1 i ntroduction to accounting lecture 3 and 4. learning objectives: part a balance sheet vertical...

TRANSCRIPT

1

I NTRODUCTION TO ACCOUNTING

LECTURE 3 AND 4

Learning Objectives: Part A

Balance Sheet vertical format Income Statement vertical format Working Capital Main Types of Business Transactions

2

The balance sheet is a financial “snap shot”: instant explosion: It lists the assets and liabilities of the business on a particular day.

The balance sheet is a list of all the assets (what the business owns) and all the liabilities (what the business owes) of a business.

Fixed Assets are assets that the business owns: They will keep these assets for several years so they are fixed.

Current assets mean that the assets will not stay in the business for long. Examples: materials, debtors, money in the bank, petty ca

The start up of the business is funded by: CAPITAL & RESERVES CAPITAL- The amount of money contributed by the owner or partners In the case of LTD company SHARE CAPITAL – The amount of money

paid by shareholders in return for a share in the business. PROFIT & LOSS ACCOUNT – Net profit from the previous financial year is

transferred into the balance sheet. In the case of LTD company we also have: RETAINED PROFIT –

businesses do not give all of their profits back to shareholder. In Accounting I we will only concerned with the Capital in general not share capital and with

the Net Profit or Loss.3

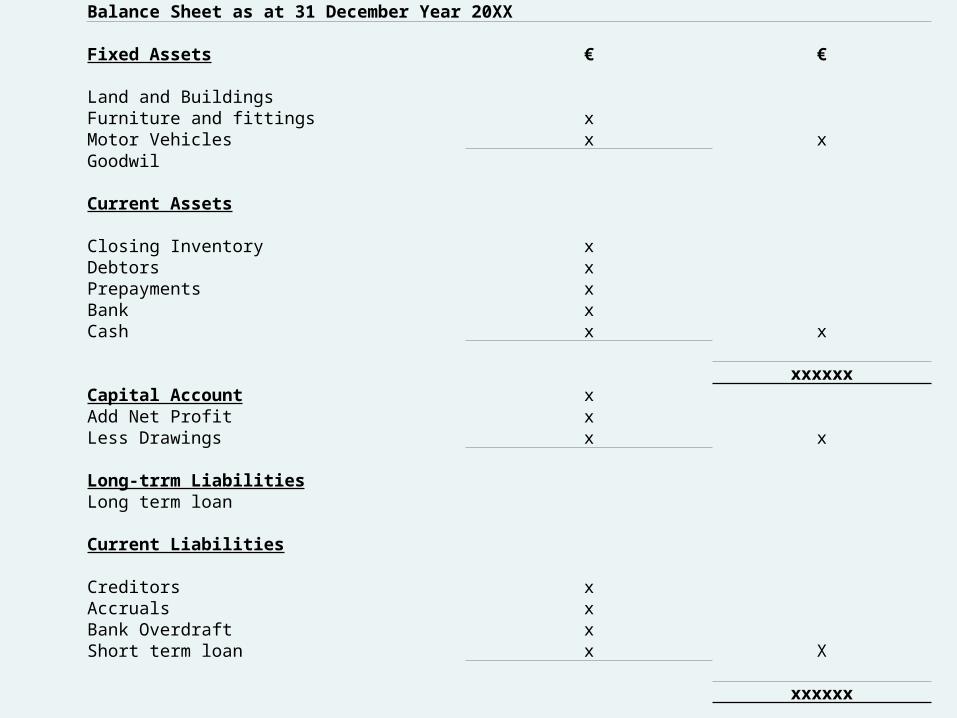

Balance Sheet as at 31 December Year 20XX

Fixed Assets € €

Land and BuildingsFurniture and fittings xMotor Vehicles x xGoodwil

Current Assets

Closing Inventory xDebtors xPrepayments xBank xCash x x

xxxxxxCapital Account xAdd Net Profit xLess Drawings x x

Long-trrm LiabilitiesLong term loan

Current Liabilities

Creditors xAccruals xBank Overdraft xShort term loan x X

xxxxxx

5

NET ASSETS SHOULD EQUAL THE AMOUNT OF MONEY THAT HAS BEEN INVESTED IN THE BUSINESS.BOTH PARTS OF THE BALANCE SHEET MUST BALANCE

6

The Trading Account

This account concentrates all transactions and accounts related to stock.

The Trading Account shows the profit, before charging any expenses like heat, light, wages or telephone bills.

This allows the owner to see how healthy the profit is before these expenses are included.

Profit and Loss Account

A profit and loss account is a summary of business transactions for a given period - normally 12 months. By deducting total expenditure from total income, it shows on the "bottom line" whether your business made a profit or loss at the end of that period.

A profit and loss account is produced primarily for business purposes – to show owners, shareholders or potential investors how the business is performing. But most of the information is also used by the Inland Revenue to work out your tax bill.

7

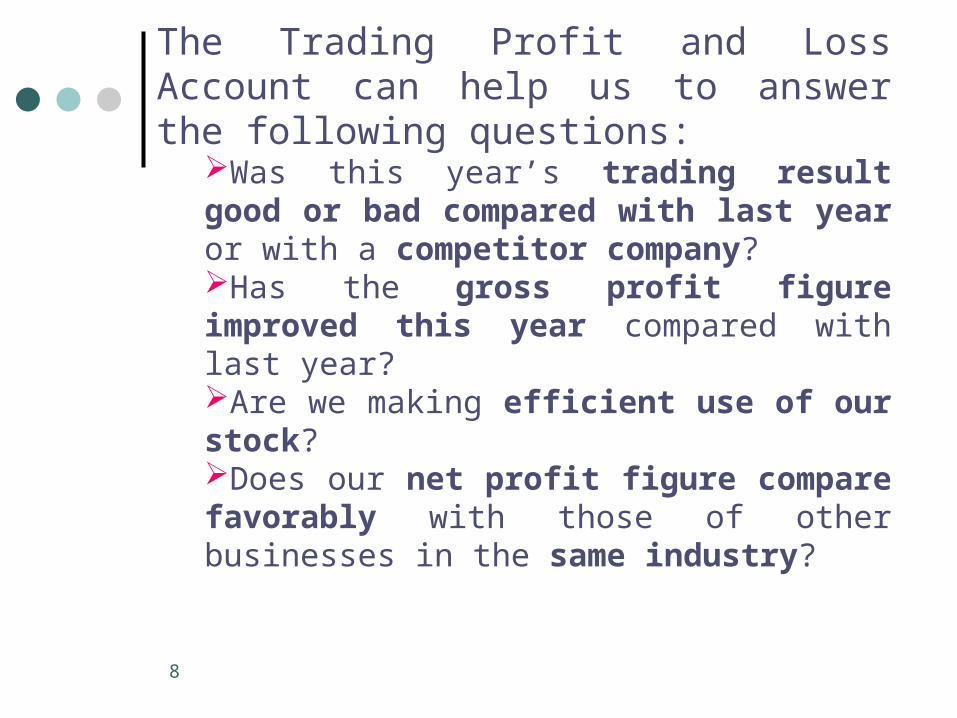

8

The Trading Profit and Loss Account can help us to answer the following questions:

Was this year’s trading result good or bad compared with last year or with a competitor company?Has the gross profit figure improved this year compared with last year?Are we making efficient use of our stock?Does our net profit figure compare favorably with those of other businesses in the same industry?

9

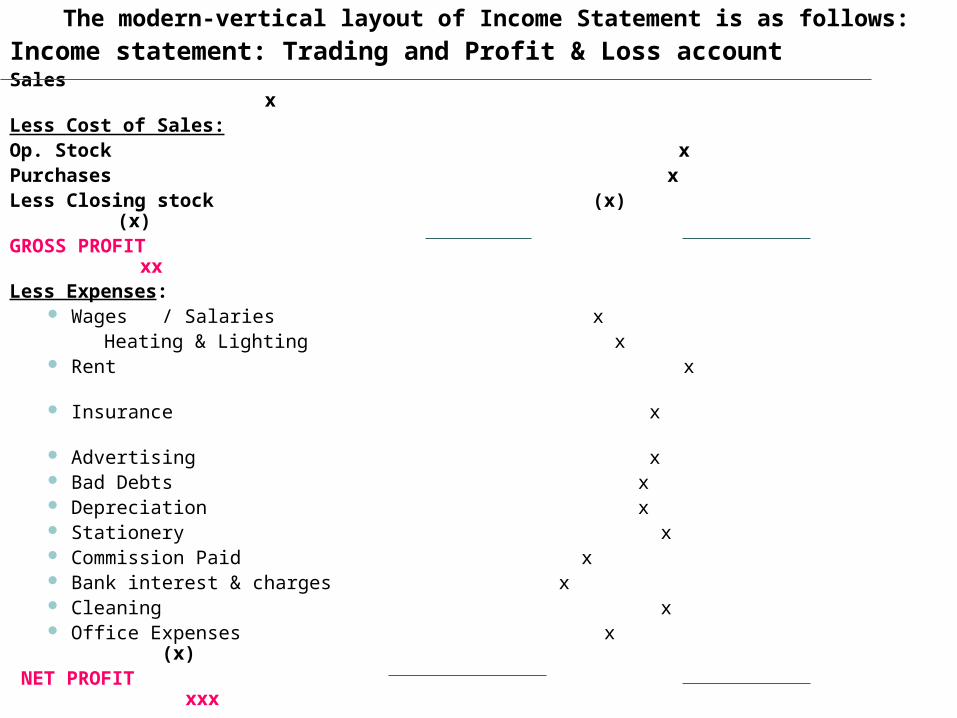

The modern-vertical layout of Income Statement is as follows:

Income statement: Trading and Profit & Loss accountSales xLess Cost of Sales:Op. Stock xPurchases xLess Closing stock (x) (x)GROSS PROFIT xxLess Expenses:

Wages / Salaries x Heating & Lighting x Rent x Insurance x Advertising x Bad Debts x Depreciation x Stationery x Commission Paid x Bank interest & charges x Cleaning x Office Expenses x (x)

NET PROFIT xxx

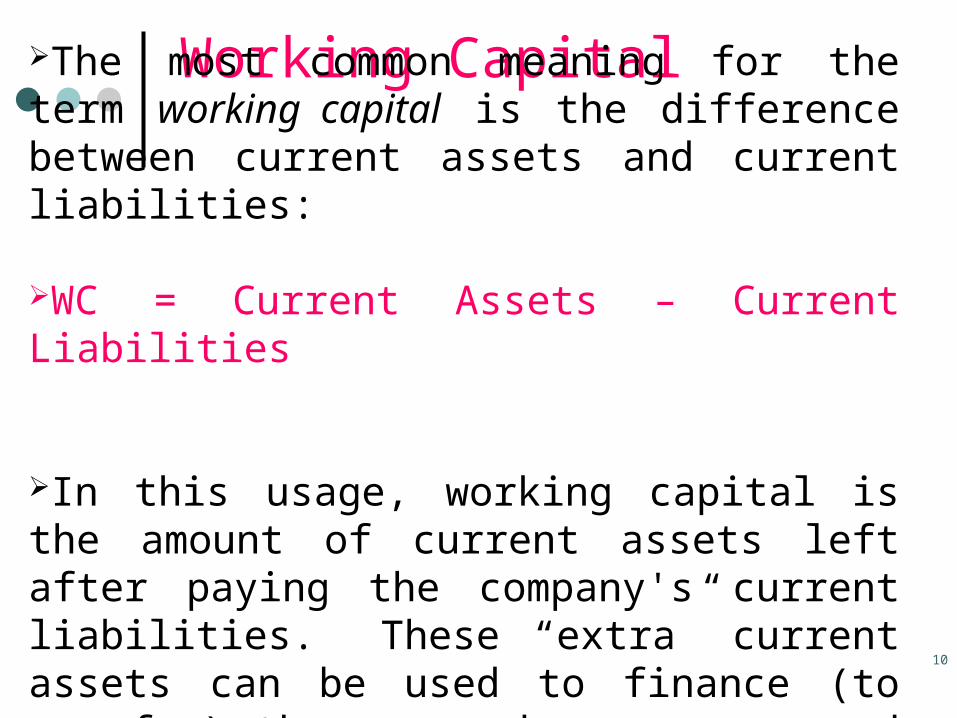

Working Capital

The most common meaning for the term working capital is the difference between current assets and current liabilities:

WC = Current Assets – Current Liabilities

In this usage, working capital is the amount of current assets left after paying the company's current liabilities. These “extra” current assets can be used to finance (to pay for) the every day expenses and needs of the company.

10

Why is important to calculate working capital?

Because it is important to check if we have enough current assets to pay current liabilities.

Business need cash to continue working and to pay for the day-to-day operations. Also it needs cash to pay unexpected expenses and working capital amount must be enough to respond to this situation of unexpected events. It answers the question: Does the business has enough cash to pay the bills?

11

12

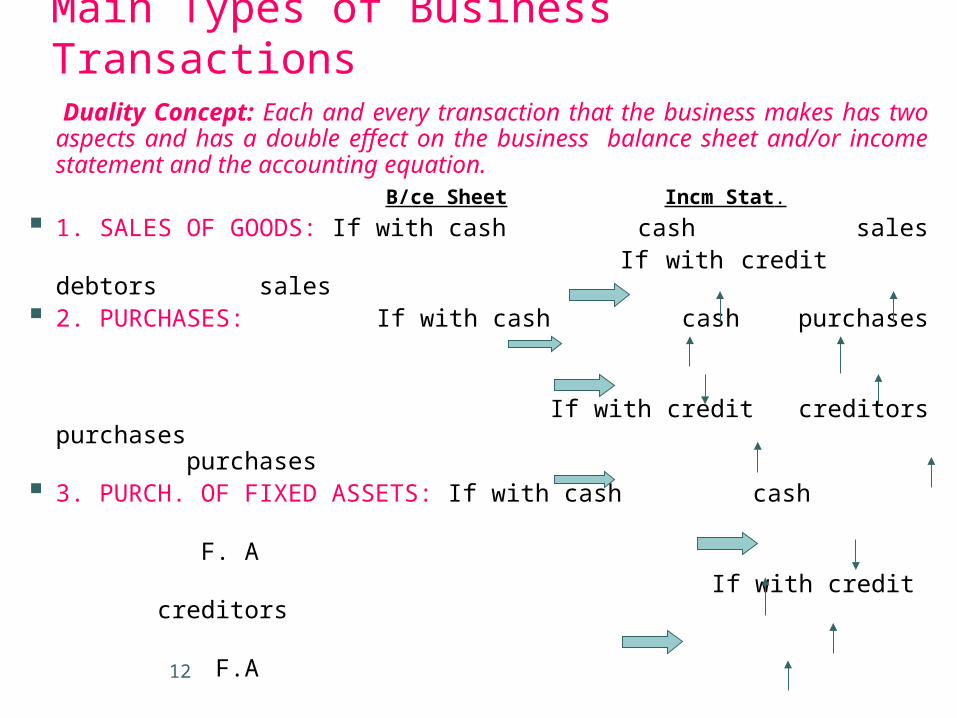

Main Types of Business Transactions

Duality Concept: Each and every transaction that the business makes has two aspects and has a double effect on the business balance sheet and/or income statement and the accounting equation.

B/ce Sheet Incm Stat.

1. SALES OF GOODS: If with cash cash sales If with credit debtors sales 2. PURCHASES: If with cash cash purchases If with credit creditors purchases

purchases 3. PURCH. OF FIXED ASSETS: If with cash cash F. A If with credit creditors F.A

13

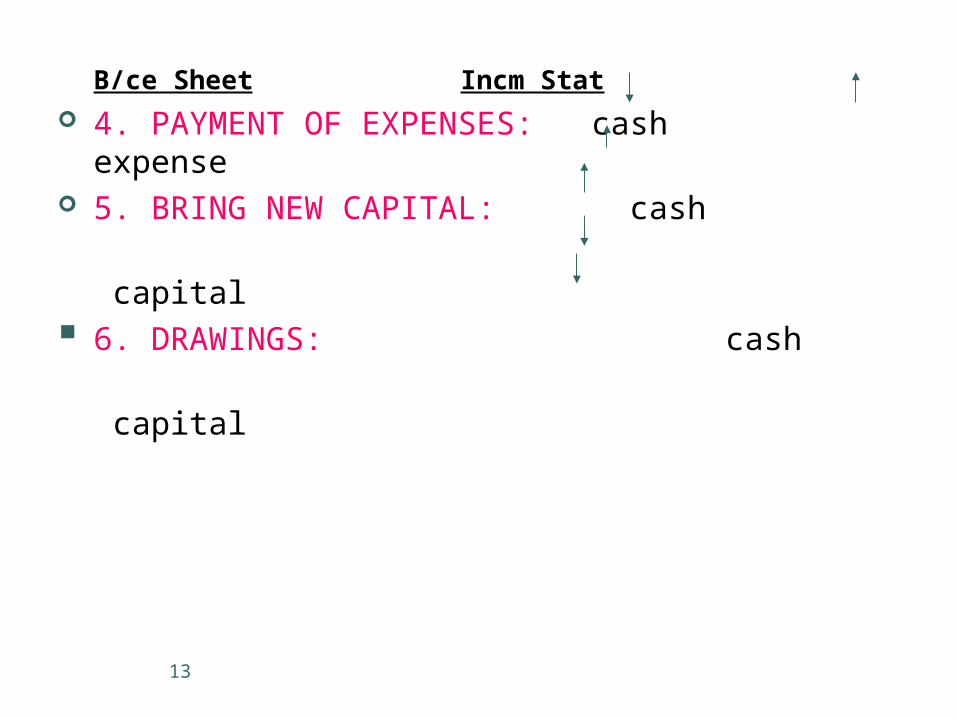

B/ce Sheet Incm Stat

4. PAYMENT OF EXPENSES: cash expense 5. BRING NEW CAPITAL: cash

capital 6. DRAWINGS: cash

capital

Exercise A company does a lot of transactions every

day and thus is impossible to prepare a balance sheet after every new transaction. Balance sheet is prepared at the end of each year.

In order to follow and update the change of accounting items in Balance sheet and Income statement, during a year, we record the transactions and changes into accounts in chronological order. Then, at the end of the year, we prepare the two financial statements.

14

15

Learning Objectives: Part B

What are accounts and what is the ledger? Understand the principles of double entry. Be familiar with the recording of different

transactions Balancing off the ledger accounts. Be familiar with the trial balance Be able to solve exercises.

16

Accounts and Ledger

ACCOUNT is a table in T- shape which records chronologically the changes caused by the trade transactions that a business proceeds in an item of the assets, liabilities or capital.

All Accounts are kept in a book which is called LEDGER (‘T’ accounts).

There is a ledger account for each asset, liability, revenue and expense item. Ledger accounts are pages in the ledger book with a separate page reserved for each one in order to record transactions.

17

The duality concept and double entry bookkeeping

Each account has two sides - the debit (Dr) and credit (Cr) sides.

Dr Name of Account Cr Date Description € Date Description €

18

The duality concept and double entry bookkeeping

Each transaction that a business realize affects the financial statements in two ways.

These two effects are equal and opposite so as the accounting equation will be always satisfied.

Assets = Liabilities + Capital Double Entry Rule: For every debit there is a credit and for every

credit there is a debit.

Each transaction will affect at least two accounts: ‘the one will be debited and the other will be credited’

19

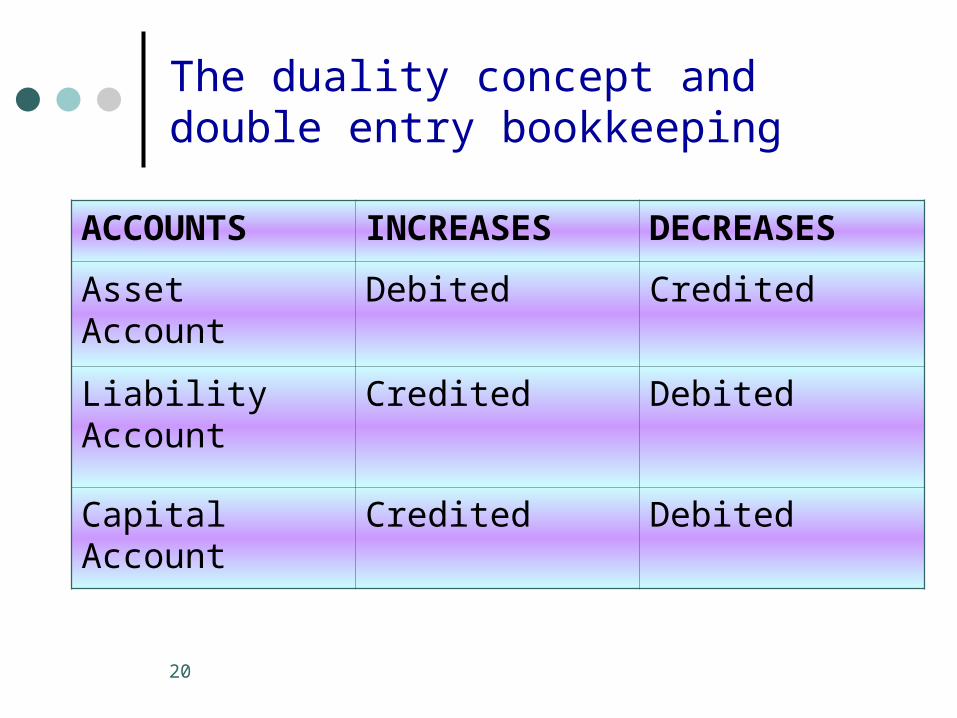

The duality concept and double entry bookkeeping

Whether an entry is to the debit or credit side of an account depends on the type of account and the transaction:

The Asset Accounts are debited when an increases of asset occurs and are credited when a diminish of asset occurs.

The Liability and Capital Accounts are credited when an increase of liability occurs and are debited when a reduce of liability occurs.

20

The duality concept and double entry bookkeeping

ACCOUNTS INCREASES DECREASES

Asset Account Debited Credited

Liability Account Credited Debited

Capital Account Credited Debited

21

The duality concept and double entry bookkeeping

SUMMARY OF STEPS TO RECORD A TRANSACTION Identify two items that are affected. Consider whether they are being increased or

decreased. Decide whether each account should be debited

or credited. Check that a debit entry and a credit entry have

been made and they are both for the same amount.

22

TRADE TRANSACTIONS 1. Recording Cash Transactions

Cash transactions are those where payment is made or received immediately.

Double Entry in the bank ledger is as follow:

A debit entry is where funds are received.A credit entry is where funds are paid out.

23

Credit sales and purchases are transactions where goods or services change hands immediately, however payment is not made right away but in some time in the future.

Money that a business is owned is recorded in the receivables or Debtor ledger account.

Money that a business owes is recorded in the payables or Creditor ledger account.

TRADE TRANSACTIONS 2. Recording Credit Sales and Purchases

24

TRADE TRANSACTIONS 3. Recording Sales and Purchases Returns

It is normal for customers and a business to return unwanted goods to a business or the supplier respectively.

The double entries arising will depend upon whether the returned goods were initially

purchased on credit or cash.

Originally a credit transactions

Originally a cash transactions

Sales Returns (returns inwards)

Dr Sales Returns Cr Receivables/ Debtors

Dr Sales ReturnsCr Cash

Purchases Returns(returns outwards)

Dr Payables/ CreditorsCr Purchases Returns

Dr CashCr Purchases Returns

25

CASH DISCOUNTS Discounts may be given in the case of credit

transactions in order to encourage quick payment. For example a cash discount of 3% is offered to any customers who pay within 14 days.

A business may give its customer a discount - known as Discount Allowed.

A business may receive a discount from a supplier – known as Discount Received.

TRADE TRANSACTIONS 4. Recording Discounts

26

Recording Discounts

Discount Allowed Dr Discount Allowed (expense) X Cr Debtors / Receivables X

Discount allowed is treated as all other expenses in the Profit and Loss Account

Discount Received Creditors / Payables X Discount Received (income) X

The income is shown beneath gross profit in the Profit and Loss Account

TRADE DISCOUNTS Is given from the person who sells to the

person who buys at the time of deal and is deducted immediately from the amount of the transaction so it doesn’t recorded in the books (only in the invoice).

Example page 44 of the book ‘Practical Book Keeping Level 1’.

27

28

cashCapital 10000 Purchases 200

Sales 250 Rent 150

B/ce c/d 9900

10250 10250

B/ce b/d 9900

Balancing off a statement of financial position ledger account

1.Total both sides of the T account and find the larger total. In the example the larger total is in debit side.

2.Put the larger in the total box on the debit and credit side.

3.Calculate the difference between the large side and the small side and set the figure in the small side naming it Balance c/d (carried down)

4.Carry the balance down diagonally and call it “balance b/f” (brought forward)

29

At the year end, the ledger accounts must be closed off and transfer the balances in the next accounting period.

Balancing the account will result in: A balance c/f (being the asset / liability at

the end of the accounting period).

equals A balance b/f (being the asset / liability at

the start of the next accounting period).

Balance c/d = Balance b/d

30

The following accounts are closing off and they are not transferring a balance to the next accounting period:

1. Expenses accounts and Purchases account

2. Income accounts (e.g. sales, discounts received)

Instead they are transferring the balancing figure on the

smallest side at the Income statement (depending if it goes

to trading a/c or profit & loss a/c)

LEDGER ACCOUNTS THAT ARE TRANSFERING AT THE

INCOME STATEMENT DO NOT HAVE AN OPENING BALANCE

WHY PURCHASES,SALES AND EXPENSES ARE NOT TRASFERING TO NEXT YEAR?

Because every year I must find the NET PROFIT concerning that year – or that specific accounting period so I have to use the purchases and income and expenses of that period not of the previous year because if I do this the result (net profit) will be wrong since it will be based on the data of the previous year. I have to use the data (purchases , income, expenses) of the year (accounting period) which I study.

31

32

CAPITAL ACCOUNT

At the start of the next accounting period the capital account will have an opening balance, i.e. A balance b/f equal to the amount that is owed to the owner at the start of that period.

This amount is equal to what was owed to the owner at the start of the previous period, plus any capital that the owner introduced in the period, plus any profits earned in the period less any drawings taken out in the period.

Therefore we transfer the balance of the Income Statement -profit or loss- and the balance on the drawings account to the capital account at the end of the period so that it will have the correct opening balance at the start of the next.

33

Capital AccountLoss for the year x B/ce b/d x

Drawings x Net Profit x

B/ce c/d x Cash injections x

x x

B/ce b/d x

34

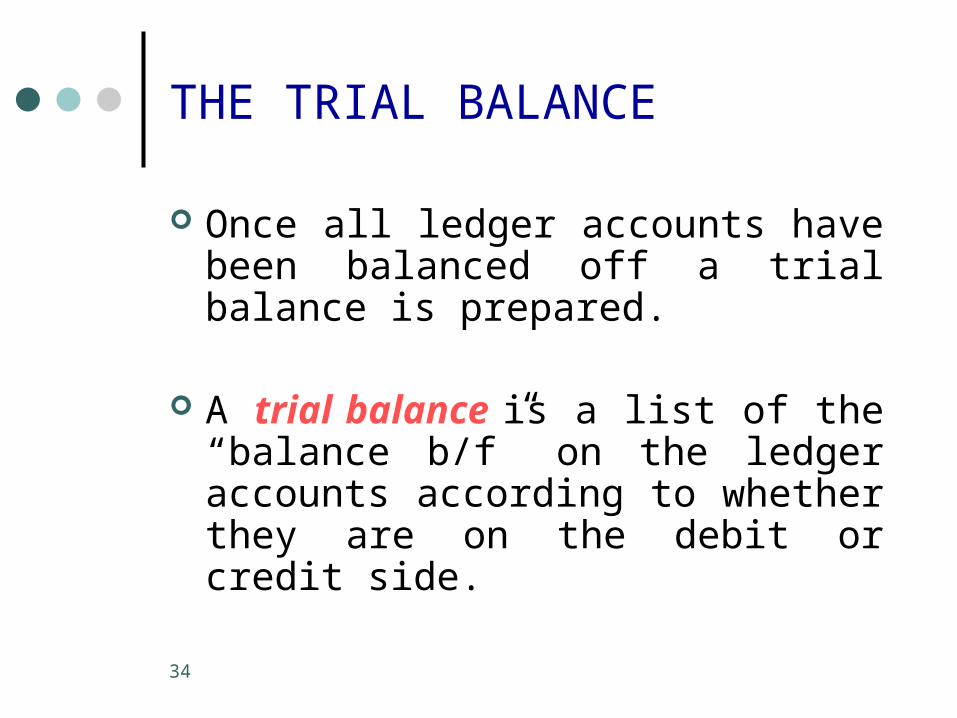

THE TRIAL BALANCE

Once all ledger accounts have been balanced off a trial balance is prepared.

A trial balance is a list of the “balance b/f” on the ledger accounts according to whether they are on the debit or credit side.

35

The purpose of a trial balance is:

To check that for every debit entry made, an equal credit entry has been made since the total amount of the two columns must be equal.

As a first step in preparing the financial statements.

Note that a number of adjustments will be made after the trial balance is extracted. These adjustments do not therefore appear in the trial balance.

36

Exercises