1 skf half-year results 2015 alrik danielson, president and ceo 15 july 2015

TRANSCRIPT

1

SKF Half-year results 2015Alrik Danielson, President and CEO

15 July 2015

© SKF Group 15 July 2015

2

Highlights - examples of new business in Q2 2015

• United Technologies Corporation, USA Long-term contract Pratt & Whitney Delivery of engine bearings

• ReGen Powertech, India Pitch and yaw bearing sets and mainshaft bearings

• PT. Kereta API Indonesia (Indonesian Railways) Tapered roller bearing units

• Floatel International AB, Sweden Global service agreement including SKF Multilog IMx-M

• Volkswagen, Mexico Wheel hub and MacPherson suspension bearing units

Slide 2

© SKF Group 15 July 2015

3

Highlights

Slide 3

• Completed the divestment of:- Erin Engineering and Research Inc. to Jensen Hughes, a US-based engineering consultancy.- Two filtration businesses, Purafil and Kaydon Custom Filtration, to Filtration Group Corporation, an affiliate of Madison Industries.

• New products:- a smaller version of a shaft alignment tool that it launched earlier in the year, designed to make shaft alignment easy and intuitive.

- an upgraded version of the third generation hub bearing unit, designed to reduce preload, friction and CO2 emissions.

© SKF Group 15 July 2015

4

Highlights – customer awards received

Slide 4

• Awards from SKF distributors:-‘Supplier of the Year’ Motion Industries in Canada and in the

Southeast and Midwest regions of the USA-‘Supplier of the Year in Transmission Imes Dexis, Benelux and Technics 2014’

• ‘Best Supplier Award Year 2014’ Shanghai Hanbell Precise Machinery Co.,

China

• ‘Best Supplier Award’ Shanghai Automobile Gear Works, China

• ‘Best Plant award’ The PSA Group, for SKF’s factories in St Cyr, France and Tudela, Spain.

© SKF Group 15 July 2015

5

Automotive Market profit improvement programme

Clear aim of improving productivity and competitiveness

Three main focus areas:1. Products – Review of product portfolio; emphasis on application-focused

offerings with the specific performance required for the application2. Competitiveness – Improve our overall competitiveness; focus on costs,

manufacturing footprint and process technology3. Vehicle Service Market – Further adapt aftermarket and OEM offerings,

as the design-life of products delivered to OEM customers continues to increase; adapt our aftermarket offering to new reality, ensuring a competitive offer and value proposition for second and third vehicle owners

Actions to run as part of normal business; possible restructuring costs to be communicated as and if they occur

Intention to develop business as part of SKF

Slide 5

© SKF Group 15 July 2015

6

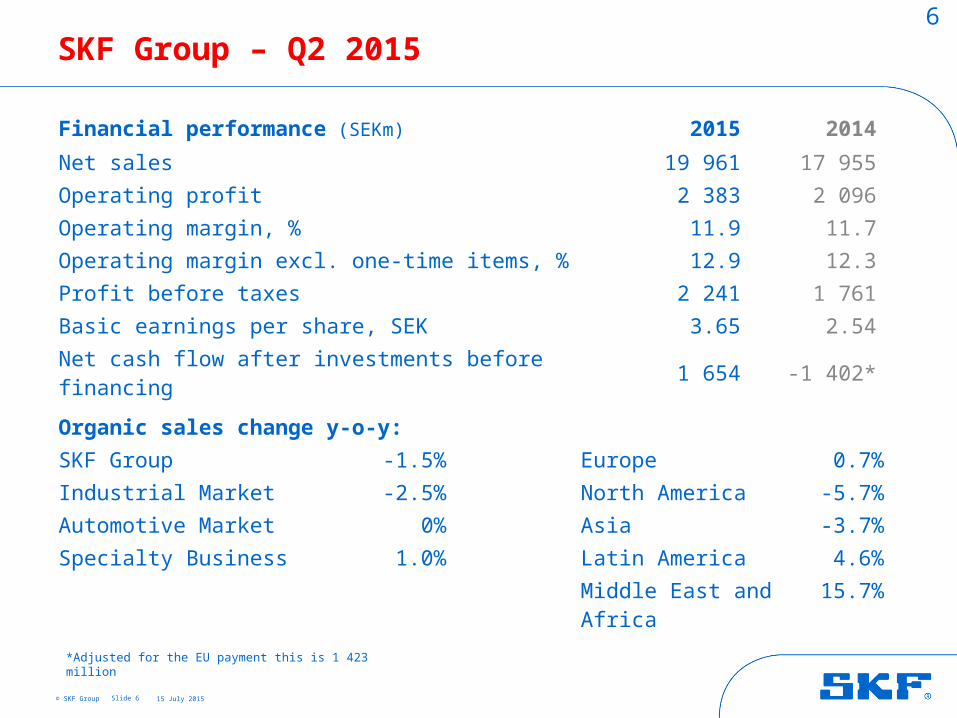

SKF Group – Q2 2015

Slide 6

Financial performance (SEKm) 2015 2014

Net sales 19 961 17 955Operating profit 2 383 2 096Operating margin, % 11.9 11.7Operating margin excl. one-time items, % 12.9 12.3Profit before taxes 2 241 1 761Basic earnings per share, SEK 3.65 2.54Net cash flow after investments before financing 1 654 -1 402*

Organic sales change y-o-y:

SKF Group -1.5% Europe 0.7%

Industrial Market -2.5% North America -5.7%Automotive Market 0% Asia -3.7%

Specialty Business 1.0% Latin America 4.6%Middle East and Africa 15.7%

*Adjusted for the EU payment this is 1 423 million

© SKF Group 15 July 2015

7

SKF Group – Half year 2015

Slide 7

Financial performance (SEKm) 2015 2014

Net sales 39 415 34 689Operating profit 4 104 4 120Operating margin, % 10.4 11.9Operating margin excl. one-time items, % 12.6 11.9Profit before taxes 3 833 3 548Basic earnings per share, SEK 6.11 5.26Net cash flow after investments before financing 2 642 -1 465*

Organic sales change y-o-y:

SKF Group -0.2% Europe 0.8%

Industrial Market -0.6% North America -4.1%Automotive Market 0.3% Asia 0.6%

Specialty Business 0.8% Latin America 1.5%Middle East and Africa 15.0%

*Previously published cash flow information is restated and adjusted for the EU payment this is 1 360 million

© SKF Group 15 July 2015

8

Organic sales growth in local currency

Slide 8

-10

-8

-6

-4

-2

0

2

4

6

8

% changey-o-y

2013 2014 2015

© SKF Group 15 July 2015

9

Organic sales growth in local currency

Slide 9

2013 2014 YTD 2015-4

-2

0

2

4

6

% y-o-y

Structure in 2013: 2.5%Structure in 2014: 3.7%Structure in 2015: -0.1%

-0.2%

3.9%

-0.7%

© SKF Group 15 July 2015

10Sales development by geographyOrganic growth in local currency Q2 2015 vs Q2 2014

Slide 10

Europe0.7%

Asia/Pacific-3.7%

Middle East& Africa15.7%

LatinAmerica

4.6%

NorthAmerica-5.7%

© SKF Group 15 July 2015

11Sales development by geographyOrganic growth in local currency YTD 2015 vs YTD 2014

Slide 11

Europe0.8%

Asia/Pacific0.6%

Middle East& Africa15.0%

LatinAmerica

1.5%

NorthAmerica-4.1%

© SKF Group 15 July 2015

12

Components in net sales

Slide 12

2013 2014 2015

Percent y-o-y Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Organic -8.0 -2.2 2.0 6.9 5.8 4.6 3.2 2.8 1.4 -1.5

Structure 1.5 2.6 1.1 4.8 4.7 3.8 5.4 0.9 0 -0.2

Sales in local currency -6.5 0.4 3.1 11.7 10.5 8.4 8.6 3.7 1.4 -1.7

Currency -4.0 -5.0 -2.2 -2.1 -0.1 1.1 5.3 8.9 14.9 12.9

Net sales -10.5 -4.6 0.9 9.6 10.4 9.5 13.9 12.6 16.3 11.2

© SKF Group 15 July 2015

13

Operating profit as reported

Slide 13

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500SEKm

2013 2014 2015

© SKF Group 15 July 2015

14

Operating profit excluding one-time items

Slide 14

0

500

1000

1500

2000

2500

3000SEKm

2013 2014 2015

© SKF Group 15 July 2015

15

Operating margin

Slide 15

2013 2014 YTD 20150

2

4

6

8

10

12

14

16

%

5.8

11.9*

One-time items

* Excluding one-time items

10.4

12.6*11.7*

11.0

© SKF Group 15 July 2015

16

Slide 16

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2-3

0

3

6

9

12

15

18

Specialty Business*

Automotive Market

%

2013 2014 2015

Operating margin per business area, as reported

Industrial Market

* Q4 2013, impacted by cost related to Kaydon acquisition

© SKF Group 15 July 2015

17

Slide 17

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2-3

0

3

6

9

12

15

18

Specialty Business

Automotive Market

%

2013 2014 2015

Operating margin per business area, excl. one-time items

Industrial Market

© SKF Group 15 July 2015

18

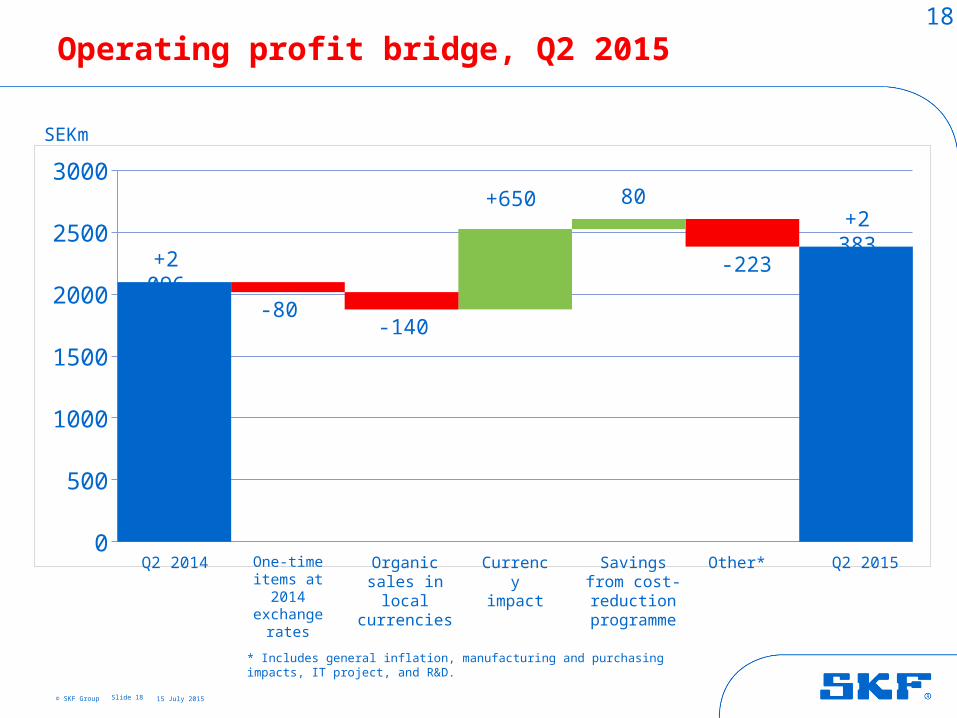

Operating profit bridge, Q2 2015

Slide 18

0

500

1000

1500

2000

2500

3000

-1 547

-80

+2 383

-140

+650

-223

SEKm

Q2 2014 Q2 2015One-time items at 2014

exchange rates

Currency impact

Other* Organic sales in local currencies

* Includes general inflation, manufacturing and purchasing impacts, IT project, and R&D.

+2 096

80

Savings from cost-reduction

programme

© SKF Group 15 July 2015

19

Operating profit bridge, YTD 2015

Slide 19

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

-1 547

-780

+4 104

-20

+1 100

-396

SEKm

YTD 2014 YTD 2015One-time items at 2014

exchange rates

Currency impact

Other* Organic sales in local currencies

* Includes general inflation, manufacturing and purchasing impacts, IT project, and R&D.

+2 096

80

Savings from cost-reduction

programme

© SKF Group 15 July 2015

20

Employee productivity and efficiency

• Expected productivity and efficiency gains from new organisation on-track:- merging the two industrial businesses- general staff optimization and productivity improvements

• Agreements have been reached covering 60% of the concerned individuals.

Q1 2015 Q2 2015 Target

Cost, SEKm 535 224 1 400

People affected 575 270 1 500

Cost savings - 80 -

Annual cost savings, SEKm 460* 170* 1 200

Slide 20

* On a full-year basis, as of Jan 2016

© SKF Group 15 July 2015

21

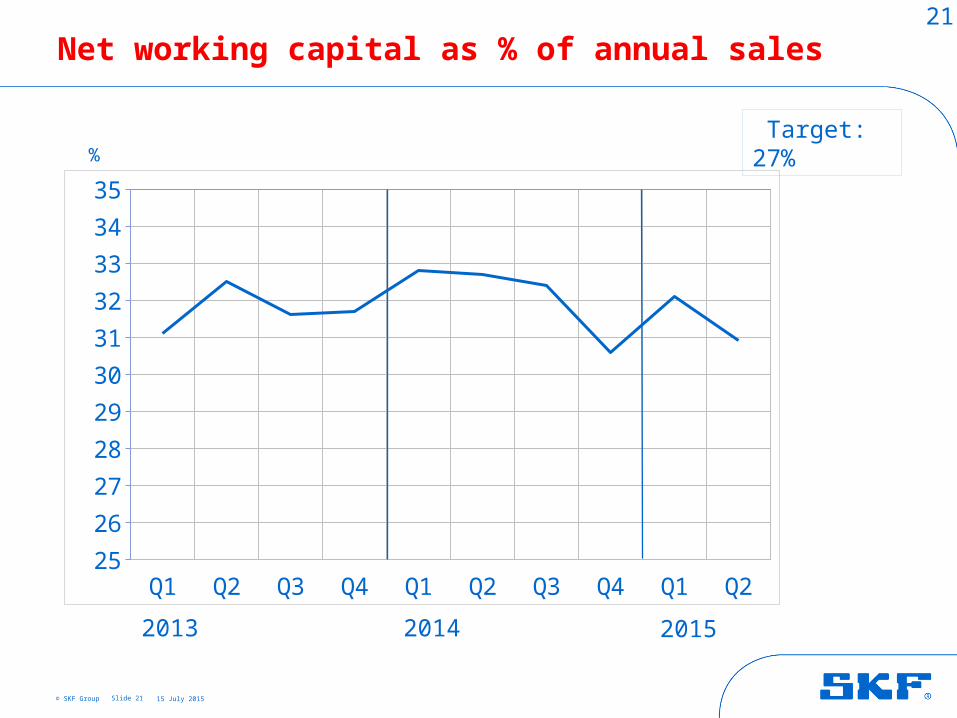

Net working capital as % of annual sales

Slide 21

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q225

26

27

28

29

30

31

32

33

34

35

%

2013 2014 2015

Target: 27%

© SKF Group 15 July 2015

22

Return on capital employed

Slide 22

2013 2014 YTD 20150

5

10

15

20

%

12.6

7.5

15.1*

One-time items * Excluding one-time items

ROCE: Operating profit plus interest income, as a percentage of twelve months rolling average of total assets less the average of non-interest bearing liabilities.

14.7*14.8*

13.9

© SKF Group 15 July 2015

23

-7,000

-6,000

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

Cash flow, after investments before financing*

Slide 23

SEKm

2013 2014 2015

Excl. acq. and div.: 1) Q1 2013 SEK -69 million2) Q3 2013 SEK 871 million3) Q4 2013 SEK 1 122 million

Excl. EU payment 4) Q2 2014 SEK 1 423 million

3)

4)

2)

1)

* 2013 and 2014 are restated

© SKF Group 15 July 2015

24

Net debt

Slide 24

-35,000

-30,000

-25,000

-20,000

-15,000

-10,000

-5,000

0SEKm

2013 2014 2015

AB SKF, dividend paid (SEKm):2013 Q2 2 5302014 Q2 2 5302015 Q2 2 567

Cash out from majoracquisitions (SEKm):

2013 Q1 8232013 Q4 7 900

Net debt: Loans and net provisions for post-employment benefits less short-term financial assets excluding derivatives.

EU payment (SEKm):

2014 Q2 2 825

Cash from divestments (SEKm):

2015 Q2 1 000

© SKF Group 15 July 2015

25

Debt structure, maturity years

Slide 25

2015 2016 2017 2018 2019 2020 20210

100

200

300

400

500

600

700

800

900

EURm

• Available credit facilities:EUR 500 million 2019SEK 3 000 million 2018

EUR 150 million 2017

• No financial covenants nor material adverse change clause

200

100 110

500 500

850

© SKF Group 15 July 2015

26

July 2015: SKF demand outlook Q3 2015

Slide 26

Demand compared to the third quarter 2014The demand for SKF’s products and services is expected to be relatively unchanged for the Group, Europe and Asia. For North America it is expected to be lower and for Latin America higher. For all business areas it is expected to be relatively unchanged.

Demand compared to the second quarter 2015The demand for SKF’s products and services is expected to be slightly lower for the Group. For Europe it is expected to be lower and for all other regions it is expected to be relatively unchanged. For the business areas, Industrial Market and Specialty Business it is expected to be relatively unchanged and for Automotive Market it is expected to be lower.

© SKF Group 15 July 2015

27

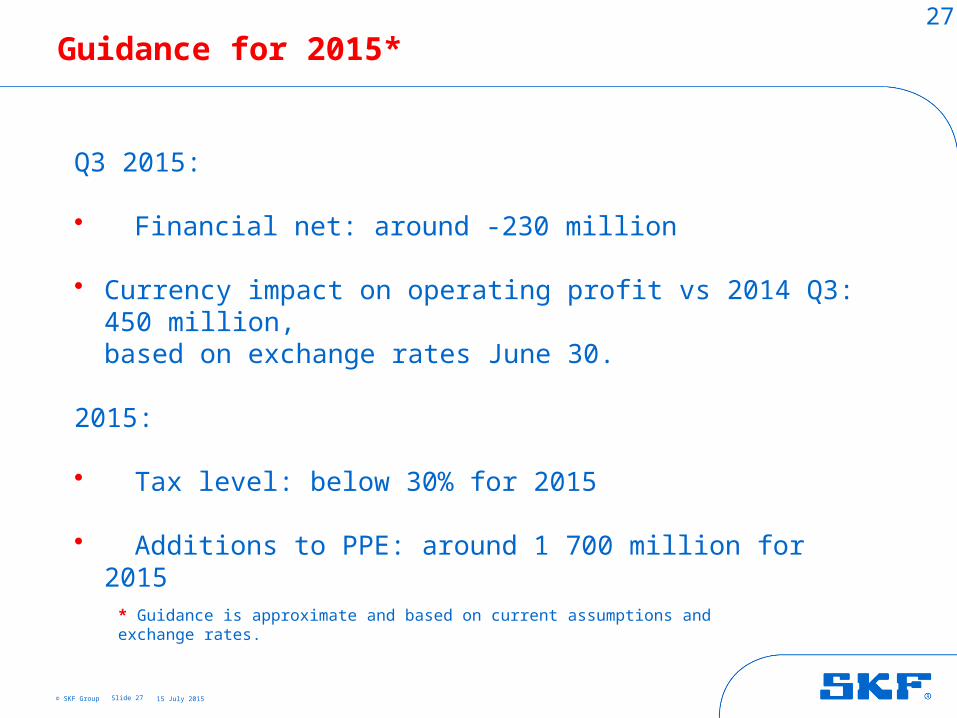

Guidance for 2015*

Slide 27

Q3 2015:

• Financial net: around -230 million

• Currency impact on operating profit vs 2014 Q3: 450 million, based on exchange rates June 30.

2015:

• Tax level: below 30% for 2015

• Additions to PPE: around 1 700 million for 2015

* Guidance is approximate and based on current assumptions and exchange rates.

© SKF Group 15 July 2015

28

Cautionary statement

Slide 28

This presentation contains forward-looking statements that are based on the current expectations of the management of SKF.

Although management believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those implied in the forward-looking statements as a result of, among other factors, changes in economic, market and competitive conditions, changes in the regulatory environment and other government actions, fluctuations in exchange rates and other factors mentioned in SKF's latest annual report (available on www.skf.com) under the Administration Report; “Important factors influencing the financial results", "Financial risks" and "Sensitivity analysis”.