12 may 2015 les politiques de recherche et d’innovation dans les pays de l’ocde -...

TRANSCRIPT

Les politiques de recherche et d’innovation dans les

pays de l’OCDELes Perspectives de STI de l’OCDE 2014

Sandrine KERGROACHDirection de l’OCDE de la Science, Technologie et Innovation

JOURNEES ANPR - Le paysage de la Recherche et de l’Innovation en Tunisie : Etat des lieux et Perspectives,

Hammamet, 12 Mai 2015

Outline

• OECD STI Outlook: a guide through complexity.

• Global trends in STI

– A modest recovery

– Shifts in global STI landscape

– Persistent ‘Grand’ challenges

• Adjustments in STI policies

– A “new deal” for innovation

– Public support to firms

– Public research policy

• For further information: OECD infrastructure for innovation policy analysis and a few words on international cooperation for building capacity: EC and World Bank.

2

OECD STI Outlook: 20-year tradition

• “What’s new in the field of science, technology and innovation policy? “

• International review of key recent trends in STI for the STI policy community and analysts

• Based on latest STI policy information and indicators

• OECD Flagship publication

3

Drawing on a unique policy questionnaire

4

Country coverage of the STI Outlook

from 2008 to 2014

Response rate 2014: 93%

2012: + Colombia, Egypt2014 : + Costa Rica, Latvia, Lithuania, Malaysia, Peru

European Commission joint survey in 2016

53 countries

The three components of the STI Outlook 2014

5

COUNTRY PROFILES

POLICY PROFILES

OVERALL STI PERFORMANCE AND POLICY TRENDS

Selected trends for STI and national STI policies

6

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistent ‘grand’ challenges

Trend 4 • Adjustments in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

The recovery remains modest and contrasted

7

GDP growthAnnual growth rate, 2003-13 and projections for 2014 and 2015

Source: OECD Economic Outlook n.95 Database, May 2014.

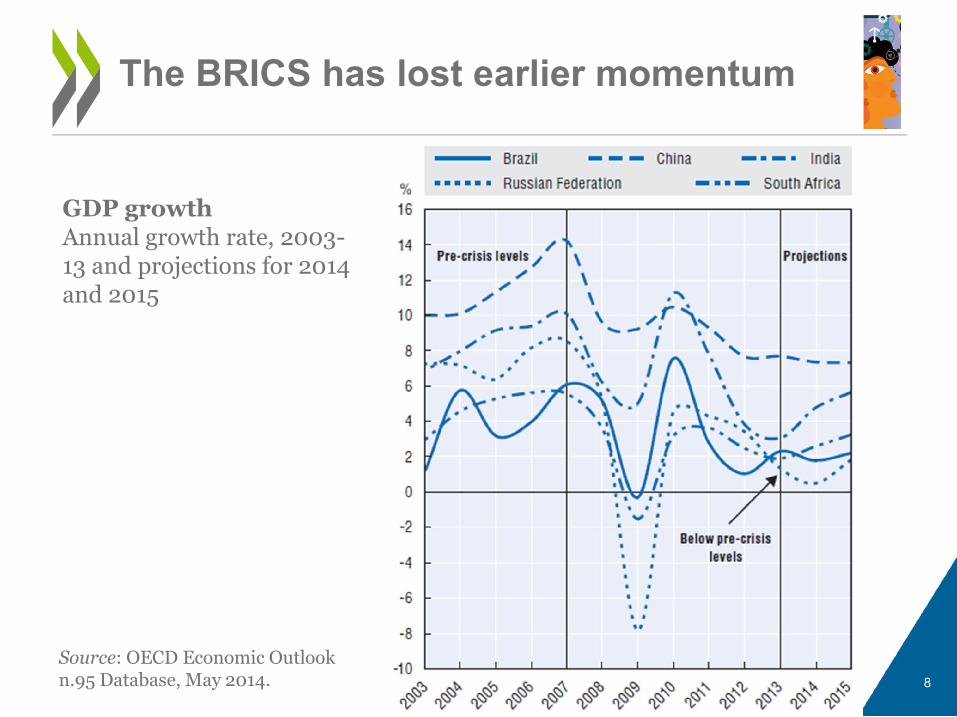

The BRICS has lost earlier momentum

8

GDP growthAnnual growth rate, 2003-13 and projections for 2014 and 2015

Source: OECD Economic Outlook n.95 Database, May 2014.

Innovation in the crisis

9

Annual growth rate of GDP and GERD, OECD, 1993-2013 and projections to 2015

Source: OECD Economic Outlook no95 Database, May 2014; OECD Main Science and Technology Indicators (MSTI) database, June 2014.

The buffer effect of public R&D expenditure has faded

10

Annual growth rate of GDP and GERD, OECD, 1993-2013 and projections to 2015

Source: OECD Economic Outlook no95 Database, May 2014; OECD Main Science and Technology Indicators MSTI database, June 2014.

Knowledge-intensive investments have been relatively preserved

11

Source: OECD MSTI, June 2014, OECD National Accounts Database, April 2014.

recovered earlier than in physical assets

Reluctance of firms to engage profits and build new production capacity

Corporate gross fixed capitalformation

Central role of knowledge-based assets in market competition

12

Labour productivity deteriorated significantly

Source: OECD Productivity Database, May 2014.

Budgets are levelling off or receding…

13

Public R&D budgets (GBAORD), as % of GDP, 2013 compared to 2011

Source: OECD estimates based on OECD MSTI database, June 2014.

The shock of the crisis is not fully absorbed

14

• A strong resurgence in R&D and innovation in the next years is unlikely

• Governments’ financial capacity to intervene in the field of STI is limited due to budgetary pressure

• Future growth in innovation activities is likely to be primarily driven by business investments.

Maintaining jobs and economic growth in open economies requires greater competitiveness (48 million people unemployed in the OECD, the fear of “the middle income trap”)

Selected trends for STI and national STI policies

15

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistent ‘grand’ challenges

Trend 4 • Adjustments in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

Global value chains (GVCs) : trade …

16Economies participate to GVCs both as users of foreign inputs and as suppliers of intermediate goods and services

GVCs: fragmentation of production processes globally, including R&D

17

GVCs have changed the nature of global competition

• Competitive advantage increasingly driven by innovation….

• … in turn driven by investments in intangibles (KBC beyond R&D)

18

Computerised information

• Software• Databases

Innovative property

• Patents• Copyrights• Trademarks• Design

Economic competencies

• Brand equity• Firm-specific

human capital• Business

networks• Organisational

know-how

Reach segments with higher valued added (and job creation) in GVCs

A changing global R&D landscape

19

GERD, million USD 2005 PPP, 2000-12 and projections to 2024

Source: OECD estimates based on OECD MSTI database, June 2014.

R&D intensity, % GDP (2012)

EU28 = 1.97%China = 1.98%

International collaboration networks in science

20

Internationally co-authored documents, 2011 and 1998 (whole counts)

Source: OECD (2013), OECD Science, Technology and Industry Scoreboard 2013, Paris.

Global competition for knowledge-based assets is on the rise

21

• Emergence of globally interconnected innovation hubs

• Growing worldwide competition for / availability of talent and knowledge-based assets and the increasing international mobility of such assets.

• GVCs have changed the nature of global competition: companies and countries no longer only compete for market share in high value-added industries, but also increasingly for high value-added activities within GVCs.

Innovation is more than ever important for strategic positioning in global value chains

Selected trends for STI and national STI policies

22

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistent ‘grand’ challenges

Trend 4 • Adjustments in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

Challenges and opportunities

23

• The transition to a low-carbon economy and the preservation of natural resources would require technological breakthroughs, deployment of existing technologies and new infrastructures, systemic changes (behaviours, governance).

• Ageing would require new technologies/services to assist the elderly remain active and autonomous longer, assist care providers, funding and better coordination between social care and health services.

• Income inequality has increased during the crisis. ICTs offer opportunities to support inclusive innovation. Education and training policies will be essential to avoid exclusion.

Raising the status of innovation in the policy portfolio

Broaden the scope of policy intervention

Global trends in innovation policies

24

Selected trends for STI and national STI policies

25

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistant ‘Grand’ challenges

Trend 4 • Adjustments in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

• Knowledge triangle at the top of policy agenda

• Broaden the scope of policy intervention :

– Multiple goals (industrial transformation, inclusive innovation, grands challenges etc.)

– Going beyond the scope of national innovation policies

• Growing complexity:

– Growing number of STI actors (ministries, agencies, non-state actors) involved in the design and implementation of STI policy

– Multi-level governance

– In search for synergies with the private sector, strategic P/PPs and joint investments.

– Larger portfolio / mix of policy instruments

• Evaluation is key but would require a ‘whole of government’ approach.

26

The future of innovation policies

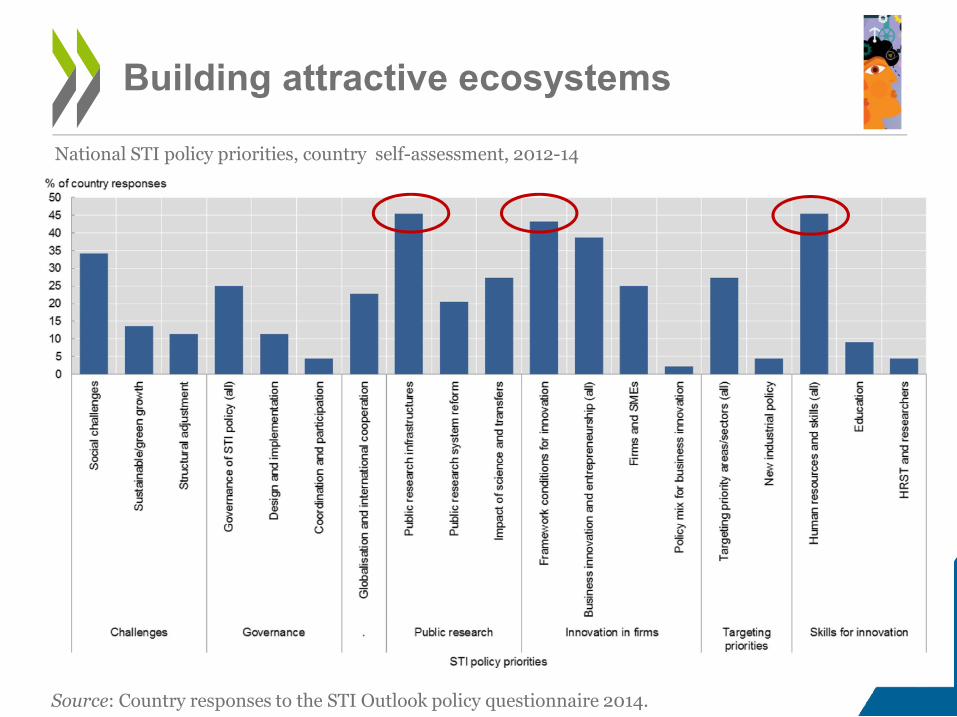

Building attractive ecosystems

27

Source: Country responses to the STI Outlook policy questionnaire 2014.

National STI policy priorities, country self-assessment, 2012-14

Good framework conditions to encourage the reallocation of resources

28

Product market regulations Bankruptcy law Employment protection legislation

AUSAUT

BEL

CAN

CZEDEU

DNK

ESP

FIN

FRA

GBR

GRC

HUN

IRL ITA

JPN

LUX

NLD

POLPRT

SWE

USA

0

0.02

0.04

0.06

0.08

0.1

0.12

0 0.5 1 1.5 2 2.5 3

PMR

KBC Investment to GDP

y = -0.031x + 0.116

T-statistics: -3.92***

AUSAUT

BEL

CAN

CZE

DEU

DNK

ESP

FIN FRA

GBR

GRC

HUN

IRL ITA

JPN

LUX

NLD

POLPRT

SVN

SWE

USA

0

0.02

0.04

0.06

0.08

0.1

0.12

0 5 10 15 20 25

Bankruptcy law

y = -0.002x + 0.086

T-statistics: -3.87***

KBC Investment to GDP

AUS AUT

BEL

CAN

CZE

DEU

DNK

ESP

FIN

FRA

GBR

GRC

HUN

IRL

ITA

JPN

NLD

POLPRT

SWE

USA

0

0.02

0.04

0.06

0.08

0.1

0.12

0 1 2 3 4 5

EPL

y = -0.031x + 0.116

T-statistics: -3.92***

KBC Investment to GDP

Product market regulations Bankruptcy law

Employment protection legislation

• KBC investments to GDP

• The accumulation and optimal use of KBC requires experimentation => effective reallocation of resources + well-functioning debt and equity funding systems

A “new deal” for innovation

29Source: Country responses to the STI Outlook policy questionnaire 2014.

Substantial changes in various STI policy areas , country self-assessment, 2012-14

Selected trends for STI and national STI policies

30

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistant ‘Grand’ challenges

Trend 4 • Mutation in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

Governments have increased financial support to business R&D since 2007

31Source: OECD, MSTI Database, June 2014; OECD data collection on R&D tax incentives, 2013, and country responses to the OECD STI Outlook policy questionnaire 2014.

In most countries, 10% to 20% of business R&D is funded by public money.

As a % of total BERD

Driven by more generous R&D tax incentives -> tax competition?

32Source: OECD, based on OECD R&D tax incentive data collection, 2013; country responses to the OECD STI Outlook policy questionnaire 2014 and OECD MSTI Database, June 2014

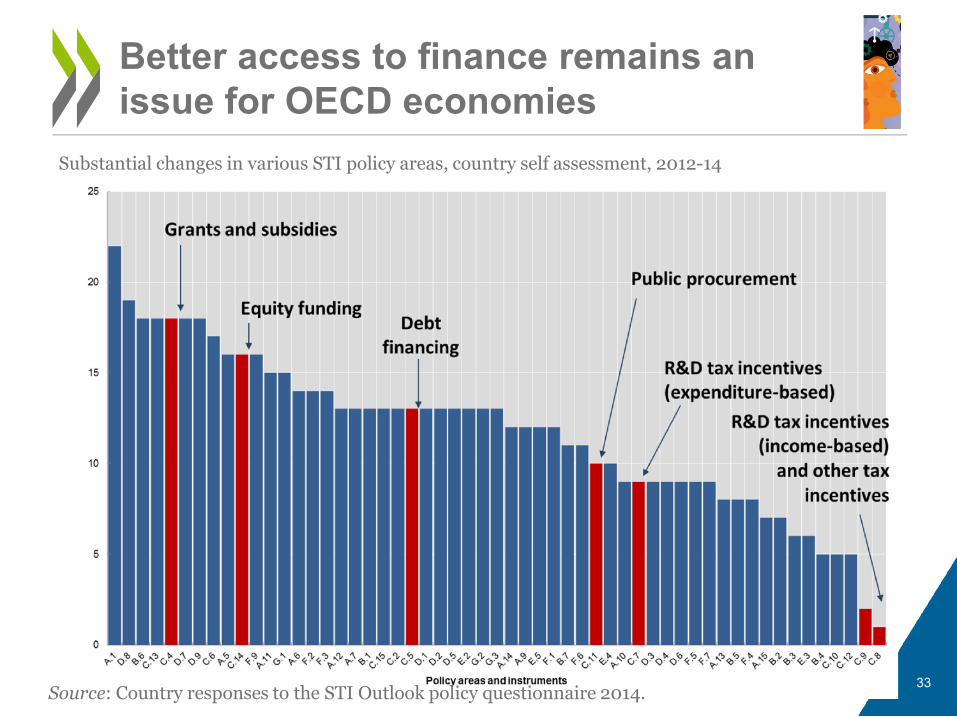

Better access to finance remains an issue for OECD economies

33

Substantial changes in various STI policy areas, country self assessment, 2012-14

Source: Country responses to the STI Outlook policy questionnaire 2014.

More targeted approach in the policy mix for business R&D and innovation

34Source: Country responses to the STI Outlook policy questionnaire 2014.

Changing balance in the policy mix for business R&D and innovation, based on own country ranking, 2014

More SME-targeted tax schemes

35Source: Adapted from OECD (2013), OECD Science, Technology and Industry Scoreboard 2013.

Profit-making scenario Loss-making scenario

Generosity of tax subsidy for R&D expenditures, 1- B-index, 2013

The policy debate on the legitimacy of industrial policy has resurfaced

36

Substantial changes in various STI policy areas , country self assessment, 2012-14

Source: Country responses to the STI Outlook policy questionnaire 2014.

Selected trends for STI and national STI policies

37

Trend 1 • A modest recovery

Trend 2 • Shifts in global STI landscape

Trend 3 • Persistant ‘Grand’ challenges

Trend 4 • Mutation in STI policies

Trend 5 • Public support to firms

Trend 6 • Public research policy

Challenges of public research policy

38

• Governance and coordination: more autonomous universities, multiple stakeholders (industry, local actors, students etc.)

• Globalisation and openness: keep pace with knowledge/technology development and compete for talents and assets

• Turning science into business: the ‘third’ mission of universities

• Technology convergence: require multidisciplinary research arrangements, platforms, shift away from ‘silo’ approach in doing/funding/evaluating research.

• Ageing workforces: skills gap to be increased and some evidence of disinterest in science among youth.

• Funding public research in times of budgetary austerity

Focus on excellence

39

• Research infrastructures: through national strategy, long-term planning (roadmaps etc.), and investments in capacity and platforms

• New approaches in funding:

• Prioritisation and concentration of resources to reach a critical of mass

• More competitive funding: project-based versus ‘block’ grants, and performance-based block funding.

• Research Excellence Initiatives (REIs): new funding instrument that combines stability of long-term grants and selectivity through competition-based processes. Multidisciplinarity.

• Full economic cost recovery.

• Evaluation has taken on greater importance.

• Internationalisation of universities: recent initiatives to attract talents and raise international visibility (joint programmes, campus offshore, ‘MOOCS’)

Knowledge transfer is a central objective of public research

40

Substantial changes in various STI policy areas , country self assessment, 2012-14CC

Source: Country responses to the STI Outlook policy questionnaire 2014.

OECD infrastructure for innovation policy analysis

41

For further reading… An infrastructure for knowledge sharing and building

Measurement work

42

Country reviews of innovation

policy (peer reviews)

STI Outlook (Policy database,

benchmarking tools)

OECD Committees 2015-16: impact assessment,

inclusive innovation, foresight

The IPP is a web-based learning tool on innovation policy for policy makers and experts. Co-developed by the OECD and the WB.

43

Coordination across international Organisations: EC and WB

• Taxonomies and common standards to support a dialogue between 2 global platforms: OECD/WB IPP and EC Policy Support Facility (PSF).

• STI Outlook Policy Database: joint development with the EC – next update: June 2015

• Information sharing:

– Publications, briefs, policy/working papers, case studies etc. (>2 000)

– STI e-Outlook (profiles, policy database, benchmarking tools) – next release : June 2015

– IPP.Stat : indicators and visualisation – next update: June 2015

• Identifying issues and solutions: Diagnostic tools to support policy decision process

• Exchanging and networking: Communities of Practices

THANKS!

44

www.oecd.org/sti/outlook

www.innovationpolicyplatform.org/content/STIe-Outlook-2014(forthcoming)

www.innovationpolicyplatform.org/oecd-stio-forward-look(forthcoming)

www.innovationpolicyplatform.org

www.oecd.org/innovation/reviews

Contact: Sandrine [email protected]