© 2015 skp business consulting llp. all rights reserved. · notifications and circulars issued by...

TRANSCRIPT

© 2015 SKP Business Consulting LLP. All rights reserved.

For private circulation only.

ABOUT THIS PUBLICATION

This SKP publication contains general information existing at the time of its preparation only. It is intended as a

news update and is not intended to be comprehensive nor to provide specific accounting, business, financial,

investment, legal, tax or other professional advice or opinion or services. This publication is not a substitute for

such professional advice or services, and it should not be acted on or relied upon or used as a basis for any

decision or action that may affect you or your business. Before making any decision or taking any action that

may affect you or your business, you should consult a qualified professional adviser and also refer to the

source pronouncement/documents on which this publication is based. It is also expressly clarified that this

publication is not a solicitation or an invitation of any sort whatsoever or a source of advertising from SKP

Group or any of its entities to create any adviser-client relationship.

Whilst every effort has been made to ensure the accuracy of the information contained in this publication, this

cannot be guaranteed, and neither SKP Group nor any related entity shall have any liability to any person or

entity that relies on the information contained in this publication. Any such reliance is solely at the user's risk.

Contents

1. Introduction ........................................................................................................................... 4

2. CSR under the Companies Act, 2013 ..................................................................................... 5

2.1 Scope and Applicability ......................................................................................................... 5

2.2 CSR Committee....................................................................................................................... 6

2.2.1 Composition ........................................................................................................................... 6

2.2.2 Roles and responsibilities: .................................................................................................... 6

2.3 CSR Policy Implementation ................................................................................................... 6

2.4 Roles and Responsibilities: Board of Directors ..................................................................... 6

2.4.1 Modalities for CSR activities .................................................................................................. 7

2.4.2 Qualifying CSR activities ....................................................................................................... 7

2.4.3 Inclusive scope of CSR ........................................................................................................... 8

2.4.4 Activities expressly disallowed as CSR activities .................................................................. 8

2.5 CSR Spending ......................................................................................................................... 9

2.5.1 Computation of the amount of CSR expenditure ................................................................. 9

2.5.2 Treatment of CSR expenditure .............................................................................................. 9

2.5.3 Mandatory disclosures ........................................................................................................ 10

3. Issues relating to CSR .......................................................................................................... 11

3.1 The MCA’s Clarifications ..................................................................................................... 11

3.2 Issues Pending Clarification ................................................................................................ 13

3.2.1 Contributions to Promoters’/Directors’ family trusts ......................................................... 13

3.2.2 Net profit of Indian companies for the calculation of profit of foreign companies ......... 13

3.2.3 Acceptable reasons for non-compliance............................................................................. 13

3.2.4 CSR activities through Section-8 companies ....................................................................... 13

3.2.5 CSR activities through the formation of charitable trusts ................................................. 13

4. Integrating CSR into Business Strategy ............................................................................... 13

5. Conclusion ........................................................................................................................... 15

1. Introduction

While India’s economic policies have been instrumental in creating a favourable climate for growth, there

are significant socio-economic disparities that still exist across the country. This issue has been the focus of

various non-governmental organisations (NGOs), businesses, and government bodies and has led to the

development of innovative approaches to uplift those in need while ensuring self-sufficiency and

sustainability for the future.

Traditionally, corporate social responsibility (CSR) has always been perceived as an act of charity. With

India’s diverse population, CSR activities also typically revolved around making donations to improve the

living standards of the community one belonged to.

With the advent of new corporate regulations, the nature and perception of CSR are expected to evolve

and it will be interesting to see how traditional companies integrate CSR into their plans while ensuring

that the spirit of the CSR regulations is strongly upheld.

The guiding principles enshrined in the Draft Corporate Social Responsibility (CSR) Rules under Section 135

of the Companies Act, 20131 specify that CSR activities are not charity or donation but a “way of conducting

business by which corporate entities visibly contribute to the social good. Socially responsible companies

do not limit themselves to using resources to engage in activities that increase only their profits. They use

CSR to integrate economic, environmental and social objectives with the company’s operations and

growth”.

India is reportedly the first country in the world to introduce statutory guidelines requiring certain

specified companies to undertake CSR activities. The Companies Act, 2013, which gives statutory force to

CSR activities, was passed in 2013. The relevant provisions under the Companies Act, 2013 (the Act) with

respect to CSR are:

Section 135;

Schedule VII;

Companies (Corporate Social Responsibility Policy) Rules, 2014 (CSR Rules); and

Notifications and Circulars issued by the Ministry of Corporate Affairs (MCA) from time to time.

The Institute of Chartered Accountants of India is working on a Guidance Note on Accounting for

Corporate Social Responsibility Expenditure, which is expected to be released soon. Section 135, Schedule

VII and the CSR Rules were notified on 27 February 2014 and came into effect from 1 April 2014.

With the concept of mandatory CSR activities being relatively new, several areas require clarifications from

the MCA. This makes interpretation of the provisions and their implementation challenging. Our note aims

to provide an insight into the regulations governing CSR activities in India, issues clarified by the MCA and

the benefits of integrating CSR activities into your business strategy.

1 Companies Act, 2013, Ministry of Corporate Affairs, http://www.mca.gov.in/Ministry/pdf/CompaniesAct2013.pdf

2. CSR under the Companies Act, 2013

2.1 Scope and Applicability

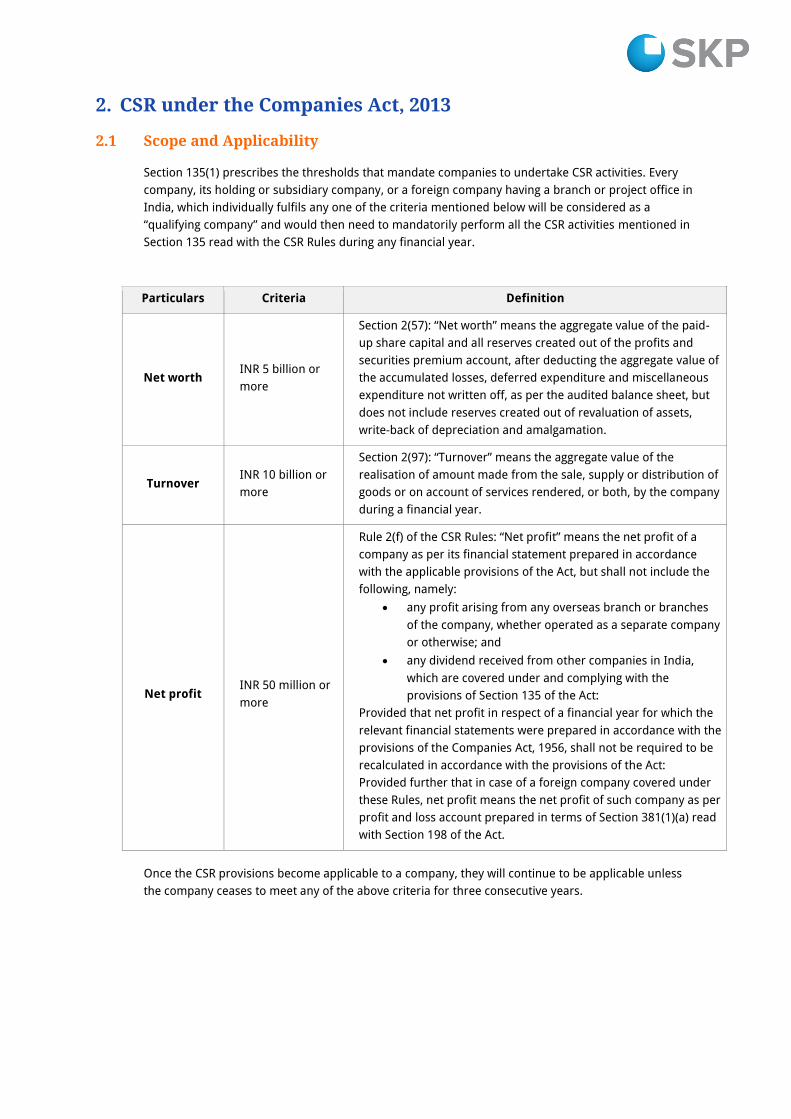

Section 135(1) prescribes the thresholds that mandate companies to undertake CSR activities. Every

company, its holding or subsidiary company, or a foreign company having a branch or project office in

India, which individually fulfils any one of the criteria mentioned below will be considered as a

“qualifying company” and would then need to mandatorily perform all the CSR activities mentioned in

Section 135 read with the CSR Rules during any financial year.

Particulars Criteria Definition

Net worth INR 5 billion or

more

Section 2(57): “Net worth” means the aggregate value of the paid-

up share capital and all reserves created out of the profits and

securities premium account, after deducting the aggregate value of

the accumulated losses, deferred expenditure and miscellaneous

expenditure not written off, as per the audited balance sheet, but

does not include reserves created out of revaluation of assets,

write-back of depreciation and amalgamation.

Turnover INR 10 billion or

more

Section 2(97): “Turnover” means the aggregate value of the

realisation of amount made from the sale, supply or distribution of

goods or on account of services rendered, or both, by the company

during a financial year.

Net profit INR 50 million or

more

Rule 2(f) of the CSR Rules: “Net profit” means the net profit of a

company as per its financial statement prepared in accordance

with the applicable provisions of the Act, but shall not include the

following, namely:

any profit arising from any overseas branch or branches

of the company, whether operated as a separate company

or otherwise; and

any dividend received from other companies in India,

which are covered under and complying with the

provisions of Section 135 of the Act:

Provided that net profit in respect of a financial year for which the

relevant financial statements were prepared in accordance with the

provisions of the Companies Act, 1956, shall not be required to be

recalculated in accordance with the provisions of the Act:

Provided further that in case of a foreign company covered under

these Rules, net profit means the net profit of such company as per

profit and loss account prepared in terms of Section 381(1)(a) read

with Section 198 of the Act.

Once the CSR provisions become applicable to a company, they will continue to be applicable unless

the company ceases to meet any of the above criteria for three consecutive years.

2.2 CSR Committee

2.2.1 Composition

Section 135 of the Act states that the qualifying company shall constitute a CSR Committee of the

Board of Directors which would comprise of three or more directors, of which at least one director

shall be an independent director2.

2.2.2 Roles and responsibilities

The mandate of the CSR Committee shall be:

To formulate and recommend a CSR Policy. The Policy shall be formulated considering the

activities best suited as per the industry and sector-specific issues adhering to the activities and

broad principles set out in Schedule VII;

Recommend the amount of expenditure that the company shall incur on CSR activities;

Monitor the CSR Policy of the company from time to time.

2.3 CSR Policy Implementation

The Act expressly states that during implementation of the CSR Policy, preference must be given by

the company to the local area and the area around which it operates. The CSR Rules lay down the

method of implementation of CSR activities. The responsibilities, modalities and activities qualifying as

CSR expenditure have been discussed in the following section.

2.4 Roles and Responsibilities: Board of Directors

The Act provides the following roles and responsibilities for the Board of Directors (BOD):

Approval of the CSR Policy of the company;

Disclosing the content of the Policy in the report of the Board of Directors;

Placing the Policy on the company’s website in such a manner as prescribed under Section 135 of

the Companies Act, 2013 read with the CSR Rules;

Ensuring that the CSR Policy is implemented and the activities undertaken by the company are

carried out;

Ensuring that the company spends, in every financial year, at least 2% of the average net profits of

the company made during the three immediately preceding financial years;

Ensuring that, if the earmarked amount is not spent, the same is specified in its report;

The Board shall have the power to make any change(s) in the Committee constitution.

2 Refer to Section 3.1 – Issues relating to CSR, The MCA’s Clarifications related to independent directors

2.4.1 Modalities for CSR activities

Instead of carrying out the CSR activities by itself, the company may undertake CSR activities in any of

the following modes:

If CSR is undertaken through any other entity, the company should specify the project or programmes

to be undertaken through these entities, the modalities of utilisation of funds on such projects, and

the monitoring and reporting mechanism.

2.4.2 Qualifying CSR activities

The CSR Policy formulated and recommended by the CSR Committee shall lay down the activities to be

undertaken by the company and the expenditure to be incurred in implementing them. Activities

undertaken in the normal course of business are excluded from the scope of CSR activities. The

activities that qualify as CSR activities are specified in Schedule VII to the Companies Act, 2013 and are

as follows:

Eradicating hunger, poverty and malnutrition, promoting preventive health care and sanitation

including contribution to the Swachh Bharat Kosh set-up by the central government for the

promotion of sanitation and making available safe drinking water;

Promoting education, including special education and employment enhancing vocation skills,

especially among children, women, the elderly, and the differently-abled, and livelihood

enhancement projects;

CSR Activities

Registered Trust or Registered Society

Establish a Section-8 company

Collaboration of Companies

Establish a trust or society

under the relevant laws by

itself or in collaboration with

other companies who may

not necessarily have to be

group companies.

If the registered trust or

society is not established by

the company, its holding or

subsidiary company, it

should have an established

track record of three years in

undertaking programmes or

projects similar to those the

company wishes to execute

through its CSR policy.

Group companies, related

companies and unrelated

companies can collaborate

for such activities. More

inflow of funds shall enable

effective management and

execution for a dedicated

cause.

A Section-8 company can be

established either:

by the company singly, or

jointly with its holding,

subsidiary or associate

company, or

jointly with any other

company or with such other

company’s holding,

subsidiary or associate

company.2

(Refer to Section 3 - Issues)

Promoting gender equality, empowering women, setting up homes and hostels for women and

orphans; setting up old-age homes, day-care centres and such other facilities for senior citizens,

and measures for reducing inequalities faced by socially and economically backward groups;

Ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal

welfare, agro forestry, conservation of natural resources and maintaining quality of soil, air and

water including contribution to the Clean Ganga Fund set up by the central government for

rejuvenation of the river Ganga;

Protection of national heritage, art and culture including restoration of buildings and sites of

historical importance and works of art; setting up public libraries; promotion and development of

traditional arts and handicrafts;

Measures for the benefit of armed forces veterans, war widows and their dependents;

Training to promote rural sports, nationally recognised sports, Paralympics sports and Olympic

sports;

Contribution to the Prime Minister's National Relief Fund or any other fund set up by the central

government for socio-economic development and relief and welfare of Scheduled Castes,

Scheduled Tribes, other backward classes, minorities and women;

Contributions or funds provided to technology incubators located within academic institutions

that are approved by the central government;

Rural development projects; and

Slum area development.

2.4.3 Inclusive scope of CSR

The Companies Act, 2013, in Schedule VII, listed down the activities that may be included by

companies in their CSR policies. The MCA has issued a clarification regarding the scope of Schedule VII

vide a circular3 stating that the activities undertaken by a company in pursuance of the CSR Policy

must be relatable to Schedule VII indicating that it is not necessary that for an activity to qualify as a

CSR activity, it should squarely fall within any of the entries under Schedule VII. Furthermore, the MCA

states that the entries in Schedule VII must be interpreted liberally in order to capture the essence of

the subjects enumerated in the Schedule and that the items enlisted in the Schedule VII are broad-

based and are intended to cover a wide range of activities. The inclusive definition of CSR assumes

significant importance as it allows companies to engage in projects or programmes related to activities

enlisted under the Schedule. It also gives flexibility to companies by allowing them to choose their

preferred CSR engagements that are in conformity with the CSR Policy.

2.4.4 Activities expressly disallowed as CSR activities The MCA, through the abovementioned circular, provided that CSR activities should be carried out in a

project or programme mode and shall not include the following:

Activities undertaken outside India;

Activities meant exclusively for employees and their families;

One-off events such as marathons/awards/charitable contributions/advertisements/sponsorships

of television programmes, etc.;

Expenses incurred by companies for the fulfilment of any Act/Statute of regulations (such as

Labour Laws, Land Acquisition Act, etc.);

Contributions made to a political party under Section 182 of the Companies Act, 2013.

3 General Circular No. 21 dated 18 June 2014

2.5 CSR Spending

2.5.1 Computation of the amount of CSR expenditure

It is the responsibility of the Board of Directors to ensure that the company spends at least 2% of the

average net profit of the three immediately preceding financial years to pursue and implement its CSR

Policy. The average profits are to be computed in accordance with the provisions of Section 198 of the

Act as shown below:

Statement showing computation of net profit as per Section 198 for the calculation of 2% of the

net profit for the purpose of CSR

Particulars* Amount

Profits as per Profit & Loss account XXX

Credit to be provided for:

Bounties and subsidies received from the government XXX

Credit not to be provided for:

Premium/profit on sale of shares

Profits of capital nature – including profits on sale of undertakings

Profits from sale of immovable property/ fixed assets – unless undertaken

Permissible deductions:

Usual working Charges – revenue expenditures, bonus or commission, abnormal or

special tax, interest on debentures, loans or advances, compensations/damages in

virtue of legal liability, bad debts written off, etc.

(XXX)

(XXX)

(XXX)

(XXX)

Non-permissible deductions:

Income tax paid under the Income Tax Act, 1961

Capital loss

Compensations/damages paid voluntarily

Profits as per Section 198 XXX

Source: Companies Act, 2013

Note: Net profit shall not include any profit arising from any overseas branch or branches of the

company whether operated as a separate company or otherwise; and any dividend received from

other companies which are required to comply under Section 135 of the Act.

2.5.2 Treatment of CSR expenditure

The Income Tax Act, 1961 states that expenses that are not incurred wholly or exclusively for carrying

on business cannot be considered as application of income, i.e. expenditure. Further, Section 37 of the

Income Tax Act disallows expenditure incurred under Section 135 as a deduction.

However, CSR expenditure that is in the nature described in other sections such as Section 35AC,

which coincides with the list of items mentioned in Schedule VII of the Companies Act, 2013 for CSR

purposes may be eligible for 100% deduction of the contribution made and one may have greater

comfort in claiming deduction regardless of whether there is deductibility under Section 37 of the

Income Tax Act or not as no direct nexus of the same with the business of the company needs to be

proved.

Furthermore, it is pertinent to note that in the Union Budget 2015-16, it has been proposed that

contributions/donations made towards the Swachh Bharat Kosh and Clean Ganga Fund with the aim of

fulfilling CSR requirements would not be eligible for a tax deduction under Section 80G. However, any

other assessee contributing to such funds would be eligible for a 100% deduction under Section 80G,

which seems discriminatory.

Activity (vii) in Schedule VII of the Companies Act, 2013 covers contributions to the Prime Minister’s

National Relief Fund or any other fund set up by the central government for socio-economic

development and relief and welfare of the Scheduled Castes, Scheduled Tribes, other backward

classes, etc. Hence, a company can contribute to such funds under its CSR initiatives and claim a 100%

tax deduction for the same.

2.5.3 Mandatory disclosures

The Companies Act, 2013 mandates the following disclosures with respect to the CSR Policy of

the company:

The Board of Directors must disclose the contents of the CSR Policy in the Board Report as per

Section 134(3) of the Companies Act, 2013 (for a foreign company, the balance sheet filed under

381(1)(b) of the Act should contain an annexure with a report on CSR);

The contents of the CSR Policy must be placed on the company’s website;

The Board shall disclose by way of Notes to the Statement of Profit and Loss, the amount of

expenditure incurred on CSR activities;

The Board shall disclose the composition of the CSR committee in the Board Report which shall be

attached to the financial statements of the company and be laid before the members in the

general meeting.

The disclosures mandated by the CSR Rules are as under:

Rule 9 of the CSR Rules requires the company to disclose the contents of its CSR Policy on the

company website as per the Annexure to the CSR Rules. The format of this disclosure is as under:

Format for disclosure of CSR Policy on company website

Sr.

no.

CSR

activity

project/

activity

identified

Sector in

which the

project is

covered

Projects/

programmes

(1), local area

(2), separate

state/district

Amount of

outlay: Project/

programme-

wise

Cumulative

expenditure

of reporting

Amount spent:

Direct or

through

implementing

agency

1

2

3

...

Total

Specific inclusions to be made in the CSR Policy

As per Rule 6(1) of the CSR Rules, the CSR Policy of a company shall specifically include the following:

List of specified projects or programmes that a company plans to undertake within the purview of

Schedule VII;

Modalities of execution of such projects or programmes and implementation schedules for the

same;

Monitoring process of such projects or programmes

The CSR Policy is also required to specifically state that the surplus arising out of the CSR projects or

programmes or activities shall not form part of the business profit of the company.

CSR Corpus

The disclosure under the CSR Policy in respect of Corpus would include the following:

2% of the average net profits;

Any income arsing thereon; and

Surplus arising out of CSR activities.

Failure to disclose

The Act mandates spending of at least 2% of the average net profits; there is no provision of rolling

over the unspent amount to succeeding financial years. In case the company fails to spend the

amount, the Board shall specify its reason of this failure in its report.

Failure to explain or report is punishable by a fine on the company of not less than INR 50,000

and up to INR 2.5 million; and

Officers who default on the reporting provision could be subject to up to three years in prison

and/or fines of not less than INR 50,000 and as high as INR 500,000.

3. Issues relating to CSR

3.1 The MCA’s Clarifications

Issue Clarification SKP’s Comments

Scope and Applicability

Foreign company The CSR Rules prescribe the following:

CSR provision shall be applicable to a

foreign company that has its branch

or project office in India.

The balance sheet and profit and loss

account of a foreign company will be

prepared in accordance with Section

381(1)(a) and net profit is to be

computed as per Section 198 of the

Companies Act.

No clarity is provided towards any

mechanism that allows computation of

accounts of a foreign company in order

to determine the net worth or turnover of

a branch or a project office. Ascertaining

the incidence of CSR exposure in the

absence of any clear provision for

financial computation of branch or

project offices of foreign companies may

prove challenging and create practical

difficulties.

Independent

directors

The CSR Rules have done away with the

requirement of appointing an

independent director on the CSR

Committee of the Board of an unlisted

company as well as a private company.

The CSR Rules have relaxed the

requirement regarding the presence

of three or more directors on the CSR

Committee of the Board. In case a

private company has only two

directors on the Board, the CSR

Committee can be constituted with

these two directors.

The CSR Committee of a foreign

company shall comprise of at least

two persons wherein one or more

persons should be resident in

India and the other person is

nominated by the foreign company.

This is a constructive development which

will provide relief to many companies

that were not otherwise required to have

independent directors on their Board.

CSR Spending

Section 135(5)

requires profit to

be calculated as

per Section 198.

Section198 is to

be used to

calculate profits

only for the

purposes of

Section197.

There is no direct clarification on this

aspect.

Section 198 of the Companies Act, 2013

lays down the method of computation of

profits specifically for the purpose of

Section 197, i.e. managerial

remuneration.

A harmonious application of Section 135

dealing with CSR and Section 197 dealing

with managerial remuneration would

imply that the net profit to be calculated

would be on the same lines for the

purposes of both sections.

Surplus arising

out of CSR

activities

The surplus from CSR activities shall not

form a part of the business profits of the

company.

This implies that surplus shall be re-

invested to perform CSR activities.

This surplus shall not be included in the

spend to be calculated for any future

years. This amount shall be over and

above the mandatory contribution the

company has to make towards CSR

activities.

Costs incurred to

build capacities

for carrying out

CSR activities

forming part of

CSR expenditure

These costs cannot exceed 5% of the

total CSR expenditure of the company in

one financial year.

The computation is to be noted carefully.

Reconciliation of

profits calculated

as per the Act of

1956 and 2013

The proviso to Rule 3(1) of the CSR

Rules, 2014 states that net profit in

respect of a financial year to which the

relevant financial statements were

prepared under the Companies Act,

1956 shall not be required to be re-

computed.

-

Disclosure

Profit and loss

statement vs

Note in the

financials

- Schedule III to the Companies Act, 2013

has given the format of statement of

profit and loss account. According to this

format, expenditures are classified based

on the nature of expenses and not based

on function.

Hence, expenditure incurred on CSR

activities cannot be shown on the face of

the statement of profit and loss.

However it will be shown under “Other

expenses” with a detailed break up in the

Notes to accounts with a separate line

item on CSR spending.

3.2 Issues Pending Clarification

3.2.1 Contributions to Promoters’/Directors’ family trusts

The MCA is yet to clarify whether contributions to Promoters’/Directors’ family trusts or trusts in which

they are interested parties will be considered as compliance to CSR obligations, if such trusts are

promoting the areas mentioned in Schedule VII of the Companies Act, 2013.

3.2.2 Net profit of Indian companies for the calculation of profit of foreign companies

Rule 2(f) of the CSR Rules specifically states profits of foreign companies are to be calculated as per the

profit and loss account prepared in terms of Section 381(1)(a) read with Section 198 of the Act to

determine applicability of CSR provisions.

Rule 2(f) is clear on the exclusions to be made from the profits of Indian companies. However, the Act,

Rules, Notifications and Circulars are silent on whether the amounts of net profit that determine

applicability for an Indian company are either:

Profits computed as per Section 198; or

Profits calculated as per Schedule III of the Companies Act, 2013 i.e. Profits as per the audited

financial statements.

Further, if they are to be net profits as disclosed as per the audited financial statements, another issue

that requires clarification from the MCA is whether these profits are to be considered before tax or

after tax.

3.2.3 Acceptable reasons for non-compliance

The MCA is yet to clarify the reasons that shall be accepted for failure in spending the prescribed

amounts on CSR activities.

3.2.4 CSR activities through Section-8 companies

Rule 4 provides that a company may carry out CSR activities through a Section-8 company established

by the company itself, or jointly by the company and any other company as specified therein.

However, the proviso mentions that if CSR activities are carried out through a Section-8 company that

is not established by the qualifying company, then it should have an established track record of three

years in undertaking similar programmes or projects.

3.2.5 CSR activities through the formation of charitable trusts

The CSR Rules also contain guidance on how companies can conduct CSR activities through trusts. This

leads to another issue that for income tax purposes, whether contribution to the trust would be

allowed wholly or be restricted to 50% under Section 80G of the Income Tax Act or be completely

disallowed. Furthermore, whether such trusts would get approvals for 80G from Income Tax

Commissioners is also not clarified.

4. Integrating CSR into Business Strategy

As mentioned at the start of this note, the practice of CSR in India remains within the philanthropic space

and needs to evolve into having a much wider scope. It is essential for CSR to become more strategically

linked with business than being restricted to acts of charity.

While CSR is not a new concept for many Indian companies, formulating relevant and sustainable policies

and practices will depend largely on a company’s ability to innovate and adapt. It is important that social

objectives are not superficially tied to business objectives. A well-aligned strategy would lead to

improvements for both, the organisation and the society it functions in.

In the Indian context, maternal health, infant mortality, food security, availability of clean drinking water,

education and gender equality are some vital areas in need of attention. In fact, the first draft of Schedule VII

was entirely in line with the United Nations’ Millennium Development Goals (MDGs) on hunger, health and

sustainability. The mandatory CSR Policy can enable the corporate sector to accelerate action towards achieving

the MDGs.4

Creating a strategy that results in improvements in social welfare would also help strengthen the brand of the

contributing company, eventually leading to economic benefits. This can be seen in Vodafone India’s

contribution to the Gujarat government’s e-Mamta Mother-Child programme. Vodafone developed a voice-

based closed user group (CUG) solution providing 42,000 SIM cards to ASHAs (Accredited Social Health

Activists), doctors and health workers connecting them to expectant mothers to monitor their health status and

ensure timely care. This not only resulted in reducing infant mortality but also helped Vodafone’s image

building, improved its rural reach, increasing business as the health workers consumed 200,000 minutes within

the CUG and 500,000 outgoing minutes on a daily basis.5

The key to maximising returns from the newly mandated statutes is to emphasise on developing effective,

need-based CSR strategies so that these investments can yield the intended results. CSR initiatives should be

sustainable, scalable and result oriented. These initiatives may be better undertaken in a project-based manner

to ensure that tangible results and real-time benefits are enjoyed both, by the company and the recipients of its

assistance.

4 The CSR Policy outlined in the Companies Act 2013 offers enormous potential for businesses in India to accelerate action

towards the most pressing MDGs, UNDP in India, http://www.in.undp.org/content/india/en/home/presscenter/pressreleases/2013/12/19/the-corporate-social-responsibility-policy-outlined-in-the-companies-act-2013-offers-enormous-potential-for-businesses-in-india-to-accelerate-action-towards-the-most-pressing-mdgs.html 5 Press release: Vodafone’s e-Mamta initiative helps reduce infant mortality in Gujarat,

www.vodafone.in/documents/pdfs/pressreleases/pr_1178.pdf

Customer Retention

Opportunities

Brand Development

Social Capital

Value Creation

Effective CSR policy

integrated with

business goals

5. Conclusion

The inclusion of the CSR mandate under the Companies Act, 2013 is an attempt to complement the Indian

government’s efforts of delivering the benefits of economic development to all sections of society by

engaging the corporate world.

While an organisation’s CSR activities and business goals can be compatible, the activities specified in the

Act may seem restrictive and could lead to forced participation instead of a truly sincere approach. The

success of a company’s CSR activities will be determined by how the company attempts to integrate the

mandate into its core business strategy. If pursued in a planned, organised manner, it could maximise

value and justify the investment made, while contributing to the betterment of society.

Contact

Mumbai

19, Adi Marzban Path

Ballard Estate

Fort

Mumbai 400 001

T: +91 22 6730 9000

Pune

VEN Business Centre

Baner–Pashan Link Road

Pashan

Pune 411 021

T: +91 20 6720 3800

Hyderabad

6-3-249/3/1 SSK Building

Ranga Raju Lane

Road No. 1, Banjara Hills

Hyderabad 500 034

T: +91 40 2338 6912

New Delhi

B-376

Third Floor

Nirman Vihar

New Delhi 110 092

T: + 91 11 2242 8454

Chennai

Office No. 3

Crown Court

128 Cathedral Road

Chennai 600 086

T: +91 44 4208 0335

Bengaluru

Barton Centre

Office No. 312/313

Mahatma Gandhi Road

Bengaluru 560 001

T: +91 80 4140 0131

Global Desks

Canada

269 The East Mall

Toronto

ON M9B 3Z1

Canada

T: +1 647 707 5066

Japan

Kojimachi Building

3-3-6, Kudan Minami, Chiyoda-ku

Tokyo 102-0074

Japan

T: +81 (0) 3 5211 7878

www.skpgroup.com

Connect with us

www.linkedin.com/company/skp-group

www.twitter.com/SKPGroup

www.facebook.com/SKPGroupIndia

http://goo.gl/NF29sj

Subscribe to our alerts