1 (of 32) fin 200: personal finance topic 12-auto and homeowner’s insurance lawrence schrenk,...

Post on 19-Dec-2015

215 views

TRANSCRIPT

1 (of 32)

FIN 200: Personal Finance

Topic 12-Auto and Homeowner’s Insurance Lawrence Schrenk, Instructor

2 (of 32)

Learning Objectives

1. Discuss the general types of insurance. ▪

2. Explain the general features of auto insurance.

3. Explain the general features of home owners insurance.

4. Calculate annuities with non-annual payments.▪

4 (of 32)

Selected Types of Insurance

Don’t Forget: Expatriate Insurance, Pet Insurance, Kidnap and Ransom Insurance, Terrorist Insurance, etc...

5 (of 32)

Terminology

Risk Management Insurance–Financial Contract...

That redistributes costs of financial losses, or in which one party compensates another party for

losses Insurer versus Insured Premium

6 (of 32)

The Insurer

Profit Revenue

Earned Premium Investment Income

Costs Incurred Loss Underwriting Expenses

Diversification of Risk Captive versus Independent Agents

7 (of 32)

Insurer Issues

Moral Hazard–Possibility that someone insured will act differently, i.e., to the detriment of the insurer, than when uninsured. If your apartment is insured against theft then

there is less incentive to be security conscious. Insurance changes our behavior.

Insurance Fraud

8 (of 32)

The Insured The Psychological Bases of Finance

Greed Risk Aversion

Income

Smoothing Can’t insure

against

everything.

Income Patterns

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

Ye

ar

1

Ye

ar

2

Ye

ar

3

Ye

ar

4

Ye

ar

1

Ye

ar

2

Ye

ar

3

Ye

ar

4

Ye

ar

1

Ye

ar

2

Ye

ar

3

Ye

ar

4

A B C

9 (of 32)

The Effect of InsuranceThe Effect of Insurance

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

Year1

Year2

Year3

Year4

Year5

Year6

Year7

Year8

Year9

Year10

Expected

Actual

Insured

11 (of 32)

Policy

Who’s Covered People Vehicle

Coverage Dollar limits Dates

Policy/Binder Number

12 (of 32)

Coverage: Liability

Bodily Injury Caused by Insured Parties Medical and Lost Wages Limits

Individual (recommended minimum $100,000) Total (recommended minimum $400,000) You are liable above limits

Property Damage Recommended minimum $50,000

State Requirements DC 25/50/10

13 (of 32)

Coverage: Medical Payments

Bodily Injury To Those in Insured Vehicle Recommended minimum $10,000 Distinguish from Regular Health Insurance

14 (of 32)

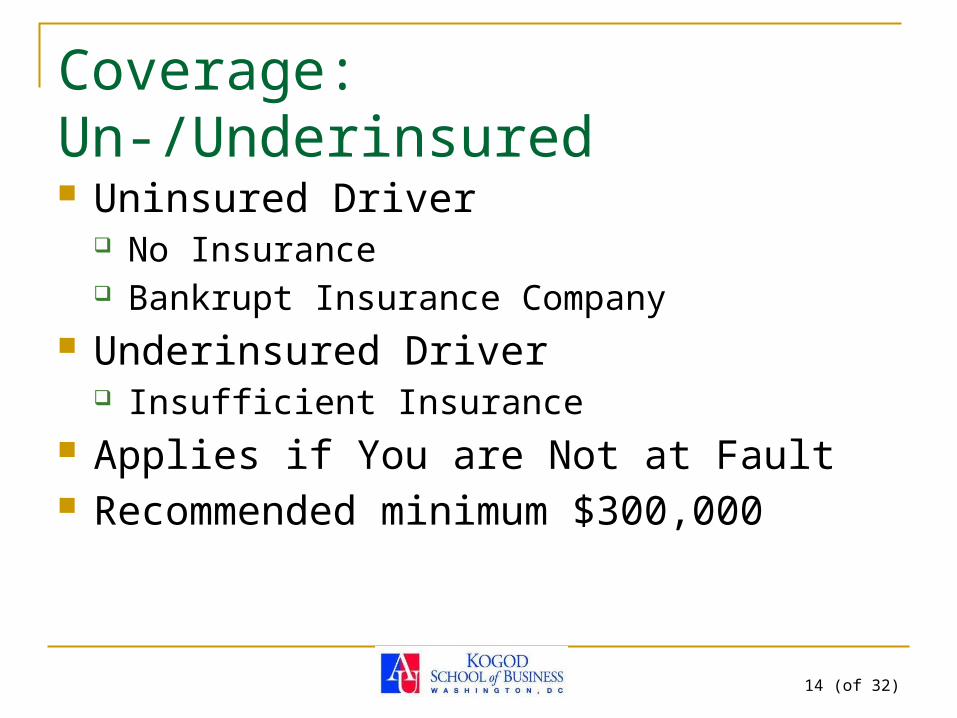

Coverage: Un-/Underinsured

Uninsured Driver No Insurance Bankrupt Insurance Company

Underinsured Driver Insufficient Insurance

Applies if You are Not at Fault Recommended minimum $300,000

15 (of 32)

Coverage: Collision and Comprehensive Collision

Damage to your car when you are at fault Comprehensive

Various damages to you car Flood, fire, theft

Optional May be required by lender

Kelley Blue Book Value Normally Maximum Deductable

17 (of 32)

Coverage Types

Coverage A–Residence Coverage B–Detached Structures Coverage C–Personal Property Coverage D–Added Living Costs Coverage E–Personal Liability Coverage F–Medical Payments

18 (of 32)

Coverage A–Residence

Repair/Replacement of Home Possible Causes or Loss

Fire, Tornado, etc. Land not included Two Suggestions

Insure for 100% of full replacement cost Don’t be underinsured.

19 (of 32)

Coverage B–Detached Structures

Generally 10% of coverage A Possible Applications

Garage Barn In-Ground

Excludes structures used for business.

20 (of 32)

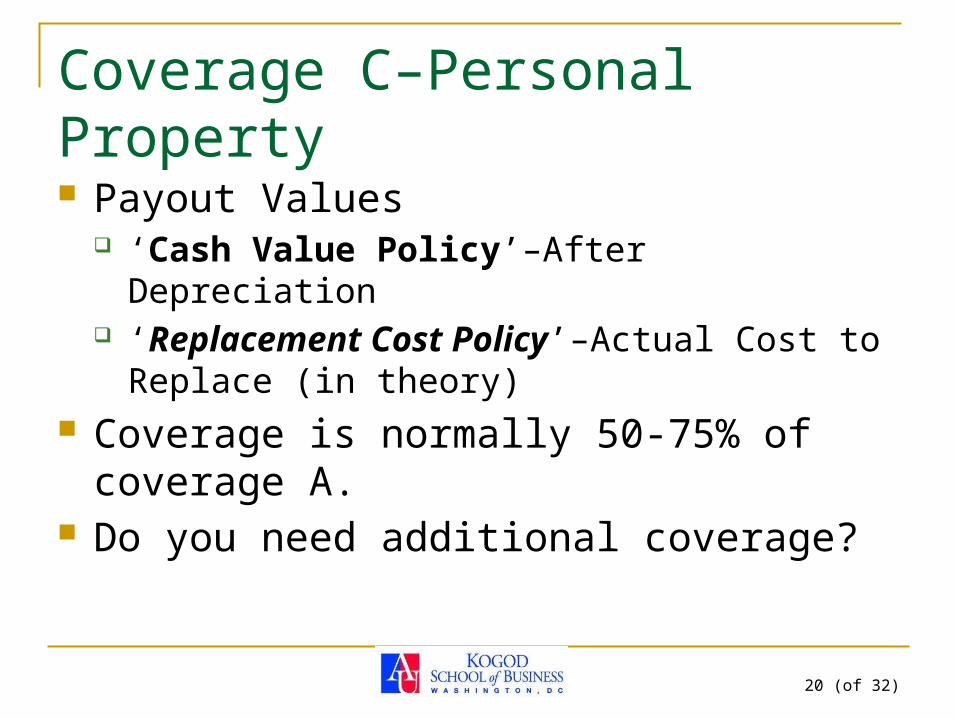

Coverage C–Personal Property

Payout Values ‘Cash Value Policy’–After Depreciation ‘Replacement Cost Policy’–Actual Cost to

Replace (in theory) Coverage is normally 50-75% of coverage A. Do you need additional coverage?

21 (of 32)

Coverage D–Added Living Costs

Home Unlivable due to Covered Loss Additional Living Expenses

New Costs Motels Take-Out Meals

Less Old Costs not Incurred Utilities

Possible Time Limits 12 Month Unlimited

22 (of 32)

Coverage E–Personal Liability

Personal Liability for injuries and property damage you cause.

Two Important Points This is general liability insurance

Not restricted to your property Does not cover vehicular incidents

Covers Lawsuits and your Defense Usually $100,000 included. Do you need more?

23 (of 32)

Coverage F–Medical Payments

Covers a guest hurt on your property. Can duplicate guests own health insurance.

Typical ‘Causes-of-Loss’

Included Fire, lightning, explosion, windstorm or hail,

smoke, aircraft or vehicle damage, riot or civil commotion, vandalism, sprinkler leakage, sinkhole collapse, and volcanic action

Excluded Earthquake, Flood, Faulty maintenance, Damage

from insects or vermin, Wear and tear, gradual damage or deterioration

24 (of 32)

25 (of 32)

Other Issues

Deductible Estimating Coverage Documentation

Photos House-Interior and Exterior, Special Features Personal Property

29 (of 32)

Annuities: Non Annual Payments

30 (of 32)

Non-Annual Payments

We need to incorporate the possibility of non-annual payments into our financial calculations.

Fortunately this is simple... You need to change the payments per year (P/Y) to

12 for monthly payments. NOTE: HP users, your calculator is set to 12 by

default. Then do the problem just as you would for

annual payments.

31 (of 32)

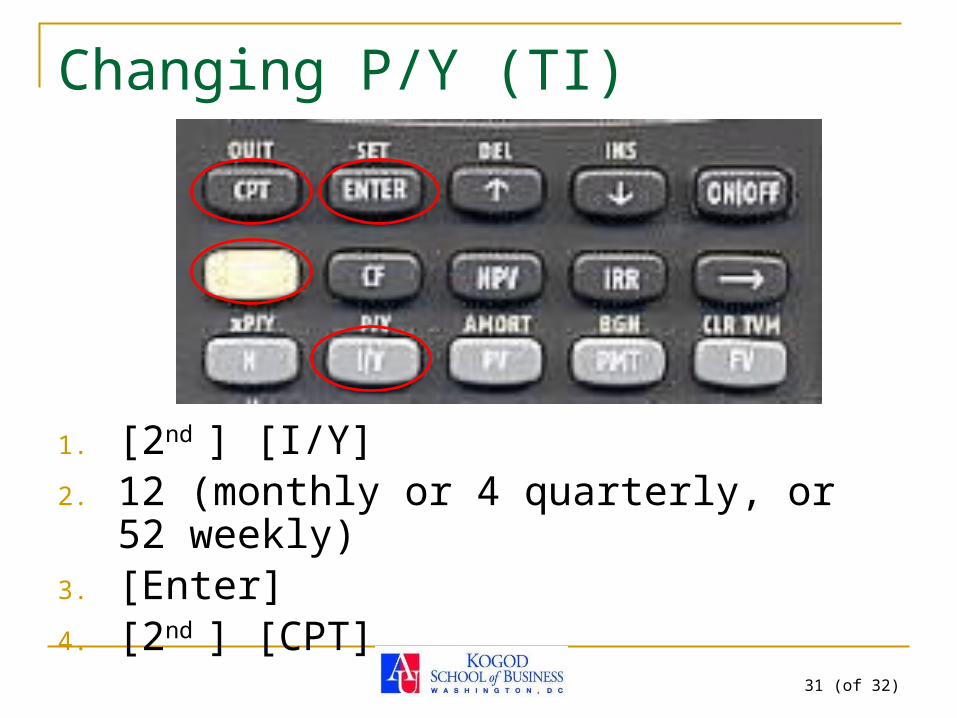

Changing P/Y (TI)

1. [2nd ] [I/Y]2. 12 (monthly or 4 quarterly, or 52 weekly)3. [Enter]4. [2nd ] [CPT]

32 (of 32)

Future Value with a Calculator How much do we have after 3 years if we

save $200 per month beginning next month and the interest rate is 12%?

1. Input 36, Press N (3 x 12 = 36)

2. Input 12, Press I/Y

3. Input 200, press +/-, press PMT (you get -200)

4. Press CPT, FV to get $8,615.38

NOTE: N is the number of periods, so if you save weekly for 2 years, N = 2 x 52 = 104.

33 (of 32)

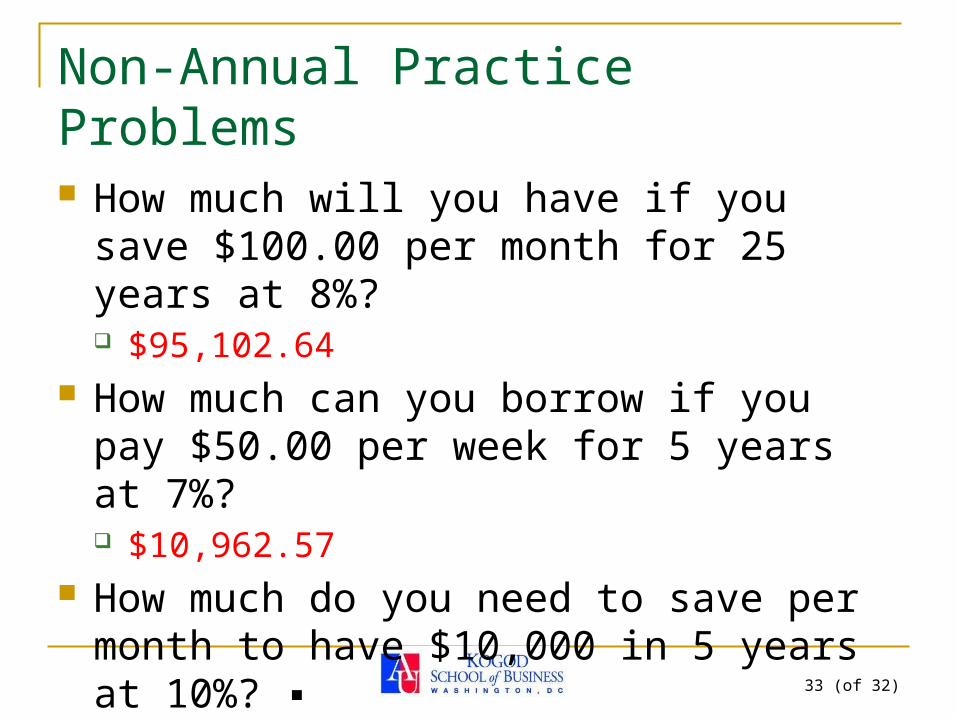

Non-Annual Practice Problems

How much will you have if you save $100.00 per month for 25 years at 8%? $95,102.64

How much can you borrow if you pay $50.00 per week for 5 years at 7%? $10,962.57

How much do you need to save per month to have $10,000 in 5 years at 10%? ▪ $129.14 ▪

34 (of 32)

Ethical Dilemma

You teach personal finance at a local community college. The state in which you teach requires proof of liability insurance in order to renew your license plates. During the discussion of this topic in class, several students admit that they obtain a liability policy just prior to the renewal of their license plates and then cancel it immediately thereafter. They do this because they know that the state has no system for is a following up on the cancellation of the liability policies once the license plates are issued. These students, who are out of work as a result of a local plant shutdown, indicate that they cannot afford to maintain the insurance, but they must have access to cars for transportation. a. Discuss whether you consider the conduct of the students to be

unethical. b. How does the conduct of these students potentially impact other

members of the class who maintain liability insurance on their vehicles?