11 december 2007 amcor management briefing

TRANSCRIPT

Ken MacKenzie

11 December 2007Amcor Management Briefing

Agenda

• Introduction – Ken MacKenzie• Presentations and Q & A’s from:

– Ron Delia– Gerard Blatrix

• Morning tea• Presentations and Q & A’s from:

– Jerzy Czubak– Peter Brues

• Sandwich lunch• Presentations and Q & A’s from:

– Eric Bloom– Billy Chan

• Summary – Ken Mackenzie

The Way Forward - Agenda

Improve shareholder

valueEXECUTION FOCUS

Strong market

positionsLow cost

Customer & market focused

Capital discipline

CULTURAL CHANGE

The Way Forward

• Solid progress across all aspects of the agenda

• Execution focus a key priority to maintain momentum

• More emphasis on developing the growth agenda

EXECUTION FOCUSStrong market

positionsLow cost

Customer and market

focused

Capital discipline

Value PlusBuilding Sales and Marketing Excellence

SydneyDecember 2007

Value Plus Debrief

Context: Value Plus & The Way Forward

Initiative overview

Progress to date

Value Plus and the Way Forward

– Universally acknowledged need to upgrade commercial capabilities– Potential source of value creation and competitive advantage

EXECUTION FOCUS

Strong market

positions

Low cost

Customer and market

focused

Capital discipline

CULTURAL CHANGE

Improve shareholder

value

Value Plus and the Way Forward

Value Plus…Building sales & marketing excellence across Amcor

EXECUTION FOCUS

Strong market

positions

Low cost

Customer and market

focused

Capital discipline

CULTURAL CHANGE

Improve shareholder

value

Objectives of Value Plus

Value Plus is an Amcor-wide, multi-year initiative to:

1. Improve returns by identifying and capturing commercial opportunities

AND

2. Upgrade the Sales & Marketing capabilitiesacross the company

Building competitive advantage, ensuring sustainability

Value Plus Debrief

Context: Value Plus & The Way Forward

Initiative overview

Progress to date

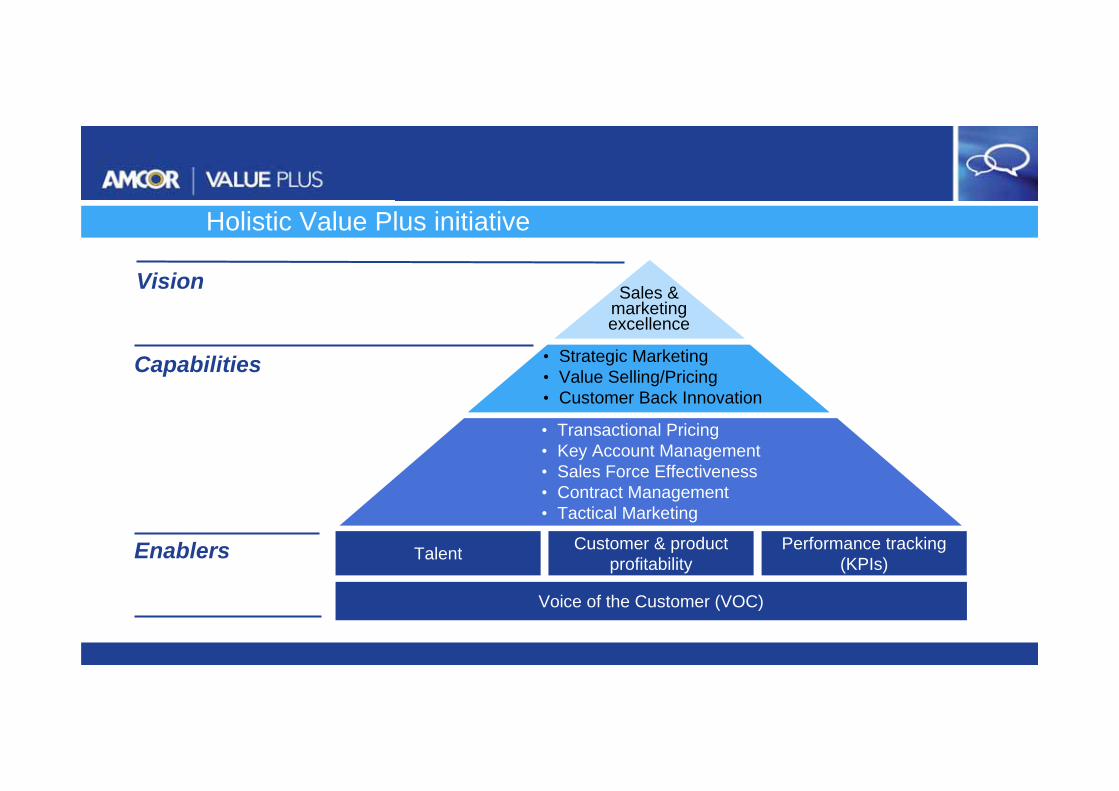

Vision

Enablers

Capabilities

• Transactional Pricing• Key Account Management• Sales Force Effectiveness• Contract Management• Tactical Marketing

• Strategic Marketing• Value Selling/Pricing• Customer Back Innovation

Sales & marketing excellence

Holistic Value Plus initiative

Voice of the Customer (VOC)

Talent Customer & product profitability

Performance tracking (KPIs)

Vision

Enablers

Capabilities

• Transactional Pricing• Key Account Management• Sales Force Effectiveness• Contract Management• Tactical Marketing

• Strategic Marketing• Value Selling/Pricing• Customer Back Innovation

Sales & marketing excellence

Holistic Value Plus initiative

Voice of the Customer (VOC)

Talent Customer & product profitability

Performance tracking (KPIs)

Vision: Sales & Marketing Excellence

“Unique insights via deeper customer and market understanding”

“Elevated stature of Marketing & Sales”

“Improved execution through upgraded commercial capabilities”

“Best commercial talent in the packaging industry”“Sustainable

Financial Impact”

Customer /Market

People

Culture

Capabilities –“Amcor Way”

Vision

Enablers

Capabilities

• Transactional Pricing• Key Account Management• Sales Force Effectiveness• Contract Management• Tactical Marketing

• Strategic Marketing• Value Selling/Pricing• Customer Back Innovation

Sales & marketing excellence

Holistic Value Plus initiative

Voice of the Customer (VOC)

Talent Customer & product profitability

Performance tracking (KPIs)

“Voice of the Customer” (VOC)

Customer Satisfaction Metrics

Importance Amcor

Overall customer satisfaction -- 8.0

Overall product quality -- 8.5

Delivery when requested -- 8.8

Ease of Doing Business 9.5 8.8

Value for the price 9.5 9.3

Resolves problems quickly and effectively 9.8 8.0

Responsive to price requests 9.3 9.3

Responsive to changing forecasts 9.7 9.3

Responsiveness to new development 9.3 7.7

Responsiveness to sample 9.0 8.7

Accounts receivable resolution 9.3 9.0

Order processing/ order confirmation Insufficient data

Account Support

Rating Comment

Quality of Account Support

8.0 “They are good at follow through and open communication.”

Knowledgeable About Business

8.3 “Amcor knows our business pretty well.”

Effective at Bringing Value Added Solutions

7.3 “Amcor should be more proactive in bringing new ideas

to us.”

Provide Proactive Communications

8.0 “They should be more focused in our account.”

How Responsive 8.0

Problem Solving 7.3 “Amcor should help us make things work better.”

Example

Talent: KPIs and dashboards Example

0%

20%

40%

60%

80%

100%

Aust Sun FH FF Ren PET Total

Intermediate High Outstanding

35

665

2

25

8

3

43

3038

42

10

20

30

40

50

60

70

80

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08

External Ins Internal Ins Pipeline

0%

20%

40%

60%

80%

100%

Aust Sun FH FF Ren PET Total Exptd

Meets some Meets mostDvp/Meets All ExceedsSignificantly exceeds

0%

20%

40%

60%

80%

100%

Head ofS&M

SalesMgr

KAM AM Reps Total

Meets some Meets mostDvp/Meets All ExceedsSignificantly exceeds

Pivotal Role Talent Review Meetings -completed & planned Group Pivotal Role Talent:- Outs/Net Change

Group Pivotal Role Talent In’s Recruitment Actual vs. Target Pipeline

Group Pivotal Role Talent Review- Performance Outcomes

BG Pivotal Role Talent Review Potential Outcomes -current cycle

BG Pivotal Role Talent Review Performance Outcomes -current cycle

Pivotal Role Talent Review Meetings -completed & planned Group Pivotal Role Talent:- Outs/Net Change

Group Pivotal Role Talent In’s Recruitment Actual vs. Target Pipeline

Group Pivotal Role Talent Review- Performance Outcomes

BG Pivotal Role Talent Review Potential Outcomes -current cycle

BG Pivotal Role Talent Review Performance Outcomes -current cycle

131 20 16 29 21 37 254

Reviews completed Last Next

AA 2 Mar 07 Jul 07Sun 2 Feb 07 Jun 07PET 3 Jan 07 Sep 07

FF 2 Feb 07 TBDFH 2 Feb 07 Aug 07

Rentsch 2 Jan 07 Jul 07

20 12 1510

25

1020304050

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08

Invol outs (ext) Invol outs (int)Lack of career opps Personal reasonsWork demands/travel RetirementRemuneration Lack of training & devOther PromotionsNet ins/outs

Excludes AFF Excludes AFF

PerformancePotential

Pipeline

Example

• Functional heads from each business

• 7of 12 are new to role since 2006 (5 of 12 new to Amcor)

• Active cross-business governance group– Value Plus/capability building– Best practice sharing– Customer/market strategies– High potential talent

Australasia

Flexibles

PET

Sunclipse

• Corporate – Michael Todd• Fibre – Paul Ward • Flexibles – Peter Briscoe

• Healthcare – Tom Cochran• Food – Andy Marko• Rentsch – Marco Hilty

• NA Beverage – Bill Featherstone• NA DPD – Kirby Losch• LA – Luiz Magalhaes

• KHL – Bernie Salvatore– Greg Hummel

• MPP – Art Castro

Sales & Marketing Leadership Council

Talent: Key appointments in leadership roles

Customer and product profitability: “Pocket margin database” (PMDB)

• Transaction-level “income statements” aggregate up to customer or product PBIT• “Pocket Margin” lexicon taking hold

EXAMPLE

Pocket marginPBIT

Net sales

Customer and product profitability: Common toolsEXAMPLE

Performance tracking: Sales rep levelEXAMPLE

Performance Tracking: Business levelEXAMPLE

Vision

Enablers

Capabilities

• Transactional Pricing• Key Account Management• Sales Force Effectiveness• Contract Management• Tactical Marketing

• Strategic Marketing• Value Selling/Pricing• Customer Back Innovation

Sales & marketing excellence

Holistic Value Plus initiative

Voice of the Customer (VOC)

Talent Customer & product profitability

Performance tracking (KPIs)

Capability Example: Key Account Management

Supply Chain

Plant QA/Ops

Product Development

Technical Service

Finance

BG/BU General

Management

Key account manager

Formal cross functional teams

ensure full organizational support for key

customers

Capability Example: Key Account Management

VOC

Fact-based account planning

EXAMPLE

PMDB

X-func teams

Talent

Capabilities: Rolled-out in ‘Waves’ across Amcor

Wave I

Flexibles

Healthcare NA

Key accountsNA

Wave II

FibreQueensland

Flexibles NZand Kewdale

Food

Healthcare EU

NA RegionalAccounts

DPD NA RegionalAccounts

Australasia

Flexibles

PET

Wave III

Fibre NSW

Mexico

Europe

Fibre Vic

Food

Healthcare

Rentsch

Sunclipse Kent H. Landsberg

Value Plus Debrief

Context: Value Plus & The Way Forward

Initiative overview

Progress to date

Progress to date: Highlights

• Enablers– New customer understanding and insights– Key recruitments and on-going talent upgrade– Granular profit data across 90% of Amcor– Performance culture intensifying in sales & marketing

• Capabilities– Completed waves across 80% of Amcor– Beginning to roll-out more sophisticated approaches– Greater emphasis across the businesses on “marketing”

Gérard Blatrix

11 December 2007Sydney

AF Food December 2007 2

Agenda

• Conclusion• Impact of External Factors• Sustainability offers Product Development Opportunities• Sustaining Benefits and Accelerating Growth• Progress on Flex1• Our Strategic Priorities• Update on 'The Way Forward'• Flexibles Food - an organisation geared for growth• Overview of the Business

AF Food December 2007 3

Overview of the Business

Coffee21%

Cheese7%

Bread15%

Ready Meals15%

Produce21%

Yoghurt13%

Conf.8%

27 Plants in 12 Countries Key Market Segments and Market Share

Flexibles Food - €1 billion sales – 4,900 employees

AF Food December 2007 4

Flexible Packaging Market in Europe

10%€400mEastern Europe (EE)€9,000mTotal

4%€600mCentral Europe (CE)1%€8,000mWestern Europe (WE)

Growth RateFlexibles Packaging DemandRegion

EECEWE

AF Food December 2007 5

Product Segments

Yoghurt Ready MealsBread

Coffee

AF Food December 2007 6

Product Segments

Cheese Confectionery Produce

AF Food December 2007 7

Leading through Innovation - PushPop

Benefits:What is it?• Innovative new packaging design• Differentiation• Stackable shape• Entire surface available for printing (including

top and bottom)• Convenience - easy open, wide opening• Gas tight and gas flushable• Use on any vertical form fill seal packaging

machine with 4-side seal facility

PushPop is an: • Easy open• Flexible• Stand-up• Stackablepack that retains its original shape and brand identity and has a wide opening

AF Food December 2007 8

Leading through Innovation - Monoflex

Benefits:What is it?• Monoweb instead of duplex• Defined tearing properties• High puncture resistance• Low temperature sealing• Runability on high speed VFFS/HFFS• Stiffness• Cost effective• Excellent transparency or high opacity• Strong euroslot

Monoweb co-extruded PP-core based blown film - can be used for direct contact seal or impulse sealing applications.Can be used on:• VFFS and HFFS packing lines • Thermoforming machines for lidding• VFFS machines with impulse sealingSuitable for Gravure and Flexo print

AF Food December 2007 9

Organisation structure

ManufacturingExcellence

MD

Sales &Marketing

HR CFO

Restructuring"Flex1" Strategy

SouthProduce & Bakery North & CEE

Lean Manufacturing

Value+Marketing & Innovation

Strong ProjectTeam

Integration of CEE

M&A and Segment

Participation

TalentManagement

Capital Discipline

& Cost Control

AF Food December 2007 10

Update on 'The Way Forward'

• Margins improved:– Price– Product/Customer Mix

• Sales slightly above last year• Improved cost base as a result of last year's restructuring

Value Plus Impact

ImprovedRoAFE

Working Capital continues to decrease17.4 15.8

12

05/06 06/07 07/08

%

ImprovedPBIT

AF Food December 2007 11

Our Strategic Priorities

1. Finalise and deliver benefits from 'Fix, Sell, Close' get fit programme:– Flex1 Execution

2. Consolidate existing capabilities and build new ones for achieving a sustainable enhanced profitability:– Value Plus– Manufacturing Excellence – SG&A Cost Reduction (including standardisation of business processes)

3. Develop "Sweet Spots" at an above-market growth rate:– Reinforce key success factors such as Innovation and increased plant

focus

4. Accelerate growth in Central and Eastern Europe:– Organic growth supported by substantial investments in Poland & Russia– Selected acquisition targets

AF Food December 2007 12

What is Flex1?

• Comprehensive programme designed to:– Strengthen market positions– Increase weighting in the lower cost regions– Improve alignment to customer needs and market trends– Create a strong platform for innovation

• The first phase was the successful closure of two plants in 2006/07

• Current phase commenced in April 2007:– Cost of €60m with benefits of €30m

AF Food December 2007 13

What is Flex1?

Flex1:Optimisation of the whole process for Food and Healthcare Europe:• Less plants• More technologically focused• Consistent with growth in CEE

Film Extrusion Film Conversion

FilmBlown Extrusion • Printing

• Lamination• Slitting

AF Food December 2007 14

Progress on Flex1 (Fix - Close - Sell):Conversion

• 27 Sites• 8 involved in Flexo Printing• 16 involved in Gravure Printing

• 36 Sites (inc. Healthcare Europe)• 13 involved in Flexo Printing• 19 involved in Gravure Printing

Future FootprintOriginal Footprint

Already Announced:• A major restructuring in Sweden September 2007• One plant closure in the UK (Flexo consolidation) October 2007• One plant closure in Denmark October 2007• Capacity investment in Poland Ongoing

We are ahead of the original schedule

AF Food December 2007 15

Flex1 Next Steps and Expected Benefits

1. Next Steps:– Additional plant closures will be announced to support our strategy

of moving East and consolidating Extrusion– Investment in new equipment– Headcount reduction of 900– Divestment of non-strategic businesses on track

2. Expected Benefits:– Previously announced benefit (Conversion and Extrusion) of €30m

per annum confirmed– Lower operating costs– Increased plant focus

AF Food December 2007 16

Sustainability offers Product Development Opportunities

NaturePlus Film - a range of recyclable, degradable, biodegradable and compostable films

Peelable PLA Film

Natureflex Film

PLA Film, P-Plussed

MaterBi Bags

AF Food December 2007 17

Influence of External Factors

• Oil Price/Inflation:– Raw materials are at historic highest– Food prices are increasing at double digit rate:

Contract Management/Value+ Programme Market conditioned for price increase

• US$ vs. Euro:Limited exposure of AF Food

• Economic Slow Down:Limited risk of reduction of volume in our traditional business

Favourable environment to push through price increases

AF Food December 2007 18

Raw Material Market Price Trends Forecast to March 2008

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0Ja

n-03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Inde

x of

Mar

ket M

ovem

ent

AF Food December 2007 19

Conclusion

1. The execution programme is well on track:• Flex1 implementation• Business turn around

2. We’ve established strategic priorities and started implementation:• Capabilities development (Value Plus, Lean Manufacturing)• Growth in selected market segments - “sweet spots”• Growth in Central/Eastern Europe (organic and potential

acquisitions)

3. We are preparing our business for the growth agenda:• Organisation• Talent

11 December 2007Amcor RentschJerzy Czubak

Agenda

• Business Overview• European Market• Projects

– Ukraine– PepsiCo plant in Poland

• Summary

• Switzerland• France• Germany• Portugal • Poland• Russia• Ukraine

Plants by Region Amcor Rentsch Global Tobacco Footprint

Europe/ CIS

Asia • China (10)• Singapore• Malaysia

Australasia

Total

• Australia

20 plants

Global Presence – Tobacco Packaging

Agenda

• Business Overview• European Market• Projects

– Ukraine– PepsiCo plant in Poland

• Summary

• The market in Europe continues to grow as measured by “printing machine hours”– Added complexity

• Shorter run lengths due to increased number of SKU’s• Introduction of Graphical Health Warnings• More value adding features including embossing and hot foil stamping

– Increased production introduced to Western Europe by a major customer

• Large customers continue to gain market share

Current European Market Position

• A leader in Western and Eastern Europe

– Focused on the large multinational customers

• Leading the market in innovation

– Value add products have had strong growth

Amcor has a Strong Position

• Across Europe available machine hours for the industry has reduced

• Additional “specialised” capabilities are required

• Amcor gaining share as large customers win share

Short Term Supply / Demand Imbalance

These combined factors have resulted in overtrading in Eastern Europe in the first half.

The Big Players (BAT, JTI and PMI) are Gaining Market Shares

7% 7%7% 7% 7%

7% 7%7% 7% 7%

13%

37%

1.462

2001

24%23%

13%

14%

35%

1.487

2002

25%

15%

15%

31%

1.485

2003

26%

16%

15%

29%

1.457

13%

27%

17%

16%

26%

1.456

20052004

JTI

BAT

ImperialAltadis

Others

100%

PMI

Source: Euromonitor (2007), team analysis

Demand Development by Customer in Bio CigarettesTotal market size*

* Total market: Africa and Middle East, Western and CIS (selected countries)** Others: Bulgartabac Holding Group, Donskoi Tabak, Karelia Tobacco, Neman Tobacco…

Expected Evolution

7% 7%

13% 15% 15%7%7%

24%

18%

1.447

17%

16%

26%

2006

27%

18%

17%

24%

1.430

2007

17%

24%

18%

1.411

28% 28%

24%

18%

15%15%

2008 2009

28%

1.376

2010

27%

1.387

Because of PMI Moving Business to EU and Export Business, EU Demand for HL Remains Stable

797811825799817837873931

973965968

537537549556563557520505498464

318233225225224224223239253247237232

2004 2005 2006 2007 2008 2009 2010

EUCISAfrica and Middle East

2000 2001 20032002

Production Volume of Cigarettes, Bio sticks

Total 1518 1666 1718 1689 1632 1617 1604 1579 1599 1573 1527

40B PMUSA sticks to PMINTL

Source: ERC, 2007, team analysis

Market shares

9%

7%

26%Amcor

22%Alcan

14% MMG

19%

Wall

4%A&RFields

Other

Competitive Situation – Western Europe (EU)

3,9

Four strong manufacturers in Western Europe

37%

Amcor

16%

Alcan

18%

MMG

8%Wall

12%A&R

18%

Other

Competitive Situation – CIS

Market shares

1,6Amcor is the clear leader in Eastern Europe

European Tobacco Market – Summary

• The market in Europe continues to grow in terms of printing machine hours and value add requirements

• Amcor, as the market leader, will focus on:– Building additional capacity

• Ukraine

– Enhancing value add production capabilities• Offset and Hot foil stamping

• Leadership in innovation and complex production will be the key differentiating factor in the future

Value Proposition• “One stop innovation shop” with all

processes on site• “Speed to Market”• Proximity to customers and key suppliers• Modern and efficient production and

converting technology • Value and cost driven customer services to

generate sustainable benefits for customers and the AR Group

• Highly flexible organisation

Strong Focus on InnovationsInnovation Centre Amcor Rentsch

Switzerland is the ideal location for the Innovation Centre:• Small• Highly competent• Well equipped • Flexible• Dedicated

Innovative Solutions• Packaging shapes• Packaging appearance• Surface treatment• New technologies• New services

Strong Focus on InnovationsInnovation Centre Amcor Rentsch

Switzerland is the ideal location for the Innovation Centre:• Small• Highly competent• Well equipped • Flexible• Dedicated

Innovative SolutionsPackaging Shapes

Lighter Pack Scissor Pack

Accordion Pack Aqua Pack

Innovative SolutionsPackaging Shapes

Rising Pack Take one Pack

Innovative SolutionsPackaging Shapes

Ink Technology• High gloss• Pearlescent inks• Metallic inks• Metallure inks• Laser-sensitive inks• Effect inks• Fluorescent / phosphorescent

inks

Innovative SolutionsPackaging Appearance

Foil Technology• Hot Foil Stamping• Hologram Foil• Defraction Foil • Holographic Security

Features• Holographic Features

Innovative SolutionsPackaging Appearance

Embossing• Structured Embossing• Relief Embossing

– Pyramid– Raised / rounded

• Embossing of lines and crest

Innovative SolutionsSurface Treatment

Contracts – Tobacco

Russia• Master agreements with customers signed at Group Level• Sub-Agreements signed with each local Russian affiliate to comply with

Russian legislation• Prices marked to, and invoiced in Euro or USD• Payments received in RUR based on Euro price at rate on date of payment

per Russian Central Bank

Contracts – Tobacco

Poland• Master agreements with customers signed at Group Level• Prices marked to Euro or USD and invoiced in PLN for local affiliates at

Polish Central Bank Rate on date of invoice• Payments received in PLN based on Euro or USD price at rate on date of

payment per Polish Central Bank

Agenda

• Business Overview• European Market• Projects

– Ukraine– PepsiCo plant in Poland

• Summary

Consumption by Country in Europe

354560

90115120130

210

0

50

100

150

200

250

German

y

Turke

y

Netherl

and

Ukraine

Polan

d

Spain

Roman

ia

Franc

eBill Sticks Ukraine – one of the largest markets in Europe

Ukraine – Project Summary

• Brownfield investment in Kharkiv, second largest city in Ukraine– Brownfield enables faster and simpler project – Project to be managed by Novgorod management – Ukraine plant will be a satellite site of Novgorod

• Location has close proximity to customers in Ukraine and southern Russia

• Production commencing in December 2007• Total investment $A20 mill

Progress Photos

Factory view from the main road

Progress Photos

Production area

Agenda

• Business Overview• European Market• Projects

– Ukraine– PepsiCo plant in Poland

• Summary

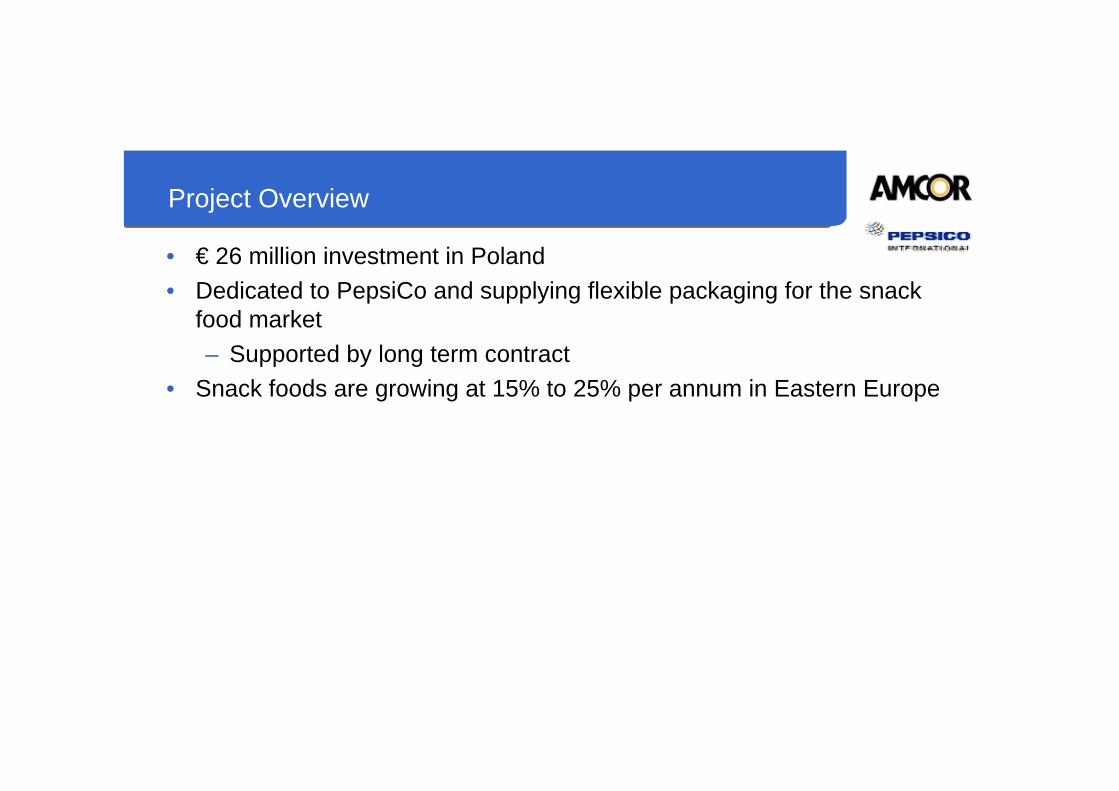

Project Overview

• € 26 million investment in Poland• Dedicated to PepsiCo and supplying flexible packaging for the snack

food market– Supported by long term contract

• Snack foods are growing at 15% to 25% per annum in Eastern Europe

Plant Visualisation

Equipment

• Most modern, fastest equipment available in the world– An 8 colour German flexographic printing press– An Italian extrusion laminator– British slitters and packing line

• Comprehensive quality control systems and data capture systems– High security site to maintain good food safety standards– Accreditations - ISO 9000 (quality), AIB (hygiene), ISO 14000

(environment), BRC• A truly world class business

Key Dates

• Contract signed April 2007• Factory build started September 2007• Commissioning of machines April 2008• Commercial start-up May 2008

Agenda

• Business Overview• European Market• Projects

– Ukraine– PepsiCo plant in Poland

• Summary

Summary

Tobacco Packaging• In Western Europe be low cost producer with well located sites• Continue to expand in growing regions of Central and Eastern

Europe• Focus on complexity and innovationsCentral and Eastern Europe Flexibles• Expand manufacturing footprint (leverage tobacco manufacturing

facilities)• New business dimension (technology, skills, dedication) with the

Pepsico plant• Support to Amcor Flexibles Food with shared services (HR; Finance,

IT, Logistic) and manufacturing excellence practices

11 December 2007Sydney

Peter Brues

2

Agenda

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

3

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

4

Global Healthcare Sites

Sales $0.7 billion16 Plants in 10 Countries

c. 2,200 Employees

AF Mundelein •AF Madison • • AF Ashland

• Mt. Holly Stevens •

AF Sligo •AF Winterbourne •

• AF LogroñoAF Leaderpack •AF Burgos •

• AF GentAF SPS • • AF Albertazzi

• AF Puerto Rico

• AF Brazil

AF Singapore •

5

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

6

Healthcare Attractions

• Packaging cost is relatively low compared to the selling price of the entire product

• Packaging often critical in protecting our customer’s products and essential in product differentiation

• Customers require package characteristics that are aligned with Amcor’s competencies

• The growth in this industry outpaces GDP

7

Medical Packaging

35%10%

14%

7%34%

AmcorAlcanBemisWipakOther

8

Leading Medical Device Manufacturers

Customer Sales Head OfficeCardinal Health $81 Billion USJ&J $53 Billion USKimberly-Clark $11 Billion USBaxter $10 Billion USCovidien (formerly Tyco Healthcare) $10 Billion US

Market Trends:• Commodity production moved to developing countries• Rising concern of hospital infections• Production of high technology devices growing in developed countries• Increased emphasis on Form-Fill-Seal from Bags & Pouches• Increase in chronic illness and access to chronic care

9

Pharmaceutical Packaging

6%50%

25%

12%

7%

AmcorAlcanKlocknerConstantiaOther

10

Leading Pharmaceutical Companies

Customer Sales Head OfficePfizer $48 Billion USGlaxoSmithKline $47 Billion UKNovartis $37 Billion CHMerck $23 Billion USAstra Zeneca $26 Billion US

Market Trends:• Differentiation through ease of delivery• Combat counterfeiting• Senior friendly + child resistant• Growing importance of India

11

Personal Care Packaging

18%25%

10%47%

AmcorAlcanBemisOther

12

Leading Personal Care Companies

Customer Sales Head OfficeProcter & Gamble $68 Billion USUnilever $56 Billion UKL’Oréal (Nestlé) $20 ($170) Billion F (CH)

Colgate $12 Billion USBeiersdorf $7 Billion D

Market Trends:• Differentiation through package appearance & features• Differentiation through package ease of use• Increased emphasis on emerging markets

13

Key Implications for Packaging Suppliers

• Quality & Service are a minimum

• Importance of Selling Skills

• Importance of Innovation

• Importance of Ease of Working with you

• Importance of Decorating Expertise

• Global Manufacturing Capabilities

14

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

15

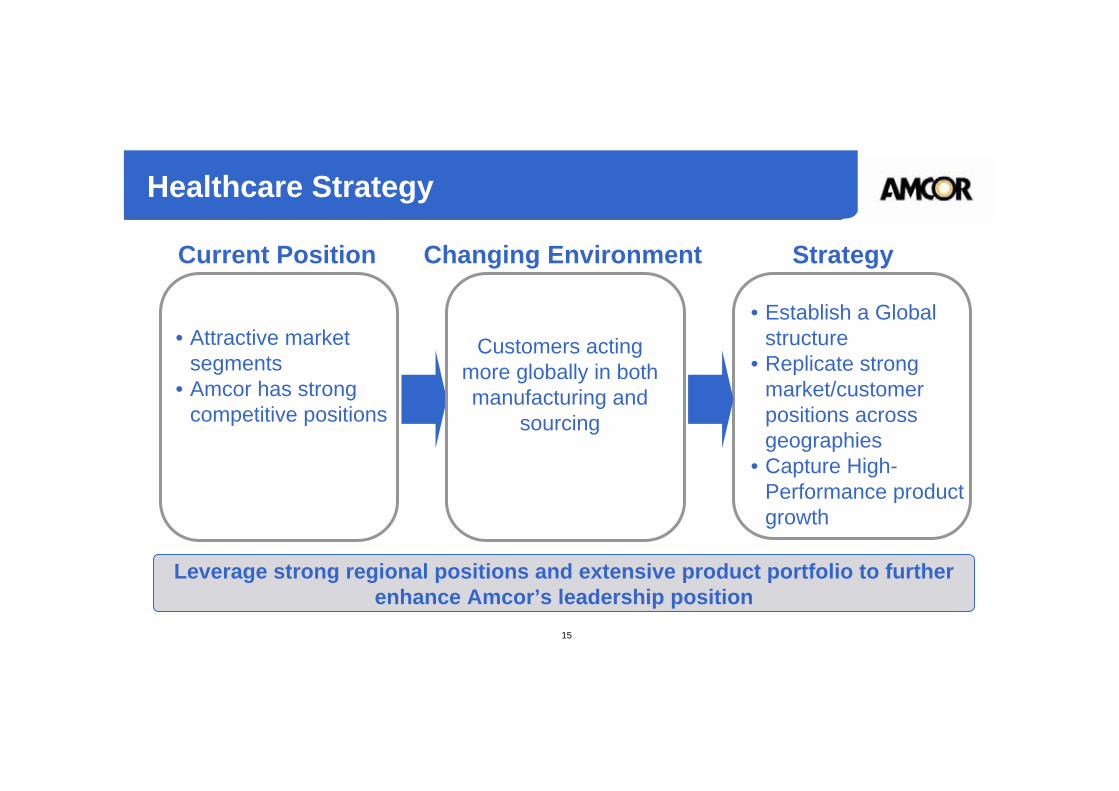

Healthcare Strategy

Leverage strong regional positions and extensive product portfolio to further enhance Amcor’s leadership position

• Attractive market segments

• Amcor has strong competitive positions

Customers acting more globally in both manufacturing and

sourcing

• Establish a Global structure

• Replicate strong market/customer positions across geographies

• Capture High-Performance product growth

Current Position Changing Environment Strategy

16

Shifting to High Performance

Sweet Spots

Maximize Share

Opportunity Spaces

Market Penetration

Focused Positions

Selective Competition

Question Marks

Fix /Planned Exit

Amcor Thrust = Leverage strong customer positions and technology platforms / effective innovation and speed to market; Exploit group

know-how to achieve high efficiencies as critical mass is established

High Performance

Amcor Thrust = Focus market participation on selected segments and partners; execute

commercial & manufacturing improvements to offset market price pressures; exit commoditized markets in a planned and appropriate manner

Standard Performance

17

Global Healthcare – Market Position

30%

Size $0.7BGrowth 4% Size $1.2B

Growth 4% Asia (ex.J) JapanSize $0.3B $0.4BGrowth 13% 3%

Size $0.3BGrowth 6%

27% 25%

7%

11%

Amcor Other

18

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

19

Key Strategic Initiatives

We will win by executing the following:

• Superior Strategic Marketing & Customer Focus

• Innovate to Create Differentiated Products

• Obtain an Advantaged Cost Position

• Acquire and Develop Strong Talent

20

Innovate to Create Differentiated Products –High Barrier/Performance Laminate Platform

Existing Customer

Package for Blood Testing device

• High barrier lamination package

Product Development

Overwrap & Bags for liquids

• Extractable component expertise

• Precipitate formation learning

• Seal Integrity

New Product Sale

High barrier package for Inhaler refill cartridge

• Significant reduction in extractables

• Increased machine speeds

• Better seal strength

• Sharper graphics

21

Advantaged Cost Positions - Progress on Flex1 Extrusion

Change Benefit• Focus on 3 Strategic Sites• 40% decrease in lines / same

capacity• Focused R&D facility

• Improved production efficiency and cost structure

• Accelerated product development

Progress:

• Investments in infrastructure underway and first lines being installed• One plant closure in Denmark announced• Resin rationalization trials underway

We are on schedule to achieve our commitments

22

Performance

StrongPBIT

SoundRoAFE

Solid Cash Flow

• Profitable sales growth

• Decreasing cost base

• Improving capital management

23

• Overview

• Market

• Strategy

• Initiatives & Performance

• Conclusion

24

Summary

We will profitably grow our global leadership position through:

• Strengthening advantaged positions, leveraging regional competencies globally and maximizing growth in high-performance product segments

• Creating a market facing organization that leverages global opportunities

• Innovating to create differentiated products

• Creating and enhancing advantaged cost positions

• Developing and recruiting exceptional talent

December, 2007

Analyst Presentation

2

Corru Kraft II

Mission Corrugated

Corru Kraft IV

Mercury Die & Container

St. Hart Container

Midway Container

Mercury Container

Silicon Valley Container

Sycamore Containers

Master Box Cerritos

Master Box Phoenix

KHL Los Angeles* KHL San Diego KHL Oakland* KHL Ontario (CA-USA)

KHL San Jose KHL Sacramento KHL Orange County KHL Inside Sales

KHL Tijuana

KHL EPS Northwest

KHL EPS Southwest

KDS Packaging

KHL Indianapolis KHL St. Louis KHL Fresno

KHL Portland

KHL Seattle KHL Juarez KHL Mexicali

KHL Memphis

KHL Chicago* KHL Phoenix KHL El Paso

KHL Sycamore

KHL Guadalajara KHL Dallas* KHL Denver

KHL Santa Barbara

KHL Houston

KHL EPS Atlanta

KHL EPS Chicago

KHL Asia

KHL New Jersey

KHL Incentive

KHL Europe

KHL Reno

LBR Master Distribution

MPP Brea

KHL Atlanta*

Amcor SunclipseNorth America

FY08 Est. $1,000M

DistributionFY08 Est. $778M

1,271 Co-Workers

MPP GroupFY08 Est.$228.8M 670

Co-Workers

CorrugatorsFY08 Est.$186.5M 283 Co-Workers

Master Box No. CA

Organizational Structure: Amcor Sunclipse North America

Box PlantsMaster Distribution Sites

Distribution Sites (Non Hub)

37 Distribution Sites7 Box Plants4 Master Distribution Sites3 Corrugated Plants

Distribution Hub Sites

Corrugated Plants

Sunclipse Locations (North America)

4

The Value ChainCorruKraft

(Corrugators)MPP Group

(Sheet Plants)Master Box(Master Distributor)

Kent H. Landsberg KHL EPS(Distributor)

END

CUSTOMER

END

CUSTOMER

MANUFACTURING

MANUFACTURING

CONVERTING

CONVERTING

DISTRIBUTION

DISTRIBUTION

MASTER

DIST

MASTER

DIST

CompetitorCompetitor Competitor

CompetitorCompetitor Competitor

5

The Sunclipse Business Model

50%

50%

50%

50%

6

Product Overview

CorruKraftCorrugated

Board

MPP GroupConverted Products

Point-Of-Purchase

Digital Printing

Master Box

Redistribution

Packaging Equipment

Packaging Materials

Promotional Products

Corrugated Boxes

Packaging Supplies

Janitorial Supplies

Kent H. Landsberg Co.KHL Engineered Packaging Solutions

Segment Attractiveness - Growth Projections

7

Estimated Annual Growth (2008/2009)Manufacturing 2.9%Contract Packaging 10.0%Warehousing & Supplies 2.0%Food & Flexibles 3.3%

Manufacturing38%

Other13%

Food & Flexibles12%

Contract Packaging12%

Warehouse & Supplies25%

Market Share: Corrugators

8

California – 50B SQ FT

CorruKraft8%

Other92%(4) 36 Integrateds

16 Independents

Market Share: Manufactured Packaging Products

9

Integrateds75%

OCC2.0%

MPP4.4%

WeyerhaeuserInternational Paper

Temple InlandSmurfit Stone

Packaging Corporation of AmericaGeorgia Pacific

California – 50B SQ FT

Market Share - Distribution

10

US Packaging Wholesale / Distribution Market

Unisource11.1%

Xpedx9.1%

Bunzl6.7% KHL

2.5% Victory Package 1.7%Stephen Gould 1.3%

Uline 3.0%

Other (+/- 7000 Co.)64.6%

STRATEGIC ACCOUNTS,TEAM WORLD

• Multi-Location• Team Objectives• Geographic Reach• EDI or Web Based

11

KHL EXPRESS• Web Based, Pay for

Freight, Credit Card

KHL SALES REPRESENTATIVE

• Call Cycle• Commercial Account• Freight Paid or Not• EDI or Web-Based• Landsberg.com Tiered Pricing

for “Never Hads”

Volume / $ Spend +

+

Cus

tom

er’s

Per

ceiv

ed N

eed

(Val

ue-A

dd) INSIDE SALES

• Call Cycle• Commercial Account

Customer Channel Plan (Distribution)

12

Distribution Sales Force

• “Rookies” (90)– Rigorous, structured, disciplined training & selection process– Two year duration– High attrition rate, but better than competitors

• “Veterans” (257)– High performance– Low attrition rate– Heavily supported

• Inside Sales Force (27)– Same rigorous recruitment and training– Different focus, skill set– Key component of Channel Plan

13

Sales Force Remuneration

• Rookies– Low base wages– Expenses– Excellent benefits

• Veterans– Full commission only

– Percentage of Adjusted Gross Profit– Expenses included in commissions– Excellent benefits

• Inside Sales– Low base wages– Commission

– Small Percentage of Adjusted Gross Profit– Excellent benefits

14

Sales Representative Development Process• Graduation• Veteran Representative• 100% Commission• Self Directed

• Graduation• Veteran Representative• 100% Commission• Self Directed

• Recruiting• Assessing• Shadowing• Inside Training• Phone Sales• LSA

• Recruiting• Assessing• Shadowing• Inside Training• Phone Sales• LSA

• Route Book• Prospecting• Daily Meetings• Morning Calls• Ride Alongs• Product Training• Boot Camp

• Route Book• Prospecting• Daily Meetings• Morning Calls• Ride Alongs• Product Training• Boot Camp

• Independent Sales Calls• Continuous Evaluation

• Quarterly Review• KPIs

• Training Ride Alongs• Continued Selling Edu.• Role Playing• Presentation Training• Socratic Sell Process

• Independent Sales Calls• Continuous Evaluation

• Quarterly Review• KPIs

• Training Ride Alongs• Continued Selling Edu.• Role Playing• Presentation Training• Socratic Sell Process

24 MONTHS6 MONTHS 12 MONTHS 18 MONTHS

2 YEARS

VALUE

•35% ROI•10+ Year Commitment

15

Sensitivities to Economic Slowdown

• Manufacturing hardest hit due to narrow focus; however is broader than it has been in the past

• Gross Profit compression– Fewer, less effective price increases– Less chance to garner new customers, substitute/redesign

to increase margin

• Easier to hire Sales Trainees, tougher to succeed

• Engineered Packaging Solutions, Strategic Accounts & Inside Sales should provide some offset

• Acquisition candidates easier to find

16

Summary

• Operating performance better than peers

• Unique business model not easily replicated

• Well positioned geographically

• Low share of market presents opportunity

• Distribution sales force recruitment/retention critical

• New product/service opportunities – Some early wins

• Execution of Channel Plan is major opportunity

• Offsetting slowing economy dependent upon key strategic initiatives– Engineered Packaging Solutions– Strategic Accounts– Inside sales

AMVIG Briefing December 2007

(Stock Code : 2300)

2

Agenda

• Industry Features & Outlook • Company Profile• Financial Analysis• Strategy

Chinese tobacco industry• Largest in the world

– Consumption approximately 2.1 trillion cigarettes• Monopoly structure

– Cigarette manufacturing in China a protected monopoly• Government owned

– The cigarette manufacturing industry is fully owned and controlled by the Chinese government

• Quota system– Production of each cigarette manufacturers is based on a quota system

• Growth market– The volume growth for cigarette production is 3-5% per year– Sales value growth is double digit

3

Industry rationalisation• Government led rationalisation began in 2000

– Number of cigarette manufacturers reduced from about 180 to 20

– Number of cigarette brands to be reduced from over 1,800 to around 60

• Focus is on building brands and value

– High volume with at least 1 million master cases

– High margin with RMB10 billion tax and profit contributions

4

AMVIG strategy• Lead rationalisation of the tobacco packaging industry

– Amcor three years ago had around 3% share

– Vision Grande (as AMVIG was named then) had about 5% share

• Build relationship with CNTC and STMA

• Focus on acquisitions

– Target “winning” manufacturers and brands

• Establish / maintain joint ventures with customers where it makes sense

5

AMVIG today• Focused

– Specialises in cigarette packaging printing in China• Scale

– Largest in tobacco packaging printing production capacity in China with around 17% market share following Brilliant Circle acquisition

• Footprint– Well positioned with 10 cigarette packaging printing factories and 4 non-

cigarette packaging printing plants across China• Enhancing value

– Manufacturing laminated papers which are a major raw material for cigarette packaging printing

• Profitable– Most profitable tobacco packaging printer in China

6

Brilliant Circle profile• One of the largest cigarette packaging printers in PRC

• Joint ventures with cigarette manufacturers and CNTC

• Established cigarette packaging businesses in Hunan, Hubei, Anhui, Guizhou and Shenzhen

• 4 cigarette packaging printing operations and 2 laminated paper operations, capacity over 3M master cases

• Designed and printed cigarette packaging for 5 of the top 10 tobacco groups, which include Hunan, Anhui, Hubei, Guizhou and Jiangsu

• Mainly serve the top and high end brands, such as Baisha (白沙), Fu Rong Wang (芙蓉王), Hong Jin Long (紅金龍), Huang Guo Shu(黃果樹), Huang Shan (黃山) and Yi Ping Huang Shan (一品黃山)

7

Acquisition terms• Acquired 100% at 7.5x PE

– Transaction completed in October 2007

• Funded principally via new share issue plus small amount of cash

– Cash payment of HK$155.5M

– Issue 200M AMVIG’s new shares at HK$7.00 per share

• 3 yrs of profit guaranteed at total of HK$630M with first year not less than HK$200M

8

Geographical coverage14 Manufacturing Plants

9

AMVIG•Beijing•Qingdao•Nanjing •Kunming•Shenzhen (2 plants)•Bengbu•Xiangfan•Changde

To commence late 2007•Dongguan

Non-cigarette packaging printing plants•Huizhou•Xian•Changde•Zhaotong

Beijing

Qingdao

Nanjing

ShenzhenDongguanKunming

ZhaotongZhaotongChangde

Xiangfan

Bengbu

Huizhou

Xian Xian

Substantial Value CreationAMVIG has number one position

Turnover

Profitability Productioncapacity

Output

NO.1

• AMVIG’s market share increases from 9% up to 17%

• Major printer to 7 of the top 10 tobacco groups

• Supplier to 6 of the top 10 brands in PRC

Financial results – key figures(HK$ Million) 2006 Interim 2007 Interim Change Turnover 404.1 891.3 +121%Gross Profit 110.5 266.9 +142%Profit from operations 66.7 162.5 +144%Share of results of associates• Nanjing 19.1 21.9 +15%• Kunming 23.9 -Profit before taxation 102.7 180.2 +75%Profit after taxation 90.1 151.7 +68%Profit attributable to equity holders 83.5 139.3 +67%

12

Financial results

Turnover

251.2 237.2

761.9

129.4139.3

885.4132.3 264.9

0

200

400

600

800

1000

1200

1400

2005 2006 1H 2006 1H 2007

HK

$M

Laminated Paper Cigarette Packaging

13

Financial resultsEarnings per Share

17.812.8

14.7

23.4 22.0

05

10152025303540

2005 2006 1H 2007

HK

Cen

ts

First Half Second Half

Net Profit after Tax

69.2 83.5

139.3112.2 166.8

04080

120160200240280320

2005 2006 1H 2007

HK

$M

First Half Second Half

181.4

34.838.1

250.3

7.2

2.812.8

8.5

0

10

20

2005 2006 1H 2007

Interim Dividend Final Dividend Special Dividend

18.5

12.8

7.07 0

Dividends

• 40% payout for the first half of 2007 • Growth stock for the next 3 to 5 years

14

HK

cen

ts p

er s

hare

7.0

Turnover by products

15

Cigarette Packages

762612

265

0200

400600

8001000

1200

1H 2006 1H 2006* 1H 2007

HK

$ M

Laminated Paper

34

74

74

34

31

0

40

80

120

160

1H 2006 1H 2006** 1H 2007

HK

$ M

108

87

42

129139

Sales to Nanjing plant (48% associate of the Group)

Sales to Kunming plant (31.5% associate of the Group before June 2006)

External sales * Turnover for Kunming, Beijing and Qingdao plants were

semi-annualised in June 2006 for comparative purpose** Excludes sales to Kunming plant

Gross margin

16

32 3027

42

0

10

20

30

40

50

FY 2005 1H 2006 FY 2006 1H 2007

%

Gross Margin

Change of product

mix

Focus on high volume

together with high margin product

To become No.1 printer

in China

To remain No.1 most profitable in China

Product mix – first half 2007

To become the No.1 in the tobacco packaging printing specialist,AMVIG will focus on different types of product to increase the market

share and remain the most profitable in the industry

17

Gross Profit Margin (%)

21%28%

38%

0

10

20

30

40

50

Mid - Low End Mid End High End

Sales Mix

17%

30%

53%

Mid - High End Mid End Mid - Low End

Turnover by locations

1H 2007

25%

46%

25%

4%

1H 2006

48%

13%

35%

4%

Shenzhen Kunming Qingdao Beijing

Turnover HK$ 404 million Turnover HK$ 891 million

Utilisation of plants

• Kunming and Qingdao plants are at full capacity, and have expansion plans• Nanjing and Beijing plants will continue to increase the utilisation rates • Shenzhen plant will improve utilisation going forward

19

100 100

8070

50

100 100

85 90

50

0102030405060708090

100

Kunming Qingdao Nanjing Beijing Shenzhen

%

2006 1H 2007

Strategy• Remain a focused tobacco packaging specialist • Grow aggressively through organic projects and bolt on acquisitions

– By 2011 target sales of HK$ 6 billion – Dongguan plant is on track to commence production in the next couple of months

• Leverage economy of scale– Integration and cost reduction

• Centralised procurement• Sharing of resources• Benchmarking

• Develop relationship with CNTC– Requires demonstrating AMVIG is clearly the best manufacturer in China

20

AMVIG Disclaimer• This presentation contains forward-looking statements that involve subjective

judgment and analysis and are subject to significant uncertainties, risks and contingencies, many of which are outside the control of, and are unknown to, AMVIG. Forward-looking statements can generally be identified by the use of forward-looking words such as “may”, “will”, “expect”, “intend”, “plan”, “seeks”, “estimate”, “anticipate”, “believe”, “continue”, or similar words.

• No representation, warranty or assurance (express or implied) is given or made in relation to any forward-looking statement by any person (including AMVIG). In addition, no representation, warranty or assurance (express or implied) is given in relation to any underlying assumption or that any forward-looking statements will be achieved. Actual future events may vary materially from the forward-looking statements and the assumptions on which the forward-looking statements are based. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

21

AMVIG Disclaimer (cont)• In particular, we caution you that these forward-looking statements are subject to

uncertainties, risks and changes that may cause its actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. The factors that may affect AMVIG’s future performance include, among others:

– changes in the legal and regulatory regimes in which AMVIG operates;– changes in behaviour of AMVIG’s major customers;– changes in behaviour of AMVIG’s major competitors;– the impact of foreign currency exchange rates; and– general changes in the economic conditions of the major markets in which AMVIG

operates.• These forward-looking statements speak only as of the date of this presentation. Subject to

any continuing obligations under applicable law or any relevant stock exchange listing rules, AMVIG disclaims any obligation or undertaking to publicly update or revise any of the forward looking statements in this presentation, whether as a result of new information, or any change in events, conditions or circumstances on which any such statement is based.

22

Ken MacKenzie

11 December 2007Summary

Key messages summary

Value Plus– Customer Focused culture– Value vs Volume

• Food Flexibles– Flex 1 – Accelerating growth where the business has strong

value propositions• Tobacco packaging

– Growth in Russia and Eastern Europe– Leading in innovation and ability to manage

complexity

EXECUTION FOCUSStrong market

positionsLow cost

Customer and market

focused

Capital discipline

Key messages summary

• Healthcare– An integrated and innovative global healthcare

business• Sunclipse

– Unique business model– Managing costs through the cycle

• AMVIG– Growth via ongoing consolidation and organic

opportunities

EXECUTION FOCUSStrong market

positionsLow cost

Customer and market

focused

Capital discipline

Summary

• Across all businesses there has been improvement in:

– Customer focus

– Capital discipline

– Talent management

• The Way Forward agenda designed to deliver permanent changes rather than short term fixes

– It is about systematically working through issues and establishing comprehensive change agendas

EXECUTION FOCUSStrong market

positionsLow cost

Customer and market

focused

Capital discipline

Summary

• Two years into The Way Forward agenda:

– Businesses are better positioned

– Balance sheet is strong

– Upside is beginning to be realised in earnings

• This will be increasingly evident in 2007/08 and beyond

• The next phase is to increase the emphasis on the growth agenda

EXECUTION FOCUSStrong market

positionsLow cost

Customer and market

focused

Capital discipline

Ken MacKenzie

11 December 2007Summary