1 copyright © 2008 thomson south-western, a part of the thomson corporation. thomson, the star...

TRANSCRIPT

1Copyright © 2008 Thomson South-Western, a part of the Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under

license.

Mowen/Hansen

Performance Evaluation, Variable Costing, and Decentralization

Chapter Eleven

Cornerstones of Managerial Accounting 2e

Cornerstones of Managerial Accounting 2e

2

Objective # 1Objective # 1

Explain how and why firms choose to decentralize.

3

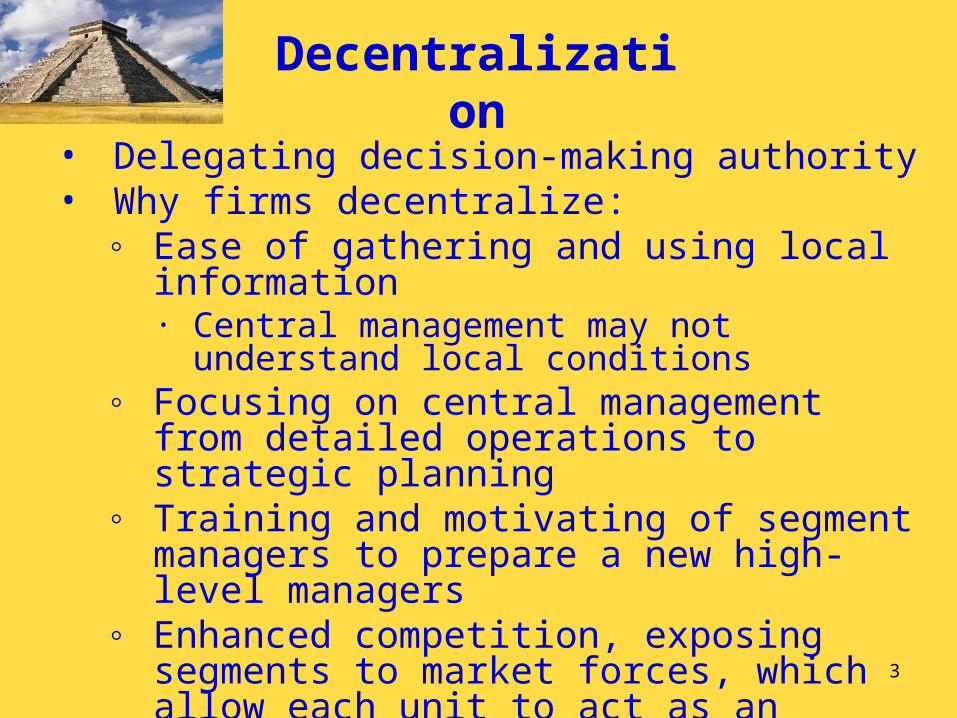

Decentralization

• Delegating decision-making authority • Why firms decentralize:

◦ Ease of gathering and using local information∙ Central management may not understand local

conditions◦ Focusing on central management from

detailed operations to strategic planning◦ Training and motivating of segment managers

to prepare a new high-level managers◦ Enhanced competition, exposing segments to

market forces, which allow each unit to act as an autonomous business unit

• Achieved by creating Divisions

4

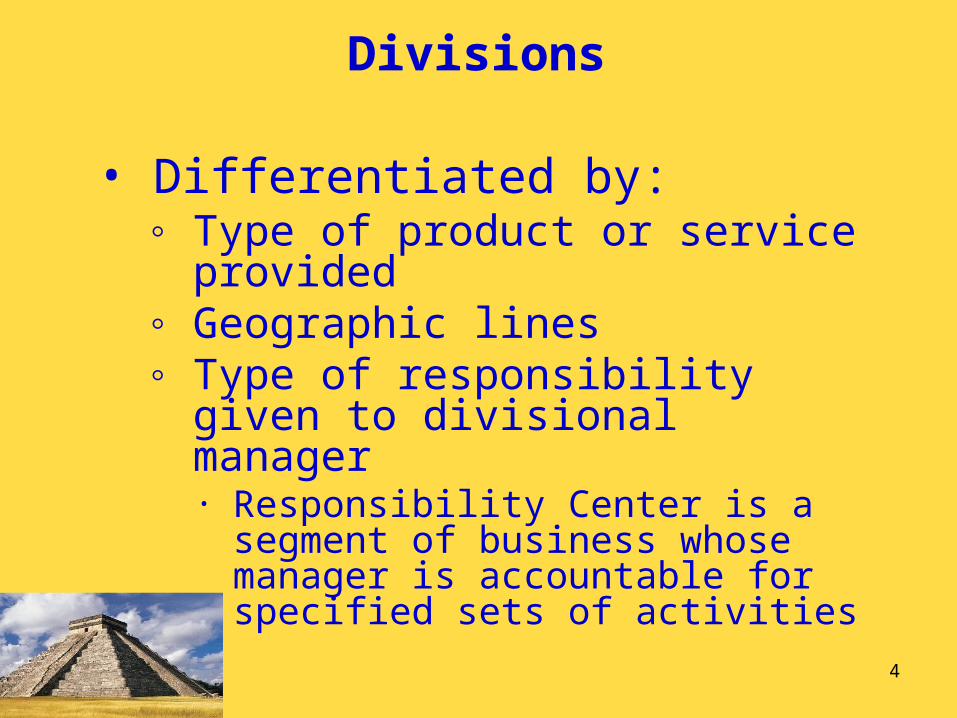

Divisions

• Differentiated by:◦ Type of product or service provided◦ Geographic lines◦ Type of responsibility given to

divisional manager∙ Responsibility Center is a segment of

business whose manager is accountable for specified sets of activities

5

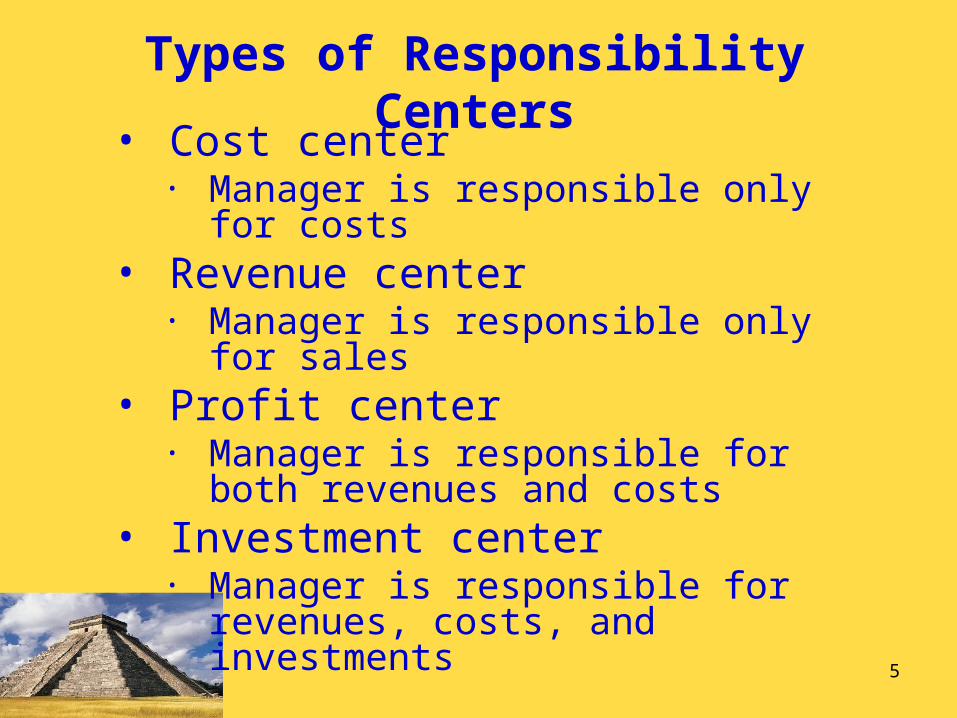

Types of Responsibility Centers

• Cost center∙ Manager is responsible only for costs

• Revenue center∙ Manager is responsible only for sales

• Profit center∙ Manager is responsible for both

revenues and costs• Investment center

∙ Manager is responsible for revenues, costs, and investments

6

Measuring the Performance of Profit Centers

• Preparation of segmented income statements ◦ Two methods of computing income:

∙ Variable costing∙ Full or Absorption costing

◦ Methods often lead to different operating income figures

7

Objective # 2Objective # 2

Explain the difference between absorption and variable costing, and prepare segmented income

statements.

8

Variable Costing Income Statement

• Assigns only variable manufacturing costs to the product◦ Direct Materials◦ Direct Labor◦ Variable Overhead

• Fixed overhead is treated as a period expense

9

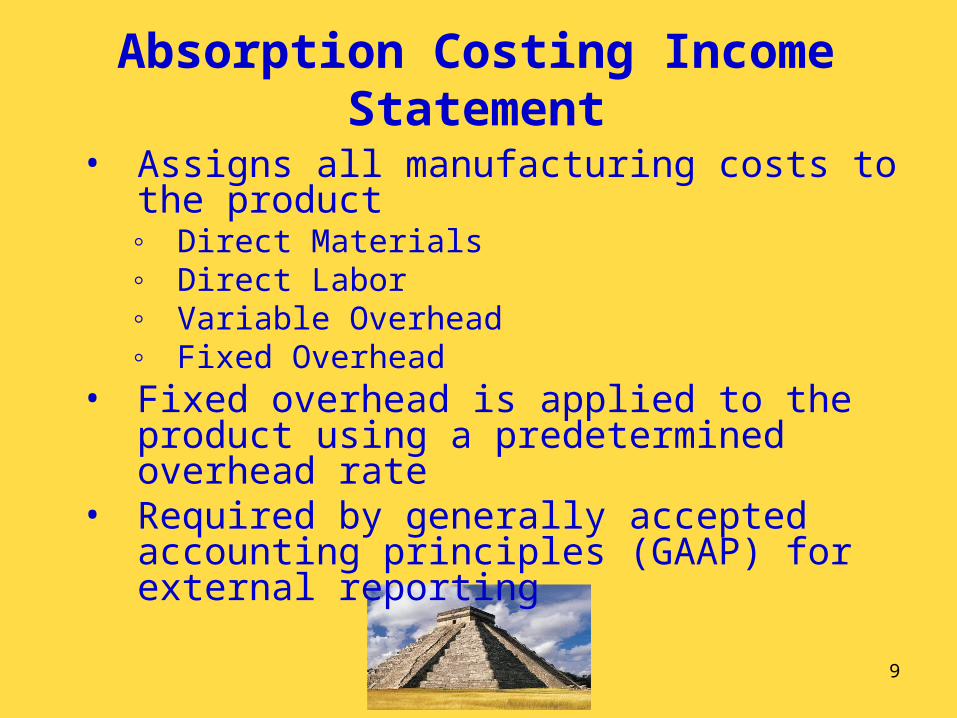

Absorption Costing Income Statement

• Assigns all manufacturing costs to the product◦ Direct Materials◦ Direct Labor◦ Variable Overhead◦ Fixed Overhead

• Fixed overhead is applied to the product using a predetermined overhead rate

• Required by generally accepted accounting principles (GAAP) for external reporting

10

Segmented Income Statements

• Segment is a subunit of a company◦ Divisions◦ Departments◦ Product lines◦ Customer classes

• Fixed expenses are broken down into two categories:

◦ Direct fixed expenses∙ Directly traceable to a segment

◦ Common fixed expenses∙ Jointly caused by two or more segments

11

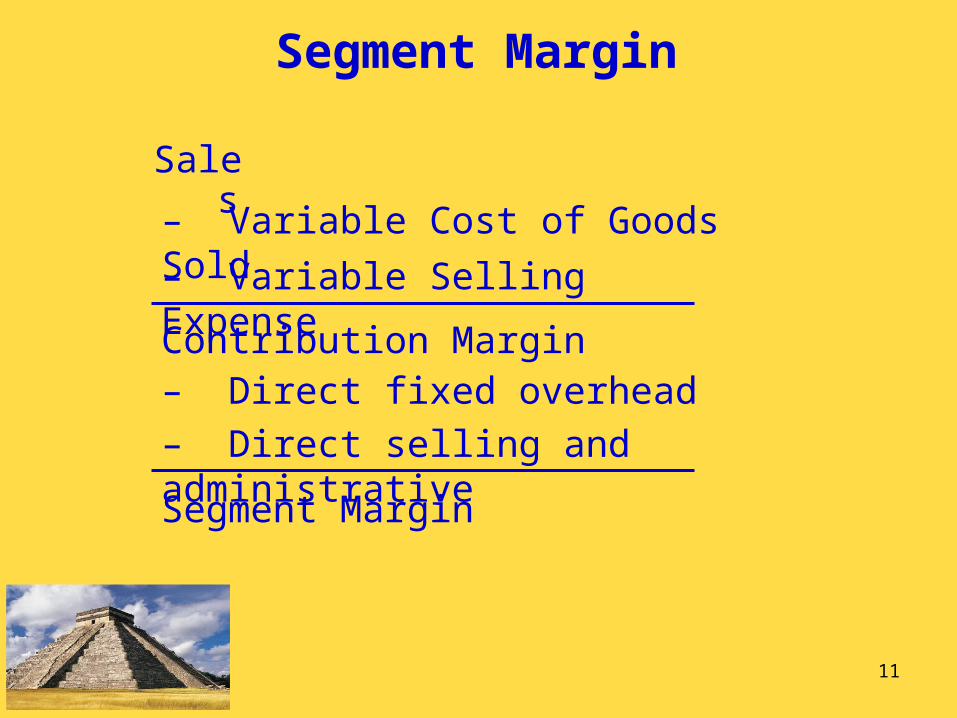

Segment Margin

Sales

– Variable Cost of Goods Sold

– Variable Selling Expense

Contribution Margin– Direct fixed overhead

– Direct selling and administrative

Segment Margin

12

Objective # 3Objective # 3

Compute and explain return on investment.

13

Return on Investment (ROI)

Operating Income ÷ Average Operating Assets

Earnings before income and taxes (EBIT)

Formula:

14

Return on Investment (ROI)

Operating Income ÷ Average Operating Assets

(Beginning assets + Ending assets) ÷ 2

Formula:

15

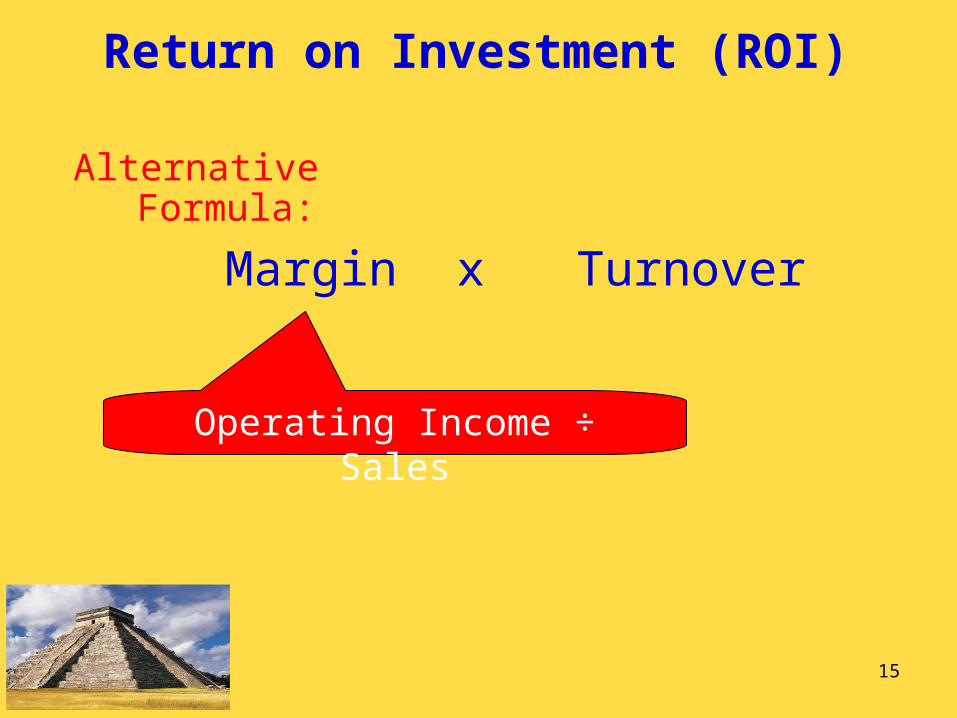

Return on Investment (ROI)

Margin

Operating Income ÷ Sales

Alternative Formula:

Turnoverx

16

Return on Investment (ROI)

Margin

Sales ÷ Average Operating Assets

Alternative Formula:

Turnoverx

17

Margin and Turnover

• Margin◦ Ratio of operating income to sales◦ Tells how many cents of operating income

result from each dollar of sales◦ Expresses the portion of sales that is

available for interest, taxes, and profit• Turnover

◦ Divides sales by average operating assets◦ Tells how many dollars of sales result

from every dollar invested in operating assets

18

Advantages of ROI

• Encourages managers to focus on◦ Relationship among:

∙ Sales∙ Expenses∙ Investment

◦ Cost efficiency◦ Operating asset efficiency

19

Disadvantages of ROI

• Can produce a narrow focus on divisional profitability at the expense of profitability for the overall firm

• Encourages managers to focus on the short run at the expense of the long run

20

Objective # 4Objective # 4

Compute and explain residual income and economic value

added.

21

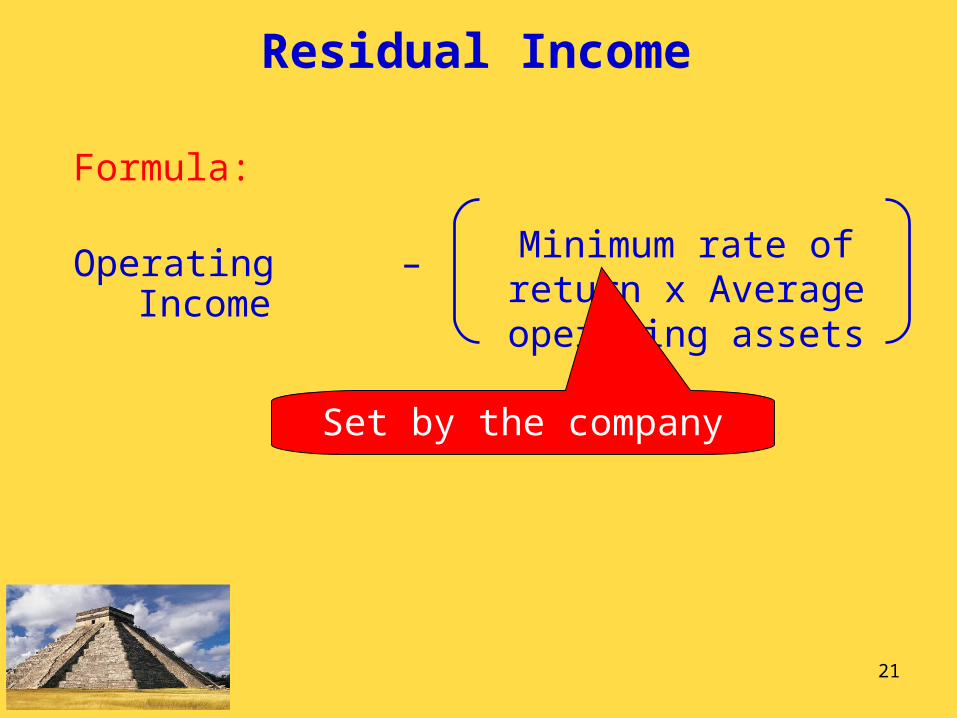

Residual Income

Formula:

Operating Income Minimum rate of return x Average operating assets

–

Set by the company

22

Residual Income

Formula:

Operating Income Minimum rate of return x Average operating assets

–

If residual income is less than zero, the company is earning less than the minimum rate of return

If residual income is exactly zero, the company is earning precisely the minimum rate of return

If residual income is greater than zero, the company is earning more than the minimum rate of return

23

Advantages & Disadvantages of Residual Income

• Advantages◦ It encourages managers to accept any project

that earns about the minimum rate

• Disadadvantages◦ Can encourage a short run orientation◦ Residual income is an absolute measure of

profitability∙ Direct comparison is difficult when level of investments

differ

24

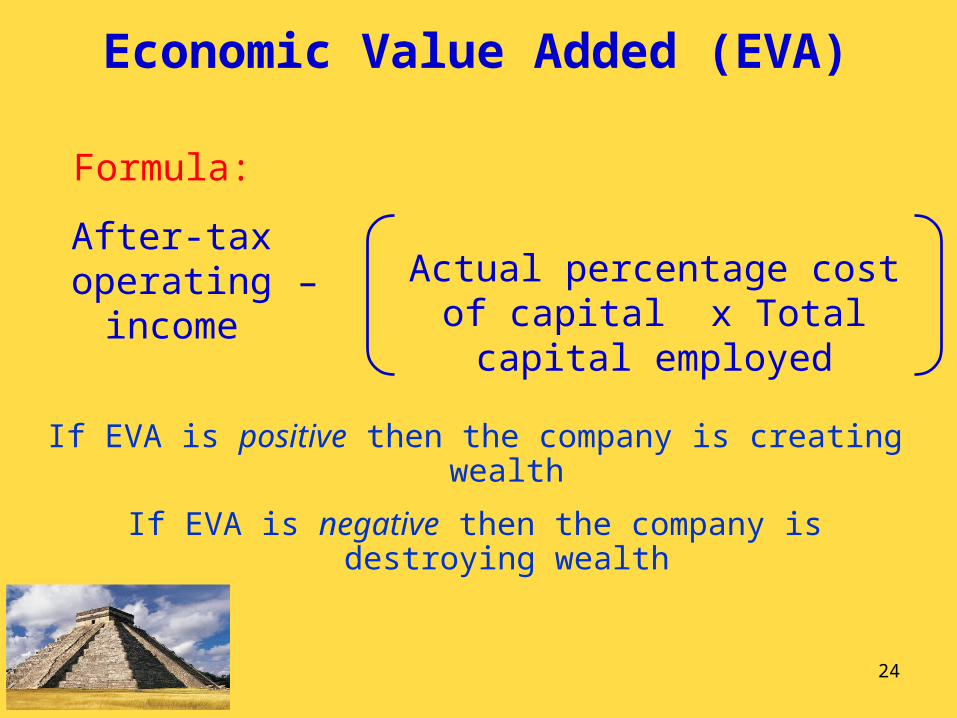

Economic Value Added (EVA)

Formula:

Actual percentage cost of capital x Total capital employed

–

If EVA is positive then the company is creating wealth

If EVA is negative then the company is destroying wealth

After-tax operating income

25

Advantages of EVA

• Helps to encourage the right kind of behavior• Relies on the true cost of capital• Cost of capital is considered a corporate expense

and is passed along to the overall income statement• Makes investment seem free to the divisions so

they want more

26

Objective # 5Objective # 5

Explain the role of transfer pricing in a decentralized firm.

27

Transfer Pricing

• Price charged for a component by the selling division to the buying division of the same company

• Sale is a revenue to the selling division• Sale is a cost to the buying division• Transfer Pricing policies:

◦ Market price◦ Cost-based transfer pricing◦ Negotiated transfer pricing

28

Example

Transfer Pricing at a Negotiated Transfer Price:

Minimum transfer price = $14 – $3 = $11

This price is set by Alpha division (the selling division)

Maximum transfer price = $14

This price is the market price and is set by Delta division (the buying division)

Alpha and Delta will negotiate a price somewhere between $11 and $14