zoom snowbooards

DESCRIPTION

ZOOM SnowbooardsTRANSCRIPT

ISSUES IN ACCOUNTING EDUCATION American Accounting AssociationVol. 27, No. 4 DOI: 10.2308/iace-502062012pp. 1193–1213

Zoom Snowboards Incorporated:Understanding the Impact of Management

Decisions on the Audit Plan

Joanne C. Jones

ABSTRACT: Zoom Snowboards Incorporated is a fictitious Canadian private company

in the snowboard industry. While the company is fictitious, many of the facts are adopted

from actual snowboard companies. The overall goal of this case is to give the students

an opportunity to develop their ability to perform a rigorous analysis of an assurance

case with multiple issues. Students assume the role of audit senior and are asked to

prepare an audit planning memo for the partner. In order to perform a rigorous analysis,

students will need to consider the broader issues related to business strategy, risk

management, and corporate governance, as well as the regular components of an audit

planning memo. Students will also need to consider how the various requests from client

management, the bank, and the audit committee impact the financial statement audit as

they are preparing their planning memo.

Keywords: audit planning; audit risk; audit strategy.

INTRODUCTION

You are an audit senior of a public accounting firm and you have been assigned to the

financial statement audit of a rapidly growing private Canadian snowboard company,

Zoom Snowboards Inc. Due to its rapid growth, the company is facing several challenges

in its operations, financing, internal controls, and corporate governance. In addition to preparing the

audit planning memo, the partner has asked you to identify signi/ficant business risks, internal

controls, and accounting issues that he should discuss with the audit committee at its next meeting.

The partner has also asked you to prepare a response to any specific client management requests.

COMPANY AND INDUSTRY BACKGROUND

Zoom Snowboards Inc. (Zoom) designs, manufacturers, and markets high-end customized

snowboards. Bill and Emma Gage, husband and wife snowboard enthusiasts, founded Zoom in

1992. Zoom originally operated out of the Gages’ garage in Whistler (British Columbia) until 2000,

when Bill and Emma purchased a manufacturing and retail facility and began full-scale production

Joanne C. Jones is a Professor at York University.

I thank Amalia Spensieri, Sandra Iacobelli, and Larry Yarmolinsky for their helpful comments on various versions of thispaper, as well as anonymous reviewers, the discussant, and participants in the 2010 AAA Auditing Section MidyearMeeting. I also thank Elizabeth Clow for her research assistance and the professors who used this case in their classroom.

Published Online: May 2012

1193

of their snowboards. In order to finance the expansion, the Gages negotiated bank financing and

brought in a group of private investors. The Gages currently own 50 percent of the common shares,

with the remaining 50 percent held by the private investors.

Snowboarding is a winter sport that resembles surfing on a ski hill. It draws mostly the

under-30 crowd, with 85 percent of the snowboarders between the ages of 12–24 years old, 75

percent male and 25 percent female (Heine 2010). Snowboarding became popular in the early

1980s and originally carried an image of being a ‘‘rebel’’ sport. By the early 1990s, it was the fastest

growing sport and was clearly becoming mainstream (Heine 2010). In 1998, snowboarding’s

mainstream status was confirmed when it made its debut in the Winter Olympics. It is a sport that

continues to grow, especially in the male teenage segment. However, the spectacular 30 to 40

percent annual gains in industry sales of the late 1990s are long gone.

As the sport becomes more and more mainstream, this creates challenges, especially for smaller

producers like Zoom. Other cutting-edge sports, such as Telemark skiing and skateboarding, canleave snowboarding with a more conservative image and potentially dampen demand among its

youthful demographic.1 In addition, snowboarders are getting older; and larger companies, with

greater marketing resources and a wider range of products, have entered the market. Another recent

challenge has been the impact of global warming on the snow season. Despite these challenges, Bill

and Emma see a long and prosperous life for Zoom Snowboards. They are committed to the

company and have no plans for an exit strategy.

To order a custom snowboard, customers go to the Zoom website and select from various

graphic designs and board models to put together their unique board. Unlike other companies that

are in the custom snowboard market, what sets Zoom apart is its ability to design and deliver a

board within one week. This delivery time is considerably less than the standard eight-

week-minimum lead time offered by other custom brands. Zoom’s key to success is its patented

machinery and graphic application process, and that it makes its own materials. In addition to fast

production, Zoom is constantly experimenting with new materials and new ideas to further its

passion to build the highest quality snowboards possible. As a result, it excels in prototyping and

developing products. Since it is located in Whistler, a world-renowned ski destination with a long

ski season, when a new prototype is developed, the developers—all hardcore snowboarders

(commonly referred to as ‘‘riders’’)—often go directly out to the slopes to try out the new model.

Zoom also places great emphasis on customer feedback in its product development process. It is

constantly getting feedback from customers, sales reps, designers, and Internet users to find outwhat riders want. It also consults extensively with its Zoom Group, a collection of professional

snowboarders who provide feedback on the style and performance of its products.

Over the years, Zoom has been very successful in developing a reputation for being ‘‘leading

edge,’’ not just in its products but also in its marketing strategy. For instance, all members of its

Whistler-based customer service team are experienced snowboarders. When customers call in to get

information or advice on particular products, they speak to a real rider who has used the products.

Zoom has also been successful in increasing its profile through the sponsorship of many high-profile

snowboarders, some of whom are Olympic medalists, and its 50 on-hill representatives who

demonstrate the boards throughout North America. In addition, it was the first snowboard company

to have its own film department in charge of producing snowboard films, commercials, and blogs.

Despite its original focus being customized boards, in the last few years, Zoom has been trying to

ramp up and expand its product line. As a result, Zoom has experienced tremendous growth in a very

short period of time. In 2008, it moved beyond offering only customized boards and began offering its

most popular boards through specialized snow sports retailers. This wider distribution network led to

1 Telemark skiing, which originated in Norway, has been around for quite some time. However, this form of a free-heel skiing, which is a combination of cross-country and alpine skiing, is growing in popularity. Younger crowdsespecially like it because of the thrill of the ‘‘tele-turn’’ and the adventure of backcountry skiing.

1194 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

a 30 percent increase in snowboard sales. Also in 2008, Zoom started its own Zoom outerwear

clothing line. Zoom uses the same approach to developing its outerwear as with its snowboards. Ituses only superior materials and relies heavily upon customer feedback. Zoom’s design team iscommitted to both superior technical and fashion details, and has created an outerwear line that can be

worn as street wear as well as on the slopes. As a result, the Zoom outerwear line has been a great hitwith both snowboarders and non-snowboarders. Demand for the outerwear has been so strong that itnow represents 40 percent of Zoom’s total revenue. Given the dramatic increase in demand for Zoomsnowboards and apparel, in November 2009, Zoom opened a sales and distribution facility in

Montreal to better service its east coast market. Also in 2009, Zoom opened three more flagship stores,in Vancouver, Toronto, and Montreal, to add to its original flagship store in Whistler.

Your firm, Grand and Hall, has been Zoom’s auditor since 2003. The primary users of thefinancial statements are the bank, the investors, the board of directors, and Zoom management. It isnow July 15, 2011, and you have been assigned the responsibility as audit senior for the company’sOctober 31, 2011 audit. This is your first year on the audit, so you are trying to get up to speed

quickly since interim procedures have already been conducted.

The partner in charge has told you that the Zoom board of directors has become very interested

in improving its corporate governance. In 2009, when Zoom’s bank increased Zoom’s operatingline, it noted that Zoom had a weak corporate governance structure. As a result, the board recruitednew members and formed an audit committee. However, the board of directors still relies heavily

upon Emma and Bill to keep them informed of the various issues and risks Zoom faces. The boardis especially concerned since Zoom’s rapid growth makes it difficult to keep up to date. The boardmembers feel that they should be more proactive in their role and investigate issues independent ofthe Gages’ input. As a result, they have requested that Grand and Hall attend their next audit

committee meeting (in two weeks) and explain significant business risks, internal control issues,and significant accounting issues.

The partner would like you to prepare an audit planning memorandum that addressessignificant engagement issues and specifically identifies the matters relevant to the upcoming auditcommittee meeting. In order to prepare the memo, you reviewed the financial statements (Exhibit 1)and have consulted last year’s audit file (Exhibit 2), the partner’s notes from a recent meeting with

Emma and the CFO (Exhibit 3), and findings of the interim procedures (Exhibit 4).

Required

Using the background information from the case, as well as Exhibits 1, 2, 3, and 4, prepare theaudit planning memorandum requested by the partner (refer to Exhibit 5 for an outline of how toprepare an audit planning memorandum). Be sure to address any other significant engagementissues and consider the impact on the financial statement audit. Also, ensure you highlight the key

issues and risks that the partner should report to the audit committee at its next meeting.

Please Note: In order to complete your planning memo, you are expected to perform both

quantitative and qualitative analysis. You are also expected to research the relevant accounting andaudit standards. Keep in mind that Zoom Snowboards is a Canadian company that followsInternational Financial Reporting Standards (IFRS),2 and Grand and Hall conducts its audits inaccordance with International Standards on Auditing (ISA).3

2 All public companies in Canada must follow IFRS. However, private companies like Zoom have the option ofadopting Accounting Standards for Private Enterprises (referred to as ASPE) or IFRS. Although many privatecompanies adopt ASPE because of its less onerous disclosure requirements, others choose to adopt IFRS for avariety of reasons. Some of the reasons may include: the company has foreign investors, creditors, or suppliersthat are more familiar with IFRS; the company’s major competitors use IFRS; the company is a multinational; orthe company plans to go public in the near future.

3 The Canadian Auditing and Assurance Standards Board (AASB) has adopted International Standards on Auditing(ISA) as Canadian Auditing Standards (CAS).

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1195

Issues in Accounting EducationVolume 27, No. 4, 2012

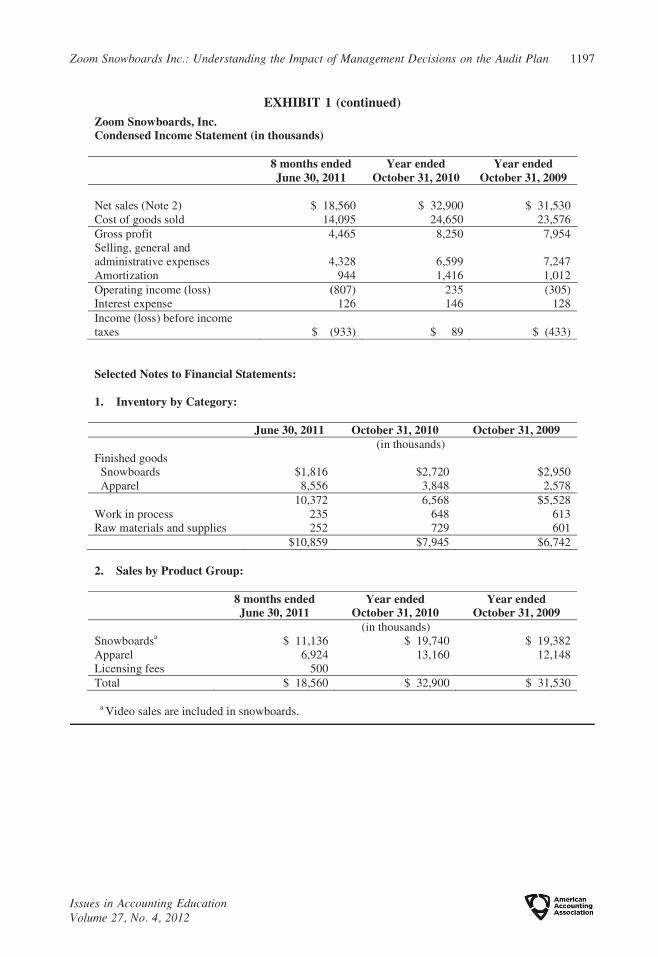

EXHIBIT 1Selected Financial Information (in Thousands)

(continued on next page)

1196 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 1 (continued)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1197

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 2Highlights of Your Review of 2010 Working Papers

(continued on next page)

1198 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 2 (continued)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1199

Issues in Accounting EducationVolume 27, No. 4, 2012

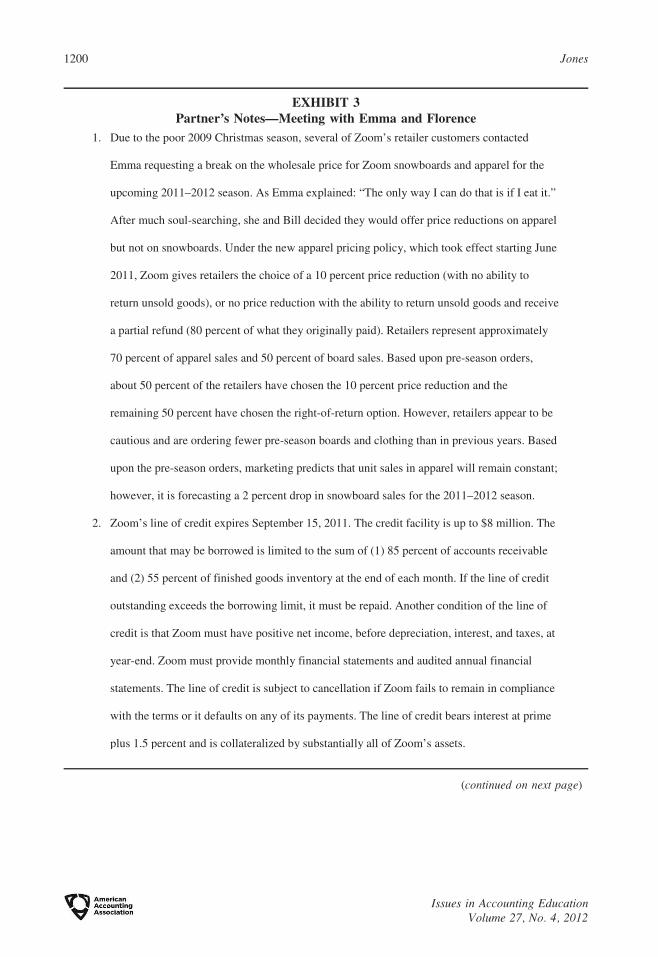

EXHIBIT 3Partner’s Notes—Meeting with Emma and Florence

(continued on next page)

1200 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 3 (continued)

(continued on next page)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1201

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 3 (continued)

1202 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 4Excerpts from 2011 Interim Working Paper Files

(continued on next page)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1203

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 4 (continued)

(continued on next page)

1204 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 4 (continued)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1205

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 5Guidelines for Preparing Audit Planning Memo

(continued on next page)

1206 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

EXHIBIT 5 (continued)

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1207

Issues in Accounting EducationVolume 27, No. 4, 2012

CASE LEARNING OBJECTIVES AND IMPLEMENTATION GUIDANCE

Overview and Learning Objectives

Zoom Snowboards Inc. (Zoom), a privately owned Canadian snowboard company, produces

snowboards, apparel, and videos. The case requires the students to prepare a planning memorandum

for the engagement partner that also highlights key issues and risks that the partner should report to

the audit committee. The students should immediately recognize that the engagement is high risk

because the bank is performing a thorough review of Zoom’s operations, and there is a possibility

that the bank will not renew its line of credit. Although this highlights that there may be a going

concern issue, in order to perform a critical analysis of the issue, the students need to consider the

broader issues related to management’s aggressive growth strategy and its approach to risk

management. The case also includes what appears to be employee fraud, and the students need to

consider both its impact on the financial statement audit as well as the client’s request that the

auditors perform a fraud investigation. Although misappropriation of assets is covered in ISA 240,

The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements, this is an area

that students have limited exposure to in most financial audit courses.4

The overall goal of this case is to give the students an opportunity to develop their ability to

perform a rigorous analysis of an assurance case with multiple issues. By successfully addressing

the case requirements, the students will learn to:

� Develop an understanding with international audit standards.� Identify engagement factors affecting client business risk, auditor business risk, inherent risk,

fraud risk, control risk, and detection risk.� Link together client business risk, financial reporting risk, and auditor business risk when

evaluating an engagement.� Formulate an audit strategy that reflects the risk factors in the case. This strategy should

consider both the overall audit approach, as well as the approach to specific high-risk

accounts.� Identify specific accounting issues and audit issues that need to be addressed on the

engagement. In addition, given the number of issues, the students will need to be able to rank

the issues and allocate the appropriate amount of attention to the issues according to their

importance.� Develop critical thinking skills that require issue identification, integration, and application

of relevant knowledge and case facts, and reach decisions about appropriate course of action

(in the context of an audit).� Develop an understanding of the impact of client requests upon planning for the financial

statement audit.� Prepare a comprehensive and rigorous analysis of the accounting and audit issues that

focuses on the partner’s concerns.� Develop a deeper appreciation of corporate governance and internal control issues faced by

privately owned companies with strong founders.� Develop written communication skills. Prepare an audit planning memo using proper

grammar, structure, and language to explain to the audit partner the key risks and issues. The

memo should also address client concerns.

4 In 2011, the equivalent American standard is SAS 99. ISA 240 and SAS 99 are essentially the same standard. In2012, SAS 99 will become AU 240 (AICPA 2011).

1208 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

Implementation Experience and Instructional Guidance

Although the company in this case is a hypothetical company, it is based upon the issues and

experiences of several smaller companies in the snowboard industry. For instance, Burton

Snowboards, as well as many others, started out of the owners’ garage (Dean 2006; Eng 2010).

Also, Emma and Bill’s decision to implement wage cuts and to forego their salary due to economic

pressures is exactly what Burton’s owners chose to do in 2009 in response to the economic

downturn (Transworld Business 2009). Zoom’s issues related to manufacturing in China, order lead

times, and pricing also reflect the actual challenges of the Canadian ski and snowboard apparel

industry (Flavelle 2007; Poggi 2010). The brief background of the snowboard industry is adequate

for the students’ analysis. If instructors wish to further their understanding of issues related to

product development, marketing, and risk diversification, they can refer to Heine’s (2010) teaching

case on Burton Snowboards, as well as the Burton website.5

This case may be used in either an undergraduate or graduate course in auditing and assurance.

Four different instructors (including the author) of an advanced undergraduate auditing course at the

author’s institution have used the case. To date, the case has been used in 15 sections with an average

class size of 40 students. The instructors have used this case in three different ways. First, it was used

as a final examination question. In this format, the students were given 105 minutes to read, analyze,

and write their responses.6 Second, the case has been used as an out-of-class written assignment for

which pairs of students prepared a planning memorandum and the case was discussed in class.

A third and alternative way we used the case was to assign the case as advanced reading along

with specific questions (mostly related to risk identification); the instructor led class discussion.

When instructors took up the case in class, most allocated approximately one hour. If instructors

decide to use this approach, we strongly suggest that the instructor require some sort of deliverable

from the students in order to ensure that the students come to class prepared to discuss the case. A

common method we used was to require the students to submit brief responses to the selected

questions.7 What we did recently was use these brief responses as part of the students’ participation

grades. (They demonstrate that they have come to class prepared.) In order to minimize paperwork

and easily track student submissions, the students electronically submitted their analyses to a web-

based submission system prior to class.8

We have also modified this approach and assigned the responsibility to lead the class

discussion to one group. That group was also required to prepare a detailed written response to the

specific questions and prepare a PowerPoint presentation.9 As in the instructor-led discussion, the

other students in the class were expected to provide brief responses to the questions and

electronically submit their analyses prior to class. When the case was used in this manner, the

assignment (for the lead group) was worth 5 percent of their total grade. The remaining students in

5 Other sources to use are websites such as Transworld Business (http://www.business.transworld.net), an actionsports magazine; and the National Ski and Snowboard Retailers Association (http://www.nssra.com). For morebackground on return policies, instructors may wish to refer to Padmanabhan (1995). Finally, since the case raisesissues related to corporate governance of privately held business with high involvement of the founders,instructors may wish to refer to Robinson (2007). The article provides some useful background on corporategovernance in family owned businesses.

6 The exam question (which did not include financial statements) was part of a three-hour final exam. Based uponthe total marks allocated to the question, students were advised that the time allocation was 105 minutes. We use arough guide of 2.5 minutes per mark; the total marks assigned for the question were 40 out of a total 70 for theentire exam.

7 We have pre-assigned the questions in Appendix A. Instructors may also choose questions from the series ofdiscussion questions provided in Appendix A of the Teaching Notes.

8 We used the Gradebook function of Turnitin.9 Since we use cases in each class, each group in the class is given the responsibility to lead one case (as well as

submit a written response to specific questions and prepare a PowerPoint presentation).

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1209

Issues in Accounting EducationVolume 27, No. 4, 2012

the class were expected to participate in class discussion. We find that when all students have read

and prepared responses, class discussion is quite lively and engaged. After the group was finished

with their presentation, the instructors took over the class discussion to ensure that all the key issues

were covered.

If instructors plan to use either of these formats, the directions and questions for the lead group

assignment are presented in Appendix A. The focus of this assignment is mostly on the

identification of risk and, in the case of the lead group format, oral communication of those risks.

The questions we have developed do not focus on all of the accounting issues; however, instructors

may choose to focus on different issues. Instructors may also choose to require all students to

submit detailed responses to specific questions (either on a group basis or an individual basis) and

the instructor leads class discussion.

Based upon student responses and instructor feedback on the case, we have created a list of

discussion prompts that other instructors can use to guide class discussion (included in Appendix A

of the Teaching Notes). When used as a final examination question and a pair writing assignment

question, the case requirements asked the students to prepare the memo requested by the partner.

The students had been exposed to several similar cases, and were provided with detailed guidance

on how to prepare a planning memorandum, throughout the semester.10

To assist instructors in assessing student responses, an evaluation guide and a grading rubric

are provided in the Teaching Notes. The evaluation guide is very comprehensive and is meant to

provide a range of potential points that could be covered in a student response. Given the

examination conditions, students were not expected to cover all the points. When the exam was set,

the preliminary expectation of the maximum grade was 40 marks, which was considered

reasonable, given the results (the highest score on the exam was 36 marks and the lowest was 21).

The grading rubric provides a competency-based assessment for the case’s key objectives and for

the writing quality of the pair assignment. The breakdown of marks by letter grade, summarized in

Table 1, demonstrates that the simulation (as either an exam question or a pair assignment) was

sufficiently challenging to differentiate the highly competent students from those who have not yet

reached the desired level of competence.

Experiential Feedback

Student responses to the written pair and group assignment were positive. They particularly

liked that they could relate the industry (one group of students brought in a snowboard when they

TABLE 1

Breakdown of Grades

Grade

Final Exama Pair Assignmenta

Number ofStudents

Percentage ofTotal Students

Number ofPairs

Percentage ofTotal Students

A 12 19% 7 20%

B 20 31% 19 55%

C 23 36% 6 18%

D 9 14% 2 6%

a Results are for two sections.

10 In their course kit, the students are provided ‘‘How to Analyze an Assurance Case,’’ prepared by the author.

1210 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

did their in-class presentation). When the case was assigned as a pair assignment, 51 students in two

sections (not taught by the author) completed an evaluation of the case. Students rated each case

component on an 11-point Likert scale, ranging from 0 to 10. Table 2 summarizes the results.11 The

students also indicated time to complete the case as well as their level of interest in the case. Since

the students worked on the case in pairs, the average time to complete the case (12.67 hours)

represents 6.33 hours per student. This time requirement met our expectations since it was the first

time the students completed a planning memo and the students were expected to research

accounting and auditing standards in order to provide a good response.

Students were asked the open-ended question: Would you recommend instructors at otheruniversities use this case? Why or why not? Of the 51 students who answered the question, 46 (90

percent) said that they would recommend the case. As to why they would recommend the case,

several students commented that the case was ‘‘comprehensive and helped to understand course

concepts.’’ Others felt that the case was ‘‘challenging and motivated them to research the accounting

TABLE 2

Student Feedback on Pair Assignment

Questiona

n ¼ 51

Mean SD Median

How much did the case help you identify factors that influence engagement risk? 7.81 (1.37) 8.00

How much did the case help you understand the influence of the factors you

identified on the level of engagement risk?

8.28 (1.10) 8.00

How much did the case help you understand how to put together a planning memo? 8.33 (1.47) 8.50

How much did the case help you understand going concern issues? 7.77 (1.62) 8.00

How much did the case help you understand issues arising from revenue

recognition?

7.48 (7.2) 7.20

How much did the case help you understand issues related to corporate governance

in small business?

7.02 (1.53) 7.00

How much did the case help you understand the issues related to a fraud

investigation?

8.44 (1.26) 8.50

How much did the case help you understand the various issues related to special

reports?

7.61 (1.54) 8.00

How much did the case help you prepare for the midterm exam? 6.96 (2.05) 7.00

How interesting was the case? 6.91 (1.56) 7.00

Case PreparationHow many hours did it take for you to complete your planning memo? 12.67 (1.92) 10.00

Who Are You?Age 25.7 (4.42) 24.5

Number of years university 4.74 (4.27) 4

Completed a previous degreeb 47% (24 students)

a The questionnaire was based upon Davies and Salterio (2007) and Feltham et al. (2003).b Our program offers a post-degree accounting certificate and is also open to students who wish to take courses on a

visiting student basis in order to complete the course requirements of the accounting designation that they are pursuing.

11 For various issues/learning objectives, respondents rated the case using a scale range from Unhelpful (0) toHelpful (10). Respondents also rated the case overall on a scale of Not Interesting (0) to Very Interesting (10).

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1211

Issues in Accounting EducationVolume 27, No. 4, 2012

and auditing standards.’’ The most common suggested improvement was to make the required more

explicit—several felt it was too vague. In this class, this assignment was the first time the students

had an opportunity to prepare a planning memo. In response to this concern, more guidance is

provided on the partner’s expectations, and a detailed template for structuring a planning memo,

based upon Early and Philips (2008), was developed and included in the case materials (Exhibit 5).

Despite student concern over the vague requirements, most students felt that the case was great

preparation for their midterm exam, which consisted of a non-directed case that required preparing a

planning memo.

TEACHING NOTES

Teaching Notes are available only to full-member subscribers to Issues in AccountingEducation through the American Accounting Association’s electronic publications system at http://

aaapubs.org/. Full-member subscribers should use their usernames and passwords for entry into the

system where the Teaching Notes can be reviewed and printed. Please do not make the Teaching

Notes available to students or post them on websites.

If you are a full member of AAA with a subscription to Issues in Accounting Education and

have any trouble accessing this material, then please contact the AAA headquarters office at info@

aaahq.org or (941) 921-7747.

REFERENCES

American Institute of Certified Public Accountants (AICPA). 2011. Substantive Difference BetweenInternational Standards on Auditing and Generally Accepted Auditing Practices. New York, NY:

AICPA.

Davies, A., and S. Salterio. 2007. Financial Times business school rankings: A nontraditional assurance

case in three parts. Accounting Perspectives 6 (1): 95–113.

Dean, J. 2006. It only looks easy. Inc. Magazine 28 (3): 112–120.

Earley, C., and F. Phillips. 2008. Assessing audit and business risks at Toy Central Corporation. Issues inAccounting Education: 23 (2): 299–307.

Eng, D. 2010. How I got started: Snowboard pioneer Jake Burton. Fortune (December).

Feltham, T. S., F. Philips, and N. Sheehan. 2003. The same difference? A transfer pricing case. Issues inAccounting Education 18 (1): 97–108.

Flavelle, D. 2007. Sellers defend cost divide. Available at: http:/www.thestar.com/printArticle/271015

Heine, P. 2010. Burton snowboards: Origins and spectacular growth. Journal of Case Research in Businessand Economics 2.

Padmanabhan, V. 1995. Return policies: Make money by making good. Sloan Management Review (Fall):

65–72.

Poggi, J. 2010. How to trade retail’s rising costs. Globe and Mail (August 26).

Robinson, G. 2007. Creating a governance system. CA Magazine 140 (5): 51–53.

Transworld Business. 2009. Burton reports salary cuts, 5% staff layoffs. http://business.transworld.net/

14120/features/burton-announces-salary-cuts-5-staff-layoffs/

APPENDIX A

INSTRUCTIONS USED FOR LEAD GROUP ASSIGNMENT

Your group is assigned to lead the discussion on Zoom Snowboards Inc. The focus of your

analysis is the risk assessment including identifying fraud risk factors, assessment of corporate

governance including discussing internal control weaknesses, and discussion of the accounting and

1212 Jones

Issues in Accounting EducationVolume 27, No. 4, 2012

audit issues associated with the going concern and the non-refundable fee for rights. Below are

some questions you are required to answer and hand in at the beginning of class. This assignment

(the report plus presentation) is worth 5 percent.

Your report should be between 2–4 pages (excluding any tables, figures, or charts that you

prepare). Your oral presentation should be no longer than 15 minutes.

Your presentation should cover the most important points in your report. You will be expected

to handle any questions that the class asks. All your group members need to be present (otherwise

they will not be given a grade for the presentation); however, you may choose as many members as

you wish to present the material.

Required

1. What are the key business risks that Zoom Snowboards Inc. is currently facing? Explain

how those risks will affect financial statement risk (FSR), explain the impact of FSR (i.e., is

it pervasive or does it impact specific accounts and assertions), and discuss how the risks

will impact the audit. (Use the table below to answer your question.)

2. Based upon your risk analysis, what is your conclusion on the risk of material misstatement

at Zoom? (Explain, along with your calculation of planning materiality.)

3. Would Zoom Snowboards Inc. be considered a high- or low-risk engagement? What

specific factors influence your judgment?

4. Discuss the current state of the corporate governance at Zoom Snowboards Inc., and explain

how this impacts your risk assessment.

5. Identify the various fraud risk factors that exist at Zoom Snowboards Inc. What is your

response (as an auditor) to these risks?

6. Is there a going concern issue with Zoom Snowboards Inc.? If so, provide your support

(consider both quantitative and qualitative factors) and your audit procedures to address this

issue.

7. Discuss the accounting treatment (revenue recognition) of the $500,000 non-refundable fee

for rights. Do you agree with the way this is being recorded in the financial statements?

What audit procedures would you undertake to audit this transaction?

8. Discuss the accounting issues surrounding the new refund policy initiated by Zoom. What

assertions are you concerned about, and what audit procedures would you need to perform

to assess the reasonableness of the accounting policy?

Zoom Snowboards Inc.: Understanding the Impact of Management Decisions on the Audit Plan 1213

Issues in Accounting EducationVolume 27, No. 4, 2012