> annual report 2005 - golden agri-resources · pt bank internasional indonesia tbk, pt bank...

TRANSCRIPT

> Annual Report 2005

> 2

00

5 A

nn

ua

l Re

po

r t Go

lde

n A

gr i-R

es o

ur c

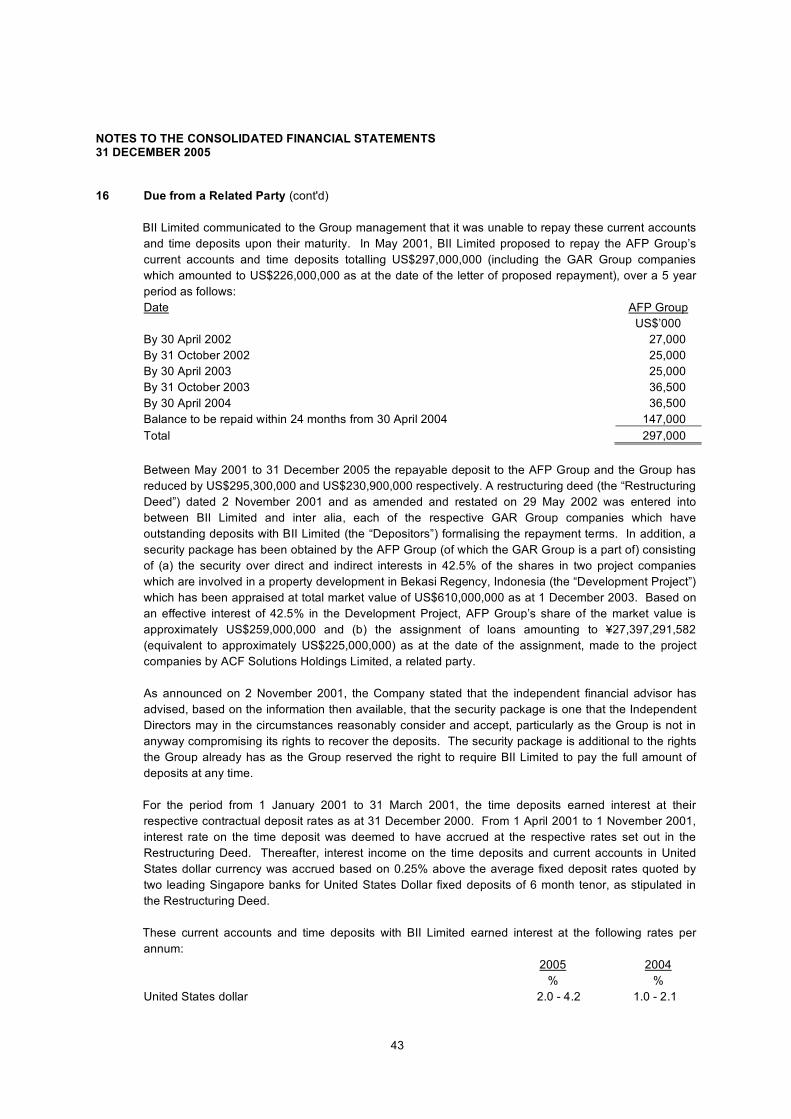

es L

t d

Golden Agri-Resources Ltd

c/o 3 Shenton Way

#17-03 Shenton House

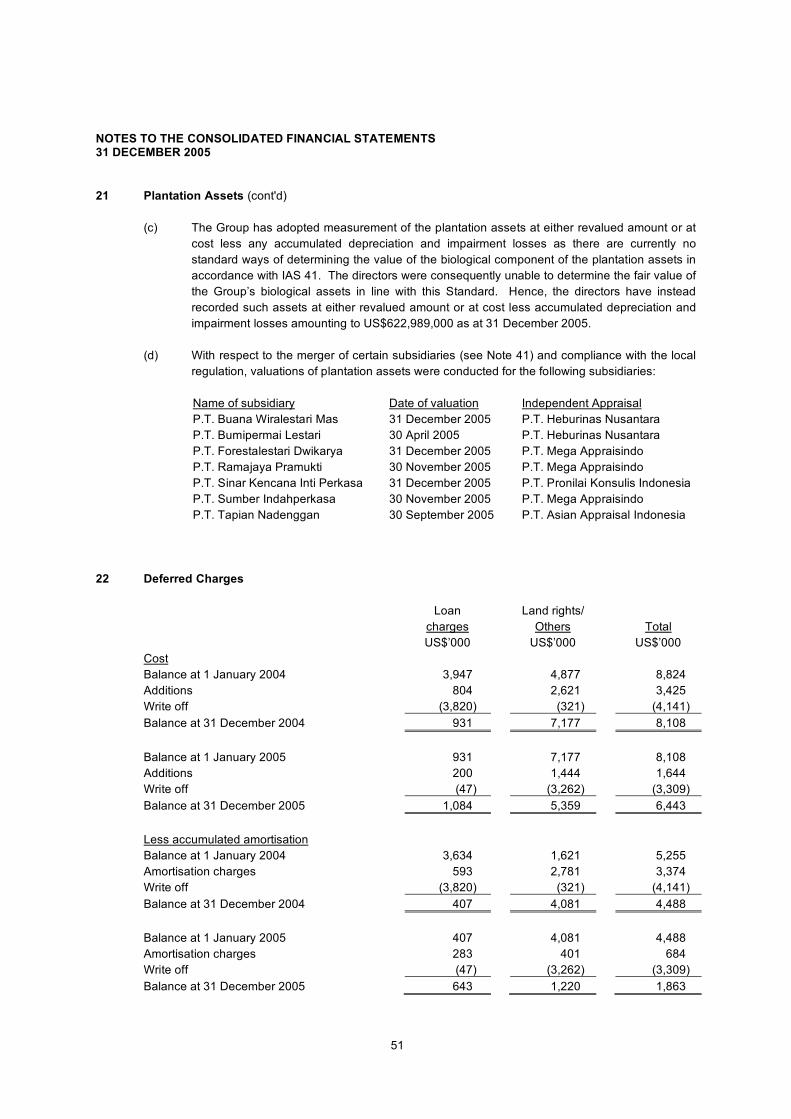

Singapore 068805

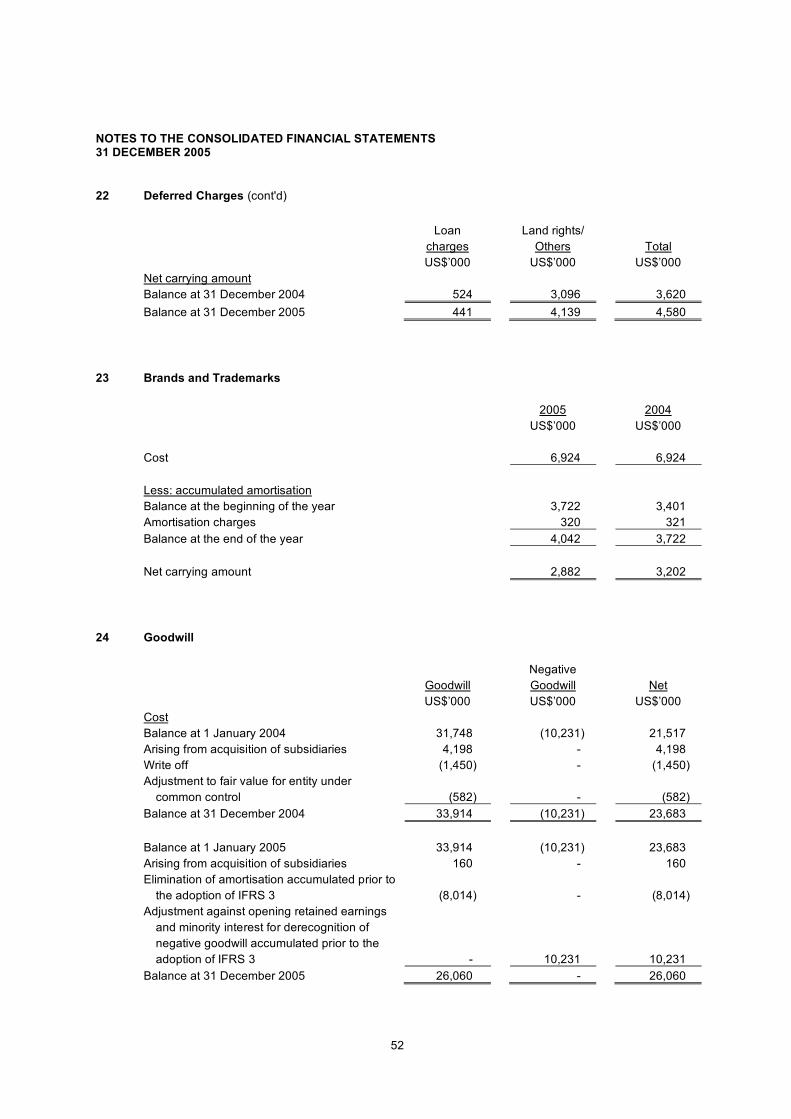

Tel : 65 - 6220 7720

Fax: 65 - 6220 7020

Email: [email protected]

1 Corporate Profile

2 Network of Operations

4 Corporate Directory

5 Corporate Structure

6 Board of Directors

9 Chairman’s Statement

11 Operations Review

15 Financial Report > Shareholding Statistics

> Notice of Annual General Meeting

> Proxy Form

> Contents

Golden Agri-Resources Ltd

> Corporate Profile

1

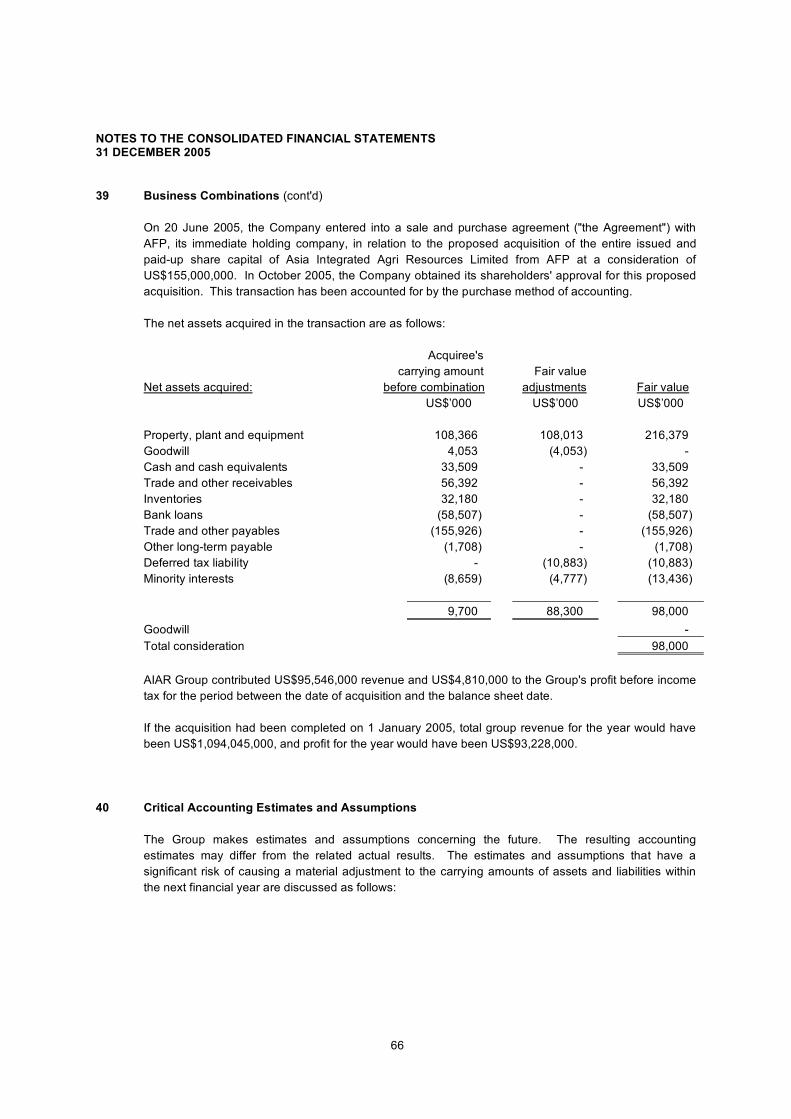

Listed on the Singapore Exchange Securities Trading Limited (SGX-ST) in 1999,

Golden Agri-Resources Ltd (GAR) is one of the largest privately owned oil palm

plantation companies in the world. Its operations are strategically located over

Indonesia.

With a total planted area of 287,000 hectares, GAR operates 31 palm oil

processing mills, two refineries and four kernel crushing plants. The Group’s

primary activities include cultivating and harvesting of oil palm trees; processing

of fresh fruit bunch into crude palm oil (CPO) and palm kernel oil; and refining

CPO into value-added products such as cooking oils, margarine and shortening.

In December 2005, GAR expanded its operations into China which include

refineries, port and oil-seed crushing facilities in Ningbo and Zhuhai.

GAR is 55 percent owned by SGX-ST listed Asia Food & Properties Limited

(AFP), an investment holding company with operating businesses in Agri-business,

Food and Property. Listed in 1997, AFP’s principal operations are located in

Indonesia, China, Singapore and Malaysia. The AFP Group of Companies employs

about 45,000 people with strong local, regional and international knowledge and

experience. AFP Group’s turnover in 2005 was S$2.5 billion.

Golden Agri-Resources Ltd

weaimtobethebest

Golden Agri-Resources Ltd

> Network of Operations

2

INDONESIA AGRI-BUSINESS

Sumatra

North Sumatra

Riau

South Sumatra

Bangka

Belitung

Jambi

Lampung

Sulawesi

South Sulawesi

Irian Jaya

Irian

Java

Jakarta

West Java

Central Java

East Java

Bali

Bali

Kalimantan

East Kalimantan

West Kalimantan

South Kalimantan

Central Kalimantan

.

.

.Distribution Centers

Refineries

Bulking Stations

.Plantations, CPO Millsand PK Crushing Plants

Sumatra Kalimantan

Sulawesi

Irian Jaya

Java

Maluku

Bali

Golden Agri-Resources Ltd3

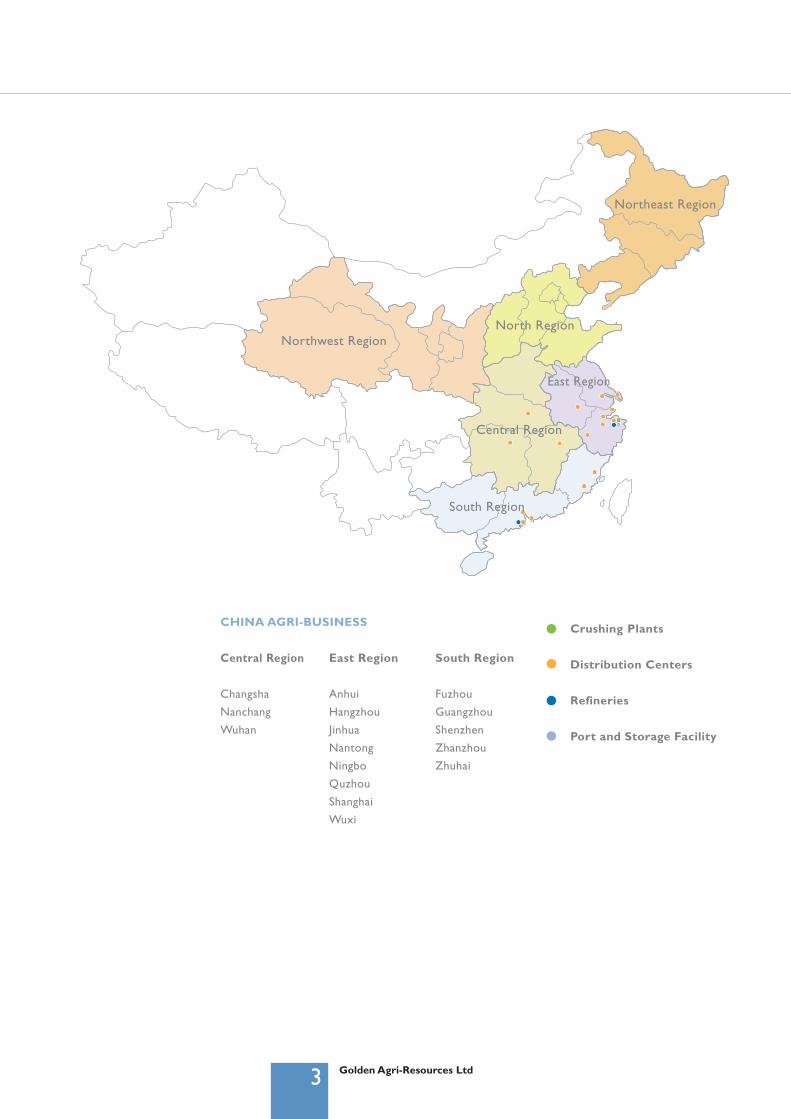

Crushing Plants

Distribution Centers

Refineries

Port and Storage Facility

CHINA AGRI-BUSINESS

Central Region

Changsha

Nanchang

Wuhan

East Region

Anhui

Hangzhou

Jinhua

Nantong

Ningbo

Quzhou

Shanghai

Wuxi

South Region

Fuzhou

Guangzhou

Shenzhen

Zhanzhou

Zhuhai

..

..

Northwest RegionNorth Region

Northeast Region

Central Region

East Region

South Region

Golden Agri-Resources Ltd

> Corporate Directory

Board of DirectorsFranky Oesman Widjaja (Chairman), Muktar Widjaja, Frankle (Djafar) Widjaja, Simon Lim, Rafael Buhay Concepcion, Jr.,Lew Syn Pau, Hong Pian Tee, Kunihiko Naito, Kaneyalall Hawabhay, Bertrand Denis Richard De Chazal

Audit CommitteeHong Pian Tee (Chairman), Kaneyalall Hawabhay, Kunihiko Naito

Nominating CommitteeHong Pian Tee (Chairman), Kunihiko Naito, Franky Oesman Widjaja

Remuneration CommitteeHong Pian Tee (Chairman), Kunihiko Naito, Frankle (Djafar) Widjaja

SecretaryMulticonsult Limited

Registered Office10 Frere Felix de Valois Street, Port Louis, Republic of MauritiusTel: (230) 202 3000 Fax: (230) 212 5265

Correspondence Address3 Shenton Way, #17-03 Shenton House, Singapore 068805Tel: (65) 6220 7720 Fax: (65) 6220 7020

Share Registrar and Transfer OfficeB.A.C.S. Private Limited63 Cantonment Road, Singapore 089758Tel: (65) 6323 6200 Fax: (65) 6323 6990

Auditors and Reporting AccountantsMoore Stephens, Certified Public Accountants11 Collyer Quay #10-02The Arcade, Singapore 049317Tel: (65) 6221 3771 Fax: (65) 6221 3815Partner-in-charge: Christopher Bruce Johnson (Appointed in December 2002)

Moore Stephens, Chartered Certified Accountants6th Floor, Nirmal House, 22 Sir William Newton Street, Port Louis, Republic of MauritiusTel: (230) 211 6535 Fax: (230) 211 6964Partner-in-charge: Arvin Rogbeer (Appointed in December 2002)

Principal BankersPT Bank Internasional Indonesia Tbk, PT Bank Mandiri (Persero) Tbk, PT Bank Central Asia Tbk and PT Bank NegaraIndonesia (Persero) Tbk

Date and Country of Incorporation15 October 1996, Republic of Mauritius

Share ListingThe Company’s shares are listed on the Singapore Exchange Securities Trading Limited

Date of Listing9 July 1999

4

Golden Agri-Resources Ltd

> Corporate Structure

Note:

*Listed on the Jakarta Stock Exchange and Surabaya Stock Exchange

A simplified corporate structure of the Group showing the main subsidiaries, directly or indirectly held by the Company

13.96%

GO

LD

EN

AG

RI

-R

ES

OU

RC

ES

LT

D

Golden Agri International Finance Ltd100%

Golden Agri International Pte Ltd100%

Silverand Holdings Ltd100%

PT P

urim

as S

asm

ita

86.04%

Asia Integrated Agri Resources Limited100%

Re f ined Product s , Por t & S torage Fac i l i t i e s

74.63%

91%

P l a n t a t i o n s

PT Sawit Mas Sejahtera

PT Sinar Kencana Inti Perkasa

100%

100%

A S A T 3 1 D E C E M B E R 2 0 0 5

5

P l a n t a t i o n s & R e f i n e d P r o d u c t s

PT Ivo Mas Tunggal

PT Sinar Mas Agro Resources and Technology Tbk *

9%

Golden Agri-Resources Ltd 6

Mr. Franky Widjaja, aged 48 was appointed Chairman in 2000. He has been a Director and Chief Executive Officer of GAR since

1996. He received his tertiary education at the Aoyama Gakuin University, Japan, where he graduated with a Bachelor’s degree

in Commerce in 1979.

Mr. Franky Widjaja has extensive management and operational experience in the different businesses of the Sinar Mas Group

such as pulp and paper, property, chemical, financial services and agriculture since 1982. He presently heads the Agri-Business and

Consumer Food Products Division of the Sinar Mas Group.

Mr. Franky Widjaja is a member of GAR’s Executive Committee and Nominating Committee. He is President Commissioner of

GAR’s Indonesian subsidiary, PT Sinar Mas Agro Resources and Technology Tbk, which is listed on the Jakarta and Surabaya Stock

Exchanges.

Mr. Franky Widjaja is Chairman and Chief Executive Officer of Asia Food & Properties Limited, and President Commissioner of

its Jakarta and Surabaya Stock Exchange listed Indonesian property subsidiary, PT Duta Pertiwi Tbk. He also sits on the Boards of

Directors of several Sinar Mas companies.

Mr. Muktar Widjaja, aged 51 was appointed as President and Vice Chairman of GAR in 2000. He has been a Director since 1999.

His last re-election as a Director was in 2004. He obtained his Bachelor’s degree in Business Administration with a major in

Commerce in 1976 from the University Concordia, Canada.

Mr. Muktar Widjaja has been actively involved in the management and operations of the property, financial services, agriculture,

chemical and pulp and paper businesses of the Sinar Mas Group since 1983. Mr. Muktar Widjaja is a member of GAR’s Executive

Committee. He is President Director of PT Sinar Mas Agro Resources and Technology Tbk, Director and President of Asia Food

& Properties Limited and President Director of PT Duta Pertiwi Tbk. He also serves on the Boards of Directors of several Sinar

Mas companies.

Mr. Frankle Widjaja, aged 49 has been a Director and Vice President of GAR since 1999. His last re-election as a Director was in

2005. He studied at the University of California, Berkeley, USA, and obtained a Bachelor of Science degree in Science (Industrial

Engineering & Operational Research) in 1978.

He has been involved in the management and operations of the pulp and paper, financial services, food and agriculture and real

estate businesses of the Sinar Mas Group since 1979.

Mr. Frankle Widjaja is a member of GAR’s Executive Committee and Remuneration Committee. He is a Director and Vice

President of Asia Food & Properties Limited, and Vice President Commissioner of PT Duta Pertiwi Tbk. He presently sits on the

Boards of Directors of several Sinar Mas companies.

Franky Oesman Widjaja, Chairman and Chief Executive Officer

Muktar Widjaja, Director and President

Frankle (Djafar) Widjaja, Director and Vice President

> Board of Directors

Golden Agri-Resources Ltd7

Mr. Lim, aged 43 was appointed as a Director and Chief Financial Officer in 2002. His last re-election as a Director was in 2003.

A 1988 graduate from University of Trisakti, Indonesia, majoring in Accounting and Finance, he later obtained a Master in

Business Management from the Asian Institute of Management, Philippines in 1992 with a full scholarship from ADB-Japan.

He has extensive financial, management and operational experience having worked in different industries.

Mr. Lim is a member of GAR’s Executive Committee. He is Vice President Director of PT Sinar Mas Agro Resources and

Technology Tbk, Commissioner of PT Duta Pertiwi Tbk, and Director and Chief Financial Officer of Asia Food & Properties

Limited.

Mr. Concepcion, aged 39 was appointed as a Director in 2002. His last re-election as a Director was in 2003. He studied at the

University of the Philippines where he obtained a Bachelor of Science in Economics in 1988. In 1992, he obtained a Master in

Business Management from the Asian Institute of Management, Philippines with scholarship from SGV Philippines. He worked

on regional projects and has extensive experience in corporate and financial planning. After 5 years with Pilipinas Shell Petroleum

Corporation, Mr. Concepcion joined PT Sinar Mas Agro Resources and Technology Tbk, and now holds the position of

Director. He is a member of GAR’s Executive Committee and a Director of Asia Food & Properties Limited.

Mr. Lew, aged 52 has been a Director of GAR since 1999. His last re-election as a Director was in 2005. A Singapore Government

scholar, Mr. Lew obtained a Master in Engineering from Cambridge University, UK and a Master of Business Administration from

Stanford University, USA.

He is Managing Director of Stanbridge International Pte Ltd. Prior to Stanbridge, Mr. Lew was Senior Country Officer and

General Manager for Banque Indosuez Singapore, where he worked from 1994 to 1997. He was General Manager and subsequently,

Managing Director of NTUC Comfort from 1987 to 1993 and Executive Director of NTUC Fairprice from 1993 to 1994. He

was a Member of Parliament from 1988 to 2001.

Mr. Lew sits on the Boards of Directors of several public listed companies namely, Poh Tiong Choon Logistics Ltd, Magnus Energy

Group Ltd, Lafe Technology Ltd, Achieva Ltd, Food Empire Holdings Ltd, RSH Limited and Guangzhao Industrial Forest Biotechnology

Group Ltd. He is also Chairman of ArianeCorp Ltd and Ascendas Pte Ltd, and President of The Singapore Manufacturers’

Federation.

Mr. Hong, aged 61 joined GAR’s Board of Directors in 2001. His last re-election as a Director was in 2005. Prior to retiring

from professional practice, he was a partner of PricewaterhouseCoopers, a position he held from 1985 to 1999.

Mr. Hong’s experience and expertise are in corporate advisory, financial reconstruction and corporate insolvencies since 1977.

He has been a corporate/financial advisor to clients with businesses in Singapore and Indonesia and in addition was engaged to

restructure companies with operations in Taiwan, Indonesia and Malaysia.

He is Chairman of GAR’s Audit Committee, Remuneration Committee and Nominating Committee. He is also Chairman of Pei

Hwa Foundation.

Simon Lim, Director and Chief Financial Officer

Rafael Buhay Concepcion, Jr., Director

Lew Syn Pau, Independent Director

Hong Pian Tee, Independent Director and Chairman of Audit Committee, Remuneration Committee and Nominating Committee

Golden Agri-Resources Ltd 8

Mr. Naito, aged 61 was appointed to GAR’s Board of Directors in 2006. He is a graduate of the Waseda University, Japan, where

he obtained his Bachelor’s degree in Engineering in 1967.

Mr. Naito is Representative Director of NSN Global Partners Ltd, Japan. Previously, Mr. Naito was the Deputy General Manager

for the South East Asia region of Nissho Iwai Corporation. The position was based in Singapore. He was with Nissho Iwai

Corporation for 36 years, of which 14 years was with its subsidiary in New York, USA, where he was actively involved in food and

automotive project management. His last title there was Chief Representative for Nissho Iwai Corporation Indonesia.

Mr. Naito is a member of GAR’s Audit Committee, Remuneration Committee and Nominating Committee.

Mr. Hawabhay, aged 58 was appointed as a Director of GAR in 2003. His last re-election as a Director was in 2004. He is a

Fellow of the Institute of Chartered Accountants in England and Wales. He has been a Partner (Assurance and Business

Advisory Services (“ABAS”)) of De Chazal du Mée & Co, Mauritius from 1987 to June 2002 and Director of Multiconsult

Limited from July 2002 to 2005. Presently, he is Partner (ABAS) of BDO De Chazal du Mee, Mauritius.

Mr. Hawabhay is a member of GAR’s Audit Committee.

Mr. De Chazal, aged 64 joined GAR’s Board of Directors in 2003. His last re-election as a Director was in 2004. He is a Fellow

of the Institute of Chartered Accountants of England and Wales. He was a Senior Financial Analyst from 1986 to 2003 with

World Bank. Mr. De Chazal’s experience and expertise include financial analysis, economic sector work and fiduciary compliance.

He is currently a non-executive director of Mauritius Commercial Bank Ltd, Promotion and Development Limited and Caudan

Properties Limited.

Kunihiko Naito, Independent Director

Kaneyalall Hawabhay, Independent Director

Bertrand Denis Richard De Chazal, Independent Director

Golden Agri-Resources Ltd9

> Chairman’s Statement

Group Performance

I am pleased to report growth momentum in our business

operations in 2005 with the increase in revenue to US$819.3

million and net profit attributable to equity holders to US$74.6

million for Golden Agri-Resources Ltd (“GAR”) and its

subsidiaries (the “Group”). These represented growth of

7.8 percent in revenue and 14 percent in net profit

attributable to equity holders as compared to US$759.7 million

and US$65.5 million respectively in 2004. Our crude palm oil

(“CPO”) production output rose 8.2 percent to 1,479,000

tonnes in 2005 from 1,367,000 tonnes produced in 2004. Our

better performance reflects the results of our innovation and

continuous improvement initiatives.

The average International CPO price (CIF Rotterdam) was

US$420 per tonne, approximately 10 percent lower than the 2004

average of US$469 per tonne. Despite the lower realised prices

of CPO and related palm products in 2005, our earnings per share

for 2005 increased 14 percent to USD 3.44 cents from USD 3.02

cents for 2004. Our net asset value per share was almost

25 percent higher at USD 46.2 cents as at 31 December 2005

compared to USD 37.2 cents at the end of December 2004.

Accordingly, we are pleased to propose a first and final dividend

of SGD 1 cent per share subject to shareholders’ approval at the

forthcoming Annual General Meeting.

In 2005, we have extended our penetration into a few key

markets including China, India, Korea and the Philippines. As part

of our long-term priority is to build geographic presence in

attractive regional markets, GAR acquired the China Agri-

business operations (Asia Integrated Agri Resources Limited

(“AIAR”) group of companies) from its immediate holding

company, Asia Food & Properties Limited in the last quarter of

2005 (“4Q2005”). The acquisition will facilitate the market

expansion of the Group’s palm oil business into China.

The increase in revenue was mainly due to the contribution from

the China Agri-business operations in 4Q2005, amounting

to US$95.5 million. This division operates a deep-sea port and

storage facility for oil and grain, oilseed crushing and vegetable oil

refining facilities in Ningbo and Zhuhai, and produces soybean oil,

soy-based animal feeds, palm oil and blended edible oils.

On the other hand, revenue from the Indonesia Agri-business

operations fell US$36 million or 4.7 percent to US$723.7 million

from US$759.7 million in 2004. This was mainly due to the lower

realised prices of CPO and related palm products during 2005.

Operations

Our total planted area was 287,000 hectares as of end 2005,

96 percent of which was mature estates. Following the

completion of three more CPO mills, Muara Wahau (East

Kalimantan), Sungai Bengkal (Jambi) and Tanah Laut (South

Kalimantan), we currently operate 31 CPO mills with combined

installed capacity of 8,045,000 tonnes per annum, and two

refineries with processing capacity of about 840,000 tonnes

per annum.

Further, our fresh fruit bunch (“FFB”) production yield increased

to 21.43 tonnes per hectare, up from the 20.23 tonnes per

hectare whereas CPO extraction rate was 23.29 percent, up

from 23.19 percent in 2004.

Outlook

Going forward, the Group’s performance continues to depend

on the global economic outlook, global climatic conditions, CPO

price, foreign exchange rates movement, and developments in

Indonesia and China.

The outlook for palm oil industry is favourable as palm oil prices

are expected to be sustained by robust demand in spite of the

Golden Agri-Resources Ltd 10

Revenue(US$ million)

EBITDA(US$ million)

anticipated increase in supply. A large part of the anticipated

demand lies in the recent lifting by the Chinese government of

its import quota on palm oil. The growing interest in using palm

oil as an alternative energy source (bio-diesel) also benefits the

industry. Further, being naturally semi-solid, palm oil does not

require hydrogenation, and is thus emerging as a viable

alternative for other edible oils. Demand is expected to grow,

especially with stricter food labelling laws coming into effect in

the United States.

Having successfully restructured all our debts that required

restructuring, we are now able to focus on our operations,

improve our operating efficiencies, increase our penetration of

our downstream businesses and grow our business both

organically and by way of acquisition.

Appreciation

On behalf of the Board, I would like to express my appreciation

to our independent directors, Dr Hong Hai and Mr Foo Meng

Kee, who resigned from the Board on 21 February 2006, for

their valuable services and contributions since their appointments

in 2001. I would also like to extend a warm welcome to the

Board, our new director, Mr Kunihiko Naito, who was appointed

on 21 February 2006.

Last but not least, I also wish to thank our shareholders, business

associates and customers for their continuous support, and our

management and staff for their contributions and commitment

to create continuous growth with long-term sustainable value.

Franky Oesman Widjaja

Chairman & Chief Executive Officer

16 March 2006

Golden Agri-Resources Ltd11

> Operations Review

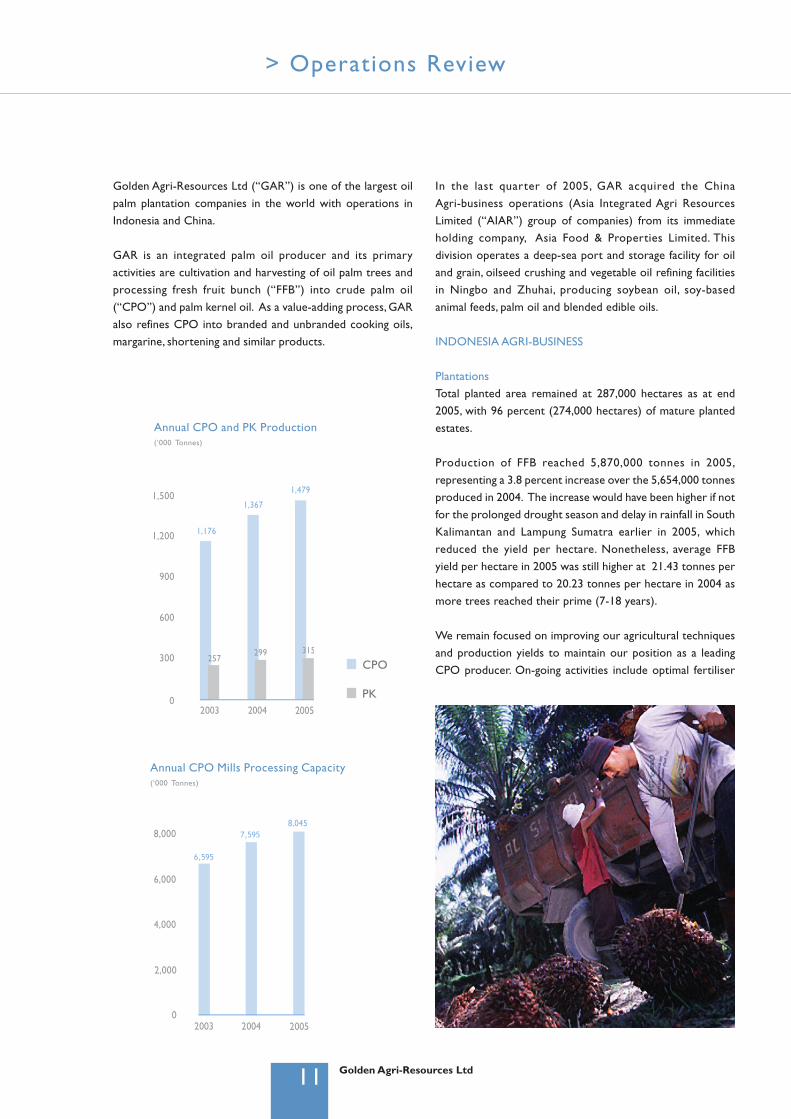

Annual CPO and PK Production(‘000 Tonnes)

CPO

PK

Annual CPO Mills Processing Capacity(‘000 Tonnes)

Golden Agri-Resources Ltd (“GAR”) is one of the largest oilpalm plantation companies in the world with operations inIndonesia and China.

GAR is an integrated palm oil producer and its primaryactivities are cultivation and harvesting of oil palm trees andprocessing fresh fruit bunch (“FFB”) into crude palm oil(“CPO”) and palm kernel oil. As a value-adding process, GARalso refines CPO into branded and unbranded cooking oils,margarine, shortening and similar products.

In the last quarter of 2005, GAR acquired the ChinaAgri-business operations (Asia Integrated Agri ResourcesLimited (“AIAR”) group of companies) from its immediateholding company, Asia Food & Properties Limited. Thisdivision operates a deep-sea port and storage facility for oiland grain, oilseed crushing and vegetable oil refining facilitiesin Ningbo and Zhuhai, producing soybean oil, soy-basedanimal feeds, palm oil and blended edible oils.

INDONESIA AGRI-BUSINESS

PlantationsTotal planted area remained at 287,000 hectares as at end2005, with 96 percent (274,000 hectares) of mature plantedestates.

Production of FFB reached 5,870,000 tonnes in 2005,representing a 3.8 percent increase over the 5,654,000 tonnesproduced in 2004. The increase would have been higher if notfor the prolonged drought season and delay in rainfall in SouthKalimantan and Lampung Sumatra earlier in 2005, whichreduced the yield per hectare. Nonetheless, average FFByield per hectare in 2005 was still higher at 21.43 tonnes perhectare as compared to 20.23 tonnes per hectare in 2004 asmore trees reached their prime (7-18 years).

We remain focused on improving our agricultural techniquesand production yields to maintain our position as a leadingCPO producer. On-going activities include optimal fertiliser

Golden Agri-Resources Ltd 12

Immature Mature Total

Sumatra 6 205 211

Kalimantan 7 59 66

Irian Jaya 0 10 10

Total 13 274 287

Total Tree Planted (By Location)(‘000 Hectares)

Total Planted Area(‘000 Hectares)

application, field management techniques, oil palm breedingand selection and research to cultivate seedlings withsuperior characteristics.

Selective replanting to replace old palm trees will be carriedout to sustain long-term production volume. We are carefulto ensure zero burning in clearing our plantations, in line withour commitment to responsible environmental practices.

ProductionWe completed the construction of three additional CPO mills,Muara Wahau (East Kalimantan), Sungai Bengkal (Jambi) andTanah Laut (South Kalimantan) in 2005, bringing our totalnumber of CPO mills to 31, with combined installed capacityof 8,045,000 tonnes of FFB per annum. We processed 6,352,000tonnes of FFB in 2005 compared to 5,896,000 tonnes in 2004,utilising about 79 percent of our total annual capacity.

We have two refineries with processing capacity of about840,000 tonnes per annum, and four palm kernel crushing plantswith processing capacity of 324,000 tonnes per annum.

Despite the prolonged drought season in South Kalimantanand Lampung Sumatra earlier in 2005, CPO production roseto 1,479,000 tonnes in 2005, 8.2 percent higher than the1,367,000 tonnes produced in 2004, mainly due to the increasein planted hectares of prime age. In addition, we saw markedimprovement in our production in the second half of 2005,

having recovered from the adverse effect of the droughtseason in previous quarters.

CPO extraction rate was 23.29 percent up from 23.19percent in 2004. We will continue to improve CPO qualityand extraction rates of our milling operations and achieveoptimum levels of output.

We firmly believe in preserving the environment andmaintaining quality; occupational health and safety isof paramount importance. PT Sinar Mas Agro Resourcesand Technology Tbk (“SMART”) has implemented theISO 14001:2000 for environment and ISO 9001:2000 forquality throughout its plantations and refineries.

In January 2006, SMART received the HACCP (HazardAnalysis Critical Control Point) Certification for both itsrefineries in Medan and Surabaya for implementinginternational standard for food safety. This is an accreditationfor food safety for our cooking oil, margarine and shortening.The certification is recognition of our refined products ashallmarks of quality.

Downstream ActivitiesThe high level of integration through our refineries in Medanand Surabaya, gives us the flexibility to sell either CPO orrefined products, and to either export or sell locally. The CPOand palm kernel we produce is largely being utilised inour downstream manufacturing operations. Sales of refinedproducts accounted for about 32 percent of our revenuein 2005.

The research facility at our Surabaya refinery is developingnew refined palm oil based products and testing ways toimprove the quality of our refined products through blendingand alternative processing methods to reduce production cost.

Golden Agri-Resources Ltd13

A. Cooking OilsB. CPOC. PKO & PKMD. Margarine and ShorteningE. Other Refined Palm Oil Based

ProductsF. Other Products

Sales: By Products(Percentage)

Net Sales: Domestic vs Exports(Percentage)

Indonesia

40% 60%

Outside Indonesia

We have continued to maintain our market share of brandedproducts in the Indonesia market and expand our penetrationin the China market through various marketing efforts suchas mass media advertising, sale promotions and expandeddistribution coverage.

In January 2005, our flagship brand FILMA received theIndonesian Customer Loyalty Award from SWA Magazine andMars Marketing Research for the highest customer loyalty inthe cooking oil category. In July 2005, FILMA was awardedSuperbrand Status 2005/2006 by Superbrands International.As part of our marketing initiatives to enhance the salesof our established brands, FILMA and KUNCI MAS, welaunched our new product ‘FILMA Margarine’ with considerablesuccess in the middle of 2005.

CHINA AGRI-BUSINESSOur newly acquired China Agri-business division (AIAR groupof companies) is one of the largest fully integrated port,oilseed storage and processing, palm oil refining and vegetableoil trading operations in China, with logistics advantages inits target markets. Subsequent to GAR’s acquisition ofthis division, the 3-month results for the fourth quarter of2005 of this division were accounted for in the Group’sconsolidated results.

We intend to expand our presence in China by increasingthis division’s capacity utilisation rate, established distributionand sales network. We plan to tap on our experienceand expertise in the Indonesia market and replicate ourdownstream palm oil based products business model in China.Like the Indonesia Agri-business division, we also have researchfacilities at our refineries in Ningbo and Zhuhai to improvethe quality of our refined products and research alternativeprocessing methods.

In Ningbo, Zhejiang Province, the division has a deep-seaport and storage facility for oil and grain and an oilseed crush-ing plant with one million tonnes annual capacity. It also hasrefining facilities in Ningbo and a refining plant in Zhuhai,Guangdong Province with 280,000 tonnes and 100,000 tonnesannual capacity respectively.

The oilseed crushing operations produce soybean meal,which are sold locally under our in-house brand, and crudesoybean oils, which are in turn processed by the refineriestogether with other edible oils. These refined oils are sold toconsumers in bulk and in consumer packs; the small-packcooking oils are mainly sold under Grand Slam brand (one ofthe top three brands in eastern China).

Capacity utilisation rate of the oilseed crushing facilities inNingbo rose to approximately 91 percent in 2005 from

Golden Agri-Resources Ltd 14

Age Profile of Trees(Percentage)

CPO Prices cif Rotterdam(US$ per Tonne)

75 percent in 2004. Utilisation rates of the refineries at Ningboand Zhuhai, were 63 percent (2004: 65 percent) and 66percent (2004: 49 percent) respectively. Our crushingoperations processed 928,000 tonnes of soybeans in 2005(2004: 768,000 tonnes); and produced 742,000 tonnes ofsoybean meal (2004: 614,000 tonnes) and 166,000 tonnes ofcrude soybean oil (2004: 139,000 tonnes).

Consumer packs remained competitive with new blendedproducts, including sunflower oil, olive oil and corn oil, beinglaunched to increase our market share. We are now focusingon high-margin products and improved sales distributionto concentrate on markets in the vicinity. We launched theMaster Chef brand of cooking oil in September 2005 as partof a niche marketing initiative targeting at the restaurant,hotel and catering businesses.

STRATEGYOur commitment to grow our core businesses to yieldlong-term sustainable value to our stakeholders is on-track.To this end, we remain focused on our core business and willcapitalise on our position as a leading CPO producer,our expertise in cultivating oil palm plantations, and our value-added capability to produce refined palm oil and edible oilproducts for commercial and retail markets.

We will continue to strengthen our competitive advantage inour core business through:

> Improving overall efficiency of our integrated operations

from plantations, mills and refineries to refined end-products;

> Strengthening our foothold in domestic markets by

maintaining our branded product market share in Indonesia

and expanding our market presence in China;

> Expanding our export sales for branded and unbranded

products;

> Consolidating our range of brands and being a one-stop shop

supplier for the high-margin range of industrial oil and fat

products in the Indonesia market;

> Planting and acquiring oil palm plantations; and

> Exploiting the growing interest to use palm oil as an

alternative energy source, bio-diesel included, and

exploring the possibility to participate in the production

of this value-added product.

Golden Agri-Resources Ltd

> Financial Report

GOLDEN AGRI-RESOURCES LTD (Incorporated in Mauritius) AND ITS SUBSIDIARIES

REPORT OF THE DIRECTORS AND FINANCIAL STATEMENTS

31 DECEMBER 2005

GOLDEN AGRI-RESOURCES LTD (Incorporated in Mauritius) AND ITS SUBSIDIARIES

REPORT OF THE DIRECTORS AND FINANCIAL STATEMENTS

31 DECEMBER 2005

CONTENTS PAGE Report of the Directors 1 - 9 Statement by the Directors 10 Report of the Auditors 11 - 12 Consolidated Income Statement 13 Consolidated Balance Sheet 14 - 15 Consolidated Statement of Changes in Equity 16 Consolidated Cash Flow Statement 17 - 19 Notes to the Consolidated Financial Statements 20 - 77

1

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) REPORT OF THE DIRECTORS 31 DECEMBER 2005 The directors are pleased to present their report together with the audited financial statements of Golden Agri-Resources Ltd ("GAR" or the "Company") and its subsidiaries (the "Group") for the financial year ended 31 December 2005. 1 Directors

The directors of the Company in office at the date of this report are: Franky Oesman Widjaja Muktar Widjaja Frankle (Djafar) Widjaja Simon Lim Rafael Buhay Concepcion, Jr. Lew Syn Pau Hong Pian Tee Kunihiko Naito (appointed on 21 February 2006) Kaneyalall Hawabhay Bertrand Denis Richard De Chazal Hong Hai and Foo Meng Kee resigned as directors of the Company on 21 February 2006. The directors would like to thank them for their contributions while serving as directors of the Company.

2 Arrangements to Enable Directors to Acquire Benefits by Means of the Acquisition of Shares and

Debentures

Neither at the end of the financial year nor at any time during the financial year did there subsist any arrangement whose object was to enable the directors to acquire benefits by means of the acquisition of shares in or debentures of the Company or any other body corporate.

3 Directors' Interests in Shares and Debentures No director holding office at 31 December 2005 had an interest in the shares or debentures of the

Company. The directors' interest in Shares and Debentures of the Company at 21 January 2006 were the same as

at 31 December 2005. 4 Directors’ Receipt and Entitlement to Contractual Benefits

Since the beginning of the financial year, no director has received or become entitled to receive a benefit by reason of a contract made by the Company or a related corporation with the director or with a firm of which he is a member, or with a company in which he has a substantial financial interest except that certain directors have received remuneration from related corporations in their capacity as directors and/or executives of those related corporations and except as disclosed in the financial statements.

2

4 Directors’ Receipt and Entitlement to Contractual Benefits (cont'd) There were certain transactions (shown in the consolidated financial statements) with corporations in

which certain directors have an interest. 5 Options to Take Up Unissued Shares

During the financial year, no option to take up unissued shares of the Company was granted. 6 Options Exercised

During the financial year, there were no shares of the Company or any corporation in the Group issued by virtue of the exercise of an option to take up unissued shares.

7 Unissued Shares Under Options

At the end of the financial year, there were no unissued shares under option. 8 Corporate Governance

The Company recognises the importance and is committed to attaining high standards of corporate governance in conformity with the Code of Corporate Governance (the “Code”) issued by Singapore Exchange Securities Trading Limited (“SGX-ST”). This Report outlines the Company's corporate governance processes and activities.

The Board of Directors

Presently, the Board of Directors (the “Board”) comprises 10 directors, with 5 executive directors and 5 non-executive, independent directors. The names and key information of the directors are set out in pages 6 to 8 of the Annual Report.

3

8 Corporate Governance (cont'd) The Board of Directors (cont’d)

The Board meets to consider, inter alia, the following corporate events and actions:

• approval of results announcements; • approval of the annual report and accounts; • convening of shareholders’ meetings; • material acquisitions and disposal of assets; • annual budgets; • interested person transactions; and • corporate governance.

Certain matters are delegated to the various Board Committees set up by the Board, which act within their respective terms of references as approved by the Board. See paragraphs (i) to (iv) on Board Committees below.

In 2005, the Board held 5 meetings. The Company’s Articles of Association provides for meetings of the Board by means of teleconference or similar communication equipment. The attendance of the directors and committee members at meetings of the Board and Board Committees respectively, in 2005 is as follows:

GAR Board Audit Committee Nominating Committee Remuneration Committee

Name

No. of Meetings

Held

No. of Meetings Attended

No. of Meetings

Held

No. of Meetings Attended

No. of Meetings

Held

No. of Meetings Attended

No. of Meetings

Held

No. of Meetings Attended

Franky Oesman Widjaja (executive) 5 4 - - 1 1 - -

Muktar Widjaja (executive) 5 5 - - - - - -

Frankle (Djafar) Widjaja (executive) 5 5 - - - - 2 2

Simon Lim (executive) 5 4 - - - - - -

Rafael Buhay Concepcion, Jr. (executive) 5 5 - - - - - -

Lew Syn Pau (non-executive, independent) 5 5 8 8a 1 1a - -

Hong Pian Teeb (non-executive, independent) 5 5 8 8 - - 2 2

Kaneyalall Hawabhayc (non-executive, independent) 5 5 - - - - - -

Bertrand Denis Richard De Chazal (non-executive, independent) 5 2 - - - - - -

Hong Haid (non-executive, independent) 5 5 8 7** 1 1 - -

Foo Meng Keee (non-executive, independent) 5 5 8 7** - - 2 2

Kunihiko Naitof (non-executive, independent) - - - - - - - -

** Represents full attendance at all relevant audit committee meetings a Resigned on 21 February 2006 (Audit Committee and Nominating Committee) b Appointed on 21 February 2006 (Nominating Committee) c Appointed on 21 February 2006 (Audit Committee) d Resigned on 21 February 2006 (Board, Audit Committee and Nominating Committee) e Resigned on 21 February 2006 (Board, Audit Committee and Remuneration Committee) f Appointed on 21 February 2006 (Board, Audit Committee and Remuneration Committee) and on 27 February

2006 (Nominating Committee)

4

8 Corporate Governance (cont’d)

The Board of Directors (cont’d) The Board examines its size and comprises directors from different industries, with vast experience and knowledge. There is a strong and independent element on the Board, with independent directors making up half of the Board. We believe that the independent directors have demonstrated a high commitment in their roles as directors and have ensured that there is a good balance of power and authority. In view of the Chairman and Chief Executive Officer posts being held by the same person, the Chairman of the Audit Committee acts as the Lead Independent Director. The Board Committees

Particulars of the various Committees set up by the Board are as follows:

(i) Executive Committee

The Executive Committee ("EC") currently comprises the following members:

Group A Franky Oesman Widjaja Muktar Widjaja Frankle (Djafar) Widjaja Group B Simon Lim Rafael Buhay Concepcion, Jr. Bertrand Denis Richard De Chazal

Kaneyalall Hawabhay (resigned from EC on 21 February 2006) The EC's role includes supervising the management of the business and affairs of the Group. (ii) Audit Committee

The Audit Committee ("AC") currently comprises 3 members all of whom are non-executive and independent. Members of the AC are as follows:

Hong Pian Tee (appointed as Chairman on 21 February 2006) Kunihiko Naito Kaneyalall Hawabhay

In 2005, the AC held 8 meetings.

The AC has the explicit authority to investigate any matter within its terms of reference. In addition, the AC has full access to and co-operation of Management and has full discretion to invite any director or executive officer to attend its meetings. Reasonable resources are made available to enable it to discharge its functions properly.

The duties of the AC include keeping under review the scope and results of the audit and its cost effectiveness and the independence and objectivity of the external auditors.

5

8 Corporate Governance (cont’d)

The Board Committees (cont'd)

(ii) Audit Committee (cont'd) In performing its functions, the AC meets with the internal and external auditors, and reviews the overall scope of both internal and external audits, and the assistance given by Management to the auditors. Where necessary, the AC also meets with the internal and external auditors without the presence of Management. The internal and external auditors have unrestricted access to the AC. During the course of audit, the external auditors carried out a review of the effectiveness of the Company’s material internal controls, including financial, operational and compliance controls to the extent of their scope as laid out in their audit plan. Material non-compliance and internal control weaknesses noted during their audit are reported to the AC together with their recommendations. The AC has reviewed the Group's risk assessment, and, based on the audit reports and management controls in place, is satisfied that there are adequate internal controls in the Group.

In addition to its statutory functions, the AC considers and reviews any other matters as may be agreed to by the AC and the Board. In particular, it reviews with Management, and where relevant, the auditors, the results announcements, annual report and accounts, interested person transactions and corporate governance, before submission to the Board for approval or adoption. The AC also reviews the audit plans, and the co-operation and assistance given by Management to the external auditors.

The AC reviews the independence of the external auditors and recommends to the Board of Directors the nomination of external auditors. The Chief Internal Auditor reports to the chairman of the AC. On administrative matters, he reports to the Chief Executive Officer. The Chief Internal Auditor has met the standards set by nationally or internationally recognised professional bodies including the Standards for the Professional Practice of Internal Auditing set by The Institute of Internal Auditors.

The AC ensures that the internal audit function is adequately staffed and has appropriate standing within the Company. It also ensures the adequacy of the internal audit function. (iii) Nominating Committee

The Nominating Committee ("NC") currently comprises 3 members, a majority of whom, including the chairman, is non-executive and independent. Members of the NC are as follows:

Hong Pian Tee (appointed as Chairman on 21 February 2006) Kunihiko Naito Franky Oesman Widjaja

In 2005, the NC met once.

The role of the NC is to establish a formal and transparent process for the Company, for the appointment of new directors and re-nomination and re-election of directors at regular intervals. Except for the director holding the position of Chief Executive Officer, all directors are to submit themselves for re-election at regular intervals.

6

8 Corporate Governance (cont’d)

The Board Committees (cont'd)

(iii) Nominating Committee (cont’d)

The Company has in place a system to assess the effectiveness/performance of the Board. In proposing objective performance criteria for such evaluation and determination, for the Board's approval, consideration was given to a number of factors, including those set out in the Code. The Board has approved specific objective performance criteria for such evaluation. The Board adopts the independence test recommended by the Code. Taking into account the independence test, the NC considers and determines the independence of directors. (iv) Remuneration Committee

The Remuneration Committee ("RC") currently comprises 3 members, a majority of whom, including the chairman, is non-executive and independent. Its members are as follows:

Hong Pian Tee (Chairman) Kunihiko Naito Frankle (Djafar) Widjaja

In 2005, the RC held 2 meetings.

The RC’s role is to review and recommend to the Board, an appropriate and competitive framework of remuneration or compensation policy for the Board, key executives and employees within the Group. Currently, the Company does not have long-term incentive schemes, including share schemes. Detailed public disclosure of the directors and key executives' remuneration is currently not adopted. The number of directors falling under the remuneration bands of S$250,000 are as follows:

Number of Directors Remuneration Band 2005 2004 S$500,000 to S$749,999 1 1 S$250,000 to S$499,999 1 1 Below S$250,000 9 10 11 12

Access to Information

In order to ensure that the Board is able to fulfill its responsibilities, Management provides the Board with complete and adequate information in a timely manner. Such information extends to documents on matters to be brought up before the Board at board meetings. Senior staff and professionals, who can provide additional insights into the matters to be discussed at Board meetings, are also invited to be present at meetings. As directors may have further enquiries on the information provided, they have separate and independent access to the Company’s senior management. Management provides the Board with financial statements of the Group on a quarterly basis. In view of the Group's size and nature of operations, such quarterly, and not monthly, reporting is considered adequate.

7

8 Corporate Governance (cont’d)

Access to Information (cont'd)

The directors also have separate and independent access to the company secretary’s nominee(s) who attends all Board meetings. Where the directors, either individually or as a group, in the furtherance of their duties, require professional advice, the company secretary’s nominee(s) can assist them in obtaining independent professional advice, at the Company’s expense. Communication with Shareholders

Since 2003, the Company announces its results on a quarterly basis. All information and its quarterly results are disseminated via SGXNET.

The Company does not practise selective disclosure. Results and annual reports are announced or issued within the mandatory period.

All shareholders of the Company receive the annual report and notice of annual general meeting. The notice is also advertised in the newspapers. At the annual general meeting, shareholders are given the opportunity to air their views and ask directors questions regarding the Group. The Articles of Association of the Company allows a member of the Company to appoint one or two proxies to attend and vote instead of the member. Dealings in Securities

The Company adopts the SGX-ST Best Practices Guide, applicable to the Company, its directors and officers, in relation to dealings in the Company’s securities. Dealings in the Company’s securities are prohibited during the period commencing (i) two weeks before announcement of the Company’s first, second and third quarter results and (ii) one month before the announcement of the Company’s full year results, and ending on the date of the announcement of the results. Such dealings are also prohibited whilst in possession of unpublished material price-sensitive information.

8

9 Interested Person Transactions Disclosure The aggregate value of all interested person transactions during the financial year under review is as

follows:

Name of interested person

Aggregate value of all interested person

transactions during the financial year under review (excluding transactions less

than S$100,000 and transactions conducted under

shareholders' mandate* pursuant to Rule 920)

Aggregate value of all

interested person transactions conducted

under shareholders' mandate* pursuant to

Rule 920 (excluding transactions less than S$100,000)

US$ US$ Asia Food & Properties Limited 155,000,000** 4,448,288 AFP International Finance (2) Ltd Nil 1,354,115 Asia Integrated Agri Resources

Limited

Nil

18,012,195

P.T. Asuransi Sinar Mas Nil 2,140,095 P.T. Cakrawala Mega Indah Nil 1,351,175 P.T. Rolimex Kimia Nusamas Nil 21,145,090 P.T. Royal Oriental Nil 1,433,230 Zhuhai Huafeng Foodstuff Co., Ltd Nil 219,358 Zhuhai Shining Gold Oil and Fats

Industry Co., Ltd

Nil

4,650,745

Total 155,000,000 54,754,291

Name of interested person

Aggregate value of all interested person

transactions during the financial year under review (excluding transactions less

than S$100,000 and transactions conducted under

shareholders' mandate* pursuant to Rule 920)

Aggregate Balance as at 31 December 2005***

US$ US$ BII Limited, Cook Islands Nil 3,304,000

* Renewed at Annual General Meeting on 28 April 2005. ** Independent shareholders' approval obtained for the interested person transaction at the

Extraordinary General Meeting held on 13 October 2005. *** This refers to the placement of deposits with an interested person as at 31 December 2005.

There was no placement of further or fresh deposits with BII Limited, Cook Islands during the year; transactions comprised only roll-overs of deposits and its accrued interest thereon. No disclosure is made of the aggregate value of these transactions conducted during the financial year as it is not practicable to determine these aggregate values since these transactions involve numerous roll-over of placements. Subsequently, these deposits have been fully repaid on 7 February 2006.

9

10 Key Management Staff

The key management staff are also directors of the Company, and their background information are set out in pages 6 to 8 of the Annual Report.

11 Auditors

The auditors, Moore Stephens, have expressed their willingness to accept reappointment.

On behalf of the Board of Directors FRANKY OESMAN WIDJAJA Director SIMON LIM Director 16 March 2006

10

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) STATEMENT BY THE DIRECTORS 31 DECEMBER 2005 In the opinion of the directors, the consolidated financial statements set out on pages 13 to 77 are drawn up so as to give a true and fair view of the state of affairs of the Group as at 31 December 2005 and of the results of the business, changes in equity and cash flows of the Group for the financial year then ended and at the date of this statement there are reasonable grounds to believe that the Group will be able to pay its debts as and when they fall due. On behalf of the Board of Directors FRANKY OESMAN WIDJAJA SIMON LIM Director Director 16 March 2006

11

REPORT OF THE AUDITORS TO THE MEMBERS OF GOLDEN AGRI-RESOURCES LTD (Incorporated in Mauritius) 1 We have audited the accompanying consolidated financial statements of Golden Agri-Resources Ltd

(the "Company") and its subsidiaries (the "Group") as at 31 December 2005 and for the year then ended set out on pages 13 to 77. These financial statements are the responsibility of the directors of the Company whose opinion thereon is set out in the statement by the directors. Our responsibility is to express an opinion on these financial statements based on our audit.

2 We conducted our audit in accordance with International Standards on Auditing. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes an examination, on a test basis, of evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

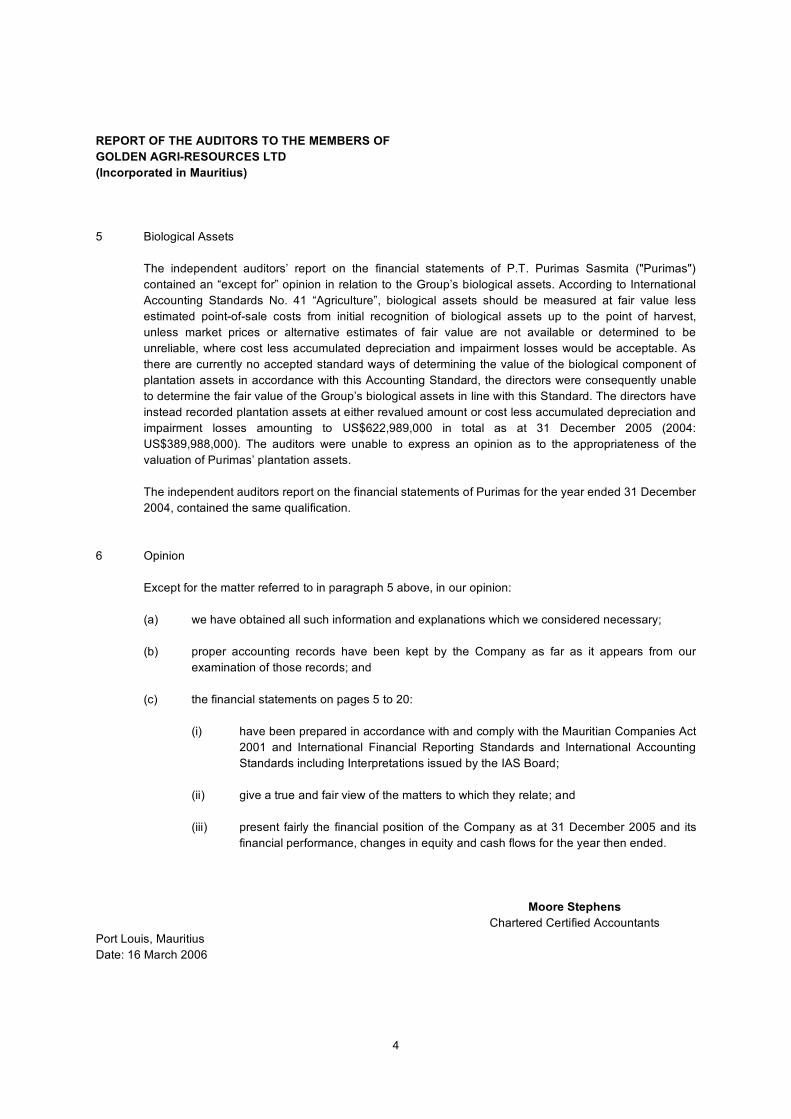

3 Biological Assets The independent auditors’ report on the financial statements of P.T. Purimas Sasmita ("Purimas")

contained an “except for” opinion in relation to the Group’s biological assets. According to International Accounting Standards No. 41 “Agriculture”, biological assets should be measured at fair value less estimated point-of-sale costs from initial recognition of biological assets up to the point of harvest, unless market prices or alternative estimates of fair value are not available or determined to be unreliable, where cost less accumulated depreciation and impairment losses would be acceptable. As there are currently no accepted standard ways of determining the value of the biological component of plantation assets in accordance with this Accounting Standard, the directors were consequently unable to determine the fair value of the Group’s biological assets in line with this Standard. The directors have instead recorded plantation assets at either revalued amount or cost less accumulated depreciation and impairment losses amounting to US$622,989,000 in total as at 31 December 2005 (2004: US$389,988,000). The auditors were unable to express an opinion as to the appropriateness of the valuation of Purimas’ plantation assets. The independent auditors report on the financial statements of Purimas for the year ended 31 December 2004, contained the same qualification.

12

REPORT OF THE AUDITORS TO THE MEMBERS OF GOLDEN AGRI-RESOURCES LTD (Incorporated in Mauritius) 4 Opinion

Except for the matter referred to in the preceding paragraph, in our opinion the consolidated financial statements present fairly, in all material respects, the financial position of the Group as at 31 December 2005, the results of its operations, its cash flows and changes in equity for the financial year then ended, in accordance with International Financial Reporting Standards.

Moore Stephens Certified Public Accountants Singapore Date: 16 March 2006 Date:

13

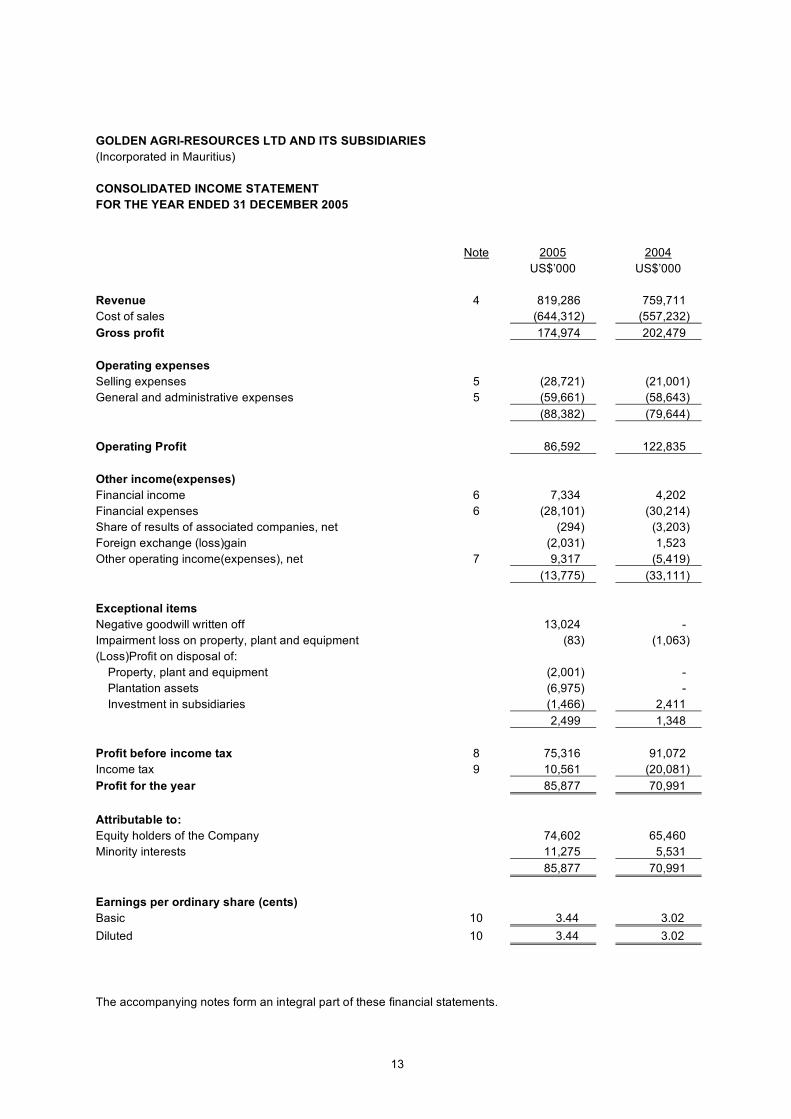

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2005 Note 2005 2004 US$’000 US$’000 Revenue 4 819,286 759,711 Cost of sales (644,312) (557,232) Gross profit 174,974 202,479 Operating expenses Selling expenses 5 (28,721) (21,001) General and administrative expenses 5 (59,661) (58,643) (88,382) (79,644) Operating Profit 86,592 122,835 Other income(expenses) Financial income 6 7,334 4,202 Financial expenses 6 (28,101) (30,214) Share of results of associated companies, net (294) (3,203) Foreign exchange (loss)gain (2,031) 1,523 Other operating income(expenses), net 7 9,317 (5,419) (13,775) (33,111) Exceptional items Negative goodwill written off 13,024 - Impairment loss on property, plant and equipment (83) (1,063) (Loss)Profit on disposal of: Property, plant and equipment (2,001) - Plantation assets (6,975) - Investment in subsidiaries (1,466) 2,411 2,499 1,348 Profit before income tax 8 75,316 91,072 Income tax 9 10,561 (20,081) Profit for the year 85,877 70,991 Attributable to: Equity holders of the Company 74,602 65,460 Minority interests 11,275 5,531 85,877 70,991 Earnings per ordinary share (cents) Basic 10 3.44 3.02 Diluted 10 3.44 3.02 The accompanying notes form an integral part of these financial statements.

14

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED BALANCE SHEET AS AT 31 DECEMBER 2005 Note 2005 2004 US$’000 US$’000 Assets Current Assets Cash and cash equivalents 11 79,988 51,389 Short-term investments 12 21,142 39,694 Due from a related party 16 3,304 - Trade receivables 13 49,282 33,381 Other receivables 14 64,885 27,161 Inventories 15 143,335 89,979 361,936 241,604 Non-Current Assets Due from a related party 16 - 118,632 Other long-term receivables 17 94,657 155,550 Associated companies 19 18,047 18,632 Property, plant and equipment 20 647,962 414,027 Plantation assets 21 622,989 389,988 Deferred income tax 18 18,173 10,394 Deferred charges 22 4,580 3,620 Brands and trademarks 23 2,882 3,202 Goodwill 24 26,060 18,194 1,435,350 1,132,239 Total Assets 1,797,286 1,373,843 The accompanying notes form an integral part of these financial statements.

15

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED BALANCE SHEET (cont’d) AS AT 31 DECEMBER 2005 Note 2005 2004 US$’000 US$’000 Liabilities and Equity Current Liabilities Bank overdraft, unsecured - 8 Short-term loans 25 158,448 122,629 Trade payables 26 139,317 53,823 Other payables 27 48,094 49,156 Taxes payable 9 3,355 4,352 Obligations under finance leases 28 715 105 349,929 230,073 Non-Current Liabilities Obligations under finance leases 28 1,327 212 Long-term borrowings 29 207,040 271,693 Deferred income tax 18 103,347 31,976 Other long-term payables 30 1,715 1 313,429 303,882 Total Liabilities 663,358 533,955 Equity Attributable to Equity Holders of the Company Issued capital 31 216,867 216,867 Share premium 296,595 296,595 Other paid-in capital 184,318 184,318 Other reserves 125,389 9,031 Hedging reserve (1,853) - Foreign currency translation reserve 196 - Cumulative translation adjustments (16,684) (16,684) Retained earnings 197,075 116,676 1,001,903 806,803 Minority Interests 132,025 33,085 Total Equity 1,133,928 839,888 Total Liabilities and Equity 1,797,286 1,373,843 The accompanying notes form an integral part of these financial statements.

16

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2005 Minority Total <------------------------------------------------Attributable to Equity Holders of the Company-----------------------------------------------> Interests Equity Foreign Other Currency Cumulative Issued Share Paid-in Other Hedging Translation Retained Translation Capital Premium Capital Reserves Reserve Reserve Earnings Adjustments Total

US$’000 US$’000 US$’000 US$’000 US$’000 US$’000 US$’000 US$’000 US$’000 US$’000 US$’000

Balance at 1.1.2004 216,867 296,595 184,318 9,199 - - 51,216 (16,684) 741,511 27,180 768,691 Profit for the year - - - - - - 65,460 - 65,460 5,531 70,991 Revaluation Surplus - - - 414 - - - - 414 374 788 Adjustment to fair value for entities under common control

-

-

-

(582)

-

-

-

-

(582)

-

(582) Net (loss)gain recognised directly in equity - - - (168) - - - - (168) 374 206

Balance at 31.12.2004

216,867

296,595

184,318

9,031

-

-

116,676

(16,684)

806,803

33,085

839,888

Balance at 1.1.2005 as previously reported

216,867

296,595

184,318

9,031

-

-

116,676

(16,684)

806,803

33,085

839,888

Effect of adopting IFRS3 - - - - - - 5,797 - 5,797 1,908 7,705 Balance at 1.1.2005 as restated

216,867

296,595

184,318

9,031

-

-

122,473

(16,684)

812,600

34,993

847,593

Profit for the year - - - - - - 74,602 - 74,602 11,275 85,877 Revaluation Surplus - - - 116,358 - - - - 116,358 72,000 188,358 Arising from acquisition of a subsidiary

-

-

-

-

-

-

-

-

-

13,436

13,436 Additional investment in subsidiaries

-

-

-

-

-

-

-

-

-

(872)

(872) Cash subscribed by minority shareholders

-

-

-

-

-

-

-

-

-

1,165

1,165 Decrease in fair value of hedging derivatives

-

-

-

-

(1,853)

-

-

-

(1,853)

-

(1,853) Foreign currency translation

-

-

-

-

-

196

-

-

196

28

224

Net gain(loss) recognised directly in equity - - - 116,358 (1,853) 196 - - 114,701 85,757 200,458

Balance at 31.12.2005

216,867

296,595

184,318

125,389

(1,853)

196

197,075

(16,684)

1,001,903

132,025

1,133,928

The accompanying notes form an integral part of these financial statements.

17

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED CASH FLOW STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2005 2005 2004 US$’000 US$’000 Cash flows from operating activities Profit before income tax 75,316 91,072 Adjustments for: Depreciation 58,710 55,580 Amortisation 1,004 4,562

Unrealised foreign exchange gain on short-term loans, long-term borrowings and receivables, net

(3,050)

(4,401)

(Gain)Loss on conversion of project plasma plantations (282) 3,305 Share of results of associated companies, net 294 3,203 Write off of negative goodwill (13,024) (366) Impairment loss on property, plant and equipment 83 1,063 Loss on disposal and write off of: Property, plant and equipment 2,314 396 Plantation assets 7,189 8,638 Loss(Profit) on disposal of investment in subsidiaries 1,466 (2,411) Allowance(Write-back) for impairment loss on: Inventories (824) - Trade receivables and trade receivables written off 73 1,168 Non-trade receivables - 755 Interest income (7,334) (4,202) Interest expense 27,709 29,488 Operating cash flows before working capital changes 149,644 187,850 Changes in operating assets and liabilities: Trade receivables (3,857) (10,322) Inventories (20,146) (6,565) Other receivables (7,356) 3,646 Trade payables (2,822) 5,271 Other payables (2,227) (12,035) Cash generated from operations 113,236 167,845 Interest paid (34,974) (27,573) Interest received 4,251 2,433 Income tax refund 3,962 6,225 Net cash from operating activities 86,475 148,930 The accompanying notes form an integral part of these financial statements.

18

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED CASH FLOW STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2005 (cont’d) 2005 2004 US$’000 US$’000 Cash flows from investing activities Proceeds from sale of property, plant and equipment 5,966 3,973 Proceeds from sale of plantation assets 8,785 670 Capital expenditure on property, plant and equipment (56,694) (49,966) Capital expenditure on plantation assets (9,633) (17,083) Net decrease(increase) in short-term investments 18,890 (39,206) Repayments of current account and deposit with a related party 118,156 57,755 Investments in Plasma/KKPA program plantations, net 2,158 (54) Net decrease(increase) in other long-term receivables from related parties 62,034 (52,706) Dividends received 215 - Acquisition of subsidiaries, net of cash acquired (Note A) (121,672) (1,810) Proceeds from sale of investment in subsidiaries (Note B) 1,390 5,100 Investments in software development (199) (1,213) Increase in deferred land rights (1,245) (1,408) Net decrease in other receivables 608 289 Net cash from(used in) investing activities 28,759 (95,659) Cash flows from financing activities Proceeds from short-term loans and overdraft 57,131 24,614 Proceeds from long-term borrowings 8,119 114,967 Payments of short-term loans (47,051) (23,876) Payments of long-term borrowings (103,483) (154,302) Decrease in trade financing (795) (1,085) Due to related parties - (500) Decrease in trust receipt payables (1,521) (1,229) Cash subscribed from minority shareholders 1,165 - Deferred loan charges and long-term bank loan administration costs (200) (804) Net cash used in financing activities (86,635) (42,215) Net increase in cash and cash equivalents 28,599 11,056 Cash and cash equivalents at the beginning of the year 51,389 40,333 Cash and cash equivalents at the end of the year (Note 11) 79,988 51,389

The accompanying notes form an integral part of these financial statements.

19

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) CONSOLIDATED CASH FLOW STATEMENT (cont’d) FOR THE YEAR ENDED 31 DECEMBER 2005 Notes to the Consolidated Cash Flow Statement: A. Summary of the effect of acquisition of subsidiaries 2005 2004 US$’000 US$’000 Cash and cash equivalents 33,741 1,087 Other current assets 89,628 1,845 Other current liabilities (159,062) (12,443) Non-current assets 217,043 8,210 Non-current liabilities (12,591) - Minority interests (13,491) - Net assets(liabilities) acquired 155,268 (1,301) Goodwill on consolidation 145 4,198 Total purchase price 155,413 2,897 Cash of acquired subsidiaries (33,741) (1,087) Net cash outflow on acquisition of subsidiaries 121,672 1,810 B. Summary of the effect of disposal of subsidiaries 2005 2004 US$’000 US$’000 Cash and cash equivalents 119 184 Other current assets 76 1,134 Current liabilities (450) (1,774) Net current liabilities (255) (456) Non-current assets 3,230 4,842 Non-current liabilities - (1,513) Exceptional (loss)gain on disposal of subsidiaries (1,466) 2,411 Proceed from disposal of subsidiaries 1,509 5,284 Cash of disposed subsidiaries (119) (184) Net cash inflow on disposal of subsidiaries 1,390 5,100 The accompanying notes form an integral part of these financial statements.

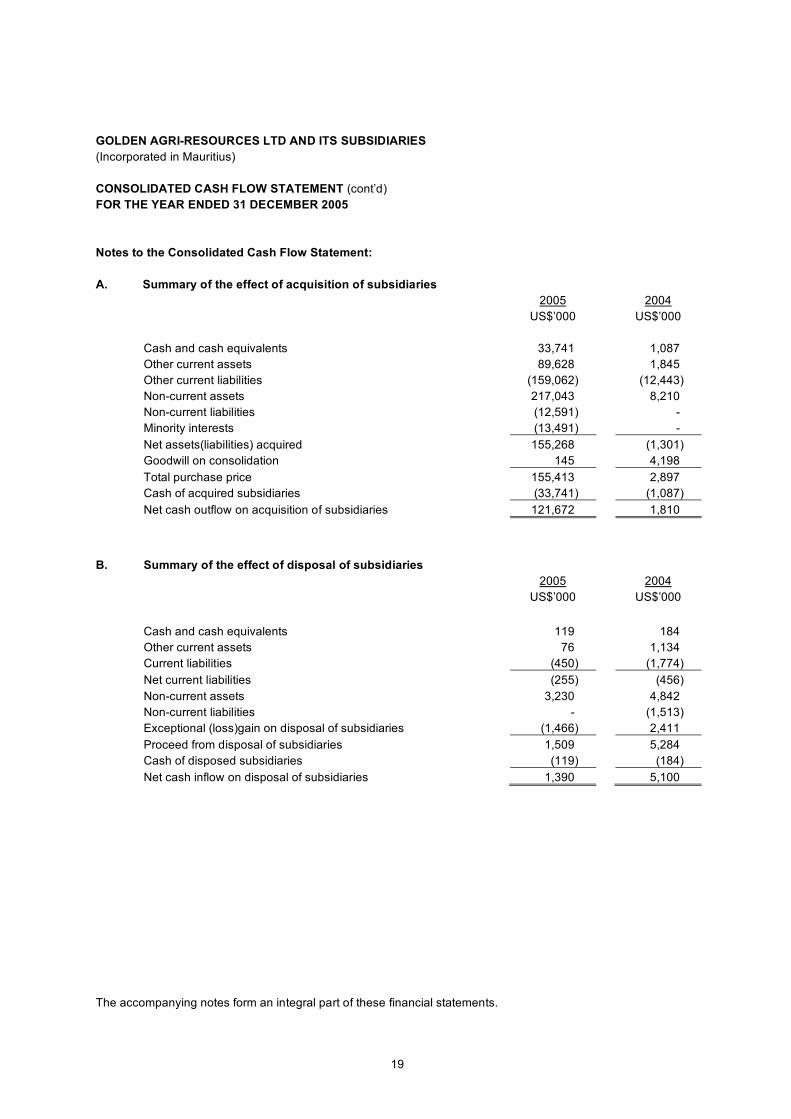

20

GOLDEN AGRI-RESOURCES LTD AND ITS SUBSIDIARIES (Incorporated in Mauritius) NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2005 These notes form an integral part of and should be read in conjunction with the accompanying consolidated financial statements. 1 General

Golden Agri-Resources Ltd (the "Company") is a limited company incorporated in Mauritius. The registered office of the Company is at 10, Frère Félix de Valois Street, Port Louis, Mauritius.

The immediate holding company is Asia Food & Properties Limited (“AFP”), incorporated in Singapore. The directors regard Flambo International Limited, a company incorporated in the British Virgin Islands as the ultimate holding company. The Controlling Shareholders of the Company comprise certain members of the Widjaja Family. The Company is principally engaged as an investment holding company. The principal activities of the subsidiaries and associated companies are described in Note 41 to the consolidated financial statements.

The consolidated financial statements for the year ended 31 December 2005 were authorised for issue by the Board of Directors on 16 March 2006.

2 Adoption of New and Revised International Financial Reporting Standards ("IFRS")

In the current year, the Group has adopted the following new and revised Standards and Interpretations issued by the International Accounting Standards Boards ("IASB") and the International Financial Reporting Interpretations Committee of the IASB that are relevant to its operations, and effective for accounting periods beginning on 1 January 2005. • IFRS 3, Business Combinations (New 2003) • IFRS 5, Non-current Assets Held for Sale and Discontinued Operations (New 2004) • IAS 1, Presentation of Financial Statements (Revised 2003) • IAS 2, Inventories (Revised 2003) • IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors (Revised 2003) • IAS 10, Events after the Balance Sheet Date (Revised 2003) • IAS 16, Property, Plant and Equipment (Revised 2003) • IAS 17, Leases (Revised 2003) • IAS 21, The Effect of Changes in Foreign Exchange Rates (Revised 2003) • IAS 24, Related Party Disclosures (Revised 2003) • IAS 27, Consolidated and Separate Financial Statements (Revised 2003) • IAS 28, Investments in Associates (Revised 2003) • IAS 32, Financial Instruments: Disclosure and Presentation (Revised 2003) • IAS 33, Earnings per Share (Revised 2003) • IAS 39, Financial Instruments: Recognition and Measurement (Revised 2004)

Except for the adoption of IFRS 3, Business Combinations as disclosed below, the adoption of the above mentioned standards had no significant impact on the Group's financial statements.

21

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2005 2 Adoption of New and Revised International Financial Reporting Standards ("IFRS") (cont'd)

The adoption of IFRS 3, Business Combinations, has resulted in a change in the accounting policy for goodwill. Goodwill is stated at cost less any accumulated impairment losses and is no longer amortised. Instead, goodwill is tested annually for impairment or when circumstances change, indicating that goodwill might be impaired. Negative goodwill is recognised immediately in the income statement, instead of being amortised over its useful life. In accordance with the transitional rules of IFRS 3, in respect of goodwill acquired in business combinations for which the agreement date was before 31 March 2004, the Group has applied the revised accounting policy for goodwill prospectively from the beginning of its first annual period beginning on or after 31 March 2004, i.e. 1 January 2005. Therefore, from 1 January 2005, the Group has discontinued amortising such goodwill and has tested the goodwill for impairment. As at 1 January 2005, the carrying amount of amortisation accumulated before that date of US$8,014,000 has been eliminated, with a corresponding decrease in the cost of goodwill. The carrying amount of negative goodwill which amounted to US$7,705,000 has been derecognised, with a corresponding credit to opening retained earnings and minority interests of US$5,797,000 and US$1,908,000 respectively. Because this revised accounting policy has been applied prospectively, the change has had no impact on amounts reported for 2004 or prior periods. No amortisation has been charged in 2005. The net amortisation charged in year 2004 was US$867,000.

3 Summary of Significant Policies

(I) Accounting Policies

(a) Basis of Financial Statements Preparation

The consolidated financial statements, which are expressed in United States dollars, are prepared in accordance with the historical cost convention, except as disclosed in the accounting policies below. The consolidated financial statements are drawn up under IFRS, however, as disclosed in Note 21(c), they are not prepared in accordance with International Accounting Standards No. 41, Agriculture, as the directors are unable to determine the fair value of the Group's biological assets in line with this Standard. The preparation of financial statements requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the financial year. Although these estimates are based on management's best knowledge of current events and actions, actual results may actually differ from these estimates. (b) Basis of Consolidation

The consolidated financial statements include the financial statements of the Company and its subsidiaries (the "Group") made up to 31 December. The results of subsidiaries acquired or disposed during the year are included in or excluded from the consolidated financial statements from the effective date of acquisition or disposal. All inter-company balances, transactions and any unrealised profit or loss on inter-company transactions are eliminated on consolidation.

22

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2005 3 Summary of Significant Policies (cont’d)

(I) Accounting Policies (cont’d) (b) Basis of Consolidation (cont'd)

A company is a subsidiary if it is controlled by any of the Group companies, which generally occurs when more than 50% of the issued voting capital is held long-term, directly or indirectly, by the Group and the Group is able to govern the financial and operating policies of the company so as to obtain benefits from its activities. Minority interests in the net assets of consolidated subsidiaries are identified separately from the Group’s equity therein. Minority interests consist of the amount of those interests at the date of the original business combination and the minority’s share of changes in equity since the date of the combination. Losses applicable to the minority in excess of the minority’s interest in the subsidiary’s equity are allocated against the interests of the Group except to the extent that the minority has a binding obligation and is able to make an individual investment to cover losses. The purchase method of accounting is used to account for the acquisition of subsidiaries. The cost of an acquisition is measured at the fair value of the assets given, equity instruments issued or liabilities incurred or assumed at the date of exchange, plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values on the date of acquisition, irrespective of the extent of any minority interests.

Business combinations which involve the transfer of net assets or the exchange of shares between entities under common control are accounted for as a uniting of interests. The financial information included in the consolidated financial statements reflects the combined results of the entities concerned as if the merger had been in effect for all periods presented.

(c) Associated Companies

Associated companies are entities in which the Group has significant influence, but not control, which generally occurs when the Group has a direct or indirect ownership interest of 20% to 50% or is in the position to exercise significant influence on the financial and operating policy decisions, and are accounted for by the equity method. Under the equity method, the cost of investment is increased or decreased by the Group's share in net earnings or losses and other equity changes of the associated company since the date of acquisition. Losses of an associated company in excess of the Group's interest in that associated company (which includes any long-term interests, in substance, form part of the Group's net investments in that associated company) are not recognised.

(d) Functional and Presentation Currency

The functional currency of the Company, its Indonesian subsidiaries and a number of its other subsidiaries is the United States dollar. Because of the international nature of the crude palm oil and soybean products that the Group is principally engaged in and the fact that the transactions are usually denominated in or derived from United States dollars, the directors are of the opinion that the United States dollar reflects the primary economic environment in which the entities operate.

23

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2005 3 Summary of Significant Policies (cont’d)

(I) Accounting Policies (cont’d)

(d) Functional and Presentation Currency (cont'd)

The consolidated financial statements are presented in United States dollars, which is the Company’s functional currency and presentation currency.

(e) Foreign Currencies Transactions involving foreign currencies are translated into the respective functional currencies of the companies in the Group at the rates of exchange prevailing at the time the transactions are entered into. At the balance sheet date, monetary assets and liabilities denominated in foreign currencies are translated into the respective functional currencies at exchange rates prevailing at such date, and any exchange difference are taken to the income statement. Currency translation differences on non-monetary items, such as equity investments held at fair value through profit or loss, are reported as part of the fair value gain or loss. Currency translation differences on non-monetary items, such as equity investments classified as available-for-sale financial assets, are included as part of the fair value gain or loss. In the preparation of the consolidated financial statements, the financial statements of those subsidiaries whose functional currency is not the United States dollar (i.e. “foreign entities”) have been translated to United States dollars, the functional currency of the Company, as follows:

(i) all assets and liabilities at the exchange rates approximating those prevailing on the

balance sheet dates;

(ii) share capital and reserves at historical exchange rates; and (iii) profit and loss items at the average exchange rates for the years.

Exchange differences arising from the above translations are taken directly to “Foreign Currency Translation” reserve. Such translation differences are recognised in income statement in the period in which the foreign entity is disposed of. (f) Revenue Recognition

Revenue arising from sales of goods is recognised when the products are shipped for export sales and when the products are delivered to the customers for domestic sales and collectibility of the related receivables is probable. Revenue from processing services is recognised when the services are rendered. Interest income is accrued on a time-proportion basis, by reference to the principal outstanding and at the effective interest rate applicable.

24

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2005 3 Summary of Significant Policies (cont’d)

(I) Accounting Policies (cont’d)

(g) Cash and Cash Equivalents Cash for the cash flow statement includes cash and cash equivalents. Cash and cash equivalents

classified under current assets comprise cash on hand, cash in banks and time deposits which are short term, highly liquid assets that are readily convertible into known amounts of cash and which are subject to an insignificant risk of change in value.

(h) Trade Receivables

Trade receivables are measured at initial recognition at fair value which is normally the original invoiced amount, and are subsequently measured at amortised cost using the effective interest rate method. Appropriate allowances for estimated irrecoverable amounts are recognised in income statement when there is objective evidence that the asset is impaired. The allowance recognised is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the effective interest rate computed at initial recognition. (i) Inventories

Inventories are stated at the lower of cost and net realisable value. Cost comprises all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition. Cost is determined by the weighted average method for finished goods and by the moving average method for other inventories, such as raw material, spare parts and fuel, chemical and packing supplies and others. Net realisable value is the estimated selling price less all estimated costs of completion necessary to make the sale.

(j) Financial Assets