11th annual domestic tax conference - building a … annual accounting for income tax 2016 insights...

TRANSCRIPT

Domestic Tax Conference28 April 2016 | New York City

11th Annual

Accounting for income tax2016 insights and challenge areas

Page 2

Disclaimer

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

This presentation is © 2016 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 3

Today’s presenters

Charlie GenglerPartner, Ernst & Young LLP

John VitalePartner, Ernst & Young LLP

George WongPartner, Ernst & Young LLP

Joan SchumakerPartner, Ernst & Young LLP

Page 4

Agenda

► Developments ► Recent legislative and other developments► Accounting standard updates► FASB project status► Internal control over financial reporting ► PCAOB focus areas ► SEC focus areas

► Tax provision challenges and current issues► Restatement trends and common causes of tax restatements► Other current tax accounting issues

► Tax provision process – best practices

Page 5

Legislative and other developmentsFederal

Legislation enacted in 2015 with effects in 2016 and later years

► On 18 December 2015, President Obama signed into law the Consolidated Appropriations Act, 2016 (the Act) reinstating retroactively certain tax benefits and credits (collectively, tax extenders) that had expired. The Act made a number of the provisions permanent and extended the others for two or five years.

► On 2 November 2015, President Obama signed into law legislation introducing a new audit system and income tax liability rules for certain partnerships. The Bipartisan Budget Act of 2015 repealed the prior audit system and income tax liability rules for certain partnerships. The changes are effective for tax years beginning after 31 December 2017.

Page 6

Legislative and other developmentsState

Significant legislation enacted since 1 January 2016

► Delaware – On 27 January, enacted legislation phasing in a single sales factor apportionment formula by 2020. Asset management companies, telecommunication companies and companies whose principal headquarters are in Delaware may use either a single-sales factor or an equally weighted three-factor apportionment formula. The changes are effective for tax years beginning on or after 1 January 2017.

► Louisiana – On 4 March, enacted exemption from tax 100% (rather than 72%) of dividend income received by corporations from certain banks. Change applies to all exclusions from taxable income claimed on any return filed or any tax year beginning on or after 1 January 2015, regardless of the tax year to which the return relates.

► On 9 March, enacted permanent (rather than temporary) limit on net operating loss (NOL) usage to 72% of taxable income. Effective 1 January 2016. Other changes include:► Require use of NOLs in order of newest to oldest (effective 1 January 2017)

► Require adjustment to state taxable income to add back certain related party interest expenses, intangible expenses and management fees deducted for federal income tax purposes (applies tax years beginning on or after 1 January 2016)

► On 10 March, enacted legislation changing the order in which companies may claim tax credits. Change effective upon enactment.

Page 7

Legislative and other developmentsInternational

Significant legislation enacted since 1 January 2016

► Chile – On 27 January, enacted legislation simplifying the new income tax system enacted under the Tax Reform Law. The enacted legislation includes the following changes:► Election of new regimes, Attribution Regime vs. Semi-integrated Regime► Modification of imputation orders to determine tax treatment on distributions from 1 January

2017► Modification of thin capitalization rules► Modification of foreign tax credits► Substitution tax in lieu of Global Aggregate Tax or Withholding tax ► Limitation of the general anti-avoidance rules to transactions executed after 30 September 2015► Clarification of CFC (Controlled Foreign Corporation) rules► Other reporting obligations

Page 8

Legislative and other developmentsInternational

Significant legislation enacted since 1 January 2016 ► Israel – On 5 January 2016, Israel enacted legislation reducing the corporate income tax rate to 25%

from 26.5%. In addition, the withholding tax rates on interest, royalties, and capital gains related to corporate investors are reduced to 25%. Changes are retroactively effective to 1 January 2016.

► Japan – On 29 March 2016, Japan enacted legislation reducing its 23.9% corporate income tax rate to 23.4% for tax years beginning on or after 1 April 2016, and to 23.2% for tax years beginning on or after 1 April 2018. Other changes include:► Reducing the limit on NOL usage to 60% (from 65%) of taxable income for tax years beginning

on or after 1 April 2016, 55% of taxable income for tax years beginning on or after 1 April 2017, and 50% of taxable income for tax years beginning on or after 1 April 2018

► Reducing the local enterprise tax rate applicable to base income to 3.6% from 6% for tax years beginning on or after 1 April 2016

Page 9

Legislative and other developmentsOECD

► October 2015, Organisation for Economic Co-operation and Development (OECD) issued final reports on all 15 focus areas in Base Erosion and Profit Sharing (BEPS) project. OECD divided recommendations into 4 categories► Minimum standards agreed by the participating countries:

► Harmful tax practices – Action 5, Addressing treaty abuse – Action 6, country-by-country (CbC) reporting –Action 13, More effective dispute resolution – Action 14

► Reinforced international standards:► Transfer Pricing Guidelines, Actions 8-10 on transfer pricing, Action 13 on transfer pricing documentation► OECD Model Tax Convention, including Action 2 on hybrids, Action 7 on permanent establishment status

► Common standards and best practices:► Hybrids – Action 2, Controlled foreign company (CFC) rules – Actions 3, Interest limitations – Action 4,

Disclosure of aggressive tax planning – Action 12► Analytical reports

► Digital economy – Action 1► Economic analysis of BEPS – Action 11► Multilateral instrument – Action 15

Page 10

Legislative and other developmentsOECD

► OECD indicated additional technical work will be done in 2016 and beyond on several of focus areas, including digital economy, harmful tax practices, treaty abuse, permanent establishment and transfer pricing.

► BEPS Actions 8-10 entitled “Aligning Transfer Pricing Outcomes with Value Creation” contains revisions to existing OECD Transfer Pricing guidelines; become part of guidelines once formally adopted by OECD council.

► As a non-government organization, OECD actions are not legislative, however, some laws refer directly to OECD guidelines.► Countries that explicitly incorporate the OECD transfer pricing guidelines (e.g., Hungary, Mexico, Norway)

► Countries that need to act to incorporate the OECD transfer pricing guidelines (e.g., UK, Ireland, Australia)

Page 11

Legislative and other developmentsOECD

► Ongoing activity – In addition to the follow-up technical work, the OECDcontinues to work on the following: ► Development of multilateral instrument

► Mechanism to amend bilateral tax treaties to incorporate the treaty-based BEPS recommendations

► Will include mandatory binding arbitration as an optional provision► Negotiations are underway and are to be completed by the end of 2016 so that the

instrument is ready for signature in 2017

► Peer review processes► Work to establish a peer review process to monitor countries' performance in resolving

disputes under treaty mutual agreement procedures (MAP) are reportedly "well advanced" ► Work will continue on identifying and addressing harmful tax practices in OECD and G20

countries and beyond

Page 12

Legislative and other developmentsEuropean Commission

► European Union – On 28 January 2016, the European Commission released an anti-tax avoidance package designed to provide uniform implementation of BEPS measures and minimum standards across Member States. The package includes:► A proposed European Union (EU) anti-tax avoidance directive that addresses interest

deductibility, a general anti-abuse rule, controlled foreign company rules, and a framework to take hybrid mismatches

► A proposed directive that requires Member States to implement the exchange of Country-by-Country (CbC) reporting in relation to multinational enterprises for fiscal years beginning on or after 1 January 2016

► A communication proposing a framework for a new EU external strategy for effective taxation ► A recommendation on the implementation of measures against tax treaty abuse

Page 13

Legislative and other developmentsEuropean Commission

► On 12 April 2016, the European Commission (EC) published a draft directive on CbCreporting. If adopted, this would: ► amend existing EU law on disclosure of income tax information.► require certain large multinational companies to disclose publicly on the company’s

website, and on an official register in the EU, specific information including a breakdown of profits, revenues, taxes and employees.

► This initiative is separate from the OECD BEPS action on CbC reporting, and is also different from the CbC reporting that was proposed as part of the anti-tax avoidance package.

► This latest EC proposal may be adopted with the support of only a qualified majority rather than unanimous consent.► After adoption, all EU member states would have to enact conforming legislation in

order to implement into local law.

Page 14

Legislative and other developmentsAltera US Federal share-based compensation case

► On 27 July 2015, US Tax Court ruled in favor of the taxpayer in Altera v. Comm’r, 145 T.C. No. 3 (2015).

► Court held the 2003 revision of cost-sharing regulations (T.D. 9088), to include Stock-Based Compensation (SBC) in shared costs was a legislative regulation subject to the Administrative Procedures Act’s (APA) requirement for a Notice and Comment Period. Decision has potentially broad implications for IRS regulatory procedures.

► Court specifically ruled the IRS failed to address the extensive evidence received that unrelated parties in joint ventures do not share SBC costs. Consequently, rule “epitomizes arbitrary and capricious decision making.”

► Treas. Reg. section 1.482-7(d)(2) rule that SBCs be included in the pool of intangible development costs (IDCs) for qualified cost sharing arrangements (QCSAs) was held to be invalid.

► In February 2016, IRS filed notice of appeal in Ninth Circuit Court of Appeals.► The Tax Court’s holding does not eliminate the regulation.

Page 15

Legislative and other developmentsState aid: European Commission actions and developments

2013 2014 2015 2016

June 2013: European Commission requested Information on IP-regimes from ten Member States (Belgium, Cyprus, France, Hungary, Luxembourg, Malta, the Netherlands, Portugal, Spain, and United Kingdom)

June 2013: Information on the tax ruling practices in seven countries requested (i.e., Cyprus, Gibraltar, Malta, the United Kingdom, The Netherlands, Ireland and Luxembourg)

October 2013: European Commission opens investigation into Gibraltar’s corporate tax system

11 June 2014: The European Commission opened three in-depth investigations to examine decisions of the tax authorities in Ireland, the Netherlands and Luxembourg with regard to tax paid by two US and one Italian multinational corporations (MNC)

1 October 2014: The European Commission extended the scope of its investigation in the Gibraltar corporate tax system to include the Gibraltar tax ruling practice

7 October 2014: The European Commission opened another in-depth investigation to examine a decision of the Luxembourg tax authority with regard to tax paid by a US MNC

15 October 2014: The European Commission ordered Spain to recover aid granted through amended application of tax scheme for acquisition of indirect shareholdings in foreign companies

17 December 2014: The European Commission extended the information enquiry on tax ruling practice to all Member States

3 February 2015: The European Commission opened an in-depth investigation into the Belgian excess profit ruling system

21 October 2015: The European Commission issued a press release announcing that it has decided that the selective tax advantages granted to an MNC in Luxembourg and an MNC in the Netherlands are illegal under EU state aid rules

November/December 2015: Netherlands and Luxembourg appealed the Commission’s decision

3 December 2015: The European Commission opened an in-depth investigation to examine a decision of Luxembourg's tax authority with regard to tax treatment of a US MNC

11 January 2016 The European Commission concluded that the Belgian excess profit scheme is illegal

Page 16

Legislative and other developmentsState aid

► State aid is defined as: “The selective granting of an advantage/award to a specific undertaking or specific undertakings which is capable to distort trade between EU Member States.”► Considered incompatible with EU’s common market because it distorts competition

► On 21 October 2015, EC releases that selective tax advantages for Fiat in Luxembourg and Starbucks in Netherlands are illegal state aid.

► On 11 January 2016, EC announces its decision that Belgium’s excess profit tax regime is illegal under EU state aid rules.► EC held that Belgium’s tax rulings granted a selective advantage to multinationals by allowing

their corporate tax base to be reduced by the excess profits that allegedly resulted from being part of a multinational group.

► EC decision is against the Belgian state, however enforcement is against the taxpayer.► EC ordered Belgian government to recover approximately 700m Euros of corporate taxes

from approximately 35 multinational companies.

Page 17

Accounting standard updates

Page 18

Revenue recognition ASU 2014-09

► Revenue recognition accounting standard issued on 28 May 2014► Supersedes virtually all industry and interpretive guidance

► Requires more estimates and judgments than current guidance ► The FASB has issued a one-year deferral of the original effective date of ASU 2014-09

► Standard will be effective for public entities for annual periods beginning after 15 December 2017 (2018 for calendar-year companies)

► Nonpublic entities will still have the option of an additional year (effective for annual periods beginning after 15 December 2018)

► Early adoption will be allowed for both public and nonpublic entities – using original effective dates (2017 for calendar-year companies)

► The deferral was issued in ASU 2015-14 on 13 August 2015► The IASB voted for a one-year deferral as well

Page 19

Revenue recognition standard Effective date

► Dates shown are for calendar year-end entitiesMandatory adoption

PublicNonpublic

Early adoption

Nonpublic

► 1 January 2019

► 1 January 2017

► 1 January 2018

► 31 December 2017 annual F/S

Effective date First presentation► 31 March 2018 10-Q► 31 December 2019 annual F/S

Public ► 1 January 2017 ► 31 March 2017 10-Q► 31 March 2017 interim F/S

► 1 January 2018► 31 December 2018 annual F/S► 31 March 2018 interim F/S

► 1 January 2019 ► 31 March 2019 interim F/S

Page 20

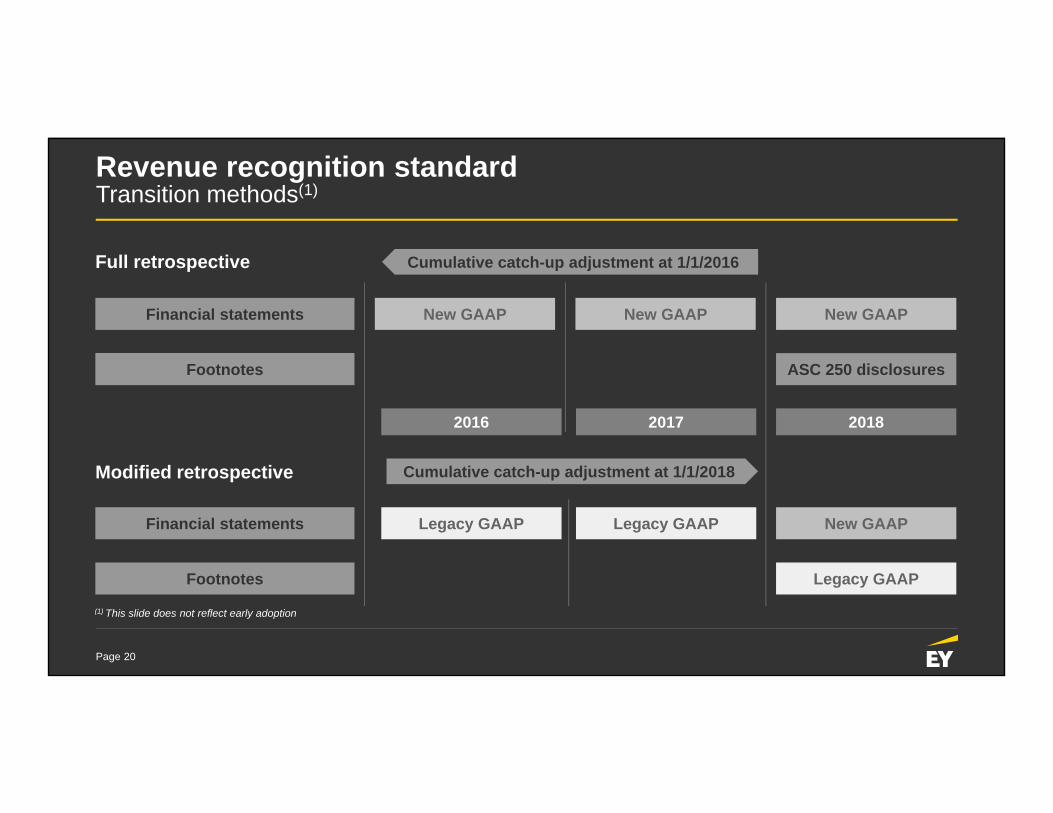

Revenue recognition standardTransition methods(1)

Full retrospective

Modified retrospective

Financial statements

Financial statements

Footnotes

Footnotes

New GAAP New GAAP New GAAP

New GAAPLegacy GAAP Legacy GAAP

Legacy GAAP

ASC 250 disclosures

Cumulative catch-up adjustment at 1/1/2016

20182016 2017

Cumulative catch-up adjustment at 1/1/2018

(1) This slide does not reflect early adoption

Page 21

TransitionFull retrospective

► Apply new revenue recognition standard to all existing contracts as of 1 January 2016 (for calendar year-end entities who do not adopt early)► Need to inventory contracts with performance remaining as of 1 January 2016

► Will have to keep two sets of books for FY 2016 and FY 2017 if the standard creates differences ► Cumulative catch-up adjustment as of 1 January 2016 for contracts with performance remaining

under current guidance► Practical expedients

► Need not restate contracts completed before adoption that begin and end within the same annual reporting period

► Need not estimate variable consideration for contracts completed before adoption (i.e., use known consideration as of contract completion)

► Need not disclose the amount of the transaction price allocated to remaining performance obligations for prior periods presented

► Disclose which expedients used and a qualitative assessment of their effects

Page 22

TransitionModified retrospective

► Apply new revenue recognition standard to all existing contracts as of1 January 2018 (for entities who do not adopt early)► Need to inventory contracts with performance remaining as of 1 January 2018

► Cumulative catch-up adjustment as of 1 January 2018 for contracts with performance remaining under current guidance

► Present comparative periods (2016 and 2017 for calendar year-end entities) under current revenue guidance

► Required to report in the year of adoption (2018 for calendar year entities) under both the new standard (on the face of the financial statements) and under current guidance (disclosure), requiring two sets of books► Disclose the amount by which each financial statement line item is affected compared with

current accounting► Explain significant changes

Page 23

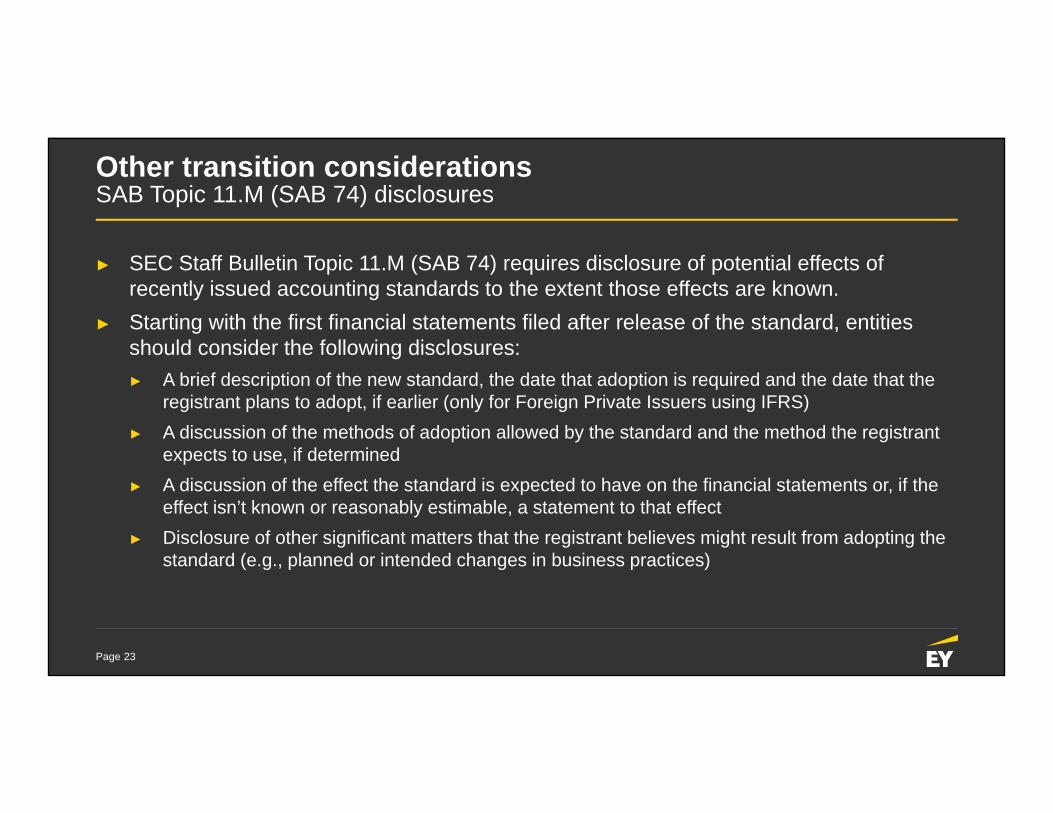

Other transition considerationsSAB Topic 11.M (SAB 74) disclosures

► SEC Staff Bulletin Topic 11.M (SAB 74) requires disclosure of potential effects of recently issued accounting standards to the extent those effects are known.

► Starting with the first financial statements filed after release of the standard, entities should consider the following disclosures:► A brief description of the new standard, the date that adoption is required and the date that the

registrant plans to adopt, if earlier (only for Foreign Private Issuers using IFRS)► A discussion of the methods of adoption allowed by the standard and the method the registrant

expects to use, if determined► A discussion of the effect the standard is expected to have on the financial statements or, if the

effect isn’t known or reasonably estimable, a statement to that effect► Disclosure of other significant matters that the registrant believes might result from adopting the

standard (e.g., planned or intended changes in business practices)

Page 24

Revenue recognition standardTax technical considerations

► Taxpayers will need to determine when and how any change in revenue recognition for financial reporting purposes is recognized for tax purposes.► For taxpayers applying a deferral method for advance payments, the amounts deferred for tax purposes are determined

by reference to the amounts deferred for financial statement purposes.

► Consider whether a change in revenue recognition for financial statement purposes is also a permissible method for tax purposes.

► In certain jurisdictions, local tax liability is based upon statutory financial statements.

► When local statutory financial statements are prepared under IFRS, the statutory financial statements may change with adoption of the standard

► Evaluate whether a foreign subsidiary’s earnings and profits (E&P) or local tax change the amount by which a distribution is taxable as a dividend, the amount of Subpart F inclusion, or deemed paid foreign tax credits.

► Evaluate intercompany prices and transfer pricing policies where adoption changes revenue, profits or third-party comparables used in determining transfer pricing.

► Companies may need to review the methodology for compiling sales apportionment data.

Page 25

Revenue recognition standardIncome tax accounting considerations

► New temporary differences may arise or existing temporary differences may be computed differently► Companies may need to revise their processes and data collection tools

► Valuation allowance considerations may change► Change in deferred tax assets, temporary difference reversals or expected future taxable income may affect judgments

regarding the realizability of deferred tax assets

► Multinational companies will need to consider the effects of changes in revenue recognition for financial reporting purposes at foreign subsidiaries► Jurisdiction-by-jurisdiction analysis necessary to assess whether the change in revenue recognition for financial reporting

results in temporary differences due to differences in timing and amount of revenue recognized for financial reporting and tax purposes

► Current and deferred tax consequences of the cumulative effect adjustment reported in the period of adoption► Requires careful consideration of the income tax accounting effect of individual items included in the cumulative effect

adjustment

► A change in an accounting method for tax purposes requires careful consideration of the period the change in method is considered for financial reporting purposes

Page 26

Classification of deferred taxesASU 2015-17

► FASB issued ASU 2015-17, Balance Sheet Classification of Deferred Taxes, that requires the classification of all deferred tax assets and liabilities as noncurrent ► No longer allocate valuation allowances between current and noncurrent ► No change to jurisdictional offsetting requirements► For public business entities, standard effective for annual periods, and interim periods within

those annual periods, beginning after 15 December 2016► For nonpublic business entities, standard effective for annual periods beginning after 15

December 2017 and interim periods in annual periods beginning after 15 December 2018► Early adoption permitted for all entities in any interim or annual period► Entities may elect either a prospective or retrospective transition approach

Page 27

Financial instruments: Classification and measurementASU 2016-01

► FASB issued ASU 2016-01, Recognition and Measurement of Financial Assets and Financial Liabilities

► Measure many equity investments at fair value and recognize changes in fair value in net income unless the investments qualify for practicability exception

► Assess the realizability of a deferred tax asset (DTA) related to an available-for-sale (AFS) debt security in combination with other DTAs ► Use the same four sources of taxable income that are used for other DTAs► Include the expected reversal of unrealized losses on AFS debt securities that an entity has both

the intent and ability to hold until recovery as a component of its overall projection of future taxable income

► May not be able to rely on projections of future taxable income for purposes of evaluating realizability of DTAs if significant negative evidence exists (e.g., cumulative losses in recent years)

Page 28

Financial instruments: Classification and measurement ASU 2016-01

► No longer separately evaluate the DTAs related to AFS debt securities ► Can not solely rely on intent and ability to hold debt securities with unrealized losses until

recovery, which may not be until maturity, akin to a tax planning strategy

► For public business entities, standard effective for annual periods, and interim periods within those annual periods, beginning after 15 December 2017

► For nonpublic business entities, standard effective for annual periods beginning after 15 December 2018 and interim periods in annual periods beginning after 15 December 2019► Can early adopt as of effective date for public business entities

► Early adoption permitted for certain provisions (does not include income tax provision)► Generally apply modified retrospective approach

Page 29

LeasesASU 2016-02

► The IASB issued IFRS 16 Leases in January 2016.► The FASB issued ASU 2016-02, Leases, in February 2016.

► Effective date – 1 January 2019 for calendar-year public business entities with early adoption permitted

► Key changes to today’s US GAAP guidance include:► Lessees would recognize assets and liabilities for most leases.► For lessors, the guidance would modify today’s classification criteria and accounting for sales-

type and direct financing leases.► Leases would be classified using criteria similar to current US GAAP without the bright lines.

► Classification would determine how entities recognize lease-related revenue and expense, and would continue to affect what lessors record on the balance sheet.

► New presentation and disclosure requirements

Page 30

LeasesASU 2016-02

► Application of the new guidance results in changes to pre-tax book accounting:► Lessees

► Likely recognize new lease-related assets and liabilities on the balance sheet and may change measurement of other lease-related assets and liabilities

► Lessors► May see a change in the recognition and measurement of lease-related assets and/or derecognition of

underlying assets for certain leases► Timing of recognition of lease income may change for some leases► Special accounting for leveraged leases is eliminated

► These changes affect certain aspects of accounting for income taxes such as:► Recognition and measurement of DTAs and deferred tax liabilities (DTLs)► Assessment of the recoverability of DTAs (i.e., the need for and measurement of a

valuation allowance)

Page 31

Stock compensationASU 2016-09

► ASU 2016-09, Improvements to Employee Share-Based Payment Accounting, issued in March 2016► Excess tax benefits and tax deficiencies recognized in the income statement (prospective transition)

► Account for excess tax benefits and tax deficiencies as discrete items in the interim period in which they occur

► Eliminates the requirement that excess tax benefits not be recognized until they are realized (modified retrospective transition with a cumulative catch-up adjustment to retained earnings)

► Excess tax benefits presented as an operating activity in the statement of cash flows (prospective or retrospective transition)

► For public business entities, effective for annual periods, and interim periods within those annual periods, beginning after 15 December 2016

► For nonpublic business entities, effective for annual periods beginning after 15 December 2017 and interim periods in annual periods beginning after 15 December 2018

► Early adoption is permitted for all entities in any interim or annual period for which financial statements have not been issued

Page 32

IFRS developmentsIAS 12 amendments – recognition of DTAs for unrealized losses

► IAS 12 amended for years beginning on/after 1 January 2017, early adoption permitted ► Decreases below cost in the carrying amount of a fixed-rate debt instrument measured at fair value

for which the tax base remains at cost give rise to a deductible temporary difference irrespective of whether the debt instrument’s holder expects to recover the carrying amount of the debt instrument by sale or by use, e.g., continuing to hold it to maturity

► Determining temporary differences and estimating probable future taxable profit against which deductible temporary differences are assessed for utilization are two separate steps and the carrying amount of an asset is relevant only to determining temporary differences

► The carrying amount of an asset does not limit the estimation of probable future taxable profit► Future taxable profit includes the probable inflow of taxable economic benefits that results from

recovering an asset, and that may exceed the carrying amount of the asset► Must consider whether tax law restricts the sources of taxable profits against which it may make

deductions on the reversal of that deductible temporary difference, e.g., capital loss limitations

Page 33

FASB project status

Page 34

FASB income taxes simplification project Intercompany scope exception

► Proposal would eliminate exception that requires deferral of the income tax effects of intercompany sales/transfers of assets ► Would recognize income tax expense in the period of the sale/transfer

► Would recognize deferred tax effects of the difference between the tax basis of the asset in the buyer’s jurisdiction and its book basis after elimination of the intercompany profit

► For public business entities, FASB expects proposed amendments effective for annual periods, and interim periods within those annual periods, beginning after 15 December 2016

► For nonpublic business entities, FASB expects proposed amendments effective for annual periods beginning after 15 December 2017 and interim periods in annual periods beginning after 15 December 2018► Early adoption permitted, but not before the effective date for public business entities

► Modified retrospective transition approach

► In October 2015, FASB asked its staff to research the costs and benefits of deferring the income tax effects only for intercompany inventory transactions

Page 35

FASB income taxes disclosure projectInitial deliberations – foreign earnings

► FASB tentatively decided to require additional disclosures as follows: ► Pre-tax income (loss) disaggregated between domestic and foreign earnings► Income tax expense (benefit) disaggregated between domestic and foreign► Income taxes paid disaggregated between domestic and foreign► Foreign income taxes paid to any country that are significant relative to total income

taxes paid ► The amount of and explanation for a change in assertion about the temporary

difference for the cumulative amount of investments associated with undistributed earnings that are (1) asserted to be essentially permanent in duration, or (2) no longer asserted to be essentially permanent in duration

► Foreign earnings that are indefinitely reinvested for any country that represents at least 10% of the entity’s total foreign earnings that are indefinitely reinvested

Page 36

FASB income taxes disclosure projectInitial deliberations – uncertain tax positions

► FASB tentatively decided to add requirements that public entities disclose as part of the tabular rollforward of unrecognized tax benefits the following: ► Settlements disaggregated between those that are cash and noncash (e.g., an

existing net operating loss carryforward used to settle with the taxing authority)► A breakdown of the total amount of unrecognized tax benefits by the balance sheet

line item in which the amounts are presented

► FASB also tentatively decided to eliminate for all entities the requirement to disclose certain information when it is reasonably possible that the total amounts of unrecognized tax benefits will significantly increase or decrease within 12 months of the reporting date

Page 37

FASB income taxes disclosure projectInitial deliberations – other disclosures

► The FASB also made tentative decisions for other income tax disclosures that would require entities to disclose: ► Information about an enacted change in tax law if it is probable that the change will

affect the entity in a future period

Page 38

FASB income taxes disclosure projectInitial deliberations – other disclosures

► FASB also made tentative decisions for other income tax disclosures that would require public entities to disclose: ► Income tax rate reconciliations

► Individual reconciling items of more than 5% of amount of pretax income times applicable federal statutory income tax rate

► A qualitative description of items that have caused a significant change in the rate

► An explanation of the nature and amounts of valuation allowances recorded and released during the reporting period

► The amounts and expiration dates of tax carryforwards recorded on the tax return (not tax effected) and in the financial statements (tax effected) and the total amount of unrecognized tax benefits that offsets carryforwards.

Page 39

FASB income taxes disclosure projectInitial deliberations – transition and next steps

► FASB tentatively decided to require prospective transition for all income tax disclosures

► FASB asked its staff to perform outreach on the operability of requiring companies to disclose cash and cash equivalents, marketable securities and loans underlying undistributed earnings that are indefinitely reinvested

► After the outreach is complete, FASB plans to issue an exposure draft on the proposal

Page 40

FASB government assistance disclosure project – proposal

► FASB proposal would require for-profit entities to make certain disclosures about assistance they receive from legally enforceable agreements with governments: ► The nature of the assistance, including a general description of the significant

categories and the form in which the assistance has been received ► The accounting policy used to account for the government assistance ► The line items on the balance sheet and income statement that are affected by

government assistance and the amounts ► The amounts of government assistance received that are not directly recorded in the

financial statements (e.g., loan guarantees, loans with below-market rates, tax abatements) unless impracticable to do so

Page 41

FASB government assistance disclosure project – proposal

► The disclosure requirements would apply to certain arrangements accounted for under the income tax guidance in addition to grants, loan guarantees and other types of government assistance.

► The guidance would be applied prospectively to all agreements existing at the effective date and those entered into after the effective date.

► Entities would be permitted to apply the guidance retrospectively. ► FASB is currently redeliberating the proposal based upon feedback received

during the comment period.

Page 42

Internal control over financial reporting (ICFR)

Page 43

ICFR – focus areas

Complete understanding of the process and therelated controls

Completeness and accuracy of data used in the performance of controls

Evidence of control operation, particularly for management review controls

Page 44

Management review controls

► The objectives of management review controls typically involvedetermining whether:► Accounting is appropriate.► There are potential errors or misstatements. ► Information is complete and accurate. ► Other controls were performed timely and effectively.

► Detect and correct controls – may be manual or dependent on IT ► Performed by an individual(s) with appropriate competence and authority► Management review controls are very common in income tax processes.

Review of the incometax provision

Review of uncertaintax positions

Review of realizability of deferred tax assets

Page 45

Management review controls

► When designing review controls, management should consider:► Risk of material misstatement (i.e., importance of the control)► Verification of the completeness, accuracy and integrity of data and reports used► Precision of the control

► Criteria used by the reviewer to identify matters for investigation► How items identified for investigation are resolved

► Review control documentation► Evidence of control operation► Policies and procedures – design of the review control

Page 46

Management review controls

► Control evidence can include:

► PCAOB Std five – auditor testing of design and operating effectiveness of a control includes a mix of: ► Inquiry of appropriate personnel (inquiry alone does not provide

sufficient evidence)► Observation of the company’s operations► Inspection of relevant documentation► Re-performance of the control

Meetings(participation/observation)

Draft documents or documents with tickmarks,

notes, questions

Emails

Calculation reiterations

Page 47

AICPA national conference – December 2015SEC staff remarks on ICFR

► Commission’s management guidance for ICFR is aligned with PCAOB AS No. 5

► PCAOB’s ICFR findings may reflect not only inadequate audit execution but also deficiencies in management’s controls and management’s assessments

► Discussed the level of evidence that management is required to retain to support the effectiveness of controls (including management review controls)

Page 48

PCAOB focus areas

Page 49

PCAOB 7 May 2015 audit committee dialogue

► Identified deficiencies related to: Auditing estimates (including tax-related estimates) – auditing the estimate and related internal controls

► Identified emerging risk area: Auditing of management’s indefinite reinvestment assertion and the related internal controls

Questions to consider: How is understanding of critical assumptions and methods obtained?

What is the nature of evidence gathered regarding management’s assertions?

How is contrary evidence evaluated? Are indefinite reinvestment assertions consistent with other disclosures (e.g., MD&A)?

Page 50

AICPA national conference – December 2015PCAOB remarks related to tax

► PCAOB staff stated that inspections will likely focus on the following areas of emerging risks in 2016 that pertain to tax:► Risks associated with mergers and acquisitions► Income taxes, specifically matters related to a company’s assertions related to

undistributed cash held in overseas subsidiaries► Cybersecurity risks

Page 51

SEC focus areas

Page 52

AICPA national conference – December 2015SEC staff remarks on income tax

► Focus on quality and clarity of management discussion and analysis (MD&A) disclosures, including those related to income tax rate reconciliations, valuation allowances and earnings that have not been repatriated

► Enhance disclosures in MD&A when:► Income tax expense is material to financial statements – both recorded expense and

expense based on statutory tax rate► There are material fluctuations or lack of fluctuations that were expected in the

effective tax rate (ETR)► There are risks and uncertainties

► Provide transparent disclosure in MD&A of significant foreign earnings, including earnings and tax rates within specific jurisdictions and jurisdictions’ effects on the ETR

Page 53

AICPA national conference – December 2015SEC staff remarks on reinvestment of foreign earnings

► SEC staff has asked registrants to explain how they have overcome the presumption and to provide evidence of specific plans for reinvestment of foreign earnings (e.g., past experience, working capital forecasts, long-term liquidity plans, capital improvement programs, merger and acquisition plans, investment plans).

► SEC staff also requests similar evidence when registrants assert that they intend to indefinitely reinvest only a portion of undistributed foreign earnings or when undistributed foreign earnings are considered to be indefinitely reinvested, but there is a recent history of repatriation.

► Staff indicated that when there is a change in assertion, registrants should disclose the facts and circumstances that led to it during the reporting period.

Page 54

AICPA national conference – December 2015SEC staff remarks on liquidity and reinvested foreign earnings

► Example SEC staff comment► If significant to an understanding of your liquidity, in future filings please clarify the

amount of cash and investments held outside of the US. Additionally, to the extent material, please describe any significant amounts that may not be available for general corporate use related to cash and investments held by foreign subsidiaries where you consider earnings to be indefinitely invested. Also, address the potential tax implications of repatriation.

Page 55

SEC comment focus

Comment area 2015 Ranking 2014 Ranking

2014 and 2015 % of total registrants that received

comment letters

Management’s discussion and analysis 1 1 44%

Fair value measurements 2 2 21%

Revenue recognition 3 5 16%

Non-GAAP financial measures 4 6 15%

Signatures, exhibits and agreements 5 3 16%

Income taxes 6 4 14%

Segment reporting 7 9 12%

Intangible assets and goodwill 8 7 12%

Acquisitions and business combinations 9 10 11%

Executive compensation disclosures 10 8 12%

Page 56

Tax provision challenges and current issues

Page 57

Deferred tax accounting

44%

Acquisitions/dispositions

16%

Valuationallowance

11%

Other 16%

Stock-basedcompensation

8%

Classificationerrors

5%

Tax restatements increased past three years Common errors

► Generally, three most common causes of restatements are:

► Deferred tax accounting

► Accounting for acquisitions/dispositions (specifically purchase accounting and goodwill impairment calculations)

► Valuation allowance adjustments

► During 2015, issues relating to stock-based compensation arose more frequently

► Improper classification of current and non-current deferred tax assets also commonly cited

► “Other” errors often cited:

► Errors relating to intercompany activities

► Treatment of federal and state carryforwards

► Foreign taxes (foreign tax credits, currency translation adjustments)

► Capitalization/depreciation/amortization of tangible and intangible assets purposes

► Pension plan accounting (foreign and domestic)

Page 58

Material weaknessesCauses

► Primary causes fall in three general areas:

► People

► Processes and controls

► Accounting errors (valuation allowances, NOLs, pensions state taxes, leases, impairment mentioned in 2015)

► People issues are typically described as:

► Personnel with insufficient technical knowledge, experience, training in tax accounting

► Lack of investment, resources and focus in tax reporting

► Process and control issues include:

► Lack of adequate policies and procedures to ensure the completeness, accuracy, preparation and review of the income tax provision

► Lack of documentation

► Lack of timely reconciliation of tax accounts

► Inadequate monitoring of significant transactions and new reporting requirements

► Financial close and work compressions

► Improper segregation of duties

Improper treatment40%

Segregation of duties 6%

People 31%

Documentation6%

Review procedures17%

Page 59

Appropriate application of tax basis

► Essential starting point: Maintaining a detailed and accurate record of the tax basis of all assets and liabilities, including those without a book basis ► A fluctuation analysis of tax basis supporting the deferred tax balances may not

provide sufficient audit evidence

► Common pitfall: Not properly identifying a tax basis or attribute or not appropriately recording and tracking the tax basis or attribute insubsequent periods► Requires technical understanding of tax law

► Often for multiple taxing jurisdictions ► May be simple or complex

How is the tax basis evaluated?

Page 60

Intraperiod allocation

► Be mindful of the complexity of the intraperiod allocation rules► Common pitfalls:

► Failure to apply the exception (losses from continuing operations and income fromother sources)

► Failure to consider interaction of exception with the interim reporting rules► Inappropriate “backwards tracing”► Failure to follow two-step process when income from discontinued operations is

recognized in an interim period and losses from continuing operations are expected for the year

Are there losses from continuing operations and income from another source? Does the financial reporting reflect the exception to the intraperiod allocation rules?

Page 61

Intraperiod allocation

► Exceptions to the general rule apply in all situations where there is: ► A loss from continuing operations ► Cumulative income from all other sources

► Exception also applies to interim periods when company anticipates an ordinary loss from continuing operations for the year

► Applicable even to periods of a full valuation allowance► Does not change overall annual tax provision (benefit) ► However, may change tax provision (benefit) between interim periods

The result of this computation (as well as the need to do the computation)is often counterintuitive.

Page 62

Accounting for outside basis differences

► Outside basis differences may not be recognized if certain exceptionsare applicable► Section 14.1.2 of Income taxes FRD (Financial Reporting Developments),

Exceptions to deferred tax accounting for outside basis differences: Summary of application of exceptions and common entity types

► Common pitfalls: ► Not providing taxes for outside basis difference related to investments in

partnerships or equity method investments► No longer qualifying for exception with changes in investment ownership

Are the exceptions to outside basis differences appropriately applied?

Page 63

Realizability of deferred tax assets (DTAs)

► Same framework► Establishing a valuation allowance for the first time► Determining whether a valuation allowance continues to be necessary

► Have all four sources of taxable income been considered?► Is there taxable income in carryback periods of the appropriate character?► Are tax planning strategies considered appropriately?

Page 64

Realizability of DTAs

► Future reversals of existing taxable temporary differences► Evaluate DTAs on a gross basis ► Consider the timing of reversal of existing taxable temporary differences ► Common pitfall: DTAs evaluated on a net basis► Common pitfall: Naked credits are used as a source of taxable income

Will the deferred tax liabilities result in taxable income in the appropriate period?Are there deferred tax liabilities associated with book balances that do not have a

known period when they may affect the income statement?

Page 65

Tax provision process – best practices

Page 66

Tax provision process – best practices

► Prepare tax basis balance sheets to prove cumulative deferred taxes by entity► Prepare technical tax accounting white papers for issues and transactions► Analyze state (including apportionment changes) and foreign tax rates

for changes► Document outside basis differences, including indefinite reinvestment

assertions and prepare outside basis difference calculations (consider previously taxed income and unrecaptured Subpart F income)

► Document valuation allowance considerations (four sources of taxable income) and prepare position paper

► Consider tool to improve computations related to uncertain tax positions

Page 67

Tax provision process – best practices

► Evaluate intercompany transactions and tax provision effects► Conduct regular meetings with external auditors for significant transactions,

changes in business, etc.► Challenge annually prior-year processes to identify areas for improvement► Build-in controls to reduce risk of Excel templates► Implement standardized global procedures► Refresh internal controls for income taxes

Domestic Tax Conference28 April 2016 | New York City

11th Annual