10. company accounts 1100.. ccoommppaannyy …

TRANSCRIPT

Page 123

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

1100.. CCOOMMPPAANNYY AACCCCOOUUNNTTSS

UUNNIITT 11 :: IINNTTRROODDUUCCTTIIOONN TTOO CCOOMMPPAANNYY AACCCCOOUUNNTTSS

CCOONNCCEEPPTT 11 :: MMEEAANNIINNGG OOFF CCOOMMPPAANNYY

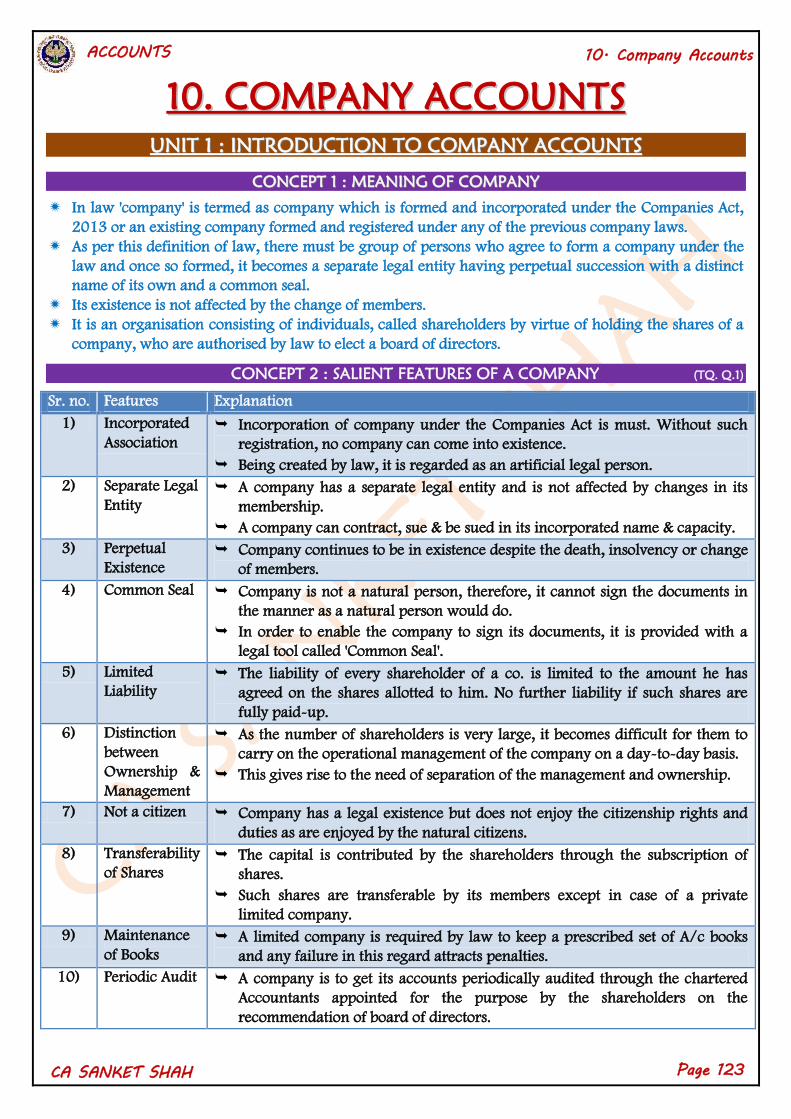

In law 'company' is termed as company which is formed and incorporated under the Companies Act,

2013 or an existing company formed and registered under any of the previous company laws.

As per this definition of law, there must be group of persons who agree to form a company under the

law and once so formed, it becomes a separate legal entity having perpetual succession with a distinct

name of its own and a common seal.

Its existence is not affected by the change of members.

It is an organisation consisting of individuals, called shareholders by virtue of holding the shares of a

company, who are authorised by law to elect a board of directors.

CONCEPT 2 : SALIENT FEATURES OF A COMPANY (TQ. Q.1)

Sr. no. Features Explanation

1) Incorporated

Association Incorporation of company under the Companies Act is must. Without such

registration, no company can come into existence.

Being created by law, it is regarded as an artificial legal person.

2) Separate Legal

Entity A company has a separate legal entity and is not affected by changes in its

membership.

A company can contract, sue & be sued in its incorporated name & capacity.

3) Perpetual

Existence Company continues to be in existence despite the death, insolvency or change

of members.

4) Common Seal Company is not a natural person, therefore, it cannot sign the documents in

the manner as a natural person would do.

In order to enable the company to sign its documents, it is provided with a

legal tool called 'Common Seal'.

5) Limited

Liability The liability of every shareholder of a co. is limited to the amount he has

agreed on the shares allotted to him. No further liability if such shares are

fully paid-up.

6) Distinction

between

Ownership &

Management

As the number of shareholders is very large, it becomes difficult for them to

carry on the operational management of the company on a day-to-day basis.

This gives rise to the need of separation of the management and ownership.

7) Not a citizen Company has a legal existence but does not enjoy the citizenship rights and

duties as are enjoyed by the natural citizens.

8) Transferability

of Shares The capital is contributed by the shareholders through the subscription of

shares.

Such shares are transferable by its members except in case of a private

limited company.

9) Maintenance

of Books A limited company is required by law to keep a prescribed set of A/c books

and any failure in this regard attracts penalties.

10) Periodic Audit A company is to get its accounts periodically audited through the chartered

Accountants appointed for the purpose by the shareholders on the

recommendation of board of directors.

Page 124

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

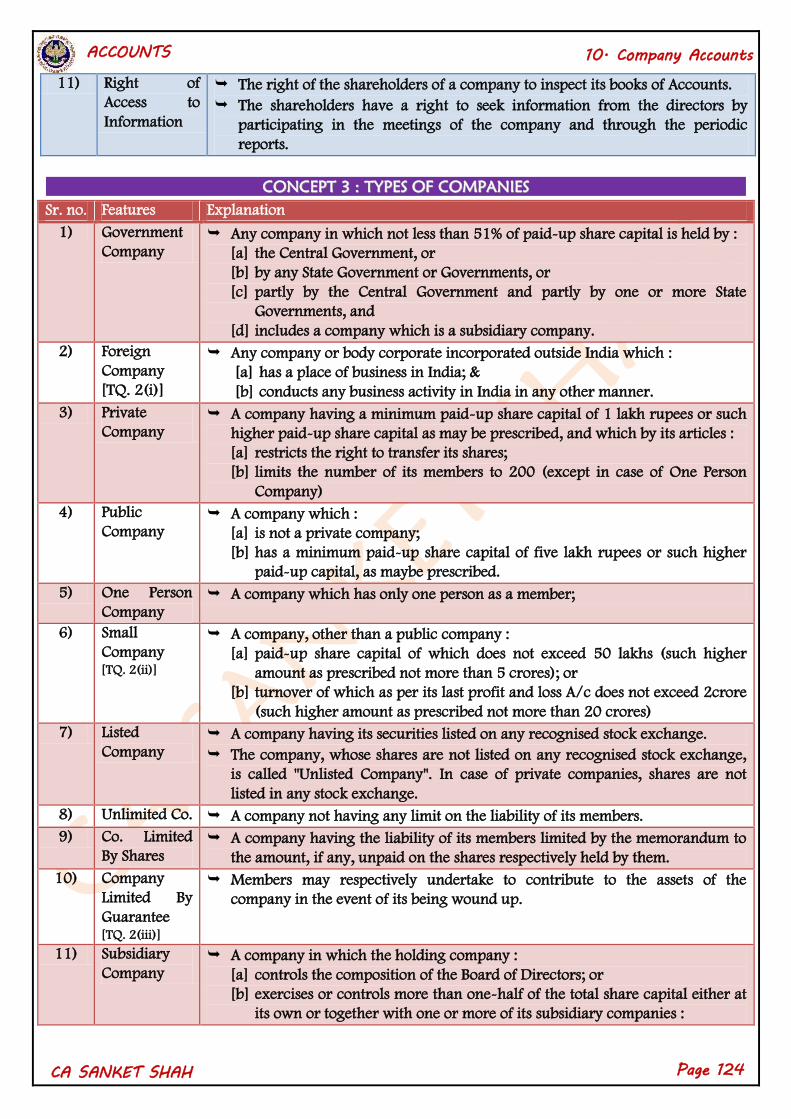

11) Right of

Access to

Information

The right of the shareholders of a company to inspect its books of Accounts.

The shareholders have a right to seek information from the directors by

participating in the meetings of the company and through the periodic

reports.

CCOONNCCEEPPTT 33 :: TTYYPPEESS OOFF CCOOMMPPAANNIIEESS

Sr. no. Features Explanation

1) Government

Company Any company in which not less than 51% of paid-up share capital is held by :

[a] the Central Government, or

[b] by any State Government or Governments, or

[c] partly by the Central Government and partly by one or more State

Governments, and

[d] includes a company which is a subsidiary company.

2) Foreign

Company

[TQ. 2(i)]

Any company or body corporate incorporated outside India which :

[a] has a place of business in India; &

[b] conducts any business activity in India in any other manner.

3) Private

Company A company having a minimum paid-up share capital of 1 lakh rupees or such

higher paid-up share capital as may be prescribed, and which by its articles :

[a] restricts the right to transfer its shares;

[b] limits the number of its members to 200 (except in case of One Person

Company)

4) Public

Company A company which :

[a] is not a private company;

[b] has a minimum paid-up share capital of five lakh rupees or such higher

paid-up capital, as maybe prescribed.

5) One Person

Company A company which has only one person as a member;

6) Small

Company [TQ. 2(ii)]

A company, other than a public company :

[a] paid-up share capital of which does not exceed 50 lakhs (such higher

amount as prescribed not more than 5 crores); or

[b] turnover of which as per its last profit and loss A/c does not exceed 2crore

(such higher amount as prescribed not more than 20 crores)

7) Listed

Company A company having its securities listed on any recognised stock exchange.

The company, whose shares are not listed on any recognised stock exchange,

is called "Unlisted Company". In case of private companies, shares are not

listed in any stock exchange.

8) Unlimited Co. A company not having any limit on the liability of its members.

9) Co. Limited

By Shares A company having the liability of its members limited by the memorandum to

the amount, if any, unpaid on the shares respectively held by them.

10) Company

Limited By

Guarantee [TQ. 2(iii)]

Members may respectively undertake to contribute to the assets of the

company in the event of its being wound up.

11) Subsidiary

Company A company in which the holding company :

[a] controls the composition of the Board of Directors; or

[b] exercises or controls more than one-half of the total share capital either at

its own or together with one or more of its subsidiary companies :

Page 125

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

CONCEPT 4 : MAINTENANCE OF BOOK OF ACCOUNTS

Every company shall prepare and keep at its registered office books of A/c and

other relevant books and papers and

financial statement for every financial year

which give a true and fair view of the state of the affairs of the company, including that of its branch

office or offices. (Provided further that the company may keep such books in electronic mode).

CCOONNCCEEPPTT 55 :: PPRREEPPAARRAATTIIOONN OOFF FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS

The financial statements comply with the notified Accounting Standards and in the form Schedule III.

The Board of Directors of the company shall lay financial statements at every AGM of a company.

Financial Statements as per Section 2(40) of the Companies Act, 2013, inter-alia include :

[a] a balance sheet as at the end of the financial year;

[b] a profit and loss A/c

[c] cash flow statement for the financial year;

[d] a statement of changes in equity (SOCE), if applicable; and

[e] any explanatory note

Provisions Applicable

[1] Specific Act is Applicable For instance any

[a] insurance company

[b] banking company or

[c] any company engaged in generation or supply of electricity or

[d] any other class of company for which a Form of balance sheet or Profit and loss A/c has been

prescribed under the Act governing such class of company

[2] In case of all other companies

In the form of Schedule

Balance Sheet Schedule III Part I

Profit & Loss Statement Schedule III Part II

PART I - Form of BALANCE SHEET

Name of the Company.........................

Balance Sheet as at...........................

Sr. no. Particulars Notes

No.

Figures as at end

of the current

reporting period

Figures as at end

of the previous

reporting period

EQUITY AND LIABILITIES

1

a

b

c

Shareholders' funds

Share capital

Reserves and Surplus

Money received against share warrants

2 Share application money pending allotment

3

a

b

c

d

Non-current liabilities

Long-term borrowings

Deferred tax liabilities (Net)

Other long term liabilities

Long-term provisions

Page 126

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

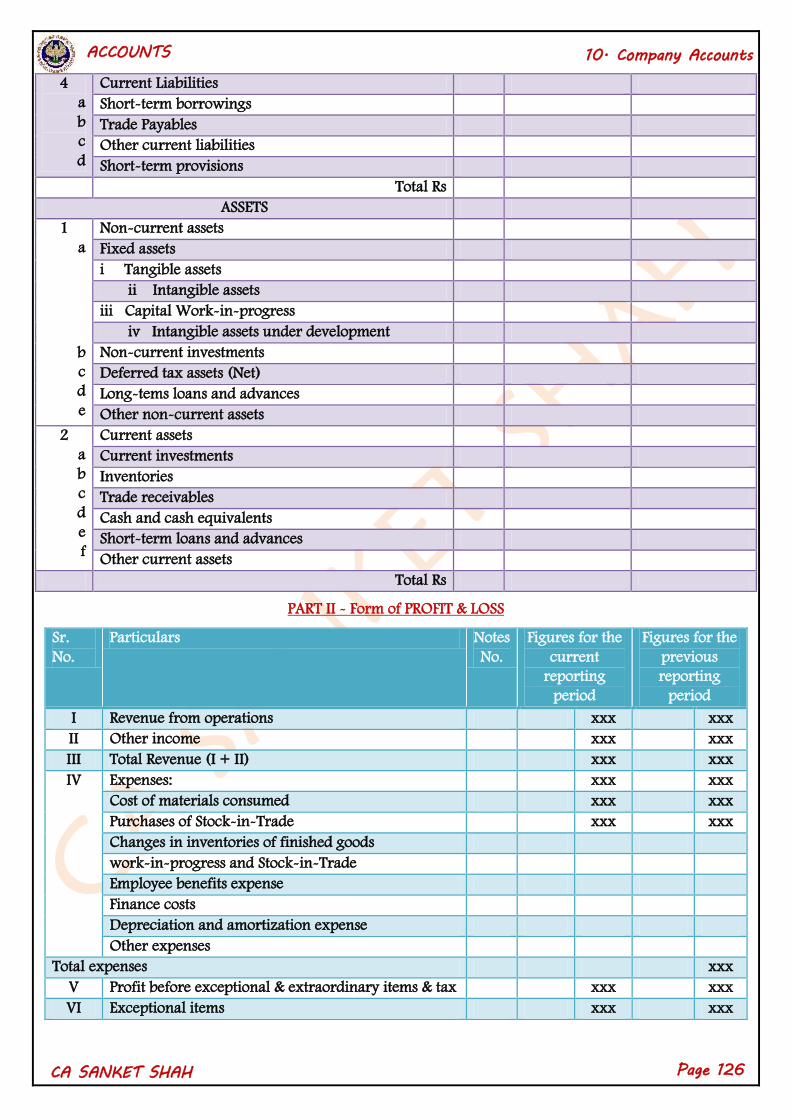

4

a

b

c

d

Current Liabilities

Short-term borrowings

Trade Payables

Other current liabilities

Short-term provisions

Total Rs

ASSETS

1

a

b

c

d

e

Non-current assets

Fixed assets

i Tangible assets

ii Intangible assets

iii Capital Work-in-progress

iv Intangible assets under development

Non-current investments

Deferred tax assets (Net)

Long-tems loans and advances

Other non-current assets

2

a

b

c

d

e

f

Current assets

Current investments

Inventories

Trade receivables

Cash and cash equivalents

Short-term loans and advances

Other current assets

Total Rs

PART II - Form of PROFIT & LOSS

Sr.

No.

Particulars Notes

No.

Figures for the

current

reporting

period

Figures for the

previous

reporting

period

I Revenue from operations xxx xxx

II Other income xxx xxx

III Total Revenue (I + II) xxx xxx

IV Expenses: xxx xxx

Cost of materials consumed xxx xxx

Purchases of Stock-in-Trade xxx xxx

Changes in inventories of finished goods

work-in-progress and Stock-in-Trade

Employee benefits expense

Finance costs

Depreciation and amortization expense

Other expenses

Total expenses xxx

V Profit before exceptional & extraordinary items & tax xxx xxx

VI Exceptional items xxx xxx

Page 127

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

VII Profit before extraordinary items and tax (V-VI) xxx xxx

VIII Extraordinary Items xxx xxx

IX Profit before tax (VII- VIII) xxx xxx

X Tax expense:

(1) Current tax xxx xxx

(2) Deferred tax xxx xxx xxx xxx

XI Profit (Loss) for the period from continuing

operations

xxx xxx

XII Profit/(Loss) from discontinuing operations xxx xxx

XIII Tax expense of discontinuing operations xxx xxx

XIV Profit/(Loss) from Discontinuing operations (after

tax) (XII-XIII)

xxx xxx

XV Profit (Loss) for the period (XI + XIV) xxx xxx

XVI Earnings per equity share:

(1) Basic xxx xxx

(2) Diluted xxx xxx

Page 128

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

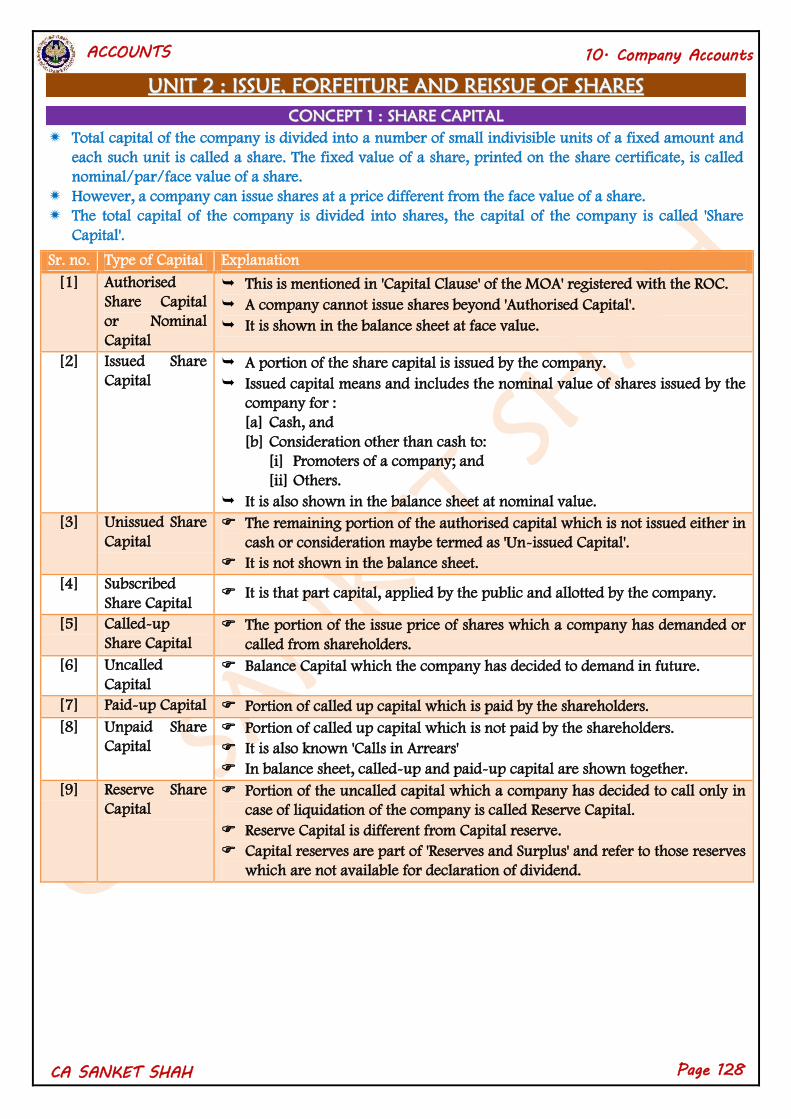

UUNNIITT 22 :: IISSSSUUEE,, FFOORRFFEEIITTUURREE AANNDD RREEIISSSSUUEE OOFF SSHHAARREESS

CCOONNCCEEPPTT 11 :: SSHHAARREE CCAAPPIITTAALL

Total capital of the company is divided into a number of small indivisible units of a fixed amount and

each such unit is called a share. The fixed value of a share, printed on the share certificate, is called

nominal/par/face value of a share.

However, a company can issue shares at a price different from the face value of a share.

The total capital of the company is divided into shares, the capital of the company is called 'Share

Capital'.

Sr. no. Type of Capital Explanation

[1] Authorised

Share Capital

or Nominal

Capital

This is mentioned in 'Capital Clause' of the MOA' registered with the ROC.

A company cannot issue shares beyond 'Authorised Capital'.

It is shown in the balance sheet at face value.

[2] Issued Share

Capital A portion of the share capital is issued by the company.

Issued capital means and includes the nominal value of shares issued by the

company for :

[a] Cash, and

[b] Consideration other than cash to:

[i] Promoters of a company; and

[ii] Others.

It is also shown in the balance sheet at nominal value.

[3] Unissued Share

Capital

The remaining portion of the authorised capital which is not issued either in

cash or consideration maybe termed as 'Un-issued Capital'.

It is not shown in the balance sheet.

[4] Subscribed

Share Capital It is that part capital, applied by the public and allotted by the company.

[5] Called-up

Share Capital

The portion of the issue price of shares which a company has demanded or

called from shareholders.

[6] Uncalled

Capital

Balance Capital which the company has decided to demand in future.

[7] Paid-up Capital Portion of called up capital which is paid by the shareholders.

[8] Unpaid Share

Capital Portion of called up capital which is not paid by the shareholders.

It is also known 'Calls in Arrears'

In balance sheet, called-up and paid-up capital are shown together.

[9] Reserve Share

Capital Portion of the uncalled capital which a company has decided to call only in

case of liquidation of the company is called Reserve Capital.

Reserve Capital is different from Capital reserve.

Capital reserves are part of 'Reserves and Surplus' and refer to those reserves

which are not available for declaration of dividend.

Page 129

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

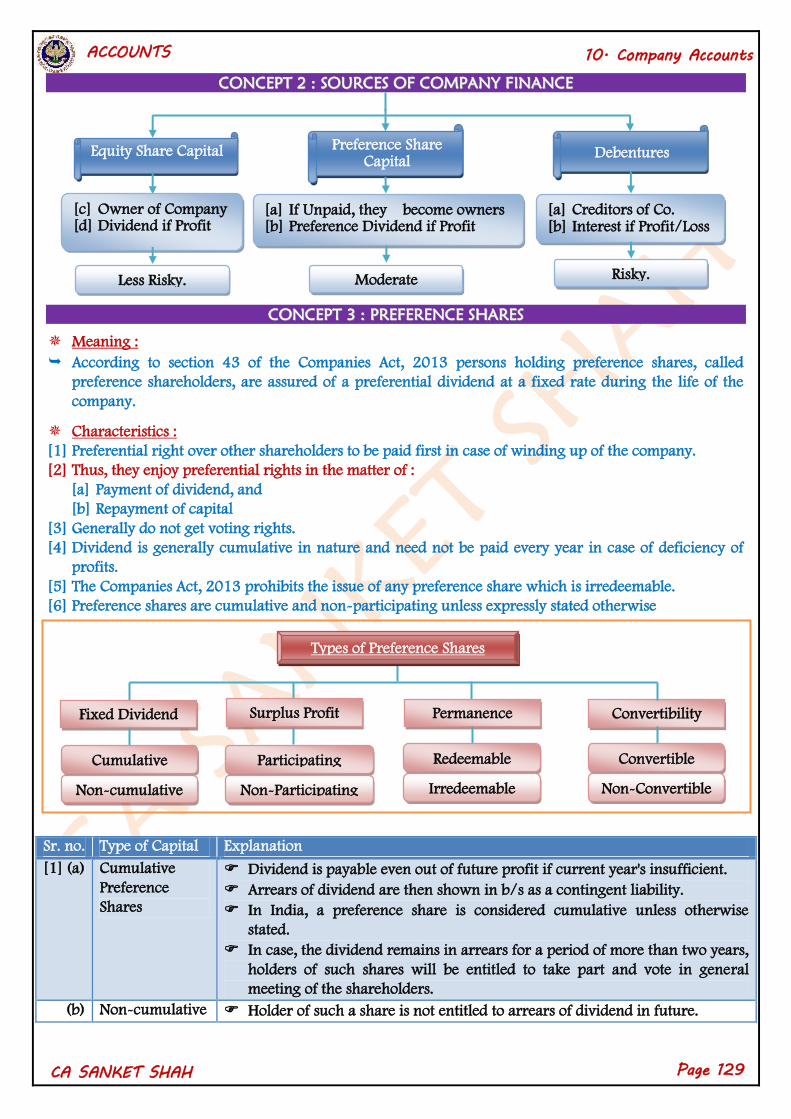

CCOONNCCEEPPTT 22 :: SSOOUURRCCEESS OOFF CCOOMMPPAANNYY FFIINNAANNCCEE

CCOONNCCEEPPTT 33 :: PPRREEFFEERREENNCCEE SSHHAARREESS

Meaning :

According to section 43 of the Companies Act, 2013 persons holding preference shares, called

preference shareholders, are assured of a preferential dividend at a fixed rate during the life of the

company.

Characteristics :

[1] Preferential right over other shareholders to be paid first in case of winding up of the company.

[2] Thus, they enjoy preferential rights in the matter of :

[a] Payment of dividend, and

[b] Repayment of capital

[3] Generally do not get voting rights.

[4] Dividend is generally cumulative in nature and need not be paid every year in case of deficiency of

profits.

[5] The Companies Act, 2013 prohibits the issue of any preference share which is irredeemable.

[6] Preference shares are cumulative and non-participating unless expressly stated otherwise

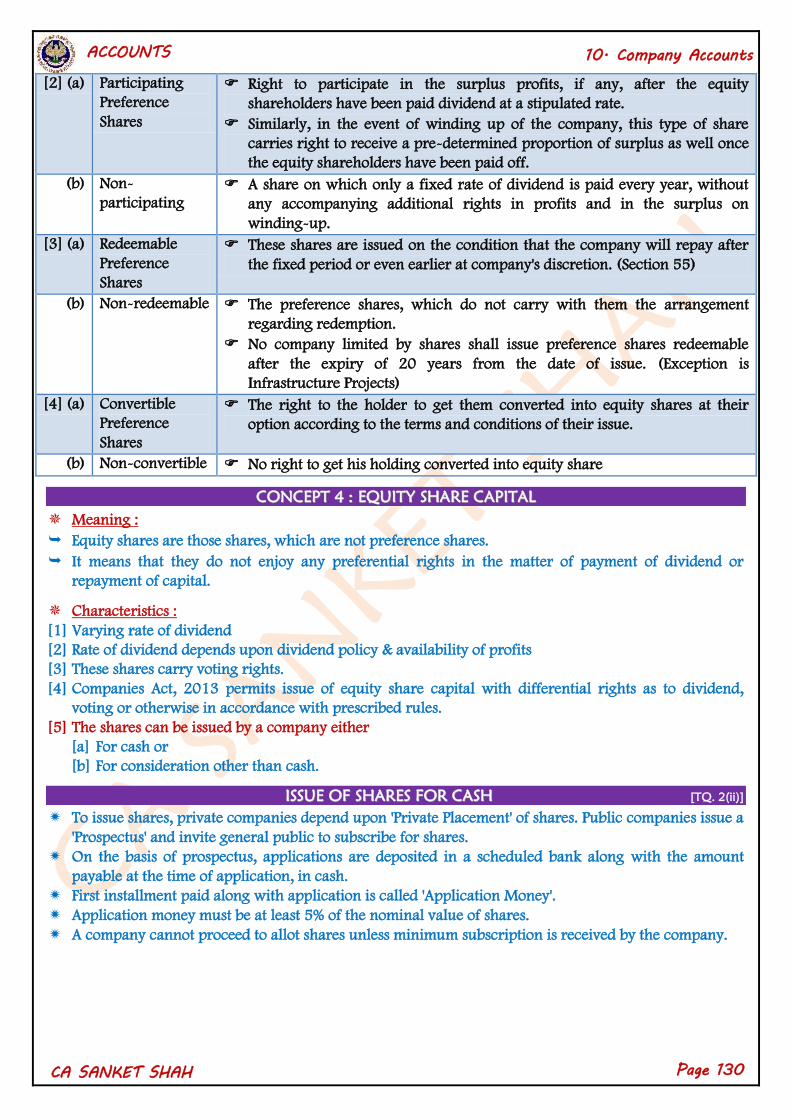

Sr. no. Type of Capital Explanation

[1] (a) Cumulative

Preference

Shares

Dividend is payable even out of future profit if current year's insufficient.

Arrears of dividend are then shown in b/s as a contingent liability.

In India, a preference share is considered cumulative unless otherwise

stated.

In case, the dividend remains in arrears for a period of more than two years,

holders of such shares will be entitled to take part and vote in general

meeting of the shareholders.

(b) Non-cumulative Holder of such a share is not entitled to arrears of dividend in future.

Equity Share Capital Preference Share Capital

Debentures

[c] Owner of Company [d] Dividend if Profit

[a] If Unpaid, they become owners [b] Preference Dividend if Profit

[a] Creditors of Co. [b] Interest if Profit/Loss

Less Risky. Moderate Risky.

Fixed Dividend Surplus Profit

Permanence

Convertibility

Cumulative

Non-cumulative

Participating

Non-Participating

Redeemable

Irredeemable

Convertible Non-Convertible

Types of Preference Shares

Page 130

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

[2] (a) Participating

Preference

Shares

Right to participate in the surplus profits, if any, after the equity

shareholders have been paid dividend at a stipulated rate.

Similarly, in the event of winding up of the company, this type of share

carries right to receive a pre-determined proportion of surplus as well once

the equity shareholders have been paid off.

(b) Non-

participating A share on which only a fixed rate of dividend is paid every year, without

any accompanying additional rights in profits and in the surplus on

winding-up.

[3] (a) Redeemable

Preference

Shares

These shares are issued on the condition that the company will repay after

the fixed period or even earlier at company's discretion. (Section 55)

(b) Non-redeemable The preference shares, which do not carry with them the arrangement

regarding redemption.

No company limited by shares shall issue preference shares redeemable

after the expiry of 20 years from the date of issue. (Exception is

Infrastructure Projects)

[4] (a) Convertible

Preference

Shares

The right to the holder to get them converted into equity shares at their

option according to the terms and conditions of their issue.

(b) Non-convertible No right to get his holding converted into equity share

CCOONNCCEEPPTT 44 :: EEQQUUIITTYY SSHHAARREE CCAAPPIITTAALL

Meaning :

Equity shares are those shares, which are not preference shares.

It means that they do not enjoy any preferential rights in the matter of payment of dividend or

repayment of capital.

Characteristics :

[1] Varying rate of dividend

[2] Rate of dividend depends upon dividend policy & availability of profits

[3] These shares carry voting rights.

[4] Companies Act, 2013 permits issue of equity share capital with differential rights as to dividend,

voting or otherwise in accordance with prescribed rules.

[5] The shares can be issued by a company either

[a] For cash or

[b] For consideration other than cash.

IISSSSUUEE OOFF SSHHAARREESS FFOORR CCAASSHH [TQ. 2(ii)]

To issue shares, private companies depend upon 'Private Placement' of shares. Public companies issue a

'Prospectus' and invite general public to subscribe for shares.

On the basis of prospectus, applications are deposited in a scheduled bank along with the amount

payable at the time of application, in cash.

First installment paid along with application is called 'Application Money'.

Application money must be at least 5% of the nominal value of shares.

A company cannot proceed to allot shares unless minimum subscription is received by the company.

Page 131

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

MMIINNIIMMUUMM SSUUBBSSCCRRIIPPTTIIOONN

The amount of minimum subscription to be disclosed in prospectus by the Board of Directors taking

into A/c the following:

[a] Preliminary expenses of the company,

[b] Commission payable on issue of shares,

[c] Cost of fixed assets purchased or to be purchased,

[d] Working capital requirements of the company, and

[e] Any other expenditure for the day to day operation of the business.

As per SEBI, a company must receive a minimum of 90% subscription against the entire issue before

making any allotment of shares or debentures to the public.

If the Company does not receive the minimum subscription of 90% the entire subscription shall be

refunded to the applicants within 15 days after the date of closure of issue in case of non-

underwritten issue and 7 days after the date of closure of issue in case of underwritten issue.

However, as per SEBI Regulations, the minimum application moneys to be paid by an applicant along

with the application money shall not be less than 25% of the issue price.

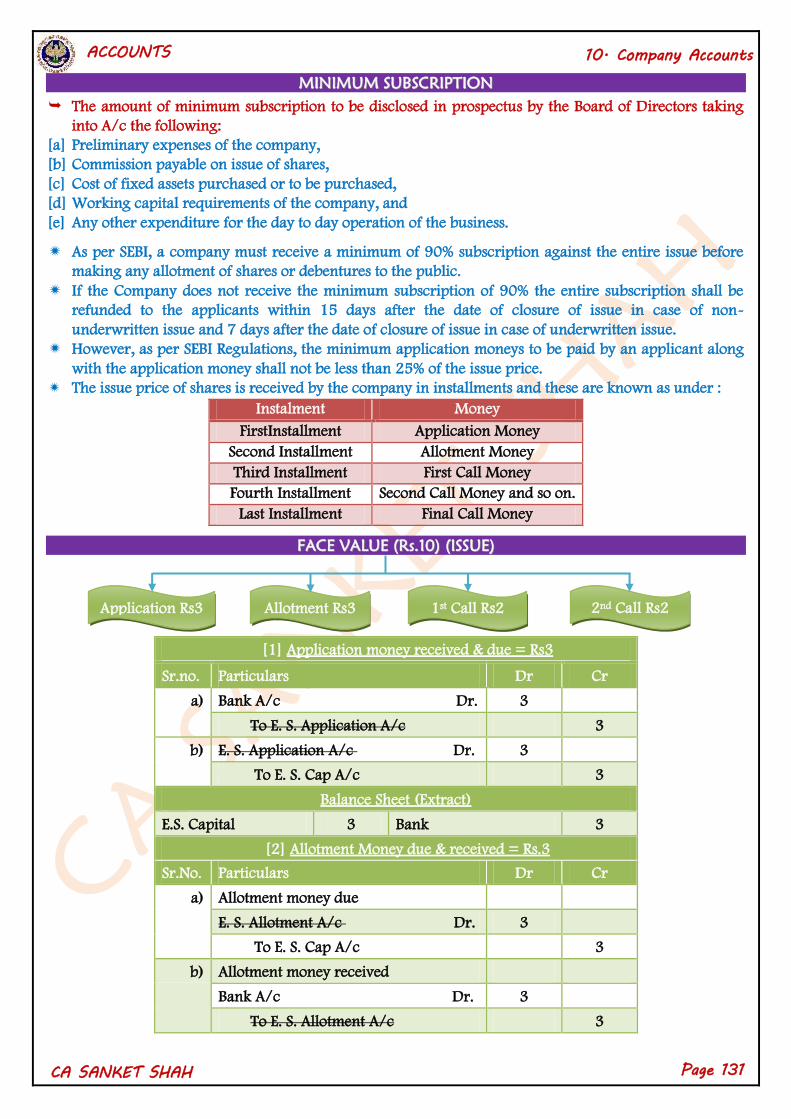

The issue price of shares is received by the company in installments and these are known as under :

Instalment Money

FirstInstallment Application Money

Second Installment Allotment Money

Third Installment First Call Money

Fourth Installment Second Call Money and so on.

Last Installment Final Call Money

FFAACCEE VVAALLUUEE ((RRss..1100)) ((IISSSSUUEE))

[1] Application money received & due = Rs3

Sr.no. Particulars Dr Cr

a) Bank A/c Dr. 3

To E. S. Application A/c 3

b) E. S. Application A/c Dr. 3

To E. S. Cap A/c 3

Balance Sheet (Extract)

E.S. Capital 3 Bank 3

[2] Allotment Money due & received = Rs.3

Sr.No. Particulars Dr Cr

a) Allotment money due

E. S. Allotment A/c Dr. 3

To E. S. Cap A/c 3

b) Allotment money received

Bank A/c Dr. 3

To E. S. Allotment A/c 3

Application Rs3 2nd Call Rs2 Allotment Rs3 1st Call Rs2

Page 132

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

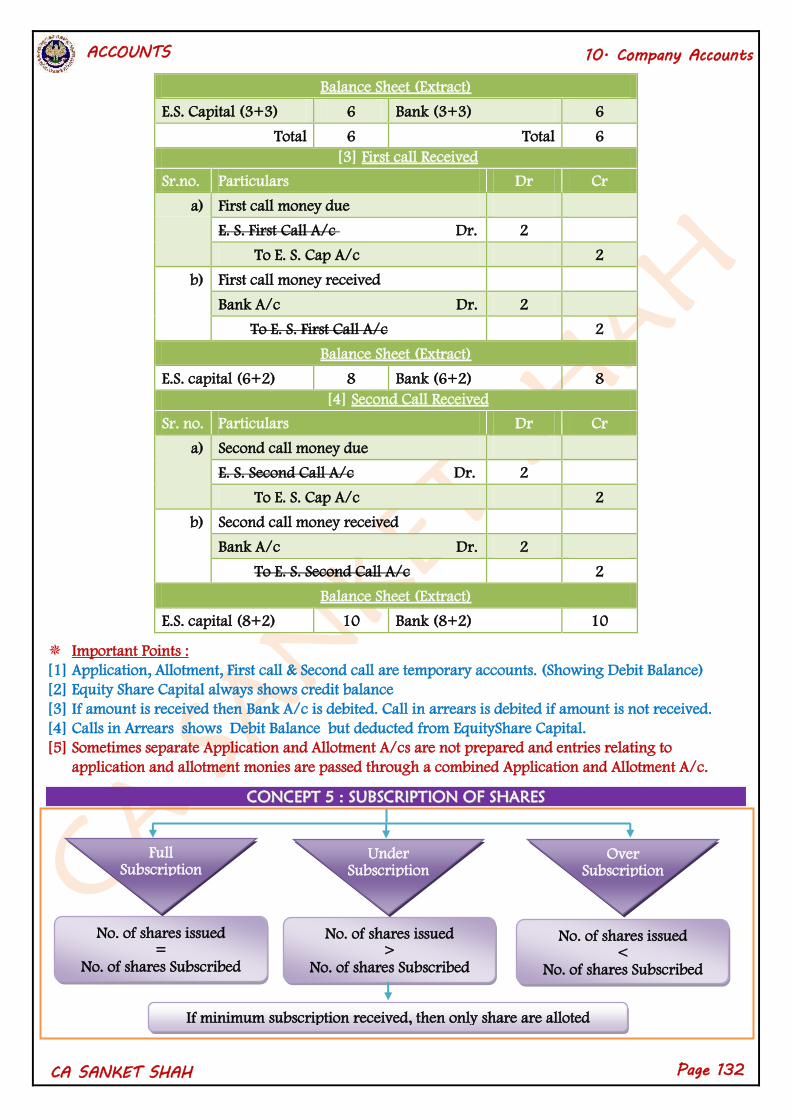

Balance Sheet (Extract)

E.S. Capital (3+3) 6 Bank (3+3) 6

Total 6 Total 6

[3] First call Received

Sr.no. Particulars Dr Cr

a) First call money due

E. S. First Call A/c Dr. 2

To E. S. Cap A/c 2

b) First call money received

Bank A/c Dr. 2

To E. S. First Call A/c 2

Balance Sheet (Extract)

E.S. capital (6+2) 8 Bank (6+2) 8

[4] Second Call Received

Sr. no. Particulars Dr Cr

a) Second call money due

E. S. Second Call A/c Dr. 2

To E. S. Cap A/c 2

b) Second call money received

Bank A/c Dr. 2

To E. S. Second Call A/c 2

Balance Sheet (Extract)

E.S. capital (8+2) 10 Bank (8+2) 10

Important Points :

[1] Application, Allotment, First call & Second call are temporary accounts. (Showing Debit Balance)

[2] Equity Share Capital always shows credit balance

[3] If amount is received then Bank A/c is debited. Call in arrears is debited if amount is not received.

[4] Calls in Arrears shows Debit Balance but deducted from EquityShare Capital.

[5] Sometimes separate Application and Allotment A/cs are not prepared and entries relating to

application and allotment monies are passed through a combined Application and Allotment A/c.

CCOONNCCEEPPTT 55 :: SSUUBBSSCCRRIIPPTTIIOONN OOFF SSHHAARREESS

Full Subscription

If minimum subscription received, then only share are alloted

Under Subscription

Over Subscription

No. of shares issued =

No. of shares Subscribed

No. of shares issued >

No. of shares Subscribed

No. of shares issued <

No. of shares Subscribed

Page 133

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

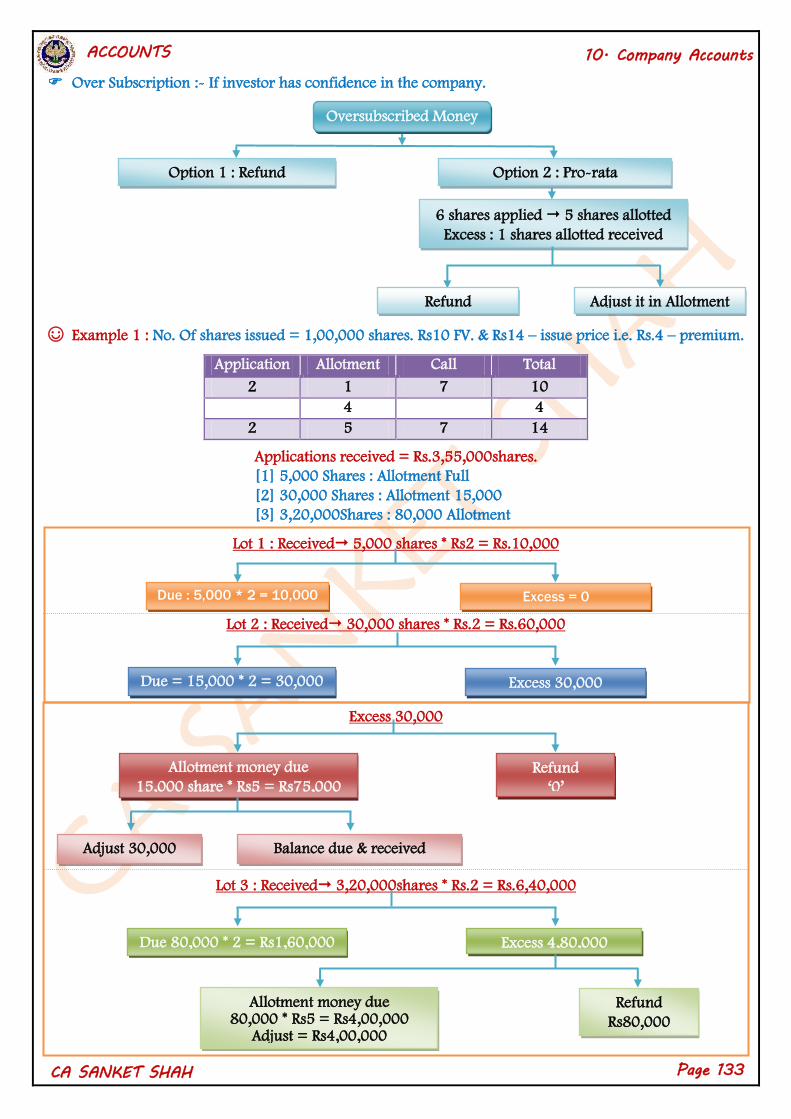

Over Subscription :- If investor has confidence in the company.

☺ Example 1 : No. Of shares issued = 1,00,000 shares. Rs10 FV. & Rs14 – issue price i.e. Rs.4 – premium.

Application Allotment Call Total

2 1 7 10

4 4

2 5 7 14

Applications received = Rs.3,55,000shares.

[1] 5,000 Shares : Allotment Full

[2] 30,000 Shares : Allotment 15,000

[3] 3,20,000Shares : 80,000 Allotment

Lot 1 : Received 5,000 shares * Rs2 = Rs.10,000

Lot 2 : Received 30,000 shares * Rs.2 = Rs.60,000

Excess 30,000

Lot 3 : Received 3,20,000shares * Rs.2 = Rs.6,40,000

Option 1 : Refund Option 2 : Pro-rata

6 shares applied 5 shares allotted

Excess : 1 shares allotted received

Refund

Adjust it in Allotment

Due : 5,000 * 2 = 10,000 Excess = 0

Due = 15,000 * 2 = 30,000 Excess 30,000

Allotment money due

15,000 share * Rs5 = Rs75,000

Refund

‘0’

Adjust 30,000

Balance due & received

45,000

Due 80,000 * 2 = Rs1,60,000 Excess 4,80,000

Allotment money due 80,000 * Rs5 = Rs4,00,000

Adjust = Rs4,00,000

Refund

Rs80,000

Oversubscribed Money

Page 134

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

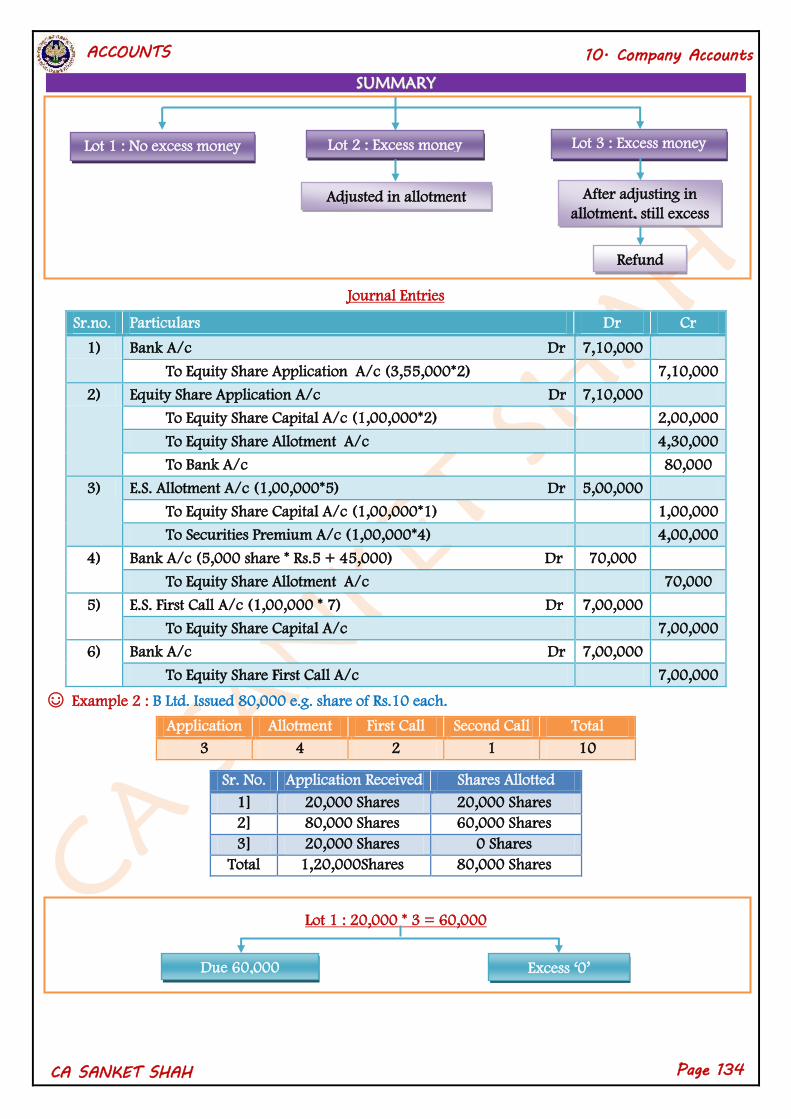

SSUUMMMMAARRYY

Journal Entries

Sr.no. Particulars Dr Cr

1) Bank A/c Dr 7,10,000

To Equity Share Application A/c (3,55,000*2) 7,10,000

2) Equity Share Application A/c Dr 7,10,000

To Equity Share Capital A/c (1,00,000*2) 2,00,000

To Equity Share Allotment A/c 4,30,000

To Bank A/c 80,000

3) E.S. Allotment A/c (1,00,000*5) Dr 5,00,000

To Equity Share Capital A/c (1,00,000*1) 1,00,000

To Securities Premium A/c (1,00,000*4) 4,00,000

4) Bank A/c (5,000 share * Rs.5 + 45,000) Dr 70,000

To Equity Share Allotment A/c 70,000

5) E.S. First Call A/c (1,00,000 * 7) Dr 7,00,000

To Equity Share Capital A/c 7,00,000

6) Bank A/c Dr 7,00,000

To Equity Share First Call A/c 7,00,000

☺ Example 2 : B Ltd. Issued 80,000 e.g. share of Rs.10 each.

Application Allotment First Call Second Call Total

3 4 2 1 10

Sr. No. Application Received Shares Allotted

1] 20,000 Shares 20,000 Shares

2] 80,000 Shares 60,000 Shares

3] 20,000 Shares 0 Shares

Total 1,20,000Shares 80,000 Shares

Lot 1 : 20,000 * 3 = 60,000

Lot 1 : No excess money

Lot 2 : Excess money

Lot 3 : Excess money

Adjusted in allotment

After adjusting in

allotment, still excess

Refund

Due 60,000 Excess ‘0’

Page 135

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

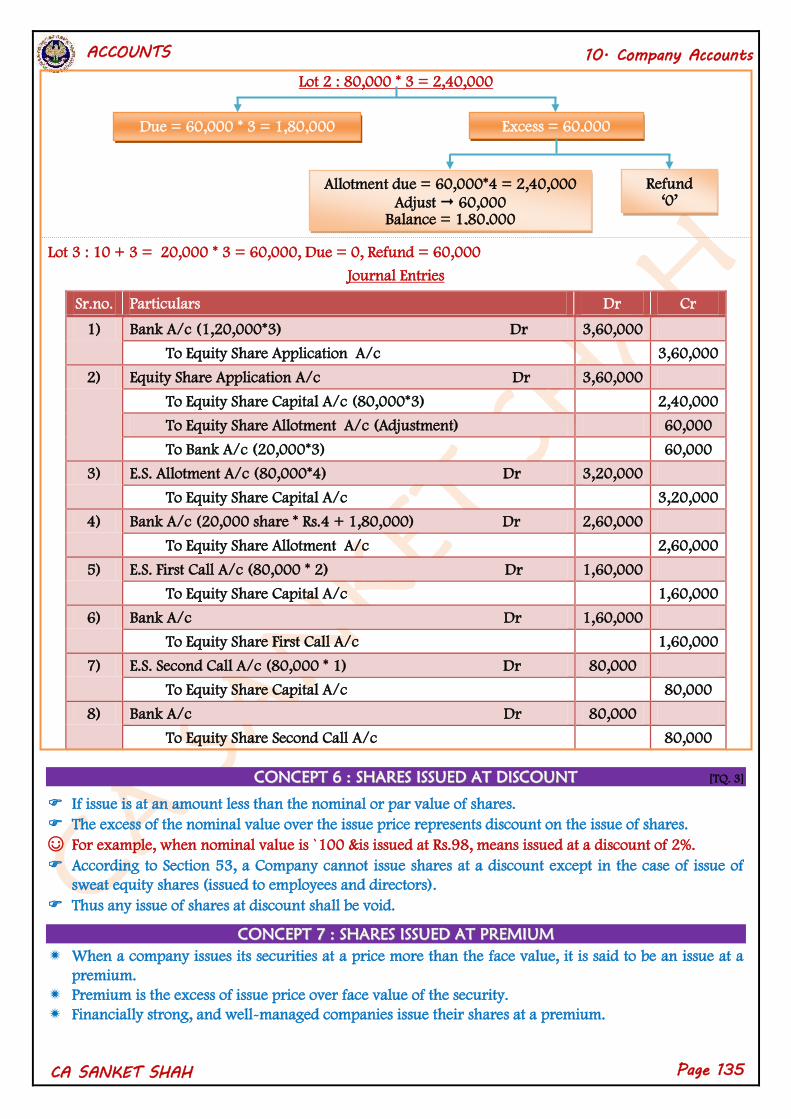

Lot 2 : 80,000 * 3 = 2,40,000

Lot 3 : 10 + 3 = 20,000 * 3 = 60,000, Due = 0, Refund = 60,000

Journal Entries

Sr.no. Particulars Dr Cr

1) Bank A/c (1,20,000*3) Dr 3,60,000

To Equity Share Application A/c 3,60,000

2) Equity Share Application A/c Dr 3,60,000

To Equity Share Capital A/c (80,000*3) 2,40,000

To Equity Share Allotment A/c (Adjustment) 60,000

To Bank A/c (20,000*3) 60,000

3) E.S. Allotment A/c (80,000*4) Dr 3,20,000

To Equity Share Capital A/c 3,20,000

4) Bank A/c (20,000 share * Rs.4 + 1,80,000) Dr 2,60,000

To Equity Share Allotment A/c 2,60,000

5) E.S. First Call A/c (80,000 * 2) Dr 1,60,000

To Equity Share Capital A/c 1,60,000

6) Bank A/c Dr 1,60,000

To Equity Share First Call A/c 1,60,000

7) E.S. Second Call A/c (80,000 * 1) Dr 80,000

To Equity Share Capital A/c 80,000

8) Bank A/c Dr 80,000

To Equity Share Second Call A/c 80,000

CCOONNCCEEPPTT 66 :: SSHHAARREESS IISSSSUUEEDD AATT DDIISSCCOOUUNNTT [TQ. 3]

If issue is at an amount less than the nominal or par value of shares.

The excess of the nominal value over the issue price represents discount on the issue of shares.

☺ For example, when nominal value is `100 &is issued at Rs.98, means issued at a discount of 2%.

According to Section 53, a Company cannot issue shares at a discount except in the case of issue of

sweat equity shares (issued to employees and directors).

Thus any issue of shares at discount shall be void.

CCOONNCCEEPPTT 77 :: SSHHAARREESS IISSSSUUEEDD AATT PPRREEMMIIUUMM

When a company issues its securities at a price more than the face value, it is said to be an issue at a

premium.

Premium is the excess of issue price over face value of the security.

Financially strong, and well-managed companies issue their shares at a premium.

Due = 60,000 * 3 = 1,80,000 Excess = 60,000

Allotment due = 60,000*4 = 2,40,000

Adjust 60,000 Balance = 1,80,000

Refund ‘0’

Page 136

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

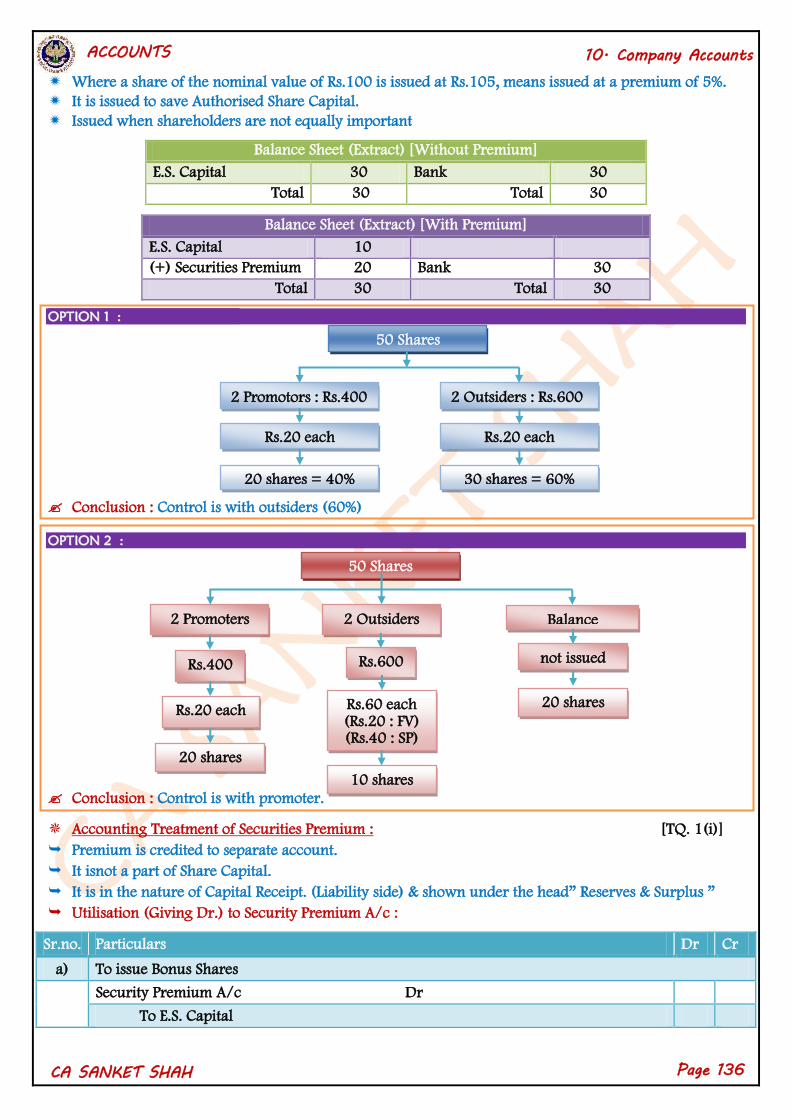

Where a share of the nominal value of Rs.100 is issued at Rs.105, means issued at a premium of 5%.

It is issued to save Authorised Share Capital.

Issued when shareholders are not equally important

Balance Sheet (Extract) [Without Premium]

E.S. Capital 30 Bank 30

Total 30 Total 30

Balance Sheet (Extract) [With Premium]

E.S. Capital 10

(+) Securities Premium 20 Bank 30

Total 30 Total 30

OOPPTTIIOONN 11 ::

Conclusion : Control is with outsiders (60%)

OOPPTTIIOONN 22 ::

Conclusion : Control is with promoter.

Accounting Treatment of Securities Premium : [TQ. 1(i)]

Premium is credited to separate account.

It isnot a part of Share Capital.

It is in the nature of Capital Receipt. (Liability side) & shown under the head” Reserves & Surplus ”

Utilisation (Giving Dr.) to Security Premium A/c :

Sr.no. Particulars Dr Cr

a) To issue Bonus Shares

Security Premium A/c Dr

To E.S. Capital

2 Promotors : Rs.400

2 Outsiders : Rs.600

Rs.20 each

Rs.20 each

20 shares = 40%

30 shares = 60%

2 Promoters Balance 2 Outsiders

Rs.400 Rs.600 not issued

Rs.20 each Rs.60 each (Rs.20 : FV) (Rs.40 : SP)

20 shares

20 shares

10 shares

50 Shares

50 Shares

Page 137

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

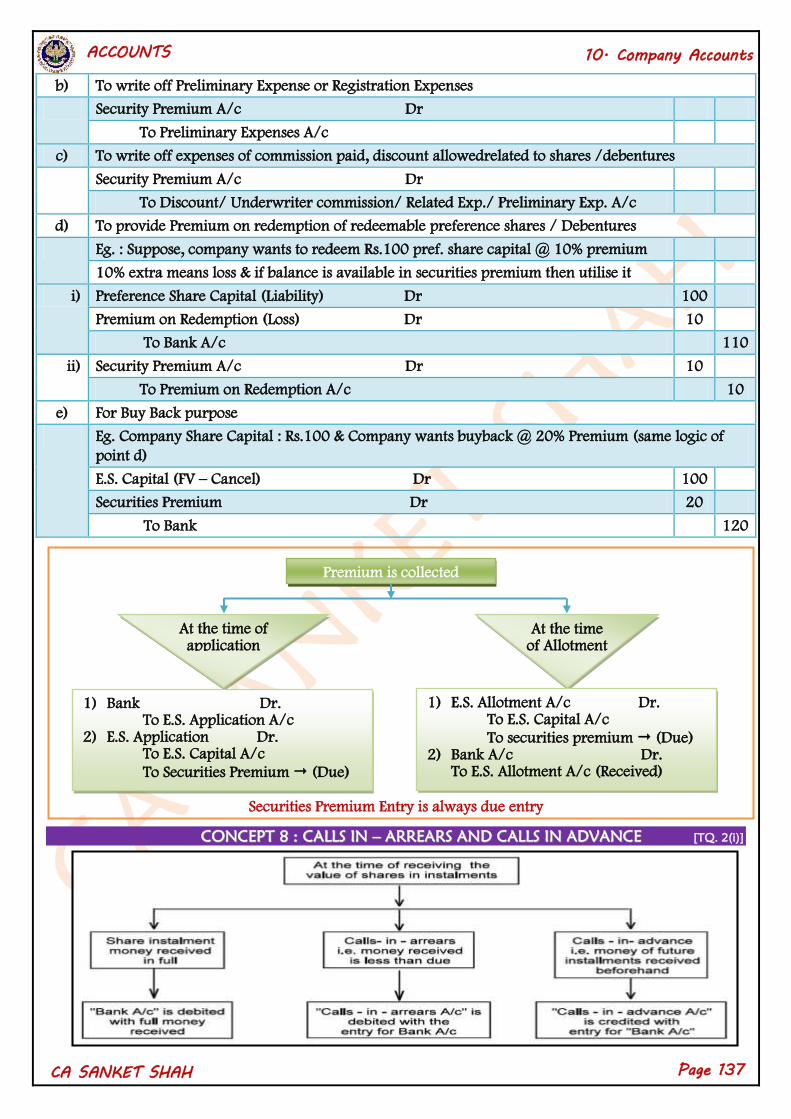

b) To write off Preliminary Expense or Registration Expenses

Security Premium A/c Dr

To Preliminary Expenses A/c

c) To write off expenses of commission paid, discount allowedrelated to shares /debentures

Security Premium A/c Dr

To Discount/ Underwriter commission/ Related Exp./ Preliminary Exp. A/c

d) To provide Premium on redemption of redeemable preference shares / Debentures

Eg. : Suppose, company wants to redeem Rs.100 pref. share capital @ 10% premium

10% extra means loss & if balance is available in securities premium then utilise it

i) Preference Share Capital (Liability) Dr 100

Premium on Redemption (Loss) Dr 10

To Bank A/c 110

ii) Security Premium A/c Dr 10

To Premium on Redemption A/c 10

e) For Buy Back purpose

Eg. Company Share Capital : Rs.100 & Company wants buyback @ 20% Premium (same logic of

point d)

E.S. Capital (FV – Cancel) Dr 100

Securities Premium Dr 20

To Bank 120

Securities Premium Entry is always due entry

CCOONNCCEEPPTT 88 :: CCAALLLLSS IINN –– AARRRREEAARRSS AANNDD CCAALLLLSS IINN AADDVVAANNCCEE [TQ. 2(i)]

At the time of application

At the time of Allotment

1) Bank Dr. To E.S. Application A/c

2) E.S. Application Dr. To E.S. Capital A/c

To Securities Premium (Due)

1) E.S. Allotment A/c Dr. To E.S. Capital A/c

To securities premium (Due) 2) Bank A/c Dr.

To E.S. Allotment A/c (Received)

Premium is collected

Page 138

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

CCAALLLLSS--IINN--AARRRREEAARRSS

Shareholders fail to pay the amount due on allotment or calls.

The total unpaid amount on one or more instalments is known as Calls-in-Arrears or Unpaid Calls.

It is shown by way of deduction from 'called-up capital' to arrive at paid-up value of the share capital.

For recording 'Calls-in-Arrears', the following journal entry is recorded :

Calls-in-Arrears A/c Dr. [Amount of Unpaid Calls]

To Share Allotment A/c

To Share Calls A/c

According to Table F interest at the rate of 10% per annum is to be charged on unpaid calls.

The journal entries for calls-in-arrears are as follows :

Sr. No. Particulars Dr Cr

1) For interest receivable on calls-in-arrears

Shareholders' A/c Dr.

To Interest on calls-in-arrears A/c

2) For receipt of interest

Bank A/c Dr.

To Shareholders' A/c

CCAALLLLSS--IINN--AADDVVAANNCCEE

Some shareholders may sometimes pay a part, or whole, of the amount not yet called up, such amount

is known as Calls-in-advance.

According to Table F, interest at a rate not exceeding 12 % p.a. is to be paid on such advance call

money.

This amount is credited in Calls-in-Advance A/c.

The following entry is recorded:

Sr. no. Particulars Dr Cr

1) Bank A/c Dr.

To Call-in-Advance A/c

When calls become actually due, calls-in-advance A/c is adjusted at the time of the call.

2) Calls-in-Advance A/c Dr. [Call amount due]

To Particular Call A/c

Interest on Calls-in-Advance

3) a) Interest Due

Interest on Calls-in-Advance A/c Dr. [Amount of interest due for payment]

To Shareholder's A/c

b) Payment of Interest

Shareholder's A/c Dr. [Amount of interest paid]

To Bank A/c (Interest paid on calls-in-advance)

CCAALLLL IINN AARRRREEAARRSS

Arrears

Advance

Interest Income

Interest Expense

10%

12%

From respective call upto amt received

From amt received upto respective call

Page 139

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

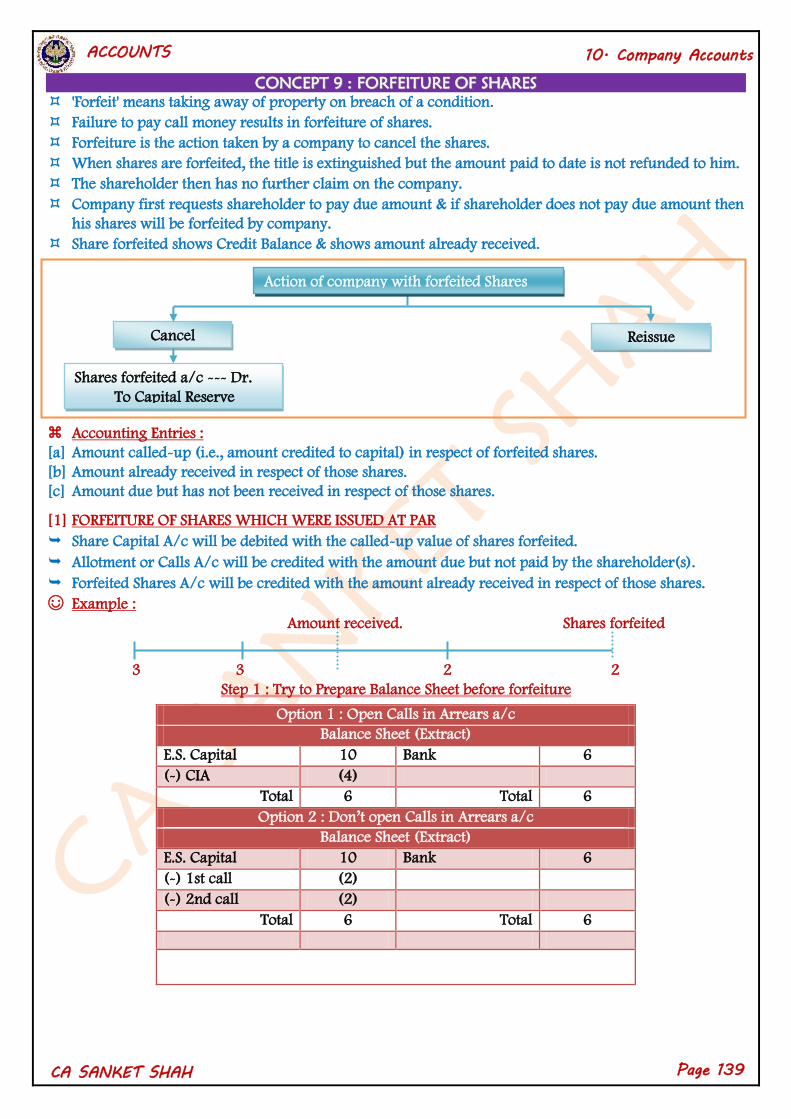

CCOONNCCEEPPTT 99 :: FFOORRFFEEIITTUURREE OOFF SSHHAARREESS

'Forfeit' means taking away of property on breach of a condition.

Failure to pay call money results in forfeiture of shares.

Forfeiture is the action taken by a company to cancel the shares.

When shares are forfeited, the title is extinguished but the amount paid to date is not refunded to him.

The shareholder then has no further claim on the company.

Company first requests shareholder to pay due amount & if shareholder does not pay due amount then

his shares will be forfeited by company.

Share forfeited shows Credit Balance & shows amount already received.

Accounting Entries :

[a] Amount called-up (i.e., amount credited to capital) in respect of forfeited shares.

[b] Amount already received in respect of those shares.

[c] Amount due but has not been received in respect of those shares.

[1] FORFEITURE OF SHARES WHICH WERE ISSUED AT PAR

Share Capital A/c will be debited with the called-up value of shares forfeited.

Allotment or Calls A/c will be credited with the amount due but not paid by the shareholder(s).

Forfeited Shares A/c will be credited with the amount already received in respect of those shares.

☺ Example :

Amount received. Shares forfeited

3 3 2 2

Step 1 : Try to Prepare Balance Sheet before forfeiture

Option 1 : Open Calls in Arrears a/c

Balance Sheet (Extract)

E.S. Capital 10 Bank 6

(-) CIA (4)

Total 6 Total 6

Option 2 : Don’t open Calls in Arrears a/c

Balance Sheet (Extract)

E.S. Capital 10 Bank 6

(-) 1st call (2)

(-) 2nd call (2)

Total 6 Total 6

Cancel Reissue

Shares forfeited a/c --- Dr.

To Capital Reserve

Action of company with forfeited Shares

Page 140

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

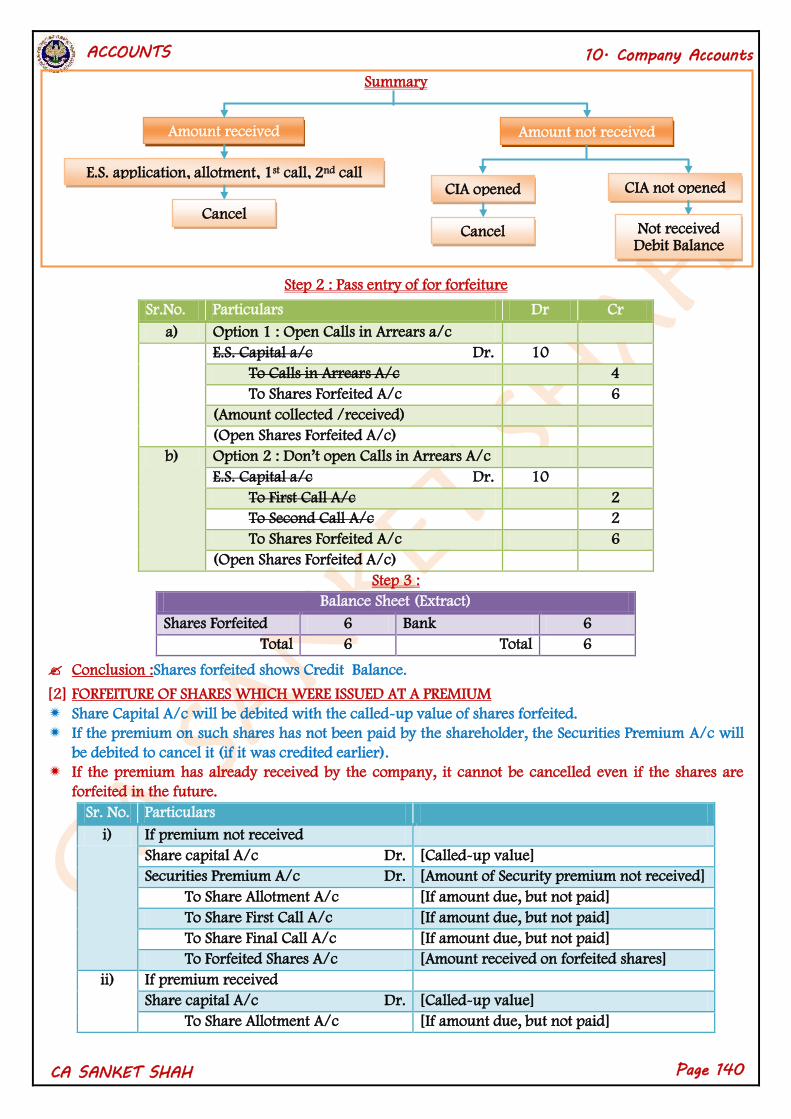

Summary

Step 2 : Pass entry of for forfeiture

Sr.No. Particulars Dr Cr

a) Option 1 : Open Calls in Arrears a/c

E.S. Capital a/c Dr. 10

To Calls in Arrears A/c 4

To Shares Forfeited A/c 6

(Amount collected /received)

(Open Shares Forfeited A/c)

b) Option 2 : Don’t open Calls in Arrears A/c

E.S. Capital a/c Dr. 10

To First Call A/c 2

To Second Call A/c 2

To Shares Forfeited A/c 6

(Open Shares Forfeited A/c)

Step 3 :

Balance Sheet (Extract)

Shares Forfeited 6 Bank 6

Total 6 Total 6

Conclusion :Shares forfeited shows Credit Balance.

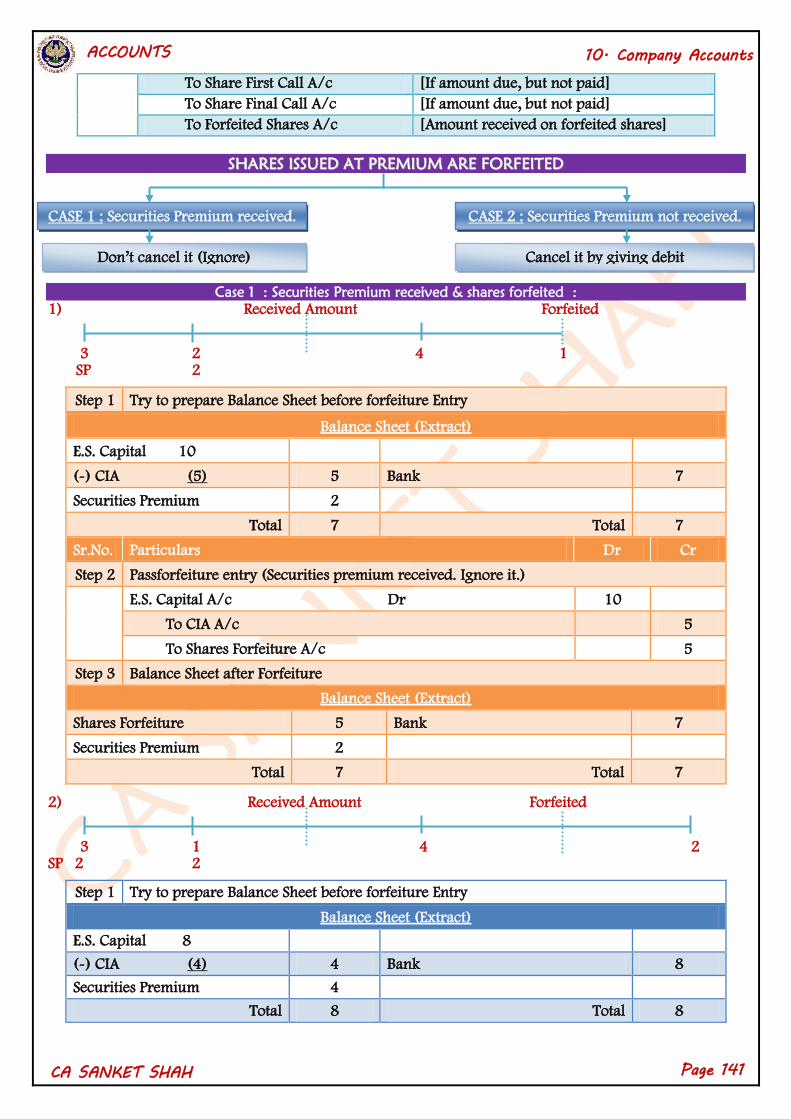

[2] FORFEITURE OF SHARES WHICH WERE ISSUED AT A PREMIUM

Share Capital A/c will be debited with the called-up value of shares forfeited.

If the premium on such shares has not been paid by the shareholder, the Securities Premium A/c will

be debited to cancel it (if it was credited earlier).

If the premium has already received by the company, it cannot be cancelled even if the shares are

forfeited in the future.

Sr. No. Particulars

i) If premium not received

Share capital A/c Dr. [Called-up value]

Securities Premium A/c Dr. [Amount of Security premium not received]

To Share Allotment A/c [If amount due, but not paid]

To Share First Call A/c [If amount due, but not paid]

To Share Final Call A/c [If amount due, but not paid]

To Forfeited Shares A/c [Amount received on forfeited shares]

ii) If premium received

Share capital A/c Dr. [Called-up value]

To Share Allotment A/c [If amount due, but not paid]

Amount received Amount not received

E.S. application, allotment, 1st call, 2nd call CIA opened CIA not opened

Cancel Not received

Debit Balance Cancel

Page 141

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

To Share First Call A/c [If amount due, but not paid]

To Share Final Call A/c [If amount due, but not paid]

To Forfeited Shares A/c [Amount received on forfeited shares]

SSHHAARREESS IISSSSUUEEDD AATT PPRREEMMIIUUMM AARREE FFOORRFFEEIITTEEDD

Case 1 : Securities Premium received & shares forfeited :

1) Received Amount Forfeited

3 2 4 1 SP 2

Step 1 Try to prepare Balance Sheet before forfeiture Entry

Balance Sheet (Extract)

E.S. Capital 10

(-) CIA (5) 5 Bank 7

Securities Premium 2

Total 7 Total 7

Sr.No. Particulars Dr Cr

Step 2 Passforfeiture entry (Securities premium received. Ignore it.)

E.S. Capital A/c Dr 10

To CIA A/c 5

To Shares Forfeiture A/c 5

Step 3 Balance Sheet after Forfeiture

Balance Sheet (Extract)

Shares Forfeiture 5 Bank 7

Securities Premium 2

Total 7 Total 7

2) Received Amount Forfeited

3 1 4 2 SP 2 2

Step 1 Try to prepare Balance Sheet before forfeiture Entry

Balance Sheet (Extract)

E.S. Capital 8

(-) CIA (4) 4 Bank 8

Securities Premium 4

Total 8 Total 8

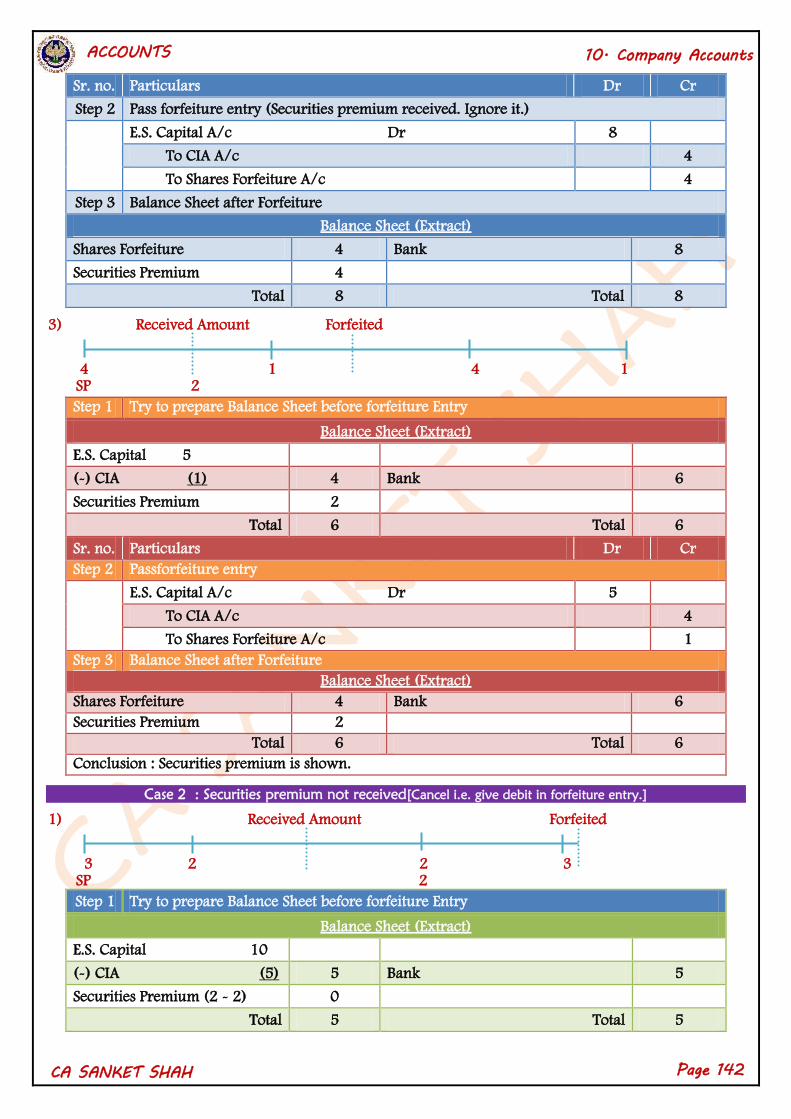

CASE 1 : Securities Premium received.

CASE 2 : Securities Premium not received.

Don’t cancel it (Ignore) Cancel it by giving debit

Page 142

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

Sr. no. Particulars Dr Cr

Step 2 Pass forfeiture entry (Securities premium received. Ignore it.)

E.S. Capital A/c Dr 8

To CIA A/c 4

To Shares Forfeiture A/c 4

Step 3 Balance Sheet after Forfeiture

Balance Sheet (Extract)

Shares Forfeiture 4 Bank 8

Securities Premium 4

Total 8 Total 8

3) Received Amount Forfeited

4 1 4 1 SP 2

Step 1 Try to prepare Balance Sheet before forfeiture Entry

Balance Sheet (Extract)

E.S. Capital 5

(-) CIA (1) 4 Bank 6

Securities Premium 2

Total 6 Total 6

Sr. no. Particulars Dr Cr

Step 2 Passforfeiture entry

E.S. Capital A/c Dr 5

To CIA A/c 4

To Shares Forfeiture A/c 1

Step 3 Balance Sheet after Forfeiture

Balance Sheet (Extract)

Shares Forfeiture 4 Bank 6

Securities Premium 2

Total 6 Total 6

Conclusion : Securities premium is shown.

Case 2 : Securities premium not received[Cancel i.e. give debit in forfeiture entry.]

1) Received Amount Forfeited

3 2 2 3 SP 2

Step 1 Try to prepare Balance Sheet before forfeiture Entry

Balance Sheet (Extract)

E.S. Capital 10

(-) CIA (5) 5 Bank 5

Securities Premium (2 - 2) 0

Total 5 Total 5

Page 143

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

Sr. no. Particulars Dr Cr

Step 2 Pass forfeiture entry

E.S. Capital A/c Dr 10

Securities Premium A/c Dr 2

To CIA A/c (5 + 2) 7

To Shares Forfeiture A/c 5

Step 3 Balance Sheet after Forfeiture

Balance Sheet (Extract)

Shares Forfeiture 5 Bank 5

Total 5 Total 5

Conclusion : Securities premium not shown in Balance Sheet

Securities Premium

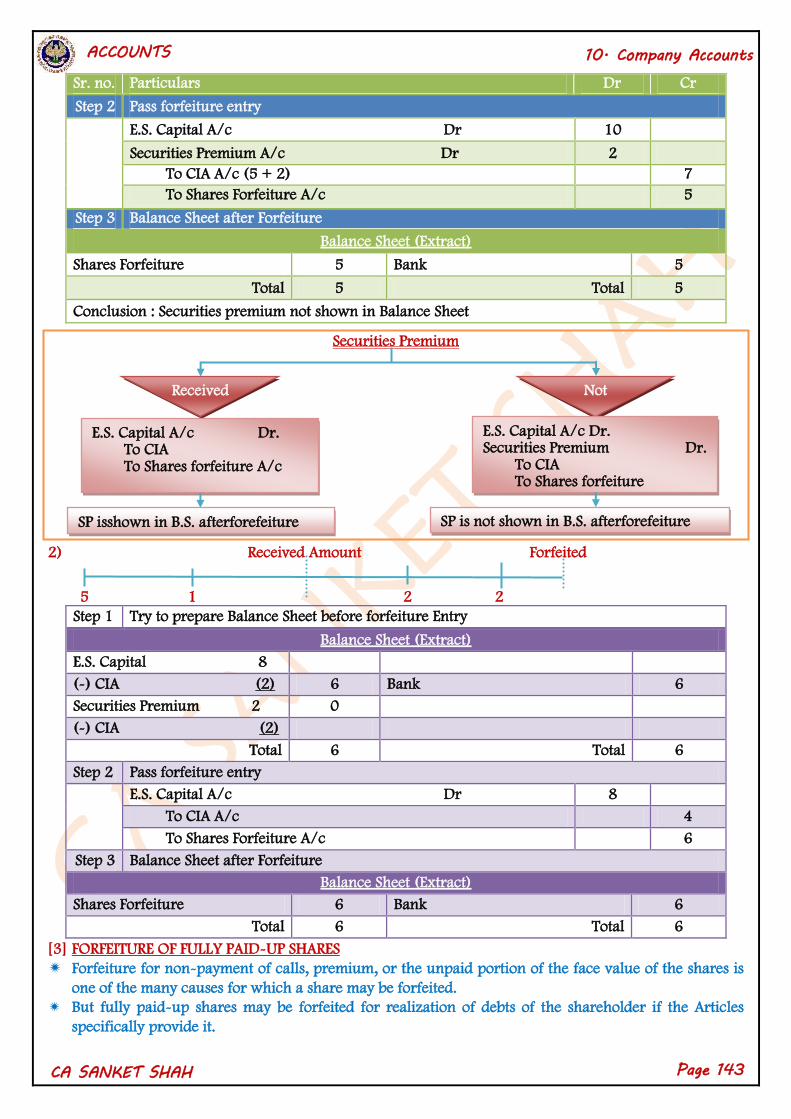

2) Received Amount Forfeited

5 1 2 2

Step 1 Try to prepare Balance Sheet before forfeiture Entry

Balance Sheet (Extract)

E.S. Capital 8

(-) CIA (2) 6 Bank 6

Securities Premium 2 0

(-) CIA (2)

Total 6 Total 6

Step 2 Pass forfeiture entry

E.S. Capital A/c Dr 8

To CIA A/c 4

To Shares Forfeiture A/c 6

Step 3 Balance Sheet after Forfeiture

Balance Sheet (Extract)

Shares Forfeiture 6 Bank 6

Total 6 Total 6

[3] FORFEITURE OF FULLY PAID-UP SHARES

Forfeiture for non-payment of calls, premium, or the unpaid portion of the face value of the shares is

one of the many causes for which a share may be forfeited.

But fully paid-up shares may be forfeited for realization of debts of the shareholder if the Articles

specifically provide it.

Received Not

Received

E.S. Capital A/c Dr. To CIA To Shares forfeiture A/c

E.S. Capital A/c Dr. Securities Premium Dr. To CIA To Shares forfeiture

SP isshown in B.S. afterforefeiture SP is not shown in B.S. afterforefeiture

Page 144

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

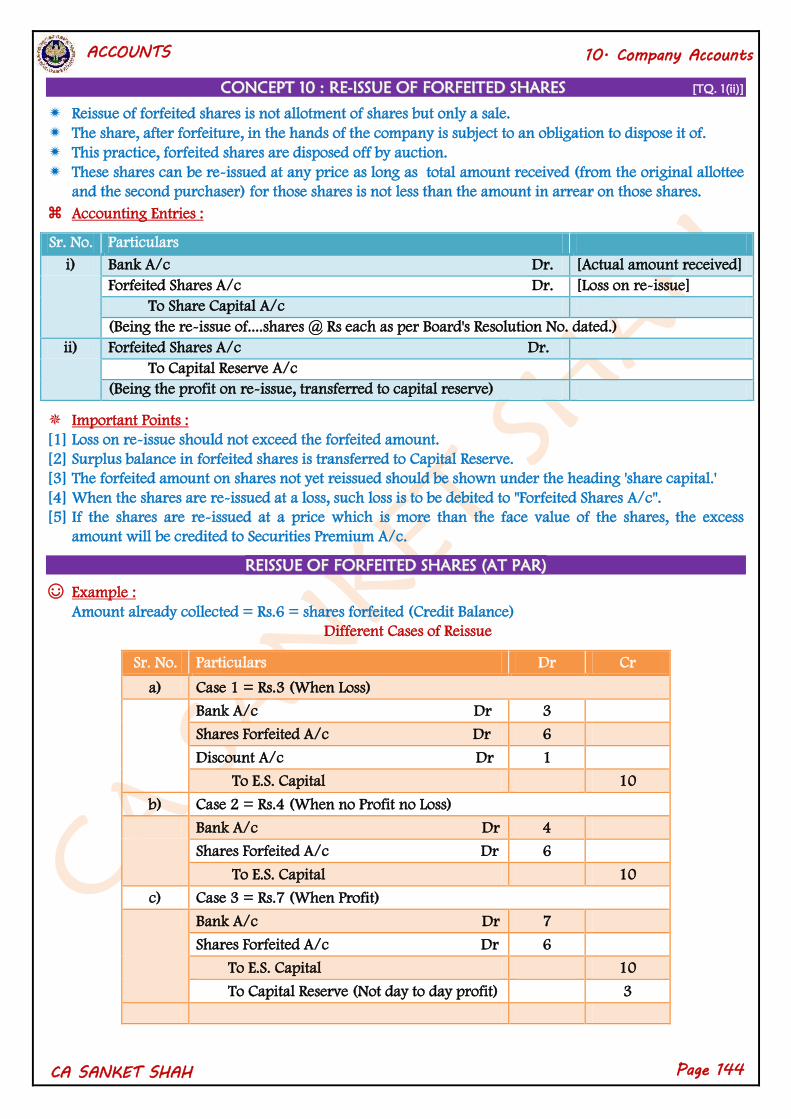

CCOONNCCEEPPTT 1100 :: RREE--IISSSSUUEE OOFF FFOORRFFEEIITTEEDD SSHHAARREESS [TQ. 1(ii)]

Reissue of forfeited shares is not allotment of shares but only a sale.

The share, after forfeiture, in the hands of the company is subject to an obligation to dispose it of.

This practice, forfeited shares are disposed off by auction.

These shares can be re-issued at any price as long as total amount received (from the original allottee

and the second purchaser) for those shares is not less than the amount in arrear on those shares.

Accounting Entries :

Sr. No. Particulars

i) Bank A/c Dr. [Actual amount received]

Forfeited Shares A/c Dr. [Loss on re-issue]

To Share Capital A/c

(Being the re-issue of....shares @ Rs each as per Board's Resolution No. dated.)

ii) Forfeited Shares A/c Dr.

To Capital Reserve A/c

(Being the profit on re-issue, transferred to capital reserve)

Important Points :

[1] Loss on re-issue should not exceed the forfeited amount.

[2] Surplus balance in forfeited shares is transferred to Capital Reserve.

[3] The forfeited amount on shares not yet reissued should be shown under the heading 'share capital.'

[4] When the shares are re-issued at a loss, such loss is to be debited to "Forfeited Shares A/c".

[5] If the shares are re-issued at a price which is more than the face value of the shares, the excess

amount will be credited to Securities Premium A/c.

RREEIISSSSUUEE OOFF FFOORRFFEEIITTEEDD SSHHAARREESS ((AATT PPAARR))

☺ Example :

Amount already collected = Rs.6 = shares forfeited (Credit Balance)

Different Cases of Reissue

Sr. No. Particulars Dr Cr

a) Case 1 = Rs.3 (When Loss)

Bank A/c Dr 3

Shares Forfeited A/c Dr 6

Discount A/c Dr 1

To E.S. Capital 10

b) Case 2 = Rs.4 (When no Profit no Loss)

Bank A/c Dr 4

Shares Forfeited A/c Dr 6

To E.S. Capital 10

c) Case 3 = Rs.7 (When Profit)

Bank A/c Dr 7

Shares Forfeited A/c Dr 6

To E.S. Capital 10

To Capital Reserve (Not day to day profit) 3

Page 145

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

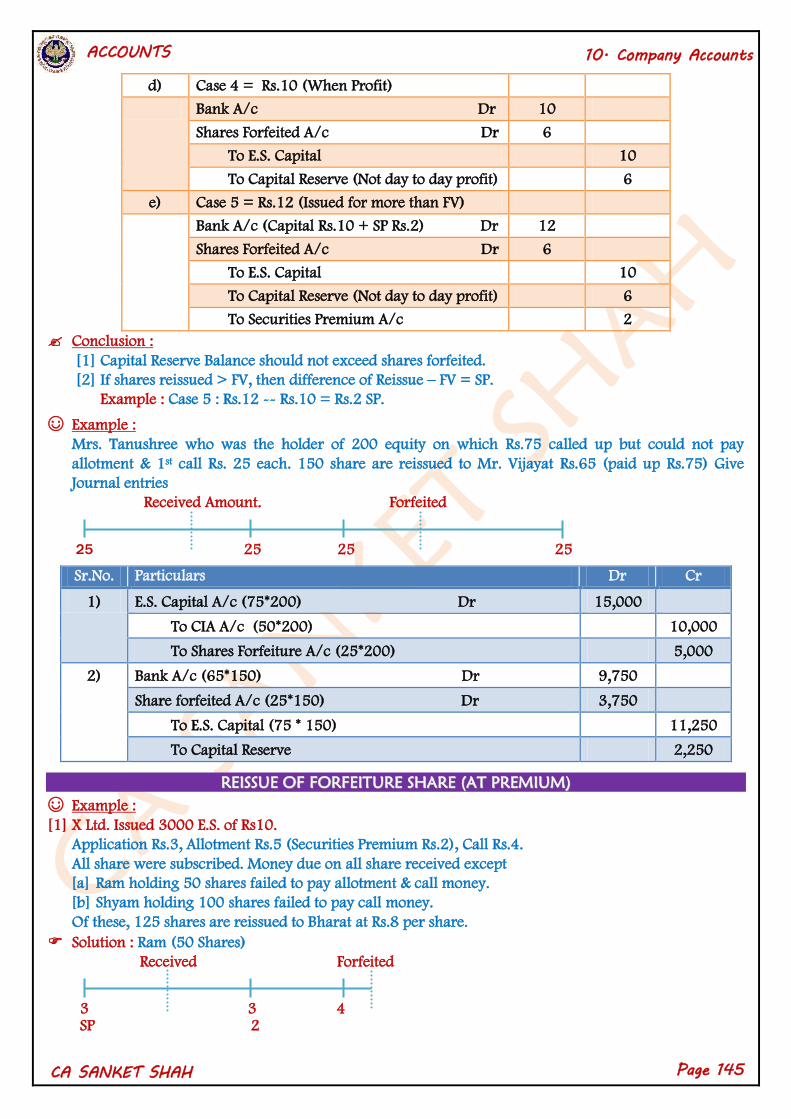

d) Case 4 = Rs.10 (When Profit)

Bank A/c Dr 10

Shares Forfeited A/c Dr 6

To E.S. Capital 10

To Capital Reserve (Not day to day profit) 6

e) Case 5 = Rs.12 (Issued for more than FV)

Bank A/c (Capital Rs.10 + SP Rs.2) Dr 12

Shares Forfeited A/c Dr 6

To E.S. Capital 10

To Capital Reserve (Not day to day profit) 6

To Securities Premium A/c 2

Conclusion :

[1] Capital Reserve Balance should not exceed shares forfeited.

[2] If shares reissued > FV, then difference of Reissue – FV = SP.

Example : Case 5 : Rs.12 -- Rs.10 = Rs.2 SP.

☺ Example :

Mrs. Tanushree who was the holder of 200 equity on which Rs.75 called up but could not pay

allotment & 1st call Rs. 25 each. 150 share are reissued to Mr. Vijayat Rs.65 (paid up Rs.75) Give

Journal entries

Received Amount. Forfeited

25 25 25 25

Sr.No. Particulars Dr Cr

1) E.S. Capital A/c (75*200) Dr 15,000

To CIA A/c (50*200) 10,000

To Shares Forfeiture A/c (25*200) 5,000

2) Bank A/c (65*150) Dr 9,750

Share forfeited A/c (25*150) Dr 3,750

To E.S. Capital (75 * 150) 11,250

To Capital Reserve 2,250

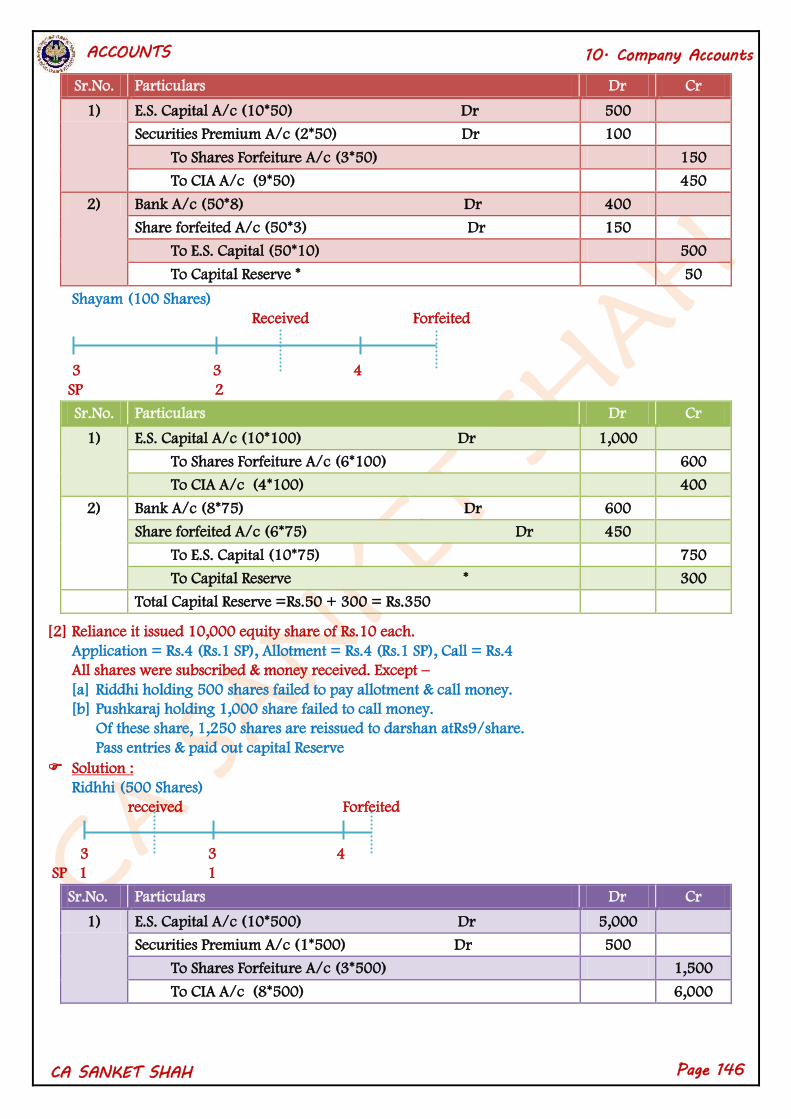

RREEIISSSSUUEE OOFF FFOORRFFEEIITTUURREE SSHHAARREE ((AATT PPRREEMMIIUUMM))

☺ Example :

[1] X Ltd. Issued 3000 E.S. of Rs10.

Application Rs.3, Allotment Rs.5 (Securities Premium Rs.2), Call Rs.4.

All share were subscribed. Money due on all share received except

[a] Ram holding 50 shares failed to pay allotment & call money.

[b] Shyam holding 100 shares failed to pay call money.

Of these, 125 shares are reissued to Bharat at Rs.8 per share.

Solution : Ram (50 Shares)

Received Forfeited

3 3 4 SP 2

Page 146

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

Sr.No. Particulars Dr Cr

1) E.S. Capital A/c (10*50) Dr 500

Securities Premium A/c (2*50) Dr 100

To Shares Forfeiture A/c (3*50) 150

To CIA A/c (9*50) 450

2) Bank A/c (50*8) Dr 400

Share forfeited A/c (50*3) Dr 150

To E.S. Capital (50*10) 500

To Capital Reserve * 50

Shayam (100 Shares)

Received Forfeited

3 3 4

SP 2

Sr.No. Particulars Dr Cr

1) E.S. Capital A/c (10*100) Dr 1,000

To Shares Forfeiture A/c (6*100) 600

To CIA A/c (4*100) 400

2) Bank A/c (8*75) Dr 600

Share forfeited A/c (6*75) Dr 450

To E.S. Capital (10*75) 750

To Capital Reserve * 300

Total Capital Reserve =Rs.50 + 300 = Rs.350

[2] Reliance it issued 10,000 equity share of Rs.10 each.

Application = Rs.4 (Rs.1 SP), Allotment = Rs.4 (Rs.1 SP), Call = Rs.4

All shares were subscribed & money received. Except –

[a] Riddhi holding 500 shares failed to pay allotment & call money.

[b] Pushkaraj holding 1,000 share failed to call money.

Of these share, 1,250 shares are reissued to darshan atRs9/share.

Pass entries & paid out capital Reserve

Solution :

Ridhhi (500 Shares)

received Forfeited

3 3 4

SP 1 1

Sr.No. Particulars Dr Cr

1) E.S. Capital A/c (10*500) Dr 5,000

Securities Premium A/c (1*500) Dr 500

To Shares Forfeiture A/c (3*500) 1,500

To CIA A/c (8*500) 6,000

Page 147

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

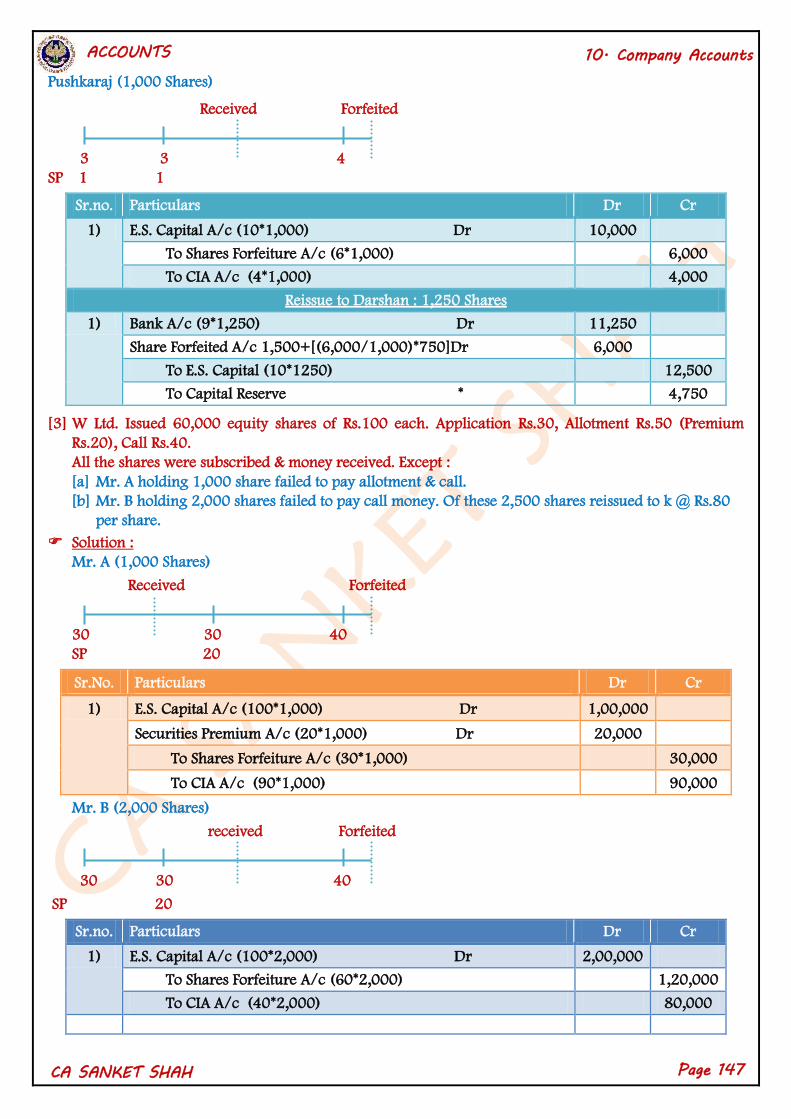

Pushkaraj (1,000 Shares)

Received Forfeited

3 3 4

SP 1 1

Sr.no. Particulars Dr Cr

1) E.S. Capital A/c (10*1,000) Dr 10,000

To Shares Forfeiture A/c (6*1,000) 6,000

To CIA A/c (4*1,000) 4,000

Reissue to Darshan : 1,250 Shares

1) Bank A/c (9*1,250) Dr 11,250

Share Forfeited A/c 1,500+[(6,000/1,000)*750]Dr 6,000

To E.S. Capital (10*1250) 12,500

To Capital Reserve * 4,750

[3] W Ltd. Issued 60,000 equity shares of Rs.100 each. Application Rs.30, Allotment Rs.50 (Premium

Rs.20), Call Rs.40.

All the shares were subscribed & money received. Except :

[a] Mr. A holding 1,000 share failed to pay allotment & call.

[b] Mr. B holding 2,000 shares failed to pay call money. Of these 2,500 shares reissued to k @ Rs.80

per share.

Solution :

Mr. A (1,000 Shares)

Received Forfeited

30 30 40

SP 20

Sr.No. Particulars Dr Cr

1) E.S. Capital A/c (100*1,000) Dr 1,00,000

Securities Premium A/c (20*1,000) Dr 20,000

To Shares Forfeiture A/c (30*1,000) 30,000

To CIA A/c (90*1,000) 90,000

Mr. B (2,000 Shares)

received Forfeited

30 30 40

SP 20

Sr.no. Particulars Dr Cr

1) E.S. Capital A/c (100*2,000) Dr 2,00,000

To Shares Forfeiture A/c (60*2,000) 1,20,000

To CIA A/c (40*2,000) 80,000

Page 148

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

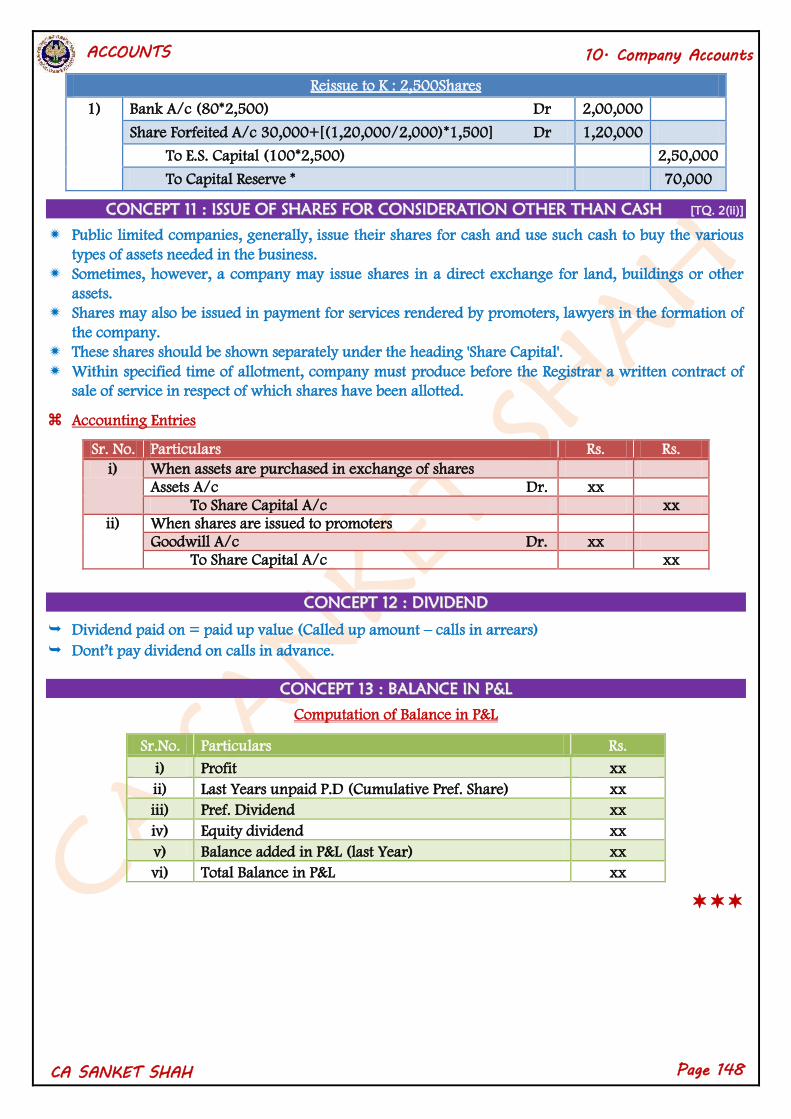

Reissue to K : 2,500Shares

1) Bank A/c (80*2,500) Dr 2,00,000

Share Forfeited A/c 30,000+[(1,20,000/2,000)*1,500] Dr 1,20,000

To E.S. Capital (100*2,500) 2,50,000

To Capital Reserve * 70,000

CCOONNCCEEPPTT 1111 :: IISSSSUUEE OOFF SSHHAARREESS FFOORR CCOONNSSIIDDEERRAATTIIOONN OOTTHHEERR TTHHAANN CCAASSHH [TQ. 2(ii)]

Public limited companies, generally, issue their shares for cash and use such cash to buy the various

types of assets needed in the business.

Sometimes, however, a company may issue shares in a direct exchange for land, buildings or other

assets.

Shares may also be issued in payment for services rendered by promoters, lawyers in the formation of

the company.

These shares should be shown separately under the heading 'Share Capital'.

Within specified time of allotment, company must produce before the Registrar a written contract of

sale of service in respect of which shares have been allotted.

Accounting Entries

Sr. No. Particulars Rs. Rs.

i) When assets are purchased in exchange of shares Assets A/c Dr. xx To Share Capital A/c xx

ii) When shares are issued to promoters Goodwill A/c Dr. xx To Share Capital A/c xx

CCOONNCCEEPPTT 1122 :: DDIIVVIIDDEENNDD

Dividend paid on = paid up value (Called up amount – calls in arrears)

Dont’t pay dividend on calls in advance.

CCOONNCCEEPPTT 1133 :: BBAALLAANNCCEE IINN PP&&LL

Computation of Balance in P&L

Sr.No. Particulars Rs.

i) Profit xx

ii) Last Years unpaid P.D (Cumulative Pref. Share) xx

iii) Pref. Dividend xx

iv) Equity dividend xx

v) Balance added in P&L (last Year) xx

vi) Total Balance in P&L xx

Page 149

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

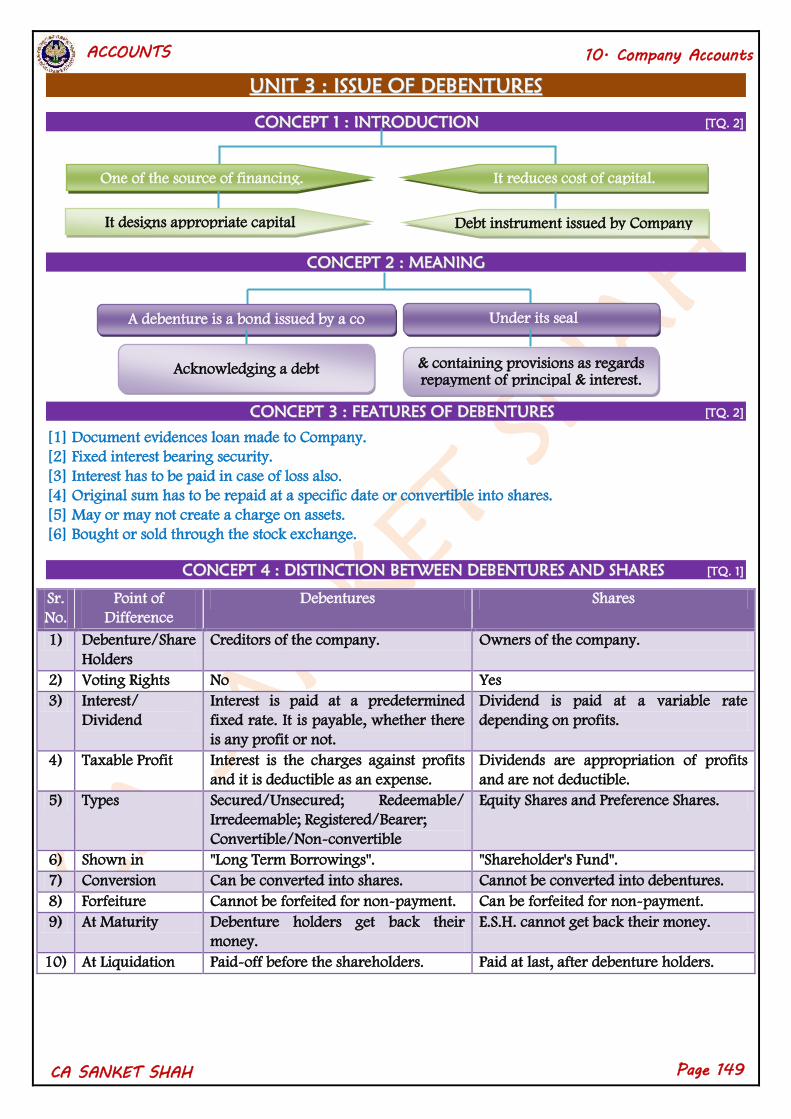

UUNNIITT 33 :: IISSSSUUEE OOFF DDEEBBEENNTTUURREESS

CCOONNCCEEPPTT 11 :: IINNTTRROODDUUCCTTIIOONN [TQ. 2]

CCOONNCCEEPPTT 22 :: MMEEAANNIINNGG

CCOONNCCEEPPTT 33 :: FFEEAATTUURREESS OOFF DDEEBBEENNTTUURREESS [TQ. 2]

[1] Document evidences loan made to Company.

[2] Fixed interest bearing security.

[3] Interest has to be paid in case of loss also.

[4] Original sum has to be repaid at a specific date or convertible into shares.

[5] May or may not create a charge on assets.

[6] Bought or sold through the stock exchange.

CCOONNCCEEPPTT 44 :: DDIISSTTIINNCCTTIIOONN BBEETTWWEEEENN DDEEBBEENNTTUURREESS AANNDD SSHHAARREESS [TQ. 1]

Sr.

No.

Point of

Difference

Debentures Shares

1) Debenture/Share

Holders

Creditors of the company. Owners of the company.

2) Voting Rights No Yes

3) Interest/

Dividend

Interest is paid at a predetermined

fixed rate. It is payable, whether there

is any profit or not.

Dividend is paid at a variable rate

depending on profits.

4) Taxable Profit Interest is the charges against profits

and it is deductible as an expense.

Dividends are appropriation of profits

and are not deductible.

5) Types Secured/Unsecured; Redeemable/

Irredeemable; Registered/Bearer;

Convertible/Non-convertible

Equity Shares and Preference Shares.

6) Shown in "Long Term Borrowings". "Shareholder's Fund".

7) Conversion Can be converted into shares. Cannot be converted into debentures.

8) Forfeiture Cannot be forfeited for non-payment. Can be forfeited for non-payment.

9) At Maturity Debenture holders get back their

money.

E.S.H. cannot get back their money.

10) At Liquidation Paid-off before the shareholders. Paid at last, after debenture holders.

One of the source of financing.

It reduces cost of capital.

It designs appropriate capital structure.

Debt instrument issued by Company

A debenture is a bond issued by a co Under its seal

Acknowledging a debt

& containing provisions as regards repayment of principal & interest.

Page 150

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

CCOONNCCEEPPTT 55 :: TTYYPPEESS OOFF DDEEBBEENNTTUURREESS

Sr. no. Type Explanation

1] SECURITY :

a] Secured Debentures These are secured by a charge upon some or all assets of the company.

There are two types of charges :

[i] Fixed charge; and

[ii] Floating charge.

A fixed charge is a mortgage on specific assets.

These assets cannot be sold without consent of the debenture holders.

Sale proceeds of these assets are utilized first for repaying debenture

holders.

A floating charge generally covers all the assets of the company

including future one.

b] Unsecured or

"Naked" Debentures

:

These debentures are not secured by any charge upon any assets.

A company merely promises to pay interest on due dates and to repay

the amount due on maturity date.

These types of debentures are very risky from investor view point.

2] CONVERTIBILITY :

a] Convertible

Debentures : These are debentures which will be converted into equity shares

(either at par or premium or discount) after a certain period of time

from the date of its issue.

These debentures may be fully or partly convertible.

In future, holders get a chance to become shareholders of the co.

b] Non-Convertible

Debentures : These are debentures which cannot be converted into shares in future.

As per the terms of issue, these debentures are repaid.

3] PERMANENCE :

a] Redeemable

Debentures : These debentures are repayable as per the terms of issue, for example,

after 8 years from the date of issue.

b] Irredeemable

Debentures : These debentures are not repayable during the life time of the co.

These are also called perpetual debentures.

These are repaid only at the time of liquidation.

4] NEGOTIABILITY :

a] Registered

Debentures : These are payable to a registered holder whose name, address &

particulars of holding is recorded in the Register of Debenture holders.

They are not easily transferable.

The provisions of the Companies Act, 2013 are to be complied with for

effecting transfer of these debentures.

Debenture interest is paid either to the order of registered holder or the

bearer of the interest coupons.

Security Convertibility

Permanence

Negotiability

Priority

Secured

Unsecured

Convertible

Non Convertible

Redeemable

Irredeemable

Registered

Bearer

Second Mortgage

First Mortgage

Page 151

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

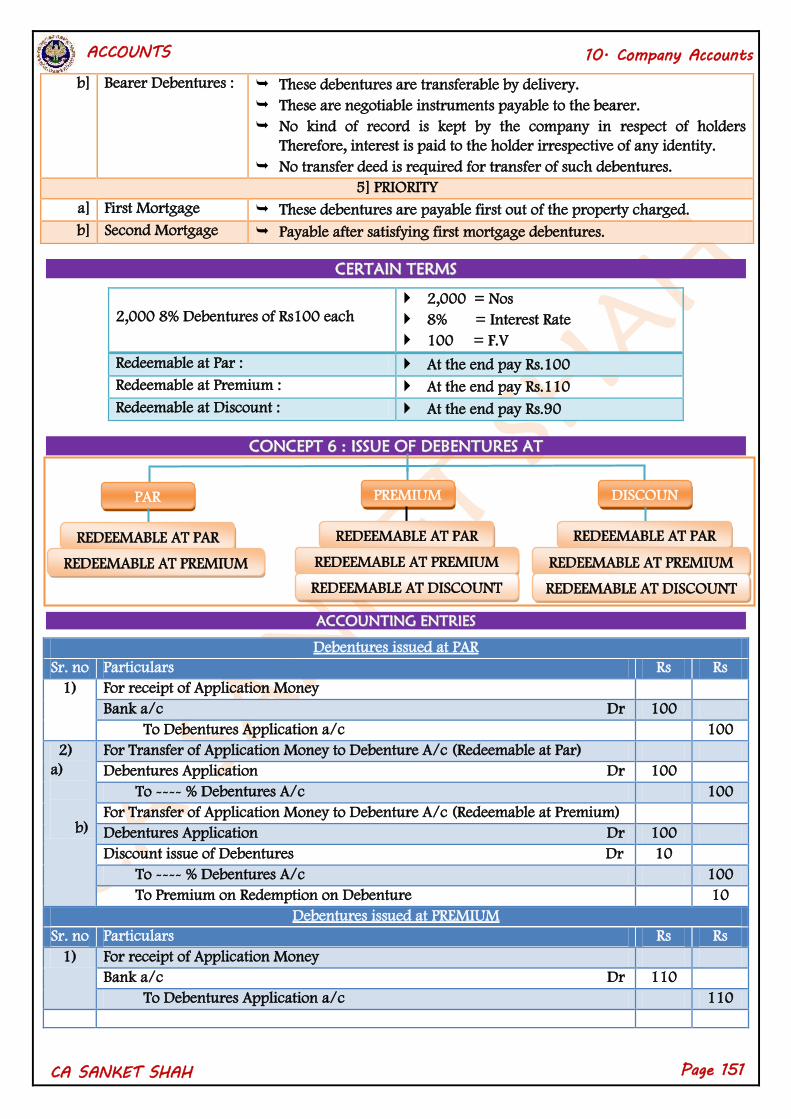

b] Bearer Debentures : These debentures are transferable by delivery.

These are negotiable instruments payable to the bearer.

No kind of record is kept by the company in respect of holders

Therefore, interest is paid to the holder irrespective of any identity.

No transfer deed is required for transfer of such debentures.

5] PRIORITY

a] First Mortgage These debentures are payable first out of the property charged.

b] Second Mortgage Payable after satisfying first mortgage debentures.

CCEERRTTAAIINN TTEERRMMSS

2,000 8% Debentures of Rs100 each 2,000 = Nos

8% = Interest Rate

100 = F.V

Redeemable at Par : At the end pay Rs.100

Redeemable at Premium : At the end pay Rs.110

Redeemable at Discount : At the end pay Rs.90

CCOONNCCEEPPTT 66 :: IISSSSUUEE OOFF DDEEBBEENNTTUURREESS AATT

AACCCCOOUUNNTTIINNGG EENNTTRRIIEESS

Debentures issued at PAR

Sr. no Particulars Rs Rs

1) For receipt of Application Money

Bank a/c Dr 100

To Debentures Application a/c 100

2)

a)

b)

For Transfer of Application Money to Debenture A/c (Redeemable at Par)

Debentures Application Dr 100

To ---- % Debentures A/c 100

For Transfer of Application Money to Debenture A/c (Redeemable at Premium)

Debentures Application Dr 100

Discount issue of Debentures Dr 10

To ---- % Debentures A/c 100

To Premium on Redemption on Debenture 10

Debentures issued at PREMIUM

Sr. no Particulars Rs Rs

1) For receipt of Application Money

Bank a/c Dr 110

To Debentures Application a/c 110

PAR

PREMIUM

DISCOUN

T

REDEEMABLE AT PAR

REDEEMABLE AT PREMIUM

REDEEMABLE AT PAR

REDEEMABLE AT PREMIUM

REDEEMABLE AT DISCOUNT

REDEEMABLE AT PAR

REDEEMABLE AT PREMIUM

REDEEMABLE AT DISCOUNT

Page 152

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

2)

a)

b)

Transfer of Application Money to Debenture A/c (Redeemable at Par & Disc)

Debentures Application Dr 110

To ---- % Debentures A/c 100

To Security Premium A/c 10

For Transfer of Application Money to Debenture A/c (Redeemable at Premium)

Debentures Application Dr 110

Loss on issue of Debentures Dr 5

To ---- % Debentures A/c 100

To Security Premium A/c 10

To Premium on Redemption on Debenture 5

Debentures issued at DISCOUNT

Sr. no Particulars Rs Rs

1) For receipt of Application Money

Bank a/c Dr 90

To Debentures Application a/c 90

2)

a)

b)

Transfer of Application Money to Debenture A/c (Redeemable at Par & Disc)

Debentures Application Dr 90

Discount on issue of Debenture A/c Dr 10

To ----- % Debenture A/c 100

For Transfer of Application Money to Debenture A/c (Redeemable at Premium)

Debentures Application Dr 90

Discount / Loss on issue of Debenture Dr 25

To ---- % Debentures A/c 100

To Premium on Redemption on Debenture A/c 15

UUTTIILLIISSAATTIIOONN OOFF DDEEBBEENNTTUURREESS PPRREEMMIIUUMM

The premium on debentures is credited to Security Premium Account.

Restriction of utilisation of debentures premium will also be governed by Sec 52 of Companies Act

2013.

Security Premium can be utilised for :

[a] Issue of Fully Paid Bonus Shares

[b] Writing off Preliminary Expenses

[c] Writing off : i) Expenses Incurred

ii) Commission paid

iii) Disc allowed on issue of debentures or shares of the company.

[d] Providing premium on redemption of debentures or Preference shares

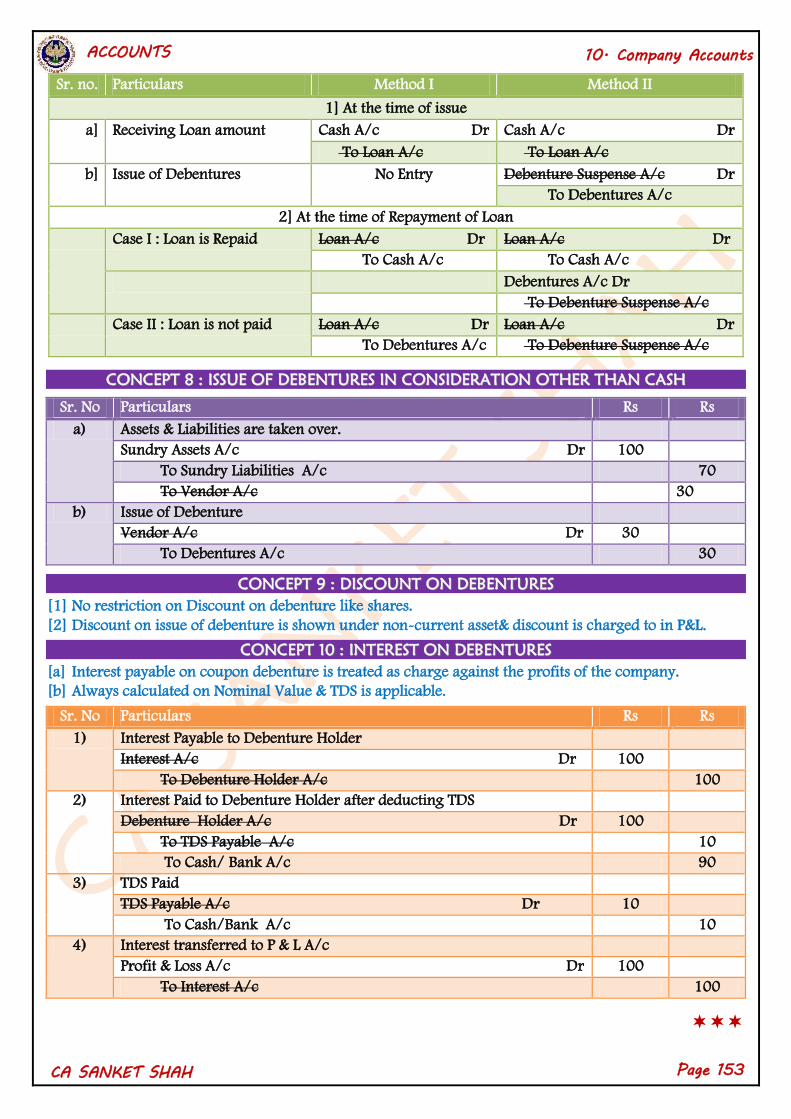

CCOONNCCEEPPTT 77 :: IISSSSUUEE OOFF DDEEBBEENNTTUURREESS AASS CCOOLLLLAATTEERRAALL SSEECCUURRIITTYY

Collateral Security means Secondary security for loan if loan is unpaid.

The holder of such debentures is entitled to interest only on amount of loan.

METHOD I : NO DEBENTURE

ENTRIES AT THE TIME OF ISSUE

METHOD II : DEBENTURE

ENTRIES AT THE TIME OF ISSUE

METHOD OF ACCOUNTING

Page 153

ACCOUNTS

10. Company Accounts

CA SANKET SHAH

Sr. no. Particulars Method I Method II

1] At the time of issue

a] Receiving Loan amount Cash A/c Dr Cash A/c Dr

To Loan A/c To Loan A/c

b] Issue of Debentures No Entry Debenture Suspense A/c Dr

To Debentures A/c

2] At the time of Repayment of Loan

Case I : Loan is Repaid Loan A/c Dr Loan A/c Dr

To Cash A/c To Cash A/c

Debentures A/c Dr

To Debenture Suspense A/c

Case II : Loan is not paid Loan A/c Dr Loan A/c Dr

To Debentures A/c To Debenture Suspense A/c

CCOONNCCEEPPTT 88 :: IISSSSUUEE OOFF DDEEBBEENNTTUURREESS IINN CCOONNSSIIDDEERRAATTIIOONN OOTTHHEERR TTHHAANN CCAASSHH

Sr. No Particulars Rs Rs

a) Assets & Liabilities are taken over.

Sundry Assets A/c Dr 100

To Sundry Liabilities A/c 70

To Vendor A/c 30

b) Issue of Debenture

Vendor A/c Dr 30

To Debentures A/c 30

CCOONNCCEEPPTT 99 :: DDIISSCCOOUUNNTT OONN DDEEBBEENNTTUURREESS

[1] No restriction on Discount on debenture like shares.

[2] Discount on issue of debenture is shown under non-current asset& discount is charged to in P&L.

CCOONNCCEEPPTT 1100 :: IINNTTEERREESSTT OONN DDEEBBEENNTTUURREESS

[a] Interest payable on coupon debenture is treated as charge against the profits of the company.

[b] Always calculated on Nominal Value & TDS is applicable.

Sr. No Particulars Rs Rs

1) Interest Payable to Debenture Holder

Interest A/c Dr 100

To Debenture Holder A/c 100

2) Interest Paid to Debenture Holder after deducting TDS

Debenture Holder A/c Dr 100

To TDS Payable A/c 10

To Cash/ Bank A/c 90

3) TDS Paid

TDS Payable A/c Dr 10

To Cash/Bank A/c 10

4) Interest transferred to P & L A/c

Profit & Loss A/c Dr 100

To Interest A/c 100