1 “new federal initiatives on enforcement” michael brustein brustein & manasevit 3105 south...

TRANSCRIPT

1

“New Federal Initiatives on Enforcement”

Michael BrusteinBrustein & Manasevit

3105 South Street, NWWashington, DC 20007

NACTEI

Pre-Conference May 16, 2006Palm Springs, CA

2

SEAs must use a risk-based plan to assess and monitor all LEAs to ensure that they have systems in place to properly account for, and adequately document and support, claims submitted for reimbursement.

-OIG

3

SEAs must ensure that monitoring teams include financial personnel to look at financial issues and check for compliance with financial requirements.

-OIG

4

Significant Cultural Shift at ED to “Internal Controls”

5

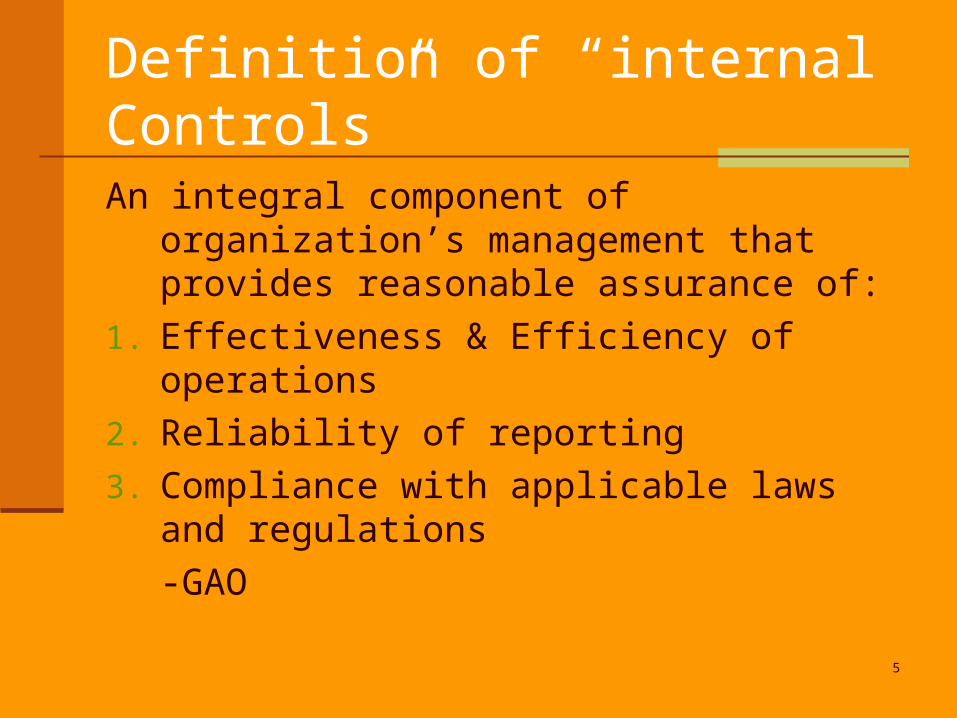

Definition of “internal Controls”

An integral component of organization’s management that provides reasonable assurance of:

1. Effectiveness & Efficiency of operations

2. Reliability of reporting

3. Compliance with applicable laws and regulations

-GAO

6

States and locals scheduled for monitoring from now on can expect much closer examinations of financial records

7

Such financial records must detail:

1. Flow of funds to locals

2. Audit findings and corrective action plans

3. Procurement, distribution, equipment

-James Evans

OCFO

8

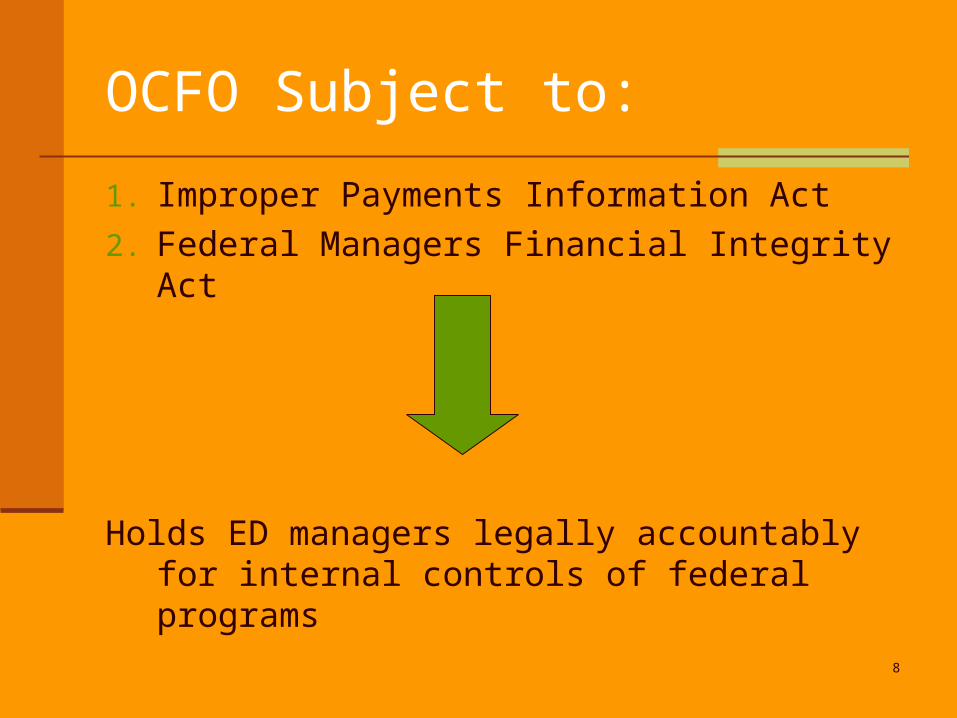

OCFO Subject to:

1. Improper Payments Information Act

2. Federal Managers Financial Integrity Act

Holds ED managers legally accountably for internal controls of federal programs

9

OCFO now assesses the risk that federal funds are being spent erroneously.

OCFO ensures effective internal controls are in place and adhered to at the state and local level

10

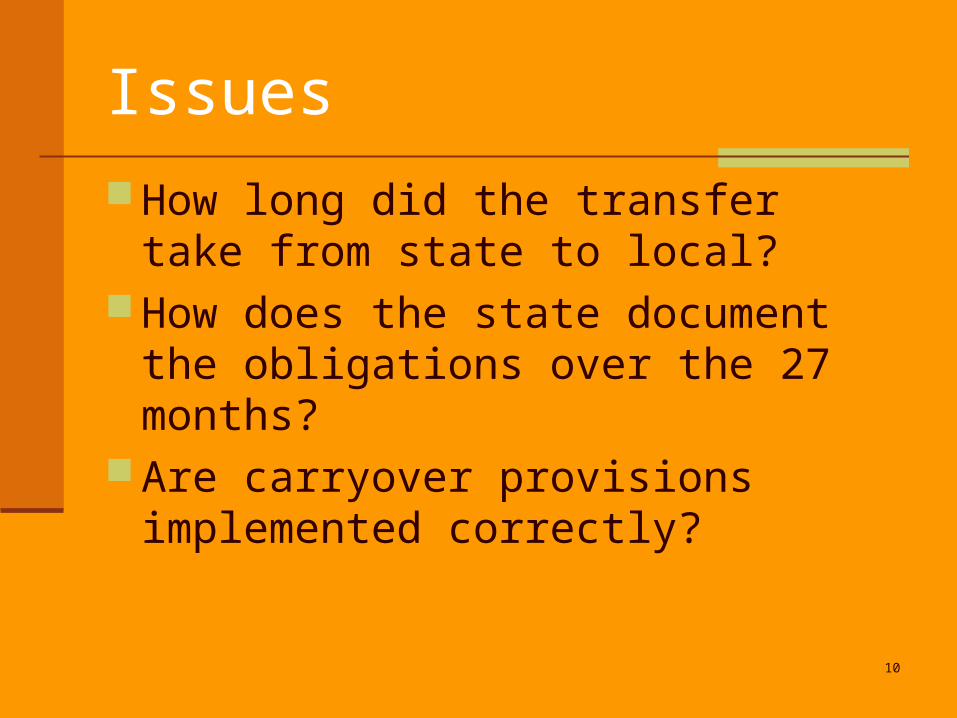

Issues

How long did the transfer take from state to local?

How does the state document the obligations over the 27 months?

Are carryover provisions implemented correctly?

11

How well does the state monitor corrective action plans developed in response to audits?

12

Equipment

16 of 17 states and districts visited did not maintain accurate equipment inventory

13

Equipment

OCFO will select a piece of equipment from inventory list and then see if they can find it.

14

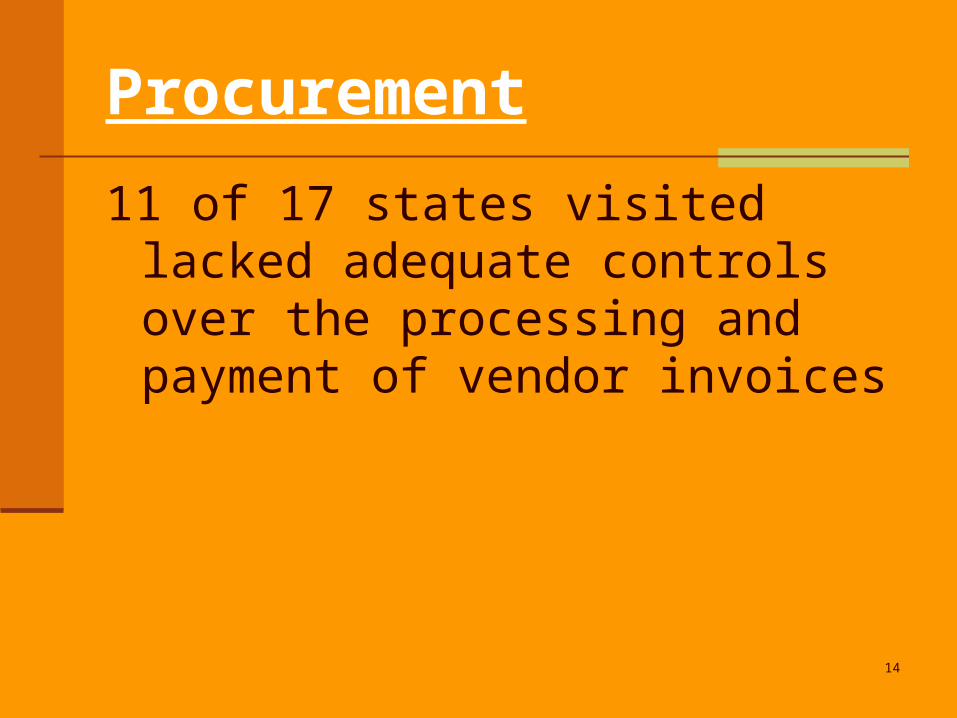

Procurement

11 of 17 states visited lacked adequate controls over the processing and payment of vendor invoices

15

2006 OIG Workplan

1) SEA monitoring of LEAs

16

Audits

Corrective action plans to address audit findings in the A-133 single audit reports were either unavailable for review, improperly prepared, or prepared in an untimely manner (8)

Management and internal control letters addressing A-133 and financial statement audit reports were unavailable for review (2)

No documentation provided to indicate that A-133 audits had been conducted or copies were not available for review (2)

17

Procurement & Disbursement Controls

Inadequate controls over purchase orders (13) Inadequate controls over processing and payment of

vendor invoices (11) Lack of adequate controls over the distribution of Title

I finds by SEA and/or LEA (10) Inadequate controls over funds distribution

documents (FDDs) and P638 draw down forms (4) Inadequate controls over SEA/LEA contracts issued

to vendors (3) Inadequate controls over travel advances and travel

payment vouchers (3)

18

Inadequate documentation to demonstrate proper application of indirect cost principles (2)

Lack of documentation for the approval function in an automated procurement system (2)

Lack of supporting documentation for journal entries (2)

Lack of documented competitive bidding process (1) Lack of documentation to support use of Title I funds

for payroll (1) Inadequate controls over the purchase card process

(1) Student lunch applications used for eligibility not

complete (1)

Procurement & Disbursement Controls cont…

19

Equipment Title I equipment inventory not available (16) Lack of adequate controls to account for

location and custody of Title I equipment (7) No property tags on equipment (3) The capitalization threshold for Title I

equipment exceeds $5,000 (2) Inadequate procedures for recording the

transfer of Title I equipment (2) Inadequate controls to ensure that Title I

funds are not used to purchase equipment for the exclusive use of other programs (1)

20

A-133 Common Audit Findings

1. Cash Management Minimize time elapsing between

drawing down federal cash and disbursing it.

21

2. Property records 80.32(d)(1)Make sure all required data elements are maintained1. Description of the property

2. Identification number

3. Source of property

4. Who holds the title

5. Acquisition date

6. Cost

7. Percent of federal participation

8. Location of the property

9. Use & condition of the property

10. Ultimate disposition- Date of disposal Sale price

22

3. Equipment Inventory

Inventory all equipment purchased with federal funds at least once every two years

Control system to safeguard against loss or damage

23

4. Noncompetitive Procurement

If contracts awarded on a sole source basis, prepare a written justification, e.g. emergency no responses to solicitation

24

5. Obtain Prior Written Approval

If grant agreement states that an administrative act requires prior approval, make sure you get it in writing from the grantor agency.

25

6. Timely Accurate Financial & Performance Reports

Late or inaccurate reports are a “red flag” of weakness in the system –

often invites greater scrutiny.

26

7. Cost Transfers

Shifts of costs between programs invites audit scrutiny.

-Supplanting

-Allocability

27

8. Time & Effort Reports

This is the most frequently cited violation.

28

THE KEY:Aligning Effort and Funding

29

Audit inquiries may commence with focus on funding side (federal grants received) or effort side (payroll distribution records or P.D.’s)

30

Attendance Records are NOT the Equivalent of Effort Records

31

A-87 / A-21

Distribution of salaries must be based on payrolls documented in

accord with the generally accepted practices of the agency.

32

There is no single best method for documenting the distribution of effort

.

33

But the method must recognize the principle of “after-the-fact” confirmation, so that charges to a grant reflect actual charges.

Budgets do not reflect actual charges.

34

Confirmation must be done by employee under A-87 or “responsible person with suitable means of verification” under A-21

35

While charges may be made initially on the basis of estimates before the services are performed, changes in the work activity must be entered into the payroll distribution system.

36

Where employees are expected to work solely on a single cost objective, salaries must be supported by semi-annual certification signed by employee or supervisor.

37

Where employees work on more than one cost objective, use either PARS or substitute systems

38

Elements of PARS

1. After the fact distribution of actual activity of each employee

2. Account for total activity for which employee is compensated

3. Prepared at least monthly

4. Signed by the employee

39

Questions on Time and Effort

Is the distinction between single or multiple cost objectives based on how

employees are paid?NO!

40

Questions on Time and Effort cont…Questions on Time and Effort cont…

If employee is paid with nonfederal funds, but effort is counted toward a match, are T/E

records required?YES!

41

Questions on Time and Effort cont…Questions on Time and Effort cont…

What if the employee works only a brief time on an activity unrelated to

the federal cost objectives?

42

If deviations between budget estimates and actual costs are less than 10% are adjustments required?

43

Questions on Time and Effort cont…Questions on Time and Effort cont…

If the employee works on an activity that is allowable under more than one

program, must the time be allocated?

NO!

44

Substitute Systems

1. Lamar Alexander Guidance 1992

2. The Florida, North Carolina, Michigan Models

45

Substitute Systems

1. Account for actual effort weekly for three representative months;

2. Actual effort is within 10% of projected effort;

3. Regardless of deviation, adjustments required;

4. Then account for effort weekly for two representative months;

5. Adjustments required.

46

Substitute Systems

1. ED approves SEA process

2. SEA approves LEA process

3. LEA may use substitute system even if SEA does not

47

Consequences for Legally Deficient System

48

Reconstruction of Documents

Not a substitute for contemporaneous records

But often accepted by OALJ on appeal

49

Reconstruction

Affidavits of employees with first hand knowledge

Work product Calendars Schedules

50

Where to Find Federal Education Grants Management Requirements

Program Rules: www.ed.gov Statutes Regulations Guidance

General Education Provisions Act (GEPA): http://straylight.law.cornell.edu/uscode/html/uscode20/usc_sup_01_20_10_31.html

Education Department General Administrative Regulations (EDGAR): http://www.ed.gov/policy/fund/reg/edgarReg/edgar.html

51

Where to Find Federal Education Grants Management Requirements Office of Management & Budget Circulars

http://www.whitehouse.gov/omb/circulars/ OMB Circulars A-21, A-87, A-122 Cost

Principles OMB Circular A-133 Single Audit OMB Circular A-133 Compliance Supplement

Note – for audits performed after June 30, 2004, must look at 2004 AND 2005 Supplements

52

Federal Cost Principles

53

Federal Cost Principles

A-21 Educational Institutions

A-87 State, Local & Indian Tribal Governments

A-122 Non-Profit Organizations

48 CFR pt. 31 For-Profit Organizations

54

Cost Principles: Basic GuidelinesAll Costs Must Be:

Necessary ReasonableAllocableLegal under state and local law

55

Cost Principles: Basic Guidelines In addition, all costs must:

Conform with federal law & grant termsConsistently treated In accordance with GAAPNot included as matchNet of applicable creditsAdequately documented

56

Basic Guidelines (cont.)

Adequately documented Amount of funds under grant How the funds are used Total cost of the project Share of costs provided by other sources Records that show compliance Records that show performance Other records to facilitate an effective audit

57

A-87, Attachment B– Selected Items of Costs

43 specific costs detailedListed in alphabetical order

58

EDGAR Overview Education Department General Administrative

Regulations: 34 CFR pts. 74-99 Part 74: Admin. of Grants to Institutions of

Higher Ed, Hospitals, and other Nonprofit Organizations

Part 75: Direct Grant Programs Part 76: State-Administered Programs Part 77: Definitions Part 80: Uniform Administrative

Requirements for Grants and Cooperative Agreements to State and Local Governments

59

Financial Management34 CFR 80.20 & 34 CFR 74.21 Fiscal control and

accounting procedures must be sufficient to: Prepare reports Trace funds to a level

of expenditure adequate to show funds spent properly

60

Matching/Cost Sharing34 CFR 80.24 & 34 CFR 74.23 Costs must be allowable under the grant Includes:

Grantee expenditures (cash contribution)

Donations (in-kind contribution) Must be verifiable from records

61

Program Income34 CFR 80.25 & 34 CFR 74.24Income directly generated by a grant supported

activity or earned only as a result of the grant agreement, includes income from:

Fees for services performed Use of property acquired under grant Sale of commodities or items fabricated

under a grant agreement Payments of principal and interest on

loans made with grant funds

62

Program Income – cont.RoyaltiesGenerally, revenue from:RoyaltiesLicense feesPatents

Is not considered program income unless specifically identified in the grant agreement

63

Use of Program Income

Deducted from total allowable costs and used for allowable expenses

Added to the total grant award and used for allowable expenses

Used to meet cost sharing or matching requirements

64

Changes to Approved Budget34 CFR 80.30 & 34 CFR 74.25 Must report deviations from

budget and program plans Must request prior approval:

Change in scope or objective

Change in key personnel Authority to bring in 3rd party

contractor Certain budget transfers

65

EDGAR Part 80.36 Procurement

Competition 80.36(c). All procurement transactions must be conducted with

full and open competition.

66

Equipment34 CFR 80.32 & 34 CFR 74.34 Title vests in the grantee May use for other

projects as long as no interference

Must ensure adequate maintenance

67

Equipment (cont.)

Property acquired under the grant must be recorded in an inventory management system Property records (description, serial number or

other ID, title info, acquisition date, cost, percent of Federal participation, location, use and condition, and ultimate disposition)

Physical inventory (at least every two years) Control system to prevent loss, damage, theft

(all must be investigated)

68

Disposition When no longer needed:

Property may be used for other activities currently or previously supported with federal funds

Otherwise, must dispose according to regulations34 CFR 80.32(e)

69

Copyrights34 CFR 80.34 & 34 CFR 74.36 Grantee may copyright work that was

developed for or purchased under federal grant

Federal government may reproduce, publish, or otherwise use the copyright in any work developed under the grant

Federal government does not need to pay royalties

70

Record Retention34 CFR 80.42 & 34 CFR 74.53 Must retain records that show:

Amount of funds under by grant or subgrant How the state or subgrantee uses funds Total cost Share of costs provided from other sources Compliance with program requirements Other records to facilitate and audit

Federal: 3 years Statute of limitations: 5 years

71

Cash Management Requirements

72

Period of Availability34 CFR 80.23 & 34 CFR 74.28 Tydings Amendment

Does not apply to all grants Funds are available to state for 27 months:

15 months under the grant award (July 1, 2005 – September 30, 2006)

Plus 12 months (October 1, 2006 – September 30, 2007)

State may limit period of availability! Check award notice

73

Definition of Obligation Under Federal Law

Acquisition of Property Date of binding

written commitment

Personal Services

by Employee

When services

are performed

Personal Services

by Contractor

Date of binding

written commitment

Travel When travel is taken

74

Liquidations Federal regulations: Must liquidate all obligations

within 90 days after the end of the period of availability Example:

Period of availability: July 1 – September 30 Liquidation period ends: December 30

ED may extend this deadline State may limit the period!

Check award notice

75

“Lapsing” of Perkins Funds

Sclafani September 2, 2005 memo

76

Supplement, Not Supplant

77

Supplement Not Supplant

Cannot use federal funds to pay for services, staff, programs, or materials that would otherwise be paid with state or local funds

Always ask: “What would have happened in the absence of federal funds?”

78

Supplement Not Supplant (cont.) A-133 Compliance Supplement presumes

supplanting in 3 situations:1. Used federal funds to provide services the

SEA or LEA is required to make available under other federal, state or local laws

2. Used federal funds to provide services the SEA or LEA provided with state or local funds in the prior year

79

Supplement Not Supplant (cont.)

Presumption may be rebutted: If SEA or LEA

demonstrates it would not have provided the services with state or local funds if the federal funds were not available

80

Questions???

81

This presentation is intended solely to provide general information and does not constitute legal advice. Attendance at the presentation or later review of these printed materials does not create an attorney-client relationship with Brustein & Manasevit. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar with your particular circumstances.