2010-2012 three year plan · the return to pre-crisis profitability levels ... need to increase...

TRANSCRIPT

2010-2012 Three Year Plan

October, 2010

© Copyright Datalogic 2007-2010

DISCLAIMER

This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts and is solely for information purposes. The information set out herein has not been verified by an independent audit company. Neither the Company nor any of its subsidiaries, affiliates, branches, representative offices (the “Group”), as well as any of their directors, officers, employees, advisers or agents (the “Group Representatives”) accepts any responsibility for/or makes any representation or warranty, , p y , g ( p p ) p y p y y p y,express or implied, as to the accuracy, timeliness or completeness of the information set out herein or any other related information regarding the Group, whether written, oral or in visual or electronic form, transmitted or made available. This document may contain forward-looking statements about the Company and/or the Group based on current expectations and opinions developed by the Company, as well as based on current plans, estimates, projections and projects of the Group. These forward-looking statements are subject to significant risks and uncertainties (many of which are outside the control of the Company and/or the Group) which could cause a material difference between forward looking information and actual future resultswhich could cause a material difference between forward-looking information and actual future results. The information set out in this document is provided as of the date indicated herein. Except as required by applicable laws and regulations, the Company assumes no obligation to provide updates of any of the aforesaid forward-looking statements. Under no circumstances shall the Group and/or any of the Group Representatives be held liable (for negligence or otherwise) for any loss or damage howsoever arising from any use of this document or its contents or otherwise in connection with the document or the aforesaid forward-looking statements. This document does not constitute an offer to sell or a solicitation to buy or subscribe to Company shares and neither this entiredocument or a portion of it may constitute a recommendation to effect any transaction or to conclude any legal act of any kind whatsoever. This document may not be reproduced or distributed, in whole or in part, by any person other than the Company.By viewing and/or accepting a copy of this document, you agree to be bound by the foregoing limitations.

© Copyright Datalogic 2007-2010 22

THE GROUP

THREE YEAR PLAN

FINANCIAL DATA

APPENDIX

© Copyright Datalogic 2007-2010 33

Investment Highlights

Worldwide leader in the Automatic Data Capture (ADC)p ( )and Factory Automation (FA) markets

Proven track record in facing and overcominginternational crisisinternational crisis

Strong growth potential in emerging markets Sustainable margins recovery thanks to recentlyg y y

completed efficiency plan, stable product pricing andvolume improvements

Strong cash generator to sustain future growth Strong cash generator to sustain future growth Experienced management team with proven capability in

company integration

© Copyright Datalogic 2007-2010 44

Datalogic at a Glance

World-class producer of bar code readers, datacollection mobile computers, RFID and visionsystemssystems

Datalogic offers innovative solutions for acomprehensive range of applications in the

f t i t il t t ti & l i timanufacturing, retail, transportation & logisticsmarkets

Founded in 1972 in Bologna, Italyg , y

Listed on the STAR Segment of the Italian StockExchange since 2001

About 2,000 employees

Direct presence in 30 countries worldwide selling Direct presence in 30 countries worldwide sellingto +100 countries

+1,000 partners worldwide

© Copyright Datalogic 2007-2010 5

Datalogic Management Team

© Copyright Datalogic 2007-2010 6

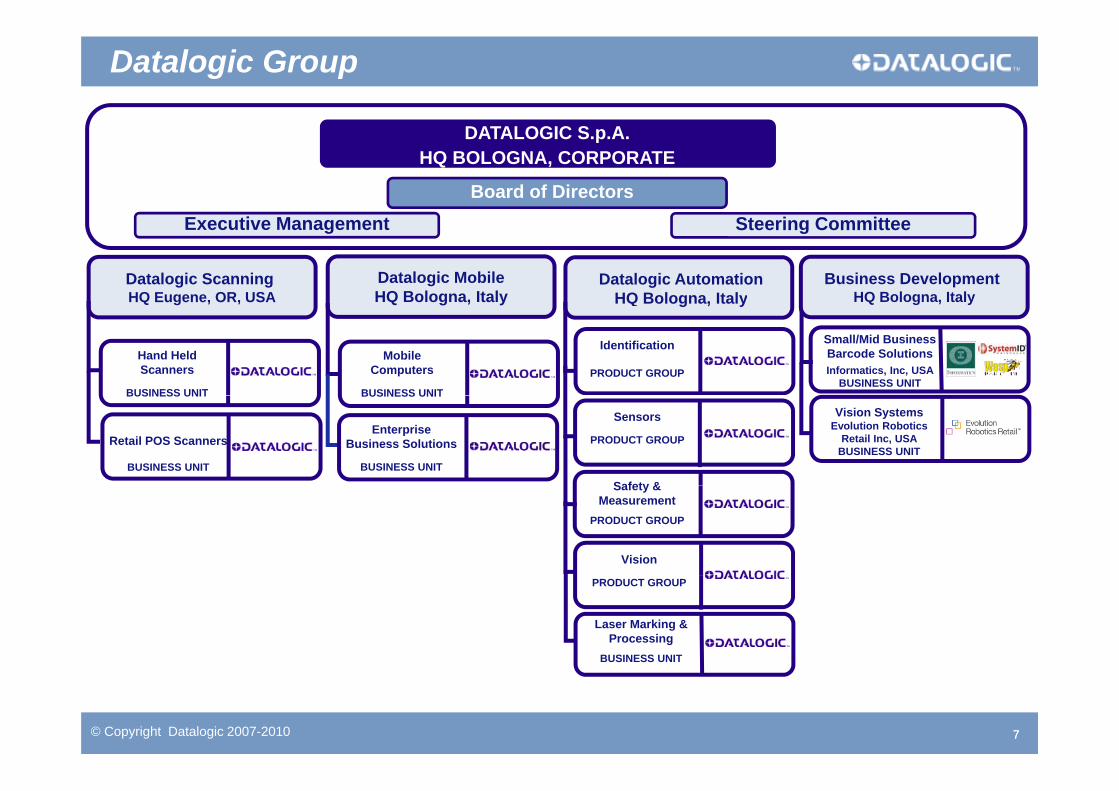

DATALOGIC S A

Datalogic Group

DATALOGIC S.p.A.HQ BOLOGNA, CORPORATE

Board of Directors

Datalogic Scanning HQ Eugene, OR, USA

Datalogic Automation HQ Bologna, Italy

Datalogic MobileHQ Bologna, Italy

Business Development HQ Bologna, Italy

Executive Management Steering Committee

Hand Held Scanners

BUSINESS UNIT

g , y

Identification

PRODUCT GROUPMobile

Computers

BUSINESS UNIT

Small/Mid BusinessBarcode SolutionsInformatics, Inc, USA

BUSINESS UNITBUSINESS UNIT

Retail POS Scanners

BUSINESS UNIT

Sensors

PRODUCT GROUP

Safety &

Enterprise Business Solutions

BUSINESS UNIT

BUSINESS UNIT

Vision SystemsEvolution Robotics

Retail Inc, USABUSINESS UNIT

Safety & Measurement

PRODUCT GROUP

Vision

PRODUCT GROUP

Laser Marking & Processing

BUSINESS UNIT

© Copyright Datalogic 2007-2010 77

A Wide Geographical FootprintH110 REVENUES – TOTAL €191M - BREAKDOWN BY AREA

EUROPE 37%

NORTH AMERICA 27%

ITALY 11%

APAC 12%

SOUTH AMERICA 13%

Direct presence in 30 countries worldwide7 Manufacturing Plants 9 R&D Centers

© Copyright Datalogic 2007-2010

7 Manufacturing Plants 9 R&D Centers

8

A History of Growth

Acquisition of Informatics

Completed transformation intoListing on the Milan St k E h Acquisition of Laservall

Inc. (TX, U.S.A.)

Acquisition of PSC Inc. (OR, U.S.A.)

Acquisition of Evolution Robotics Retail, USA

Completed transformation into 3 divisions: Scanning, Mobile, and Automation

Acquisition of Datasensor SpA

Stock Exchange

Acquisition of Minec AB (Sweden)

Acquisition of Laservall SpA (AO, I)

REVENUES: ~14% 2001-2009 CAGRREVENUES: ~14% 2001-2009 CAGRH110 SALES REVENUES (191 M Euro) UP BY 28% COMPARED TO 2009

2001 2002 2003 20052004 2006 2007 2008 2009 H1 2010

© Copyright Datalogic 2007-2010 99

A solid track record to overcome the crisis…

The restructuring and efficiency program launched in the first half of 2009 enabled the Group The restructuring and efficiency program launched in the first half of 2009 enabled the Group to significantly lower its fixed cost structure and to create the basis for future growth

Right-sized cost structure; not just temporary measures Quarter to quarter growth trend confirms Company’s turnaround successfully completed and g y y

the return to pre-crisis profitability levels Robust free cash generation Gained market shares, consolidating leadership in reference markets, fully exploiting all the

t iti f th

PROFITABILITY TRENDWORLDWIDE MARKET SHARE

opportunities of growth

6 2

11,6

7,18,7

10,6

15,3

9 3%10,1%

11,8%

15,1%

31,8% 30,6% 31,5%

1,32,9

6,2

-0,5

4,3

,

5,7%

9,3%

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

12,3% 12,3%14,6%

-6,8

-10,2-0,7%

E B T fit/(l ) b f T E B I T D A EBITDA M i

2007 2008 2009

POS Retail Scanners Industrial Stationary Barcode Scanners

© Copyright Datalogic 2007-2010 10

E.B.T.profit/(loss) bef. Taxes E.B.I.T.D.A. EBITDA MarginPOS Retail Scanners Industrial Stationary Barcode Scanners

…leveraging strong commercial partnerships…

More than 1,000 partners worldwide

Longstanding relations with the biggest retailers, couriers and automotive manufacturers in the world

Over 350 installations of Self Shopping in Europe

Over 1,000 reading stations installed in more than 100 airports worldwide

© Copyright Datalogic 2007-2010 11

Relentless investments in R&D have provided new fuel to beat reference market growth without

…and cutting edge technology and innovationp g

price policy Research & Development investments at > €25 million in 2009 or 8% on sales

+30 new products in 2009, +22 in 2010 up to date A large and growing portfolio of 890 patents: +70 patents in 2009 9 Research & Development Centers

Acquisition of the American company Evolution Robotics Retail, leader in the field of visualpattern recognition that will be a key technology building block in Datalogic industrial focusedpattern recognition that will be a key technology building block in Datalogic industrial focusedbusinesses; this acquisition adds an innovative technological capability protected by 5 patents

PRODUCT INNOVATION PATENTS PORTFOLIO

20

32

23

23 23

35

27

33

682761 789

867 885

1012

9

20

12

6

9 8

17

11

85 6 5

11

6

10

23

13

17 16

22

14 1316

23

264 283328 342

682

4 5

2 1

4 532 1 0 1 0 1

3 24

0

4

0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

PRODUCT UPDATES NEW LINE OF PRODUCTS

2001 2002 2003 2004 2005 2006 2007 2008 2009

© Copyright Datalogic 2007-2010 12

PRODUCT UPDATES NEW LINE OF PRODUCTS

BREAKTHROUGH INNOVATION TOTAL DEVELOPMENTS

T GTHE GROUP

T Y PTHREE YEAR PLAN

FINANCIAL DATA

APPENDIX

© Copyright Datalogic 2007-2010 1313

Reference Market Growth Trends

GLOBAL TRENDS Technology shifts: analogue to digital; wireless technology Globalization of the world economyy Increased focus on gaining efficiencies and cost reduction in supply chains Greater safety and security concerns

VALUE TO THE CUSTOMER Better information, faster Improved real time decision making Operate more efficiently reducing operating expenses Operate more efficiently reducing operating expenses Increase safety, security and compliance Measurable, sustainable ROI

+8% average market growth* 2010 through 2012

© Copyright Datalogic 2007-2010 1414

+8% average market growth* - 2010 through 2012*Company’s estimates based on available market trend data

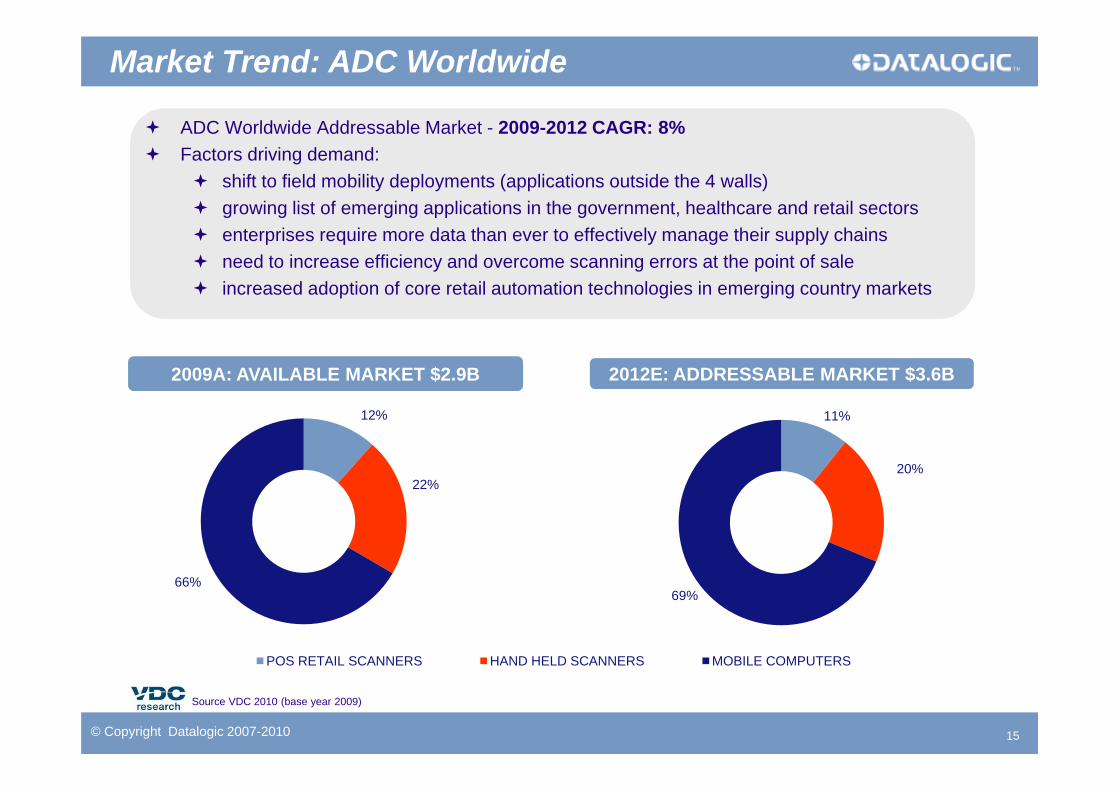

ADC Worldwide Addressable Market 2009 2012 CAGR: 8%

Market Trend: ADC Worldwide

ADC Worldwide Addressable Market - 2009-2012 CAGR: 8% Factors driving demand:

shift to field mobility deployments (applications outside the 4 walls) growing list of emerging applications in the government, healthcare and retail sectorsg g g g pp g , enterprises require more data than ever to effectively manage their supply chains need to increase efficiency and overcome scanning errors at the point of sale increased adoption of core retail automation technologies in emerging country markets

2009A: AVAILABLE MARKET $2.9B 2012E: ADDRESSABLE MARKET $3.6B

12%

22%

11%

20%22%

66%

POS RETAIL SCANNERS HAND HELD SCANNERS MOBILE COMPUTERS

69%

© Copyright Datalogic 2007-2010

POS RETAIL SCANNERS HAND HELD SCANNERS MOBILE COMPUTERS

15

Source VDC 2010 (base year 2009)

Factory Automation Worldwide Available Market - 2009-2012 CAGR: 8% V f t d i d t ith t ti l dditi l k t th $2 7B

Market Trend: Factory Automation Worldwide

Very fragmented industry with potential additional markets worth $2.7B Factors driving demand:

delocalization of manufacturing plants increasing the demand for traceability of processes and goods

$

supply chain streamlining; increased focus on cost containment, productivity, quality controlnew regulations (e.g. traceability, safety and security) increased adoption of technological solutions in industrial segments in emerging markets

2012E ADDRESSABLE MARKET $5 6B

19%12% 8%

7%

4%

2009A: AVAILABLE MARKET $2.3B 2012E: ADDRESSABLE MARKET $5.6B

13% 47%9%

10%

14%

41%15%

10%

19% 19%

IDENTIFICATION (Source:DLA*VDC 2010) SENSOR (Source:VDC 2010)

SAFETY (Source:DLA*VDC 2008) VISION (Source:DLA*AIA 2008 &EMVA 2010)

10%

Inductive Sensors

Safety Controllers & Laser ScannersVision ASMV Low-end

© Copyright Datalogic 2007-2010

LASERMARKING (Source: DLA* Penwell 2010) POTENTIAL ADDITIONAL MARKETSs o S o e d

Fiber Lasermarking

16

Source: * Market Researches and Datalogic Automation Management's Best Estimate

Datalogic Positioning in ADC Available Market

2009 ADC A il bl M k t 9 8% M k t Sh2009 ADC Available Market: 9.8% Market Share

Datalogic market shares

POS Retail Scanners#1 WW 31 5% kt h

>30%#1 WW – 31.5% mkt share

Handheld Scanners#1 in EMEA - 30.7% mkt share #3 WW -15 9% mkt sharerk

et S

hare

>10%

#3 WW -15.9% mkt share

Mobile Computers#4 in EMEA - 7.9% mkt share #4 WW - 4.0% mkt share20

09 M

ar

4%

$100 M $300 M $950 M

<2%

$200 M$50 M

2009 ADC Available Market including POS Retail Scanners, Hand Held Scanners and Mobile Computers (Hand Held and PDA) segments

2009 Revenues

© Copyright Datalogic 2007-2010 1717

Source VDC 2010 (base year 2009)

Datalogic Positioning in FA Available Market

2009 FA (Factory Automation) Available Market:2009 FA (Factory Automation) Available Market: 3.7% Market Share

Datalogic market shares(*)

Industrial Stationary Se

>12%

Scanners#2 in EMEA - 29% mkt share#3 WW - 14.6% mkt share

arke

t Sha

re 10%

2009

Ma

5%

<2%

$50 M $100 M $200 M $300 M

2009 FA Available Market including Barcode Scanners, Imagers, RFID Industrial Readers and Tags, Photoelectric Sensors, Safety Light Curtains, Smart Cameras/Vision Sensors and Low Power Lasermarking segments

2009 Revenues

© Copyright Datalogic 2007-2010 18

Source (*) VDC 2010 - Market Researches and Datalogic Automation Management's Best Estimate

Datalogic 2010-2012 Growth Strategy

MARKET EXPANSION PRODUCT INNOVATION

F t j k t Invest 7-8% in R&D spend to launch new products and platforms

Become a value-added solutions provider developing software for intelligent products

Focus on Vision and Imaging technologies

Focus on two major markets: ADC (Automatic Data Capture) Factory Automation (FA)

External growth through M&A activities, mainly in the Factory Automation market

Achievingdouble digit

Focus on Vision and Imaging technologies 25% of sales from new products (*)

mainly in the Factory Automation market Gain market share with no price erosion

double-digitReturn on Equity

Expand emerging market (BRIC) presence through strategic alliances and foreign

World class performance through the global adoption of best in class Supply Chaing g g

investments Increase penetration in large mature

markets in North America and Western Europe addressing High-End products/solutions and higher technology

adoption of best in class Supply Chain Management

Improve operational efficiency and leverage industrial global footprint

Activate scale economies

INTERNATIONAL GROWTH EFFICIENCY IMPROVEMENTS

products/solutions and higher technology businesses

© Copyright Datalogic 2007-2010 1919

(*) Sales derived from new products released during the past 2 calendar years divided by total sales

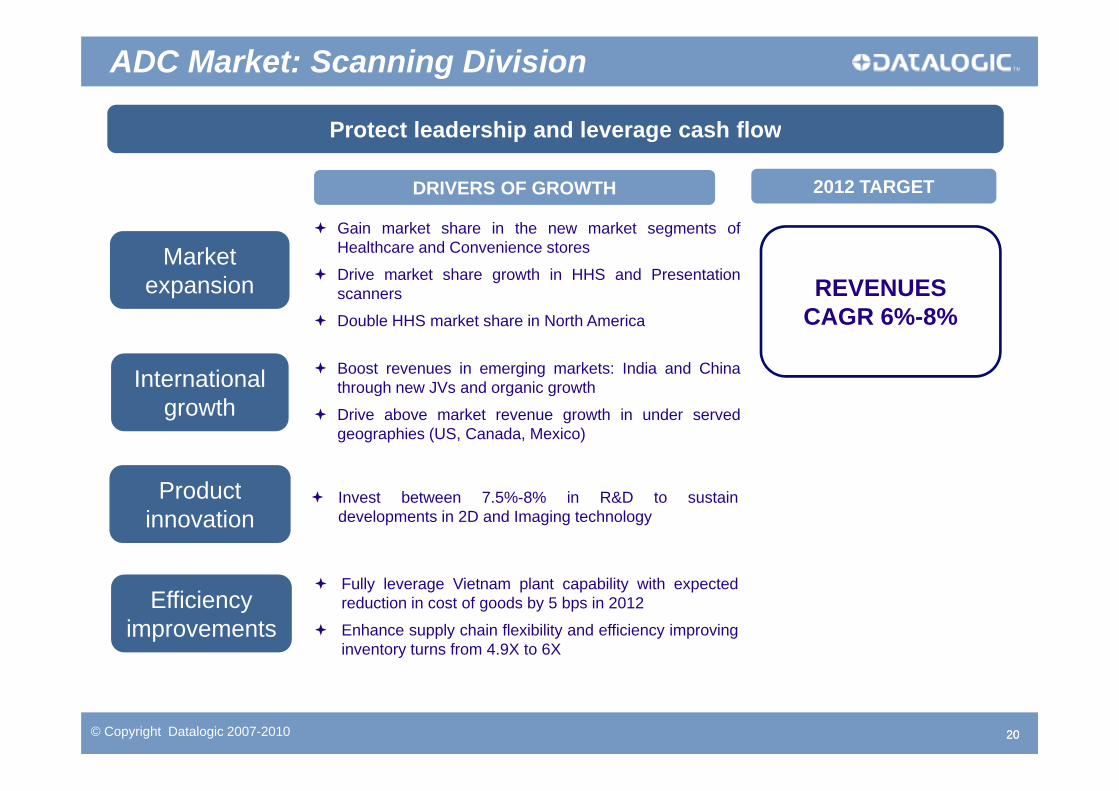

ADC Market: Scanning Division

Protect leadership and leverage cash flow

2012 TARGET DRIVERS OF GROWTH

Protect leadership and leverage cash flow

Market expansion

Gain market share in the new market segments ofHealthcare and Convenience stores

Drive market share growth in HHS and Presentationscanners REVENUES

Double HHS market share in North America

International Boost revenues in emerging markets: India and Chinathrough new JVs and organic growth

CAGR 6%-8%

growthg g g

Drive above market revenue growth in under servedgeographies (US, Canada, Mexico)

P d t Invest between 7.5%-8% in R&D to sustaindevelopments in 2D and Imaging technology

Productinnovation

Efficiency improvements

Fully leverage Vietnam plant capability with expectedreduction in cost of goods by 5 bps in 2012

Enhance supply chain flexibility and efficiency improvinginventory turns from 4.9X to 6X

© Copyright Datalogic 2007-2010 2020

ADC Market: Mobile Division

2012 TARGETDRIVERS OF GROWTH 2012 TARGET DRIVERS OF GROWTH

Lean, fast and flexible technology integrator able to compete with giants

Market i

Outperform market trend by increasing penetration in thefastest growing market of Retail (In store applications)

Aggressively address Transportation & Logistics (T&L)

2012 TARGET DRIVERS OF GROWTHDRIVERS OF GROWTH

REVENUESexpansion Aggressively address Transportation & Logistics (T&L)market (Warehouse and Field Force Automationapplications)

Focus on large regions: increase penetration in North

REVENUESCAGR 13%-16%

Internationalgrowth

America, doubling market share

Strengthen position in Western Europe

Promote Self Shopping solutions in US market

Invest 7% in R&D to develop products and platforms inRetail and T&L markets

Develop the innovative and highly profitable SelfShopping Solution in Retail market

Productinnovation

pp g

Efficiency improvements

Adopt state of the art Supply Chain Management to gainefficiency and leverage the industrial global footprint

© Copyright Datalogic 2007-2010 2121

improvements Become best in class in working capital management

FA Market: Automation Division

2012 TARGET DRIVERS OF GROWTH 2012 TARGET DRIVERS OF GROWTH

Become a Leading Player in Factory Automation and Trasportation & Logistics

Market expansion

Potential for external growth to achieve critical mass in amore fragmented market

Address a huge market worth approx. $6B in 2012,

DRIVERS OF GROWTH

REVENUESexpansion

Internationalth

focusing on Vision and Safety segments

Boost revenues in emerging markets – South Americaand Asia - through organic growth

D i b k t i th i t k t

REVENUESCAGR 10%-12%

growth

P d t Keep a challenging 8% in R&D spend to sustain

developments in the promising markets of Vision and

Drive above market organic growth in mature marketaddressing High End products and solutions

Productinnovation

developments in the promising markets of Vision andSafety

Drive the portfolio offer from just products to value addedsolutions with software designed to satisfy customersrequirements

Efficiency improvements

Adopt state of the art supply chain management to gainefficiency and leverage the industrial global footprint

Dramatically improve working capital throughrationalization of SKU’s and warehouse processes

© Copyright Datalogic 2007-2010 2222

rationalization of SKU s and warehouse processesreengineering

Group Three Year Plan Target

420-430 60-65

REVENUES GROWTH EBITDA GROWTH

€mln €mlnCAGR 11%

312

19 7

14-15%CAGR >45%

CAGR 11%

19,7

6,3%

2009 2012 2009 2012

EBITDA Ebitda Margin

2012 organic revenues target in the range of 420-430 million Euro, CAGR at 11%

2012 EBITDA target in the range of 60-65 million Euro, CAGR >45%

R&D investments between 7%-8% of revenues per year

© Copyright Datalogic 2007-2010 2323

Group Three Year Plan Target

PFN* EVOLUTION ROE GROWTHPFN EVOLUTION ROE GROWTH

€mln

100

20 85-90

18% 20%100

12%

18%-20%

25-35

2009 EVO Acquisition **

Cash Flow 2012 2008 2009 2012

Strong cash generation and expected debt reduction

-9,6%

Investment in capex stable at around 2.5% of revenues per year

ROE target around 20%

© Copyright Datalogic 2007-2010 2424

* PFN gross of expected dividends ** Acquisition of Evolution Robotics Retail in July 2010

Group Three Year Plan – Potential Upside

POTENTIAL UPSIDE ON REVENUES

420-430€mln

CAGR 11%

520-530Potential upside from acquisitions

312

2009 2012

The 3 – Year Plan target is based on organic growth driven by: Innovation: launch of new products and platforms addressing Imaging and Vision technologies Strengthening of positioning in reference markets Expansion in the emerging market (BRIC) p g g ( ) Improvement of productivity and efficiency leveraging Vietnam plant capability and adopting

a state-of-the-art supply chain management

Potential for further upside is not incorporated:p p A proven track record in integrating acquired companies Strong commitment for external growth Strong cash flow generation and Group financial soundness allow to target additional €100

mln revenues by external growth

© Copyright Datalogic 2007-2010 2525

y g Scouting for M&A activity to reinforce positioning in the FA market is currently ongoing

T GTHE GROUP

T Y PTHREE YEAR PLAN

FINANCIAL DATA

APPENDIX

© Copyright Datalogic 2007-2010 2626

Strong Recovery in Profitability

Strong growth of revenues and recovery in profitability confirms Company’s turnaround compared to the negative trend of the beginning of FY09

EBITDA margin returns to pre-crisis levels Profitability has traced a steady trend of recovery mainly thanks to the cost cutting and efficiency Profitability has traced a steady trend of recovery, mainly thanks to the cost cutting and efficiency

program launched in the first half of last year, which enabled the Group to significantly lower its fixed cost structure

Jump of net profit to €11.3 mln from a loss of €14.5 mln Improvement of the Net Financial Position Improvement of the Net Financial Position

€000 H1 10 H1 09 Var % Quarterly Growth

Revenues 190,832 149,112 28.0%

Gross Operating Margin (GOM) 87,534 61,504 42.3%73,1 76,0 76,0

86,9 89,5

101,3€ mln

Ord.Operating Profit (EBITANR*) 20,145 (3,457) n.m.

Operating Profit (EBIT) 18,484 (13,490) n.m.

EBT 17,823 (16,995) n.m. 4 3 7,1 8,8 10,615,3

4 0 7 712,4,8 3 ( 6,995)

Net Income 11,255 (14,538) n.m.

EBITDA 25,923 3,804 n.m.

-0,54,3 7,1

-4,1 0,64,0 5,7 7,7

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

Revenues EBITDA EBITANR

© Copyright Datalogic 2007-2010 2727

*Ebitnar: earnings before interest, taxes, acquisition and non recurring

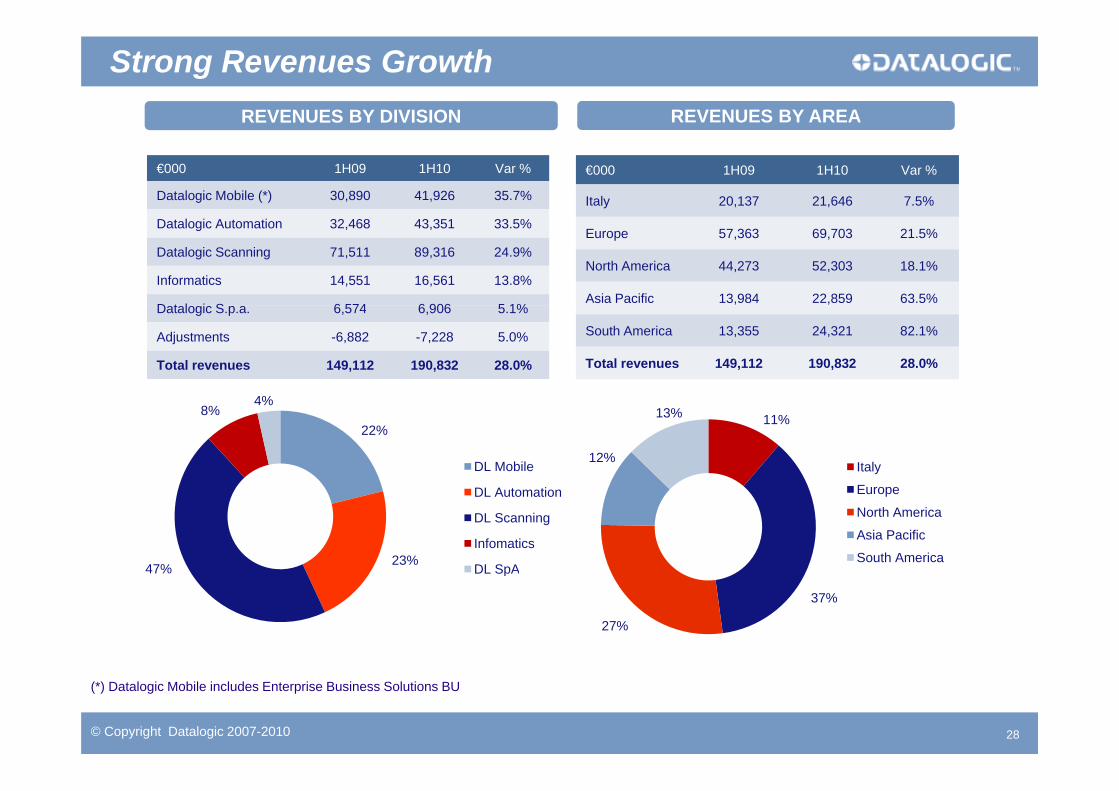

Strong Revenues GrowthREVENUES BY DIVISION REVENUES BY AREA

€000 1H09 1H10 Var %

Datalogic Mobile (*) 30,890 41,926 35.7%

€000 1H09 1H10 Var %

Italy 20,137 21,646 7.5%

Datalogic Automation 32,468 43,351 33.5%

Datalogic Scanning 71,511 89,316 24.9%

Informatics 14,551 16,561 13.8%

D t l i S 6 574 6 906 5 1%

Europe 57,363 69,703 21.5%

North America 44,273 52,303 18.1%

Asia Pacific 13,984 22,859 63.5%

4%

Datalogic S.p.a. 6,574 6,906 5.1%

Adjustments -6,882 -7,228 5.0%

Total revenues 149,112 190,832 28.0%

South America 13,355 24,321 82.1%

Total revenues 149,112 190,832 28.0%

22%8%

4%

DL Mobile

11%

12%

13%

Italy

E

23%47%

DL Automation

DL Scanning

Infomatics

DL SpA

Europe

North America

Asia Pacific

South Americap

37%

27%

© Copyright Datalogic 2007-2010 28

(*) Datalogic Mobile includes Enterprise Business Solutions BU

Segment Reporting

REVENUES EBITDA(€mln)

REVENUES EBITDA

191

36%33%

25% 28%

2637,0%(€mln)

31 32

72149

42 43

89

25%

14%

5% 3 4

11

3

13,1%11,4% 12,7% 13,9%

13,6%31 32

15 717 7

5%

Mobile Automation Scanning Informatics DL SpA Total Group

H1 2009 H1 2010 YoY rev increase

0

-2

2 2 3 45 5 2 3

Mobile Automation Scanning Informatics DL SpA Total Group

H1 2009 H1 2010 % on H1 2010 rev

R&D COSTS TWC

7,1%7,6%

6,7% 6 6%

76 7327,0% 27,3%(€mln) (€mln)

6

14

6

136,7% 6,6%

26 29 31

14,3%17,1%

9 6%

19,1%

34

0,3 0,3

3 3

0,3 0,1

1,8% 1,7%

Mobile Automation Scanning Informatics DL SpA Total Group

15

26

3 3

12

23

3 4

9,6%

Mobile Automation Scanning Informatics DL SpA Total Group

© Copyright Datalogic 2007-2010 29

Mobile Automation Scanning Informatics DL SpA Total Group

H1 2009 H1 2010 % on H1 2010 rev

Mobile Automation Scanning Informatics DL SpA Total Group

H1 2009 H1 2010 % on H1 2010 rev

(€000)V l l /Mi +23 835

EBITANR * - 1H10 vs. Last Year(€000)

Exch rate on sales + 309

Exch rate on DCOGS - 215

Exch rate on Op Exp - 127

Vol.sales/Mix +23,835

Service sales + 811

4,931 -33 -2,614740

2,917 20,145

24,636

Act June 09 Price Vol. Sales/Mix New Prod. Exch rate € vs $

Oper Exp Informatics Other Act June '10

-3,457

-6,975

$

Other revenues - 580

Other variable costs - 2,495

Notes:

The Exchange rate variance has been calculated on Sales/COGS/Operating expenses originally denominated in USD ($). The variance was the result of the differencebetween H1 ’10 Actual (1,327) and H1 ’09 Actual (1,33) €/USD exchange rate.

Direct Cogs +5,992

© Copyright Datalogic 2007-2010 30

Therefore, this variance does not include the exchange rate effect on competitive scenario.

For Informatics has been considered its overall impact on the EBITANR.

Consolidated Balance Sheet€000 At 31/12/2009 At 30/06/2010

Intangible fixed assets 39,621 41,555

Goodwill 87,081 99,394

Tangible fixed assets 50,822 51,888

Non Consolidated investments 2 675 3 035Non Consolidated investments 2,675 3,035

Other fixed assets 23,181 25,298

Total Fixed Assets 203,380 221,170

Net trade account receivables 65,455 77,691

ST account payables (43,816) (51,968)

Inventory 39,082 47,266

Trade Working Capital 60,721 72,989

Other current receivables 17,512 15,174

Other ST payables and provision for risk & future charges (34,989) (41,549)

Net Working Capital 43,244 46,614

Other LT payables (17 373) (19 225)Other LT payables (17,373) (19,225)

Employees’ severance Indemnity (7,739) (7,101)

LT provision for risk & future charges (4,319) (7,300)

Net Invested Capital 217,193 234,158p , ,

Equity 116,695 142,055

Net Financial Position (100,498) (92,103)

E h t 1 4406 1 2271

© Copyright Datalogic 2007-2010 3131

Exchange rate 1.4406 1.2271

Net Debt Analysis: December ’09 - June ’10

100,498 19,34112,576 3,898 569

2,973 1,974 11,044

92,103

(€000)

Acc. Receivable - 12,544

Inventory - 8,188

Net Debt Dec 09 Operating cash Ch Trade NWC Capex Purch /sale own Non-recurring out- tax payments Other Net Debt June 10

Acc. Payable + 8,152

Net Debt Dec 09 Operating cash Flow

Ch Trade NWC Capex Purch./sale own shares

Non-recurring out-flows

tax payments Other Net Debt June 10

Positive Cash flow Negative Cash Flow

Net Income + 11,255

Deprec&Amort + 7,777

Provision

© Copyright Datalogic 2007-2010 32

(severance and bad debt) + 308

T GTHE GROUP

T Y PTHREE YEAR PLAN

FINANCIAL DATA

APPENDIX

© Copyright Datalogic 2007-2010 3333

Stock and GovernanceSHAREHOLDERS’ STRUCTUREDATALOGIC PRICE PERFORMANCE

6.4%6.3%

4 2

4,4

4,6

4 2

4,4

4,6

Price for Datalogic S.p.A. (IT) in EUR as of 27/09/10

20.2%3,6

3,8

4,0

4,2

3,6

3,8

4,0

4,2

67.1%

Hydra S p A Free Float2,8

3,0

3,2

3,4

2,8

3,0

3,2

3,4

Hydra S.p.A. Free Float

Tamburi Investment P. Treasury Shares

M k t S t STAR MTA

ago 09 set 09 ott 09 nov 09 dic 09 gen 10 feb 10 mar 10 apr 10 mag 10 giu 10 lug 10 ago 10 set 10

Datalogic S.p.A. Italy FTSE Italia All-Share (Rebased)

P i (S t b 28th 2010) € 4 38Market Segment: STAR MTA

Ticker: DAL

Reuters Code: DAL.MI

Price (September 28th 2010): € 4.38

Market Cap (September 28th 2010): € 253 mln

Specialist: Intermonte SIM

Bloomberg Code: DAL IM

Number of Shares Outstanding: 58,446,491

Share Par-Value: 0.52€ each

Auditing Company: Ernst & Young

© Copyright Datalogic 2007-2010 3434

Datalogic Scanning Division

Handheld Scanners#1 in EMEA, 30.7% mkt share

#3 Worldwide, 15.9% mkt share

POS Retail Scanners#1 Worldwide, 31.5% mkt share

,

Over 5 million Datalogic handheld scanners have been sold since 1998

d h b h b

Datalogic Magellan Scanner/Scales have been installed by every one of

and have been chosen by over 30,000 customers

the Top Ten Retailers worldwide

Scanning Division: 146.8M€ in 2009, 47% of Group Sales

© Copyright Datalogic 2007-2010 3535

Source 2010 (base year 2009)

Datalogic Mobile Division

Mobile Computers#4 in EMEA, 7.9% mkt share

#4 Worldwide, 4.0% mkt share

Datalogic Mobile – EBS Self Shopping Solutions

Over 350 installations in Europe!#1 in Italy with 140 installations

#1 in France with 110 installations#1 in Belgium with 90 installations

A full range of professional mobile solutions dedicated to the main target application fields: Warehousing, Field Force Automation and Retail In-Store solutions

Mobile Division: 67.9M€ in 2009, 22% of Group Sales

© Copyright Datalogic 2007-2010 3636

Source 2010 (base year 2009)

Datalogic Automation Division

Laser Marking & Processing Business Unit

Sensors Product Group

Industrial Stationary Scanners#2 i EMEA 29% kt h

IdentificationProduct Group

Vi i

#2 in EMEA, 29% mkt share#3 Worldwide, 14.6% mkt share

VisionProduct Group

Safety & Measurement

Product Group

A wide range of cutting edge solutions helping industries streamline processes in industrial A wide range of cutting edge solutions helping industries streamline processes in industrialand logistics applications

Hundreds of applications for the major courier and logistics operators, +1,000 readingstations installed in 100 airports worldwide

Automation Division: 66.7M€ in 2009, 21% of Group Sales

© Copyright Datalogic 2007-2010 3737

Source 2010 (base year 2009)

Business Development - Informatics

Complete Range of Easy-To-Use Barcoding Solutions

Barcoding solutions for the millions of Small – Medium Business that increase productivity and profitability

Based in the US, serving over 155 thousand small and medium businesses!

Informatics, US:30 5M€ in 2009 10% of Group Sales

© Copyright Datalogic 2007-2010 3838

30.5M€ in 2009, 10% of Group Sales

.

Thank You!This presentation contains statements that are neither reported financial results nor other historical information. These statements are forward-looking

statements. These forward-looking statements rely on a number of assumptions and are subject to a number of risks and uncertainties, many of which are

outside the control of Datalogic S.p.A., that could cause actual results to differ materially from those expressed in or implied by such statements, such asg p y p p y

future market conditions, currency fluctuations, the behavior of other market participants and the actions of governmental and state regulators

© 2010 Datalogic S.p.A. - All rights reserved. • Protected to the fullest extent under U.S. and international laws. • Copying, or altering of this document is

prohibited without express written consent from Datalogic S.p.A. Datalogic and the Datalogic logo are registered trademarks of Datalogic S.p.A. in many

Datalogic S.p.A.Via Candini 2

countries, including the U.S.A. and the E.U. All other brand and product names may be trademarks of their respective owners.

Via Candini, 240012 Lippo di Calderara di RenoBologna – ItalyTel. +39 051 3147011 – Fax +39 051 3147205E-mail [email protected]

© Copyright Datalogic 2007-2010 3939

www.datalogic.com

We Welcome Your Questions!We Welcome Your Questions!

© Copyright Datalogic 2007-2010 4040