= total long term load/shareholders’ fund = shareholders ... vi - ar 7615 - sapm.pdf · iv....

TRANSCRIPT

Model Answer / Suggested Solution

Code AR 7615 Subject: Security Analysis and Portfolio Management

Q.1. Short Answered Questions

i. The deviation from the Arithmetic Mean from the following figures through

graphic presentation:

45, 44, 40, 45, 50, 35, 30, 42, 43 and 46

Average of given numbers=420/10=42

ii. Debt-Equity Ratio = total long term load/shareholders’ fund

=25,000/(60,000+20,000+10,000)

=25,000/90,000 = 1:3.6

Proprietary Ratio = Shareholders’ fund/total assets

= 90,000/1,50,000 = 1:1.67

iii. When a person invests his funds for the acquisition of some financial assets like

shares, debentures, insurance policies, mutual fund units etc, such investments

are known as financial investments.

When a person invests his funds for the acquisition of some physical assets, say

a building or equipment, such types of investments are called economic

investments. Economic investment can be defined as the investment that

contributes to the net additions to the capital stock of society.

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10

Arithmatic Mean

Actual Value

iv. Components of risks:

For the purpose of better analysis and understanding, the total risks in an

investment can be split into two types, viz. systematic and unsystematic risk.

Total risk = Systematic risk + Unsystematic risk

Systematic risk is that risk that is caused by caused by system-wide factors.

Changes in economic conditions, changes in political system, changes in social

system etc., are some factors that affect the entire community. These are called

system-wide factors.

Systematic risk can be divided into the following three sub heads:

Market risk, Interest rate risk and Purchasing power risks

Unsystematic risk is caused by factors specific to the company issuing securities.

In other words, unsystematic risk is caused by ‘firm-specific’ factors.

Unsystematic risk is unique to companies to companies and differs from one

company to another.

The unsystematic risk, which is caused due to firm-specific factors, can be

classified into two types, viz. Business risk and Financial risk.

v. Porter Model:

Michael Porter identified the following five factors as the essential factors

required for the sustenance of an industry. He puts forth that profit required for

the sustenance of an industry. He puts forth that the profit potential of an

industry depends on the combined strength of these five factors.

a. Threat of new entrant

b. Rivalry among the existing firms

c. Pressure from substitute products

d. Bargaining power of buyers

e. Bargaining power of suppliers

vi. Leverage Ratios: Leverage ratios represent the nature of capital structure of a

company. Leverage ratios indicate the long term solvency of a company, i.e.,

the ability of the company to service long-term debts.

The following are some of the Leverage Ratios:

Debt Equity Ratio

Total Debt to Total Assets Ratio

Proprietary Ratio

Interest Coverage Ratio

vii. DOW Theory: According to Dow Theory the prices of securities in the stock

market do not move at random, but more in cyclical pattern influenced by three

distinct cyclical trends. DOW observed that the price of most stocks move in

accordance with the movement of the market. When the market goes up, the

price of most stocks also go up and vice-versa. Hence, before attempting to

predict the price movement of a particular security, the behavior of the market

Substitute

products

Buyers

Rivalry

among

existing firms

in an industry Suppliers

Bargaining

power of

suppliers

New Entrants

Threat from

new entrants

Bargaining

power of

buyers

Pressure from

substitute products

Figure: Porter Model

as a whole is to be studied and understood. Dow theorized that the trend of

overall stock prices could be determined by studying the price movements of a

selected group of stocks. To understand the behavior of the market, Dow

constructed two indices calling them as Industrial Average and Rail Average.

The industrial average is known by the name DOW-Jones Industrial Average

(DJIA).

The DJIA is a price-weighted average of 30 large, well-known industrial stocks

that are generally the leaders in their industry and are listed on the New York

Stock Exchange. By the time the index was built by Charles H. DOW there

were 15 stocks included in the index which was later expanded to 30.

The Rail Average was built with 12 rail road stocks. The Rail Average was

intended to serve as a representative index for transportation stocks. With the

evolution of joint stock companies of other modes of transportation, the Rail

Average was latter modified as the Transportation Average incorporating

addition of stocks of transportation companies of other modes than Rail road

mode and the index later came to be known as DOW-Jones Transportation

Average (DJTA).

viii. Triangle:

The wedge is formed after the arrival of some information about the scrip in

the market. The commencement of wedge formation means that the market has

started to react on the basis of information received. However, to start with,

there used to be greater uncertainty about the validity as well as the influence of

the information on the performance of the company. As the time progresses, the

information received and its impact are better assimilated by the market and the

uncertainty gradually gets reduced. This is reflected in the formatting triangle

from wedge. Finally when the uncertainty is resolved, the resistance and support

boundaries intersect. Following figures show the formation of a triangle pattern

from a wedge pattern.

Pri

ce

Time

Pri

ce

Time

Pri

ce

Time

Pri

ce

Time

Pri

ce

Time

Pri

ce

Time

ix. Semi Strong form Efficiency:

Semi strong form of the efficiency market hypothesis holds that the current stock

prices not only reflect all known information with regard to past stock prices

and their movements but also reflect all publicity available information about

the company, whose stocks are being studied.

The following are some of the publicly available information:

Latest corporate annual reports.

Expectations regarding future annual reports with regard to changes in sales,

earnings, dividends, capital structure etc.

Company announcements of forthcoming dividends, stock splits etc.

Press releases

Charges in Government policies that will affect/improve the prospects of the

company.

x. Optimal Portfolio: All the portfolios that lie on the efficient frontier are efficient

portfolios and rational investors opt to invest only in such efficient portfolios.

The particular portfolio that an investor will select from among the efficient

portfolios depends upon the degree of risk that investor prefers to bear. An

investor who is highly averse to risk may prefer the global minimum variance

portfolio. An investor who is prepared to take the maximum risk will prefer to

choose the portfolio represented by the top most point in the Efficient Frontier

curve. Investors who opt for moderate risk will choose any portfolio that lie on

the Efficient Frontier between the starting and end point of the effective frontier,

depending on their risk bearing capacity.

Q.2. Investment Avenues:

There are many investment avenues available for investors. The investment

avenues differ in their risk-return characteristics. The investment avenues with higher

level of risk offer higher returns while the avenues with minimum level of risk offer

lower return. There is nothing such as a bad investment. A good investment can

become a bad if not handled properly. The term good and bad for investments is

relative to the investor and his expectation for returns. Everyone would like to earn a

fortune out of their investments but it is impossible to do so without facing risk; risk

of losing one's hard earned money. Investments are made to meet specific financial

goals and one wrong step could take one’s plan back over years.

Modern investment theory states that - 'High risk, High returns; Low risk, low

returns'. This gives the possibility of high returns on high risk, not the guarantee of

high returns as there are chances of high potential losses also. Hence, before investing

a person needs have to be certain about his risk bearing capacity and various

investment options to suit his financial condition, risk tolerance, life situation and

financial goals. It is important to balance the risk and return while investing to

achieve a trade off. If a person’s investments are giving him too much anxiety, it

cannot be termed as a balanced investment. Risks cannot be totally isolated from

investments, but the amount of risk associated with a particular investment should be

acceptable. Acceptable risk means managing and controlling risk and returns so that

the returns are maximized and risk minimized.

One of the basic rules of investing is to make diversified investments. This is the

best method to spread the risk across various investments instead of concentrating it at

a single place. Sometimes, losses in a particular investment are offset against the

profits from other investments in a diversified portfolio. Diversification of

investments means investing in different high risk as well as risk free instruments to

reduce the inherent risk in a particular investment. The proportion of investment in

different risk bearing securities depends on the risk tolerance of a person. A young

earning individual can put more in risky instruments while an old age person can keep

more amounts in fixed income securities. There is no thumb rule that specifies the

percentages of investments in different securities; it is relative to the person investing.

There are a variety of financial and non financial instruments to choose from for

investing. On the basis of risk involved these can be classified as -

The major investment avenues available for investment can be broadly classified into

two categories as below:

Ownership Securities

Creditorship Securities

Ownership Securities:

Ownership securities are of two types, viz.

Equity Shares

Preference Shares

(Students are supposed to discuss these points with their advantages and disadvantages)

Creditorship Securities:

While ownership securities represent the equity capital, creditorship securities represent

the debt capital of company. Debentures and Bonds are the creditorship securities.

Debentures

Bonds

(Students are supposed to discuss these points with their advantages and disadvantages)

Q.3. Economy Analysis

Return assumptions for the stock and bond markets and sales, cost, and profit

projections for industries and nearly all companies necessarily embody economic

assumptions. Investors are concerned with those forces in the economy which affect

the performance of organization in which they wish to participate, through purchase

of stock. By identifying key assumptions and variables, we can monitor the economy

and gauge the implications of new information on our economic outlook and industry

analysis. In order to beat the market on a risk adjusted basis, the investor must have

forecasts that differ from the market consensus and must be correct more often than

not.

Economic trends can take two basic forms: cyclical changes that arise from ups

and downs of the business cycle, and structural changes that occur when the economy

is undergoing a major change in how it functions. Some of the broad forces which

impact the economy are:

a. Agriculture

b. Population

c. Interest rate

d. Natural resources

e. Government policies/ Government spending, revenues

f. Foreign trade, balance of payments and exchange rate

g. Inflation

h. National income

i. Demographic factors

j. Stability of government

k. Level of savings

l. Infrastructural facilities

m. Research and development activities.

(Students are supposed to discuss these points briefly)

Q.4. Limitations of Markowitz Model:

The analysis as done by Markowitz require a large number of data

inputs and involve lengthily / complex computations. The complexity

increases as the number of available securities increases. If there are ‘N’

securities available for investment, the data inputs required for analyzing the

risk-return relationship of the portfolio containing the ‘N’ securities are as

under:

No. of return estimates from securities = N

No. of variance estimates from securities = N

No. of covariance estimates from securities = N (N -1)/2

Hence,

Total no. of data inputs = 2N + N(N-1)/2

Suppose 50 securities are available for investment. The number of data

inputs required is 122500. Thus, the identification of efficient portfolios on the

basis of Markowitz’s model has found little use in practical applications only

if the data inputs required are considerably reduced and the process of

calculation is simplified. In this regard, William Sharp developed a simplified

variant of the Markowitz model.

Sharp Single Index Model:

William Sharp developed a simplified variant of the Markowitz model.

This model reduces the data inputs and computational requirements

considerably and thus overcome the practical difficulties encountered by

average investors in the application of Markowitz model.

Sharp single index model has its name because it relies on a single

index that represents the security market. Instead of comparing each security

with every other available security, each security is compared only with the

market index. In other words, the return from each security is compared only

with the market return. The market index may be any widely accepted index

like the BSE index in India. Sharpe suggested that the relationship of each

security with the market index gives reasonably accurate information about

that security and that it is needless to study the relationship of each security

with every other security.

Sharpe gave the following relationship for arriving at the expected return from

a security.

Ri = i + i Rm + ei

Where

Ri = expected return of security ‘i'

i = component of return from security ‘I’ that is independent of the

performance of the market (Alpha coefficient of security)

i = a constant that measure the expected change in Ri for a given change in

Rm(Beta coefficient of security)

Rm= rate of return on the market index

ei = error term representing the residual return

According to Sharpe, fluctuation in the value of a stock relative to the value of

another stock depends on the correlation between each security return with a

security market index.

The error term ‘ei' is the unexpected return resulting from influences not

identified by the model. Sharpe observed that in the long run (i.e., when more

and more number of securities are analysed) the value of ‘ei’ terms out to be

zero. In other words + ei and - ei cancel out and hence the formula can be

simplified as,

Ri = i + i Rm

i.e.,

Return from a security = ‘’ of the security + [‘’ of the security x market

return]

Q.5. TECHNICAL ANALYSIS

Technical analysis has an important bearing on the study of price behavior and

has its own method in predicating significant price behavior.

Technical analysis is probably the most controversial aspect of investment

management. That technical analysis is a delusion, that it can never be more

useful in predicating stock performance than examining the insides of a dead

sheep, in the ancient Greek traditions. Technical analysis involves a study of

market generated data like prices and volumes to determine the future direction of

price movement. Martin J. Pring explains as “The technical approach to investing

is essentially a reflection of the idea that prices move in trends which are

determined by the changing attitudes of investors toward a variety of economic,

monetary, political and psychological forces. The art of technical analysis-for it is

an art-is to identify trend changes at an early stage and to maintain an investment

posture until the weight of the evidence indicates that the trend has been reversed.

Limitations of Technical Analysis:

The arguments against the technical analysis are,

i. Most technical analysts are not able to offer convincing explanations for the tools

employed by them.

ii. Empirical evidence in support of the random-walk hypothesis casts its shadow over

the usefulness of technical analysis.

iii. By the time an uptrend or downtrend may have been signaled by technical analysis, it

may already have taken place.

iv. Ultimately, technical analysis must be self-defeating proposition. As more and more

people employ it, the value of such analysis tends to decline.

v. The numerous claims that have been made for different chart patterns are simply

untested assertions.

vi. There is a great deal of ambiguity in the identification of configurations as well as

trend lines and channels on the charts. The same chart can be interpreted differently.

Differences between Technical Analysis and Fundamental Analysis

The key differences between technical analysis and fundamental analysis are as

follows:

i. Technical analysis mainly seeks to predict short –term price movements, whereas

fundamental analysis tries to establish long term values.

ii. The focus of technical analysis is mainly on internal market data, particularly price

and volume data. The focus of fundamental analysis is on fundamental factors relating

to the economy, the industry, and the firm.

iii. Technical analysis appeals mostly to short-term traders, whereas fundamental analysis

appeals primarily to long-term investors.

(These points are expected from the students; change in description may be accepted)

Q.6. Markowitz efficient frontier:

The efficient frontier is a concept in modern portfolio theory introduced by Harry

Markowitz and others. A combination of assets, i.e. a portfolio, is referred to as

"efficient" if it has the best possible expected level of return for its level of risk

(usually proxied by the standard deviation of the portfolio's return). Here, every

possible combination of risky assets, without including any holdings of the risk-free

asset, can be plotted in risk-expected return space, and the collection of all such

possible portfolios defines a region in this space. The upward-sloped (positively-

sloped) part of the left boundary of this region, a hyperbola, is then called the

"efficient frontier". The efficient frontier is then the portion of the opportunity set that

offers the highest expected return for a given level of risk, and lies at the top of the

opportunity set or the feasible set. For further detail see modern portfolio theory.

Dominance of Efficient frontier:

If we draw Loci of all possible combinations of a portfolio starting from two

securities to ‘n’ securities, the number of curves will be too many with the result we

will get an entire region as a feasible region for investment.

The many points in the feasible region represent the feasible set of portfolios in which

an investor can possibly invest. This set of feasible portfolios is called the portfolio

opportunity set.

It may be noted that if there are ‘n’ securities available in the market for investment, it

is not necessary (and not practical) for an investor to invest in all the ‘n’ securities. He

may choose a handful of securities that are acceptable to him and construct a

portfolio. However, the extreme situation of choosing all the ‘n’ securities can also be

not ruled out, since this is also a feasible portfolio theoretically. Thus, the portfolio set

will consist of all feasible combination of the available security. Every point in the

feasible region corresponds to a particular portfolio (containing a few securities) that

has its own risk-return characteristics. Looking at the feasible region we find that the

locus EF (which is called the Efficient Frontier) dominates all the other portfolios in

the regions.

Q.7. Security – A

(xi) P(xi) xi p(xi) Expected

return ̅

x - ̅ (x - ̅)2

p(xi).(x - ̅)2

15 0.50 7.50 }

16.80

- 1.80 3.24 1.620

17 0.20 3.40 0.20 0.04 0.008

19 0.10 1.90 2.20 4.84 0.484

20 0.20 4.00 3.20 10.24 2.048

∑

16.80 2 4.160

Expected return = 16.80%

Variance of the expected return ( 2) = 4.16

Standard deviations of the expected = √

= 2.04

Security – B

(xi) P(xi) xi p(xi) Expected

return ̅

x - ̅ (x - ̅)2

p(xi).(x - ̅)2

15 0.60 7.20 }

16.80

- 4.80 23.04 13.824

17 0.20 4.00 3.20 10.24 2.048

19 0.10 2.20 5.20 27.04 2.704

20 0.20 3.40 17.20 295.84 29.584

∑

16.80 2 48.160

Expected return = 16.80%

Variance of the expected return ( 2) = 48.16

Standard deviations of the expected = √

= 6.94

Though the expected return from the two securities is the same, the Standard

Deviations of the return from security B is higher than that of security A. Hence security ‘A’

shows lesser risk.

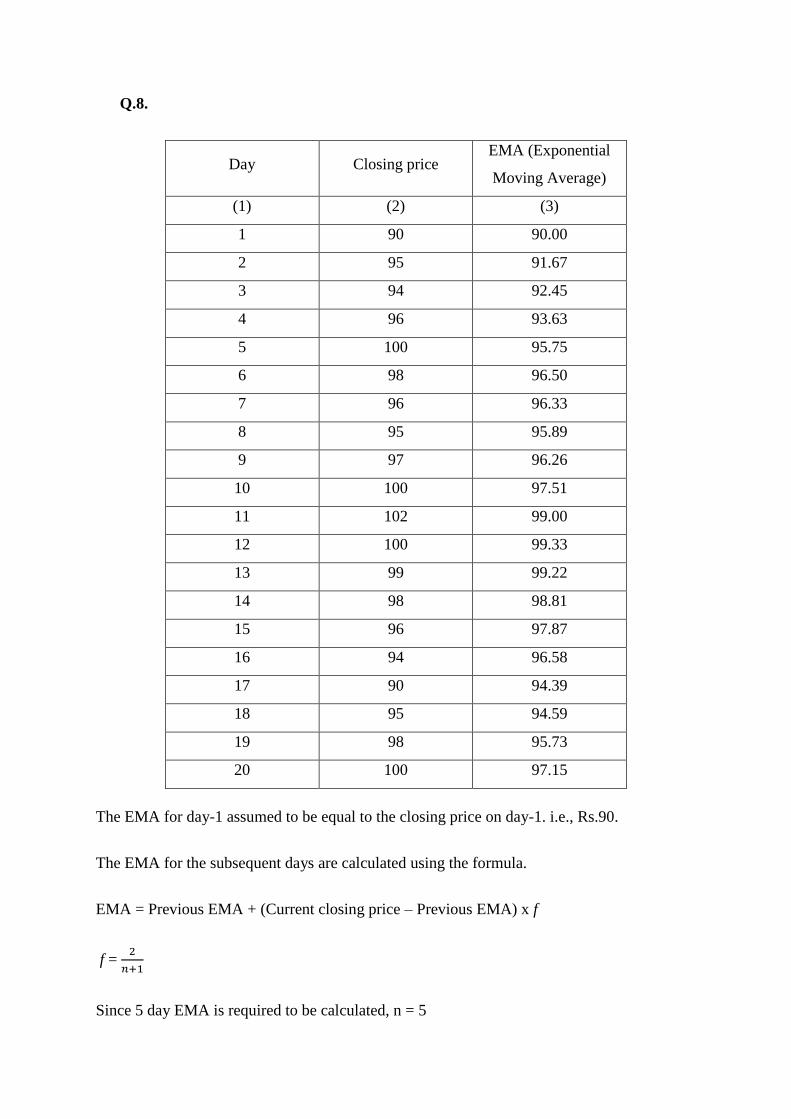

Q.8.

Day Closing price EMA (Exponential

Moving Average)

(1) (2) (3)

1 90 90.00

2 95 91.67

3 94 92.45

4 96 93.63

5 100 95.75

6 98 96.50

7 96 96.33

8 95 95.89

9 97 96.26

10 100 97.51

11 102 99.00

12 100 99.33

13 99 99.22

14 98 98.81

15 96 97.87

16 94 96.58

17 90 94.39

18 95 94.59

19 98 95.73

20 100 97.15

The EMA for day-1 assumed to be equal to the closing price on day-1. i.e., Rs.90.

The EMA for the subsequent days are calculated using the formula.

EMA = Previous EMA + (Current closing price – Previous EMA) x f

f =

Since 5 day EMA is required to be calculated, n = 5

f =

= 0.333

EMA (for day 2) = 90 + (95-90) x 0.333 = 91.67

EMA (for day 2) = 90 + (95-90) x 0.333 = 92.45

EMA (for day 2) = 90 + (95-90) x 0.333 = 93.63

………………………………………………….. and so on.

The EMA for all the other days have been calculated and entered in the table.

Prepared By:

Dr. Shishir Pandey

Assistant Professor

Department of Commerce

Guru Ghasidas

Vishwavidyalaya, Bilaspur, C.G.