11 alternative transportation technologies: hydrogen, biofuels, advanced ices, hevs and phevs...

TRANSCRIPT

11

Alternative Transportation Technologies: Hydrogen, Biofuels, Advanced ICEs, HEVs and PHEVs

Results of two Reports from theNational Research Council

National Petroleum Council 10-7-10

Michael Ramage

2

Committee on Assessment of Resource Needs for Fuel Cell and Hydrogen

Technologies

• MICHAEL P. RAMAGE, NAE1, ExxonMobil Research and Engineering Company (retired), Chair

• RAKESH AGRAWAL, NAE, Purdue University• DAVID L. BODDE, Clemson University• DAVID FRIEDMAN, Union of Concerned Scientists• SUSAN FUHS, Conundrum Consulting• JUDI GREENWALD, Pew Center on Global Climate Change• ROBERT L. HIRSCH, Management Information Services, Inc.• JAMES R. KATZER, NAE, Massachusetts Institute of Technology• GENE NEMANICH, ChevronTexaco Technology Ventures (retired)• JOAN OGDEN, University of California, Davis• LAWRENCE T. PAPAY, NAE, Science Applications International Corporation (retired)• IAN W.H. PARRY, Resources for the Future• WILLIAM F. POWERS, NAE, Ford Motor Company (retired)• EDWARD S. RUBIN, Carnegie Mellon University• ROBERT W. SHAW, JR., Aretê Corporation• ARNOLD F. STANCELL, NAE, Georgia Institute of Technology• TONY WU, Southern Company

1NAE, National Academy of Engineering.

3

Major Options for Reducing Oil Use

• Improved fuel economy; evolutionary.• Biofuels; some new infrastructure required.• Hydrogen fuel cell vehicles; major technical

and infrastructure improvements needed.• Battery-powered vehicles; major technical

and some infrastructure changes needed.

44

Goals

• Establish as a goal the maximum practicable number of alternative vehicles and fuels the can penetrate the market by 2020 ( and beyond to 2050)

• Evaluate technology status

• Determine potential oil and CO2 savings

• Determine the funding, public and private, to reach that goal

• Establish a budget roadmap to achieve the goal

• Determine the government actions required to achieve the goal

55

Presentation Outline

• Scenarios

Market Penetration Rates

Technology Status

FCV and PHEV Costs• Oil and CO2 Savings

• Timing and Transition Costs to Achieve Market Competitiveness for FCVs and PHEVs

• Infrastructure Issues• Conclusions

6

SCENARIOS Case1) H2 SUCCESS H2 & fuel cells play a major

role beyond 2025

Case 2) EFFICIENCY(ICEV) Potential improvements in gasoline ICE and HEV technologies successful

Case 3) BIOFUELS Large scale use of biofuels, focus ethanol

Case 4) PLUG-IN HYBRID SUCCESS PHEVs play a major role beyond 2025

Case 5) PORTFOLIO APPROACH More efficient ICEVs + biofuels + FCVs or PHEVs introduced

7

Case 1-Hydrogen Fuel Cell Vehicles

Hydrogen Fuel Cell VehiclesHydrogen Production Routes

Coal

Reformer

Gasifier

Natural Gas

Electric Power Plant

Solar PV

Hydrogen

Primary Energy Resource• Coal• Natural Gas• Nuclear• Hydro•

Renewables

Wind

Biomass

Generator

Generator

Nuclear heat

Gasifier

Electrolyzer

Steam Electrolysis

CO2 Sequestration

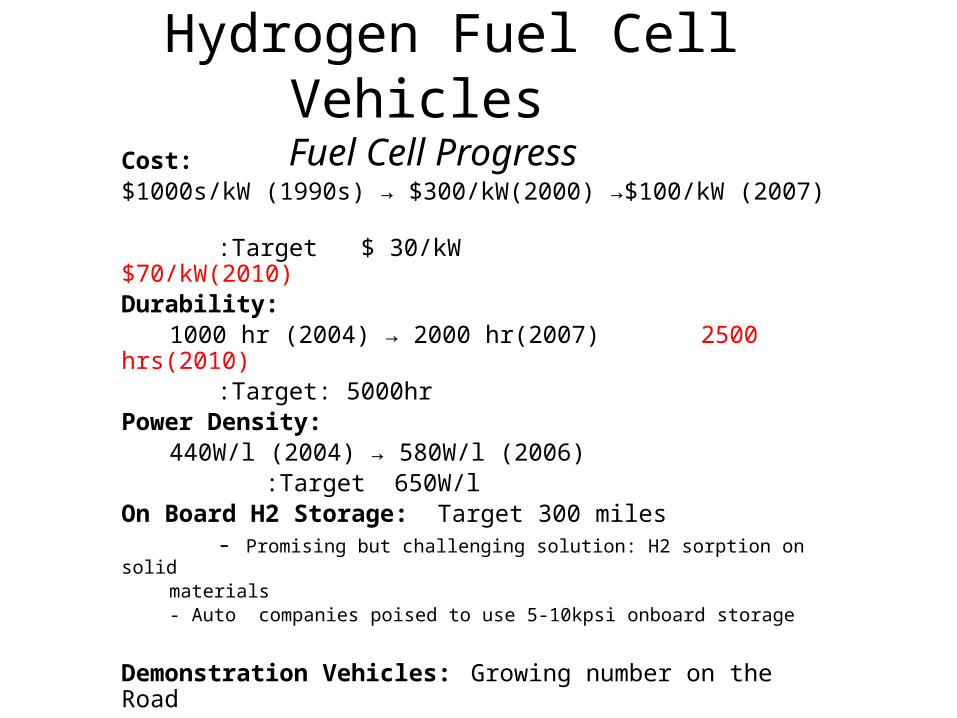

Hydrogen Fuel Cell Vehicles Fuel Cell Progress

Cost:

$1000s/kW (1990s) → $300/kW(2000) →$100/kW (2007) :Target $ 30/kW $70/kW(2010)

Durability:

1000 hr (2004) → 2000 hr(2007) 2500 hrs(2010):Target: 5000hr

Power Density:

440W/l (2004) → 580W/l (2006) :Target 650W/l On Board H2 Storage: Target 300 miles - Promising but challenging solution: H2 sorption on solid

materials - Auto companies poised to use 5-10kpsi onboard storage

Demonstration Vehicles: Growing number on the Road

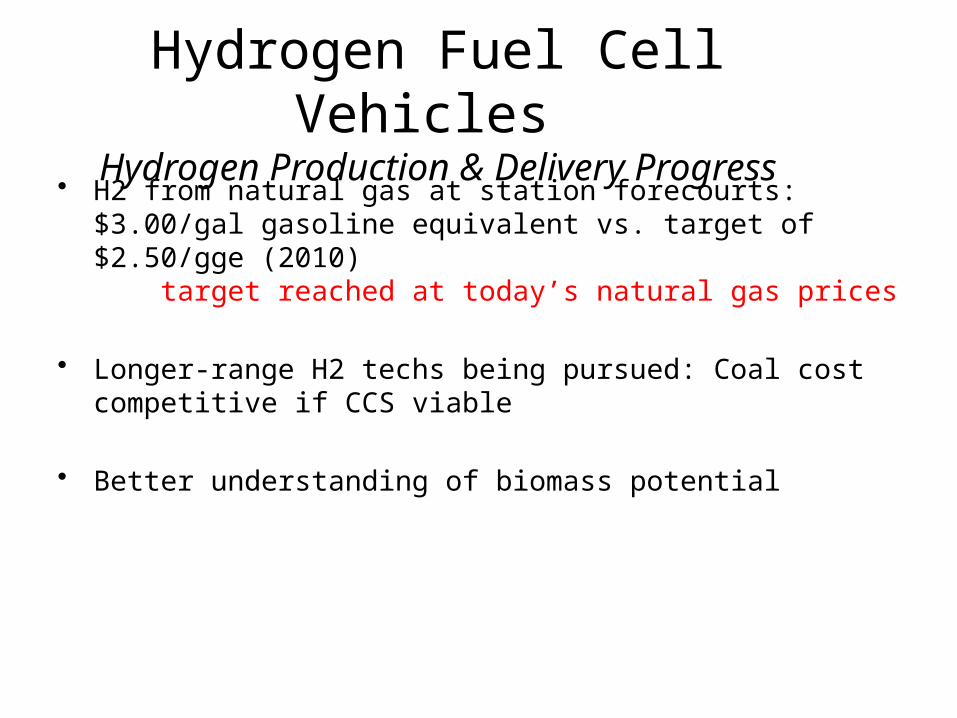

Hydrogen Fuel Cell Vehicles Hydrogen Production & Delivery Progress

• H2 from natural gas at station forecourts: $3.00/gal gasoline equivalent vs. target of $2.50/gge (2010) target reached at today’s natural gas prices

• Longer-range H2 techs being pursued: Coal cost competitive if CCS viable

• Better understanding of biomass potential

11

Hydrogen Fuel Cell VehiclesMaximum Practical Penetration Rate

Maximum practical penetration rate estimated assuming:

• Technical goals are met• Consumers accept HFCVs• Oil prices remain high (EIA high oil

price scenario used as reference case)• Policies are in effect to support HFCVs

and hydrogen production.

12

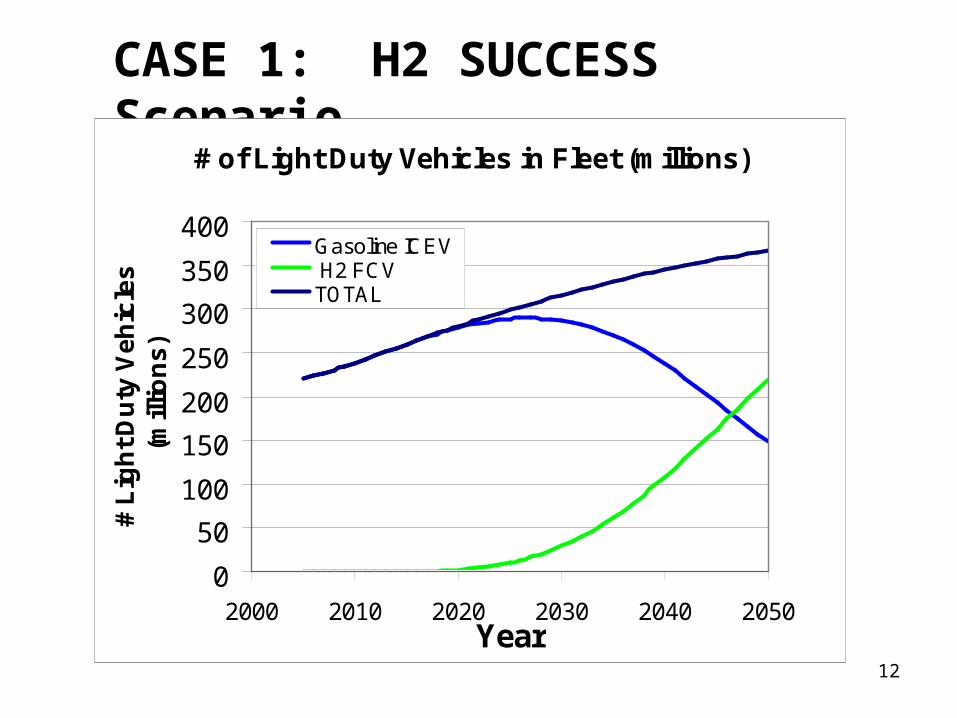

CASE 1: H2 SUCCESS Scenario

# of Light Duty Vehicles in Fleet (millions)

0

50

100

150

200

250

300

350

400

2000 2010 2020 2030 2040 2050Year

# L

igh

t D

uty

Ve

hic

les

(m

illio

ns

)

Gasoline ICEV H2 FCVTOTAL

13

Case 1 (Hydrogen Success): Gasoline Consumption

0

50000

100000

150000

200000

2000 2010 2020 2030 2040 2050

Year

Mill

ion

gal

lon

s g

aso

line

per

yea

r Case 1 (H2Success)

Reference

14

• The estimated government cost to support a transition to HFCVs is roughly $55 B from 2008 to 2023.

$40 B - the incremental cost of HFCV $8 B - the initial deployment of H2 supply infrastructure $5 B for R&D.

• Industry cost for H2 infrastructure $400 B by 2050 * -180,000 stations - 210 central plants - 80,000 miles of pipeline

* 220,000,000 HFCVs

Hydrogen Fuel Cell VehiclesImplementation Costs

15

add section title

1. Add picture of ICE and Hybrid vehicle 1 picture use something from one of the auto presentations

2. Add slide as what we did ie did not look at costs, but tech = penetration potential

Case 2 - Fuel Economy Improvement

16

Fuel Economy Improvement

• The Energy Independence and Security Act of 2007 raises fuel economy standards to 35 mpg by 2020.

• This study evaluated technologies to improve fuel economy but did not closely examine costs.

• Gasoline HEVs dominate; no FCVs or PHEVs• Continued advancements in conventional vehicles offer

significant potential• 2.6%/year 2010 to 2025• 1.7%/year 2026 to 2035• 0.5%/year 2036 to 2050

17

Fuel Economy ImprovementTechnologies

FE Improvement 2015 2025• Engine/Transmission: 14% 20%

– Variable valve timing & lift– Cylinder deactivation– Gasoline direct injection

• Weight, drag, tires: 8% 12%• Accessories: 2% 4%• Idle Stop: 3% 4%

18

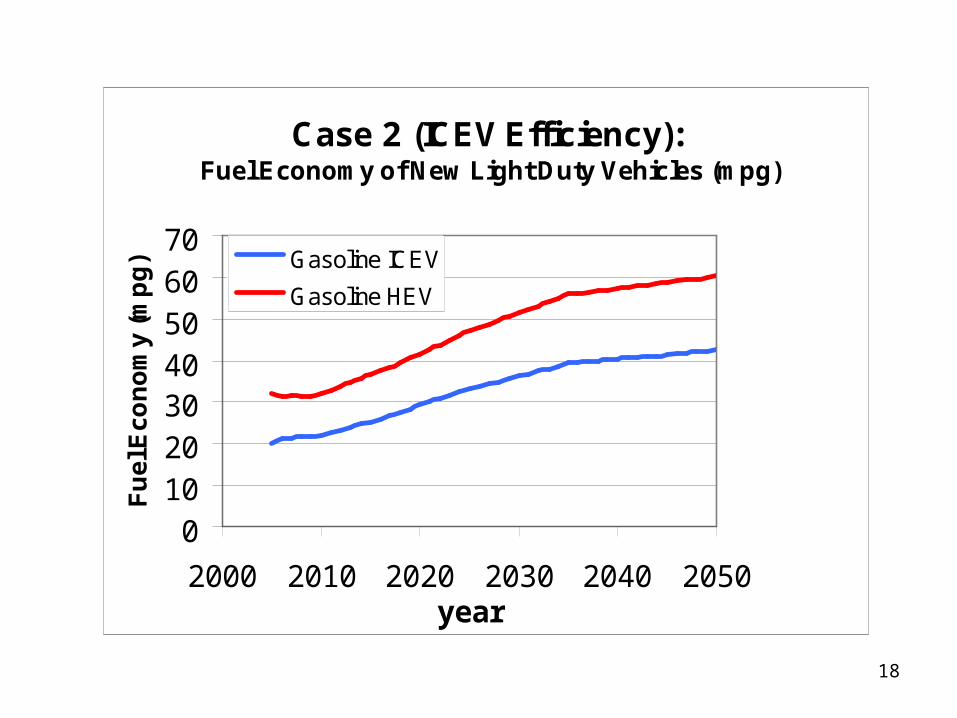

Case 2 (ICEV Efficiency): Fuel Economy of New Light Duty Vehicles (mpg)

010203040506070

2000 2010 2020 2030 2040 2050year

Fu

el E

con

om

y (m

pg

) Gasoline ICEV

Gasoline HEV

19

Case 2 (ICEV Efficiency): Number of Light Duty Vehicles (millions)

0

100

200

300

400

2000 2010 2020 2030 2040 2050

Year

# V

ehic

les

(mill

ions

)Gasoline ICEV

Gasoline HEV

TOTAL

Fuel Economy Improvement Fuel Consumption

Case 2 (ICEV Efficiency): Gasoline Consumption (million gallons per year)

0

50000

100000

150000

200000

1990 2010 2030 2050

Year

Gas

olin

e C

on

sum

pti

on

(mill

ion

gal

lon

s p

er y

ear)

Case 2 (ICEVEfficiency)

Reference

21

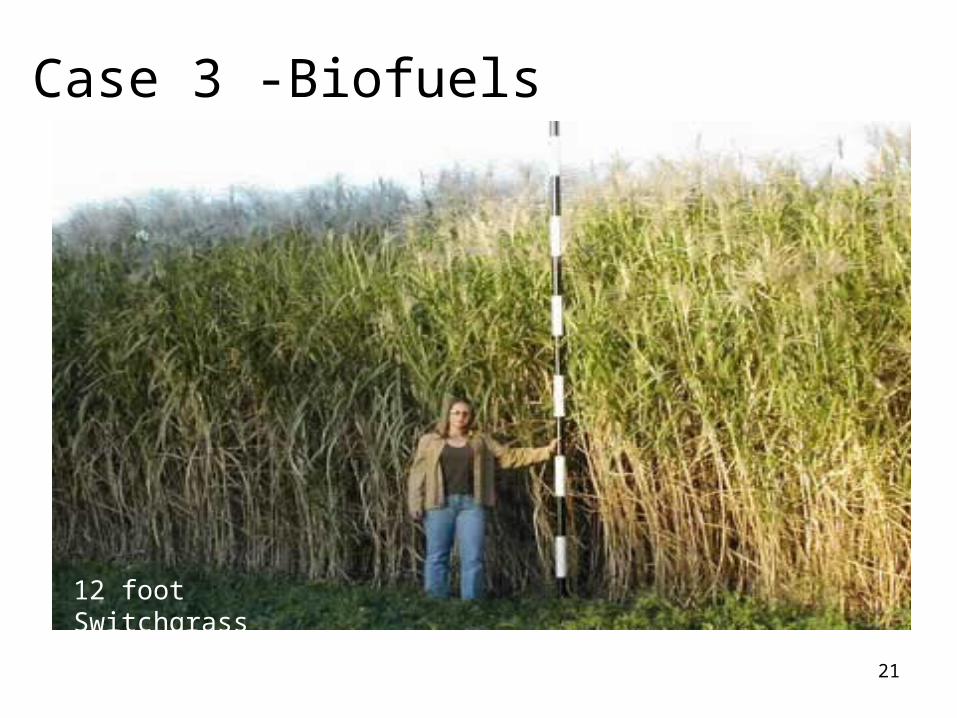

Case 3 -Biofuels

12 foot Switchgrass

Biofuels• Study analyzed

Potential amount of sustainable biomass

Technologies to convert biomass to fuels

Fuel products

• Looked at technical potential but did not closely examine costs

• Study focus was on US oil and CO2 reduction

BIOFUEL SUCCESS

• Grain and Sugar based ethanol - maximum potential 12 billion gallons/year

• Sustainable biomass (million dry tons per year)*

300 mtpy current, 500 mtpy 2030, 700 mtpy 2050• Cellulosic ethanol has significant potential, 10 billion

gallons/year by 2020 and 45 billion(gas eq) by 2050 **• Large portion of biomass could be converted other

advanced biofuels after 2020

*crop residues, energy crops, forest residues

** gasoline equilvalent

*** maximum practicable case

BiofuelsTotal Production

CASE 4 - PHEVS

Chevy VOLT

25

26

CASE 4: PHEVS

• 2 mid-size vehicle types: PHEV-10s, PHEV-40s• 2 market penetration rates:

– Maximum Practical (same as H2 FCVs but start earlier (2010)

– Probable• 2 electricity grid mixes (business as usual and

EPRI/NRDC scenario for de-carbonized generation in a 2007 study)

• PHEV gasoline and electricity use based on estimates by MIT, NREL, ANL

PHEV Cost Analysis: Batteries are Key

Need acceptable cost for reasonable range, durability, and safety

27

2828

Batteries

• Looked at 10 and 40 mile midsize cars - PHEV-10s and PHEV-40s

• Battery packs with 2 and 8 kWh useable

or 4 and 16kWh nameplate energy– Start of life, not after degradation– 200 Wh/mile – 50% State of Charge range (increases to compensate

for degradation)

2929

Current PHEV Battery Pack Cost* Estimates Compared ($/kWh nameplate)

• $700-1500/kWh (McKinsey Report)• $1000/kWh (Carnegie Mellon University)• $800-1000/kWh (Pesaran et al)• $500-1000/kWh (NRC: America’s Energy Future

report)• $875/kWh (probable) NRC PHEV Report• $625/kWh (optimistic) NRC PHEV Report• $560/kWh (DOE, adjusted to same basis)• $500/kWh (ZEV report for California)*Unsubsidized costs

3030

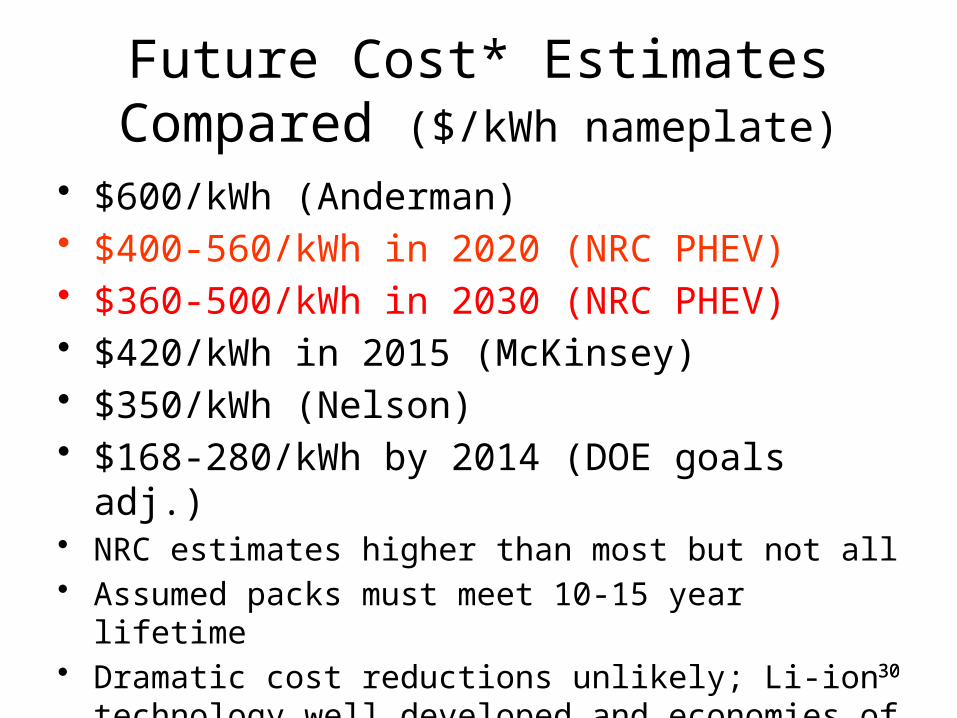

Future Cost* Estimates Compared ($/kWh nameplate)

• $600/kWh (Anderman)• $400-560/kWh in 2020 (NRC PHEV)• $360-500/kWh in 2030 (NRC PHEV)• $420/kWh in 2015 (McKinsey)• $350/kWh (Nelson)• $168-280/kWh by 2014 (DOE goals adj.)• NRC estimates higher than most but not all • Assumed packs must meet 10-15 year lifetime• Dramatic cost reductions unlikely; Li-ion technology well

developed and economies of scale limited*Unsubsidized costs

3131

Vehicle Costs

PHEV-40• Total Pack cost now $10,000 - $14,000• Total PHEV cost increment over current conventional

(non-hybrid) car: $14,000 - $18,000• PHEV cost increment in 2030: $8,800 - $11,000

PHEV-10• Total Pack cost now $2500 - $3,300• Total PHEV cost increment over current conventional

(non-hybrid) car $5,500 - $6,300• PHEV cost increment in 2030: $3,700 - $4,100

3232

Electric Infrastructure

• No major problems are likely to be encountered for several decades in supplying the power to charge PHEVs, as long as most vehicles are charged at night.

• May need smart meters with TOU billing and other incentives to charge off-peak.

• Charging time could be 12 hours for PHEV-40s at 110-V and 2-3 hours at 220-V. Thus home upgrade might be needed.

• If charged during hours when power demand is high, potential for significant issues with electric supply in some regions.

0

50

100

150

200

250

2000 2010 2020 2030 2040 2050

No

. o

f v

eh

icle

s (

mil

lio

ns

)

Maximumpracticalpenetration

Probablepenetration

33

CASE 4: PHEV Market penetration• Maximum Practical (with optimistic tech development

estimates): 4 million PHEVs in 2020 and 40 million in 2030• Probable (with probable technical development): 1.8 million

PHEVs in 2020 and 13 million in 2030

33

• Many uncertainties, especially willingness and ability of drivers to charge batteries almost every day.

3434

Gasoline Use

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2010 2020 2030 2040 2050

Year

Ga

so

line

us

e (

mill

ion

ga

llon

s/y

r) Reference Case

Efficiency Case

PHEV-10(maximum)+Efficiency

PHEV-40(maximum) +Efficiency

CASE 4: PHEV Fuel SavingsRelative to Efficiency Case

35

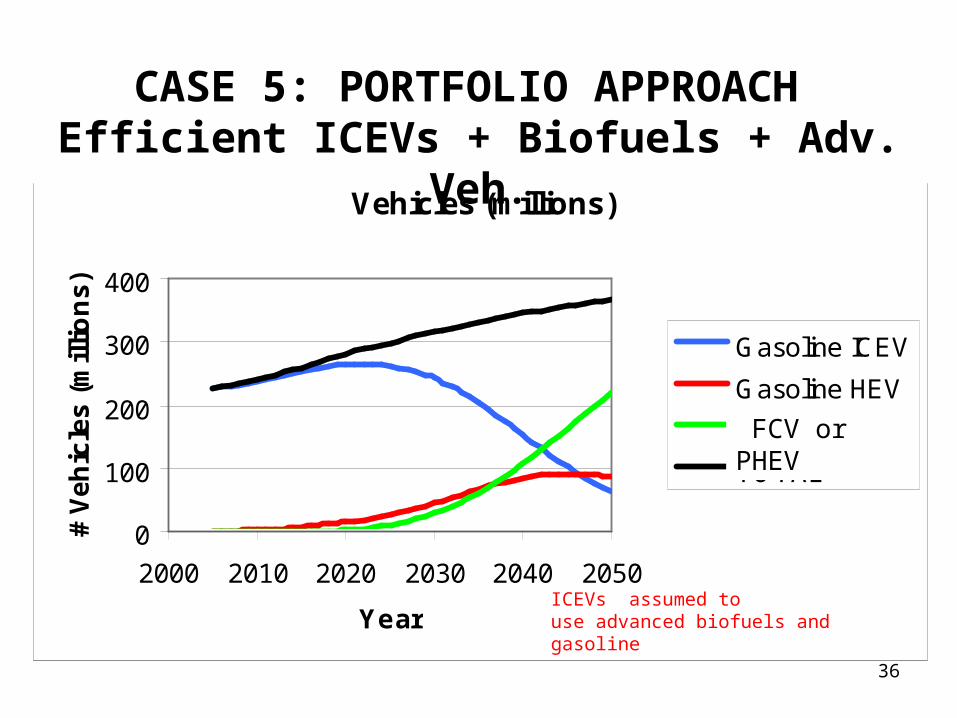

CASE 5: PORTFOLIO APPROACH

Efficient ICEVs + Biofuels + Adv. FCV+PHEVs

36

Case 4 (portfolio): Number of Light Duty Vehicles (millions)

0

100

200

300

400

2000 2010 2020 2030 2040 2050

Year

# V

eh

icle

s (

mil

lio

ns

)

Gasoline ICEV

Gasoline HEV

Hydrogen FCV

TOTAL

CASE 5: PORTFOLIO APPROACH Efficient ICEVs + Biofuels + Adv. Veh.

FCV or PHEV

ICEVs assumed to use advanced biofuels andgasoline

3737

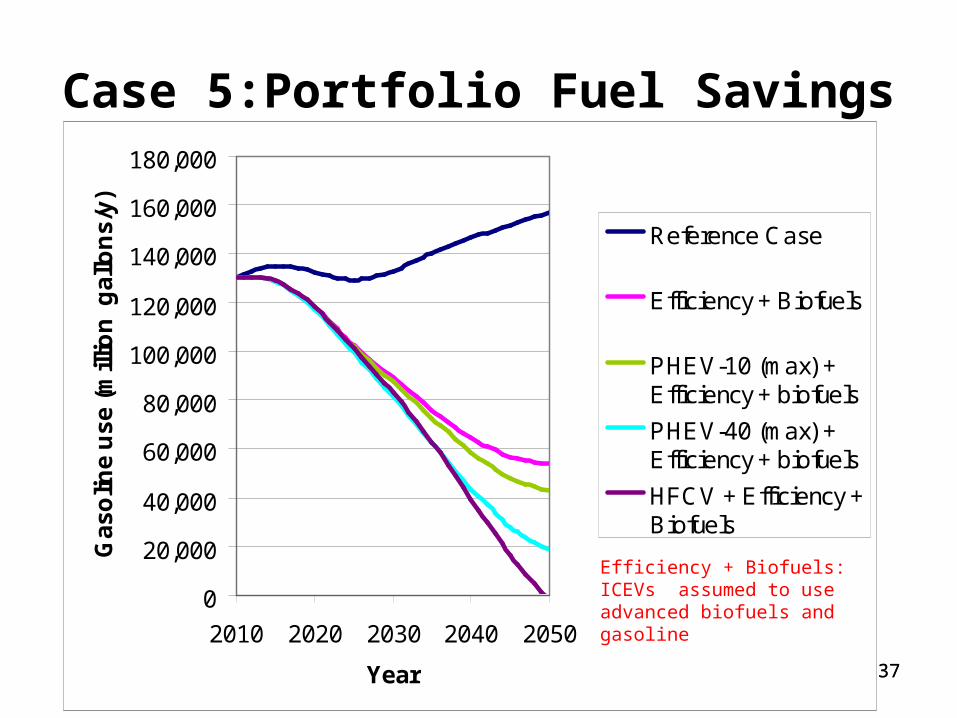

Case 5:Portfolio Fuel Savings

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2010 2020 2030 2040 2050

Year

Ga

so

line

us

e (

mill

ion

ga

llon

s/y

)

Reference Case

Efficiency + Biofuels

PHEV-10 (max) +Efficiency + biofuels

PHEV-40 (max) +Efficiency + biofuels

HFCV + Efficiency +Biofuels

Efficiency + Biofuels: ICEVs assumed to use advanced biofuels and gasoline

3838

GHG Emissions EIA Grid (million tonnes CO2e/yr)

0

200400

600800

1000

12001400

16001800

2000

2010 2020 2030 2040 2050

Year

GH

G e

mis

sio

ns

(m

illio

n t

on

ne

s C

O2

e p

er

ye

ar) Ref Case

Efficiency +Biofuels

PHEV-10 (max) +Efficiency +Biofuels

PHEV-40 (max) +Efficiency +Biofuels

HFCV + Efficiency+ Biofuels

Case 5:Portfolio GHG Emissions BAU Electric Grid

3939

GHG Emissions EPRI/NRDC Grid (million tonnes CO2e/yr)

0

200400

600800

1000

12001400

16001800

2000

2010 2020 2030 2040 2050

Year

GH

G e

mis

sio

ns

(m

illio

n t

on

ne

s C

O2

e p

er

ye

ar) Reference Case

Efficiency +Biofuels

PHEV-10 (max) +Efficiency +Biofuels

PHEV-40 (max) +Efficiency +Biofuels

HFCV + Efficiency+ Biofuels

Case 5:Portfolio GHG Emissions De-carbonized Electric Grid(EPRI/NRDC)

Potential Transition Costs for HFCV and PHEVs

40

41

PHEV-10 PHEV-40 PHEV-40 Sensitivity Cases

High Oil DOE Goal

HFCVSuccess Partial

Success

Breakeven Year

2024 2040 2025 2024 2023 2033

Cum. Cash flow to breakeven ($billion)

24 408 41 24 22 46

Cum. Vehicle Retail Price Diff to breakeven ($ billion)

82 1639 174 82 40 82

# Vehicles at breakeven (million)

10 132 13 10 5.6 10

Infrastructure Cost at breakeven ($ Billion)

10(in-home charger @$1000)

132(in-home charger @$1000)

13(in-home charger @$1000)

10(in-home charger @$1000)

8 (H2 stations for first 5.6 million FCVs)

19 (H2 stations for first 10 million FCVs)

41

TRANSITION COSTS: PHEVs and H2 FCVS

1-3 decade transition time; Transition cost $10s-100s Billions;Results very sensitive to oil price and vehicle (battery& fcell) costs

4242

Major Findings• Significant fuel and CO2 reductions can be achieved over

next 20 years with efficient ICE/HEV technologies and biofuels.

• PHEVs and HFCVs have greater long-term potential for fuel savings. HFCVs can greatly reduce CO2 emissions, but savings from PHEVs dependent on grid fuel source.

• A portfolio of technologies has potential to eliminate oil and greatly reduce CO2 from US light duty transportation by 2050

• The U.S. could have tens of millions of H2 FCVs and PHEVs on the road in several decades, but that would require tens or hundreds of billions in subsidies

• Technology breakthroughs are essential for both fuel cells and batteries; cost reductions from manufacturing economies of scale will be much greater for fuel cells than batteries

Backup Slides

43

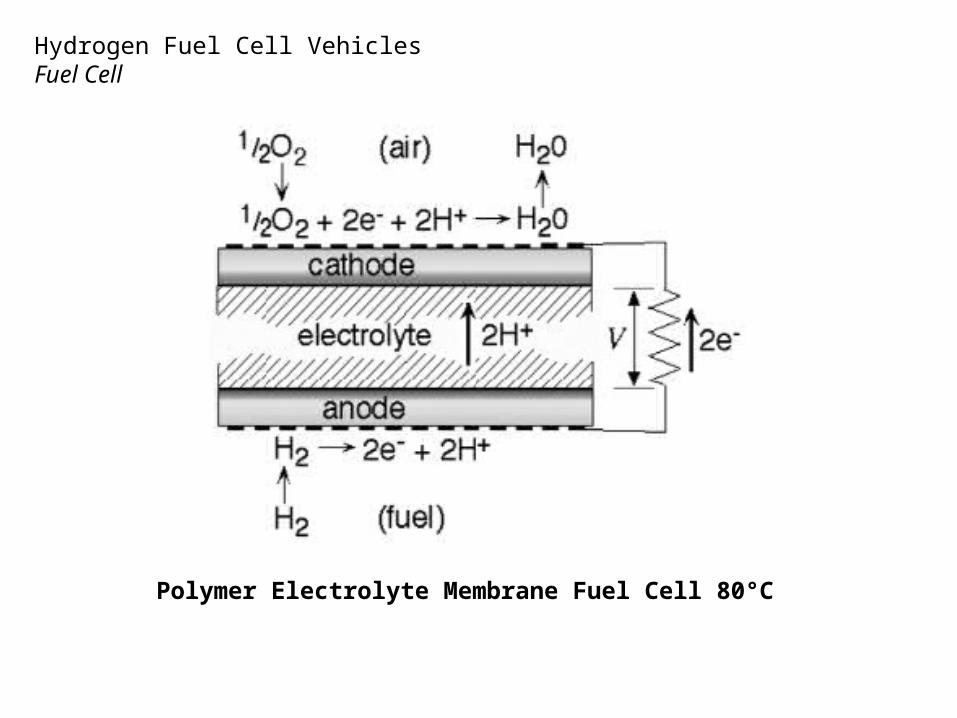

Hydrogen Fuel Cell VehiclesFuel Cell

Polymer Electrolyte Membrane Fuel Cell 80°C

Hydrogen Fuel Cell VehiclesInfrastructure Cases

4646

AEO 2008 High Oil Prices Case and EPRI/NRDC 2007. Environmental Assessment of Plug-In Hybrid Electric Vehicles. Volume 1: Nationwide Greenhouse Gas Emissions.

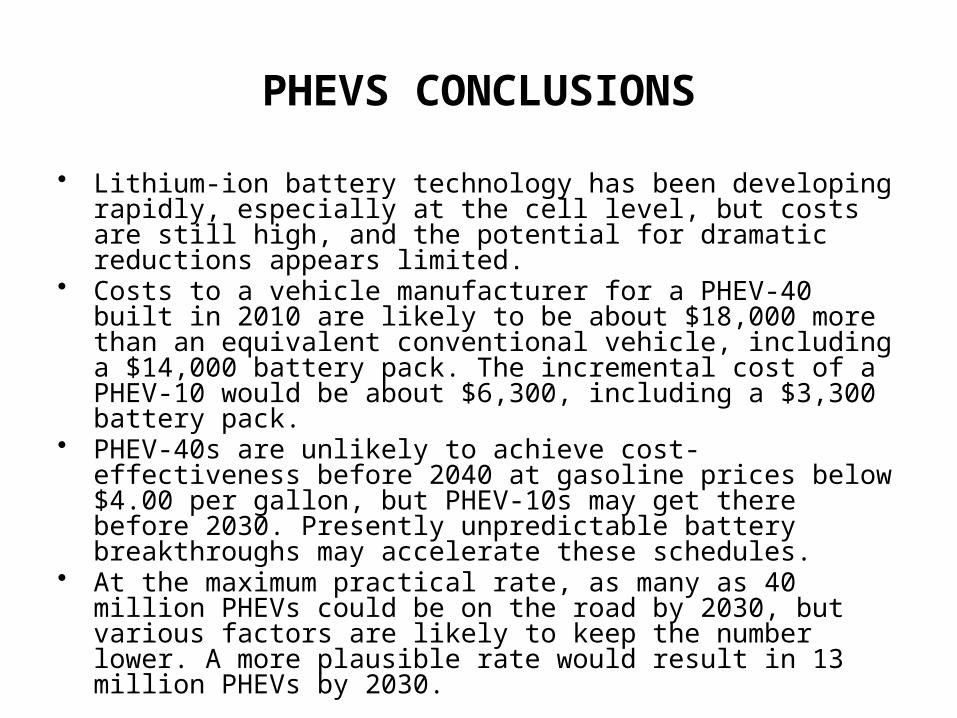

PHEVS CONCLUSIONS

• Lithium-ion battery technology has been developing rapidly, especially at the cell level, but costs are still high, and the potential for dramatic reductions appears limited.

• Costs to a vehicle manufacturer for a PHEV-40 built in 2010 are likely to be about $18,000 more than an equivalent conventional vehicle, including a $14,000 battery pack. The incremental cost of a PHEV-10 would be about $6,300, including a $3,300 battery pack.

• PHEV-40s are unlikely to achieve cost-effectiveness before 2040 at gasoline prices below $4.00 per gallon, but PHEV-10s may get there before 2030. Presently unpredictable battery breakthroughs may accelerate these schedules.

• At the maximum practical rate, as many as 40 million PHEVs could be on the road by 2030, but various factors are likely to keep the number lower. A more plausible rate would result in 13 million PHEVs by 2030.

PHEVS CONCLUSIONS cont• PHEVs will have little impact on oil consumption before 2030

because there will not be enough of them in the fleet. More substantial reductions could be achieved by 2050. PHEV-10s will reduce oil consumption only slightly more than can be achieved by HEVs.

• PHEV-10s will emit less carbon dioxide than nonhybrid vehicles, but show little advantage over HEVs after accounting for emissions from the electric power generation.

• No major problems are likely to be encountered for several decades in supplying the power to charge PHEVs, as long as most vehicles are charged at night.

• A portfolio approach to research, development, demonstration, and, perhaps, market transition support is essential.

Liquid Fuel DemandGlobal, United States, and U.S. Imports

2006

2006

2006

2030

2030

2030

2030

2030

2030

0

20

40

60

80

100

120

140

Global Demand U.S. Demand U.S. Imports (net)

Mil

lio

n B

arre

ls p

er D

ay

2006 - Actual

2030 - Reference

2030 - High Price

Non-OPEC

Saudi Arabia

Venezuela

Nigeria

Algeria

Iraq

Kuwait

Other OPEC

OPEC

50

United States

United States

Global

Global

0

2000

4000

6000

8000

10000

12000

14000

2006 2030

Mill

ion

Met

ric T

ons

of C

arbo

nCarbon Emissions

51

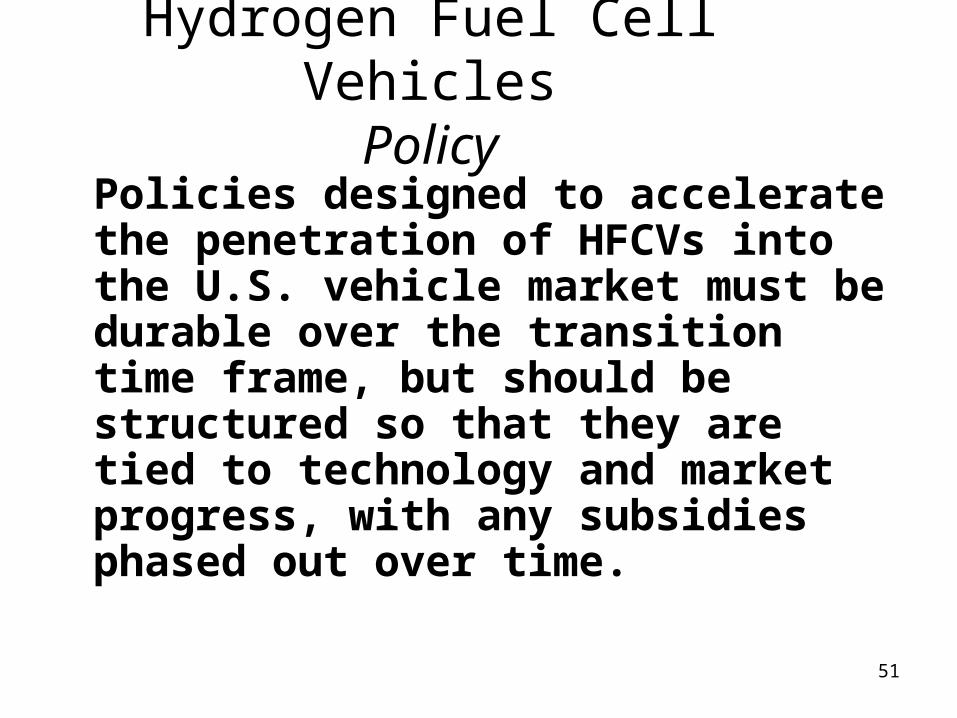

Policies designed to accelerate the penetration of HFCVs into the U.S. vehicle market must be durable over the transition time frame, but should be structured so that they are tied to technology and market progress, with any subsidies phased out over time.

Hydrogen Fuel Cell VehiclesPolicy

Transportation Energy Policy

Hydrogen fuel cell vehicles and other emerging technologies collectively

- potential to eliminate oil demand from LDT 2050.

- reduce GHG emissions to less than 20% of current

Policies must support a portfolio of technologies to achieve these results and be durable and sustainable

53

Type of Hydrogen Supply over Time

Case 1 (Hydrogen Success) 2020 2035 2050

No. of cars served (percentage of total fleet)

1.8 million (0.7%) 61 million (18%) 219 million (60%)

Infrastructure capital cost $2.6 billion $139 billion $415 billion

Total No. of stations 2,112 (all on-site SMR)

56,000 (40% on-site SMR)

180,000 (44% on-site SMR)

No. of central plants 0 113 (20 coal, 93 biomass)

210 (79 coal, 131 biomass)

Pipeline length (miles) 0 39,000 80,000

Hydrogen demand (tonnes per day)

1,410 (100% NG)

38,000 (22% NG, 42% biomass, 36% coal with CCS)

120,000 (31% NG, 25% biomass, 44% coal with CCS)

NOTE: NG = natural gas.