2005 annual report -...

TRANSCRIPT

2005ANNUAL REPORT

Head N.V. is a Dutch Company. It listed its ordinary shares on the New York Stock Exchange and Vienna Stock Exchangein September 2000.

We are a leading global manufacturer and marketer of premium sports equipment. We have a strong heritage in sportinggoods equipment, having brought the first metal ski to the market in 1951. More recently we introduced the firstmicro-chip controlled tennis racquets and skis. In keeping with this tradition, we believe our products are highlyinnovative and technology-driven.

We own some of the best-known and most highly respected brands in the sports equipment market:

The Head brand was established in 1950 after Howard Head invented the first laminated metal ski. It has since beenextended to cover a leading range of sports equipment including tennis, squash and racquetball racquets, alpine skis andboots, and snowboards, bindings and boots. Head is currently the number two tennis racquet brand in the world and isone of the top alpine ski and boot manufacturers.

The Penn Company was founded almost 100 years ago and has been making history ever since, introducing the firstpressurized ball cans in 1922 and the first fluorescent yellow tennis ball in 1968. Penn was acquired by Head in 1999 andtoday Penn is the official ball of the Tennis Masters Series and the number one selling tennis ball in the United States.Penn racquetball balls are currently the number one selling racquetball ball worldwide.

Tyrolia is estimated to be the world’s number one alpine ski binding producer. Tyrolia has been producing bindings since1928 and has brought to market innovations such as the first step-in alpine binding in 1962 and the first carving bindingin 1996.

Mares was founded in 1949 as one of the first industrial diving companies. Today it is one of the leading dive brandsworldwide with particular strengths in regulators and all-in-one diving systems (the H.U.B.). Dacor, founded in 1953 andbased in the United States, specializes in scuba equipment.

Our products appeal to a wide range of users from novices to some of the world’s top athletes including Andre Agassi,Gustavo Kuerten, Marat Safin, Swetlana Kusnezowa, Johann Grugger, Marco Büchel and Maria Riesch.

Our products are sold through over 30,000 accounts including pro shops, specialty sporting goods stores and massmerchants in over 85 countries around the world.

For more information, please visit our website: www.head.com

A B O U T H E A D

1

About Head . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Inside front cover

Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Chairman’s Letter to Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Management’s Discussion and Analysis of Financial Statements and Results of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Consolidated Balance Sheets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Consolidated Statements of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Consolidated Statements of Stockholders’ Equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Consolidated Statements of Cash Flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Notes to the Consolidated Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Report of Independent Registered Public Accounting Firm . . . . . . . . . . . . . . . . . . . . . . . 33

List of Significant Participations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

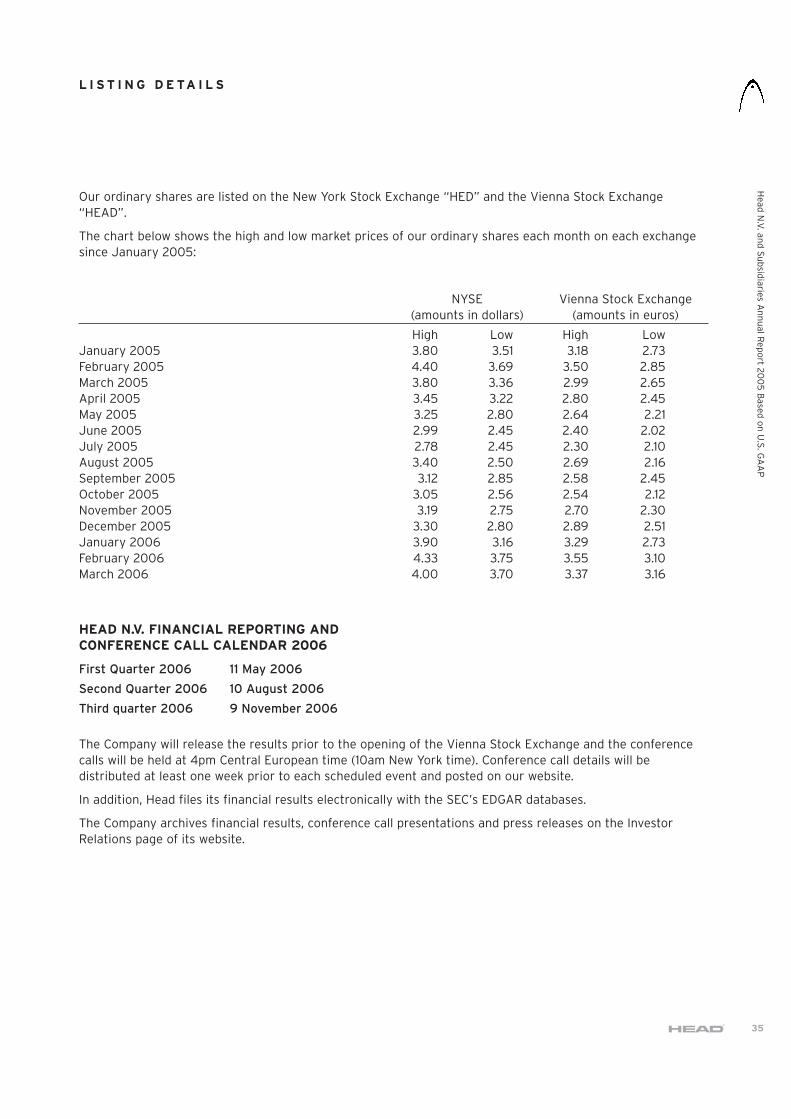

Listing Details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Shareholder Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Corporate Directory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

C O N T E N T S

Head

N.V

. An

nu

al Rep

ort 20

05

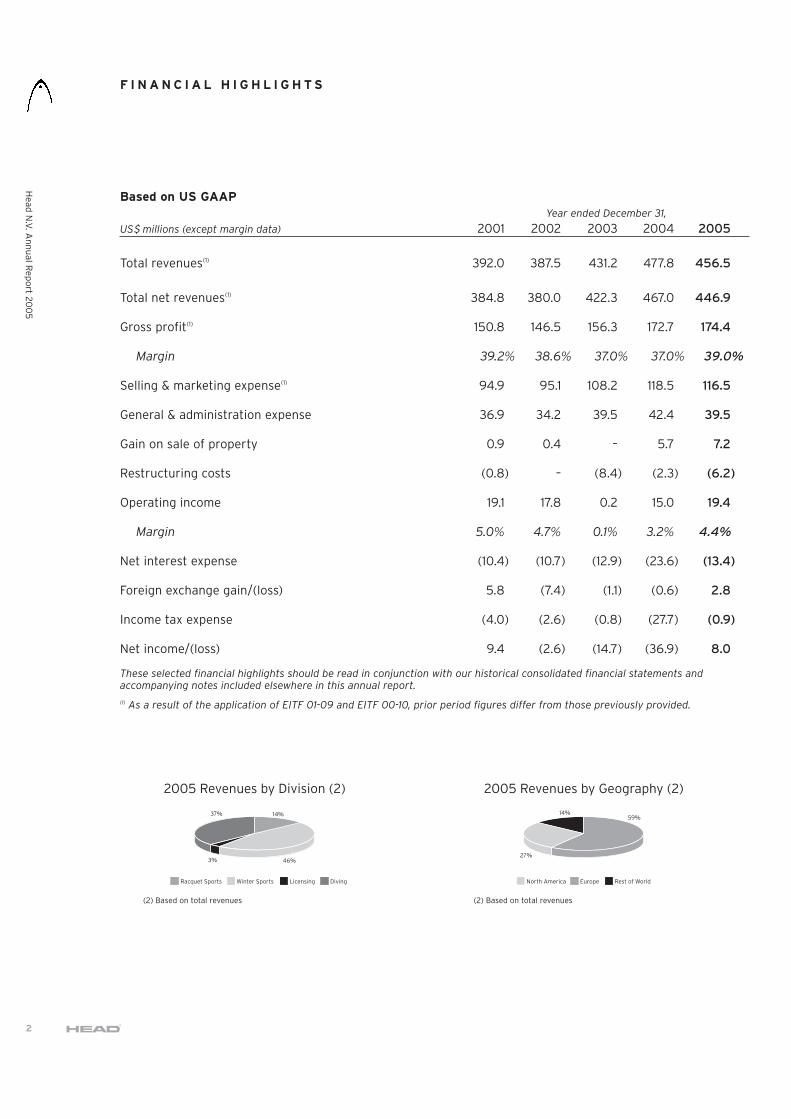

Based on US GAAPYear ended December 31,

US$ millions (except margin data) 2001 2002 2003 2004 2005

Total revenues(1) 392.0 387.5 431.2 477.8 456.5

Total net revenues(1) 384.8 380.0 422.3 467.0 446.9

Gross profit(1) 150.8 146.5 156.3 172.7 174.4

Margin 39.2% 38.6% 37.0% 37.0% 39.0%

Selling & marketing expense(1) 94.9 95.1 108.2 118.5 116.5

General & administration expense 36.9 34.2 39.5 42.4 39.5

Gain on sale of property 0.9 0.4 – 5.7 7.2

Restructuring costs (0.8) – (8.4) (2.3) (6.2)

Operating income 19.1 17.8 0.2 15.0 19.4

Margin 5.0% 4.7% 0.1% 3.2% 4.4%

Net interest expense (10.4) (10.7) (12.9) (23.6) (13.4)

Foreign exchange gain/(loss) 5.8 (7.4) (1.1) (0.6) 2.8

Income tax expense (4.0) (2.6) (0.8) (27.7) (0.9)

Net income/(loss) 9.4 (2.6) (14.7) (36.9) 8.0

These selected financial highlights should be read in conjunction with our historical consolidated financial statements andaccompanying notes included elsewhere in this annual report.

(1) As a result of the application of EITF 01-09 and EITF 00-10, prior period figures differ from those previously provided.

F I N A N C I A L H I G H L I G H T S

Head

N.V

. An

nu

al Rep

ort 20

05

2

2005 Revenues by Division (2)

46%

37% 14%

Racquet Sports

3%

Winter Sports Licensing Diving

(2) Based on total revenues

2005 Revenues by Geography (2)

59%

27%

North America

14%

Europe Rest of World

(2) Based on total revenues

Dear Shareholders,

The Head Group experienced a solid year in 2005,with strong operating income, and a substantialimprovement in net income from 2004. The sportinggoods equipment market continues to be a toughoperating environment; the development ofinnovative, high performance products remainsessential to achieve sales and margin improvements.Our implementation of cost saving & restructuringinitiatives is an on-going strategy, which continues tohave a beneficial impact on the Group’s results.

GROUP RESULTSTotal Group net revenues for 2005 were $446.9million, a decrease of 4% on 2004’s total netrevenues of $467.0 million. This decrease was due tolower sales in all of the Company’s divisions exceptLicensing and was partially offset by lower salesdeductions.

Our reported operating profit of $19.4 million is $4.4million above the reported operating profit of $15.0million in 2004. When adjusted for restructuringcosts ($6.2 million in 2005, and $2.3 million in 2004)and one-off gains on the sale of property ($7.2million in 2005, $5.7 million in 2004) the operatingprofit increase is $6.7 million from a $11.7 millionadjusted operating profit in 2004 to $18.4 million in2005.

DIVISIONAL RESULTSRevenues in our Winter Sports division decreased by3%, to $216.3 million from $223.2 million in 2004.This decrease was due to lower sales volumes forskis and bindings and the weakening of the euroagainst the U.S. dollar in the last quarter of the year,partly offset by higher sales volumes for ski bootsand the introduction of snowboard protection wear.

Revenues in our Racquet Sport division decreasedmarginally, by 1%, to $166.6 million from $168.0million in 2004. This decrease resulted mainly fromlower sales due to less favorable product and countrymix for the Company’s tennis racquets and lowersales volumes of its bags and tennis balls. This

decrease was partly offset by significantly highersales volumes in tennis racquets, better product mixin tennis balls and the strengthening of the euroagainst the U.S. dollar during the main deliveryperiod.

Revenues in our Diving division decreased 19% to$61.4 million from $75.5 million in 2004. This reflectsthe unfavorable market conditions, together with ourstrategy of improving product mix and generatinghigher margins (as opposed to increasing revenues).The strengthening of the euro against the U.S. dollarpartly offset the decline in revenues.

Revenues from licensing agreements increased by$1.2 million, or 11%, to $12.2 million from $11.1 millionin 2004. This was mainly due to increased revenuesfrom existing contracts and from new licensingagreements.

REORGANISATION AND RESTRUCTURINGDuring 2005, we continued to implementrestructuring projects; it is anticipated that these willhave a beneficial impact on future costs. The mainelements were as follows:

• Outsourcing tennis racquet production to China,resulting in a 90% reduction in our tennis racquetproduction in Kennelbach, Austria and Budweis,Czech Republic

• Restructuring of our ski binding production• Reduction of our production capacity at our plant

in Rapallo, Italy• Transfer of the remaining ski boot production from

Maser, Italy to Litovel, Czech Republic

NEW PRODUCTSAs in previous years, we have continued to focus oninnovation and the development of the nextgeneration of technologically advanced products.

In Winter Sports, we have introduced the new“Supershape” ski, appropriately named because ofthe pronounced side-cut in the design. Incorporationof Intelligence Technology ensures it rapidly adaptsto any situation, and Liquidmetal provides additional

C H A I R M A N ’ S L E T T E R T O S H A R E H O L D E R S

Head

N.V

. An

nu

al Rep

ort 20

05

3

power and vitality. We have also focused on ourrange for women; the “Cool Thang” providesoutstanding edge grip, and easy turn initiation forthe mid-speed range.

The S10 boot is designed for Freeride skiers; topspeeds & tight turns demand excellent materialcomposition, and the security of double powerbuckles. Head Winter Sports launched a newcategory of products in 2005: Head Protection. Thehighly technical products (based on spine & headprotection) are the result of 2 years of research &collaboration with international industrial designers,engineers & industry experts. The products havedistinct visual appeal, and include helmets,protection jackets, vests and backpacks, for bothskiing and snowboarding.

In Racquet Sports, our most significant new productlaunch, in Spring 2005, was Flexpoint Technology.Incorporating Liquidmetal, Flexpoint technology usestwo precisely engineered control holes, giving theracquet a revolutionary new flexpoint. This allowssignificantly more control over the ball, whileretaining all the power. It was with the FlexpointRadical that Andre Agassi reached the final of the USOpen during the summer. The other notable successwith a Head racquet was Marat Safin winning theAustralian Open.

In 2005, the Diving division launched a rangespecifically tailored to women divers, with a focus onperformance, fashion & comfort. The diving division’slatest product launch is the Quattro Excel fin.Following numerous tests on new materials, togetherwith lengthy computer simulations, the “SuperChannel Thrust” design makes it possible to channelthe water & optimize thrust in comparison to otherfins of similar size.

OUTLOOK FOR 2006Whilst market conditions have not improvedsignificantly, our performance continues to improve.We are encouraged by the strong performance in2005, and anticipate that our on-going restructuring& cost-saving initiatives will produce furtherefficiencies & savings in 2006. Our overriding

strategy continues to be the development ofinnovative products across all of the markets withinwhich we operate.

Sincerely,

Johan Eliasch

Chairman and Chief Executive Officer, Head N.V.

May 2006

C H A I R M A N ’ S L E T T E R T O S H A R E H O L D E R S( c o n t i n u e d )

He

ad

N.V

. An

nu

al R

ep

ort 2

00

5

4

Overview:The Company is a leading global manufacturer andmarketer of branded sporting goods serving theskiing, tennis and diving markets. The Company hascreated or acquired a portfolio of brands – Head(principally alpine skis, ski boots and snowboardproducts, tennis, racquetball and squash racquets),Penn (tennis balls and racquetball balls), Tyrolia (skibindings), Mares and Dacor (diving equipment). TheCompany’s key products have attained leadingmarket positions based on sales and reputation andhave gained high visibility through their use by manyof today’s top athletes.

With a broad product offering marketed mainly frommiddle to high price points, the Company suppliessporting equipment and accessories to all majordistribution channels in the skiing, tennis and divingmarkets, including pro shops, specialty sportinggoods stores and mass merchants. Head N.V.’sproducts are sold through some 30,000 customers inover 85 countries and target sports enthusiasts ofvarying levels of ability and interest ranging from thenovice to the professional athlete. The Company’sstrongest presence has traditionally been in Europe,and in recent years the Company has built marketshare in the United States, the next largest marketfor the Company’s products after Europe.

Over the last 56 years, the Company believes it hasearned a reputation as a leading developer andmanufacturer of innovative, high-quality andtechnologically advanced sporting equipment. TheCompany’s focus continues to be its core products ofskiing, tennis and diving equipment. In order toexpand market share and maximize profitability, forthe last ten years the Company has increased itsemphasis on marketing and new productdevelopment, leveraging further its brands, globaldistribution network and traditional strength inmanufacturing and in 2003, the Company initiated aprogram to reduce its fixed costs and streamline itsorganizational structure.

The Company generates revenues in its principalmarkets by selling goods directly to retail stores and toa lesser extent, by selling to distributors. It alsoreceives licensing and royalty income. As many of its

goods, especially Winter Sports goods, are shippedduring a specific part of the year, the Companyexperiences highly seasonal revenue streams.Following industry practice, the Company begins toreceive orders from its customers in the Winter Sportsdivision from March until June, during which time theCompany books approximately three quarters of itsorders for the year. The Company will typically beginshipment of skis, boots and bindings in July andAugust, with the peak shipping period occurring inOctober and November. At this time, the Company willbegin to receive re-orders from customers, whichconstitute the remaining quarter of its yearly orders.Re-orders are typically shipped in December andJanuary. Racquet Sports and Diving product revenuesalso experience seasonality, but to a lesser extent thanWinter Sports revenues. Revenue from sales isgenerally recognized at the time of shipment.

Market EnvironmentWinter Sports. Snowfalls at the end of November, andthe beginning of December 2005 in all our majorWinter Sports markets, including Japan, generatedearly interest in winter sports products and retailersreported improved sales at the beginning of thewinter sports season 2005/06 compared to theprevious year. Ski boots, in particular, were reportedcomparatively high sales. The Eastern Europe marketfor Winter Sports equipment also developed well.Although the Eastern Europe market volume for2005 remained relatively stable compared withprevious years, we may see an improvement inmarket share for 2006. The snowboard market for2005 was adversely affected by the late start of the2004/05 winter sports season, but has beenpositively affected by the early snow of the 2005/06season. However, the Company still expects themarket for snowboard products to decline byapproximately 15%.

Racquet Sports. Due to an unprecedented number ofnew racquet launches in the premium segment of theworldwide market, the US market for tennis racquetsales in 2005 improved substantially over 2004. TheEuropean tennis markets also showed slight growthfor 2005. Only the Japanese tennis market declinedin 2005 compared to 2004, albeit marginally.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I SO F F I N A N C I A L S TAT E M E N T S A N D R E S U LT S O F O P E R AT I O N S

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

5

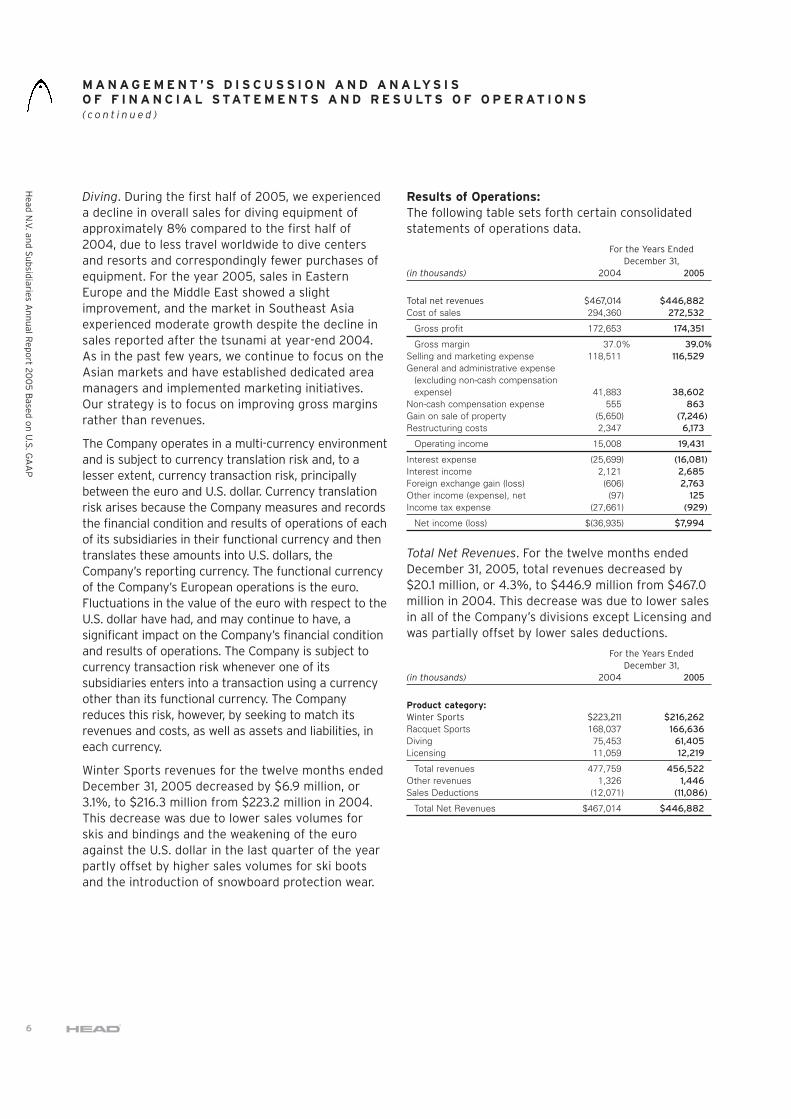

Diving. During the first half of 2005, we experienceda decline in overall sales for diving equipment ofapproximately 8% compared to the first half of2004, due to less travel worldwide to dive centersand resorts and correspondingly fewer purchases ofequipment. For the year 2005, sales in EasternEurope and the Middle East showed a slightimprovement, and the market in Southeast Asiaexperienced moderate growth despite the decline insales reported after the tsunami at year-end 2004.As in the past few years, we continue to focus on theAsian markets and have established dedicated areamanagers and implemented marketing initiatives.Our strategy is to focus on improving gross marginsrather than revenues.

The Company operates in a multi-currency environmentand is subject to currency translation risk and, to alesser extent, currency transaction risk, principallybetween the euro and U.S. dollar. Currency translationrisk arises because the Company measures and recordsthe financial condition and results of operations of eachof its subsidiaries in their functional currency and thentranslates these amounts into U.S. dollars, theCompany’s reporting currency. The functional currencyof the Company’s European operations is the euro.Fluctuations in the value of the euro with respect to theU.S. dollar have had, and may continue to have, asignificant impact on the Company’s financial conditionand results of operations. The Company is subject tocurrency transaction risk whenever one of itssubsidiaries enters into a transaction using a currencyother than its functional currency. The Companyreduces this risk, however, by seeking to match itsrevenues and costs, as well as assets and liabilities, ineach currency.

Winter Sports revenues for the twelve months endedDecember 31, 2005 decreased by $6.9 million, or3.1%, to $216.3 million from $223.2 million in 2004.This decrease was due to lower sales volumes forskis and bindings and the weakening of the euroagainst the U.S. dollar in the last quarter of the yearpartly offset by higher sales volumes for ski bootsand the introduction of snowboard protection wear.

Results of Operations:The following table sets forth certain consolidatedstatements of operations data.

For the Years EndedDecember 31,

(in thousands) 2004 2005

Total net revenues $467,014 $446,882Cost of sales 294,360 272,532

Gross profit 172,653 174,351

Gross margin 37.0% 39.0%Selling and marketing expense 118,511 116,529General and administrative expense

(excluding non-cash compensation expense) 41,883 38,602

Non-cash compensation expense 555 863Gain on sale of property (5,650) (7,246)Restructuring costs 2,347 6,173

Operating income 15,008 19,431

Interest expense (25,699) (16,081)Interest income 2,121 2,685Foreign exchange gain (loss) (606) 2,763Other income (expense), net (97) 125Income tax expense (27,661) (929)

Net income (loss) $(36,935) $7,994

Total Net Revenues. For the twelve months endedDecember 31, 2005, total revenues decreased by$20.1 million, or 4.3%, to $446.9 million from $467.0million in 2004. This decrease was due to lower salesin all of the Company’s divisions except Licensing andwas partially offset by lower sales deductions.

For the Years EndedDecember 31,

(in thousands) 2004 2005

Product category:Winter Sports $223,211 $216,262Racquet Sports 168,037 166,636Diving 75,453 61,405Licensing 11,059 12,219

Total revenues 477,759 456,522Other revenues 1,326 1,446Sales Deductions (12,071) (11,086)

Total Net Revenues $467,014 $446,882

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I SO F F I N A N C I A L S TAT E M E N T S A N D R E S U LT S O F O P E R AT I O N S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

6

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I SO F F I N A N C I A L S TAT E M E N T S A N D R E S U LT S O F O P E R AT I O N S( c o n t i n u e d )

Head N

.V. and Subsidiaries A

nnual Report 2005 B

ased on U.S

. GA

AP

7

Racquet Sports revenues for the twelve monthsended December 31, 2005 decreased by $1.4 million,or 0.8%, to $166.6 million from $168.0 million in2004. This decrease resulted mainly from lower salesdue to less favorable product and country mix for theCompany’s tennis racquets and lower sales volumesof its bags and tennis balls. This decrease was partlyoffset by significantly higher sales volumes in tennisracquets, better product mix in tennis balls and thestrengthening of the euro against the U.S. dollarduring the main delivery period.

Diving product revenues for the twelve monthsended December 31, 2005, decreased by $14.0million, or 18.6%, to $61.4 million from $75.5 millionin 2004, reflecting the unfavorable market conditionsand our strategy of improving product mix andgenerating higher margins rather than increasingrevenues. The strengthening of the euro against theU.S. dollar partly offset the decline in revenues.

Licensing revenues for the twelve months endedDecember 31, 2005, increased by $1.2 million, or10.5%, to $12.2 million from $11.1 million in 2004mainly due to increased revenues from existingcontracts and from new licensing agreements.

Other revenues include amounts billed to customersfor shipping and handling. These amounts arerecognized also as selling and marketing expense.

Sales deductions for the twelve months endedDecember 31, 2005, decreased by $1.0 million, or8.2%, to $11.1 million from $12.1 million in 2004mainly due to declining revenues.

Gross Profit. For the twelve months ended December31, 2005, gross profit increased by $1.7 million to$174.4 million from $172.7 million in 2004 due toimproved operating performance as a result of theCompany’s restructuring programs which positivelyaffected manufacturing cost, as well as morefavorable product mix. Gross margin increased to39.0% for the twelve months ended December 31,2005 from 37.0% in the comparable 2004 period.

Selling and Marketing Expense. For the twelvemonths ended December 31, 2005, selling andmarketing expense decreased by $2.0 million, or1.7%, to $116.5 million from $118.5 million in 2004.

The decrease was due mainly to lower variabledistribution costs as a consequence of declining salespartly offset by higher expenditures for advertisingand selling departments.

General and Administrative Expense. For the twelvemonths ended December 31, 2005, general andadministrative expense decreased by $3.3 million, or7.8%, to $38.6 million from $41.9 million in 2004.This decrease was due to lower expenses forwarehouse and administration due to tight expensecontrols and the Company’s restructuring programs.

Non-Cash Compensation Expense. For the twelvemonths ended December 2004 and 2005, theCompany recorded a non-cash compensationexpense of $0.6 million and $0.9 million, respectively,due to the grant of stock options under theCompany’s stock option plans 1998, 2001 and 2005and the resulting amortization expense.

Gain on sale of property. In June 2005, the Companysold the property in Tallinn, Estonia which waspreviously leased and realized a gain of $7.2 million.In September 2004, the Company realized a gain of$5.7 million from the sale of its property in Mullingar,Ireland.

Restructuring Costs. The Company recordedrestructuring costs of $6.2 million in the twelvemonth period ended December 31,2005 in relation tothe reduction by 90% of the Company’s tennisracquet production in Kennelbach, Austria andBudweis, Czech Republic, the restructuring programof the Company’s ski binding production, thereduction of its production capacity in its plant inRapallo, Italy and the transfer of the remaining skiboot production from Maser, Italy to Litovel, CzechRepublic. The Company recorded restructuring costsof $2.3 million in the twelve month period endedDecember 31, 2004 consisting of dismissal andtransfer costs in connection with the closing of itsproduction facility in Mullingar, Ireland and the plantin Tallinn, Estonia (see Note 25).

Operating Income. As a result of the foregoingfactors, for the twelve months ended December 31,2005, operating income increased by $4.4 million to$19.4 million from $15.0 million in 2004.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I SO F F I N A N C I A L S TAT E M E N T S A N D R E S U LT S O F O P E R AT I O N S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

8

Interest Expense. For the twelve months endedDecember 31, 2005 interest expense decreased by$9.6 million or 37.4% to $16.1 million from $25.7million in 2004. This decrease was mainly due to thewrite-off of the capitalized debt issuance costs of$3.2 million relating to the Company’s former 10.75%senior notes, which were repaid with proceeds fromits newly issued 8.5% senior notes in January 2004.The premium of $4.4 million for the early redemptionof the 10.75% senior notes was reported in 2004. Inaddition, interest expenses for the 8.5% senior notesdecreased as a result of the Company’s noterepurchase program.

Interest Income. For the twelve months endedDecember 31, 2005 interest income increased by$0.6 million to $2.7 million from $2.1 million in 2004.This increase was due mainly to higher cash on hand.

Foreign Exchange Gain (Loss). For the twelve monthsended December 31, 2005, the Company recorded aforeign currency exchange gain of $2.8 million,compared to a loss of $0.6 million in 2004 as a resultof the revaluation of foreign currency assets andliabilities at the exchange rate as of December 31,2005.

Other Income (Expense), net. For the twelve monthsended December 31, 2005, other income, netincreased by $0.2 million to $0.1 million from otherexpense, net of $0.1 million in 2004.

Income Tax Expense. For the twelve months endedDecember 31, 2005, income tax expense decreasedby $26.7 million to $1.0 million from $27.7 million in2004. This decrease in income tax expense is mainlydue to a reduction in the Austrian tax rate which, in2004, led to a decrease in deferred tax assetsresulting from tax losses carried forward of $24.9million as well as the not taxable gain on sale ofproperty in Estonia.

Net Income (Loss). As a result of the foregoingfactors, for the twelve months ended December 31,2005, the Company had net income of $8.0 million,compared to net loss of $36.9 million in 2004.

Liquidity and Capital Resources:Payments from the Company’s customers are themost important source of the Company’s liquidity.Additional sources of liquidity include credit facility,financing under capital lease arrangements andvendor financing. The cash provided by these sourceshas a variety of uses. Most importantly, the Companymust pay its employees and vendors for the servicesand materials they supply. Additional uses includecapital expenditures, development of new products,payment of interest, extension of credit to theCompany’s customers, and other general funding ofthe Company’s day-to-day operations.

For the twelve months ended December 31, 2005,cash generated from operating activities increasedby $32.2 million, or over 400% to $40.0 million from$7.8 million in 2004. This increase is mainly theresult of the Company’s higher net income and lowerworking capital requirements in 2005, due to lowertrade accounts receivable resulting from lower salesand lower inventories at year end compared to 2004.The Company used this cash from operations andcash from the sale of its premises in Estonia topurchase property, plant and equipment for $18.6million, to repurchase $18.8 million of the Company’s8.5% senior notes and to pay back $1.1 million ofother long term debt and to purchase available forsale marketable securities principally cash bonds for$5.3 million.

As of December 31, 2005, the Company had $131.1million (€111.0 million) of senior notes due 2014outstanding, $16.2 million of long-term obligationsunder a sale-leaseback agreement and a mortgageagreement due 2017 and $10.4 million of other long-term debt comprising secured loans in Italy and theCzech Republic. In addition, the Company used linesof credit with several banks in Austria, Canada andJapan of $32.7 million.

As of December 31, 2005, the Company had $1.0million in available unused credit facilities and $53.7million cash on hand, mainly in euro. In addition, theCompany had $17.4 million cash bonds held in eurowhich were recognized in the Company’s balancesheet as “Prepaid expense and other current assets”.

The Company believes that its current level of cashon hand, anticipated cash flows from operations andother available sources of liquidity are sufficient tomeet the Company’s operating needs for at least thenext twelve months.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I SO F F I N A N C I A L S TAT E M E N T S A N D R E S U LT S O F O P E R AT I O N S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

9

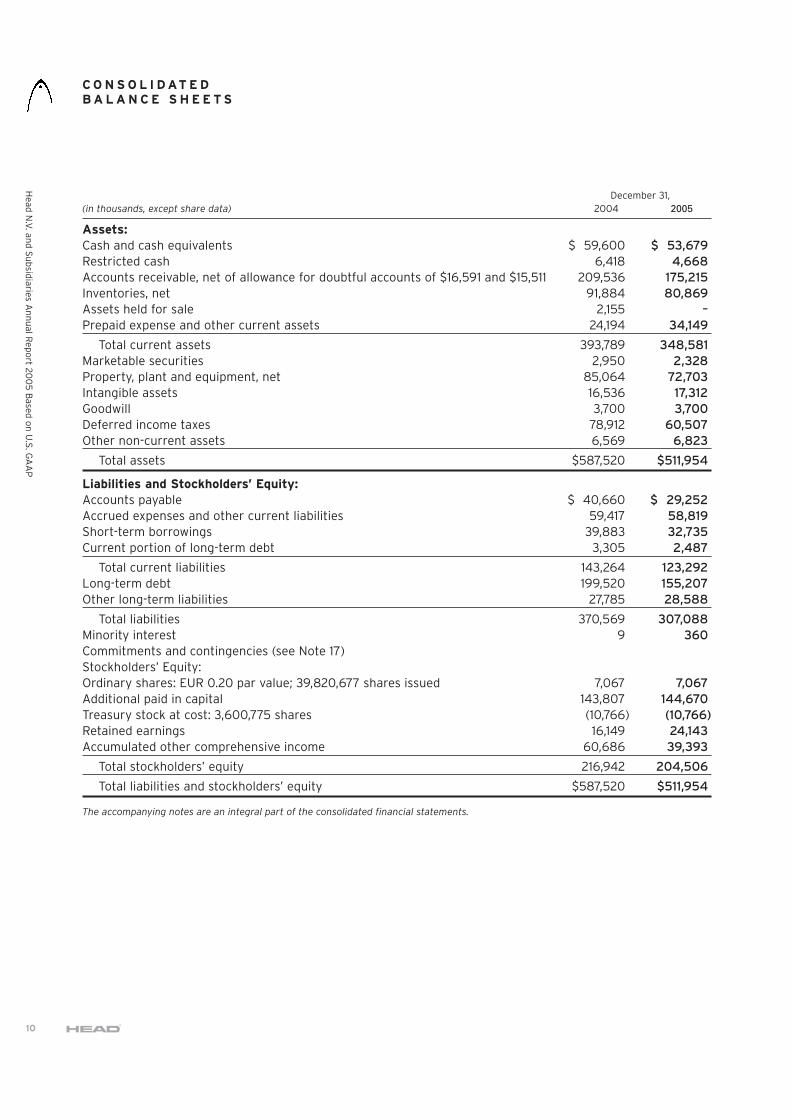

December 31,(in thousands, except share data) 2004 2005

Assets:Cash and cash equivalents $ 59,600 $ 53,679Restricted cash 6,418 4,668Accounts receivable, net of allowance for doubtful accounts of $16,591 and $15,511 209,536 175,215Inventories, net 91,884 80,869Assets held for sale 2,155 –Prepaid expense and other current assets 24,194 34,149

Total current assets 393,789 348,581Marketable securities 2,950 2,328Property, plant and equipment, net 85,064 72,703Intangible assets 16,536 17,312Goodwill 3,700 3,700Deferred income taxes 78,912 60,507Other non-current assets 6,569 6,823

Total assets $587,520 $511,954

Liabilities and Stockholders’ Equity:Accounts payable $ 40,660 $ 29,252Accrued expenses and other current liabilities 59,417 58,819Short-term borrowings 39,883 32,735Current portion of long-term debt 3,305 2,487

Total current liabilities 143,264 123,292Long-term debt 199,520 155,207Other long-term liabilities 27,785 28,588

Total liabilities 370,569 307,088Minority interest 9 360Commitments and contingencies (see Note 17)Stockholders’ Equity:Ordinary shares: EUR 0.20 par value; 39,820,677 shares issued 7,067 7,067Additional paid in capital 143,807 144,670Treasury stock at cost: 3,600,775 shares (10,766) (10,766)Retained earnings 16,149 24,143Accumulated other comprehensive income 60,686 39,393

Total stockholders’ equity 216,942 204,506

Total liabilities and stockholders’ equity $587,520 $511,954

The accompanying notes are an integral part of the consolidated financial statements.

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5B

ased o

n U

.S. G

AA

P

10

C O N S O L I D AT E DB A L A N C E S H E E T S

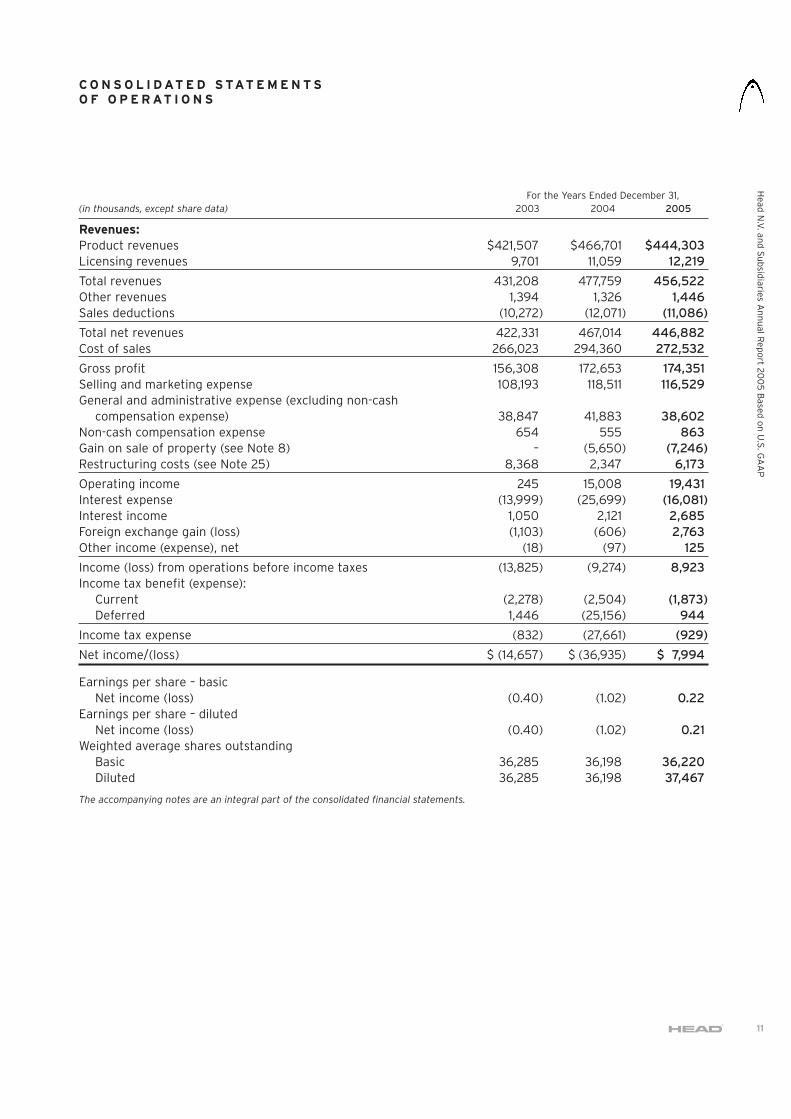

For the Years Ended December 31,(in thousands, except share data) 2003 2004 2005

Revenues:Product revenues $421,507 $466,701 $444,303Licensing revenues 9,701 11,059 12,219

Total revenues 431,208 477,759 456,522Other revenues 1,394 1,326 1,446Sales deductions (10,272) (12,071) (11,086)

Total net revenues 422,331 467,014 446,882Cost of sales 266,023 294,360 272,532

Gross profit 156,308 172,653 174,351Selling and marketing expense 108,193 118,511 116,529General and administrative expense (excluding non-cash

compensation expense) 38,847 41,883 38,602Non-cash compensation expense 654 555 863Gain on sale of property (see Note 8) – (5,650) (7,246)Restructuring costs (see Note 25) 8,368 2,347 6,173

Operating income 245 15,008 19,431Interest expense (13,999) (25,699) (16,081)Interest income 1,050 2,121 2,685Foreign exchange gain (loss) (1,103) (606) 2,763Other income (expense), net (18) (97) 125

Income (loss) from operations before income taxes (13,825) (9,274) 8,923Income tax benefit (expense):

Current (2,278) (2,504) (1,873)Deferred 1,446 (25,156) 944

Income tax expense (832) (27,661) (929)

Net income/(loss) $ (14,657) $ (36,935) $ 7,994

Earnings per share – basicNet income (loss) (0.40) (1.02) 0.22

Earnings per share – dilutedNet income (loss) (0.40) (1.02) 0.21

Weighted average shares outstandingBasic 36,285 36,198 36,220Diluted 36,285 36,198 37,467

The accompanying notes are an integral part of the consolidated financial statements.

C O N S O L I D AT E D S TAT E M E N T SO F O P E R AT I O N S

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5B

ased o

n U

.S. G

AA

P

11

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5B

ased o

n U

.S. G

AA

P

12

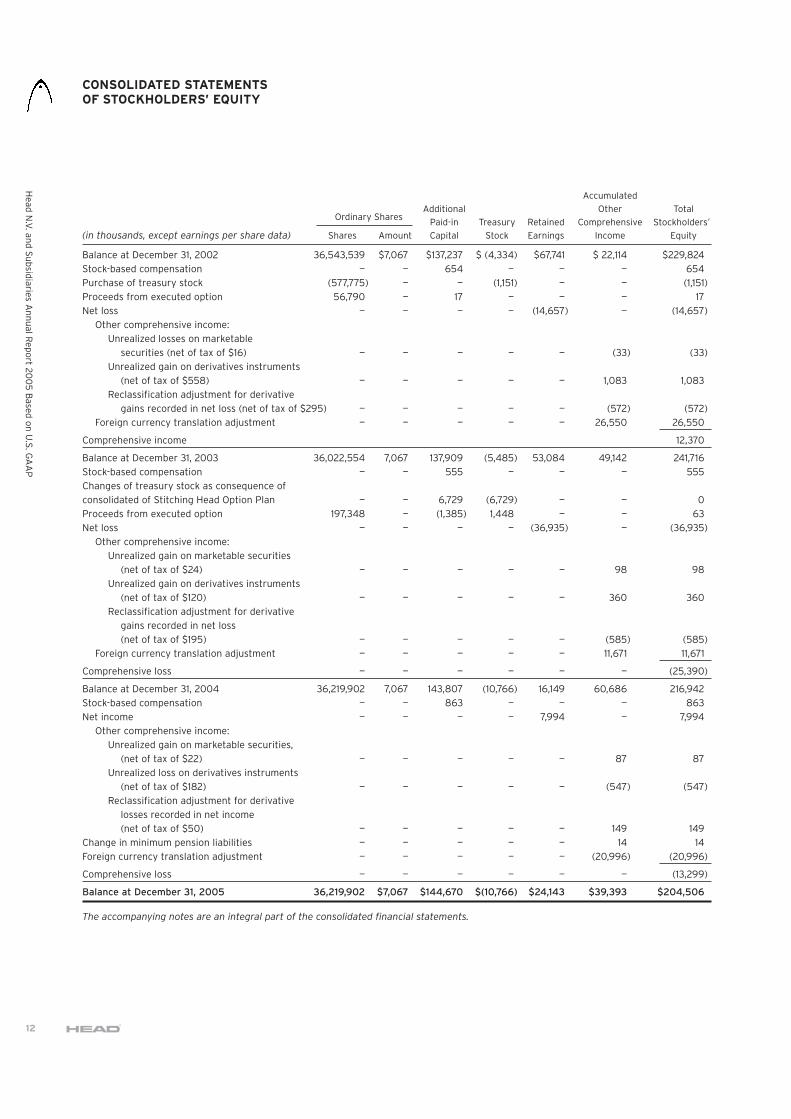

Accumulated

Ordinary SharesAdditional Other Total

Paid-in Treasury Retained Comprehensive Stockholders’(in thousands, except earnings per share data) Shares Amount Capital Stock Earnings Income Equity

Balance at December 31, 2002 36,543,539 $7,067 $137,237 $ (4,334) $67,741 $ 22,114 $229,824

Stock-based compensation — — 654 — — — 654

Purchase of treasury stock (577,775) — — (1,151) — — (1,151)

Proceeds from executed option 56,790 — 17 — — — 17

Net loss — — — — (14,657) — (14,657)

Other comprehensive income:

Unrealized losses on marketable

securities (net of tax of $16) — — — — — (33) (33)

Unrealized gain on derivatives instruments

(net of tax of $558) — — — — — 1,083 1,083

Reclassification adjustment for derivative

gains recorded in net loss (net of tax of $295) — — — — — (572) (572)

Foreign currency translation adjustment — — — — — 26,550 26,550

Comprehensive income 12,370

Balance at December 31, 2003 36,022,554 7,067 137,909 (5,485) 53,084 49,142 241,716

Stock-based compensation — — 555 — — — 555

Changes of treasury stock as consequence of

consolidated of Stitching Head Option Plan — — 6,729 (6,729) — — 0

Proceeds from executed option 197,348 — (1,385) 1,448 — — 63

Net loss — — — — (36,935) — (36,935)

Other comprehensive income:

Unrealized gain on marketable securities

(net of tax of $24) — — — — — 98 98

Unrealized gain on derivatives instruments

(net of tax of $120) — — — — — 360 360

Reclassification adjustment for derivative

gains recorded in net loss

(net of tax of $195) — — — — — (585) (585)

Foreign currency translation adjustment — — — — — 11,671 11,671

Comprehensive loss — — — — — — (25,390)

Balance at December 31, 2004 36,219,902 7,067 143,807 (10,766) 16,149 60,686 216,942

Stock-based compensation — — 863 — — — 863

Net income — — — — 7,994 — 7,994

Other comprehensive income:

Unrealized gain on marketable securities,

(net of tax of $22) — — — — — 87 87

Unrealized loss on derivatives instruments

(net of tax of $182) — — — — — (547) (547)

Reclassification adjustment for derivative

losses recorded in net income

(net of tax of $50) — — — — — 149 149

Change in minimum pension liabilities — — — — — 14 14

Foreign currency translation adjustment — — — — — (20,996) (20,996)

Comprehensive loss — — — — — — (13,299)

Balance at December 31, 2005 36,219,902 $7,067 $144,670 $(10,766) $24,143 $39,393 $204,506

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED STATEMENTSOF STOCKHOLDERS’ EQUITY

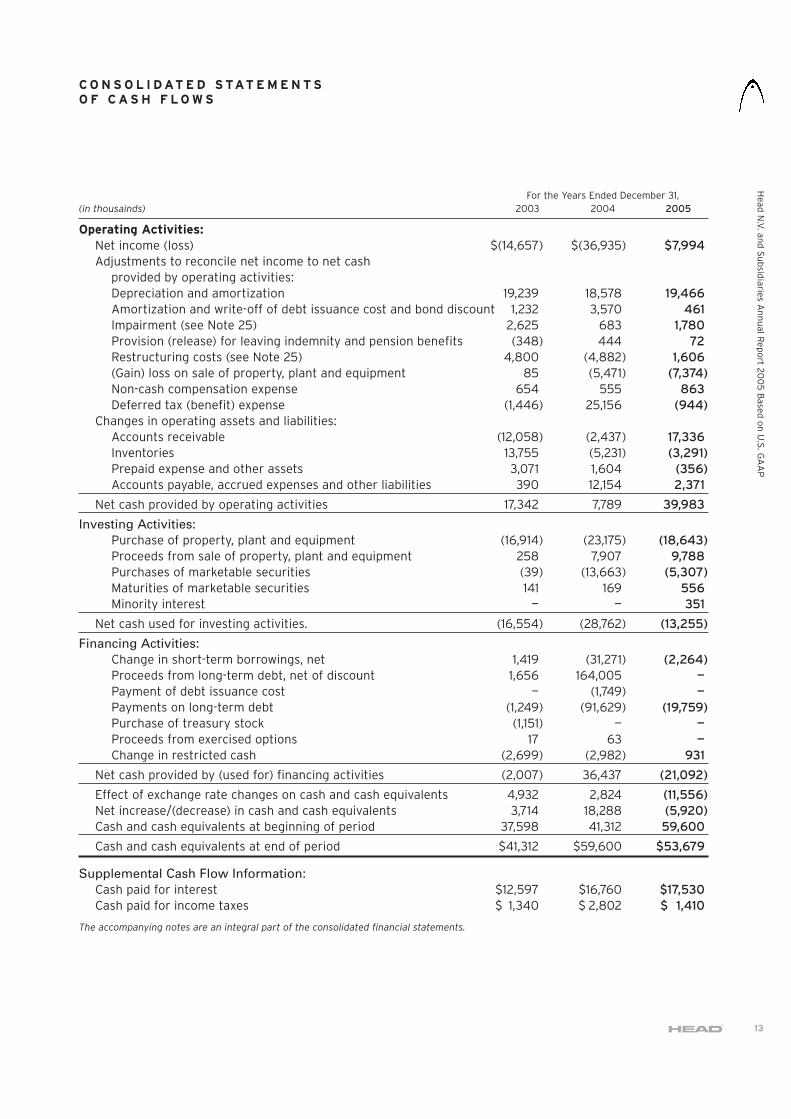

For the Years Ended December 31,(in thousainds) 2003 2004 2005

Operating Activities:Net income (loss) $(14,657) $(36,935) $7,994Adjustments to reconcile net income to net cash

provided by operating activities:Depreciation and amortization 19,239 18,578 19,466Amortization and write-off of debt issuance cost and bond discount 1,232 3,570 461Impairment (see Note 25) 2,625 683 1,780Provision (release) for leaving indemnity and pension benefits (348) 444 72Restructuring costs (see Note 25) 4,800 (4,882) 1,606(Gain) loss on sale of property, plant and equipment 85 (5,471) (7,374)Non-cash compensation expense 654 555 863Deferred tax (benefit) expense (1,446) 25,156 (944)

Changes in operating assets and liabilities:Accounts receivable (12,058) (2,437) 17,336Inventories 13,755 (5,231) (3,291)Prepaid expense and other assets 3,071 1,604 (356)Accounts payable, accrued expenses and other liabilities 390 12,154 2,371

Net cash provided by operating activities 17,342 7,789 39,983

Investing Activities:Purchase of property, plant and equipment (16,914) (23,175) (18,643)Proceeds from sale of property, plant and equipment 258 7,907 9,788Purchases of marketable securities (39) (13,663) (5,307)Maturities of marketable securities 141 169 556Minority interest — — 351

Net cash used for investing activities. (16,554) (28,762) (13,255)

Financing Activities:Change in short-term borrowings, net 1,419 (31,271) (2,264)Proceeds from long-term debt, net of discount 1,656 164,005 —Payment of debt issuance cost — (1,749) —Payments on long-term debt (1,249) (91,629) (19,759)Purchase of treasury stock (1,151) — —Proceeds from exercised options 17 63 —Change in restricted cash (2,699) (2,982) 931

Net cash provided by (used for) financing activities (2,007) 36,437 (21,092)

Effect of exchange rate changes on cash and cash equivalents 4,932 2,824 (11,556)Net increase/(decrease) in cash and cash equivalents 3,714 18,288 (5,920)Cash and cash equivalents at beginning of period 37,598 41,312 59,600

Cash and cash equivalents at end of period $41,312 $59,600 $53,679

Supplemental Cash Flow Information:Cash paid for interest $12,597 $16,760 $17,530Cash paid for income taxes $ 1,340 $ 2,802 $ 1,410

The accompanying notes are an integral part of the consolidated financial statements.

C O N S O L I D AT E D S TAT E M E N T SO F C A S H F L O W S

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5B

ased o

n U

.S. G

AA

P

13

Note 1—BusinessHead N.V. (“Head“ or the “Company”) wasincorporated in Rotterdam, Netherlands, on August24, 1998. With effect from this date, Head HoldingUnternehmensbeteiligung GmbH (“Head Holding“)merged with a wholly owned subsidiary of theCompany in a transaction treated as a merger ofentities under common control and accounted for onan “as if pooling“ basis.

The Company is a global manufacturer and marketerof branded sporting goods serving the skiing, tennisand diving markets. The Company has created oracquired a portfolio of brands – Head (principallyalpine skis, ski boots and snowboard products, tennis,racquetball and squash racquets), Penn (tennis ballsand racquetball balls), Tyrolia (ski bindings), Maresand Dacor (diving equipment).

Head conducts business in Europe (primarily inAustria, Italy, Germany, France, Switzerland, theNetherlands and the United Kingdom), NorthAmerica, and Asia (primarily Japan).

Note 2—Summary of Significant Accounting PoliciesA summary of significant accounting policies used inthe preparation of the accompanying consolidatedfinancial statements is as follows:

Basis of Presentation

The Company and its subsidiaries maintain theiraccounting records in accordance with their localregulations and have made certain adjustments tothese records to present the accompanying financialstatements in conformity with accounting principlesgenerally accepted in the United States of America(“U.S. GAAP“). In addition, the Company publishes itsstatutory financial statements in accordance withDutch corporate regulations.

Effective January 1, 2006, the Company will changeits basis of accounting to International FinancialReporting Standards as adopted by the EU (“IFRS“).The Company will provide a reconciliation for netincome, stockholders’ equity, and significant balancesheet line items reported under IFRS to U.S. GAAP.The differences between IFRS and U.S. GAAP have animpact on the financials. Additionally, the Companywill change its reporting currency from the U.S.dollar to the euro.

Principles of Consolidation

The consolidated financial statements of Headinclude the accounts of all majority-ownedsubsidiaries and entities over which the Company hasfinancial and operating control and variable interestentities in which the Company has determined it isthe primary beneficiary. All intercompanytransactions and balances have been eliminated inconsolidation.

Cash and Cash Equivalents

Cash and cash equivalents comprise of cash andshort-term, highly liquid investments with an originalmaturity of three months or less.

Restricted Cash

Restricted cash comprises of deposits pledged ascollateral on outstanding lines of credit. The amountsare collateralized with one financial institution andearn interest while in deposit.

Inventories

Inventories are stated at the lower of cost or marketwith cost being determined on a first-in first-outbasis (FIFO).

Marketable Securities

Debt securities that the Company has the positiveintent and ability to hold to maturity are classified asheld-to-maturity and reported at amortized cost.Debt and equity securities held principally for sellingin the near term are classified as trading andreported at fair value, with unrealized gains andlosses included in earnings. Debt and equitysecurities not classified as either held-to-maturity ortrading are classified as available-for-sale and arereported at fair value, with unrealized gains andlosses reported in other comprehensive income.

Property, Plant and Equipment

Property, plant and equipment are recorded at costless accumulated depreciation and impairment loss.Additions and improvements that extend the usefullives of the plant and equipment and replacements,major renewals, and betterments are capitalized. Thecost of maintenance, repair and minor renewals areexpensed as incurred. When plant and equipment isretired or otherwise disposed, the cost and relatedaccumulated depreciation are removed from therelated accounts, and any gain or loss on disposition

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

14

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

is recognized in earnings. Depreciation is calculatedusing the straight-line method over the estimateduseful lives of the assets. The Company’s buildingsare depreciated over a period of 30 – 50 years,building improvements are depreciated over a periodof 10-25 years and machinery and equipment isdepreciated over a period of 2-20 years.

Impairment

The Company accounts for impairments inaccordance with the Statement of FinancialAccounting Standards (“SFAS“) No. 144, “Accountingfor the Impairment or Disposal of Long-Lived Assets“(“SFAS 144“). The Company reviews for impairmentwhenever events or changes in circumstancesindicate that the carrying amount of the long-livedasset may not be recoverable. If the fair value is lessthan the carrying amount of the asset, a loss isrecognized in the consolidated statements ofoperations for the difference. The Company’s reviewinvolves comparing current and future cash flows tothe carrying value of the assets. Long-lived assets tobe disposed of, if any, are reported at the lower oftheir carrying amount or fair value less cost to sell.The Company recorded an impairment charge of $2.6million, $0.7 million and $1.8 million for the yearsended December 31, 2003, 2004, and 2005,respectively, and has classified such impairments asrestructuring costs in 2003 and 2005 and as generaland administrative expense in 2004 in theconsolidated income statement.

Goodwill and Other Intangible Assets

Effective January 1, 2002, the Company adoptedSFAS 142, “Goodwill and Other Intangible Assets“(“SFAS 142“). SFAS 142 requires that goodwill andintangible assets with an indefinite life are no longeramortized, but instead are tested for impairment atleast annually in December or more frequently ifevents and changes in circumstances indicate thatthe carrying value may not be recoverable. SFAS142 prescribes a two-phase process for impairmenttesting of goodwill. First, each reporting unit’s(which generally represents one level below anoperating segment) carrying value is compared to itsfair value to determine if an impairment exists.Second, where the reporting unit’s carrying valueexceeds its fair value, an impairment loss is

recognized to the extent that the goodwill carryingvalue exceeds the reporting unit’s implied goodwill,which is calculated as the difference between thereporting unit’s fair value and the fair value of thereporting unit’s recognized and unrecognized assetsand liabilities. The impairment test for indefinite-livedintangible assets requires that an impairment loss berecognized equal to the excess of its carrying valueover its fair value. The Company has goodwill andidentified intangible assets comprising of trademarkswith an indefinite life and land use rights with auseful life of 50 years. For the years endedDecember 31, 2003, 2004 and 2005, no impairmentcharges were recognized for goodwill or indefinitelived intangible assets.

Revenue Recognition

The Company recognizes revenue when persuasiveevidence of a sale arrangement exists, delivery hasoccurred, the sales price is fixed and determinable,and collectibility is reasonably assured. These criteriaare generally met when finished products areshipped to the customers and both title and the risksand rewards of ownership are transferred, or serviceshave been rendered and accepted.

Revenues from licensing agreements are recognizedover the license term for the fixed license revenueportion and based on underlying customer sales onceminimum contractual sales volumes are met for thevariable license revenue portion. Prepaymentsreceived on long-term licensing agreements arerecognized as deferred income.

Provisions are recorded for estimated productreturns at the time revenues are recognized.

Payment terms differ depending on the customer(large distributors, small shops), product line (wintersports is a very seasonal business, as are racquetsports and diving, though to a lesser extent thanwinter sports), country (payment terms vary inaccordance with local practices throughout theworld) and past experiences with customers. It is theCompany’s normal procedure to agree terms oftransactions, including payment terms (60 to 180days), with customers in advance. In the rentalbusiness the Company agrees to payment terms overone year and classifies those long-term trade

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

15

receivables as other non-current assets in theconsolidated balance sheet.

Shipping and handling costs

The Company classifies all amounts billed tocustomers for shipping and handling as otherrevenues. All shipping and handling costs arerecognized as selling and marketing expense in theconsolidated statement of operations. For the yearsended December 31, 2003, 2004 and 2005, theCompany incurred shipping and handling costs of$10.5 million, $12.3 million, and $11.3 million,respectively.

Sales deductions

The Company accrues for customer discounts basedupon estimated refund obligations and classifies allsales incentives, which are earned by the Company’scustomers subsequent to delivery of its product,including cash discounts for volume rebates andother than cash consideration, such as credits thatthe Company’s customer can apply against tradeamounts owed to us as sales deductions.

Translation of Foreign Currency

Finished goods sales to customers in Austria, Italy,Germany, Japan, France, Switzerland, Canada, Spain,Netherlands, United Kingdom and the United Statesof America are generally billed in local currency. Thelocal currency is the functional currency of thesubsidiaries in these countries. Foreign currency(functional currency) assets and liabilities aretranslated into U.S. dollars (the reporting currency)at the exchange rate on the balance sheet date, withresulting translation adjustments recorded in othercomprehensive income. Revenues and expenses aretranslated at average rates prevailing during the year.Foreign exchange gains and losses arising fromtransactions denominated in a currency other thanthe functional currency are included in income. Theeffect of exchange rate changes on intercompanytransactions of a long-term investment nature isincluded in other comprehensive income. Head N.V.has a functional currency of the Euro.

The principal exchange rates against the U.S. dollarused in preparing the consolidated balance sheetsand consolidated statements of operations is as:

1 U.S. Balance Sheet Income Statementdollar = 2004 2005 2003 2004 2005

EUR 0.7342 0.8477 0.8912 0.8082 0.7996CHF 1.1327 1.3182 1.3488 1.2489 1.2371GBP 0.5176 0.5809 0.6134 0.5490 0.5474JPY 102.5255 117.7418 116.5326 108.0565 109.5259CAD 1.2052 1.1634 1.4170 1.3059 1.2142CSK 22.3655 24.5825 28.3583 25.9236 23.9157

Financial Instruments

Statement of Financial Accounting Standards No. 133,“Accounting for Derivative Instruments and HedgingActivities, as amended“ (“SFAS 133“) requires that theCompany record all derivatives on the balance sheet atfair value. The Company uses derivative instruments,specifically foreign exchange forward and optioncontracts, to hedge the foreign exchange risk relatedto its forecasted and firmly committed foreigncurrency denominated cash flows. On the date onwhich a derivative contract is transacted, the Companydesignates the derivative as a hedging instrument aseither a fair value hedge or a cash flow hedge.Changes in derivative fair values that are designated,effective and qualify as fair value hedges arerecognized in earnings as offsets to the relatedearnings effects of changes in fair value of relatedhedged assets, liabilities and firm commitmentsattributable to the hedged risk. Changes in derivativefair values that are designated, effective and qualify ascash flow hedges will be deferred and recorded as acomponent of accumulated other comprehensiveincome (AOCI) until the hedged transactions affectearnings, at which time the deferred gains and losseson the derivative designated as cash flow hedges arerecognized in earnings, and classified in accordancewith the classification of the hedged item. TheCompany excludes the time value component of thederivatives’ change in fair value from the assessmentof hedge effectiveness. The Company enters intohedging relationships to limit the foreign exchangerate risk for periods generally not to exceed one year.For those financial instruments that do not qualify forhedge accounting, the Company recognizes thechanges in the fair value of the instruments in thestatement of operations. The Company does not utilizefinancial instruments for trading or speculativepurposes.

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

16

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Research and Development Costs

Research and development costs are expensed asincurred and are reflected in costs of sales in thestatements of operations. The Company incurredresearch and development expense in the amount of$13.6 million, $15.5 million and $13.8 million for theyears ended December 31, 2003, 2004 and 2005,respectively.

Advertising Costs

Advertising costs are expensed as incurred and arereflected in selling and marketing expense in theconsolidated statements of operations. The Companyincurred advertising costs of $36.9 million, $39.4million and $40.5 million for the years endedDecember 31, 2003, 2004 and 2005, respectively.

Stock-Based Compensation

The Company accounts for its stock option plan usingthe fair value method in accordance with SFAS 123,“Accounting for Stock-Based Compensation“ (“SFAS123“). Under the fair value recognition provisions ofSFAS 123, stock-based compensation cost ismeasured at the grant date based on the fair value ofthe award and is recognized as expense over thevesting period. Determining the fair value of stock-based awards at the grant date requires judgment,including estimating the expected term of stockoptions, the expected volatility of the Company’sstock, expected dividends, and risk-free interestrates.

Debt Issuance Costs

Debt issuance costs are capitalized and amortizedover the term of the debt using the effective interestrate method.

Pension and postretirement benefits

The Company accounts for the costs of pension plansand postretirement benefits in accordance with SFAS87, “Employers’ Accounting for Pensions“ (“SFAS87“) and SFAS 106, “Employers’ Accounting forPostretirement Benefits Other than Pensions“ (“SFAS106“), respectively.

Fair Value Disclosure

The carrying value of the Company’s financialinstruments approximates fair value at December 31,2004 and 2005. The carrying amounts reported inthe consolidated balance sheet for cash and cash

equivalents, accounts receivable, accounts payable,accrued expenses and short-term borrowingsapproximate fair value due to the short maturity ofthese instruments and the floating interest rates ofthe short-term borrowings. The carrying amounts ofmarketable securities are equal to fair value basedon quoted market prices at December 31, 2004 and2005 (see Note 7).

The carrying value of the Company’s senior notes andother long-term debt approximates fair value based oncurrent rates offered and quoted market price of debtwith similar terms.

Income Taxes

The Company utilizes the liability method ofaccounting for deferred income taxes wherebydeferred tax assets and liabilities are recognized toreflect the future tax consequences attributable totemporary differences between the financialreporting bases of existing assets and liabilities andtheir respective tax bases. With the exception ofHead Holding Unternehmensbeteiligung GmbH, all ofthe Company’s Austrian subsidiaries are included in aconsolidated Austrian federal income tax return.Separate provisions for income taxes have beenprepared for the Company’s other subsidiaries.Deferred taxes are calculated by using the prevailingtax rates.

The Company provides a valuation allowance fordeferred tax assets for which it does not considerrealization of such assets to be more likely than not.

Computation of Net Income (Loss) per Share

Net income (loss) per share is computed under SFAS128, “Earnings per Share“ (“SFAS 128“). Basic netincome (loss) per share is computed by dividing thenet income (loss) for the period by the weightedaverage number of ordinary shares outstanding duringthe period. Shares held by The Stichting Head OptionPlan (“Stichting“) are not treated as outstanding forpurposes of the income (loss) per share calculationuntil the related option has been exercised. Diluted netincome (loss) per share is computed by dividing thenet income (loss) for the period by the weightedaverage number of ordinary shares and potentialordinary shares outstanding during the period.Potential ordinary shares are composed of incremental

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

17

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

18

shares issuable upon the exercise of share options,and are included in diluted net income (loss) per shareto the extent such shares are dilutive.

For the years ended December 31, 2003, 2004, and2005, the weighted average shares outstandingincluded in basic net income (loss) per share is36,285,142 shares, 36,197,980 shares, and 36,219,902shares, respectively. For the years ended December 31,2003 and 2004, the number of options that wereoutstanding but not included in the computation ofdiluted net loss per share because their effect wouldhave been anti-dilutive was, 1,347,773 options, and1,278,201 options, respectively. For the year endedDecember 31, 2005 the number of options included inthe computation of diluted net income per share was1,247,119 options.

Comprehensive income (loss)

Comprehensive income (loss) encompasses netincome and changes in the components ofaccumulated other comprehensive income notreflected in the Company's consolidated statementsof operations during the periods presented.

Concentration of business risk

Financial instruments which potentially subject theCompany to significant concentrations of credit riskconsist primarily of cash and cash equivalents,restricted cash, marketable securities and accountsreceivable. The Company places cash with highquality financial institutions. The Company’scustomers are concentrated in the retail industryhowever, concentrations of credit risk with respect totrade accounts receivable are limited due to the largenumber of customers and their dispersion acrossmany geographic areas. The Company generallyperforms credit reviews and sometimes obtainscredit insurance before extending credit.

Use of Estimates

The preparation of financial statements in conformitywith generally accepted accounting principles in theUnited States of America requires management tomake estimates and assumptions that affect thereported amounts of assets and liabilities anddisclosure of contingent assets and liabilities at thedate of the financial statements and the reportedamounts of revenues and expenses during thereporting period. The most significant of these

estimates are impairments, allowances for doubtfulaccounts, product warranties and returns, inventoryobsolescence and valuation allowances on deferredtax assets. On an ongoing basis, managementreviews its estimates based upon currently availableinformation. Actual results could differ from thoseestimates.

Reclassifications

Certain insignificant amounts in the prior yearconsolidated financial statements have beenreclassified to be consistent with the current year’spresentation.

Recent Accounting Pronouncements

In May 2005, the FASB issued Statement of FinancialAccounting Standards No. 154, “Accounting Changesand Error Corrections–a replacement of APB OpinionNo. 20 and FASB Statement No. 3“ (“SFAS 154“), whichchanges the requirement for the accounting andreporting of a change in accounting principle. SFAS 154eliminates the requirement in APB Opinion No. 20,“Accounting Changes,“ to include the cumulative effectof changes in accounting principle in the incomestatement in the period of change. Instead, to enhancethe comparability of prior period financial statements,SFAS 154 requires that changes in accounting principlesare retrospectively applied, unless directed otherwiseby a new pronouncement. SFAS 154 is effective foraccounting changes and corrections of errors made infiscal years beginning after December 15, 2005. TheCompany does not expect the initial adoption of SFAS154 to have a material impact on the Company’sfinancial statements.

In March 2005, the FASB Staff issued InterpretationNo. 47, “Accounting for Conditional Asset RetirementObligations“ (“FIN 47“). FIN 47 clarifies the termconditional asset retirement obligation as used inFASB Statement No. 143, “Accounting for AssetRetirement Obligations“ as well as other issuesrelated to asset retirement obligations. FIN 47 iseffective for fiscal years ending after December 15,2005. The adoption of FIN 47 did not have a materialimpact on the Company’s financial statements.

In December 2004, the FASB issued Statement ofFinancial Accounting Standards No. 123 (revised2004), “Share-Based Payment“ (“SFAS 123R“). SFAS123R addresses the accounting for share-based

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

payment transactions in which an enterprise receivesemployee services in exchange for equityinstruments of the enterprise. It also addressestransactions in which an entity incurs liabilities inexchange for goods and services that are based onthe fair value of the enterprise’s equity instrumentsor that may be settled by the issuance of such equityinstruments. The revised statement generallyrequires that an entity account for those transactionsusing the fair-value-based method, and eliminatesthe intrinsic value method of accounting inAccounting Principles Board Opinion No. 25,“Accounting for Stock Issued to Employees“. SFAS123R requires an entity to recognize the grant-datefair-value of stock options and other equity-basedcompensation issued to employees in the incomestatement. SFAS 123R also requires entities todisclose information about the nature of the share-based payment transactions, the method used toestimate fair value of goods and services received orthe value of the equity instruments granted, and theeffects of those transactions on the financialstatements. On April 14, 2005, the U. S. Securitiesand Exchange Commission (the “SEC“) announcedthat SFAS 123R is to be effective for fiscal yearsbeginning after June 15, 2005 for entities other thansmall business issuers, and applies to all awardsgranted after the required effective date and toawards modified, repurchased, or cancelled after thatdate. The revised statement also applies to theportion of outstanding awards for which the requisiteservice has not yet been rendered based on thegrant-date value of these awards. Retrospectiveapplication is permitted. The SEC issued StaffAccounting Bulletin 107 “Share-Based Payment“(“SAB 107“) in March 2005 that interprets theinteraction of SFAS 123R and certain SEC rules thatmust be applied on the adoption of SFAS 123R. TheCompany will adopt SFAS 123R and SAB 107, usingmodified prospective application, for fiscal year2006. The adoption of SFAS 123R and SAB 107 is notexpected to materially impact the Company’sfinancial statements.

In December 2004, the FASB issued SFAS No. 153,“Exchanges of Non monetary Assets – An Amendmentof APB Opinion No. 29“ (“SFAS 153“) which eliminatesthe exception for non monetary exchanges of similarproductive assets and replaces it with a generalexception for exchanges of non monetary assets thatdo not have commercial substance. The Company isrequired to adopt SFAS 153 for non monetary assetexchanges occurring in the first quarter of 2006. TheCompany is currently in the process of evaluating theimpact of SFAS 153 and does not expect it, to have amaterial impact on its financial statements.

In November 2004, FASB issued SFAS No. 151,“Inventory Costs – an amendment of ARB No. 43,Chapter 4“ (“SFAS 151“). This Statement amends theguidance in ARB No. 43, Chapter 4, “InventoryPricing,“ to clarify the accounting for abnormalamounts of idle facility expense, freight, handlingcosts, and wasted material (spoilage). This Statementrequires that those items be recognized as current-period charges regardless of whether they meet thecriterion of abnormal. In addition, this Statementrequires that allocation of fixed productionoverheads to the costs of conversion be based on thenormal capacity of the production facilities. Theprovisions of this Statement shall be effective forinventory costs incurred during fiscal years beginningafter June 15, 2005. The Company is currently in theprocess of evaluating the impact of SFAS 151 anddoes not expect it to have a material impact on itsfinancial statements.

Note 3—Accounts ReceivableAccounts receivable consist of the following (inthousands):

December 31,2004 2005

Trade debtors $213,724 $182,031Other receivables 12,404 8,695Allowance for doubtful accounts (16,591) (15,511)

Accounts receivable, net $209,536 $175,215

As of December 31, 2004 and 2005, the Companyclassified long-term trade receivables of $1.9 millionand $2.2 million, respectively to other non-currentassets.

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

19

20

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

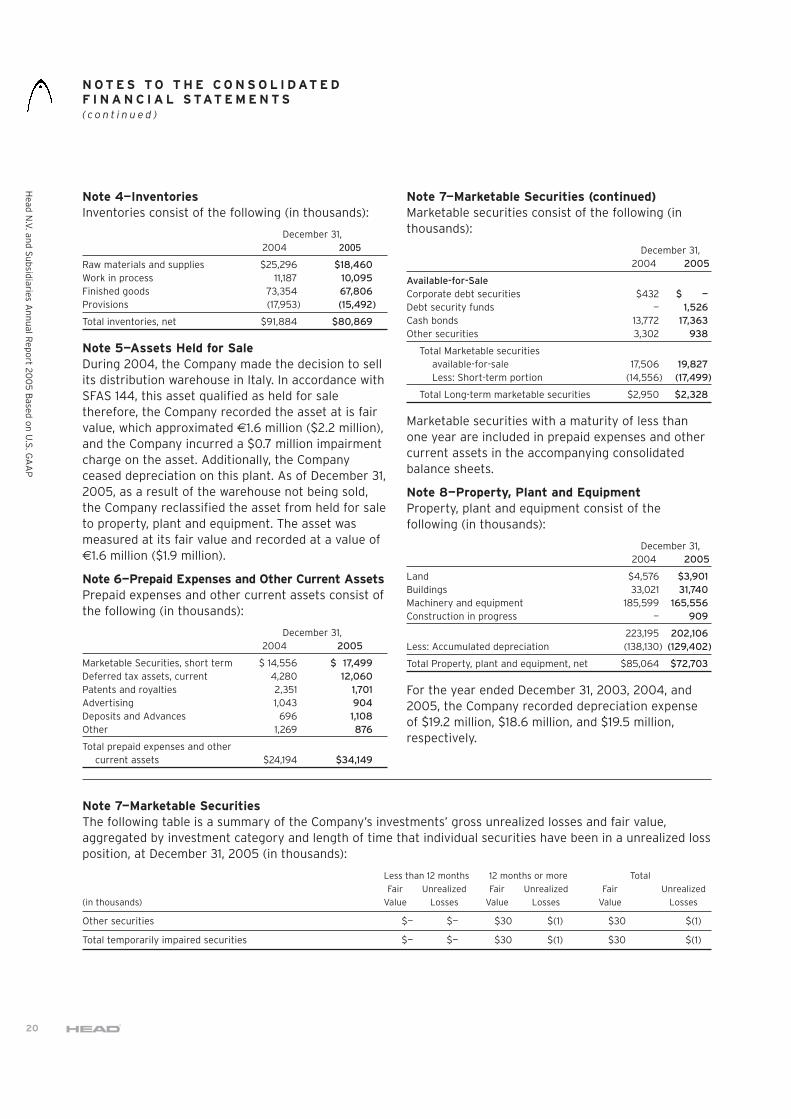

Note 4—InventoriesInventories consist of the following (in thousands):

December 31,2004 2005

Raw materials and supplies $25,296 $18,460Work in process 11,187 10,095Finished goods 73,354 67,806Provisions (17,953) (15,492)

Total inventories, net $91,884 $80,869

Note 5—Assets Held for SaleDuring 2004, the Company made the decision to sellits distribution warehouse in Italy. In accordance withSFAS 144, this asset qualified as held for saletherefore, the Company recorded the asset at is fairvalue, which approximated €1.6 million ($2.2 million),and the Company incurred a $0.7 million impairmentcharge on the asset. Additionally, the Companyceased depreciation on this plant. As of December 31,2005, as a result of the warehouse not being sold,the Company reclassified the asset from held for saleto property, plant and equipment. The asset wasmeasured at its fair value and recorded at a value of€1.6 million ($1.9 million).

Note 6—Prepaid Expenses and Other Current AssetsPrepaid expenses and other current assets consist ofthe following (in thousands):

December 31,2004 2005

Marketable Securities, short term $ 14,556 $ 17,499Deferred tax assets, current 4,280 12,060Patents and royalties 2,351 1,701Advertising 1,043 904Deposits and Advances 696 1,108Other 1,269 876

Total prepaid expenses and othercurrent assets $24,194 $34,149

Note 7—Marketable Securities (continued)Marketable securities consist of the following (inthousands):

December 31,2004 2005

Available-for-SaleCorporate debt securities $432 $ —Debt security funds — 1,526Cash bonds 13,772 17,363Other securities 3,302 938

Total Marketable securities available-for-sale 17,506 19,827Less: Short-term portion (14,556) (17,499)

Total Long-term marketable securities $2,950 $2,328

Marketable securities with a maturity of less thanone year are included in prepaid expenses and othercurrent assets in the accompanying consolidatedbalance sheets.

Note 8—Property, Plant and EquipmentProperty, plant and equipment consist of thefollowing (in thousands):

December 31,2004 2005

Land $4,576 $3,901Buildings 33,021 31,740Machinery and equipment 185,599 165,556Construction in progress — 909

223,195 202,106Less: Accumulated depreciation (138,130) (129,402)

Total Property, plant and equipment, net $85,064 $72,703

For the year ended December 31, 2003, 2004, and2005, the Company recorded depreciation expenseof $19.2 million, $18.6 million, and $19.5 million,respectively.

Note 7—Marketable Securities The following table is a summary of the Company’s investments’ gross unrealized losses and fair value,aggregated by investment category and length of time that individual securities have been in a unrealized lossposition, at December 31, 2005 (in thousands):

Less than 12 months 12 months or more Total

Fair Unrealized Fair Unrealized Fair Unrealized

(in thousands) Value Losses Value Losses Value Losses

Other securities $— $— $30 $(1) $30 $(1)

Total temporarily impaired securities $— $— $30 $(1) $30 $(1)

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

21

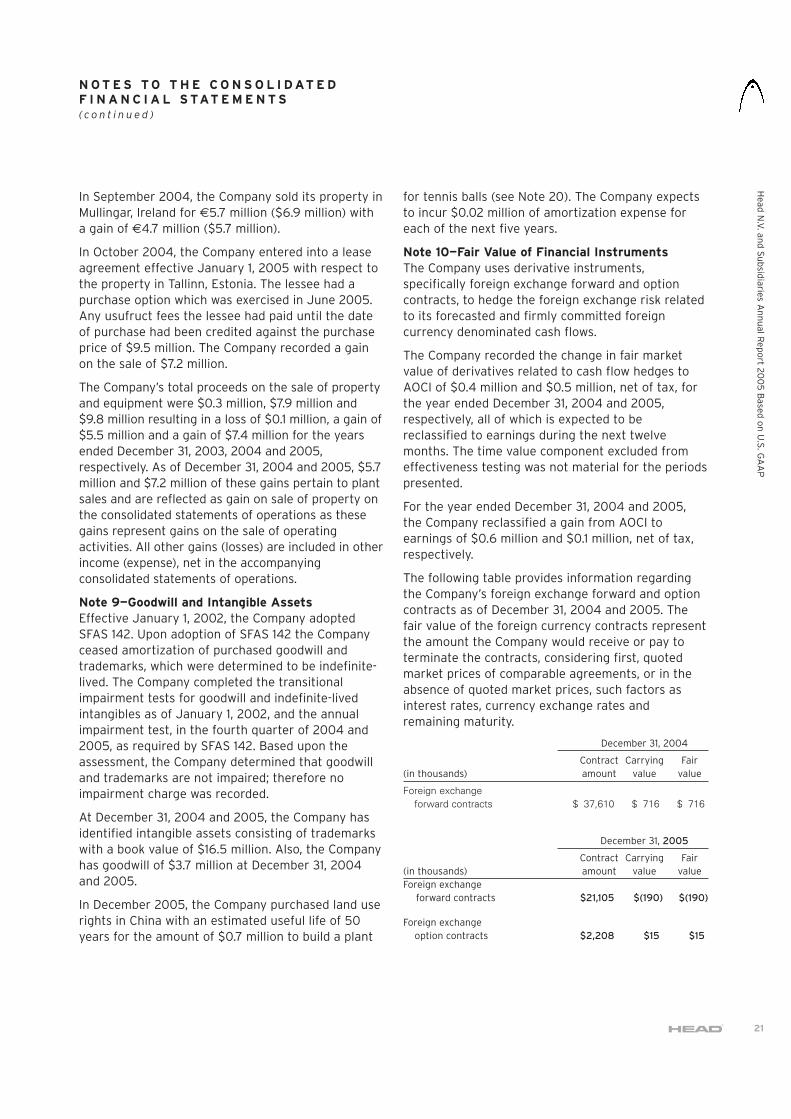

In September 2004, the Company sold its property inMullingar, Ireland for €5.7 million ($6.9 million) witha gain of €4.7 million ($5.7 million).

In October 2004, the Company entered into a leaseagreement effective January 1, 2005 with respect tothe property in Tallinn, Estonia. The lessee had apurchase option which was exercised in June 2005.Any usufruct fees the lessee had paid until the dateof purchase had been credited against the purchaseprice of $9.5 million. The Company recorded a gainon the sale of $7.2 million.

The Company’s total proceeds on the sale of propertyand equipment were $0.3 million, $7.9 million and$9.8 million resulting in a loss of $0.1 million, a gain of$5.5 million and a gain of $7.4 million for the yearsended December 31, 2003, 2004 and 2005,respectively. As of December 31, 2004 and 2005, $5.7million and $7.2 million of these gains pertain to plantsales and are reflected as gain on sale of property onthe consolidated statements of operations as thesegains represent gains on the sale of operatingactivities. All other gains (losses) are included in otherincome (expense), net in the accompanyingconsolidated statements of operations.

Note 9—Goodwill and Intangible AssetsEffective January 1, 2002, the Company adoptedSFAS 142. Upon adoption of SFAS 142 the Companyceased amortization of purchased goodwill andtrademarks, which were determined to be indefinite-lived. The Company completed the transitionalimpairment tests for goodwill and indefinite-livedintangibles as of January 1, 2002, and the annualimpairment test, in the fourth quarter of 2004 and2005, as required by SFAS 142. Based upon theassessment, the Company determined that goodwilland trademarks are not impaired; therefore noimpairment charge was recorded.

At December 31, 2004 and 2005, the Company hasidentified intangible assets consisting of trademarkswith a book value of $16.5 million. Also, the Companyhas goodwill of $3.7 million at December 31, 2004and 2005.

In December 2005, the Company purchased land userights in China with an estimated useful life of 50years for the amount of $0.7 million to build a plant

for tennis balls (see Note 20). The Company expectsto incur $0.02 million of amortization expense foreach of the next five years.

Note 10—Fair Value of Financial InstrumentsThe Company uses derivative instruments,specifically foreign exchange forward and optioncontracts, to hedge the foreign exchange risk relatedto its forecasted and firmly committed foreigncurrency denominated cash flows.

The Company recorded the change in fair marketvalue of derivatives related to cash flow hedges toAOCI of $0.4 million and $0.5 million, net of tax, forthe year ended December 31, 2004 and 2005,respectively, all of which is expected to bereclassified to earnings during the next twelvemonths. The time value component excluded fromeffectiveness testing was not material for the periodspresented.

For the year ended December 31, 2004 and 2005,the Company reclassified a gain from AOCI toearnings of $0.6 million and $0.1 million, net of tax,respectively.

The following table provides information regardingthe Company’s foreign exchange forward and optioncontracts as of December 31, 2004 and 2005. Thefair value of the foreign currency contracts representthe amount the Company would receive or pay toterminate the contracts, considering first, quotedmarket prices of comparable agreements, or in theabsence of quoted market prices, such factors asinterest rates, currency exchange rates andremaining maturity.

December 31, 2004

Contract Carrying Fair(in thousands) amount value value

Foreign exchange forward contracts $ 37,610 $ 716 $ 716

December 31, 2005

Contract Carrying Fair(in thousands) amount value valueForeign exchange

forward contracts $21,105 $(190) $(190)

Foreign exchangeoption contracts $2,208 $15 $15

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

Head

N.V

. and

Su

bsidiaries A

nn

ual R

epo

rt 200

5 B

ased o

n U

.S. G

AA

P

22

The Company formally documents all relationshipsbetween hedging instruments and hedged items, aswell as its risk-management objectives and strategiesfor undertaking various hedge transactions. TheCompany links all derivatives that are designated ashedging instruments in foreign currency cash flowhedges to forecasted transactions or firmcommitments. In accordance with the provision ofSFAS 133, the Company assesses, both at theinception of each hedge and on an on-going basis,whether the derivatives that are designated inhedging qualifying relationship are highly effective inoff-setting changes in fair values or cash flows ofhedged items. When it is determined that a derivativeis no longer highly effective as a hedge, the Companydiscontinues hedge accounting prospectively.

The counterparties to the foreign currency contractsare major international banks. Such contracts aregenerally for one year or less.

Note 11—Short-Term BorrowingsShort-term borrowings consist of the following (inthousands):

December 31,2004 2005

Lines of credit $39,883 $32,735

In the second quarter of 2001, the Company’ssubsidiaries entered into a new financing agreementproviding multiple revolving credit lines with the“Österreichische Kontrollbank” (“OEKB”) which wererenegotiated in 2003, in the total amount of €15.0million ($17.7 million) secured by all Austrian tradereceivables. As of December 31, 2005, the fair valueof trade receivables that serve as collateral for theCompany’s revolving credit lines was $72.7 million. Inaddition, the Company used lines of credit withseveral banks in Canada and Japan of $15.0 millionand had $1.0 million unused credit lines. Theweighted average interest rate on outstanding short-term borrowings was 2.7% and 2.9% as of December31, 2004 and 2005, respectively.

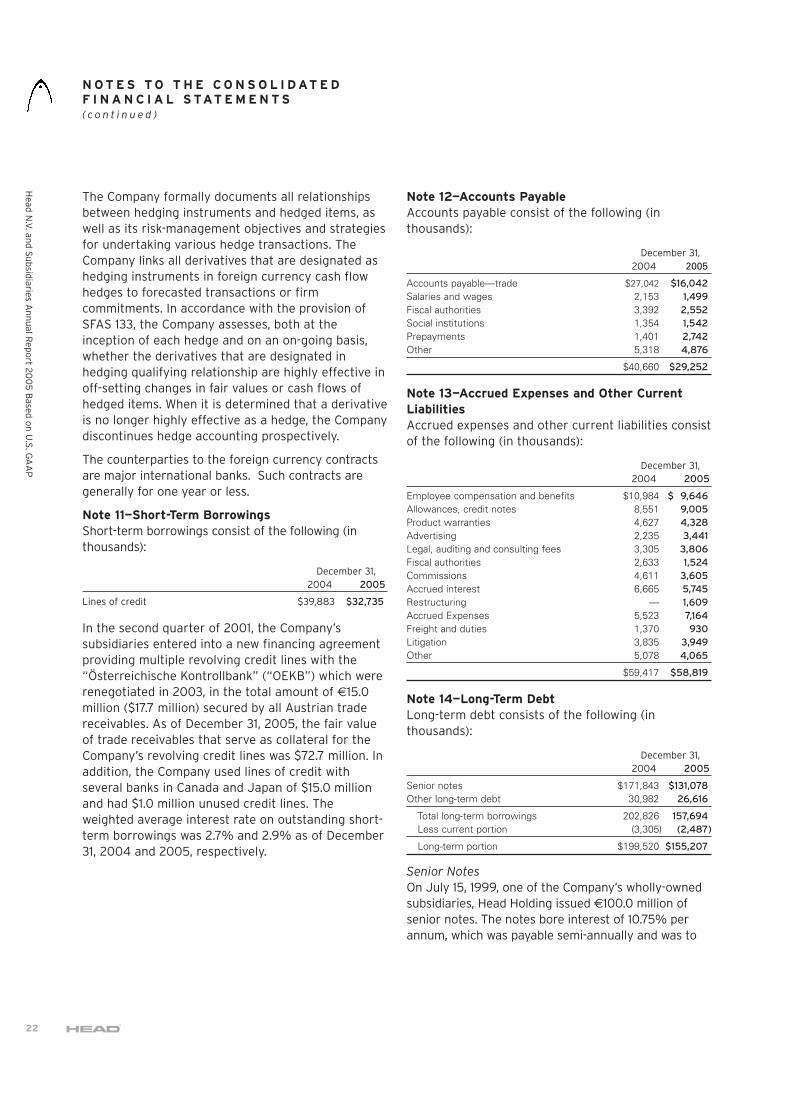

Note 12—Accounts PayableAccounts payable consist of the following (inthousands):

December 31,2004 2005

Accounts payable—trade $27,042 $16,042Salaries and wages 2,153 1,499Fiscal authorities 3,392 2,552Social institutions 1,354 1,542Prepayments 1,401 2,742Other 5,318 4,876

$40,660 $29,252

Note 13—Accrued Expenses and Other CurrentLiabilitiesAccrued expenses and other current liabilities consistof the following (in thousands):

December 31,2004 2005

Employee compensation and benefits $10,984 $ 9,646Allowances, credit notes 8,551 9,005Product warranties 4,627 4,328Advertising 2,235 3,441Legal, auditing and consulting fees 3,305 3,806Fiscal authorities 2,633 1,524Commissions 4,611 3,605Accrued interest 6,665 5,745Restructuring — 1,609Accrued Expenses 5,523 7,164Freight and duties 1,370 930Litigation 3,835 3,949Other 5,078 4,065

$59,417 $58,819

Note 14—Long-Term DebtLong-term debt consists of the following (inthousands):

December 31,2004 2005

Senior notes $171,843 $131,078Other long-term debt 30,982 26,616

Total long-term borrowings 202,826 157,694Less current portion (3,305) (2,487)

Long-term portion $199,520 $155,207

Senior Notes

On July 15, 1999, one of the Company’s wholly-ownedsubsidiaries, Head Holding issued €100.0 million ofsenior notes. The notes bore interest of 10.75% perannum, which was payable semi-annually and was to

N O T E S T O T H E C O N S O L I D AT E DF I N A N C I A L S TAT E M E N T S( c o n t i n u e d )

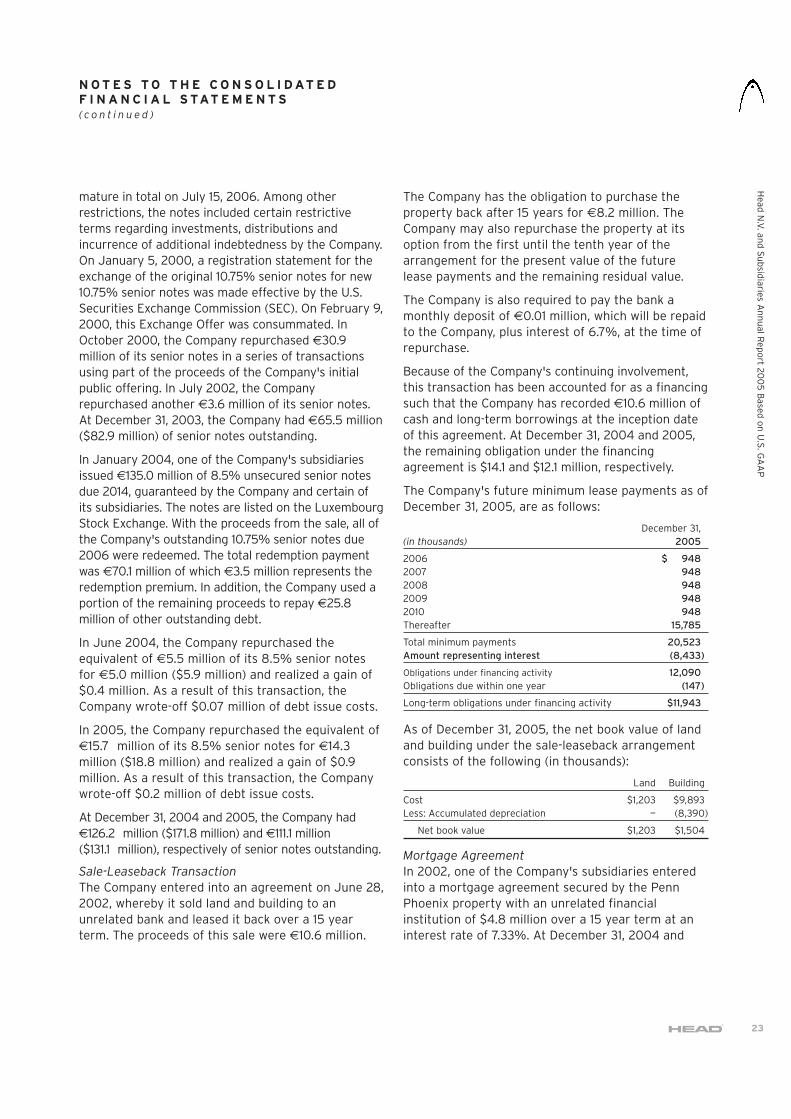

mature in total on July 15, 2006. Among otherrestrictions, the notes included certain restrictiveterms regarding investments, distributions andincurrence of additional indebtedness by the Company.On January 5, 2000, a registration statement for theexchange of the original 10.75% senior notes for new10.75% senior notes was made effective by the U.S.Securities Exchange Commission (SEC). On February 9,2000, this Exchange Offer was consummated. InOctober 2000, the Company repurchased €30.9million of its senior notes in a series of transactionsusing part of the proceeds of the Company's initialpublic offering. In July 2002, the Companyrepurchased another €3.6 million of its senior notes.At December 31, 2003, the Company had €65.5 million($82.9 million) of senior notes outstanding.

In January 2004, one of the Company's subsidiariesissued €135.0 million of 8.5% unsecured senior notesdue 2014, guaranteed by the Company and certain ofits subsidiaries. The notes are listed on the LuxembourgStock Exchange. With the proceeds from the sale, all ofthe Company's outstanding 10.75% senior notes due2006 were redeemed. The total redemption paymentwas €70.1 million of which €3.5 million represents theredemption premium. In addition, the Company used aportion of the remaining proceeds to repay €25.8million of other outstanding debt.

In June 2004, the Company repurchased theequivalent of €5.5 million of its 8.5% senior notesfor €5.0 million ($5.9 million) and realized a gain of$0.4 million. As a result of this transaction, theCompany wrote-off $0.07 million of debt issue costs.

In 2005, the Company repurchased the equivalent of€15.7 million of its 8.5% senior notes for €14.3million ($18.8 million) and realized a gain of $0.9million. As a result of this transaction, the Companywrote-off $0.2 million of debt issue costs.

At December 31, 2004 and 2005, the Company had€126.2 million ($171.8 million) and €111.1 million($131.1 million), respectively of senior notes outstanding.

Sale-Leaseback Transaction