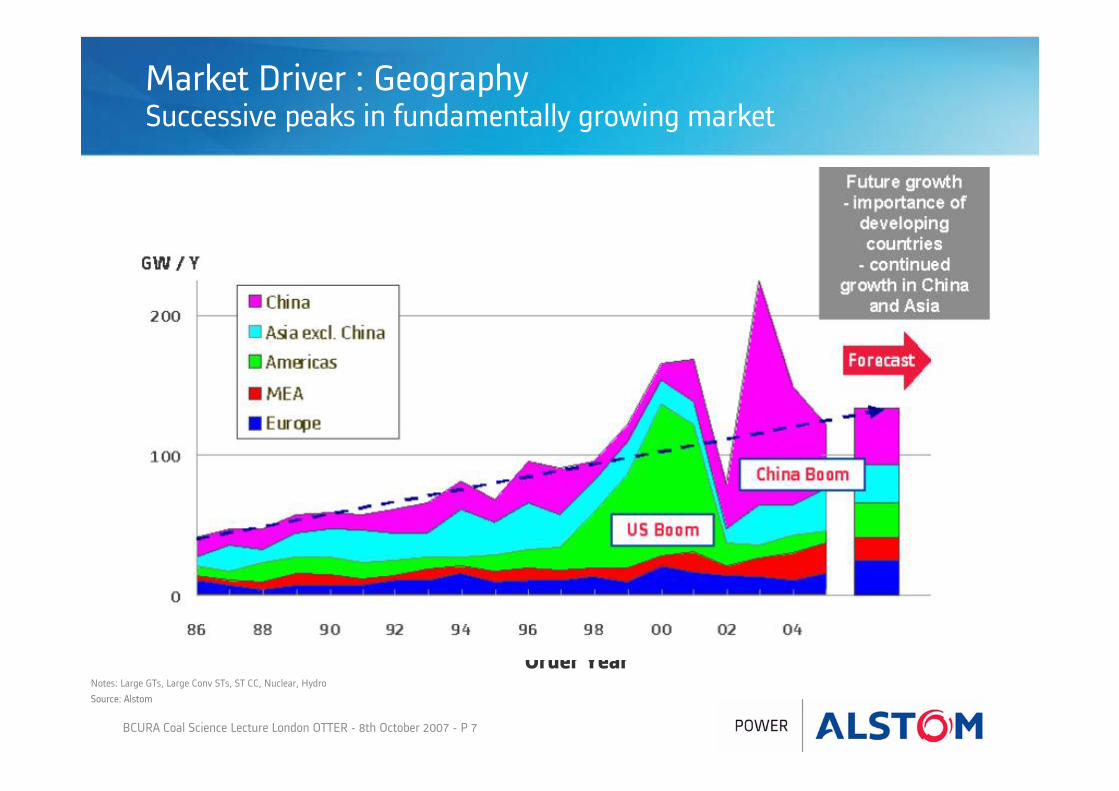

Market Driver : GeographySuccessive peaks in fundamentally growing market

Order volumes by region

Notes: Large GTs, Large Conv STs, ST CC, Nuclear, Hydro

Order YearSource: Alstom

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 8

Market Driver : TechnologyBalanced mix forecast

Order volume by technology

Source: Alstom

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 9

Market Driver : EnvironmentPower generation industry: a major contributor to CO2 emissions

0

5000

10000

15000

20000

2004 2030

million tonnes

Power Generation Industry Transport Residential & Services OtherSource: IEA

x2

* Includes agriculture and public sector** includes international marine bunkers, other transformation and non-energy use

CO2 emissions from fossil fuel combustion(reference scenario)

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 10

• Environment− What happens post 2012? − 20% GHG reductions by 2020?− 50%+ GHG reductions by 2050?

Environmental Issues

Forecasted CO2 IncreasesSource: EC/EEA, 2004

Mitigating climate change : cannot ignore fossil fuels

Rapidly changing situation …China

has overtaken US as biggest

CO2 producer in 2007

The Independent

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 11

Importance of clean use of fossil fuels, especially coal

Importance of accelerating the take-up of clean fossil

Importance of addressing issue worldwide

“Take away” Messages Summary

critical transitional issue for a sustainable energy future

an essential part of the portfolio

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 12

Agenda

1st topic Why is the topic so important?

2nd topic What is it all about?

3rd topic What is happening?

4th topic What is the way forward?

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 13

Pathway to zero emission power for fossil fuels

Originally developed for UK CAT strategy launched in 2005

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 14

Specific CO2-Emissions of Coal Power Plants

CO2 impact of efficiency increase

0

200

400

600

800

1000

1200

1400

25 30 35 40 45 50 55 60Efficiency [%]

Spec

. CO

2-E

mis

sion

s [g

/kW

h]

- 35% CO2- 35% CO2

Status of Technology

Worldwide Average

- 42%- 42%

Advanced SteamPower Plant (700°C)

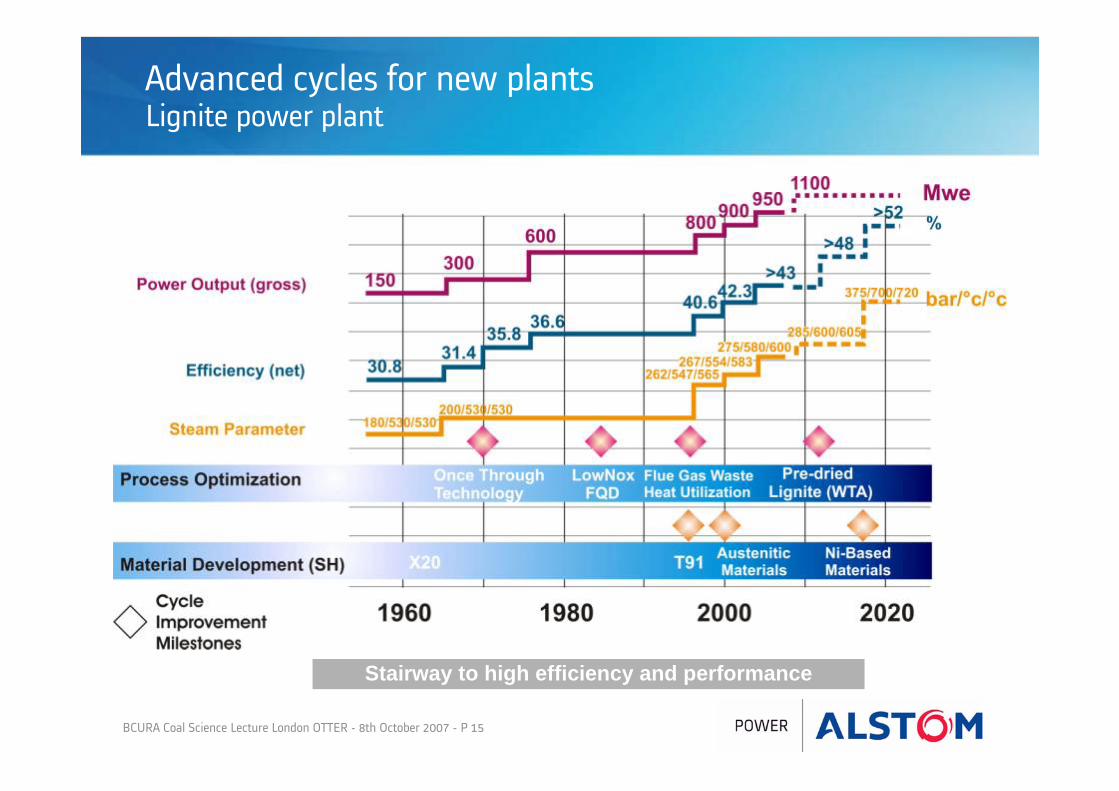

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 15

Advanced cycles for new plantsLignite power plant

Stairway to high efficiency and performance

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 16

Hazelwood 2030 project

• Contract with International Power

• Joint Alstom – RWE Technology

Drying technology can improve efficiency by 4% points

Key Features

• Removing moisture upstream of boiler

• Lignite drying from 60% moisture to 12%

• 1/8 x 200 MW Retrofit

• 500 000 t/yr of CO2 avoided

• Life extension 2030

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 17

Power Plant with CO2 Capture Pipeline

UndergroundStorage

CO2 CO2

Process Chain of Carbon Capture and Storage

Saline Aquifers

Enhanced Oil Recovery

Storage Options

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 18

Carbon Capture Technologies

• Accepted need for a portfolio approach

• All technologies need to be addressed

• Retrofit and new plant application

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 19

CO2 CAPTURE SOLUTIONSPre Combustion Solution for New Plants: IGCC+Capture

• CO2 Capture technology is proven and economical in other industries

• High Capital and Operating Costs

• Limited operation flexibility

• Plant retrofit: not generally possible

• Landspace 1,5 x PC plant for same MW

Coal gasification

Tampa Electric Company, Polk Power Station, 252 MWe, Mulberry, USA (FL)

Hydrogen-fired gas turbines

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 20

CO2 capture solutionsZero emission technology pathways

Main goal : Cost of CO2 avoided: < 20 €/t CO2

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 21

Original Equipment Manufacturer (OEM) suppliesin worldwide power plants

……..importance of addressing the installed base

OEM supplied at least the Turbine, the Generator, or the Steam Generator

Source: UDI - ALSTOM

GW

0

200

400

600

800

1000

1200

Alstom GE Siemens MHI

Nuclear Plant

Conventional SteamPlant

Hydro Plant

Gas Turbine Plant (InclST for CC)

Total World end 2005~ 4100 GW

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 22

CO2 capture solutionsPost-Combustion opportunities and challenges

− Large industrial experience

− Partial capture

− Adaptable to all boilers

− Retrofitable

− Operation flexibility

− Potential in other industries

− Advanced technologies in

pipeline

Opportunities

Innovation

Challenges

CostCost

− Solvent regeneration − Solvent consumption− CO2 compression− Integration

TechnologyTechnology− Adapt to low pressure− New solvents− Advanced process− Scale-up validation− Corrosion issues− Adaptation to installed base

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 23

0

500

1000

1500

2000

2500

3000

1990 1995 2000 2005 2010 2015 2020

Hea

t of R

eact

ion

(BTU

/lb)

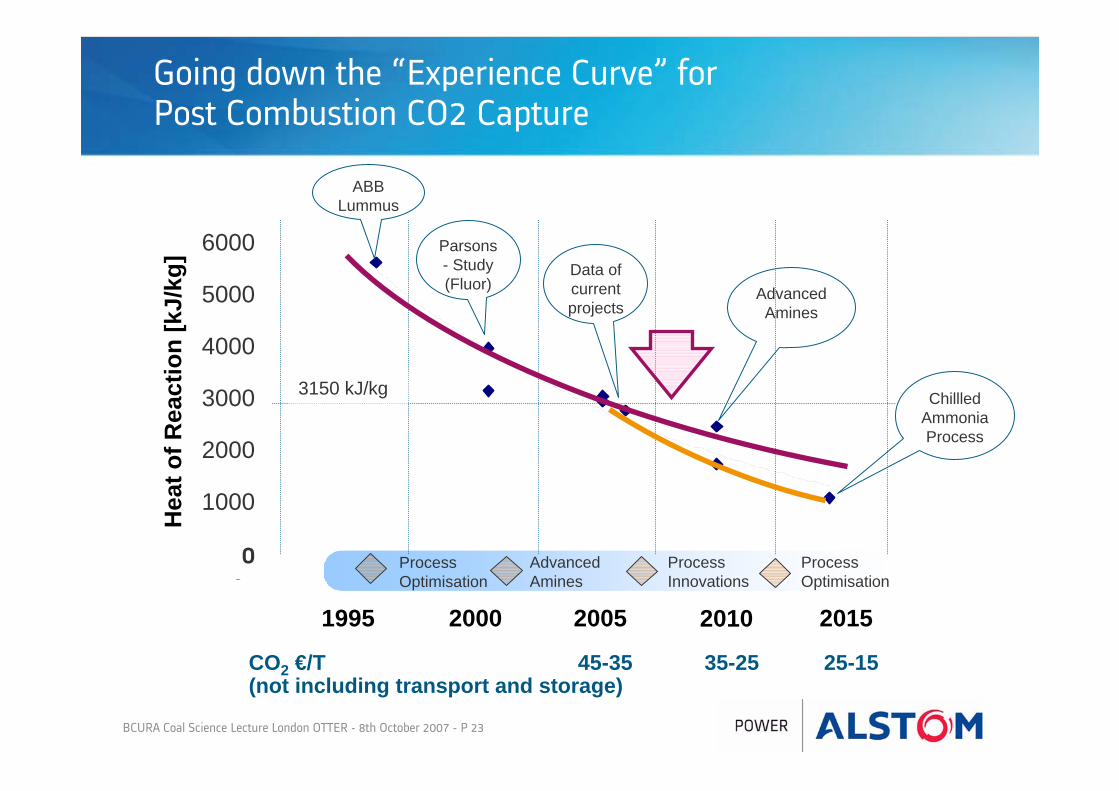

Going down the “Experience Curve” forPost Combustion CO2 Capture

1995 2000 2005 2010 2015

Parsons- Study (Fluor)

ABB Lummus

ProcessOptimisation

AdvancedAmines

ProcessInnovations

ChillledAmmonia Process

Data of current projects

1,350 BTU/lb3150 kJ/kg

6000

5000

4000

3000

2000

1000

0

Hea

t of R

eact

ion

[kJ/

kg]

Process Optimisation

CO2 €/T 45-35 35-25 25-15 (not including transport and storage)

Advanced Amines

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 24

Development Plan of Chilled Ammonia Process

2006 2007 2008 2009 2010 2011

Main Steps

Laboratory Scale

• First technical hypotheses

Large Bench Scale (0,25 MWt)

• Optimize absorber design• Establish absorber removal rate• Demonstrate limited ammonia

emissions

Field Pilot Scale (5 MWt)

• Validate key performance parameters

1

3

Demonstration Scale (30-40 MWt)

• System reliability4

2for coal and gas fired power plants

demonstration in North America and Europe

Utility Scale (+200 MWt)

• Integration5

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 25

Chilled ammonia process

A promising technology for post combustion carbon capture

Principle• Ammonia (NH3) reacts with CO2 and water. It forms ammonia carbonate or

bicarbonate• Moderately raising the temperatures reverses the above reactions – releasing

CO2

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 26

Chilled Ammonia Technology :validation at « large bench » scale

Results

• 90% Capture demonstrated

• On CO2 concentrations as low as 3-4%

• Bicarbonate solids are easy to handle

• Low NH3 emissions obtained

• Regeneration validated

• Results used to design field pilot systems at We Energies and E.ON

0.25 MW Large Bench scale

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 27

5 MWt Pilot Plant (USA)Start-up end 2007

Advantages• High efficiency capture of CO2 and low heat of reaction• Low cost reagent• No degradation during absorption-regeneration• Tolerance to oxygen and contaminations in flue gas

A promising technology for post combustion carbon capture

Chilled Ammonia Technology :validation at field pilot scale

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 28

Chilled Ammonia Technology :validation at demonstration scale

Start-up 2010 – 100 kt/yr CO2 shipped to Snøvit in Norway

Mongstad Facility– 40 MWt

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 29

CO2 capture solutionsOxy-combustion opportunities and challenges

− Lowest technological risk option

− Same power gen size possible

− Repowering and Retrofit

− All boiler technologies adaptable

− Potential boiler size reduction

− Fuel flexibility

− Rupture technology in pipeline

− Gasification

Opportunities

Innovation

Challenges

CostCost

− Cryogenic oxygen − CO2 compression− Heat flow optimisation− Integration

TimeTime− On time Development

TechnologyTechnology− Scale-up validation− Adaptation to installed base− Innovation

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 30

•Hea

tof R

eact

ion

(BTU

/lb)

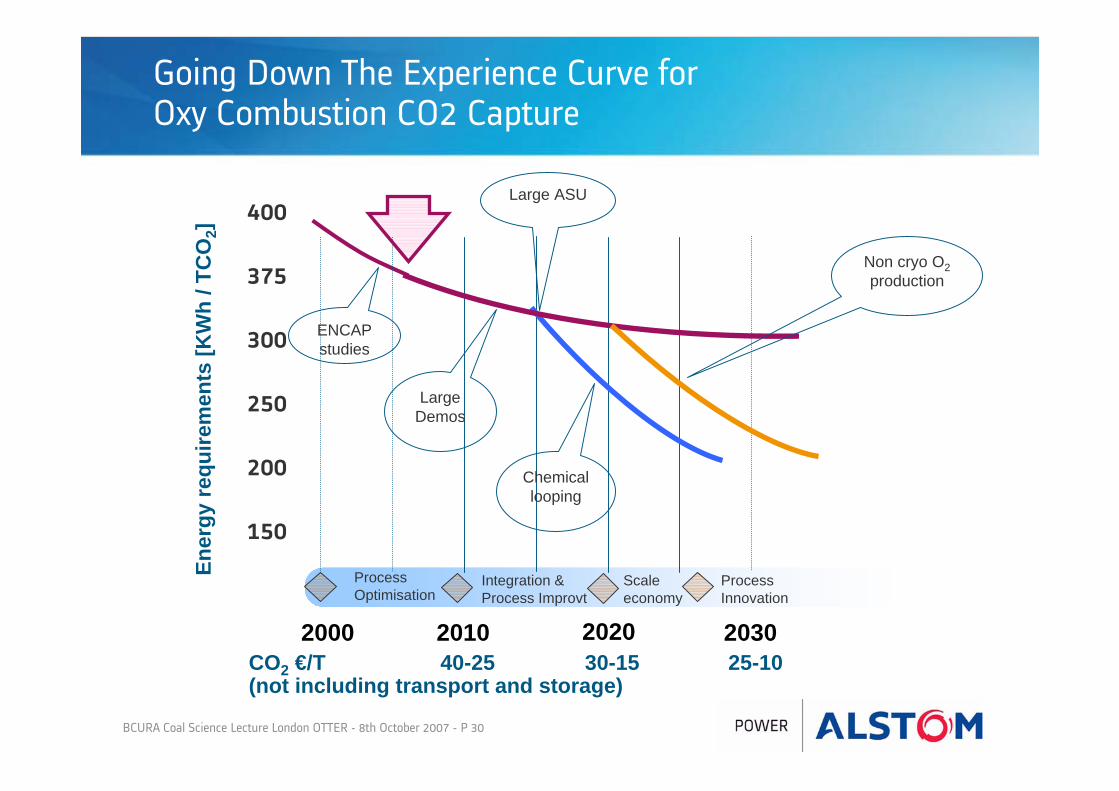

Going Down The Experience Curve forOxy Combustion CO2 Capture

2000 2010 2020 2030

Process Optimisation

Integration & Process Improvt

Process Innovation

400

375

300

250

200

150

Ener

gy re

quire

men

ts [K

Wh

/ TC

O2]

LargeDemos

Large ASU

Chemical looping

ENCAP studies

Scale economy

Non cryo O2production

CO2 €/T 40-25 30-15 25-10 (not including transport and storage)

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 31

CO2 capture solutionsOxy-combustion: 30 MWth oxyfuel demonstration scale

Test of CO2 capture at Vattenfall Site „Schwarze Pumpe“

Source: Vattenfall

Main parameters• 5,2 t/h Solid Fuel,

10 t/h Oxygen• 40 t/h Steam,

9 t/h Carbon Dioxide

• Goal: validation and improvement of oxyfuel process starting 2008

Alstom supplies the oxy-boiler (as well as steam generator and electrostatic precipitator)

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 32

Chemical Looping Gasification

Advanced Capture Processes

• Oxygen Fired CFB

• Chemical Looping

CombustionGasification

Chemical Looping Combustion H2

O2 fired CFB

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 33

Long term products: Oxy-fired PC,Oxy-fired CFB and Chemical Looping

2010 2016 - 202004 2005 2006 2007 2008 2009 2011 2012 2013 2014 2015

Commercialization

Oxy-fired PC

Lab scale tests (500kWt)

Demonstration scale tests (30MWt)

Utility scale tests (250MWe)

Oxy-fired CFB

Chemical Looping

1

2

3

4

Pilot scale (3MWt)

Demonstration Scale tests (10-40MWe)

Utility scale tests (>150MWe)

Commercialization4

2

3

1

1 Bench tests (10-100 kWt)

Pilot scale (1-3 MWt)

Demonstration scale tests 10-20 MWe

2

3

Com5

Source : ALSTOM analysis

Utility scale 50-100MWe4

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 34

Demonstration partnerships / projects

2007 2008 2009 2010 2011

CHILLED

AMMONIA

Plant Start-up

OXY-COMB

40.0

5.0

>200

30.0

5.0

0.25

STATOIL/Mongstad

EON/Karlsham

AEP/Northeastern

AEP/Mountaineer

WEnergy,EPRI

SRI,EPRI,STATOIL

30.0TOTAL/Lacq

30.0VATTENFALL/SPump

MWtGASCOAL

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 35

30

40

50

60

70

80

90

1 2 3 4 5 6 7 8 9 10 11 12 13 14

CoE

($

/ M

Wh

net)

IGCC with Capture

SCPC with Ammonia Capture

Oxy PC SCPC without Capture

IGCC without Capture

SCPC with Advanced Amine

Capture

Oxy CFB

Cost discovery zone

Carbon capture technology comparison

Cost of electricity comparison

ALSTOM technologies

A portfolio of technologies must be validated at large scale

** Based on a 400 MWnet design, versus 650 Mwnet for other technologies

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 36

..…preparing the way forward : CO2 “Capture Ready” Plant

Improve gas clean upOr possibility to add cleaning

Provisions for steam extractionsIncluding provisions for adding stagesIn the IP cylinder of the steam turbine

Control system adaptation

Provisions in arrangement planning

Provision for auxiliaryPower consumption

OptimisationOf the cooling systemRecovery of heat in the CO2 capture and compression

Optimisation of theBoiler surfaces accordingModifications of the heat load sharing

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 37

……….. multi-pollutant control

• Integrated APC system based around commercially proven and reliable technologies

• Uses readily available reagents

• Produces reusable byproduct(s)

• Superior cost/performance ratio:− Extremely compact design− Fewer moving parts reduces maintenance − Superior environmental performance

• Targeted emissions levels:− SO2: 0.02 lb/MMBTU (> 99.5%)− Hg: 1.0 lb/TBTU (> 90%)− PM: 0.01 lb/MMBTU (99.99%)− NOx: 0.05 lb/MMBTU w/SCR Controls SOx, PM10/PM2.5

Mercury & NOx

Not just CO2

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 38

…….. overall system performance and reliability

Importance of System Integration : more complex plant

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 39

CO2 Transport and Storage

Key Issues

Infrastructure Requirement

Cost Reduction

Public Acceptance

Safe and Effective Storage

Developing the Legal, Regulatory & Fiscal Framework

Safety and acceptance of CO2 storage

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 40

Agenda

1st topic Why is the topic so important?

2nd topic What is it all about?

3rd topic What is happening?

4th topic What is the way forward?

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 41

UK

Europe

International

Governmental Energy Policy Perspectives

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 42

UK

Europe

International

Governmental Energy Policy Perspectives

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 43

CAT Strategy for Fossil Fuels June 2005− alongside and complementary to other measures− Power Generation but also Industrial Processes− Efficiency through to Carbon Capture and Storage− H2FCCAT “component” demo and R&D programmes

Energy Review July 2006- acknowledged need for CCS demonstration at scale- legal and regulatory framework development- CCS in EU ETS goal- announced formation of Coal Forum

Energy White Paper May 2007- reconstituted ACCAT September 2007- strong case for CCS- CCS Demonstration Competition due November 2007

UK CAT/CCS Actions

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 44

UK CAT/CCS Missions

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 45

Energy Research− expanded overall programme and increased `CATS`− formation of Energy Research Partnership

• reinforced need for CATS/CCS

Energy Technologies Institute- formally agreed 20th September 2007- CATS/CCS likely to be one of the key themes

Environmental Transformation Fund- where the CCS Demonstration Competition will sit?- awaits CSR outcomes?

UK CAT/CCS Actions

UK expanding its support in energy … recognised role for CAT/CSS

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 46

UK

Europe

International

Governmental Energy Policy Perspectives

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 47

Internal markettowards a fully competitive market

Internal energy supplysolidarity among Member States

Energy mixdiverse efficient and sustainable

Environmentintegrated approach to tackling climate changeenergy efficiency, renewable and low C energy

Energy Technology and Innovationa strategic approach through Framework Programme FP7

External relationscoherent external energy strategy

EU Energy Policy Priority Areas

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 48

• A major new `instrument` for FP7

• Aim− to foster effective public-private partnerships between research

community, industry and policy makers

Establishment of critical mass actionsDeployment of technology

Industrial leadership

EC FP7 Technology Platforms

• Energy Topics− Hydrogen and Fuel Cells (HFP)− Electricity Networks (SmartGrids)− Photovoltaics (PVTP)− Solar Thermal (ESTTP)− Biofuels

− Zero Emission Fossil Fuel Power Plants (ZEP)

Strategic in nature for EuropeBasis for pan-EU actions

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 49

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 4

ETP ZEP :Set-up and Vision

• Primary task to set and implement strategic research agenda (SRA) and deployment document (SDD) as a major European action

• Advisory Council formed in June 2005, updated June 2007 : individuals represent

– 6 Generators: E.ON, Endesa, Enel, Energi E2, RWE, Vattenfall – 6 Equipment suppliers: Ansaldo, ALSTOM, Air Liquide, Foster Wheeler, Doosan

Babcock, Siemens– 5 Oil and Gas: BP, Shell, Statoil, Total, Schlumberger– 6 Research: BGS, CIRCE, IFP, Polish CMI, GEUS, TU-Hamburg– 3 NGOs: Bellona, E3G, WWF– 1 Financeer: Morgan Stanley– Chair: Kurt Haege/Vattenfall Vice-Chairs: Olivier Appert/IFP, Gardiner Hill/BP, Charles

Soothill/ALSTOM, Frederic Hauge/Bellona

• Formally launched : 1st December 2005

• First General Assembly, Brussels : 12-13th December 2006• Second General Assembly, Paris : 3rd October 2007

The Vision: To enable European fossil fuel power plants to have zero emission of CO2 by 2020.

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 50

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 5

ZEP Advisory Council

TaskforceDemo&Implementation

Taskforce Technology

Taskforce Policy&Regulation

TaskforcePublic Communication

Coordination Group Secretariat

Government Group

IMPLEMENTATION OF SRA AND SDD

SRA : Strategic Research Agenda SDD : Strategic Deployment Document

ETP ZEP :Organisation and Support

High level of commitment and support from ~200 individuals in 19 countries57% industry, 39% research, 4% NGOs

Government Group

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 51

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 6

• Countries involved– UK Chair

– Germany Vice-Chair

– Norway Vice-Chair

• plus– Austria Denmark Finland France– Greece Italy Netherlands Poland– Portugal Spain Switzerland

• Support from EC– FENCO (Clean Fossil Energy) Co-ordination Action

ETP ZEP :Member State Government Group

Increasingly important to engage more fully with Governments

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 52

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 7

ETP ZEP :Strategic Recommendations

• Urgently implemen10-12 integrated large scale CCS demonstration projects EU-wide

• Establish a robust technology action across whole of CO2 chain

• Kick start the CO2 value chain with urgent short and long term commercial incentives

• Establish a regulatory framework for storage

• Gain public support through a comprehensive public information campaign

SRA : set a major R&D action to reduce costs and risks of deployment

SDD : accelerate the market for efficient zero emission power plant

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 53

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 8

Major input to EC Energy Package of 10th January 2007 especially the Communique on Sustainable Power Generation from Fossil

Fuels and hence to EU 2007 Spring Council outcomes

ETP ZEP :Impact of Strategic Recommendations

www.zero-emissionplatform.eu

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 54

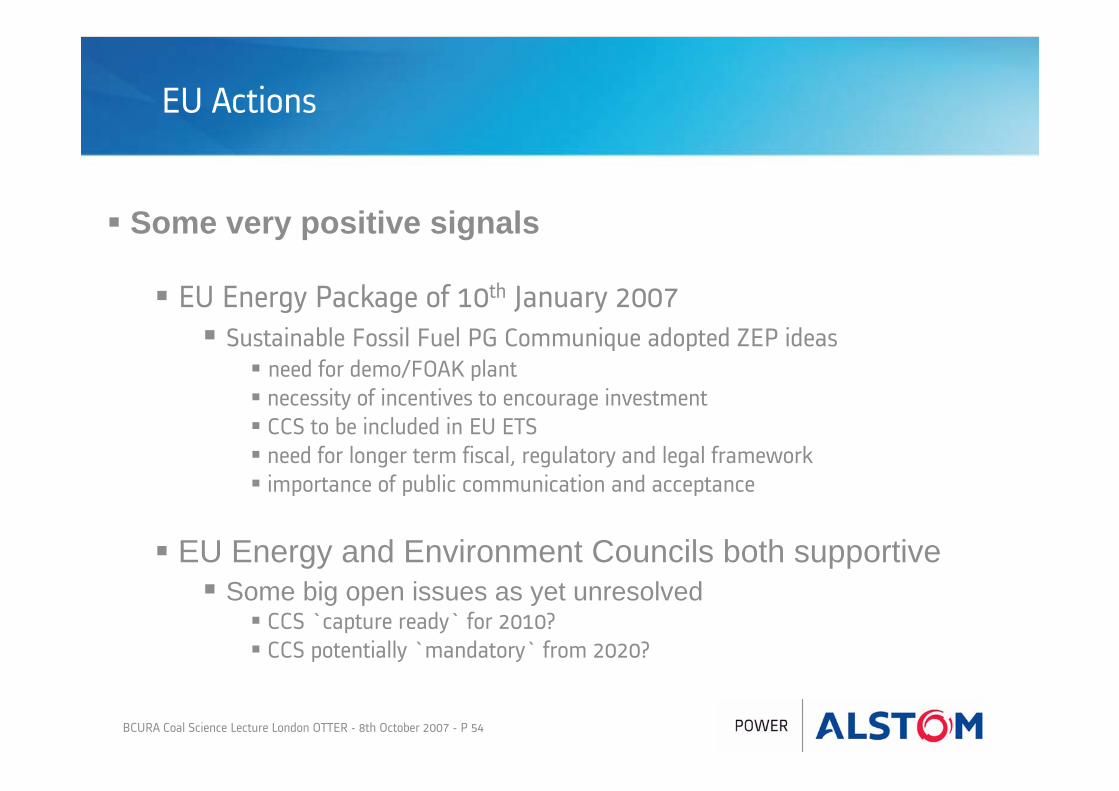

Some very positive signals

EU Energy Package of 10th January 2007Sustainable Fossil Fuel PG Communique adopted ZEP ideas

need for demo/FOAK plantnecessity of incentives to encourage investmentCCS to be included in EU ETS need for longer term fiscal, regulatory and legal frameworkimportance of public communication and acceptance

EU Energy and Environment Councils both supportiveSome big open issues as yet unresolved

CCS `capture ready` for 2010?CCS potentially `mandatory` from 2020?

EU Actions

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 55

EU Energy Policy for Europe 2007-2009“underlines importance of substantial improvements in generation efficiency and

clean fossil fuel technologies”

“urges Member States and EC to work towards strengthening R&D and developing the necessary technical, economic and regulatory framework to bring environmentally safe CCS to deployment with new fossil-fuel power plants, if possible by 2020”

“welcomes intention of EC to establish a mechanism to stimulate the construction and operation by 2015 of up to 12 demonstration plants of sustainable fossil fuel technologies in commercial power generation."

EU Strategic Energy Technology [SET] Planpriority item for Spring 2008specific reference to CCS as part of plan

Output from EU 2007 Spring Council

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 56

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 10

ETP ZEP :EU SET Plan - major outcome of 2007 Council

• ZEP Input to EU Strategic Energy Technology [SET] Plan– Holistic approach embracing all key issues

• Key ElementsI. Large scale integrated demonstration = ZEP Flagship ProgrammeII. Research and Technology Development = next generation technology, FP8 etcIII. CO2 Infrastructure = pan European network issuesIV. Public Communication = major awareness campaignV. Regulatory Framework = long term safe reliable storageVI. Fiscal Framework = short term demonstration incentives and long term investment structureVII. EU ETS = inclusion of CCS in emissions trading schemesVIII. International Collaboration = engagement of countries like China and India

EU SET Plan helps to put ETP ZEP Actions into long term overall context

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 57

2nd October 2007 ZEP and International Engagement OTTER Paris 7

ETP ZEP :demonstration – key part of an holistic approach

• ZEP Input to EU Strategic Energy Technology [SET] Plan– Holistic approach embracing all key issues

• Key ElementsI. Large scale integrated demonstration = ZEP Flagship ProgrammeII. Research and Technology Development = next generation technology, FP8 etcIII. CO2 Infrastructure = pan European network issuesIV. Public Communication = major awareness campaignV. Regulatory Framework = long term safe reliable storageVI. Fiscal Framework = short term demo incentives and long term investment

structureVII. EU ETS = inclusion of CCS in emissions trading schemesVIII. International Collaboration = engagement of countries like China and India

To provide confidence at all levels of commercial deployment of CCS

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 58

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 12

ETP ZEP :Events leading to a EU Flagship Programme

The ZEP Vision“To enable European fossil fuel power plants to have zero CO2 emissions by 2020”December 2005

The ZEP recommen-dation (SRA/SDD)10 – 12 large scale demonstration plants that will be in place and operational by 2015 across EuropeSeptember 2006

European Commission communicationTo bring environ-mentally safe CCS with new fossil fuel power plants, if possible by 2020January 2007

European Council recommendationTo establish a mechanism to stimulate construction and operation by 2015 of up to 12 demonstration plants of sustainable fossil fuel technologies in commercial power generationMarch 2007

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 59

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 16

ETP ZEP :Why an EU Flagship Programme?

• Visibility – easier to communicate• Momentum – create a step change• Knowledge – establish quicker transfer/learning to accelerate take-up• Spread - ensure geographical & technological spread• Funding - ensure effective use of public funding

To achieve commercially viable CCS in 2020

10

11

5

12

3

8

9

6

7

12

4 10

11

5

12

3

8

9

6

7

12

4

“a number of independent demo projects, to verify technology”

No strategy for sharing between projects

?10

11

5

12

3

8

9

6

7

12

4

EU Flagship program

“a well known coherent set of demo projects spread over Europe”

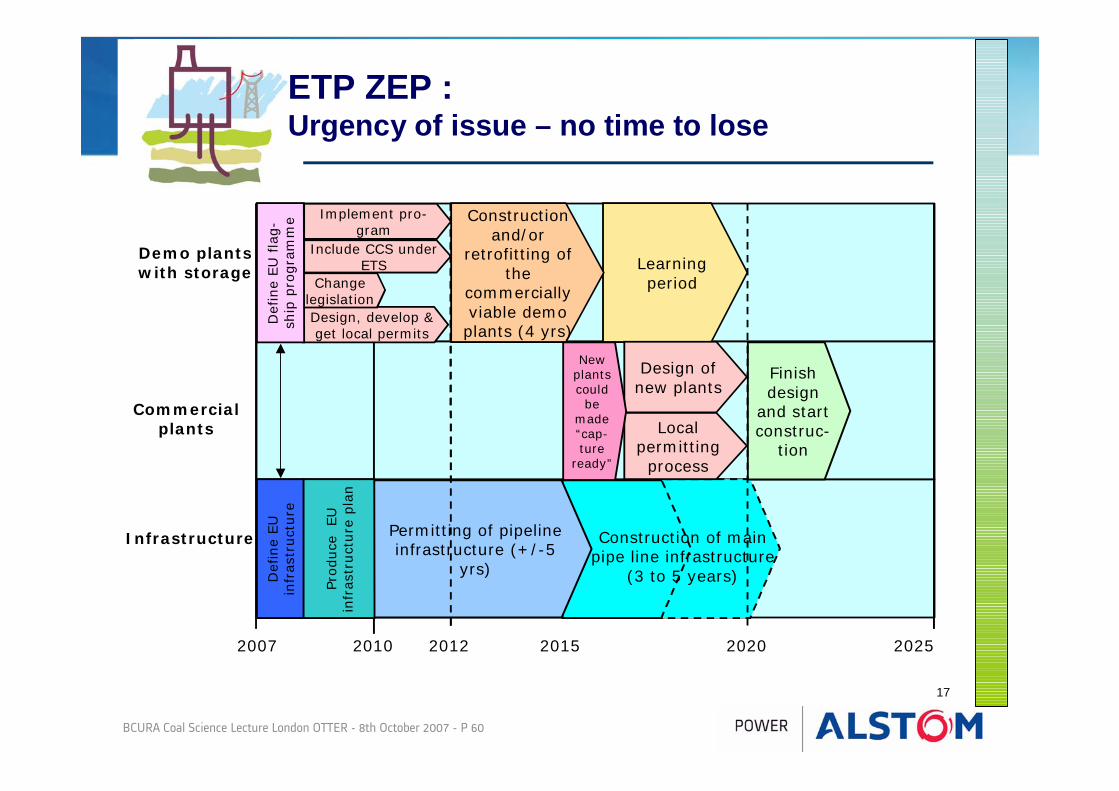

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 60

17

ETP ZEP :Urgency of issue – no time to lose

2007 20252010 2015

Demo plants with storage

Commercialplants

Infrastructure

Learningperiod

Construction and/or

retrofitting of the

commercially viable demo plants (4 yrs)

Include CCS under ETS

Design, develop & get local permits

2012

Change legislation

Def

ine

EU

fla

g-

ship

pro

gra

mm

e

Finish design

and start construc-

tionLocal

permitting process

Permitting of pipeline infrastructure (+/-5

yrs)

Construction of mainpipe line infrastructure

(3 to 5 years)

Design of new plants

Implement pro-gram

2020

Def

ine

EU

in

fras

truct

ure

Pro

duce

EU

in

fras

truct

ure

pla

nNew

plants could

be made “cap-ture

ready”

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 61

ETP ZEP :Scope of the EU Flagship Programme

Type of CO2Infrastructure

Plant technology

Trapping mechanism

(single phase gravitational, dissolution, residual, mineral; over different

timescales)

Storage geology

(cap rock and reservoir quality, overall

properties, volume etc)

Storage type (aquifers, exhausted

petroleum structures, EGR, EOR,

CBM/ECBM)

Fuel type

Capture technology

Public perception

(factors influencing the public

acceptance)

Geographical location

Portfolio of up to 12

demonstration plants give sufficient

confidence to do CCS at

scale

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 62

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 1

ETP ZEP :Issues being addressed

• Framework for Flagship Programme

• Financing Requirement

• Funding Mechanism

• Infrastructure Requirements

• Public Communication

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 63

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 20

• Purpose: Provide framework for positioning of Flagship CCS Demos

• List and definition of technology blocs• Functional specifications• Validation Status• Demonstration requirements

• Methodology:• Full CCS Value chain considered• Technologies ready for scale-up 2012

• Deliverables:• Detailed Spreadsheet

ETP ZEP :Flagship Framework

Technology Block Approach across whole CO2 chain

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 64

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 21

ETP ZEP :Technology Block Categories

Post-combustion– Fuel Combustion– Steam Cycle – CO2 enrichment in flue gas– CO2 Capture

Pre-combustion– Gasifier– Reformer– Syngas dust removal– CO Shift– CO2 Capture– Desulphurisation– H2 co-production– H2 Gas Turbine

Transport & Storage– Transport– Aquifer– EOR, EGR, ECBM– Depleted O&G fields

Efficiency– Fuel Combustion– Steam Cycle – Boiler– Turbine– Plant

Common Blocks– ASU – Air separation unit– Flue gas treatment & cooling– Fuel handling– CO2 treatment– CO2 Compression train– Overall process integration

Oxy-combustion– Fuel Combustion– Steam Cycle – Flue gas recycling (FGR)– O2 mixing w/ FG

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 65

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 22

ETP ZEP:A positioning mechanism

*Additional cost = extra cost for generating power + CCS avoided cost

Improvedtechnologies

Existingtechnologies

How many technology blocks are validated?

What is the potential to get the additional cost down?

1011

13

5

1

23

8

9

6

7

14

1215

4

Expensive Affordable

“Learning by doing axis”

“Making it affordable axis”

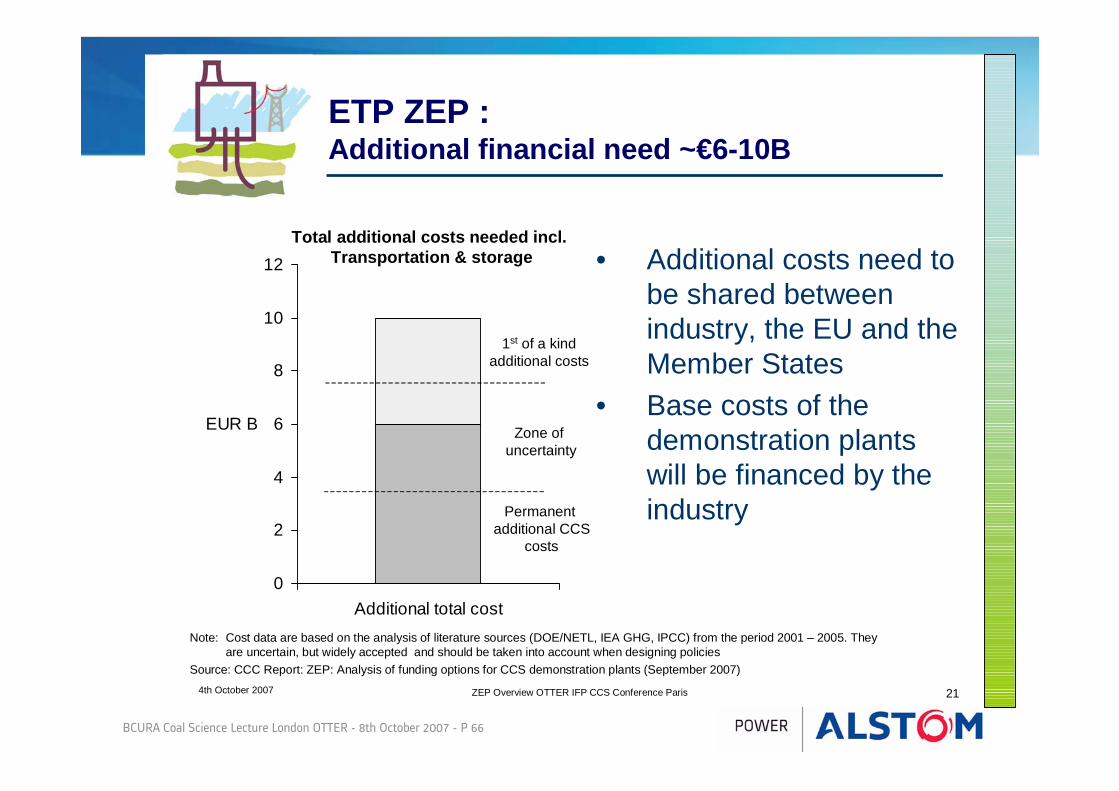

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 66

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 21

0

2

4

6

8

10

12

Additional total cost

EUR B

• Additional costs need to be shared between industry, the EU and the Member States

• Base costs of the demonstration plants will be financed by the industry

Note: Cost data are based on the analysis of literature sources (DOE/NETL, IEA GHG, IPCC) from the period 2001 – 2005. They are uncertain, but widely accepted and should be taken into account when designing policies

Source: CCC Report: ZEP: Analysis of funding options for CCS demonstration plants (September 2007)

Zone of uncertainty

Permanent additional CCS

costs

1st of a kind additional costs

Total additional costs needed incl. Transportation & storage

ETP ZEP :Additional financial need ~€6-10B

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 67

24

ETP ZEP :Funding mechanism to include several elements

Grants

• How much?• From what budget?• Through what political

process?• Coordination with

Member States?

“Market based”

• Award of incremental EUA’s?

• De-carbonized certificates?

• Feed in tariffs?• Role of Multi Lateral

Banks (e.g. EIB)?

• Which technologies?• Will projects be cross

border?

What is practicaland when?

EU Funding (Capex and Opex)Member State funding

How can marketbased options be delivered?

Flagship Projects

Relation between Member State initiatives (such as UK)

with Flagship Programme

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 68

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 2424

ETP ZEP :Importance of pan-EU infrastructure/storage

Oil fields

Gas fieldsCoal fields

IndustrialCenters

Potential Storage Sites

Fossil fuel pp

Flagship projects Flagship projects will find adequate will find adequate storage optionsstorage options

Large lines will be Large lines will be away from cities away from cities

Safety and Safety and regulatory regulatory

oversight will be oversight will be paramountparamount

EuropeEurope’’s geography will s geography will limit interconnectionlimit interconnection

Large lines will Large lines will carry up to 60Mt/yrcarry up to 60Mt/yr

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 69

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 23

Research shows that

• Without explanation, people tend to view CCS negatively:- Fossil fuels perceived to be bad- Is CO2 storage safe?

• With explanation, people tend to view CCS positively:- Rising energy demand cannot be met by renewables alone- CO2 emission targets can’t be met by renewables & energy efficiency alone- CCS can reduce CO2 on a massive scale – by over 50% by 2050- CO2 storage is safe and ‘natural’

A comprehensive public information campaign is essential

ETP ZEP :Public support is key to implementation

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 70

4th October 2007 ZEP Overview OTTER IFP CCS Conference Paris 25

• Develop suitable EU market-based funding solutions• Explore an international CO2 infrastructure

– What is the most economically feasible CO2 infrastructure, now and in the future?

– What codes and standards should be applied?– How will it be governed and financed?

• Decide how the Flagship Programme will be organised– Based on the preferred EU funding solution, what kind of organisation should

implement this solution?

• Consider interfaces outside Europe– How can the Flagship Programme be used to kick-start CCS in large CO2

emitting countries such as China, India or South Africa?

Working closely with the EC as it prepares CCS announcements in late 2007

ETP ZEP :Immediate next steps

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 71

UK

Europe

International

Governmental Energy Policy Perspectives

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 72

“the quarter finalists”AustraliaUSANorwayCanadaNetherlandsGermanyUKJapan

CAT/CCS “World Cup”

The higher up the list the more well defined Route Map and with emerging projects

“the qualifiers”Spain FrancePolandItalyAustriaDenmarkGreece

“the emerging players”ChinaIndiaSouth AfricaBrazilSaudi ArabiaSouth KoreaRussiaColumbiaMexico

CCS

“showing interest”PortugalCzechLatviaEstoniaSwitzerlandFinland

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 73

Worldwide Engagement

• Carbon Sequestration Leadership Forum (CSLF)− CSLF Technology Route Map− CSLF Project Portfolio− CSLF Stakeholder engagement

• G8 Action Plan− Financial Mechanisms/World Bank− `Capture Ready` Technology/IEA− CCT data base and worldwide case studies

• IPCC Special Report on CCS− Summary for Policy Makers : issued Sept06− Topic embraced by 2007 IPCC Report : Feb07

Austra liaBrazilCanadaChinaColombiaDenmark (new)European Commiss ionFrance (new)Germany (new)IndiaIta ly

J apanMexicoNetherlands (new)NorwayRepublic of Korea (new)Russ ian Federa tionSaudi Arabia (new)South Africa (new)UKUSAGreece (applied)

Thrust for co-ordination and engagement internationally

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 74

Agenda

1st topic Why is the topic so important?

2nd topic What is it all about?

3rd topic What is happening?

4th topic What is the way forward?

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 75

Industry oriented actions : R&D and Technology

Need for continuing R&D and Demonstration

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 76Acknowledgement to RWE, EON, SSE, NUON, Vattenfall, TOTAL, Statoil

Industry oriented actions : large scale demonstration

A portfolio of technologies must be validated at large scale

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 77

Importance of clean use of fossil fuelsa critical transitional issue in getting to a sustainable energy futurean essential part of the portfolio

Importance of accelerating the take-up of clean fossilneed for incentives for early action on `zero emission` power plantstable financial and regulatory framework to get “many of a kind”

Importance of addressing issue worldwideuse of high efficiency technologies, and ……….…………. prepare the way `zero emission`

• retrofitting of high efficient coal plant with capture to avoid “carbon lock-in”• how to ensure new plant is “capture ready”• use of low carbon technologies for new plant

Concluding Remarks

No time to lose …..urgent for action

POWER

www.alstom.com

8th October 2007

BCURA 2007 ROBENS COAL SCIENCE LECTUREThe Institute of Physics, 76 Portland Place, London

My thanks go to :

• to all those that have helped in the preparation of the talk

• to all those that have worked with me over the years to get this topic to where it is today and recognised as a critical issue

• to all those that have given me support in this quest … hopefully you will continue to do so

BCURA Coal Science Lecture London OTTER - 8th October 2007 - P 79

Future days of coal fired power generation