© 2009 by south-western, cengage learning samirlander chapter 12

TRANSCRIPT

© 2009 by South-Western, Cengage Learning

SAMSAMIRLANDERIRLANDER

Chapter 12Chapter 12

Florida Real Estate:Florida Real Estate: Principles, Practices and Principles, Practices and

License LawLicense Law

Chapter 12Chapter 12

Real Estate FinanceReal Estate Finance

© 2009 by South-Western, Cengage Learning

© 2009 by South-Western, Cengage Learning

Key TermsKey Terms

Acceleration clause

Amortized loan

Assumption

Balloon payment

Certificate of estoppel

Deed in lieu of foreclosure

Deferred interest

Deficiency judgment

Due on sale clause

Equity

Home equity loans

Hypothecation

Index plus a margin

Interest

Lien theory

Lines of credit

Lis pendens

© 2009 by South-Western, Cengage Learning

Key TermsKey Terms

Mortgage

Mortgagee

Mortgagor

Negative amortization

PITI

Power-of-sale clause

Prepayment clause

Prepayment penalty

Promissory note

Reconveyance clause

Statutory redemption

Subject to the mortgage

Subordination clause

Takeout loan

Term or straight loans

Title theory

Wraparound mortgage

© 2009 by South-Western, Cengage Learning

Mortgages and HypothecationMortgages and Hypothecation

Hypothecation: Hypothecation: Borrower retains possession

Property used as security

2 Legal theories:Title Theory

Lien Theory

© 2009 by South-Western, Cengage Learning

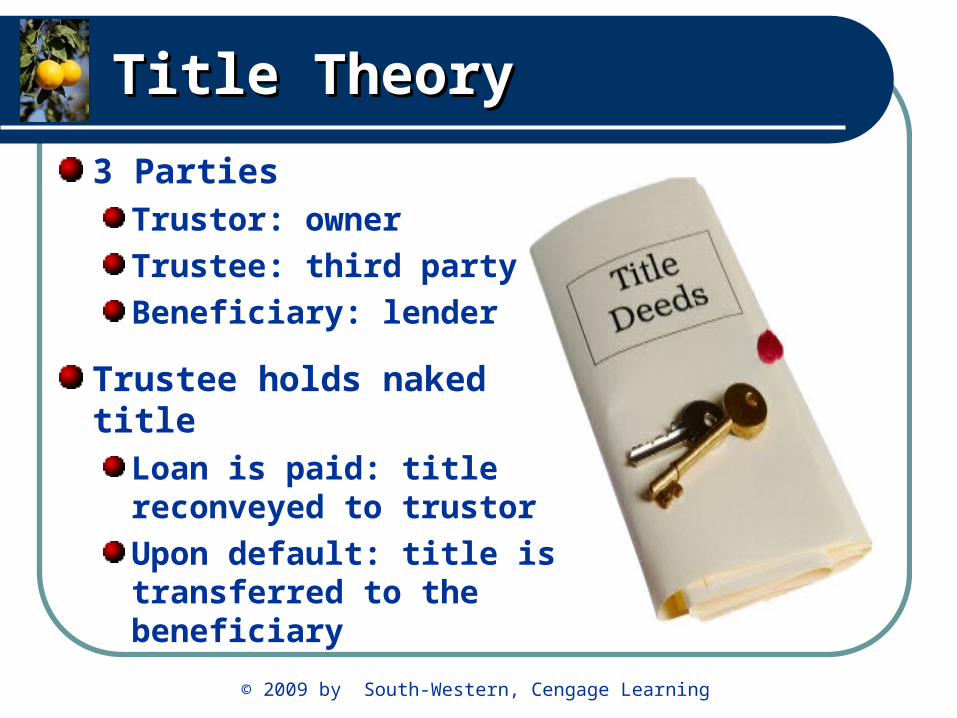

Title TheoryTitle Theory

3 PartiesTrustor: owner

Trustee: third party

Beneficiary: lender

Trustee holds naked titleLoan is paid: title reconveyed to trustor

Upon default: title is transferred to the beneficiary

© 2009 by South-Western, Cengage Learning

Title TheoryTitle Theory

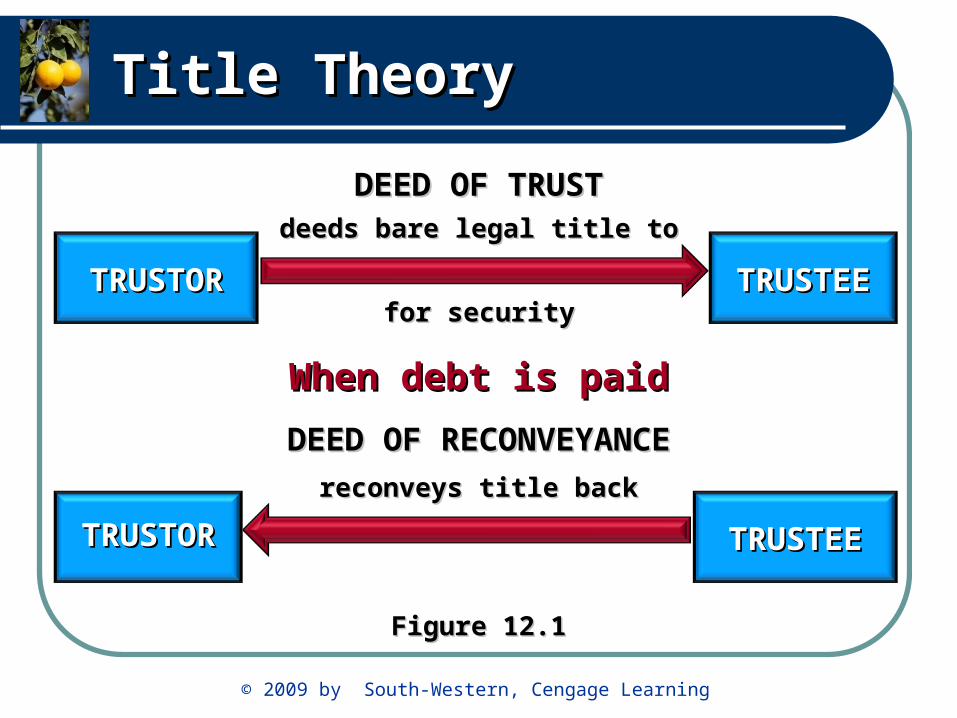

Trust deed provides security for the note

Reconveyance clause: Reconveyance clause: title returned to borrower upon payment in full

Release deed

Marginal release

© 2009 by South-Western, Cengage Learning

Title TheoryTitle Theory

TRUSTORTRUSTOR TRUSTEETRUSTEE

TRUSTEETRUSTEETRUSTORTRUSTOR

DEED OF TRUSTDEED OF TRUSTdeeds bare legal title todeeds bare legal title to

for securityfor security

When debt is paidWhen debt is paid

DEED OF RECONVEYANCEDEED OF RECONVEYANCE

reconveys title backreconveys title back

Figure 12.1Figure 12.1

© 2009 by South-Western, Cengage Learning

Title Title TheoryTheory

Power-of sale clausePower-of sale clause

Nonjudicial foreclosure:

Property sold at public auction without going to court

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Two Parties

Two instruments

Borrower has legal title

Mortgage creates a lien

Florida is a lien theory state

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Borrower's promise to pay

Prima facie: note acts as evidence of the debt

Terms of repaymentAnnual interest

Term

Type of loan

Negotiable instrument

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Will always contain:

Prepayment clause

Acceleration clause

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

May not be prepaid

May not be prepaid for a fixed period

May be prepaid

Prepaid with penalty

Prepayment penaltyPrepayment penaltyYield maintenance

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Full and immediate payment in the event borrower defaults

May be coupled with other clauses

Call in the note

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Provides security

Note without a mortgage is unsecured

Mortgage without a note is meaningless

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Parties to the mortgageParties to the mortgage

Mortgagor: Mortgagor: borrower

Mortgagee:Mortgagee: lender

Granting clauseGranting clauseTitle theory states: transfers title

Lien theory states: creates the lien

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Defeasance ClauseDefeasance Clause

Allows borrower to defeat the lien by fulfilling terms and conditions

Makes mortgage null and void when paid

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

One or more covenants

Alienation clauseAKA: Due on sale clause

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

CovenantsCovenants

Covenant to pay taxes

Covenant of insurance

Covenant against removal

Covenant of good repair

Covenant of reentry

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Alienation ClauseAlienation Clause“to transfer”

Due on saleDue on sale

Prohibits:

AssumptionAssumption

Wraparound mortgageWraparound mortgage

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

At time of contract:At time of contract:

Sales price Sales price

Remaining balanceRemaining balance

$100,000$100,000

- $80,000- $80,000

Cash requiredCash required $20,000$20,000

At time of closingAt time of closing

Sales priceSales price $100,000$100,000Remaining balanceRemaining balance - $79,000- $79,000Cash requiredCash required $21,000$21,000

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Two ways to assumePrice to control

Price is set and controls the amount of cash required

(See previous example)

Cash to controlSales prices is not fixed

Agreed amount of cash to seller controls

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Date of ContractDate of ContractRemaining balanceRemaining balance

Remaining balanceRemaining balance

Cash to be paidCash to be paid

Cash to be paidCash to be paid

Sales PriceSales Price

Sales PriceSales Price

Date of ClosingDate of Closing

$80,000$80,000

$79,000$79,000

$20,000$20,000

$20,000$20,000

$100,000$100,000

$99,000$99,000

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Buyer does not assume but makes payments

Original borrower

Gives up possession

Transfers deed

Remains liable

© 2009 by South-Western, Cengage Learning

Lien TheoryLien Theory

Certificate of estoppel Certificate of estoppel Buyer acknowledges amount owed

When selling

When placing debt on property

© 2009 by South-Western, Cengage Learning

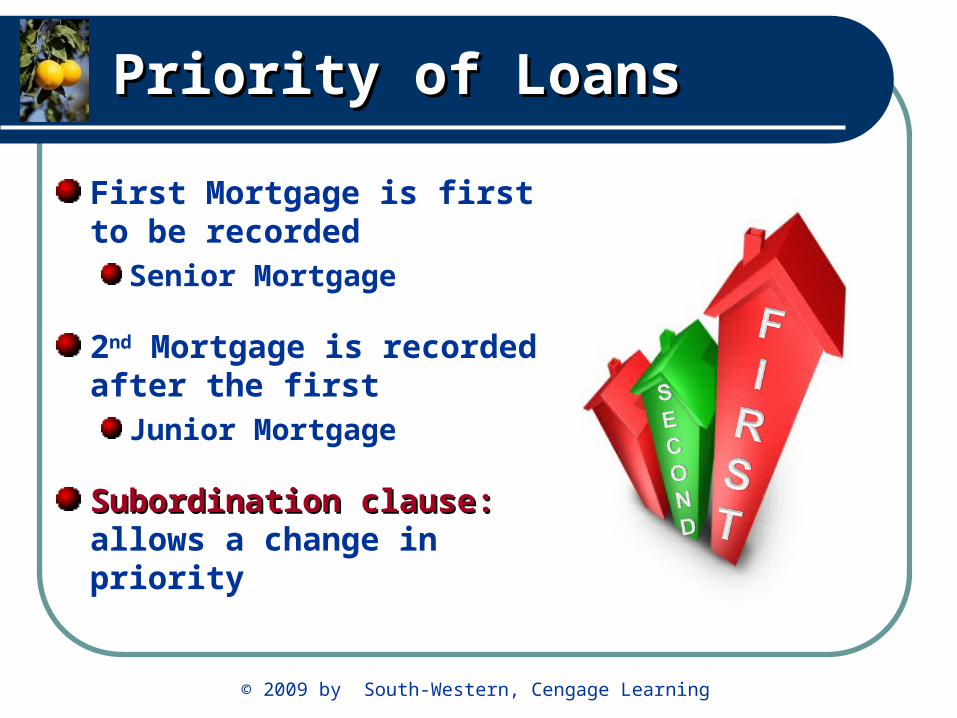

Priority of LoansPriority of Loans

First Mortgage is first to be recorded

Senior Mortgage

2nd Mortgage is recorded after the first

Junior Mortgage

Subordination clause: Subordination clause: allows a change in priority

© 2009 by South-Western, Cengage Learning

ForeclosureForeclosure

Most common

2 purposes:Lender obtains possession

Borrower’s equity is liquidated

Legal procedure upon buyer default

© 2009 by South-Western, Cengage Learning

ForeclosureForeclosure

Acceleration clause

Title search

Lis pendens

Lawsuit filed

Public notice / public auction

Court approves the sale

Lender is paid

Buyer receives title

Borrower receives excess

Nine step foreclosure process:Nine step foreclosure process:

© 2009 by South-Western, Cengage Learning

ForeclosureForeclosure

Lender bids loan amount

All others must pay cash

Recourse loan:

Deficiency judgment: Deficiency judgment: amount of outstanding debt

Nonrecourse loan:Exculpatory clause

Sheriff’s sale

© 2009 by South-Western, Cengage Learning

ForeclosureForeclosure

Excess pays other recorded liens

Period of time after foreclosure to pay the debt and reclaim the property

© 2009 by South-Western, Cengage Learning

ForeclosureForeclosure

Borrower signs deed over to lender

AKA: friendly foreclosure

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Principal: Principal: amount borrowed

Interest: Interest: money paid for using lender’s money

Term: Term: time to repay

Principal balance: Principal balance: amount owed at any point

EquityEquity: difference between

value and amount owed

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

AKA: Straight loanStraight loan

Payments cover interest only

Balloon payment: Balloon payment: principal paid in full at end of the term

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Principal and interest are paid over the term of the loan

Payment amount is the same throughout the term

Each payment covers:Interest for previous installment

Remaining toward principal

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Over the term:

Interest payment decreases

Principal payment increases

Entire principal paid by the

final payment

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

A balance remains at the end of the term

Balloon payment required

Florida law requires amount of final principal be disclosed in loan documents

© 2009 by South-Western, Cengage Learning

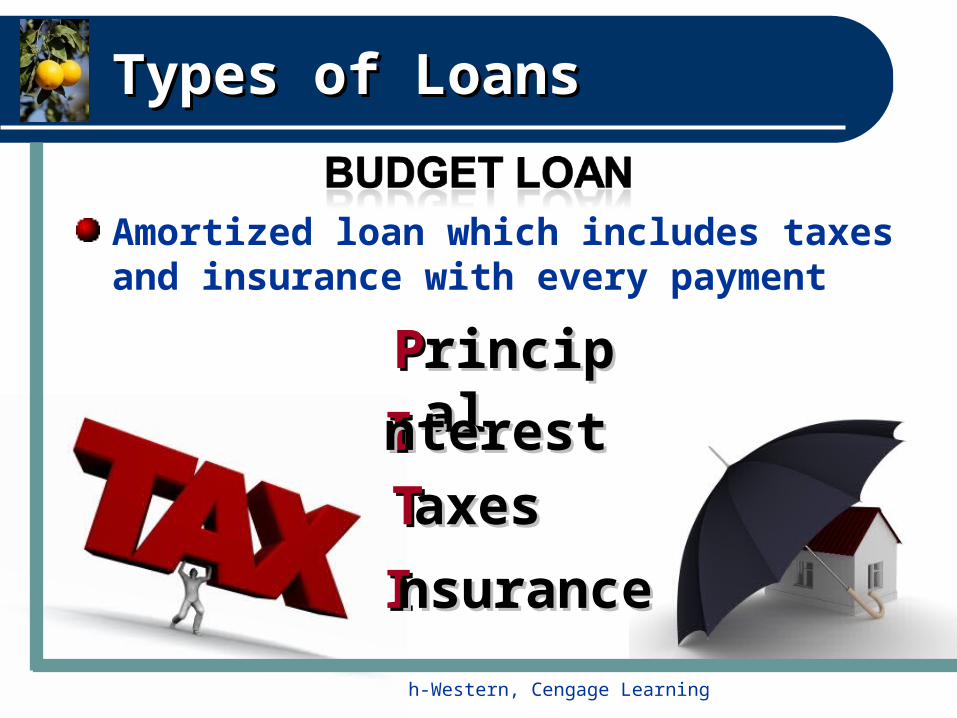

Types of LoansTypes of Loans

Amortized loan which includes taxes and insurance with every payment

PPrincipalrincipal

IInterestnterest

TTaxesaxes

IInsurancensurance

© 2009 by South-Western, Cengage Learning

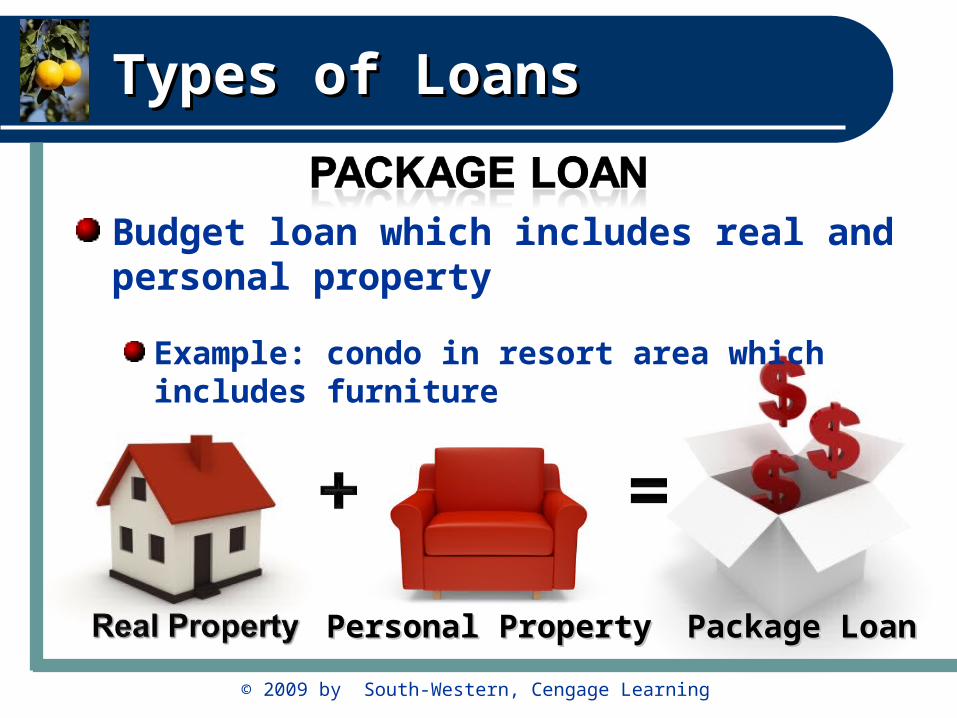

Types of LoansTypes of Loans

Budget loan which includes real and personal property

Example: condo in resort area which includes furniture

Personal PropertyPersonal Property Package LoanPackage Loan

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Seller financing

Buyer gives seller a promissory note and a mortgage

AKA: take back mortgage or

carry back financing

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Home equity loan: Home equity loan: loan to a prescribed limit

Property is pledged as collateral

Lines of credit: Lines of credit: draws on a line of credit are limited to a prescribed amount

Property is not pledged as

collateral

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

More than one property used to secure the loan

Partial release clause: allows the release of properties as the principal balance is reduced

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Low payments in the beginning which increase over time

FHA section 245

Early years result in negative amortizationnegative amortizationLoan balance increases

Payment is not enough to

cover amount due

Unpaid interest is added to

balance

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Interest rate may change

Rate is tied to an index

Loan rate = index plus a margin

Margin (spread) is a fixed number

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Adjustment limitations:

Made at the end of each adjustment period

Limit (cap) on increasesPeriodic cap

Lifetime cap

Payment cap can result in

negative amortization

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

No alienation clause1st loan assumed by buyer

Seller makes loan to buyer as a 2nd

New loan is created but original loan is not paid off

Buyer’s payment is greater than the original

Seller keeps the difference

Original rate is lower than market

rate

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

A prepaid amount reduces interest in the first few years

Lender-funded buydownRate is slightly higher but allows a lower rate during the first years.

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Short term (interim loan)

Money advanced as construction occurs

Take-out loan: Take-out loan: permanent financing Pays off construction loan

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

AKA: shared appreciation loan

Favorable terms for the borrower

Portion of the appreciation for lender

Deferred interesDeferred interest: end payment

to the lender

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Used by retirees

Borrow against the equity

Income received in monthly payments

Repaid on a specific date or

upon specific event

© 2009 by South-Western, Cengage Learning

Types of LoansTypes of Loans

Owner sells to an investor on condition of a Owner sells to an investor on condition of a lease back lease back

Frees up capital Frees up capital

Tax benefitsTax benefits

© 2009 by South-Western, Cengage Learning

Lending Practices and Lending Practices and Underwriting RiskUnderwriting Risk

Employment verification

Tax returns

Credit check

Appraisal

Loan-to-value ratio (LTV)

© 2009 by South-Western, Cengage Learning

Figure 12.3Figure 12.3

Term or straight loan

Amortized loan

Partially amortized loan

Package loans

Purchase money loan

Open-end loan

Blanket loan

Adjustable rate loan

Sale and leaseback

Shared equity

Buydown

Reverse annuity loan