12 years on, how where - actuaries · bancassurance – 12 years on, how we got here where we are...

TRANSCRIPT

Page 1

Bancassurance – 12 Years

On, How We Got Here

Where We are Heading

Teh Loo Hai

Page 2

Contents• Brief history of bancassurance development

• Factors affecting the development

• Evaluating the successfulness ofbancassurance

• What factors may shape future ofbancassurance

• How insurance companies and banks prepare themselves for the future

Page 3

History of Bancassurance Development

Page 4

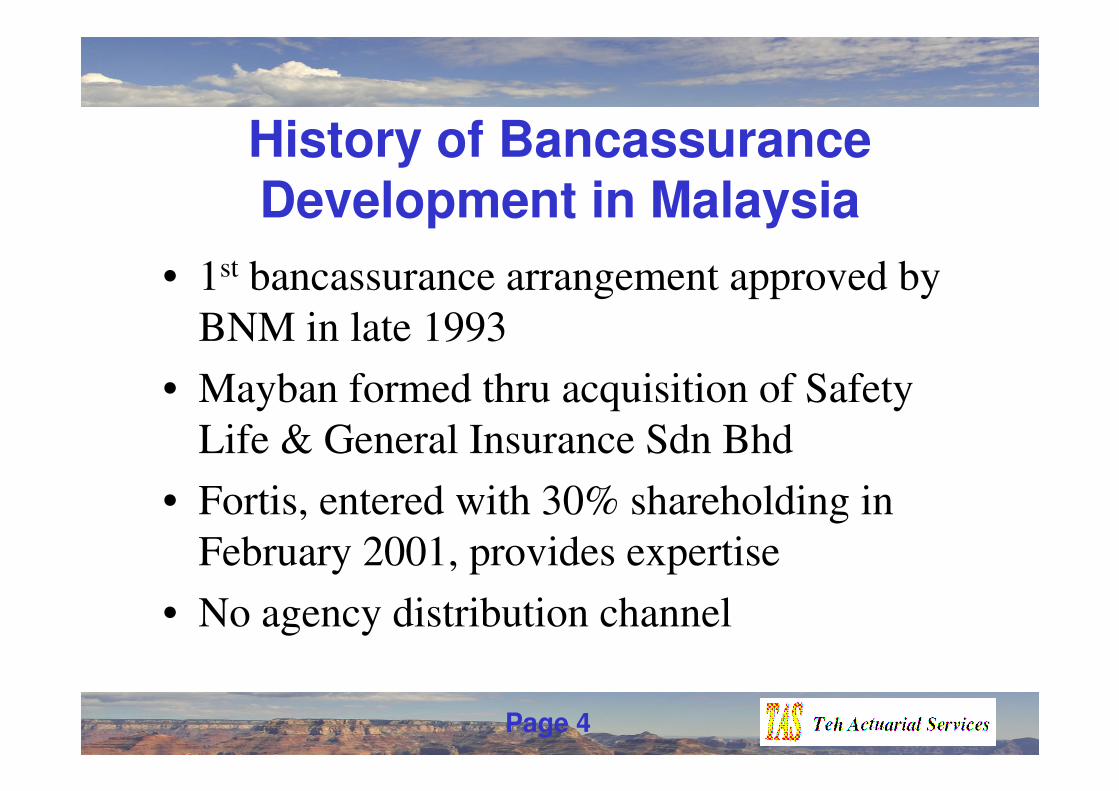

History of Bancassurance Development in Malaysia

• 1st bancassurance arrangement approved by

BNM in late 1993

• Mayban formed thru acquisition of Safety

Life & General Insurance Sdn Bhd

• Fortis, entered with 30% shareholding in

February 2001, provides expertise

• No agency distribution channel

Page 5

Growth of Mayban’s Bancassurance (1995 – 2000)

Source: Sigma No. 7/2002

Page 6

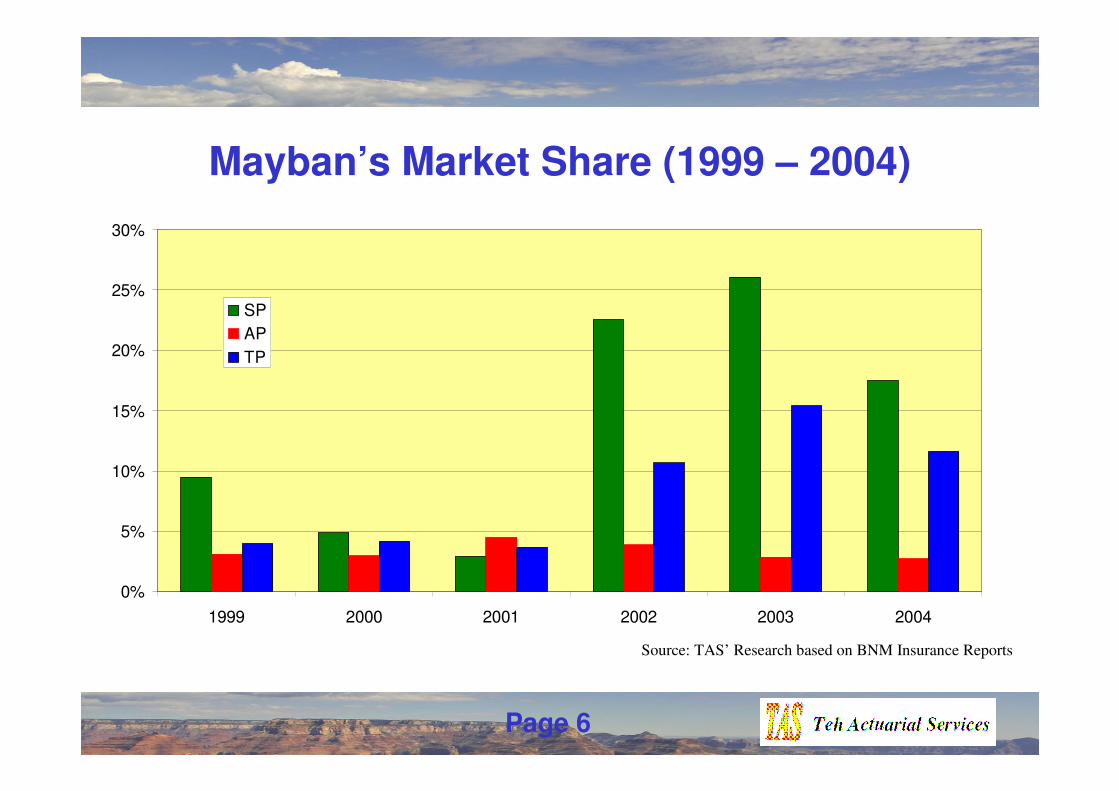

Mayban’s Market Share (1999 – 2004)

Source: TAS’ Research based on BNM Insurance Reports

0%

5%

10%

15%

20%

25%

30%

1999 2000 2001 2002 2003 2004

SP

AP

TP

Page 7

Emergence of Other Players

• Great Eastern established bancassurance

department in 2000 after merger with OAC

• EONCMG renamed Uni.Asia with entrance of

UOB bank, early 2003

• Bumiputra-Commerce acquired AMAL in 1999

• Prudential distributes via Standard Chartered Bank

• Various other distribution agreements in place

Page 8

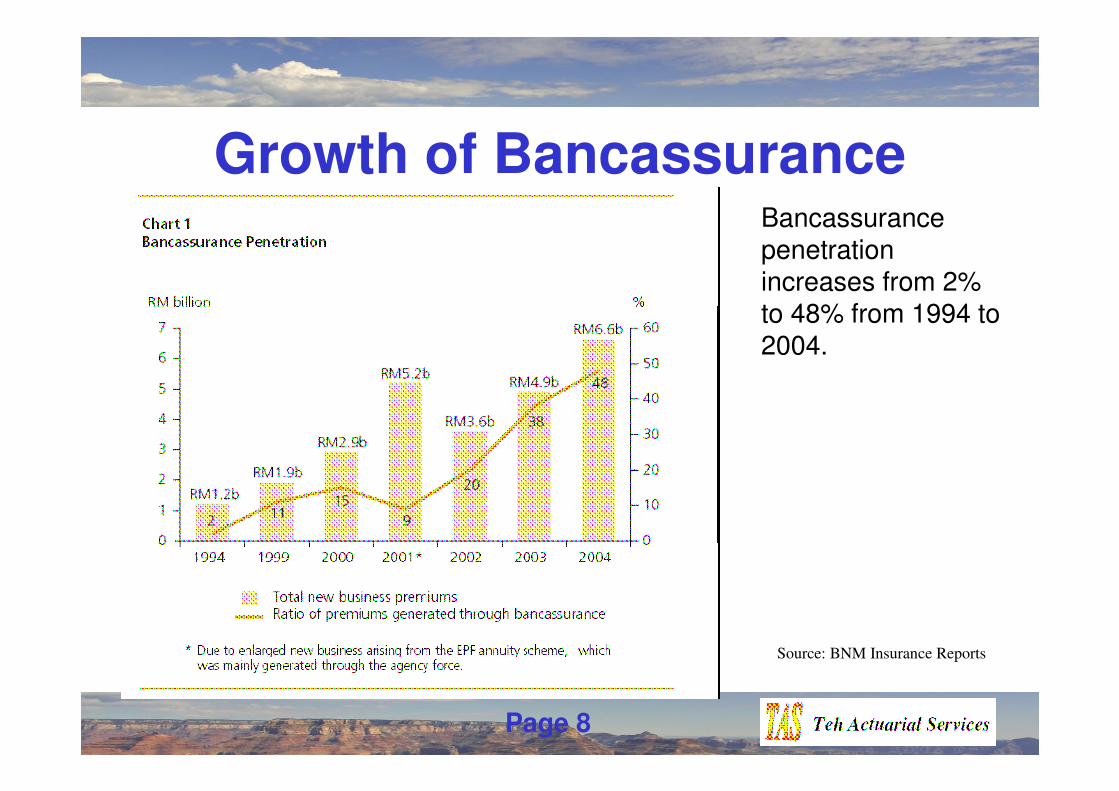

Growth of BancassuranceBancassurance penetration increases from 2% to 48% from 1994 to 2004.

Source: BNM Insurance Reports

Page 9

Factors Contributing to Growth of Bancassurance

Page 10

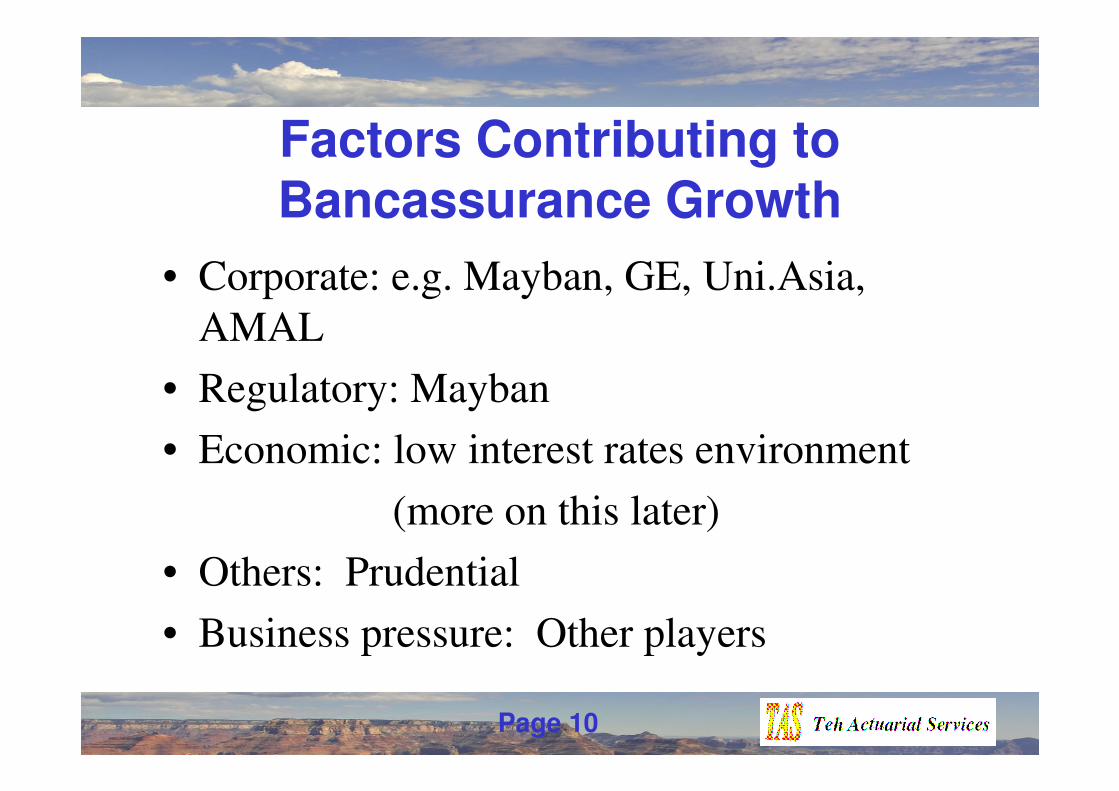

Factors Contributing to Bancassurance Growth

• Corporate: e.g. Mayban, GE, Uni.Asia,

AMAL

• Regulatory: Mayban

• Economic: low interest rates environment

• Others: Prudential

• Business pressure: Other players

Page 11

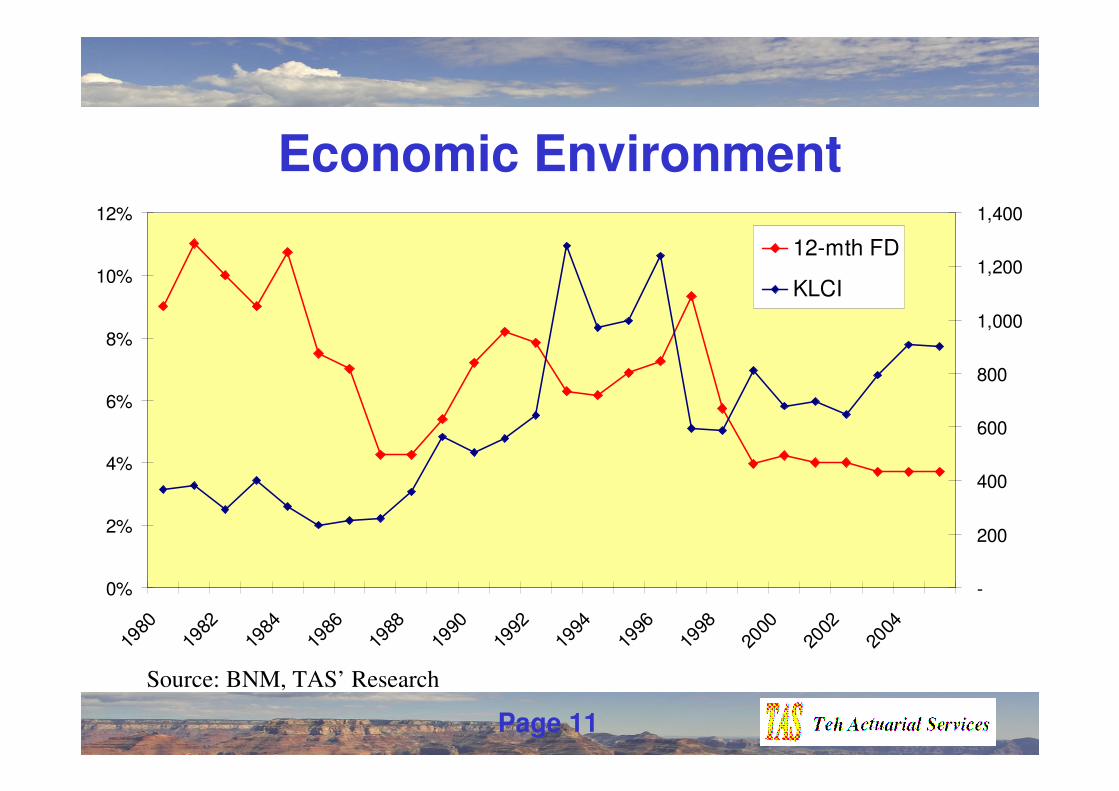

Economic Environment

0%

2%

4%

6%

8%

10%

12%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

-

200

400

600

800

1,000

1,200

1,400

12-mth FD

KLCI

Source: BNM, TAS’ Research

Page 12

Economic Environment

• Consumers had no where to park money

• Desperate search for high yielding investment instruments

• Banks wanted to offload FDs

• Insurers companies chasing for market share

• The birth of innovative products

– Short-term guaranteed endowment plans

Page 13

Successfulness of Bancassurance

Page 14

Evaluation Factors

• FSMP

• Penetration

• Spread of products

• Productivity

• Bancassurance models

Page 15

Financial Sector Masterplan

(FSMP)

• Launched in March 2001

• Recommendation 4.3: Promote

incentives for the growth of bancassurance

– Ability of banks to own insurers and distribute

insurance and pension products

– Ability of banks and insurers to share customer

information.

Page 16

Bancassurance Penetration

Bancassurance penetration increases from 2% to 48% from 1994 to 2004, but how much is due to AP business?

Source: BNM Insurance Reports

Page 17

Comparison with European Countries

Page 18

SP and AP New Business

-

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1999 2000 2001 2002 2003 2004

RM

billio

n

SP

AP

Bancassurance Growth Contributed

by Growth of SP Business

• SP business grew 612% while AP business grew 47% over the 6 years period

Source: BNM Insurance Reports

Page 19

Mayban’s Market Share (1999 – 2004)

Source: TAS’ Research based on BNM Insurance Reports

0%

5%

10%

15%

20%

25%

30%

1999 2000 2001 2002 2003 2004

SP

AP

TP

Page 20

Successfulness of Bancassurance

• Only 8% is AP

Source: BNM Insurance Reports

Page 21

Productivity of Bancassurance

ChannelNo. Cases /

Producer

Rank SP AP AP

1 443 14.6 49.2

2 261 5.0 41.4

3 110 2.7 28.2

4 100 2.4 16.1

5 56 2.3 14.5

Total 969 27.2 14.4

% Mkt Share 82.2% 83.9%

US$ '000,000

Page 22

Reasons of Lack of Success in AP Business

• Competing for shelf space in banks

• Commission less attractive

• Life insurance has to be sold rather than

bought

• Lack of commitment from bank partner

• Underwriting puts off customers

• Long payback period for banks

Page 23

Bancassurance Models

• BNM Insurance Report 2004

– Referrals

– Distribution Agreements (96%)

– Integrated Services

Page 24

Distribution of BancassuranceModels in Europe

Page 25

Factors Shaping Future of Bancassurance

Page 26

Shaping the Future of Bancassurance

• Foreign-foreign tie-up prohibited

• Rising interest rates

• Bancassurance commission rates

• Commission disclosures

• New takaful licenses

Page 27

Prohibition of Foreign Tie-ups

• Current restriction on foreign-foreign tie-up

• Will this be removed under FSMP?

• Is GE the sleeping giant?

Page 28

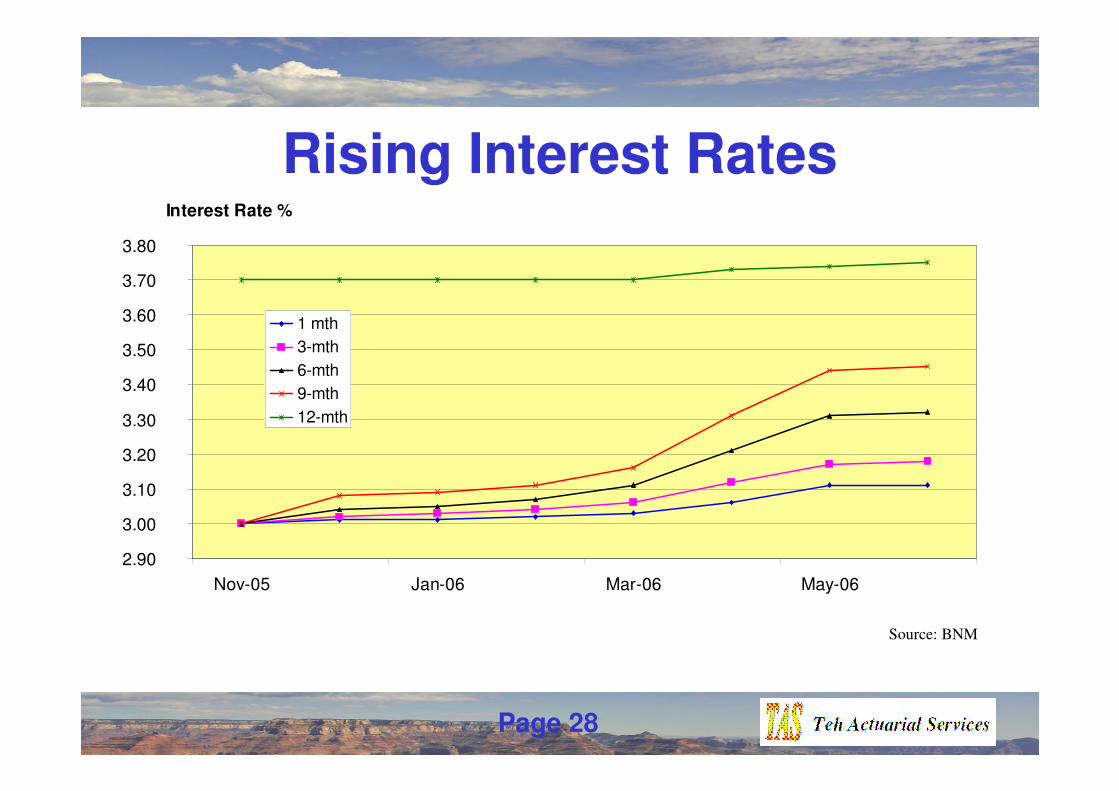

Rising Interest Rates

2.90

3.00

3.10

3.20

3.30

3.40

3.50

3.60

3.70

3.80

Nov-05 Jan-06 Mar-06 May-06

Interest Rate %

1 mth

3-mth

6-mth

9-mth

12-mth

Source: BNM

Page 29

Lowering of Bancassurance Commission Rates

• In BNM’s Insurance Report 2004, under

“Promoting Growth of Bancassurance”

– “With lower acquisition costs, consumers will

benefit from the efficient cost structures of

bancassurance arrangements.”

• More flexibility in commission rates

– Savings Products: PV 50% over 10 years

– Protection Products: PV 70% over 6 years

Page 30

Commission Disclosure

• In BNM’s Insurance Report 2004, under

“Promoting Growth of Bancassurance”

– “The requirement on commission disclosure

will also facilitate comparisons of

bancassurance products with other savings and

investment instruments.”

Page 31

New Takaful Licenses

• 4 new licenses were issued in 2005

• HSBC Amanah Takaful & HSBC

• Prudential BSN Takaful Bhd & Bank

Simpanan

Page 32

Preparing for the Future

Page 33

More Acquisitions

• Failed attempt of Southern Bank and Public

Bank on Asia Life

• Failed attempt of OCBC in taking Great

Eastern private

• Maybank acquired MNI

Page 34

Commission Rates

• Continued lobby by the industry in

increasing commission rates

– Production Commission

– Persistency Commission

Page 35

Widening Product Range

• OCBC selling Pacific Insurance medical

products

• Bancatakaful with entrance of HSBC and

Prudential-Bank Simpanan?

• Shift in focus to AP?

Page 36

Conclusion

• Past success of bancassurance in SP

• Future success lies in AP

• Entrance of more serious players

• Further relaxation of regulatory

environment one of key success factors