105361 002 sendd web · 2016-09-28 · through the $5.6 billion special dividend we paid in...

TRANSCRIPT

ANNUAL REPORT AND FORM 10-K

WEYERHAEUSER

The actions we took in 2010 enhanced our ability to return value to our shareholders through our long-term strategy to generate superior returns with sustainable land and forest solutions.

The most signifi cant action involved electing Real Estate Investment

Trust status. You’ve already benefi ted from this decision through the $5.6 billion special dividend we paid in September.

In the future, you’ll benefi t from our enhanced ability to operate and grow our core asset — the more than 6 million acres of valuable timberland we hold. We believe forests provide a source of sustainable products, green energy and carbon sequestration as well as a host of other solutions for challenges facing the world. No one is better positioned than us to meet these needs through our holdings, our intellectual property and our people.

Our taxable REIT subsidiary, composed of Wood Products, Cellulose Fibers and Real Estate, generates cash fl ow to service our debt and help fund your dividend and our growth opportunities. Cellulose Fibers, which had a record year in 2010, broadens our exposure to global markets, while Wood Products and Real Estate offer substantial upside potential from their unique position to benefi t from a return to long-term housing-start trends.

Our commitment is to provide you with a dividend that is sustainable and that we can grow over time. In December, we announced a policy of paying a dividend ratio of 75 percent of funds available for distribution over the cycle. Given the continued challenges of the housing market, our announced quarterly dividend of 15 cents per share is likely to represent nearly all of our 2011 funds available for distribution.

For 2011, we project only a modest increase in single-family housing starts from 2010 levels. This will continue to put pressure on our Timberlands, Wood Products and Real Estate businesses.

Nonetheless, I expect improved performance from continued operational changes, cost effi ciencies and improved relative competitiveness of our businesses. I expect positive cash fl ow from our Wood Products segment, while I expect our Real Estate segment to continue to deliver strong performance relative to its peers. Although our Timberlands business will continue to defer a portion of our harvest, we foresee a slight increase in logging activity, taking advantage of improved demand in Asian markets. Finally, Cellulose Fibers should maintain its strong operating performance.

2011 will be another challenging year, but I’m confi dent we’ll continue on the path to stronger results.

Dan FultonPresident and Chief Executive Offi cer

DEAR SHAREHOLDER,

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER 1-4825

WEYERHAEUSER COMPANYA WASHINGTON CORPORATION

91-0470860(IRS EMPLOYER IDENTIFICATION NO.)

FEDERAL WAY, WASHINGTON 98063-9777 TELEPHONE (253) 924-2345

SECURITIES REGISTERED PURSUANT TO SECTION 12(B) OF THE ACT:

TITLE OF EACH CLASS NAME OF EACH EXCHANGE ON WHICH REGISTERED:

Common Shares ($1.25 par value) Chicago Stock ExchangeNew York Stock Exchange

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct. [X] Yes [ ] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theAct. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the SecuritiesExchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file suchreports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter)during the preceding 12 months (or for such shorter period that the registrant was required to submit and post suchfiles). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is notcontained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smallerreporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule12b-2 of the Exchange Act.

Large accelerated filer [X] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [X] No

As of June 30, 2010, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was$6,289,093,380 based on the closing sale price as reported on the New York Stock Exchange Composite Price Transactions.

As of February 4, 2011, 536,242,106 shares of the registrant’s common stock ($1.25 par value) were outstanding.

DOCUMENTS INCORPORATED BY REFERENCEPortions of the Notice of 2011 Annual Meeting of Shareholders and Proxy Statement for the company’s Annual Meeting ofShareholders to be held April 14, 2011, are incorporated by reference into Part II and III.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K

TABLE OF CONTENTSPART IITEM 1. OUR BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

WE CAN TELL YOU MORE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1WHO WE ARE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

• REAL ESTATE INVESTMENT TRUST (REIT) CONVERSION . . . . . . . 1

• OUR BUSINESS SEGMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

• CURRENT MARKET CONDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . 2

• COMPETITION IN OUR MARKETS . . . . . . . . . . . . . . . . . . . . . . . . . 2

• SALES OUTSIDE THE U.S. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

• OUR EMPLOYEES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

• COMPARABILITY OF DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2WHAT WE DO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

• TIMBERLANDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

• WOOD PRODUCTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

• CELLULOSE FIBERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

• REAL ESTATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

• CORPORATE AND OTHER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16NATURAL RESOURCE AND ENVIRONMENTAL MATTERS . . . . . . . . . . 17

• ENDANGERED SPECIES PROTECTIONS . . . . . . . . . . . . . . . . . . . . 17

• REGULATIONS AFFECTING FORESTRY PRACTICES . . . . . . . . . . . . 17

• FOREST CERTIFICATION STANDARDS . . . . . . . . . . . . . . . . . . . . . 18

• WHAT THESE REGULATIONS AND CERTIFICATION PROGRAMSMEAN TO US . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

• CANADIAN ABORIGINAL RIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . 18

• POLLUTION-CONTROL REGULATIONS . . . . . . . . . . . . . . . . . . . . . . 18

• ENVIRONMENTAL CLEANUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

• REGULATION OF AIR EMISSIONS IN THE U.S. . . . . . . . . . . . . . . . 19

• REGULATION OF AIR EMISSIONS IN CANADA . . . . . . . . . . . . . . . . 20

• POTENTIAL CHANGES IN POLLUTION REGULATION . . . . . . . . . . . 20FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . 21

ITEM 1A. RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22RISKS RELATED TO OUR INDUSTRIES AND BUSINESS . . . . . . . . . . 22

• MACROECONOMIC CONDITIONS . . . . . . . . . . . . . . . . . . . . . . . . . 22

• COMMODITY PRODUCTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

• INDUSTRY SUPPLY OF LOGS, WOOD PRODUCTS ANDPULP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

• HOMEBUILDING MARKET AND ECONOMIC RISKS . . . . . . . . . . . . 23

• CAPITAL MARKETS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

• CHANGES IN CREDIT RATINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

• SUBSTITUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

• CHANGES IN PRODUCT MIX OR PRICING . . . . . . . . . . . . . . . . . . . 24

• INTENSE COMPETITION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

• MATERIAL DISRUPTION OF MANUFACTURING . . . . . . . . . . . . . . . 24

• CAPITAL REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

• LAWS AND REGULATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

• CURRENCY EXCHANGE RATES . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

• AVAILABILITY OF RAW MATERIALS AND ENERGY . . . . . . . . . . . . . 25

• TRANSPORTATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

• REIT STATUS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

• LEGAL PROCEEDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

• EXPORT TAXES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

• NATURAL DISASTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28RISKS RELATED TO OWNERSHIP OF OUR COMMON STOCK . . . . . . 28

• STOCK-PRICE VOLATILITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28ITEM 1B. UNRESOLVED STAFF COMMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . 28ITEM 2. PROPERTIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29ITEM 3. LEGAL PROCEEDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

PART IIITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED

STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITYSECURITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

ITEM 6. SELECTED FINANCIAL DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL

CONDITION AND RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . 33WHAT YOU WILL FIND IN THIS MD&A . . . . . . . . . . . . . . . . . . . . . . . . 33REAL ESTATE INVESTMENT TRUST (REIT) CONVERSION . . . . . . . . . 33

ECONOMIC AND MARKET CONDITIONS AFFECTING OUROPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33FINANCIAL PERFORMANCE SUMMARY . . . . . . . . . . . . . . . . . . . . . . 35RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

• CONSOLIDATED RESULTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

• TIMBERLANDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

• WOOD PRODUCTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

• CELLULOSE FIBERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

• REAL ESTATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

• CORPORATE AND OTHER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

• CONTAINERBOARD, PACKAGING AND RECYCLING . . . . . . . . . . 45

• INTEREST EXPENSE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

• INCOME TAXES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45LIQUIDITY AND CAPITAL RESOURCES . . . . . . . . . . . . . . . . . . . . . . 46

• CASH FROM OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

• INVESTING IN OUR BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . 47

• FINANCING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47OFF-BALANCE SHEET ARRANGEMENTS . . . . . . . . . . . . . . . . . . . . . 49ENVIRONMENTAL MATTERS, LEGAL PROCEEDINGS AND OTHERCONTINGENCIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49ACCOUNTING MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

• CRITICAL ACCOUNTING POLICIES . . . . . . . . . . . . . . . . . . . . . . . 49

• PROSPECTIVE ACCOUNTING PRONOUNCEMENTS . . . . . . . . . . . 52ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT

MARKET RISK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53LONG-TERM DEBT OBLIGATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . 53

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA . . . . . . . 54REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTINGFIRM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54CONSOLIDATED STATEMENT OF OPERATIONS . . . . . . . . . . . . . . . . 55CONSOLIDATED BALANCE SHEET . . . . . . . . . . . . . . . . . . . . . . . . . . 56CONSOLIDATED STATEMENT OF CASH FLOWS . . . . . . . . . . . . . . . 58CONSOLIDATED STATEMENT OF CHANGES IN EQUITY ANDCOMPREHENSIVE INCOME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59INDEX FOR NOTES TO CONSOLIDATED FINANCIALSTATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60NOTES TO CONSOLIDATED FINANCIAL STATEMENTS . . . . . . . . . . . 61

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ONACCOUNTING AND FINANCIAL DISCLOSURE . . . . . . . . . . . . . . . . 102

ITEM 9A. CONTROLS AND PROCEDURES . . . . . . . . . . . . . . . . . . . . . . . . . . . 102EVALUATION OF DISCLOSURE CONTROLS AND PROCEDURES . . . 102CHANGES IN INTERNAL CONTROL . . . . . . . . . . . . . . . . . . . . . . . . . 102MANAGEMENT’S REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTINGFIRM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

ITEM 9B. OTHER INFORMATION — NOT APPLICABLE . . . . . . . . . . . . . . . . .

PART IIIITEM 10. DIRECTORS AND EXECUTIVE OFFICERS . . . . . . . . . . . . . . . . . . . 104ITEM 11. EXECUTIVE AND DIRECTOR COMPENSATION . . . . . . . . . . . . . . . 109ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT AND RELATED STOCKHOLDER MATTERS . . . . . . 109ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS . . . . . 109ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES . . . . . . . . . . . . . . 109

PART IVITEM 15. EXHIBITS AND FINANCIAL STATEMENT SCHEDULES . . . . . . . . . 110

EXHIBITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110SIGNATURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTINGFIRM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113FINANCIAL STATEMENT SCHEDULE . . . . . . . . . . . . . . . . . . . . . . . . 114

CERTIFICATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

COMPANY OFFICERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

OUR BUSINESSWe are a forest products company that grows and harveststrees, builds homes and makes a range of forest productsessential to everyday lives. Our goal is to do this safely,profitably and responsibly. We are committed to operate as asustainable company in the 21st Century. We focus onincreasing energy and resource efficiency, reducing greenhousegas emissions, reducing water consumption, conserving naturalresources, and offering products that meet human needs withsuperior sustainability attributes. We operate with world classsafety results, understand and address the needs of thecommunities in which we operate, and present ourselvestransparently.

We have offices or operations in 10 countries and havecustomers worldwide. We manage 20.5 million acres of forests,of which we own 5.8 million acres, lease 0.7 million acres andhave renewable, long-term licenses on 14 million acres. In2010, we generated $6.6 billion in net sales.

This portion of our Annual Report and Form 10-K providesdetailed information about who we are, what we do and wherewe are headed. Unless otherwise specified, current informationreported in this Form 10-K is as of the fiscal year endedDecember 31, 2010.

We break out financial information such as revenues, earningsand assets by the business segments that form our company.We also discuss the development of our company and thegeographic areas where we do business.

We report our financial condition in two groups:

•Forest Products — our forest products-based operations,principally the growing and harvesting of timber, themanufacture, distribution and sale of forest products andcorporate governance activities; and

•Real Estate — our real estate development and constructionoperations.

Throughout this Form 10-K, unless specified otherwise,references to “we,” “our,” “us” and “the company” refer to theconsolidated company, including both Forest Products and RealEstate.

WE CAN TELL YOU MORE

AVAILABLE INFORMATION

We meet the information-reporting requirements of theSecurities Exchange Act of 1934 by filing periodic reports, proxystatements and other information with the Securities and

Exchange Commission (SEC). These reports and statements —information about our company’s business, financial resultsand other matters — are available at:

•the SEC Internet site — www.sec.gov;

•the SEC’s Public Conference Room, 100 F St. N.E.,Washington, D.C., 20549, (800) SEC-0330; and

•our Internet site — www.weyerhaeuser.com.

When we file the information electronically with the SEC, it alsois added to our Internet site.

WHO WE ARE

We started out as Weyerhaeuser Timber Company, incorporatedin the state of Washington in January 1900, when FrederickWeyerhaeuser and 15 partners bought 900,000 acres oftimberland.

REAL ESTATE INVESTMENT TRUST (REIT) CONVERSION

Our board of directors has determined that conversion to a REITbest supports our strategic direction. For tax purposes, thischange was effective January 1, 2010. To implement ourdecision to be taxed as a REIT, we distributed to ourshareholders our accumulated earnings and profits, determinedunder federal income tax provisions as a “Special Dividend” onSeptember 1, 2010.

As a REIT, we expect to derive most of our REIT income frominvestments in timberlands, including the sale of standingtimber through pay-as-cut sales contracts. REIT income can bedistributed to shareholders without first paying corporate leveltax, substantially eliminating the double taxation on income. Asignificant portion of our timberland segment earnings willreceive this favorable tax treatment. We will, however, besubject to corporate taxes on built-in-gains (the excess of fairmarket value over tax basis at January 1, 2010) on sales ofreal property (other than standing timber) held by the REITduring the first 10 years following the REIT conversion. We alsowill continue to be required to pay federal corporate incometaxes on earnings of our Taxable REIT Subsidiary (TRS), whichprincipally includes our manufacturing businesses, our realestate development business and our non-qualified timberlandsegment income.

More information about our REIT conversion is in Note 2: RealEstate Investment Trust (REIT) Conversion in the Notes toConsolidated Financial Statements, as well as in theManagement’s Discussion and Analysis of Financial Conditionand Results of Operations.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 1

OUR BUSINESS SEGMENTSIn the Consolidated Results section of Management’sDiscussion and Analysis of Financial Condition and Results ofOperations, you will find our overall performance results for ourbusiness segments:

•Timberlands;

•Wood Products;

•Cellulose Fibers;

•Real Estate;

•Corporate and Other; and

•Containerboard, Packaging and Recycling (sold in 2008).

Detailed financial information about our business segmentsand our geographic locations is in Note 3: Business Segmentsand Note 22: Geographic Areas in the Notes to ConsolidatedFinancial Statements, as well as in this section and in theManagement’s Discussion and Analysis of Financial Conditionand Results of Operations.

CURRENT MARKET CONDITIONSThe U.S. economy has gradually begun its recovery from themost severe recession since the 1930’s. However, the U.S.housing market continues to lag other sectors in the recoveryand remains burdened by excess inventory and a diminishedpool of qualified home buyers. The health of the U.S. housingmarket strongly affects our Real Estate, Wood Products andTimberlands segments. Real Estate focuses on building singlefamily homes. Wood Products primarily sells into the newresidential building and repair and remodel markets. Demand forlogs from our Timberlands segment is affected by the productionof wood-based building products. Cellulose Fibers is primarilyaffected by global demand and the value of the U.S. dollar.

COMPETITION IN OUR MARKETSWe operate in highly competitive domestic and foreign markets,with numerous companies selling similar products. Many of ourproducts also face competition from substitutes for wood andwood-fiber products. In real estate development, ourcompetitors include numerous regional and national firms. Wecompete in our markets primarily through price, product qualityand service levels.

Our business segments’ competitive strategies are as follows:

•Timberlands — Extract maximum value for each acre we ownor manage.

•Wood Products — Deliver high-quality lumber, engineeredwood products and integrated solutions to the residentialconstruction and industrial markets.

•Cellulose Fibers — Concentrate on value-added pulpproducts.

•Real Estate — Deliver unique value propositions in targetmarkets.

SALES OUTSIDE THE U.S.

In 2010, $2.1 billion — 32 percent — of our total consolidatedsales and revenues were to customers outside the U.S. The tablebelow shows sales outside the U.S. for the last three years.

SALES OUTSIDE THE U.S. IN MILLIONS OF DOLLARS

2010 2009 2008

Exports from the U.S. $1,381 $1,154 $1,649

Canadian export and domestic sales 240 166 257

Other foreign sales 467 247 563

Total $2,088 $1,567 $2,469

Percent of total sales 32% 28% 22%

OUR EMPLOYEES

We have approximately 14,250 employees. This numberincludes:

•13,400 employed in North America and

•850 employed by our operations outside of North America.

Of these employees, approximately 3,500 are members ofunions covered by multi-year collective-bargaining agreements.

COMPARABILITY OF DATA

Over the last five years, we have made an acquisition tocomplement our key operations and have exited businessesthat did not fit our long-term strategic direction. As you reviewour results for the past five years, it may be helpful to keepin mind the following acquisition and divestitures and thesegments affected.

Summary of Recent Divestitures and Acquisition

YEAR TRANSACTION SEGMENTS AFFECTED

2010 Five short line railroads – sold Corporate and Other segment

2009 Trus Joist® Commercialdivision – sold

Wood Products segment

2008 Containerboard, Packaging andRecycling segment – sold

Containerboard, Packaging andRecycling segment

2008 Australian operations – sold Corporate and Other segment

2008 Uruguay operations – partitioncompleted

Timberlands and Corporate andOther segments

2007 Fine Paper and related assets –divested

Fine Paper, Timberlands andWood Products segments

2007 New Zealand operations – sold Corporate and Other segment

2007 Canadian wood productsdistribution centers – sold

Wood Products segment

2006 North American and Irishcomposite panel operations –sold

Wood Products and Corporateand Other segments

2006 Maracay Homes – acquired Real Estate segment

Additional information related to our discontinued operationscan be found in Note 4: Discontinued Operations in the Notes

2

to Consolidated Financial Statements. Information pertaining tosegment comparability can be found in Note 3: BusinessSegments in the Notes to Consolidated Financial Statements.

WHAT WE DO

This section provides information about how we:

•grow and harvest trees,

•manufacture and sell products made from them,

•build and sell homes and

•develop land.

For each of our business segments, we provide details aboutwhat we do, where we do it, how much we sell and where weare headed.

TIMBERLANDS

Our Timberlands business segment manages 6.5 million acresof private commercial forestland worldwide. We own 5.8 millionof those acres and lease the other 0.7 million acres. Inaddition, we have renewable, long-term licenses on 14.0 millionacres of forestland located in four Canadian provinces. Thetables presented in this section include data from thissegment’s business units as of the end of 2010.

WHAT WE DO

Forestry Management

Our Timberlands business segment:

•grows and harvests trees for use as lumber, other wood andbuilding products and pulp and paper;

•exports logs to other countries where they are made intoproducts;

•plants seedlings — and in parts of Canada we use naturalregeneration — to reforest the harvested areas using themost effective regeneration method for the site and species;

•monitors and cares for the new trees as they grow tomaturity; and

•seeks to sustain and maximize the timber supply from ourforestlands while keeping the health of our environment a keypriority.

Our goal is to maximize returns by selling logs and stumpage tointernal and external customers. We focus on solid wood anduse intensive silviculture to improve forest productivity andreturns while managing our forests on a sustainable basis tomeet customer and public expectations.

International operations in this segment consist principally offorest plantations, forest licenses and converting assets inSouth America. We serve as owners or managing partner inthese operations, which are either wholly-owned subsidiaries or

joint ventures. In China, we are the managing partner in a jointventure established in 2007. We own 51 percent of this jointventure and Fujian Yong’An Forestry Company owns theremaining 49 percent. As of December 31, 2010, the jointventure managed 44,000 acres of timberlands.

Sustainable Forestry Practices

We are committed to responsible environmental stewardshipwherever we operate, managing forests to produce financiallymature timber while protecting the ecosystem services theyprovide. Our working forests include places with uniqueenvironmental, cultural, historical or recreational value. Toprotect their unique qualities, we follow regulatoryrequirements, voluntary standards and implement theSustainable Forestry Initiative® (SFI) standard. Independentauditing of all of the forests we own or manage in the UnitedStates and Canada certifies that we meet the SFI standard. Ourforestlands in Uruguay are Forest Stewardship Council (FSC)certified or managed to the developing Uruguayan nationalforestry management standard designed to meet the Programfor the Endorsement of Forest Certification (PEFC).

Canadian Forestry Operations

In Canada, we have licenses to operate forestlands that provideraw material for our manufacturing units in various provinces.When we harvest trees, we pay the provinces at stumpage ratesset by the government and generally based on prevailing marketprices. We do not generate any profit in the Timberlands segmentfrom the harvest of timber from the licensed acres in Canada.

Other Values From Our Timberlands

In the United States, we actively manage mineral, oil and gasleases on our land and use geologic databases to identify andmarket opportunities for commercial mineral and geothermaldevelopment. We recognize leasing revenue over the terms ofagreements with customers. Revenue primarily comes from:

•royalty payments on oil and gas production;

•upfront bonus payments from oil and gas leasing andexploration activity;

•royalty payments on hard minerals (rock, sand and gravel);

•geothermal lease and option revenues; and

•the sale of mineral assets.

In managing mineral resources, we generate revenue related toour ownership of the minerals and, separately, related to ourownership of the surface. The ownership of mineral rights andsurface acres may be held by two separate parties. Materialsthat can be mined from the surface, and whose value comesfrom factors other than their chemical composition, typicallybelong to the surface owner. Examples of surface materialsinclude rock, sand, gravel, dirt and topsoil. The mineral ownerholds the title to commodities that derive value from their

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 3

unique chemical composition. Examples of mineral rightsinclude oil, gas, coal (even if mined at the surface) andprecious metals. If the two types of rights conflict, then mineralrights are generally superior to surface rights. A third type ofland right is geothermal, which can belong to either the surfaceor mineral owner. We routinely reserve mineral and geothermalrights when selling surface timberlands acreage.

Timberlands Products

PRODUCTS HOW THEY’RE USED

Logs Logs are made into lumber, other wood andbuilding products and pulp and paper products

Timberlands Timberland tracts are exchanged to improve ourtimberland portfolio or are sold to third parties byour land development subsidiary within thissegment

Timber Standing timber may be sold to third parties orconverted into chips and other raw materials tobe made into pulp and paper products

Minerals, oil and gas Sold into construction and energy markets

Other products Includes seed and seedlings, poles, as well asplywood and hardwood lumber produced by ourinternational operations, primarily in SouthAmerica

HOW WE MEASURE OUR PRODUCT

We report Timberlands data in cubic meters. Cubic metersmeasure the total volume of wood fiber in a tree or log that wecan sell. Cubic meter volume is determined from the large- andsmall-end diameters and length and provides a more consistentand comparative measure of timber and log volume amongoperating regions, species, size and seasons of the year thanother units of measure.

We also use two other units of measure when transactingbusiness including:

•thousand board feet (MBF) — used in the West to measurethe expected lumber recovery from a tree or log, but it doesnot include taper or recovery of nonlumber residual products;and

•green tons — used in the South to measure weight, butfactors used for conversion to product volume can vary byspecies, size, location and season.

Both measures are accurate in the regions where they areused, but they do not provide a meaningful basis forcomparisons between the regions.

The conversion rate for MBF to cubic meters varies based onseveral factors including diameter, length and taper of thetimber. The average conversion rate for MBF to cubic meters isapproximately 6.7 cubic meters per MBF.

The conversion rate from green tons to cubic meters also variesbased on the season harvested and the specific gravity of the

wood for the region where the timber is grown. An averageconversion rate for green tons to cubic meters is approximately0.825 cubic meters per green ton.

WHERE WE DO IT

Our timberlands assets are located primarily in North America.In the U.S. we own and manage sustainable forests in ninestates for use in wood products and pulp and papermanufacturing. We own or lease:

•4.1 million acres in the southern U.S. (Alabama, Arkansas,Louisiana, Mississippi, North Carolina, Oklahoma and Texas);and

•2.0 million acres in the Pacific Northwest (Oregon andWashington).

Our international operations are located primarily in Uruguayand China where, as of December 31, 2010, we own a totalof 317,000 acres and have long-term leases on another70,000 acres.

In addition, we have renewable, long-term licenses on14.0 million acres of forestland owned by the provincialgovernment of four Canadian provinces.

Our total timber inventory — including timber on owned andleased land in our U.S. and international operations — isapproximately 303 million cubic meters. The timber inventoryon licensed lands in Canada is approximately 371 million cubicmeters. The amount of timber inventory does not translate intoan amount of lumber or panel products because the quantity ofend products:

•varies according to the species, size and quality of thetimber; and

•will change through time as the mix of these variables adjust.

The species, size and grade of the trees affects the relativevalue of our timberlands.

DISCUSSION OF OPERATIONS BY GEOGRAPHY

Summary of 2010 Timber Inventory and Timberland Locations

United States

GEOGRAPHIC AREA

MILLIONSOF CUBICMETERS

THOUSANDS OF ACRES ATDECEMBER 31, 2010

TOTALINVENTORY

FEEOWNERSHIP

LONG-TERM

LEASESTOTALACRES

U.S.:

West 157 2,038 — 2,038

South 138 3,434 681 4,115

Total U.S. 295 5,472 681 6,153

4

Western United States

Our Western acres are well situated to serve the wood productmarkets in Oregon and Washington. Their location nearWeyerhaeuser mills and many third-party facilities allows formultiple sales opportunities. In addition, our location on theWest Coast provides access to higher-value export markets forDouglas fir and hemlock logs in Japan, Korea and China. Thesize and quality of our Western timberlands, coupled with theirproximity to several deep-water port facilities, positions us tomeet the needs of Pacific Rim log markets.

Our lands are composed primarily of Douglas fir, a specieshighly valued for its structural strength. Our coastal lands alsocontain western hemlock and have a higher proportion ofhemlock than our interior holdings. Our management systems,which provide us a competitive operating advantage, range fromresearch and forestry, to technical planning models,mechanized harvesting and marketing and logistics.

The average age of timber harvested in 2010 was 50 years.Most of our U.S. timberland is intensively managed for timberproduction, but some areas are conserved for environmental,historical, recreational or cultural reasons. Some of our oldertrees are protected in acreage set aside for conservation, andsome are not yet logged due to harvest rate regulations. Whileover the long term our average harvest age will decrease inaccordance with our sustainable forestry practices, we will onlyharvest approximately 1.5 percent of our Western acreage eachyear.

Southern United States

Our Southern acres predominantly contain southern yellow pineand encompass timberlands in seven states. This areaprovides a constant year round flow of logs to a variety ofinternal and third-party customers. We sell grade logs to millsthat manufacture a diverse range of products including lumber,plywood and veneer. We also sell chips and fiber logs tooriented strand board, pulp and paper mills. Our timberlandsare well located to take advantage of road, logging andtransportation systems for efficient delivery of logs to thesecustomers.

We intensively manage our timber plantations using forestryresearch and planning systems to optimize grade logproduction. We also actively manage our land to capturerevenues from our oil, gas and hard minerals resources. We dothis while providing quality habitat for a range of animals andbirds, which is in high demand for recreational purposes. Welease more than 95 percent of our acres to the public and statewildlife agencies for recreational purposes.

The average age of timber harvested in 2010 was 31 years forsouthern yellow pine. In accordance with our sustainableforestry practices, we harvest approximately 3.0 percent to3.5 percent of our acreage each year in the South.

International

GEOGRAPHIC AREA

MILLIONSOF CUBICMETERS

THOUSANDS OF ACRES ATDECEMBER 31, 2010

TOTALINVENTORY

FEEOWNERSHIP

LONG-TERM

LEASESTOTALACRES

Uruguay 7 317 26 343

China(1) 1 — 44 44

Total International 8 317 70 387

(1) Includes Weyerhaeuser percentage ownership of timberlands owned and managedthrough joint ventures

Our forestlands in Uruguay are approximately 51 percentloblolly pine and 49 percent eucalyptus. On average, the timberin Uruguay is in the first third of its rotation age. It is enteringinto that part of the growth rotation when we will see increasedvolume accretion. About 93 percent of the area to be plantedhas been afforested to date. The afforestation program isplanned to be completed within the next two years.

In Uruguay, the target rotation ages are 21 to 22 years for pineand 14 to 17 years for eucalyptus. We manage both species toa grade (appearance) regime.

We also operate a plywood mill in Uruguay with a productioncapacity of 140,000 cubic meters and a production volume of109,000 cubic meters reached in 2010. Construction to morethan double this capacity is under way and is expected to becompleted in April 2011.

In Brazil, Weyerhaeuser is a managing partner in a jointventure. We own 67 percent and Fibria Cellulose SA owns33 percent. A hardwood sawmill with 65,000 cubic meters ofcapacity produces high-value eucalyptus (Lyptus®) lumber andrelated appearance wood products. The mill’s production in2010 was 55,000 cubic meters.

Our investment in China is a joint venture with a publiccompany that is controlled by the state and local governments.Weyerhaeuser is the managing partner in a joint venture startedin 2007. Ownership is 51 percent Weyerhaeuser and49 percent Fujian Yong’An Forestry Company. The joint venturecurrently manages 44,000 acres of timberlands.

In China, the target rotation age is seven years, since we aremanaging the forests of loblolly pine and eucalyptus for fiber.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 5

Canada — Licensed Timberlands

GEOGRAPHIC AREA

MILLIONSOF CUBICMETERS

THOUSANDS OF ACRES ATDECEMBER 31, 2010

TOTALINVENTORY

LICENSEDSTANDING

VOLUME

TOTALLICENSE

ARRANGEMENTS

Canada:

Alberta 246 5,356

British Columbia 12 1,034

Ontario 33 2,598

Saskatchewan 80 4,968

Total Canada 371 13,956

We lease and license forestland in Canada from the provincialgovernment to secure the volume for our manufacturing units inthe various provinces. When the volume is harvested, we paythe province at stumpage rates set by the government andgenerally based on prevailing market prices. The harvested logsare transferred to our manufacturing facilities at cost(stumpage plus harvest, haul and overhead costs less anymargin on selling logs to third parties). Any conversion profit isrecognized at the respective mill in either the Cellulose Fibersor Wood Products segment.

Five-Year Summary of Timberlands Production

PRODUCTION IN THOUSANDS

2010 2009 2008 2007 2006

Fee depletion –cubic meters:

West 5,569 6,359 10,626 10,403 10,666

South 8,197 8,996 12,363 12,645 13,246

International(1) 349 503 — — —

Total 14,115 15,858 22,989 23,048 23,912

(1) International forestlands started commercial thinning in 2009 leading to productionvolumes.

Our Timberlands annual fee depletion represents the harvest ofthe timber assets we own. Depletion is a method of expensingthe cost of establishing the fee timber asset base over theharvest or timber sales volume. The decline in fee depletionfrom 2008 through 2010 reflects the company’s decision todefer harvest and preserve the long-term value of the assets.

HOW MUCH WE SELL

Our net sales to unaffiliated customers over the last two yearswere:

•$874 million in 2010 — up 22 percent from 2009; and

•$714 million in 2009.

Our intersegment sales over the last two years were:

•$603 million in 2010 — up 12 percent from 2009; and

•$537 million in 2009.

Five-Year Summary of Net Sales for Timberlands

NET SALES IN MILLIONS OF DOLLARS

2010 2009 2008 2007 2006

To unaffiliatedcustomers:

Logs:

West $ 414 $ 329 $ 547 $ 565 $ 667

South 145 144 97 56 57

Canada 17 13 20 38 58

Total 576 486 664 659 782

Pay as cuttimber sales

33 31 32 25 32

Timberlandssales andexchanges(1)

109 66 73 128 96

Higher andbetter useland sales(1)

22 11 11 33 35

Minerals, oiland gas

60 62 61 40 48

Products frominternationaloperations(2)

65 44 40 12 6

Other products 9 14 18 25 24

Subtotal sales tounaffiliatedcustomers

874 714 899 922 1,023

Intersegmentsales:

United States 409 392 817 983 1,093

Other 194 145 217 363 593

Subtotalintersegmentsales

603 537 1,034 1,346 1,686

Total $1,477 $1,251 $1,933 $2,268 $2,709

(1) Higher and better use timberland and non-strategic timberlands are conducted throughForest Products subsidiaries.

(2) Includes logs, plywood and hardwood lumber harvested or produced by our internationaloperations, primarily in South America.

Five-Year Trend for Total Net Sales in Timberlands

603

874

537

714

2006 2007 2008 20102009

$1,600

$1,800

$1,200

$1,400

$1,000

$2,000

$800

$400

$200

$600

$ -

1,023

1,686

922

1,346 1,034

899

All Other ProductsSouthern LogsWestern LogsIntersegmentSales

NET SALES IN MILLIONS OF DOLLARS

6

Percentage of 2010 Sales to Unaffiliated Customers

WESTERN LOGS

SOUTHERN LOGS

TIMBERLAND EXCHANGESMINERALS, OIL AND GAS

PRODUCTS FROM INTERNATIONAL OPERATIONS(1)

OTHER PRODUCTS

(1) Includes logs, plywood and hardwood lumber harvested or produced by our international operations, primarily in South America.

17%17%

47%47%

7%7%

10%10%

7%7%

12%12%

Log Sales Volumes

Logs sold to unaffiliated customers in 2010 decreasedapproximately 106 thousand cubic meters — 1 percent — from2009.

•Sales volumes in the West were flat year to year. Ourwestern sales to unaffiliated customers are generally higher-grade logs sold into the export market and domestic-gradelogs sold to West Coast sawmills.

•Sales to unaffiliated customers in the South decreased179 thousand cubic meters — 5 percent — primarily due todeferring more fee harvest in 2010 compared to 2009. Oursouthern sales volumes to unaffiliated customers aregenerally lower-grade fiber logs sold to pulp or containerboardmills. We use most of our high-grade logs in our ownconversion facilities.

•Sales volumes from Canada increased 98 thousand cubicmeters — 24 percent — in 2010. This increase in volumewas primarily due to increased market demand for logsmainly in Alberta.

•Sales volumes from our international operations decreased22 thousand cubic meters — 7 percent — in 2010. Thisreduction in volume was due to consuming more volumeinternally in 2010.

We sell three grades of logs — domestic grade, domestic fiberand export. Factors that may affect log sales in each of thesecategories include:

•domestic grade log sales — lumber usage, primarily forhousing starts and repair and remodel activity, the needs ofour own mills and the availability of logs from both outsidemarkets and our own timberlands;

•domestic fiber log sales — demand for chips by pulp andcontainerboard mills; and

•export log sales — level of housing starts in Japan, wheremost of our North American export logs are sold.

Our sales volumes include logs purchased in the open marketand all our domestic and export logs are sold to unaffiliatedcustomers or transferred at market prices to our internal millsby the sales and marketing staff within our Timberlandsbusiness units.

Five-Year Summary of Log Sales Volumes to UnaffiliatedCustomers for Timberlands

SALES VOLUMES IN THOUSANDS

2010 2009 2008 2007 2006

Logs – cubicmeters:

West 4,476 4,479 6,967 6,212 6,602

South 3,357 3,536 2,347 1,581 1,698

Canada 507 409 529 925 1,425

International 283 305 329 — 55

Total 8,623 8,729 10,172 8,718 9,780

Log Prices

The majority of our log sales to unaffiliated customers involvessales to the export market and to other domestic sawmills inthe Pacific Northwest. Following is a five-year summary ofselected export log prices.

Five-Year Summary of Selected Export Log Prices(#2 Sawlog Bark On — $/MBF)

2009200820072006 2010

COASTAL - DOUGLAS FIR - LONGVIEW

COASTAL - HEMLOCK

833

767731

686 687

442 433389

314

408

SELECTED PRODUCT PRICES

Our log prices are affected by the supply of and demand forgrade and fiber logs and are influenced by the same factorsthat affect log sales. Export log prices are particularly affectedby the Japanese housing market.

Average 2010 log realizations in the West and South increasedfrom 2009 — primarily due to higher domestic log pricescaused by the relative recovery in lumber prices during the year

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 7

as compared to 2009. Western export realizations alsoincreased due to the demand of logs in the China market.Export prices driven by the China demand also influenced thehigher Western domestic prices.

Minerals and Energy Products

Mineral revenue decreased in 2010 as recognition of leasingrevenue was completed on some older leases and sales ofproducing oil and gas properties was limited. The decline waspartially offset by increased oil and gas royalties as productionfrom Haynesville Shale gas wells came on line. Overall royaltiesfrom construction aggregates increased slightly. Revenues fromwind power and geothermal agreements remained the samefrom year-to-year, but the company entered into five new windpower agreements.

WHERE WE’RE HEADED

Our competitive strategies include:

•managing forests on a sustainable basis to meet customerand public expectations;

•reducing the time it takes to realize returns by practicingintensive forest management and focusing on the mostadvantageous markets;

•efficiently delivering raw materials to internal supply chains;

•building long-term relationships with external customers whorely on a consistent supply of high-quality raw material;

•continuously reviewing our portfolio of land holdings to createthe greatest value for the company;

•investing in technology and advances in silviculture toimprove yields and timber quality;

•positioning ourselves as one of the largest, lowest-costgrowers of global softwood and hardwood timber;

•leveraging our mineral ownership position; and

•positioning ourselves to take advantage of new marketopportunities that may be created by energy and climatechange legislation and regulation.

In addition, we believe we will generate additional revenuesfrom new products and services, such as wetland mitigationbanking and conservation easements, and from participating inemerging carbon and energy markets.

WOOD PRODUCTS

We are a large manufacturer and distributor of wood products inNorth America and Asia.

WHAT WE DO

Our wood products segment:

•provides a family of high-quality softwood lumber, engineeredlumber, structural panels and other specialty products to theresidential structural frame market;

•delivers innovative homebuilding solutions to help ourcustomers quickly and efficiently meet their customers’needs;

•sells our products and services primarily through our ownsales organizations and distribution facilities andsupplements our product offerings with building materialsthat we purchase from other manufacturers;

•sells certain products into the repair and remodel marketthrough the wood preserving and home-improvementwarehouse channels;

•exports our softwood lumber, engineered building materialsand industrial hardwood products to Europe and Asia; and

•makes and sells hardwood lumber to manufacturers offurniture and cabinetry in more than 35 countries.

Wood Products

PRODUCTS HOW THEY’RE USED

Structural lumber Structural framing for new residential, repair andremodel, treated applications, industrial, andcommercial structures

Engineered lumber

•Solid section

•I-joists

Floor and roof joists, and headers and beams forresidential and commercial structures

Structural panels

•Oriented strand board(OSB)

•Softwood plywood

Structural sheathing, subflooring and stair treadfor residential and commercial structures

Hardwood lumber Furniture, pallets, ties, moldings, panels,cabinets, architectural millwork, components andretail boards

Other products Complementary building products such as cedar,decking, siding, insulation, rebar and engineeredlumber connectors

8

WHERE WE DO IT

We operate manufacturing facilities in the United States andCanada. We distribute through a combination of Weyerhaeuserand third-party locations. Information about the locations,capacities and actual production of our manufacturing facilitiesis included below.

Principal Manufacturing Locations

Locations of our principal manufacturing facilities as ofDecember 31, 2010, by major product group were:

•Structural lumber– U.S. — Alabama, Arkansas, Louisiana, Mississippi,

North Carolina, Oklahoma, Oregon and Washington– Canada — Alberta and British Columbia

•Engineered lumber– U.S. — Alabama, Georgia, Louisiana, Oregon and

West Virginia– Canada — British Columbia and Ontario

•Oriented strand board– U.S. — Louisiana, Michigan, North Carolina and

West Virginia– Canada — Alberta and Saskatchewan

•Softwood plywood and veneer– U.S. — Alabama, Arkansas, Louisiana and Oregon

•Hardwood lumber– U.S. — Michigan, Oregon, Washington and Wisconsin

Summary of 2010 Wood Products Capacities

CAPACITIES IN MILLIONS

PRODUCTIONCAPACITY

NUMBER OFFACILITIES

Structural lumber – board feet 4,530 19

Engineered solid section – cubic feet 37 8

Engineered I-joists – lineal feet 380 3

Oriented strand board – square feet (3/8”) 3,015 6

Softwood Plywood – square feet (3/8”) 460 2

Veneer – square feet (3/8”)(1) 1,145 5

Hardwood lumber – board feet 334 7

Capacities include four engineered solid section facilities, one engineered I-joist facility andtwo veneer mills that are indefinitely closed.(1) Veneer is primarily used internally to produce plywood and engineered lumber products.

In response to market conditions, we sold or closed a numberof facilities and curtailed production at several other mills. Thesales and closures include:

•Sales:– 2010 — one lumber mill; and– 2009 — TJ® Commercial business, Albany Trucking and

one veneer mill.

•Permanent closures:– 2010 — one lumber mill, one engineered lumber mill, one

oriented strand board mill; and– 2009 — four lumber mills, two engineered lumber mills

and six distribution centers.

•Indefinite closures:– 2010 — one engineered lumber mill; and– 2009 — one lumber mill, three engineered lumber mills

and two veneer mills.

In addition to these sales and closures, we discontinued ourcontractual relationship with two southern lumber mills in2010. We no longer produce lumber at Bogalusa, Louisianaand Silver Creek, Mississippi.

Five-Year Summary of Wood Products Production

PRODUCTION IN MILLIONS

2010 2009 2008 2007 2006

Structural lumber –board feet(1)

3,289 3,098 4,451 5,490 6,355

Engineered solidsection – cubic feet(2)

15 11 22 28 41

Engineered I-joists –lineal feet(2)

133 109 218 339 473

Oriented strand board –square feet (3/8”)

1,721 1,448 2,468 3,428 4,166

Softwood plywood –square feet (3/8”)(3)

212 150 333 423 900

Hardwood lumber –board feet

231 201 253 294 324

Composite panels –square feet (3/4”)(1)

— — — — 666

(1) Reflects the divestitures of our North American composite panel operations in July 2006and the Domtar Transaction in March 2007.

(2) Weyerhaeuser engineered I-joist facilities also may produce engineered solid section.(3) All Weyerhaeuser plywood facilities also produce veneer.

HOW MUCH WE SELL

Revenues of our Wood Products business segment come fromsales to wood products dealers, do-it-yourself retailers, buildersand industrial users. We provide products and services to theresidential construction market under the iLevel® brand. In2010, Wood Products net sales were $2.6 billion, an increaseof 16 percent, compared with $2.2 billion in 2009.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 9

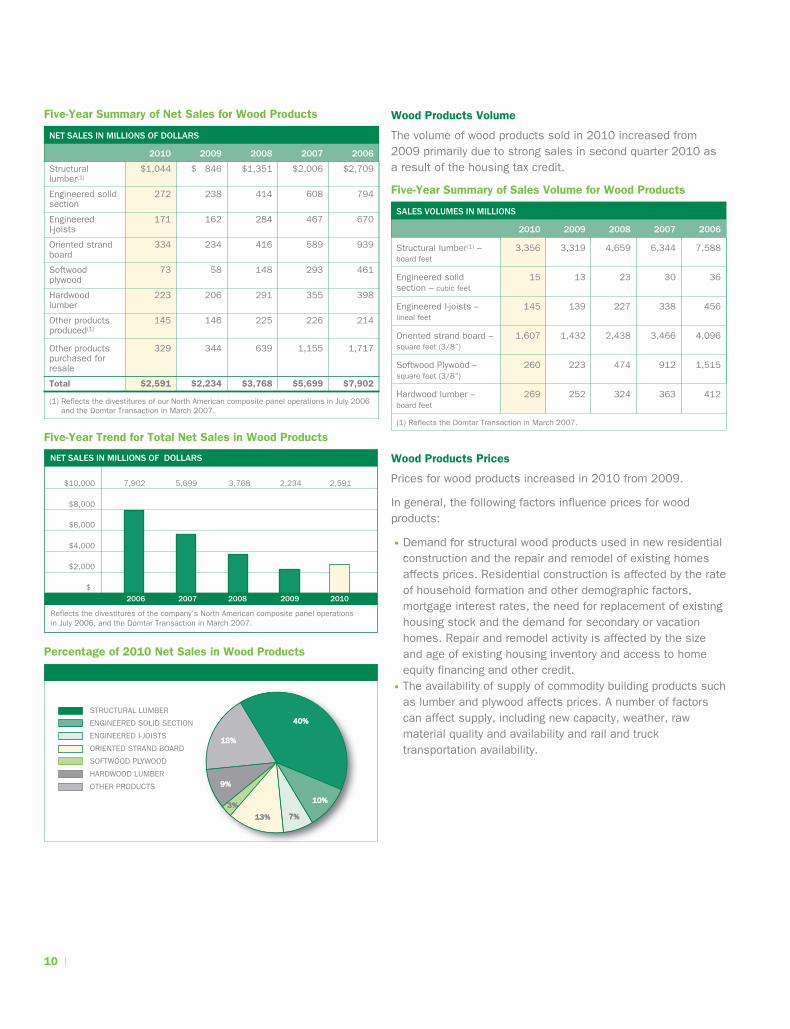

Five-Year Summary of Net Sales for Wood Products

NET SALES IN MILLIONS OF DOLLARS

2010 2009 2008 2007 2006

Structurallumber(1)

$1,044 $ 846 $1,351 $2,006 $2,709

Engineered solidsection

272 238 414 608 794

EngineeredI-joists

171 162 284 467 670

Oriented strandboard

334 234 416 589 939

Softwoodplywood

73 58 148 293 461

Hardwoodlumber

223 206 291 355 398

Other productsproduced(1)

145 146 225 226 214

Other productspurchased forresale

329 344 639 1,155 1,717

Total $2,591 $2,234 $3,768 $5,699 $7,902

(1) Reflects the divestitures of our North American composite panel operations in July 2006and the Domtar Transaction in March 2007.

Five-Year Trend for Total Net Sales in Wood Products

NET SALES IN MILLIONS OF DOLLARS

$10,000

$8,000

$6,000

$4,000

$2,000

$ -

2,234

2009

2,591

2010200820072006

Reflects the divestitures of the company’s North American composite panel operationsin July 2006, and the Domtar Transaction in March 2007.

7,902 5,699 3,768

Percentage of 2010 Net Sales in Wood Products

STRUCTURAL LUMBER

SOFTWOOD PLYWOOD

ORIENTED STRAND BOARD

HARDWOOD LUMBER

ENGINEERED I-JOISTS

ENGINEERED SOLID SECTION

OTHER PRODUCTS

40%40%

10%10%

7%7%13%13%

3%3%

9%9%

18%18%

Wood Products Volume

The volume of wood products sold in 2010 increased from2009 primarily due to strong sales in second quarter 2010 asa result of the housing tax credit.

Five-Year Summary of Sales Volume for Wood Products

SALES VOLUMES IN MILLIONS

2010 2009 2008 2007 2006

Structural lumber(1) –board feet

3,356 3,319 4,659 6,344 7,588

Engineered solidsection – cubic feet

15 13 23 30 36

Engineered I-joists –lineal feet

145 139 227 338 456

Oriented strand board –square feet (3/8”)

1,607 1,432 2,438 3,466 4,096

Softwood Plywood –square feet (3/8”)

260 223 474 912 1,515

Hardwood lumber –board feet

269 252 324 363 412

(1) Reflects the Domtar Transaction in March 2007.

Wood Products Prices

Prices for wood products increased in 2010 from 2009.

In general, the following factors influence prices for woodproducts:

•Demand for structural wood products used in new residentialconstruction and the repair and remodel of existing homesaffects prices. Residential construction is affected by the rateof household formation and other demographic factors,mortgage interest rates, the need for replacement of existinghousing stock and the demand for secondary or vacationhomes. Repair and remodel activity is affected by the sizeand age of existing housing inventory and access to homeequity financing and other credit.

•The availability of supply of commodity building products suchas lumber and plywood affects prices. A number of factorscan affect supply, including new capacity, weather, rawmaterial quality and availability and rail and trucktransportation availability.

10

Demand for home construction fell dramatically from 2006through 2009, with a corresponding drop in demand for theproducts that we produce and sell. This put significant andprolonged downward pressure on product prices. The followinggraphs reflect product price trends for the past five year period.

Five-Year Summary of Selected Published Lumber Prices —$/MBF

2006 2007 2008 2009 2010

SELECTED PUBLISHED PRODUCT PRICES

2x4 DOUGLAS FIR (GREEN)

2x4 SOUTHERN YELLOW PINE (KILN DRIED)

2x4 SPRUCE-PINE-FIR (KILN DRIED)

2x4 DOUGLAS FIR (KILN DRIED)

207

280

153

219

242

301

164

229

351

282284

231

329

279265

220

246

189

297

190

Five-Year Summary of Selected Published Oriented StrandBoard Prices — $/MSF

2010200920082007

OSB (7/16”-24/16”)NORTH CENTRAL PRICE

SELECTED PUBLISHED PRODUCT PRICES

2006

218

162 171 164

220

WHERE WE’RE HEADED

Our competitive strategies include:

•responding to difficult market conditions by actively managingour network of production facilities to balance supply withmarket demand;

•taking advantage of our size, scale, expertise and breadth ofproducts that make us unique in serving the residentialstructural-frame marketplace;

•developing and delivering innovative homebuilding solutions,such as residential structural frame construction, to meetcustomers’ needs;

•continuing to meet the needs of home-improvement repairand remodel customers;

•achieving operating excellence through the delivery chain;

•differentiating our products and services from othermanufacturers to create demand for them in themarketplace, which could generate higher prices;

•meeting international demands for hardwood products byaligning and improving our global supply; and

•conducting our activities in an environmentally sustainablemanner and developing and marketing the environmentalattributes of our products and solutions.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 11

CELLULOSE FIBERS

Our cellulose fibers segment is one of the world’s largestproducers of absorbent fluff used in products such as diapers.We also manufacture liquid packaging board and other pulpproducts. We have a 50 percent interest in North Pacific PaperCorporation (NORPAC) — a joint venture with Nippon PaperIndustries that produces newsprint and high-brightnesspublication papers.

WHAT WE DO

Our cellulose fibers segment:

•provides cellulose fibers for absorbent products in marketsaround the world;

•works closely with our customers to develop unique orspecialized applications;

•manufactures liquid packaging board used primarily for theproduction of containers for liquid products; and

•generates energy, of which 84 percent is from black liquorproduced at the mills and biomass.

Cellulose Fibers Products

PRODUCTS HOW THEY’RE USED

Pulp

•Fluff pulp (Southernsoftwood kraft fiber)

•Papergrade pulp(Southern and Northernsoftwood kraft fiber)

•Specialty chemicalcellulose pulp

•Used in sanitary disposable products thatrequire bulk, softness and absorbency

•Used in products that include printing andwriting papers and tissue

•Used in textiles, absorbent products, specialtypackaging, specialty applications andproprietary high-bulking fibers

Liquid packaging board Converted into containers to hold liquid materialssuch as milk, juice and tea

Other products

•Slush pulp

•Wet lap pulp

Used in the manufacture of paper products

WHERE WE DO IT

Our cellulose fibers (pulp) products are distributed through aglobal direct sales network, and our liquid packaging productsare sold directly to carton and food product packagingconverters in North America and Asia. Locations of our principalmanufacturing facilities by major product group are:

•Pulp– U.S. — Georgia (2), Mississippi and North Carolina– Canada — Alberta

•Liquid packaging board– U.S. — Washington

Summary of 2010 Cellulose Fibers Capacities

CAPACITIES IN THOUSANDS

PRODUCTIONCAPACITY

NUMBER OFFACILITIES

Pulp – air-dry metric tons 1,835 5

Liquid packaging board – tons 300 1

Five-Year Summary of Cellulose Fibers Production

PRODUCTION IN THOUSANDS

2010 2009 2008 2007 2006

Pulp – air-dry metric tons(1) 1,774 1,629 1,760 1,851 2,588

Liquid packagingboard – tons

316 282 297 283 282

(1) Reflects the Domtar Transaction in March 2007.

HOW MUCH WE SELL

Revenues of our Cellulose Fibers segment come from sales tocustomers who use the products for further manufacturing ordistribution and for direct use. Our net sales increased to$1.9 billion in 2010, or 26 percent, compared with $1.5 billionin 2009.

Five-Year Summary of Net Sales for Cellulose Fibers

NET SALES IN MILLIONS OF DOLLARS

2010 2009 2008 2007 2006

Pulp(1) $1,489 $1,148 $1,357 $1,478 $1,657

Liquid packagingboard

337 290 290 247 229

Other products 85 73 118 107 70

Total $1,911 $1,511 $1,765 $1,832 $1,956

(1) Reflects the Domtar Transaction in March 2007.

Five-Year Trend for Total Net Sales in Cellulose Fibers

NET SALES IN MILLIONS OF DOLLARS

2009200820072006

$2,000

$1,500

$1,000

$500

$ -2010

1,9111,511

Reflects Domtar Transaction in March 2007.

1,8321,956 1,765

12

Percentage of 2010 Net Sales in Cellulose Fibers

PULP

LIQUID PACKAGING BOARD

OTHER PRODUCTS

78%78%

18%18%

4%4%

Pulp Volumes

Our sales volumes of cellulose fiber products were 1.7 milliontons in 2010, 2009 and 2008.

Factors that affect sales volumes for cellulose fiber productsinclude:

•growth of the world gross domestic product and

•demand for paper production and diapers.

Five-Year Summary of Sales Volume for Cellulose Fibers

SALES VOLUMES IN THOUSANDS

2010 2009 2008 2007 2006

Pulp – air-dry metric tons(1) 1,714 1,697 1,704 2,070 2,621

Liquid packagingboard – tons

311 288 302 286 275

(1) Reflects the Domtar Transaction in March 2007.

Pulp Prices

Our average pulp prices in 2010 increased compared with2009 due to the:

•relative strength of the U.S. dollar,

•level of demand and

•world economic environment.

Five-Year Summary of Selected Published Pulp Prices —$/TON

2006 2007 2008 2009 2010

NORTHERN BLEACHED KRAFT PULP-AIR DRY METRIC-U.S.

SELECTED PUBLISHED PRODUCT PRICES

721

823857

718

960

WHERE WE’RE HEADED

Our competitive strategies include:

•improving our cost-competitiveness through operationalexcellence and noncapital solutions;

•focusing capital investments on new and improved productcapabilities, cost-reduction, and green energy opportunities;

•collaborating with third parties to develop new value-addedproducts; and

•focusing research and development resources on new waysto expand and improve the range of applications for cellulosefibers and new product opportunities.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 13

REAL ESTATE

Our Real Estate business segment includes our wholly-ownedsubsidiary Weyerhaeuser Real Estate Company (WRECO) andits subsidiaries.

WHAT WE DO

The Real Estate segment focuses on:

•constructing single-family housing and

•developing residential lots for our use and for sale.

Real Estate Products and Activities

PRODUCTS HOW THEY’RE USED

Single-family housing Residential living

Land Residential lots and land forconstruction and sale, master-planned communities with mixed-useproperty

WHERE WE DO IT

Our operations are concentrated in metropolitan areas inArizona, California, Maryland, Nevada, Texas, Virginia andWashington.

HOW MUCH WE SELL

We are one of the top 20 homebuilding companies in theUnited States as measured by annual single-family homeclosings.

Our revenues increased to $923 million in 2010, up 2 percent,compared with $904 million in 2009. This modest increaseoccurred despite slightly fewer home closings and challengingmarket conditions marked by low consumer confidence, highunemployment and continued downward pressure on pricingdue to foreclosures.

The following factors affect revenues in our Real Estatebusiness segment:

•The market prices of the homes that we build varies.

•The product and geographic mix of sales varies based on thefollowing:– the markets where we build, which vary by geography;– we build homes that range in price points to meet our

target customers’ needs, from first-time to semi-customhomes based on geography; and

– the mix of price points, which differ for traditional, single-family detached homes and attached products such astownhomes and condominiums.

•Land and lot sales are a component of our activities. Thesesales do not occur evenly from year to year and may rangefrom approximately 5 percent to 15 percent of total RealEstate revenues annually.

•From time to time, we sell apartment buildings and otherincome producing properties.

Five-Year Summary of Net Sales for Real Estate

REVENUE IN MILLIONS OF DOLLARS

2010 2009 2008 2007 2006

Single-family housing $842 $832 $1,294 $2,079 $2,951

Land 64 68 99 213 310

Other 17 4 15 67 74

Total $923 $904 $1,408 $2,359 $3,335

Five-Year Trend for Total Net Sales in Real Estate

NET SALES IN MILLIONS OF DOLLARS

2009200820072006

$4,000

$3,000

$2,000

$1,000

$ -

904

2010

9233,335 2,359 1,408

Percentage Breakdown of 2010 Net Sales in Real Estate

SINGLE-FAMILY HOMES

91%91%

9%9%

LAND DEVELOPMENTAND OTHER

14

Five-Year Summary of Single-Family Unit Statistics

SINGLE-FAMILY UNIT STATISTICS

2010 2009 2008 2007 2006

Homes sold 1,914 2,269 2,522 4,152 4,541

Homes closed 2,125 2,177 3,188 4,427 5,836

Homes sold butnot closed(backlog)

439 650 558 1,224 1,499

Cancellation rate 20% 23% 32% 26% 29%

Buyer traffic 68,430 65,781 112,817 181,896 231,993

Average price ofhomes closed

$396,000 $382,000 $406,000 $470,000 $506,000

Single-familygross margin –excludingimpairments (%)(1)

23.7% 17.5% 15.1% 21.5% 28.0%

(1) Single-family gross margin equals revenue less cost of sales and period costs (otherthan impairments, deposit write-offs and project abandonments).

WHERE WE’RE HEADED

Our competitive strategies include:

•offering customer-driven, distinct value propositions tospecific market niches in each of our targeted geographies;

•delivering quality homes to satisfied customers — a principlewe measure through “willingness to refer” rates fromindependent surveys of homebuyers;

•replicating best practices developed in each geographicarea; and

•optimizing value from our land portfolio.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 15

CORPORATE AND OTHERWHAT WE DO

Our Corporate and Other segment includes certain gains orcharges that are not related to an individual operating segmentand transportation operations.

WHERE WE DO IT

Our transportation operations include our marine operations,which provide shipping between North America and Asia, and,until we sold them in December 2010, our railroad operations.

As part of our strategic restructuring of our internationalholdings, we:

•sold our Irish composite panels operation —November 2006;

•restructured our investment in our Uruguay joint ventures inpreparation for a partitioning of the assets with the jointventure owners — June 2007;

•sold our investment in our New Zealand joint venture,Nelson Forests — October 2007;

•completed the partitioning of assets related to our Uruguayjoint ventures — April 2008; and

•sold our investment in our Australian operations —July 2008.

HOW MUCH WE SELL

Sales and revenues for our Corporate and Other segment areprimarily related to our marine transportation and discontinuedinternational operations. In 2010, our net sales were$253 million compared with $165 million in 2009. Theincrease in revenues is primarily due to increased revenue inour transportation business during 2010.

Factors that affect revenues in our transportation operationsinclude:

•international trade levels between North America and itstrading partners in Asia,

•the profile of our competition within our shipping lanes and

•overall demand for forest products.

Five-Year Summary of Net Sales for Corporate and Other

NET SALES IN MILLIONS OF DOLLARS

2010 2009 2008 2007 2006

Transportation $253 $165 $259 $223 $198

International woodproducts(1)

— — 133 209 277

Other — — — — 2

Total $253 $165 $392 $432 $477

(1) Reflects the divestitures of our Irish composite panels operation in November 2006 andour Australian Operations in July 2008.

Five-Year Trend for Total Net Sales in Corporate and Other

165

$500

$600

$400

$300

$200

$100

$ -

Reflects the divestitures of our Irish composite panels operations in November 2006 andour Australian operations in July 2008.

NET SALES IN MILLIONS OF DOLLARS

2009

253

2010200820072006

477 432 392

Catchlight Energy

Catchlight Energy is Weyerhaeuser’s joint venture with Chevron,which is focused on the commercialization of liquidtransportation fuels produced from conversion of forest-basedmaterial. During 2010, Catchlight was engaged in research anddevelopment work in the areas of sustainability, feedstocksourcing and scalability, and conversion technologies.Catchlight Energy also spent time developing relationships withselected technology partners. Results of Catchlight Energy arereported in the Corporate and Other segment.

16

NATURAL RESOURCE AND ENVIRONMENTALMATTERS

Many social values are expressed in the laws and regulationsthat pertain to growing and harvesting timber. We participate involuntary certification of our timberlands to assure that wesustain their values including the protection of wildlife andwater quality. We are also subject to laws regulating forestrypractices. Changes in law and regulation can significantly affectlocal or regional timber harvest levels and market values oftimber-based raw materials.

ENDANGERED SPECIES PROTECTIONS

In the United States, a number of fish and wildlife species thatinhabit geographic areas near or within our timberlands havebeen listed as threatened or endangered under the federalEndangered Species Act (ESA) or similar state laws, including:

•the northern spotted owl, the marbled murrelet, a number ofsalmon species, bull trout and steelhead trout in the PacificNorthwest;

•several freshwater mussel and sturgeon species; and

•the red-cockaded woodpecker, gopher tortoise and Americanburying beetle in the South or Southeast.

Additional species or populations may be listed as threatenedor endangered as a result of pending or future citizen petitionsor petitions initiated by federal or state agencies.

Restrictions on our timber harvests result, or could result from:

•federal and state requirements to protect habitat forthreatened and endangered species;

•additional listings of fish and wildlife species as endangered,threatened or sensitive under the ESA or similar state laws;or

•regulatory actions taken in the future by federal or stateagencies to protect habitat for these species.

Such actions also could increase our operating costs and affecttimber supply and prices in general.

In Canada, the federal Species at Risk Act (SARA) requiresprotective measures for species identified as being at risk andfor critical habitat. Environment Canada announced a series ofwestern science studies in 2010 that, with other landscapeinformation, are designed to identify critical habitat. Theidentification and protection of habitat may, over time, result inadditional restrictions on timber harvests and other forestmanagement practices that could increase operating costs foroperators of forestlands in Canada. To date these Canadianmeasures have not had, and in 2011 will not have, a significanteffect on our harvesting operations. We anticipate that future

measures will not disproportionally affect Weyerhaeuser ascompared with comparable operations.

REGULATIONS AFFECTING FORESTRY PRACTICES

In the United States, regulations established by federal, stateand local governments or agencies to protect water quality andwetlands could affect future harvests and forest managementpractices on some of our timberlands. Forest practice acts insome states in the United States that increasingly affectpresent or future harvest and forest management activitiesinclude:

•limits on the size of clearcuts,

•requirements that some timber be left unharvested to protectwater quality and fish and wildlife habitat,

•regulations regarding construction and maintenance of forestroads,

•rules requiring reforestation following timber harvest,

•procedures for state agencies to review and approveproposed forest practice activities and

•various permit programs.

Each state in which we own timberlands has developed bestmanagement practices to reduce the effects of forest practiceson water quality and aquatic habitats. Additional and morestringent regulations may be adopted by various state and localgovernments to achieve water-quality standards under thefederal Clean Water Act, protect fish and wildlife habitats, orachieve other public policy objectives.

In Canada, our forest operations are carried out on publicforestlands under forest licenses. All forest operations aresubject to:

•forest practices and environmental regulations and

•license requirements established by contract between us andthe relevant province designed to:– protect environmental values and– encourage other stewardship values.

On May 18, 2010, 21 member companies of the ForestProducts Association of Canada (FPAC), includingWeyerhaeuser’s Canadian subsidiary, announced the signing ofa Canadian Boreal Forest Agreement (CBFA) with nineenvironmental organizations. The CBFA applies to approximately72 million hectares of public forests licensed to FPAC membersand, when fully implemented, is expected to lead to theconservation of significant areas of Canada’s boreal forest andprotection of woodland caribou. CBFA signators are meetingwith provincial governments, and aboriginal and localcommunities to seek their participation in advancing the goalsof the CBFA. Progress under the CBFA will be measured by anindependent auditor.

WEYERHAEUSER COMPANY > 2010 ANNUAL REPORT AND FORM 10-K 17

FOREST CERTIFICATION STANDARDS

We operate in North America under the Sustainable ForestryInitiative®. This is a certification standard designed tosupplement government regulatory programs with voluntarylandowner initiatives to further protect certain public resourcesand values. The Sustainable Forestry Initiative® is anindependent standard, overseen by a governing boardconsisting of:

•conservation organizations,

•academia,

•the forest industry and

•large and small forest landowners.

Compliance with the Sustainable Forestry Initiative® may resultin some increases in our operating costs and curtailment of ourtimber harvests in some areas.

WHAT THESE REGULATIONS AND CERTIFICATIONPROGRAMS MEAN TO US

The regulatory and nonregulatory forest management programsdescribed above have:

•increased our operating costs;

•resulted in changes in the value of timber and logs from ourtimberlands;

•contributed to increases in the prices paid for wood productsand wood chips during periods of high demand;

•sometimes made it more difficult for us to respond to rapidchanges in markets, extreme weather or other unexpectedcircumstances; and

•potentially encouraged further reductions in the usage of, orsubstitution of other products for, lumber and plywood.

We believe that these kinds of programs have not had, and in2011 will not have, a significant effect on the total harvest oftimber in the United States or Canada. However, these kindsof programs may have such an effect in the future. We expectwe will not be disproportionately affected by these programsas compared with typical owners of comparable timberlands.We also expect that these programs will not significantlydisrupt our planned operations over large areas or forextended periods.

CANADIAN ABORIGINAL RIGHTS

Many of the Canadian forestlands are subject to theconstitutionally protected treaty or common-law rights ofaboriginal peoples of Canada. Most of British Columbia (B.C.)is not covered by treaties, and as a result the claims of B.C.’saboriginal peoples relating to forest resources are largelyunresolved, although many aboriginal groups are engaged intreaty discussions with the governments of B.C. and Canada.