1 1 introduction to accounting and business. 2 service business service service business service the...

TRANSCRIPT

1

1Introduction to Introduction to

Accounting Accounting and Businessand Business

2

ServiceService BusinessBusiness ServiceService ServiceService BusinessBusiness ServiceService

The Walt Disney Company EntertainmentDelta Air Lines TransportationMarriott International Hotels Hospitality and

lodgingBank of America Corporation Financial servicesXM Satellite Radio Satellite radio

The Walt Disney Company EntertainmentDelta Air Lines TransportationMarriott International Hotels Hospitality and

lodgingBank of America Corporation Financial servicesXM Satellite Radio Satellite radio

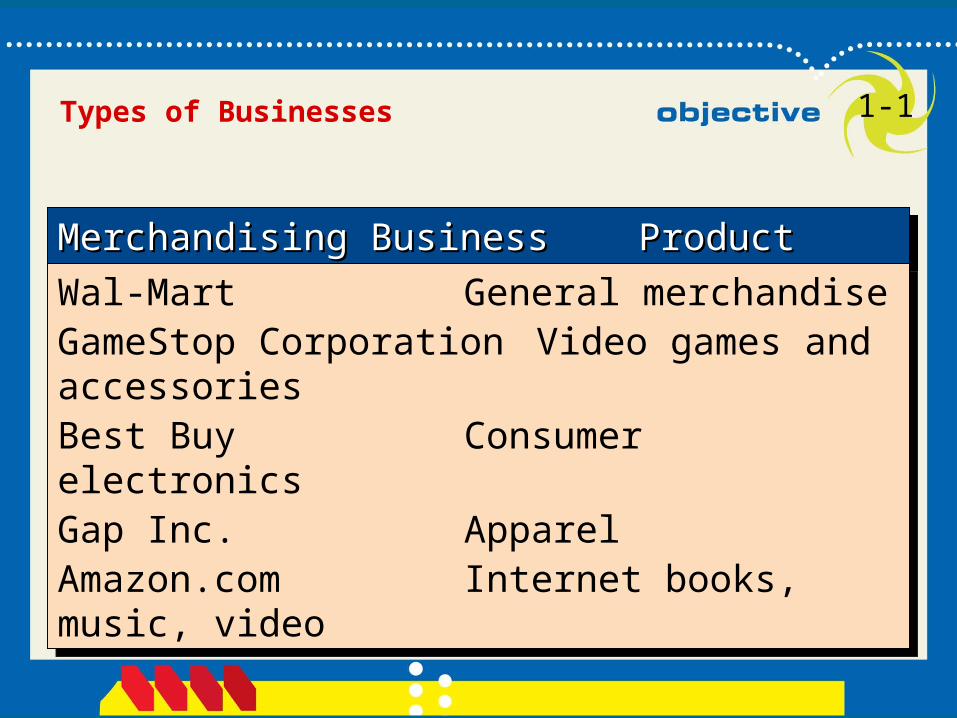

1-1Types of Businesses

3

Merchandising BusinessMerchandising Business ProductProductMerchandising BusinessMerchandising Business ProductProduct

Wal-Mart General merchandiseGameStop Corporation Video games and accessoriesBest Buy Consumer electronicsGap Inc. ApparelAmazon.com Internet books, music, video

Wal-Mart General merchandiseGameStop Corporation Video games and accessoriesBest Buy Consumer electronicsGap Inc. ApparelAmazon.com Internet books, music, video

Types of Businesses 1-1

4

Manufacturing BusinessManufacturing Business ProductProductManufacturing BusinessManufacturing Business ProductProduct

General Motors Corp. Cars, trucks, vansSamsung Cell phonesDell Inc. Personal computersNike Athletic shoes and apparelThe Coca-Cola Company BeveragesSony Corporation Stereos and televisions

General Motors Corp. Cars, trucks, vansSamsung Cell phonesDell Inc. Personal computersNike Athletic shoes and apparelThe Coca-Cola Company BeveragesSony Corporation Stereos and televisions

Types of Businesses 1-1

5

Proprietorship Partnership Corporation Limited liability company

Common Forms of Business Organizations 1-1

6

A business stakeholder is a person or entity having an interest in the economic

performance and well-being of a business.

1-1

7

Accounting can be defined as an information system that provides reports to stakeholders about the

economic activities and condition of a business.

1-1

8

The process by which accounting provides information to business stakeholders is as follows:

Identify stakeholders. Assess stakeholders’ information needs. Design the accounting information system to

meet stakeholders’ needs. Record economic data about business

activities and events. Prepare accounting reports for stakeholders.

1-1

923

1-1

10

Financial accounting is primarily concerned with the recording and reporting of economic

data and activities for a business.

Managerial accounting uses both financial accounting and estimated data to aid management in running day-to-day

operations and in planning future operations.

1-1

11

The The business entity concept limits the economic data in limits the economic data in the accounting system to the accounting system to

data related directly to the data related directly to the activities of the business.activities of the business.

1-2

12

The cost concept is the basis for entering the

exchange price, or cost of an acquisition in the

accounting records.

1-2

13

The objectivity concept requires that the accounting records and reports be based

upon objective evidence.

1-2

14

The unit of measure concept requires that

economic data be recorded in dollars.

1-2

15

Assets = Liabilities + Owner’s Equity

The resources owned by a

business

The Accounting Equation 1-3

16

The rights of the creditors, which represent debts of the business

Assets = Liabilities + Owner’s Equity

The Accounting Equation 1-3

17

The rights of the owners

Assets = Liabilities + Owner’s Equity

The Accounting Equation 1-3

18

A business transaction is an economic event or condition that

directly changes an entity’s financial condition or directly

affects its results of operations.

1-4

19

On November 1, 2007, Chris Clark begins a business that will

be known as NetSolutions.

1-4

20

a. Chris Clark deposits $25,000 in a bank account in the name of NetSolutions.

Chris Clark, Capital25,000 Investment

by Chris Clark

Cash25,000 a.

=

Assets Owner’s Equity=

40

1-4

21

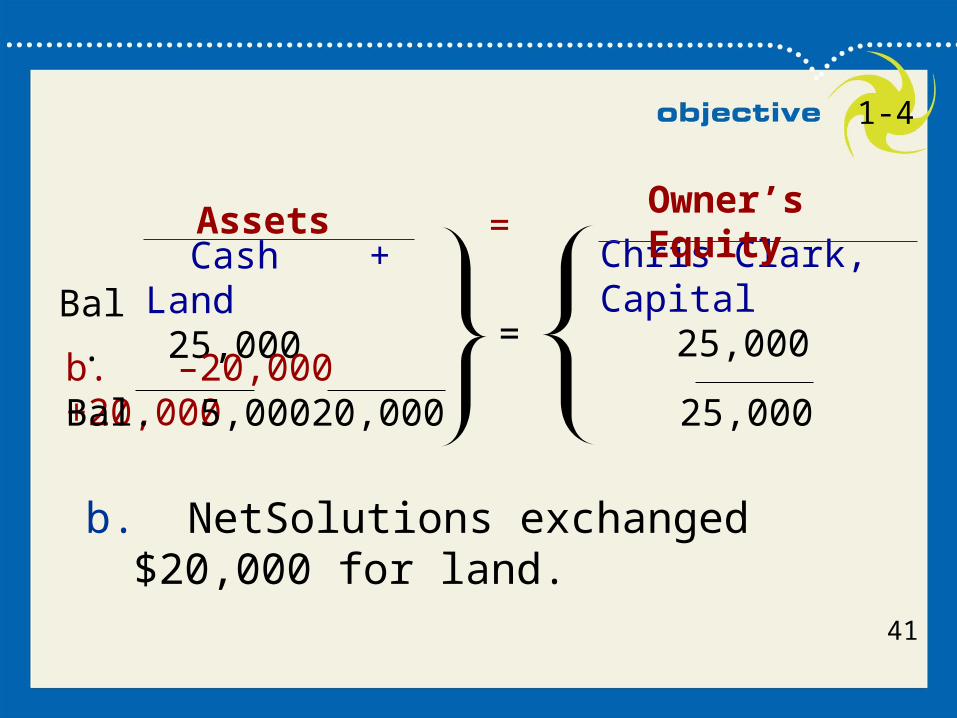

b. NetSolutions exchanged $20,000 for land.

Chris Clark, Capital25,000

Cash + Land 25,000 Bal.

Assets Owner’s Equity=

=b. –20,000 +20,000Bal. 5,000 20,000 25,000

41

1-4

22

Accounts Chris Clark, Cash + Supplies + Land Payable Capital

Assets

c. During the month, NetSolutions purchased supplies for $1,350 and agreed to pay the supplier in the near future (on account).

Owner’s Liabilities + Equity=

5,000 20,000 25,000=

+1,350 +1,350c.Bal.

5,000 1,350 20,000 1,350 25,000Bal.

42

1-4

23

Beginning with entry (d) the asset section will be shown first, then the liabilities and

owner’s equity will be shown in the following slide.

1-4

24

Cash + Supplies + Land

Assets

5,000 1,350 20,000

d. NetSolutions provided services to customers, earning fees of $7,500 and received the amount in cash.

Bal.

12,500 1,350 20,000+7,500d.

Bal.

44

1-4

25

d. NetSolutions provided services to customers, earning fees of $7,500 and received the amount in cash.

45

1-4

Liabilities + Owner’s Equity Accounts Chris Clark, Fees

Payable Capital + Earned 1,350 25,000 Bal.

+7,500 d.

+

25,000 7,500 Bal.1,350

26

1-4

The amounts used in earning revenue are called expenses. Adding expenses to the owner’s equity section results in a space

problem. To adjust for these added headings, the word “Bal.” has been omitted

from Slides 48, 50, 52, and 54. The bottom row in these four slides provides

the balances after each transaction.

Expenses

27

Cash + Supplies + Land

Assets

e. NetSolutions paid the following expenses: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

Bal. 12,500 1,350 20,000

Bal. 8,850 1,350 20,000 e. –3,650

47

1-4

28

Accounts Chris Clark, Fees Wages Rent Utilities Misc. Payable + Capital + Earned Expense Expense Expense Expense

Liabilities + Owner’s Equity

1,350 25,000 7,500

–2,125 –800 –450 –275 e.

1,350 25,000 7,500 –2,125 –800 –450 –275

48

e. NetSolutions paid the following expenses: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

1-4

29

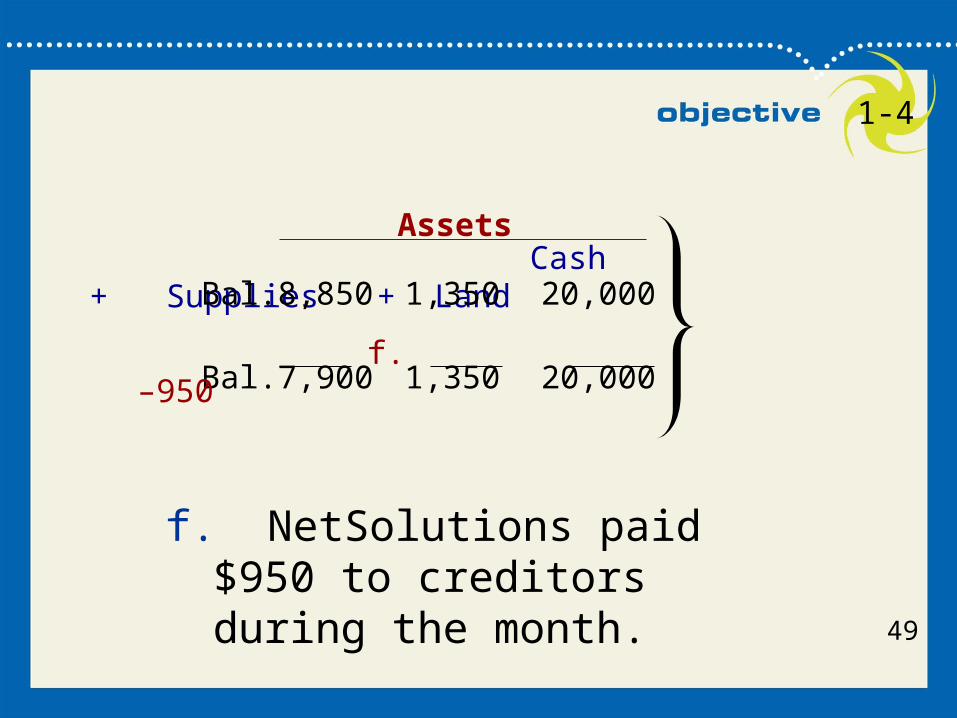

f. NetSolutions paid $950 to creditors during the month.

Cash + Supplies + Land

Assets

Bal. 8,850 1,350 20,000

Bal. 7,900 1,350 20,000 f. –950

49

1-4

30

Accounts Chris Clark, Fees Wages Rent Utilities Misc. Payable + Capital + Earned Expense Expense Expense Expense

Liabilities + Owner’s Equity

1,350 25,000 7,500 –2,125 –800 –450 –275

400 25,000 7,500 –2,125 –800 –450 –275

f. NetSolutions paid $950 to creditors during the month.

f.–950

50

1-4

31

g. At the end of the month, the cost of supplies on hand is $550, so $800 of supplies were used.

Cash + Supplies + Land

Assets

Bal. 7,900 1,350 20,000

Bal. 7,900 550 20,000 g. –800

51

1-4

32

Accounts Chris Clark, Fees Wages Rent Supplies Util. Misc. Payable + Capital + Earned Exp. Exp. Exp. Exp. Exp.

Liabilities + Owner’s Equity

400 25,000 7,500 –2,125 –800 –450 –275

g. At the end of the month, the cost of supplies on hand is $550, so $800 of supplies were used.

g. –800

400 25,000 7,500 –2,125 –800 –800 –450 –275

52

1-4

33

Cash + Supplies + Land

Assets

Bal. 7,900 550 20,000

Bal. 5,900 550 20,000 h. –2,000

h. At the end of the month, Chris withdrew $2,000 in cash from the business for personal use.

53

1-4

34

Accounts Chris Clark, Chris Clark Fees Wages Rent Supplies Util. Misc. Payable + Capital + Drawing Earned Exp. Exp. Exp. Exp. Exp.

Liabilities + Owner’s Equity

400 25,000 7,500 –2,125 –800 –800 –450 –275 h. –2,000

h. At the end of the month, Chris withdrew $2,000 in cash from the business for personal use.

400 25,000 –2,000 7,500 –2,125 –800 –800 –450 –275

54

1-4

35

Owner’s withdrawals

Expenses

Decreased byDecreased by

Owner’s Equity

Increased byIncreased by

Owner’s investments

Revenues

55

1-4

36

Accounting reports, called financial statements, provide summarized

information to the owner.

1-5

37

The income statement is a summary of the revenue

and expenses for a specific period of time,

such as a month or a year.

1-5

38

1-5

62

Net income is carried to the

statement of owner’s equity

Income Statement

39

A statement of owner’s equity is a summary of the changes

in the owner’s equity that have occurred during a specific

period of time.

1-5

4064

1-5

From the income statement

To the balance sheet

Statement of Owner’s Equity

41

A balance sheet is a list of the assets, liabilities, and

owner’s equity as of a specific date.

1-5

4266

1-5

This amount is compared to the net cash flow on the statement of cash flows

From the statement of owner’s equity

Balance Sheet

43

A statement of cash flows is a summary of the cash receipts and payments for a specific period of time.

1-5

4468

This amount should match Cash on the balance sheet.

Statement of Cash Flows 1-5

45

The income statement reports the revenues and expenses for a period of time based on the matching concept.

This concept is applied by matching the expenses with the revenue generated during a period by those expenses.

1-5Income Statement

46

The excess of revenue over the expenses is called net

income or net profit. If the expenses exceed the revenue,

the excess is a net loss.

1-5

47

The statement of owner’s equity reports the changes in

the owner’s equity for a period of time. It is prepared after the

income statement.

1-5Statement of Owner’s Equity

48

The balance sheet reports the amounts of a firm’s assets, liabilities, and

owner’s equity at the end of a specific period.

1-5Balance Sheet

49

The account form of balance sheet lists the assets on the left and the liabilities and owner’s equity on the right—similar to

design of an account.

1-5

50

The report form of balance sheet presents the liabilities and owner’s equity sections

below the assets section.

1-5

51

The statement of cash flows consists of three sections:

1-5

(1) Operating activities

(2) Investing activities

(3) Financing activities

Statement of Cash Flows

52

The cash flows from operating activities section reports a summary of cash receipts and cash payments

from operations.

1-5

53

The cash flows from investing activities section reports the cash

transactions for the acquisition and sale of relatively permanent assets.

1-5

54

The cash flows from financing activities section reports the

cash transactions related to cash investments by the owner,

borrowings, and cash withdrawals by the owner.

1-5

55

The income statement and the statement of owner’s equity are interrelated.

Net income or net loss appears on both statements.

1-5Interrelationships Among Financial Statements

56

The statement of owner’s equity and the balance sheet are interrelated.

The owner’s capital at the end of the period on the statement of owner’s equity also appears on the balance

sheet as owner’s capital.

1-5

57

The balance sheet and the statement of cash flows are interrelated.

The cash on the balance sheet also appears as the end-of-period cash on

the statement of cash flows.

1-5