1 © copyright 2007 thomson south-western, a part of the thomson corporation. thomson, the star...

TRANSCRIPT

1

© Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star

Logo, and South-Western are trademarks used herein under license.

FINANCIAL ACCOUNTING

2ND EDITION

BY

DUCHAC, REEVE, & WARREN

4 Accounting Information Systems

2

LEARNING GOALS

When you finish this chapter, you should be able to

3

1. Describe nature of business information systems.

2. Describe nature of accounting information system.

3. Describe, illustrate basic elements of transaction processing system.

LEARNING GOALSLEARNING GOALS

Continued

4

LEARNING GOALSLEARNING GOALS

4. Describe, illustrate basic elements of financial reporting system.

5. Describe accounting cycle for double-entry accounting system.

6. Describe, illustrate computation, use of earning before interest, taxes, depreciation, amortization (EBITDA).

5

SOUTHWEST AIRLINES

Southwest Airlines

Developed profitable low-cost airline

Using only Boeing 737s

Using secondary airports

Avoiding commission-based ticket sales

6

LEARNING GOALSLEARNING GOALS

1Describe nature of business information system.

7

BUSINESS INFORMATION SYSTEM

Collects, processes data

Distributes information to stakeholders

Collects, processes data

Distributes information to stakeholders

LG 1

8

LEARNING GOALSLEARNING GOALS

2Describe nature of accounting information system.

9

LG 2

EXHIBIT EXHIBIT 22

Financial, operating data

Financial, operating data

Accounting Information Systems

•Management Reporting

•Transactions Processing

•Financial Reporting

Accounting Information Systems

•Management Reporting

•Transactions Processing

•Financial Reporting

Stakeholders

Stakeholders

Stakeholders

10

What information do these 3 systems produce?

LG 2

11

MANAGEMENT REPORTING SYSTEM

MANAGEMENT REPORTING SYSTEM

• Provides internal information for decision making– Reports

• Budgets

• Variance analyses

• Provides internal information for decision making– Reports

• Budgets

• Variance analyses

LG 2

12

TRANSACTION PROCESSING SYSTEM

TRANSACTION PROCESSING SYSTEM

• Records, summarizes effects of financial transactions into accounts

• Divides transactions into cycles– Revenue cycle– Purchasing cycle– Payroll cycle– Inventory cycle– Treasury cycle

• Records, summarizes effects of financial transactions into accounts

• Divides transactions into cycles– Revenue cycle– Purchasing cycle– Payroll cycle– Inventory cycle– Treasury cycle

LG 2

13

FINANCIAL REPORTING SYSTEM

FINANCIAL REPORTING SYSTEM

• Produces financial statements– Income statement– Statement of retained earnings– Balance sheet– Statement of cash flows

• Produces financial statements– Income statement– Statement of retained earnings– Balance sheet– Statement of cash flows

LG 2

14

LEARNING GOALSLEARNING GOALS

3Describe, illustrate basic elements of transaction processing system.

15

THE ACCOUNT

Each account has a

Title

Recording place for debits

Recording place for credits

Each account has a

Title

Recording place for debits

Recording place for credits

LG 3

Left side

Debit

Right side

Credit

Title

16

RULES OF DEBIT & CREDIT

• Normal balance of account is side used to increase

• Asset accounts have debit balances

• Example: cashCASH

DEBITS INCREASE

LG 3

Continued

17

RULES OF DEBIT & CREDIT• Normal balance of account is side used to

increase

• Liability, Equity accounts have credit balances

• Example: Retained EarningsRETAINED EARNINGS

LG 3

CREDITS INCREASE

18

BALANCE SHEET EQUATION

A = L + E

LG 3

19

RULE 2 OF DEBIT & CREDIT: Assets

• Asset accounts on left side of equation are – Increased by debits and – Have debit balances

DEBIT BALANCE

ASSET ACCTS

+

LG 3

20

RULE 2 OF DEBIT & CREDIT: Liability & Equity

• Liability & equity accounts on right side of equation are – Increased by credits and – Have credit balances

LIABILITY & EQUITY ACCTS

CREDIT BALANCE

+

LG 3

21

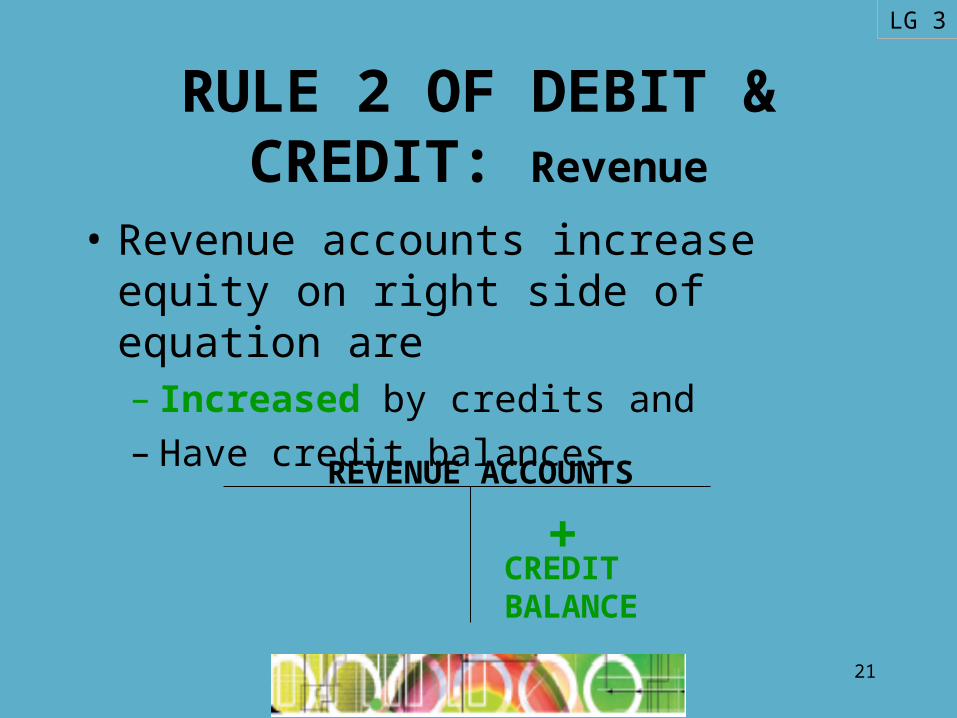

RULE 2 OF DEBIT & CREDIT: Revenue

• Revenue accounts increase equity on right side of equation are – Increased by credits and – Have credit balances

REVENUE ACCOUNTS

CREDIT BALANCE

+

LG 3

22

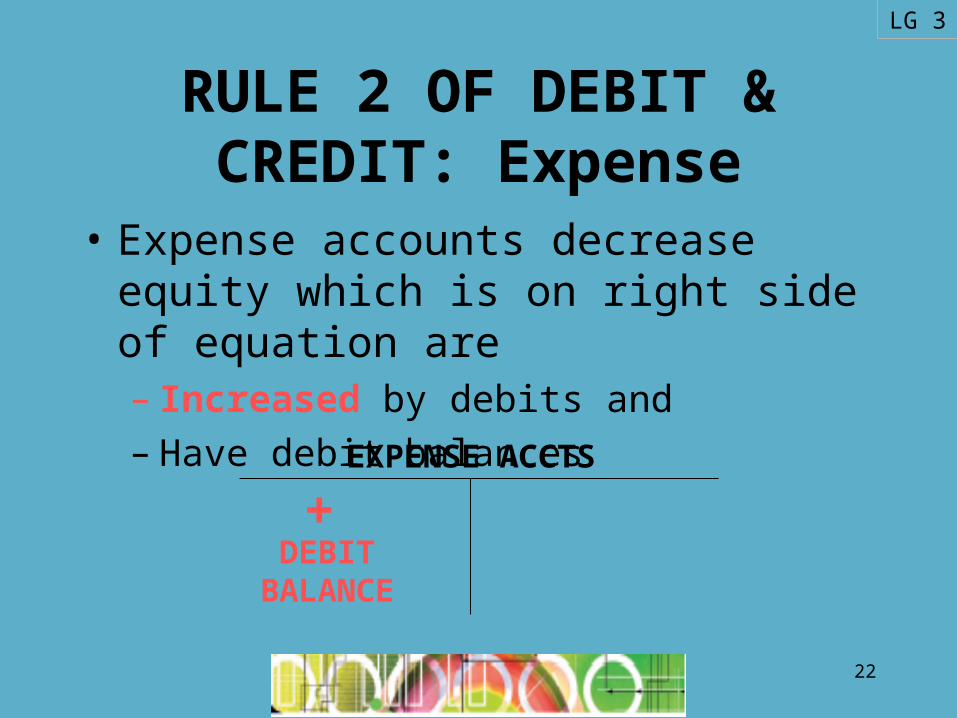

RULE 2 OF DEBIT & CREDIT: Expense

• Expense accounts decrease equity which is on right side of equation are – Increased by debits and – Have debit balances

DEBIT BALANCE

EXPENSE ACCTS

+

LG 3

23

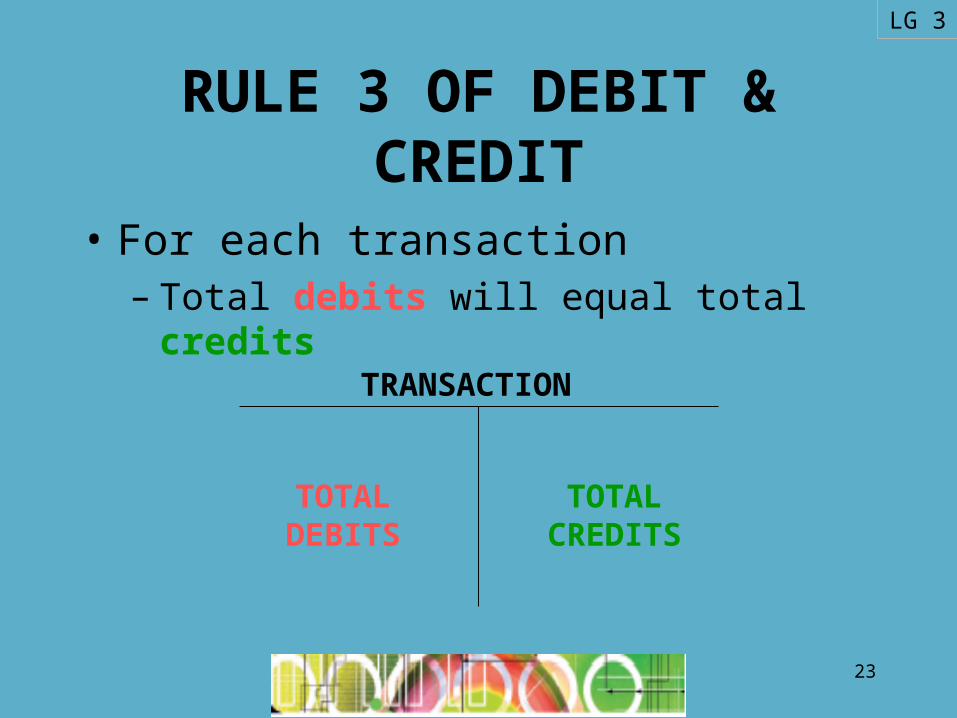

RULE 3 OF DEBIT & CREDIT

• For each transaction– Total debits will equal total credits

TRANSACTION

TOTAL CREDITS

TOTAL DEBITS

LG 3

24

LG 3

EXHIBIT EXHIBIT 33

25

RECORDING TRANSACTIONS

RECORDING TRANSACTIONS

• Transactions recorded in– Journals

• Organized by date

– Ledgers• Organized by account

Click the button to skip journal entries

26

ENTRY 11/5: Bought Land

Buying land for cash

Decreases cash flows, investing

Has no effect on balance sheet

Has no effect on income statement

LG 3

11/5 Land

Cash

20,000

20,000

Click the button to skip journal entries

SCF BS IS

27

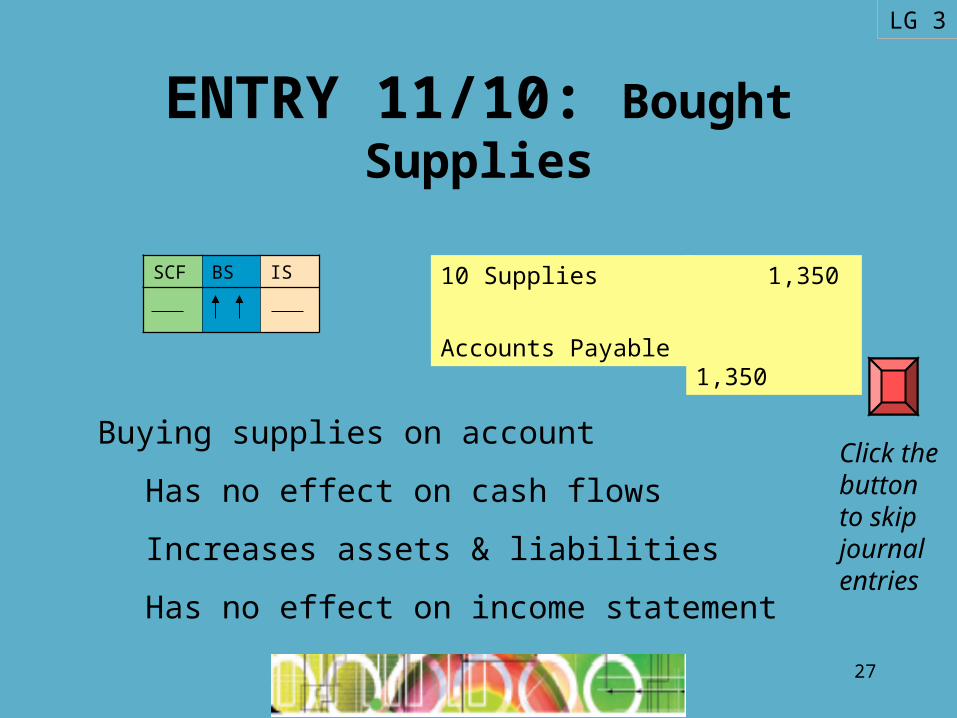

ENTRY 11/10: Bought Supplies

Buying supplies on account

Has no effect on cash flows

Increases assets & liabilities

Has no effect on income statement

LG 3

10 Supplies

Accounts Payable

1,350

1,350

Click the button to skip journal entries

SCF BS IS

28

ENTRY 11/18: Earned Fees

Received cash for fees earned

Increases cash flows from operations

Increases assets & equity

Increases revenue

LG 3

18 Cash

Fees Earned

7,500

7,500

Click the button to skip journal entries

SCF BS IS

R

29

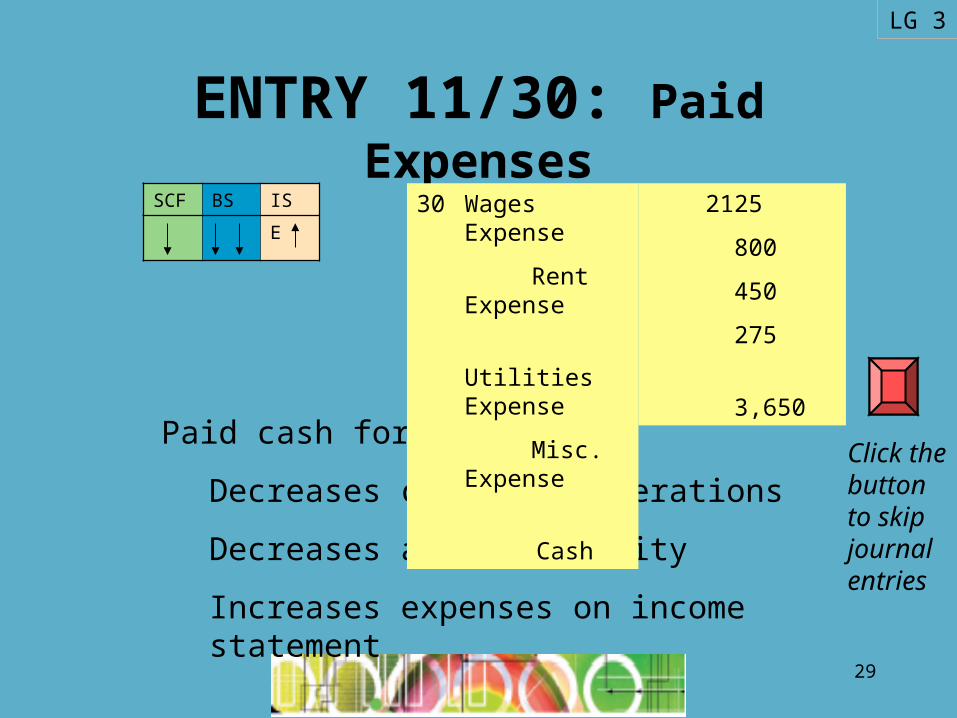

ENTRY 11/30: Paid Expenses

Paid cash for expenses

Decreases cash flow operations

Decreases assets & equity

Increases expenses on income statement

LG 3

30 Wages Expense

Rent Expense

Utilities Expense

Misc. Expense

Cash

2125

800

450

275

3,650

Click the button to skip journal entries

SCF BS IS

E

30

ENTRY 11/30: Paid Account

Paid cash to satisfy accounts payable

Decreases cash flow operations

Decreases assets, liabilities

Has no effect on income statement

LG 3

30 Accounts payable

Cash

950

950

Click the button to skip journal entries

SCF BS IS

31

ENTRY 11/30: Paid Dividend

Paid cash dividends

Decreases cash flow financing

Decreases assets, equity

Has no effect on income statement

LG 3

2,000

2,000

30 Dividends

Cash

SCF BS IS

32

EXERCISE 4-2a (modified)EXERCISE 4-2a (modified)

Press “Enter” or click left mouse button for answer.

Identify accounts of Continental Airlines with normal debit balance.

1. Accounts payable

2. Fuel expense

3. Traffic liability

4. Cargo revenue

5. Commissions expense

6. Flight equipment

7. Passenger revenue

8. Spare parts & supplies

LG 3

Click the button to skip this exercise

33

EXERCISE 4-2b (modified)EXERCISE 4-2b (modified)

Press “Enter” or click left mouse button for answer.

Identify accounts of Continental Airlines with normal credit balance.

1. Accounts payable

2. Fuel expense

3. Traffic liability

4. Cargo revenue

5. Commissions expense

6. Flight equipment

7. Passenger revenue

8. Spare parts & supplies

LG 3

Click the button to skip this exercise

34

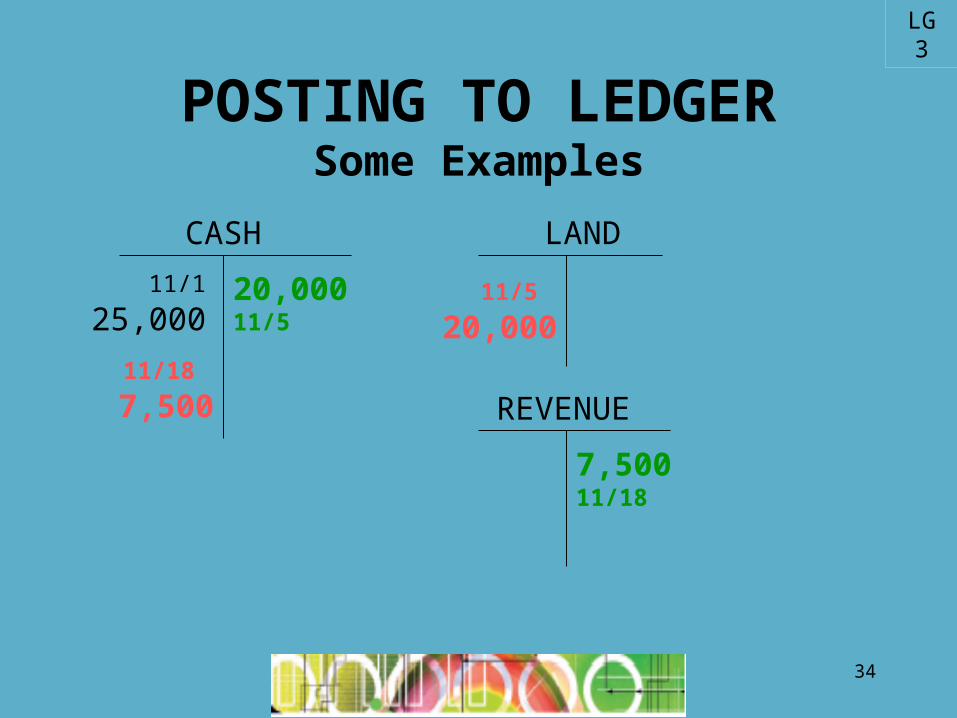

POSTING TO LEDGERSome Examples

CASH LAND

REVENUE

11/1 25,000 20,000 11/5 11/5 20,000

11/18 7,500

7,500 11/18

LG 3

35

LG 3

Trial balance lists accounts, balances in debit, credit columns to check recording process.

EXHIBIT EXHIBIT 77

36

LEARNING GOALSLEARNING GOALS

4Describe, illustrate basic elements of financial reporting system.

37

END OF YEAR: 12/31/2007END OF YEAR: 12/31/2007

• Transactions for December recorded– Journals, ledgers

• Trial balance for December transactions• Adjustments recorded

– Supplies, insurance used– Revenue earned– Wages owed– Depreciation

• Transactions for December recorded– Journals, ledgers

• Trial balance for December transactions• Adjustments recorded

– Supplies, insurance used– Revenue earned– Wages owed– Depreciation

Continued

LG 4

38

END OF YEAR: 12/31/2007END OF YEAR: 12/31/2007

• Adjusted trial balance– Final check before financial statements

• Prepare financial statements– Income statement– Statement retained earnings– Balance sheet– Statement cash flows

• Adjusted trial balance– Final check before financial statements

• Prepare financial statements– Income statement– Statement retained earnings– Balance sheet– Statement cash flows

LG 4

See Exhibit 12 p. 166-167

39

• Statement of cash flows linked to cash on balance sheet

• Net income from income statement linked to retained earnings statement

• Retained earnings linked to balance sheet in stockholders’ equity

INTEGRATED FINANCIAL STATEMENTS (IFS)

INTEGRATED FINANCIAL STATEMENTS (IFS)

LG 4

Click the button to skip Exh. 12.

40

EXHIBIT EXHIBIT 1212

IFS: Statement of cash flows linked to cash on balance sheet

LG 4

41

EXHIBIT EXHIBIT 12 12 (cont.)(cont.)

IFS: Net income from income statement linked to retained

earnings statement

LG 4

42

EXHIBIT EXHIBIT 12 12 (cont.)(cont.)

IFS: Retained earnings linked to balance sheet in stockholders’ equity

LG 4

43

AFTER FINANCIAL STATEMENTS

• Closing entries– Transfer balances of temporary (revenue,

expense, dividends) accounts to retained earnings

– Zero balances of temporary accounts to carry forward

• Post-closing trial balance– Final check for asset, liability, equity account

balances

• Closing entries– Transfer balances of temporary (revenue,

expense, dividends) accounts to retained earnings

– Zero balances of temporary accounts to carry forward

• Post-closing trial balance– Final check for asset, liability, equity account

balances

LG 4

44

LEARNING GOALSLEARNING GOALS

5Describe accounting cycle for double-entry accounting system.

45

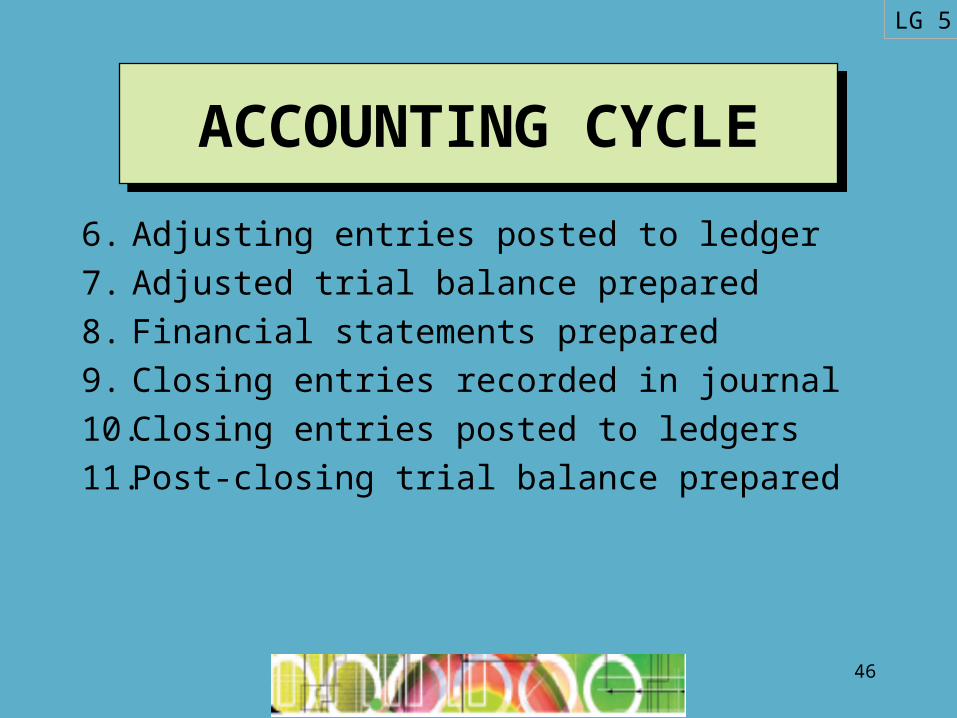

ACCOUNTING CYCLEACCOUNTING CYCLE

1. Transactions analyzed, recorded in journals

2. Transactions posted to ledgers3. Unadjusted trial balance prepared4. Adjustment data assembled, analyzed5. Adjusting entries prepared, recorded in

journal

Continued

LG 5

46

ACCOUNTING CYCLEACCOUNTING CYCLE

6. Adjusting entries posted to ledger

7. Adjusted trial balance prepared

8. Financial statements prepared

9. Closing entries recorded in journal

10. Closing entries posted to ledgers

11. Post-closing trial balance prepared

LG 5

47

THE END

CHAPTER 4