© 2001 prentice hall10-1 international business by daniels and radebaugh chapter 10 the...

TRANSCRIPT

© 2001 Prentice Hall 10-1

International Businessby

Daniels and Radebaugh

Chapter 10The Determination ofExchange Rates

© 2001 Prentice Hall 10-2

ObjectivesTo describe the International Monetary Fund and its role in the

determination of exchange ratesTo discuss the major exchange-rate arrangements countries

useTo identify the major determinants of exchange rates in the

spot and forward marketsTo show how managers try to forecast exchange-rate

movements using factors such as balance-of-payments statistics

To explain how exchange-rate movements influence business decisions

© 2001 Prentice Hall 10-3

International Monetary Fund (IMF)Promotes international monetary cooperationFacilitates expansion and balanced growth of tradePromotes exchange-rate stabilityEstablishes a multilateral system of paymentsMakes resources available to members experiencing balance-

of-payments difficultiesIMF Quotas—each member’s monetary contribution

• Based on national income, monetary reserves, trade balance, and other economic indicators

• Pool of money that can be loaned to members• Basis for how much a country can borrow• Determines voting rights of members

Board of Governors—IMF’s highest authority• One representative from each member country• Board of Executive Directors—24 persons

– handles day-to-day operations

© 2001 Prentice Hall 10-4

IMF AssistanceProvides assistance to member countries

• Intended to ease balance-of-payment difficulties• Recipient country must adopt policies to stabilize its

economy

Special Drawing Rights (SDRs)An international reserve asset

• Used to supplement members’ existing reserves• Serves as the IMF’s unit of account

– unit in which the IMF keeps its records– used for IMF transactions

• Based on the weighted average of five currencies

Evolution to Floating Exchange RateBretton Woods Agreement established par valuesJamaica Agreement—formalized break from fixed exchange

rates• Accommodated floating exchange rates

© 2001 Prentice Hall 10-5

Exchange-Rate ArrangementsIMF permitted countries to select and maintain an exchange-

rate arrangement of their choice• IMF surveillance and consultation programs

– designed to monitor exchange-rate policies– determine whether countries were acting openly and

responsibly in exchange-rate policyFrom pegged to floating currencies

• Broad IMF categories for exchange-rate regimes– peg exchange rate to another currency or basket of

currencies with only a maximum 1% fluctuation in value

– peg exchange rate to another currency or basket of currencies with a maximum of 2 ¼% fluctuation

– allow the currency to float in value against other currencies

• Countries may change their exchange-rate regime

© 2001 Prentice Hall 10-6

Regimes

Exchange arrangements with no separate legal tenderCurrency board arrangementsOther conventional fixed peg arrangementsPegged exchange rates within horizontal bandsCrawling pegsExchange rates within crawling bandsManaged floating with no pronounced path for exchange rateIndependently floating

Number OfCountries

378

44869

2548

Total = 185

Exchange-Rate RegimesSecond Quarter 1999

© 2001 Prentice Hall 10-7

Exchange-Rate Arrangements (cont.)Black markets—exists when people are willing to pay more for

dollars than the official rate• Closely approximate a price based on supply and demand

for a currency instead of a government-controlled price• The less flexible a country’s exchange-rate

arrangements, the more there will be a thriving black market

Role of central banks—responsible for the policies affecting the value of a country’s currency

• Federal Reserve Bank of New York is the central bank in the U.S.

– sells dollars to counter upward pressure on the dollar– purchases dollars to counter downward pressure

• The primary contact with foreign central banks

© 2001 Prentice Hall 10-8

Exchange-Rate Arrangements (cont.)Role of central banks (cont.)

• Reserve assets kept in three major forms: gold, foreign exchange, and IMF-related assets

– mix of reserve assets varies across countries– intervention countries—currencies in which a country

trades the most» affects mix of currencies in reserve assets

• Based on market conditions, a central bank may:– coordinate actions with other central banks– take aggressive market position to change attitudes– call for reassuring action to calm markets– intervene to reverse, resist, or support market trend– act visibly or discreetly– operate openly or indirectly with brokers

© 2001 Prentice Hall 10-9

Exchange-Rate Arrangements (cont.)Role of central banks (cont.)

• Governments vary in their intervention policies – policies affected by government administration

• Government intervention can occur on bilateral or multilateral basis

• Bank for International Settlements (BIS)– owned by central banks– purpose is to promote cooperation between central

banks to facilitate international financial stability– acts as a central banker’s bank– involved in currency transactions among central

banks

© 2001 Prentice Hall 10-10

Determination of Exchange RatesFloating rate regimes—allow changes in the exchange rates

between two currencies to occur for currencies to reach a new exchange-rate equilibrium

• Currencies that float freely respond to supply and demand conditions

• No government intervention to influence the price of the currency

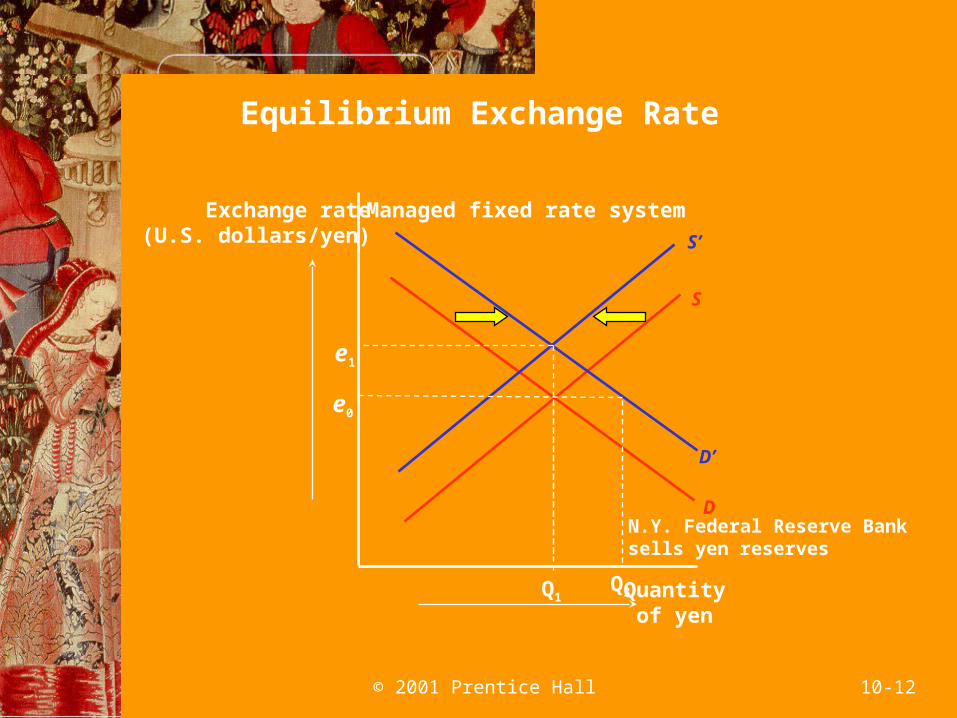

Managed fixed-rate regime—government buys and sells its currency in the open market as a means of influencing the currency’s price

• Central banks holds foreign-exchange reserves– can sell these reserves to affect exchange rates for

the currency• Governments use fiscal or monetary policy to influence

the demand for their currencies• Countries may revalue or devalue their currencies if

economic policies and intervention do not work

© 2001 Prentice Hall 10-11

Quantityof yen

Q1

Exchange rate(U.S. dollars/yen)

e1

e0

S’

S

D’

D

Equilibrium exchange ratemoves from e0 to e1

Equilibrium Exchange Rate

© 2001 Prentice Hall 10-12

Equilibrium Exchange Rate

Quantityof yen

Exchange rate(U.S. dollars/yen)

S

D

Managed fixed rate system

S’

D’

e1

Q1Q3

e0

N.Y. Federal Reserve Banksells yen reserves

© 2001 Prentice Hall 10-13

Determination of Exchange Rates (cont.)Automatic fixed rate regime—adjustment of exchange

rates is based on changes in the domestic money supply rather than government intervention

• Foreign-exchange markets have greater impact than domestic markets on exchange rates of freely floating currencies

• Not as widely used as other systems that influence exchange rates

• Currency boards operate in this system

© 2001 Prentice Hall 10-14

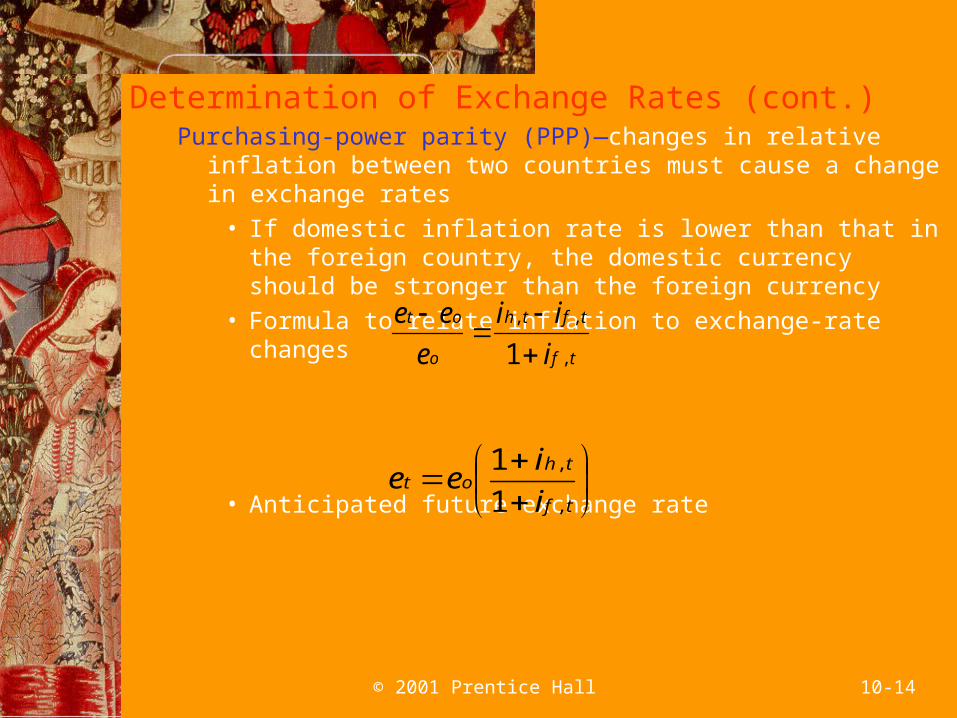

Determination of Exchange Rates (cont.)Purchasing-power parity (PPP)—changes in relative inflation

between two countries must cause a change in exchange rates

• If domestic inflation rate is lower than that in the foreign country, the domestic currency should be stronger than the foreign currency

• Formula to relate inflation to exchange-rate changes

• Anticipated future exchange rate

tf

tfth

o

ot

i

ii

e

ee

,

,,

1

tf

thot

i

iee

,

,

1

1

© 2001 Prentice Hall 10-15

Determination of Exchange Rates (cont.)Interest rates—influence exchange rates

• Fisher Effect—links inflation and interest rates– nominal interest rate in a country is the real interest

rate plus inflation

– because the real interest rate should be the same in every country, the country with the higher interest rate should have higher inflation

– International Fisher Effect (IFE)—links interest rates and exchange rates

– the interest-rate differential is a predictor of future changes in the spot exchange rate

» interest-rate differential based on differences in interest rates

– currency of the country with the lower interest rate will strengthen in the future

iRr 111

© 2001 Prentice Hall 10-16

Determination of Exchange Rates (cont.)Other factors affecting exchange rate movements

• Confidence—safe currencies considered attractive in times of turmoil

• Technical factors– release of national statistics– seasonal demands for a currency– slight strengthening of a currency following a

prolonged weakness

© 2001 Prentice Hall 10-17

Forecasting Exchange-Rate MovementsManagers should be concerned with the timing, magnitude, and

direction of an exchange-rate movement• Prediction is not a precise science

Fundamental forecasting—uses trends in economic variables to predict future rates

• Use econometric model or more subjective basesTechnical forecasting—uses past trends in exchange rates to

spot future trends in the rates• Assumes that if current exchange rates reflect all facts in

the market, then under similar circumstances future rates will follow the same patterns

• Good treasurers and bankers develop their own forecasts• Use fundamental and technical forecasts for

corroboration

© 2001 Prentice Hall 10-18

Forecasting Exchange-Rate Movements (cont.)Factors to monitor—managers can monitor factors used by

governments to manage their currencies• Institutional setting• Fundamental analysis• Confidence factors• Events• Technical analysis

Business Implications of Exchange-Rate ChangesMarketing decisions—exchange rates affect demand for a

company’s products at home and abroadProduction decisions—choice of location for production facilities

depends on strength of currencyFinancial decisions—exchange rates influence the sourcing of

financial resources, the cross-border remittance of funds, and the reporting of financial results