1 chapter 14: income taxation of trusts & estates

TRANSCRIPT

1

Chapter 14:Income Taxation of

Trusts & Estates

2

INCOME TAXATION OF INCOME TAXATION OF TRUSTS & ESTATESTRUSTS & ESTATES (1 of (1 of

2)2)

Fiduciary taxationBasic concepts and definitionsTrust taxable incomeDistributable net income (DNI)Simple trusts

3

INCOME TAXATION OF INCOME TAXATION OF TRUSTS & ESTATESTRUSTS & ESTATES (2 of (2 of

2)2)

Complex trustsIncome in respect of a

decedentGrantor Trusts

4

Fiduciary TaxationFiduciary TaxationTrusts and estates are separate taxpayersNo double taxation

Deductions permitted for income distributed to beneficiaries

Distributed income from trust retains its character in hands of beneficiary

Limited personal exemption available and no dependency exemptions

5

Basic Concepts and Basic Concepts and DefinitionsDefinitions (1 of 5) (1 of 5)

Estate comes into existence upon death of person whose assets are being administered

Trust is a legal entity created while a person is alive or under direction of a will following a person’s death

Testamentary trust receives assets from estate of decedent

6

Basic Concepts and Basic Concepts and DefinitionsDefinitions (2 of 5) (2 of 5)

Principal or corpusInitial assets transferred by grantor plus

certain additions/deductions required by provisions of trust instrument

IncomeEarnings derived from principal but certain

gains, losses or deductions may be considered adjustments to principal

7

Basic Concepts and Basic Concepts and DefinitionsDefinitions (3 of 5) (3 of 5)

GrantorParty that transfers assets to the trust

TrusteeParty that administers the trust

Income BeneficiaryParty (or parties) who receives income when

distributed by Trustee under provisions of trust instrument

8

Basic Concepts and Basic Concepts and DefinitionsDefinitions (4 of 5) (4 of 5)

RemaindermenParty (or parties) who eventually receives

trust principalSame person may receive both income and

principalSimple trust

Must distribute all income annually,Does not distribute any principal ANDMakes no contributions to charities

9

Basic Concepts and Basic Concepts and DefinitionsDefinitions (5 of 5) (5 of 5)

Complex trustAny trust that is not a simple trust

Personal exemption$300 if all income required to be

distributed annually$100 if current income may be

retained

10

Trust Taxable IncomeTrust Taxable Income

Gross Income- Deductions for expenses- Personal exemption= Taxable income before distribution- Distribution deduction= Trust taxable income

11

Distributable Net Distributable Net Income (DNI)Income (DNI) (1 of 2) (1 of 2)

DNI is maximum distribution deduction & income reportable by beneficiaries

No distribution deduction available for portion of distribution deemed to consist of tax-exempt income even though net tax-exempt income included in DNI

12

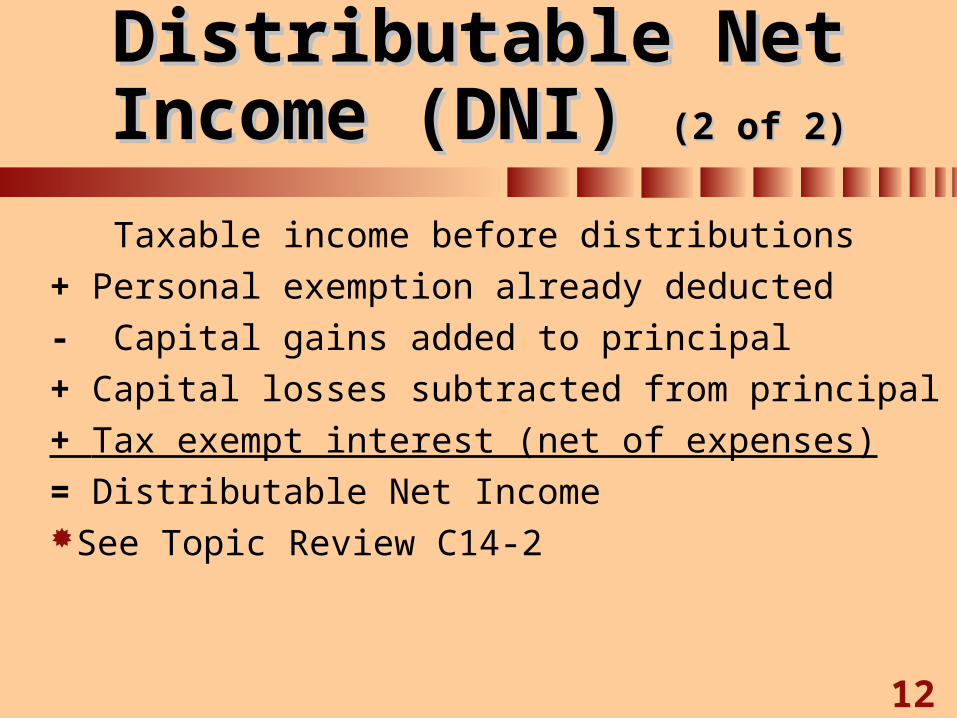

Distributable Net Distributable Net Income (DNI) Income (DNI) (2 of 2)(2 of 2)

Taxable income before distributions+ Personal exemption already deducted- Capital gains added to principal+ Capital losses subtracted from principal+ Tax exempt interest (net of expenses)= Distributable Net IncomeSee Topic Review C14-2

13

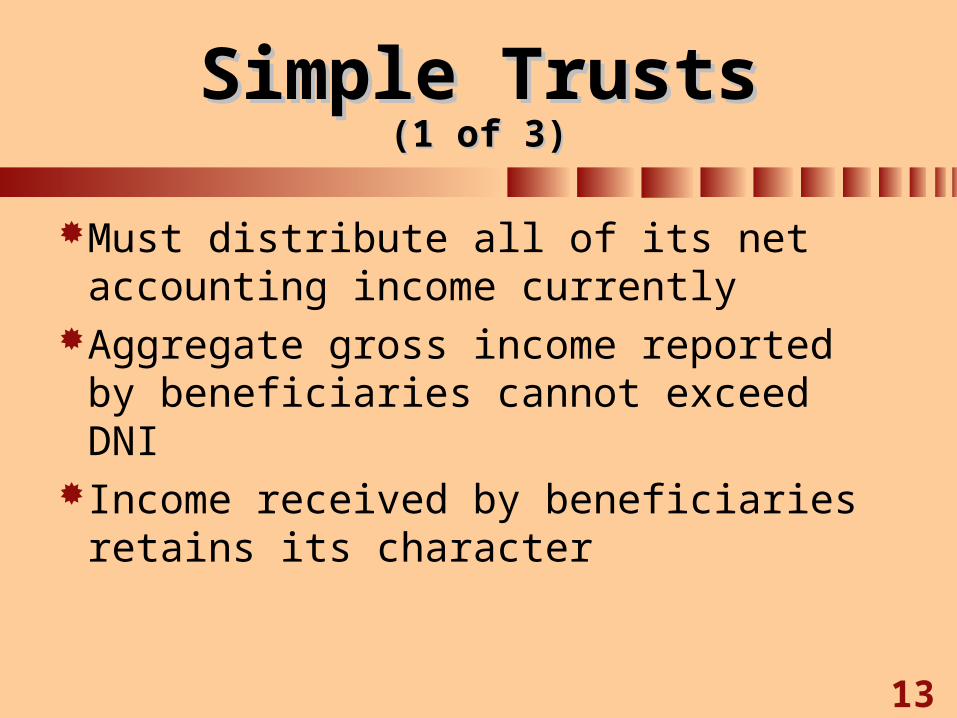

Simple TrustsSimple Trusts(1 of 3)(1 of 3)

Must distribute all of its net accounting income currently

Aggregate gross income reported by beneficiaries cannot exceed DNI

Income received by beneficiaries retains its character

14

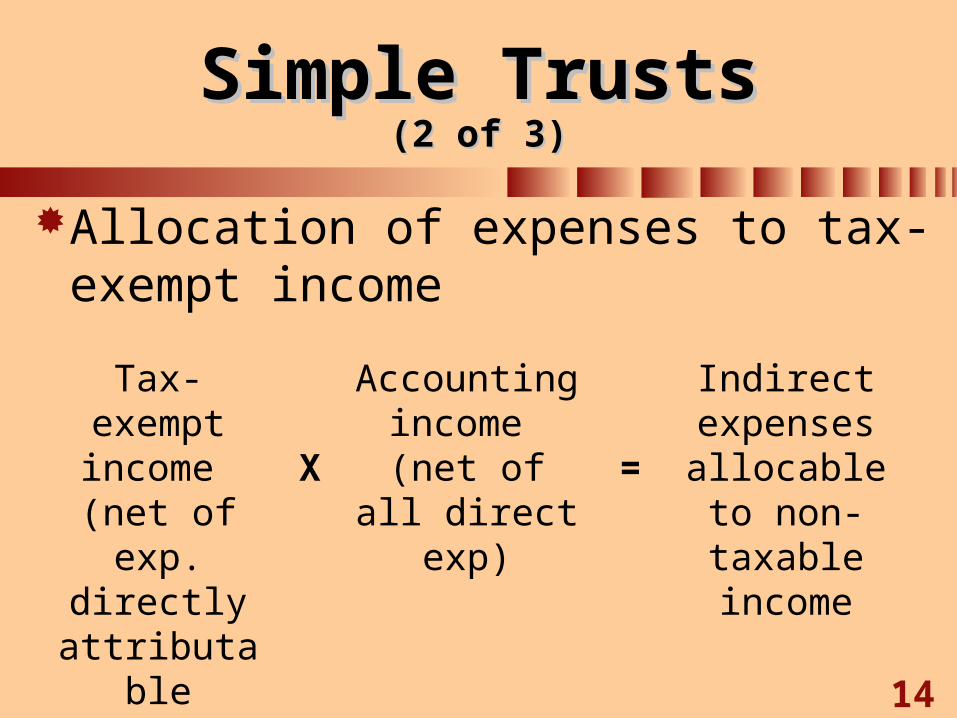

Simple TrustsSimple Trusts(2 of 3)(2 of 3)

Allocation of expenses to tax-exempt income

Tax-exempt income

(net of exp. directly

attributable thereto)

X

Accounting income

(net of all direct exp)

=

Indirect expenses allocable to non-taxable income

15

Simple TrustsSimple Trusts(3 of 3)(3 of 3)

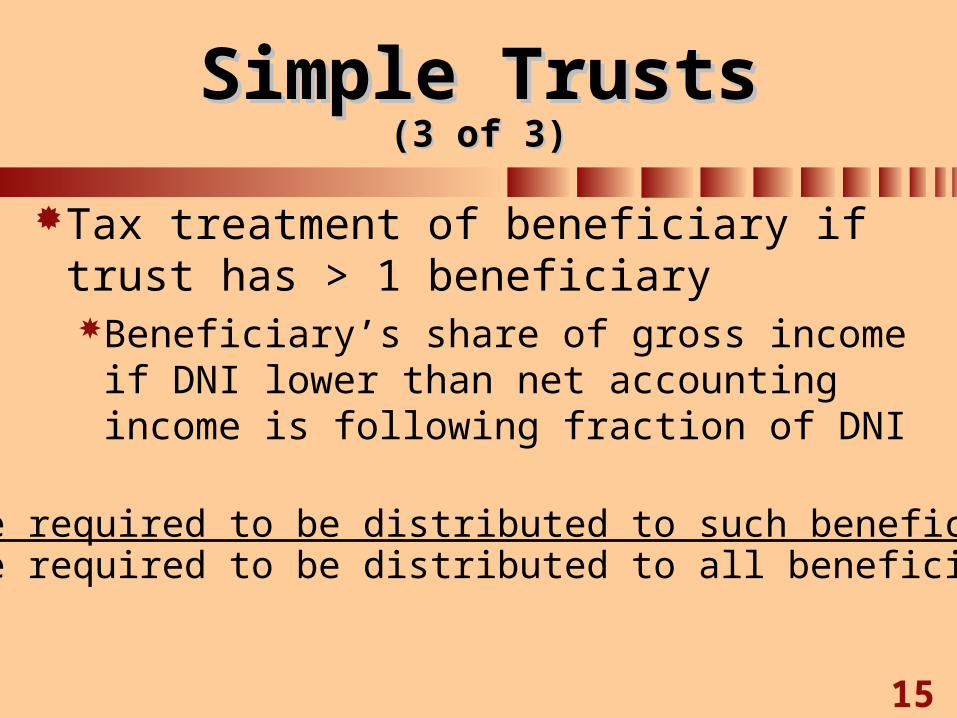

Tax treatment of beneficiary if trust has > 1 beneficiaryBeneficiary’s share of gross income

if DNI lower than net accounting income is following fraction of DNI

Income required to be distributed to such beneficiaryIncome required to be distributed to all beneficiaries

16

Complex TrustsComplex Trusts

Complex trusts permit the following activitiesMaking distributions < current earningsDistributing principalMaking charitable contributions

Complex trust’s DNIImpact on beneficiaries

17

Complex Trust’s DNI(1 of 2)

Complex DNI not reduced by charitable contribution deduction when determining maximum distribution for mandatory distributions

18

Complex Trust’s DNI(2 of 2)

DNI reduced when calculating deductible discretionary distributions

Distribution deduction is smaller of DNI or sum of mandatory and other amounts properly paid

19

Impact on Beneficiaries(1 of 2)

In generalBeneficiary includes distributions as gross income

up to current DNI for the trustAccumulation distribution or throwback rules

attempt to tax individual as if distributions were made annually

Higher trust tax rates make accumulation less desirable

20

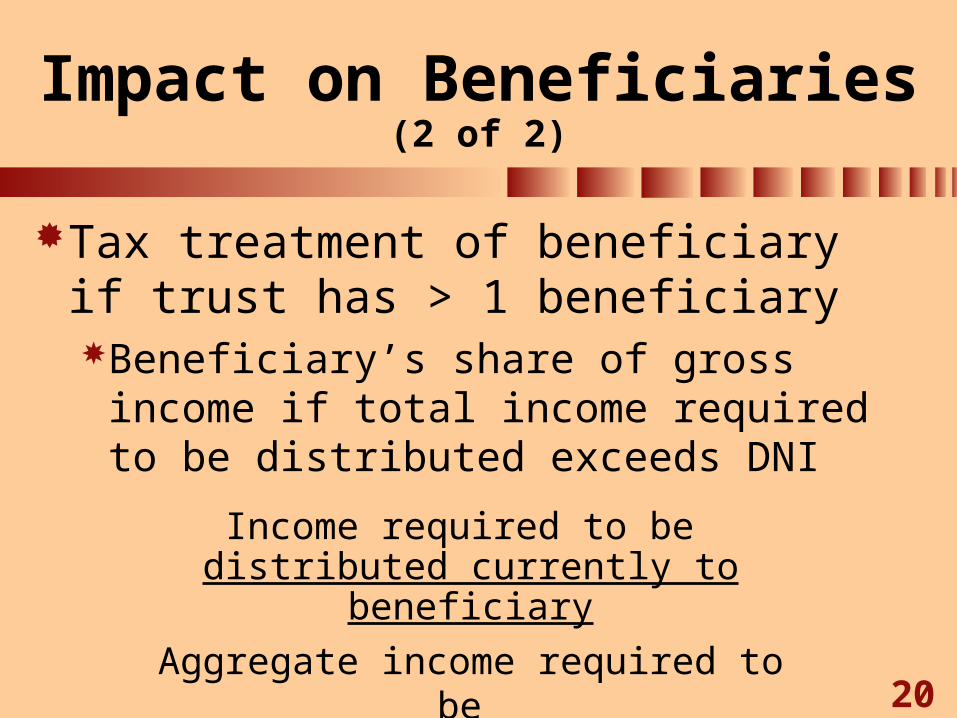

Impact on Beneficiaries(2 of 2)

Tax treatment of beneficiary if trust has > 1 beneficiaryBeneficiary’s share of gross income

if total income required to be distributed exceeds DNI

Income required to be distributed currently to beneficiary

Aggregate income required to be distributed to all beneficiaries currently

21

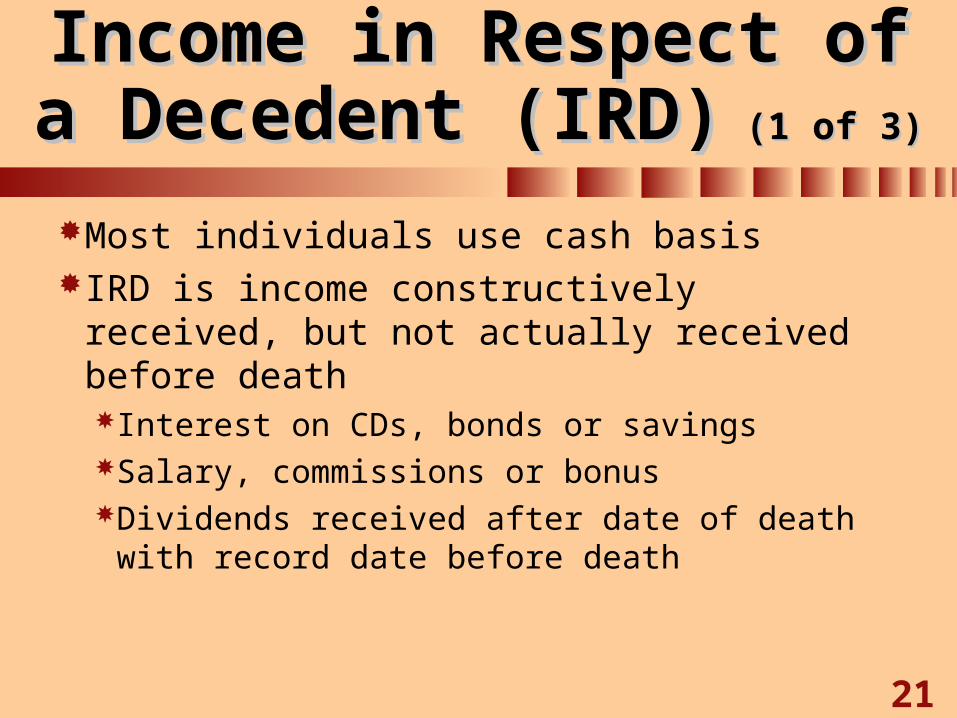

Income in Respect of a Income in Respect of a Decedent (IRD)Decedent (IRD) (1 of 3) (1 of 3)

Most individuals use cash basisIRD is income constructively received,

but not actually received before deathInterest on CDs, bonds or savingsSalary, commissions or bonusDividends received after date of death

with record date before death

22

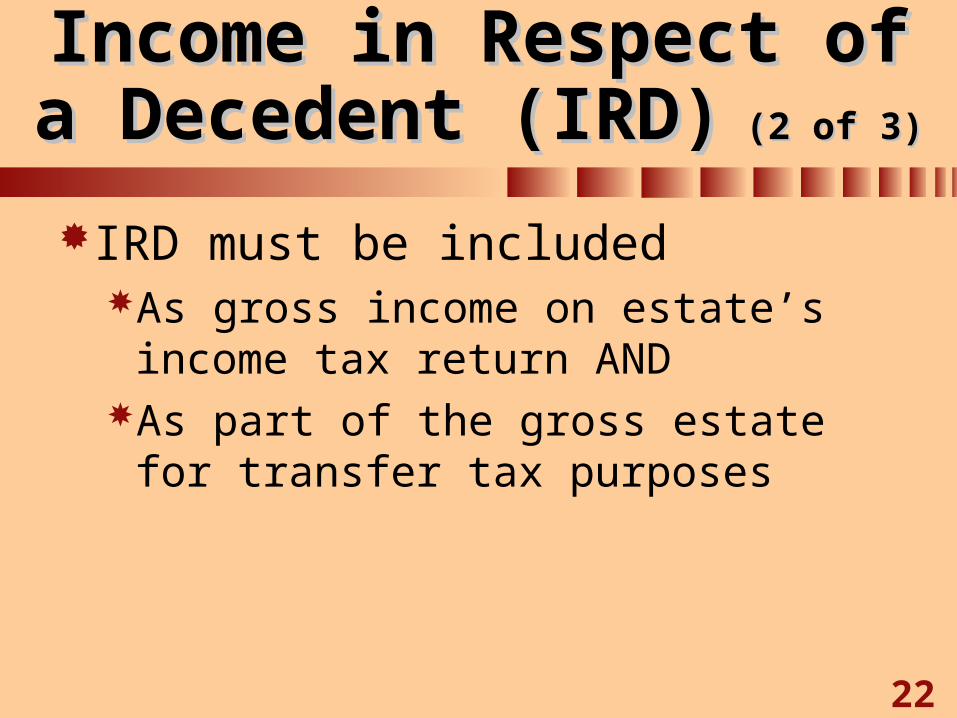

Income in Respect of a Income in Respect of a Decedent (IRD)Decedent (IRD) (2 of 3) (2 of 3)

IRD must be included As gross income on estate’s

income tax return ANDAs part of the gross estate for

transfer tax purposes

23

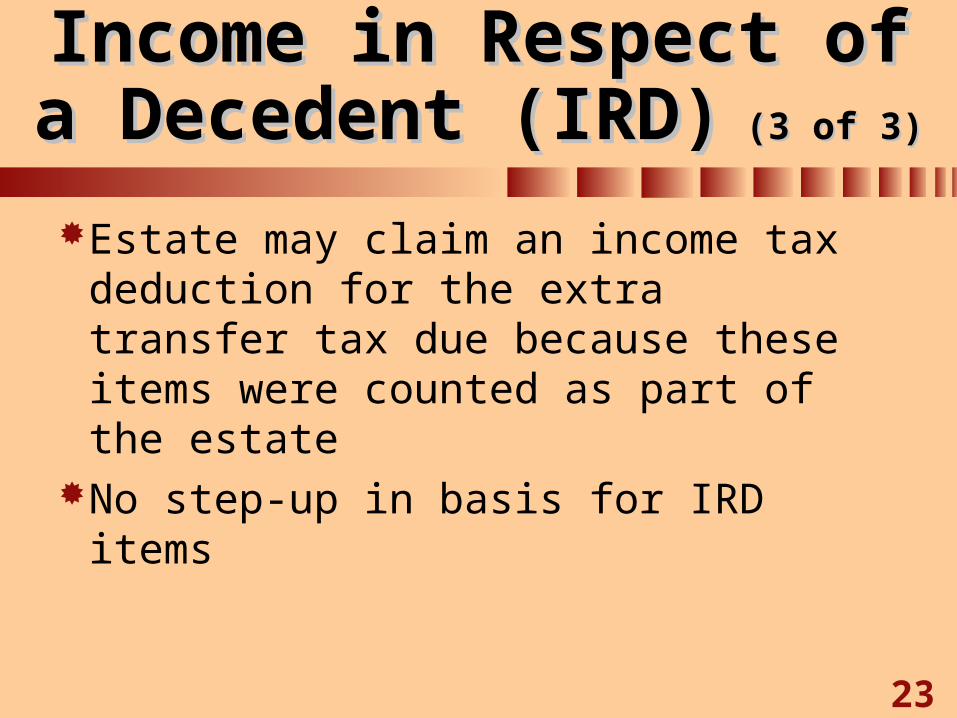

Income in Respect of a Income in Respect of a Decedent (IRD)Decedent (IRD) (3 of 3) (3 of 3)

Estate may claim an income tax deduction for the extra transfer tax due because these items were counted as part of the estate

No step-up in basis for IRD items

24

Grantor TrustsGrantor Trusts(1 of 2)(1 of 2)

Grantor does not give up enough control or economic benefit to be a completed transfer

Grantor taxed on some or all of trusts incomeEven if income distributed to

beneficiaries

25

Grantor TrustsGrantor Trusts(2 of 2)(2 of 2)

Types of grantor trustsRevocable trustsClifford TrustsPost-1986 Reversionary interest

trustsSee Topic Review C14-4

26

Comments or questions about PowerPoint Slides?Contact Dr. Richard Newmark atUniversity of Northern Colorado’s

Kenneth W. Monfort College of [email protected]