@ smr gmbh steel & metals market research reutte ... smr gmbh steel & metals market research...

TRANSCRIPT

@ SMR GmbH

Steel & Metals Market Research

Reutte, October 2013

This study was exclusively prepared for IMOA.

It may not be copied, published or disclosed to third parties without the permission of SMR GmbH.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 1

IMOA recently completed the latest update of its regular end use analysis. The Mo market perspectives for the next decade remain promising: the demand for Mo will reach more than 430,000 t by 2022; the market will grow by more than 3% in the period 2012 – 2022.

The fastest growing region will be Rest of the World (India, Africa, Middle East) with 4.8% p.a., followed by China with 4.2% p.a. Europe and America will both grow below 3% in the next decade. After two years with limited growth in 2012 and 2013, the global Mo demand will gain momentum from 2014 on.

First Use Structure

Almost 322,000 t of Mo (including Mo in scrap) was consumed in 2012

compared to around 318,000 t in the previous year, which corresponds to a

1% market growth. The first use structure only slightly changed within this time

frame, with the largest first use sectors being Engineering Steels (36%),

Stainless Steels (26%) and Tool and High Speed Steels (combined 11%).

Engineering Steels36%

Stainless Steels26%

Tool Steels11%

Chemicals10%

Foundries8%

Nickel Alloys

5%

Mo Metal4%

Total First Use

321,600 t

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 2

In 2012 the market developed somewhat better than expected in the last issue

of this report, particularly due to strong deliveries in the for the oil and gas

segment (including pipeline deliveries for Chinese gas pipelines) which

prevented a negative growth.

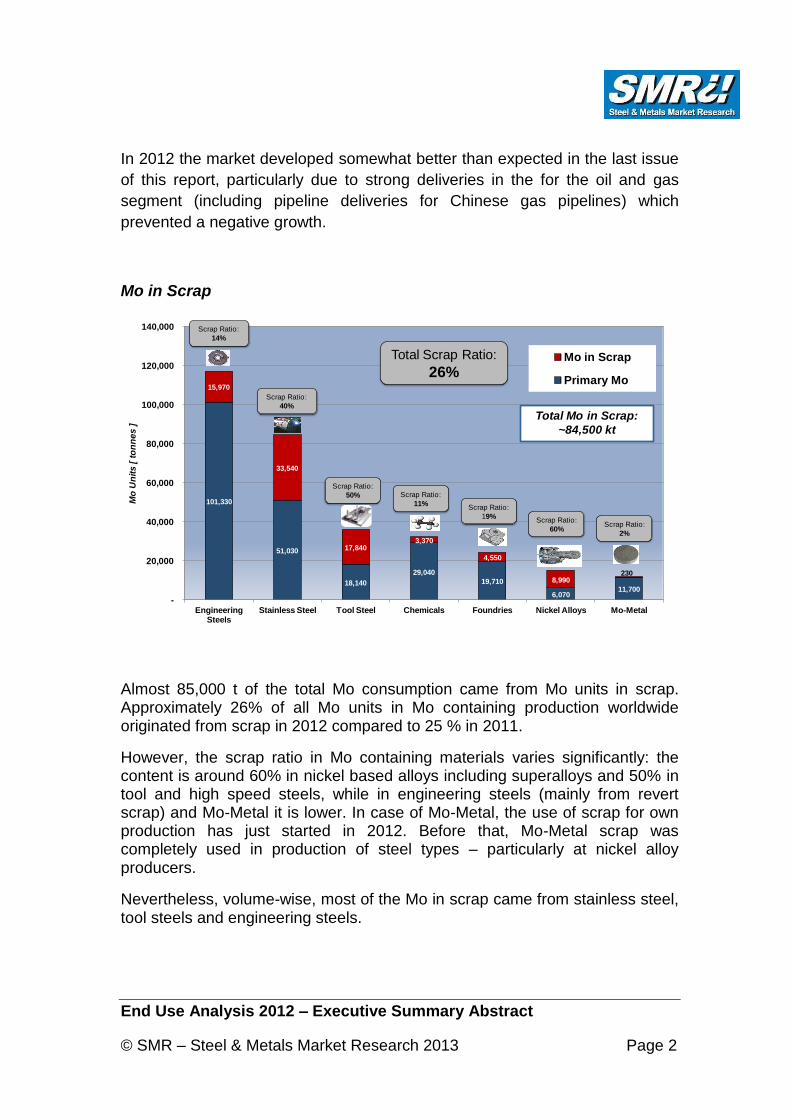

Mo in Scrap

101,330

51,030

18,140

29,040

19,710

6,07011,700

15,970

33,540

17,8403,370

4,550

8,990230

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Engineering Steels

Stainless Steel Tool Steel Chemicals Foundries Nickel Alloys Mo-Metal

Mo

Un

its

[ t

on

ne

s ]

Mo in Scrap

Primary Mo

Scrap Ratio:

14%

Scrap Ratio:

40%

Scrap Ratio:

50% Scrap Ratio:

11%Scrap Ratio:

19%Scrap Ratio:

60%

Total Scrap Ratio:

26%

Total Mo in Scrap:

~84,500 kt

Scrap Ratio:

2%

Almost 85,000 t of the total Mo consumption came from Mo units in scrap. Approximately 26% of all Mo units in Mo containing production worldwide originated from scrap in 2012 compared to 25 % in 2011.

However, the scrap ratio in Mo containing materials varies significantly: the content is around 60% in nickel based alloys including superalloys and 50% in tool and high speed steels, while in engineering steels (mainly from revert scrap) and Mo-Metal it is lower. In case of Mo-Metal, the use of scrap for own production has just started in 2012. Before that, Mo-Metal scrap was completely used in production of steel types – particularly at nickel alloy producers.

Nevertheless, volume-wise, most of the Mo in scrap came from stainless steel, tool steels and engineering steels.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 3

Primary Molybdenum (excl. Mo in Scrap)

Engineering Steels43%

Stainless Steels22%

Chemicals12%

Foundries8%

Tool Steels8%

Mo-Metal5%

Super Alloys3%

Total First Use

237,000 t

Excluding the Mo in scrap, the demand in 2012 remained relatively stable at

237,000 t. Construction engineering steels accounted for 43% of Mo use,

followed by stainless steel (22%) and chemicals (12%).

Compared to the Mo consumption including Mo from scrap, there are quite

substantial differences: engineering steels have a higher share in primary Mo

use than in Mo including scrap, due to the low portion of Mo coming from

scrap. In case of stainless steel, it is the opposite: mills are looking for high Mo

scrap ratios. Thus, the level of primary Mo use in stainless steel is lower than

the total Mo use including scrap (22 % compared to 26 % share in total use).

Mo first use in engineering steels grew by 3% in 2012, while the rest of the

segments remained stagnant (stainless steel) or even declined (all others).

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 4

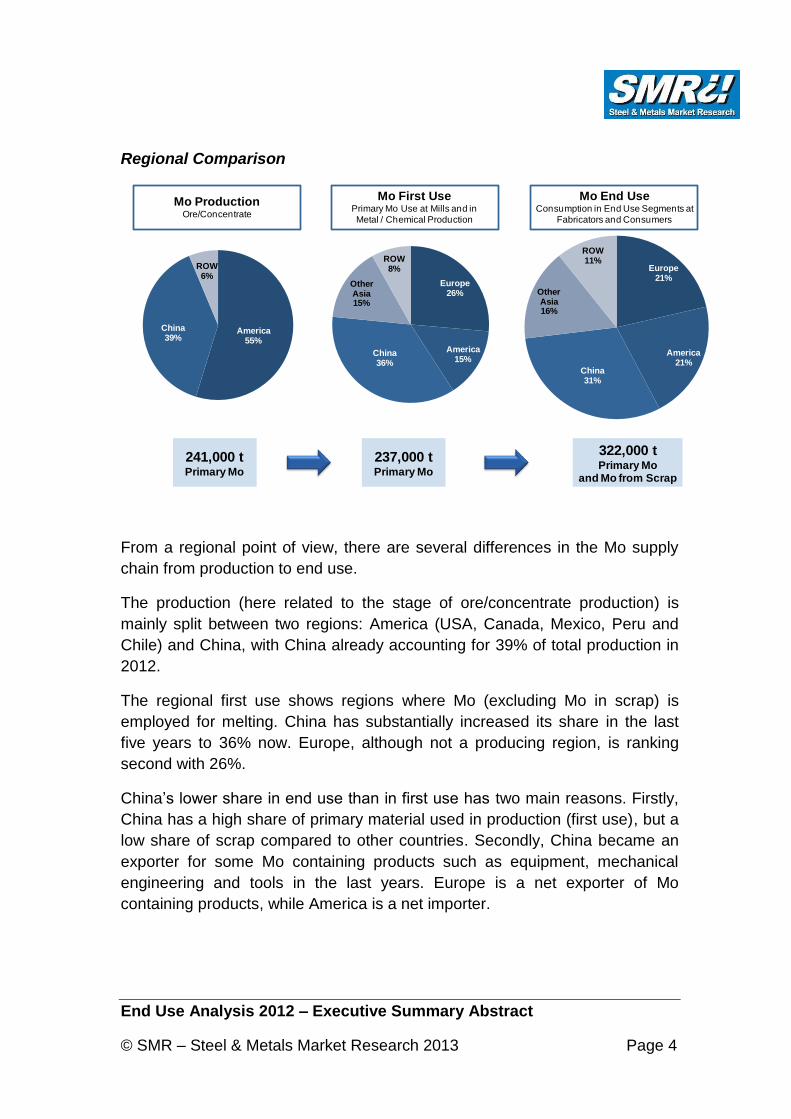

Regional Comparison

America55%

China39%

ROW6%

Europe26%

America15%

China36%

Other Asia15%

ROW8% Europe

21%

America21%

China31%

Other Asia16%

ROW11%

Mo ProductionOre/Concentrate

241,000 tPrimary Mo

Mo First UsePrimary Mo Use at Mills and in

Metal / Chemical Production

237,000 tPrimary Mo

Mo End UseConsumption in End Use Segments at

Fabricators and Consumers

322,000 tPrimary Mo

and Mo from Scrap

From a regional point of view, there are several differences in the Mo supply

chain from production to end use.

The production (here related to the stage of ore/concentrate production) is

mainly split between two regions: America (USA, Canada, Mexico, Peru and

Chile) and China, with China already accounting for 39% of total production in

2012.

The regional first use shows regions where Mo (excluding Mo in scrap) is

employed for melting. China has substantially increased its share in the last

five years to 36% now. Europe, although not a producing region, is ranking

second with 26%.

China’s lower share in end use than in first use has two main reasons. Firstly,

China has a high share of primary material used in production (first use), but a

low share of scrap compared to other countries. Secondly, China became an

exporter for some Mo containing products such as equipment, mechanical

engineering and tools in the last years. Europe is a net exporter of Mo

containing products, while America is a net importer.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 5

Enduse Structure

The chart below shows the end use industries for Mo containing steels, alloys and chemicals.

Oil and Gas (incl. Catalysts,

Ref inery)

20%

Chemical/Petrochemical14%

Automotive13%

Mechanical Engineering

13%

Process Industry (excl. CPI)8%

Other Transportation8%

Power Generation7%

Building / Construction

6%

Aerospace & Defence4%

Electronics & Medical2%

Others* 5%

Total End Use

321,600 t

The five largest end use segments in 2012 were:

Oil and gas

Chemical / petrochemical

Automotive

Mechanical engineering

Process industry (excluding CPI)

Compared to the last issue, the volume assigned to the oil and gas segment is

substantially larger now, which is, however, not only caused by a stronger

market. A major take-away from SMI’s report on CRAs in oil & gas was that

some sub-segments have been under-estimated in the previous report

(particularly the demand for OCTG). On the other hand, CPI was most likely

over-estimated in the previous reports. Thus, the quantities for Mo in stainless

and engineering steel have been re-adjusted accordingly in this issue.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 6

The oil and gas market including refineries and refinery catalysts was the

largest segment with a share of 20% in all Mo end uses. Total demand in oil

and gas has reached almost 64,000 t last year. Major applications were:

OCTG products especially alloy engineering steels (16,600 t), refinery

catalysts (18,200 t), flowlines including gas pipelines (9,500 t) and topside

processing equipment (8,100 t).

Chemical process industry (CPI) including petrochemical equipment is again

ranking second with around 14% of all end uses (~45,200 t). Stainless steel

applications (such as 316, Duplex and 6-Mo grades) are dominant in this

segment with a tonnage of ~30,000 t. The main products are pipes and tubes

as well as tanks, columns, vessels and similar equipment.

Automotive is the third largest sector with 13% share (43,000 t), defending its

position despite a falling Mo use in the European market. The main passenger

car applications for Mo are power train applications (12,400 t) including clutch,

gear and tools, followed by engine and exhaust parts (9,400 t) including

crankshafts, piston rods and exhaust systems. Chassis parts and transport

containers are the most important elements in trucks and buses.

In the field of mechanical engineering, Mo use reached ~41,500 t. Mo

containing alloy steel is used primarily in heavy machinery, printing, wood

working, recycling, milling and for bearings, while alloy tools steels are used for

tools and moulds.

All other segments account individually for less than 10%: process industry

(excluding CPI), other transportation (shipbuilding, railway, offshore vehicles

and cranes), power generation (fossil power, nuclear, wind energy, other

renewable), architecture, building and construction, aerospace and defense,

consumer goods, electronics and medical (with a high Mo-Metal share).

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 7

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

ChemicalsCast IronMo-MetalATS / HSSSuper AlloysStainless SteelConstructional Eng. Steel

Mo

Use

in t

* incl. Pigments, Coatings and Lubricants

Total End Use

321,600 t

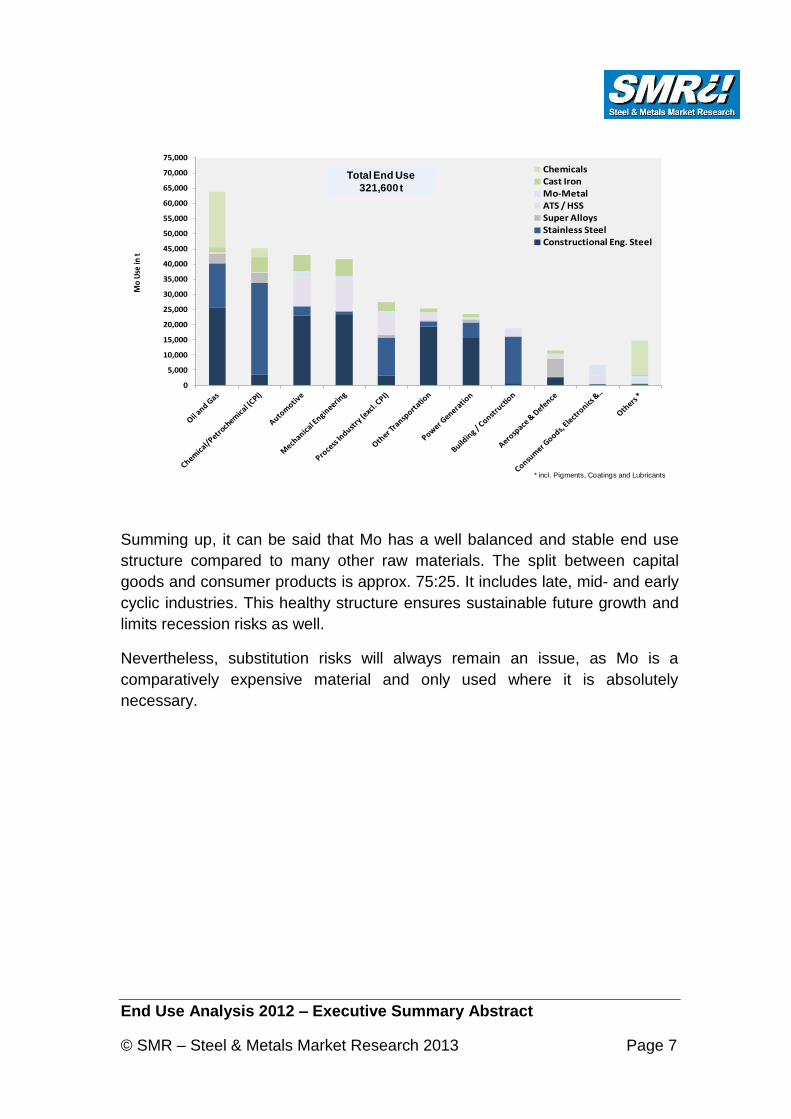

Summing up, it can be said that Mo has a well balanced and stable end use

structure compared to many other raw materials. The split between capital

goods and consumer products is approx. 75:25. It includes late, mid- and early

cyclic industries. This healthy structure ensures sustainable future growth and

limits recession risks as well.

Nevertheless, substitution risks will always remain an issue, as Mo is a

comparatively expensive material and only used where it is absolutely

necessary.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 8

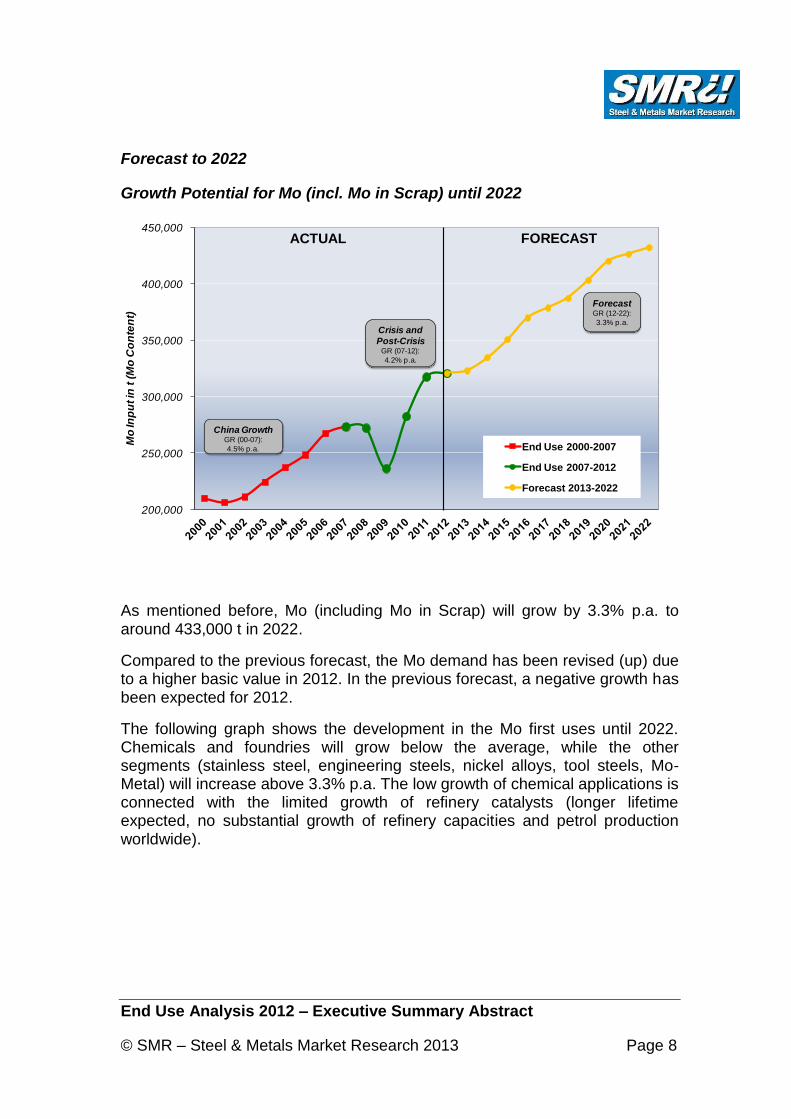

Forecast to 2022

Growth Potential for Mo (incl. Mo in Scrap) until 2022

200,000

250,000

300,000

350,000

400,000

450,000

Mo

Inp

ut in

t (

Mo

Co

nte

nt)

End Use 2000-2007

End Use 2007-2012

Forecast 2013-2022

ACTUAL FORECAST

Crisis and

Post-CrisisGR (07-12):

4.2% p.a.

China GrowthGR (00-07):

4.5% p.a.

ForecastGR (12-22):

3.3% p.a.

As mentioned before, Mo (including Mo in Scrap) will grow by 3.3% p.a. to around 433,000 t in 2022.

Compared to the previous forecast, the Mo demand has been revised (up) due to a higher basic value in 2012. In the previous forecast, a negative growth has been expected for 2012.

The following graph shows the development in the Mo first uses until 2022. Chemicals and foundries will grow below the average, while the other segments (stainless steel, engineering steels, nickel alloys, tool steels, Mo-Metal) will increase above 3.3% p.a. The low growth of chemical applications is connected with the limited growth of refinery catalysts (longer lifetime expected, no substantial growth of refinery capacities and petrol production worldwide).

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 9

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Mo-Metal Nickel AlloysFoundries Tool SteelChemicals Stainless SteelEngineering Steels

3,5 %

3,5 %

3,3 %

3,8 %

1,0%

3,5 %

4,5 %

GR in %

in m

etr

ic t

Average Growth: 3.3% p.a.

The following end use segments are expected to grow above the average by 2022:

Mechanical engineering

Other transportation

Consumer goods / electronics / medical equipment

Power generation

Process industry

Building/construction

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 10

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%G

row

th 2

012-2

022 in

%

Mo Use in t (2012)

Average Growth - All Segments

*) incl. Mo in Scrap

Oth

erT

ran

sp

ort

ati

on

Me

ch

an

ical E

ng

inee

rin

g

Po

we

r G

en

era

tio

n

Ae

ros

pac

e /

De

fen

se

Ch

em

ica

l / P

etr

oc

he

mic

al

Ind

us

try

Bu

ild

ing

& C

on

str

uc

tio

n

Co

ns

um

er G

oo

ds /

Me

d. /

Ele

ctr

.

Pro

ce

ss In

du

str

y

Au

tom

oti

ve

Oth

ers

O/G

:

Exp

lora

tio

n/ P

rod

./ P

rocessin

g

O/G

:Refi

nery

/

Cata

lysts

Total

Oil & Gas

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 11

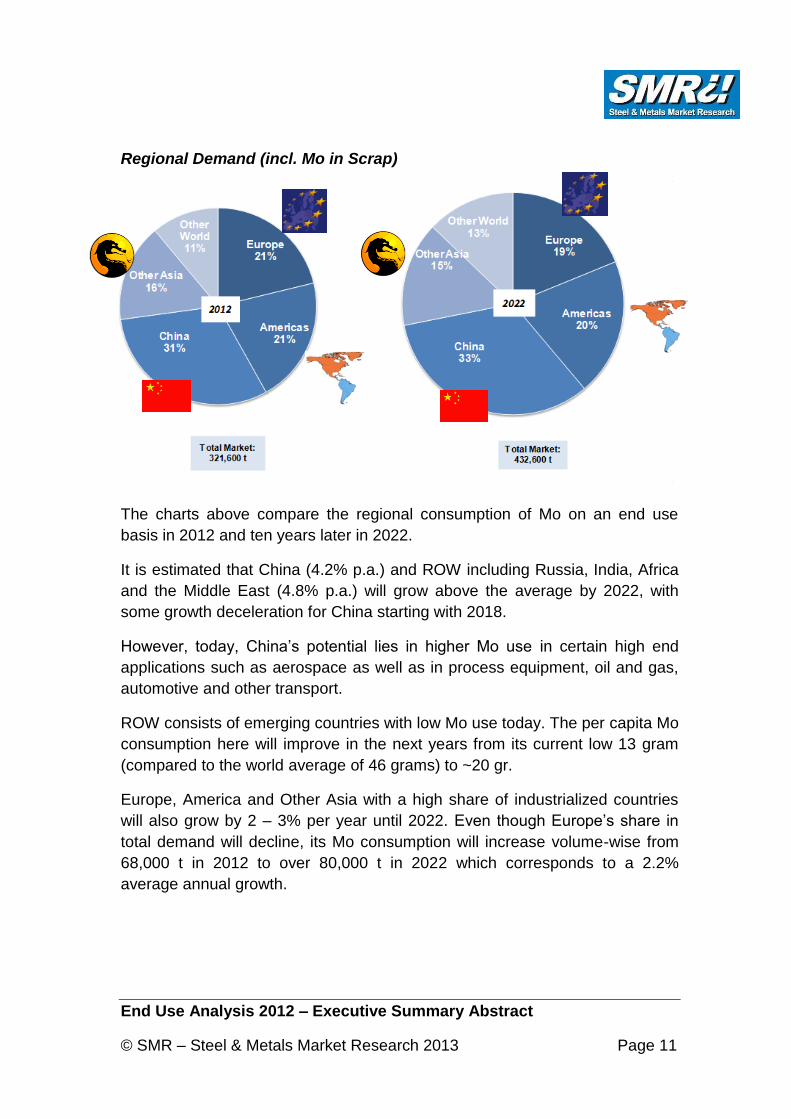

Regional Demand (incl. Mo in Scrap)

The charts above compare the regional consumption of Mo on an end use

basis in 2012 and ten years later in 2022.

It is estimated that China (4.2% p.a.) and ROW including Russia, India, Africa

and the Middle East (4.8% p.a.) will grow above the average by 2022, with

some growth deceleration for China starting with 2018.

However, today, China’s potential lies in higher Mo use in certain high end

applications such as aerospace as well as in process equipment, oil and gas,

automotive and other transport.

ROW consists of emerging countries with low Mo use today. The per capita Mo

consumption here will improve in the next years from its current low 13 gram

(compared to the world average of 46 grams) to ~20 gr.

Europe, America and Other Asia with a high share of industrialized countries

will also grow by 2 – 3% per year until 2022. Even though Europe’s share in

total demand will decline, its Mo consumption will increase volume-wise from

68,000 t in 2012 to over 80,000 t in 2022 which corresponds to a 2.2%

average annual growth.

End Use Analysis 2012 – Executive Summary Abstract

© SMR – Steel & Metals Market Research 2013 Page 12

Additional Mo Units Used by 2022

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

China Americas Other World Other Asia Europe

Mo

Un

its

in t

Incl. Mo in Scrap

2022 vs. 2012

+44%

+28%

+56%

+19%

+30%

ROW

WORLD

+ 111 kt

+ 35%

The graph above shows the increase in Mo consumption by region over a 10-year period and can be less misleading than the average annual growth rate figures.

Even Europe, which has a low average annual growth rate, is expected to consume 20% more Mo (or almost 15,000 t) than in 2012. Other regions will increase by 30 to 60% by 2012, with China being the clear leader. Its extra-volume will amount to over 40,000 t which is 44 % more than its consumption in 2012.