2013-05 restructurings responses

TRANSCRIPT

Montréal, le 9 mai 2013 Tim Beauchamp, directeur Comptabilité du secteur public 277, rue Wellington Ouest Toronto (Ontario) M5V 3H2 Monsieur, Vous trouverez ci-joint les commentaires du Groupe de travail technique Secteur public - Comptabilité dans le secteur public de l’Ordre des comptables professionnels agréés du Québec concernant l’énoncé de principes « Restructurations ». Nous vous serions reconnaissants de nous faire parvenir une copie de la traduction anglaise de nos commentaires. Veuillez prendre note que ni l’Ordre des comptables professionnels agréés du Québec, ni quelque personne que ce soit ayant participé à la préparation des commentaires ne peuvent être tenus responsables relativement à leur utilisation et ils ne sont tenus à aucune garantie de quelque nature que ce soit découlant de ces commentaires, comme décrit dans le déni de responsabilité joint à la présente. Veuillez agréer, Monsieur Beauchamp, l’expression de mes sentiments distingués. Représentante du Groupe de travail technique Secteur public - Comptabilité dans le secteur public, Annie Smargiassi CPA, CA p. j. Déni de responsabilité et commentaires

DÉNI DE RESPONSABILITÉ

Les documents préparés par le Groupe de travail technique Secteur public - Comptabilité dans

le secteur public de l’Ordre des comptables professionnels agréés du Québec (Ordre) ci-après

appelés les « commentaires », sont fournis selon les conditions décrites dans la présente, pour

faire connaître leur opinion sur des énoncés de principes, des documents de consultation, des

exposés-sondages préliminaires ainsi que des exposés-sondages publiés par le Conseil des

normes comptables, le Conseil des normes d’audit et de certification, le Conseil sur la

comptabilité dans le secteur public, le Conseil sur la gestion des risques et la gouvernance et

d’autres organismes.

Les commentaires fournis par ce comité ne doivent pas être utilisés comme substitut à des

missions confiées à des professionnels spécialisés. Il est important de noter que les lois, les

normes et les règles sur lesquelles sont émis les commentaires peuvent changer en tout temps

et que, dans certains cas, les commentaires écrits peuvent être sujets à controverse.

Ni l’Ordre, ni quelque personne que ce soit ayant participé à la préparation des commentaires ne

peuvent être tenus responsables relativement à l’utilisation de ces commentaires et ils ne sont

tenus à aucune garantie de quelque nature que ce soit découlant de ces commentaires. Les

commentaires donnés ne lient pas, par ailleurs, les membres du Groupe de travail technique

Secteur public - Comptabilité dans le secteur public, l’Ordre ou, de façon plus particulière, le

Bureau du syndic de l’Ordre.

La personne qui se réfère ou utilise ces commentaires assume l’entière responsabilité de sa

démarche ainsi que tous les risques liés à l’utilisation de ceux-ci. Elle consent à exonérer l’Ordre

à l’égard de toute demande en dommages-intérêts qui pourrait être intentée par suite de toute

décision qu’elle aurait pu prendre en fonction de ces commentaires. Elle reconnaît également

avoir accepté de ne pas faire état de ces commentaires reçus via le Groupe de travail dans les

avis exprimés ou les positions prises.

COMMENTAIRES DU GROUPE DE TRAVAIL TECHNIQUE SECTEUR PUBLIC - COMPTABILITÉ DANS LE SECTEUR PUBLIC DE L’ORDRE DES COMPTABLES PROFESSIONNELS AGRÉÉS DU QUÉBEC RELATIFS À L’ÉNONCÉ DE PRINCIPES « RESTRUCTURATIONS ».

MANDAT DU GROUPE DE TRAVAIL

Le Groupe de travail technique Secteur public - Comptabilité dans le secteur public de l'Ordre des

comptables professionnels agréés du Québec a comme mandat notamment de recueillir et de

canaliser le point de vue des praticiens exerçant en cabinet et de membres œuvrant dans les affaires,

dans les services gouvernementaux, dans l'industrie et dans l'enseignement ainsi que le point de vue

d’autres personnes concernées œuvrant dans des domaines d’expertise connexes.

Pour chaque exposé-sondage ou autre document étudié, les membres du Groupe de travail

technique mettent leurs analyses en commun. Les commentaires ci-dessous reflètent les points de

vue exprimés et, sauf indication contraire, ces commentaires ont fait l'objet d'un consensus parmi les

membres du Groupe de travail ayant participé à cette analyse.

Les commentaires formulés par le Groupe de travail ne font l'objet d'aucune sanction de l'Ordre. Ils

n'engagent pas la responsabilité de celui-ci.

COMMENTAIRES GÉNÉRAUX

Les membres du groupe de travail ont indiqué que les restructurations les plus fréquentes au Québec,

dans le secteur public, surviennent entre des entités sous contrôle communs ou apparentées.

Comme la norme proposée sur les opérations entre entités apparentées et l’énoncé de principes sur

les restructurations excluent totalement les restructurations sous contrôle commun, leurs besoins les

plus urgents ne sont pas comblés. Les membres sont d’avis que la norme proposée, qui traite

d’opérations peu fréquentes, ne devrait pas être priorisée au détriment d’un projet portant sur les

restructurations d’entités apparentés.

COMMENTAIRES SPÉCIFIQUES

1. Estimez-vous qu’il est nécessaire de se pencher sur les questions de comptabilité et

d’information qui se posent aux entités en restructuration? Dans l’affirmative, veuillez indiquer

les questions qui devraient être abordées et les raisons pour lesquelles il conviendrait de

fournir des indications à leur égard.

Les membres ont indiqué que le besoin de directives se situe surtout au niveau des restructurations

entre entités sous contrôle commun ou avec des entités apparentées. Selon eux, lorsque les

restructurations impliquent des parties qui ne sont pas apparentées, les négociations amènent

généralement à conclure à la présence d’un acquéreur, et à se référer à d’autres chapitres du Manuel

du secteur public.

Concernant les restructurations entre entités apparentées ou sous contrôle commun, les membres

ont conclu que les questions à aborder touchent les bases de mesure à utiliser, les circonstances

reliées aux modes de comptabilisation ainsi que les informations à fournir au sujet de ces opérations.

2. La définition d’une opération de restructuration est-elle pratique et applicable? Dans

l’affirmative, pouvez-vous fournir des exemples d’opérations passées auxquelles

s’appliquerait cette définition?

Oui, les membres ont indiqué que la définition semble pratique et applicable. Par contre, ils n’ont pas

été en mesure d’identifier des exemples récents (avec des entités autres que des apparentés) qui

répondraient à cette définition.

Les représentants du secteur des municipalités ont par contre indiqué que la définition pourrait

s’appliquer aux fusions municipales imposées par le Gouvernement du Québec en 2002 ainsi qu’aux

reconstitutions de certaines de ces municipalités survenues quatre ans plus tard, soit en 2006.

Les participants du réseau de la santé, ont pour leur part indiqué que certains centres de santé sont

nés de fusion ou intégration d’entités du secteur public et d’entités du secteur privé, subventionnés ou

conventionnés. Ils ont toutefois indiqués que ces restructurations n’étaient pas les plus fréquentes.

Les membres ont noté également que l’utilisation de certaines expressions, différentes et non

définies, mine leur compréhension des principes proposés. Ainsi, la définition du paragraphe .24 fait

référence à l’absence de « contreparties importantes » alors que les paragraphes .38, .39, .40 et .41

font référence à des éléments additionnels tels les « compensations substantielles sans contrepartie

importante » ou encore les « compensations symboliques ». Le tableau du paragraphe .38 ne semble

pas être en lien avec la définition proposée du paragraphe .24.

Ils se sont questionnés également sur les situations pour lesquelles aucune contrepartie n’est

transférée à la date de la restructuration, mais pour lesquelles des contreparties additionnelles sont

données subséquemment à la restructuration, pour assurer la prestation de services ou pour

compenser des réductions de valeurs. Ils croient que des indications additionnelles devraient être

fournies dans ces circonstances pour déterminer si la contrepartie subséquente répond à la définition

ou non du paragraphe .24.

3. Estimez-vous que l’utilisation de la valeur comptable est appropriée aux fins de l’évaluation

initiale des actifs et des passifs transférés lors d’une restructuration?

Les membres ont indiqué que lorsque les opérations sont effectuées avec des entités non

apparentées, les valeurs comptables ne sont pas toujours disponibles au prix d’un effort raisonnable.

Certains membres ont indiqué qu’ils avaient un malaise à évaluer des opérations avec des entités

non apparentées à une valeur autre que la valeur d’échange.

D’autres membres proposent que le champ d’application indique clairement que les propositions

visent uniquement les opérations de restructuration entre entités du secteur public et qu’elles ne

visent pas des opérations de restructuration avec des entités hors du secteur public ou avec des

partenariats. Les membres entrevoient des difficultés d’interprétation au sujet des propositions

actuelles, de la façon dont elles sont libellées.

Certains membres ont demandé des précisions concernant la valeur comptable. En effet, ils se

questionnent à savoir si certains actifs pourraient être transférés à une valeur comptable nette ou

plutôt si les valeurs brutes (actifs et provisions pour dépréciation ou dotation à l’amortissement

cumulé par exemple) devraient être utilisées.

4. Selon vous, le fait que l’entité restructurée soit une entité nouvellement constituée ou une

entité existante devrait-il déterminer la façon de comptabiliser l’opération de restructuration,

ainsi que les autres exigences de présentation et d’information, tel qu’il est indiqué dans le

Tableau 5?

Non, les membres ne sont pas d’accord à ce que la forme des opérations ait une préséance sur leur

substance et se sont donc démontrés en désaccord avec ces propositions. Ils croient que cette façon

d’aborder les normes pourrait favoriser une manipulation des opérations et de la façon dont elles sont

structurées de façon à obtenir le traitement le plus favorable pour les entités visées. Ils proposent que

les traitements comptables et les informations à fournir concernant les opérations de restructurations

ne soient pas différenciés par la présence ou non d’une nouvelle entité dans le cadre de l‘opération.

5. Êtes-vous d’accord pour que la communication d’informations sur la situation des entités

en restructuration, ou des activités transférées, avant la date de restructuration soit

encouragée, mais non exigée?

Une majorité des membres consultés se sont montrés en faveur d’encourager, mais non d’exiger la

communication d’informations sur les situations ou activités qui existaient avant la date de

restructuration. Certains membres se sont montrés en désaccord avec la présentation de ce type

d’information, notamment à cause du facteur d’imputabilité, alors que d’autres encouragent fortement

l’exigence de divulgation.

6. Pouvez-vous fournir des exemples de questions découlant de restructurations ou qui y sont

liées, qu’elles soient couvertes ou non dans le présent énoncé de principes (par exemple, les

compensations, et les opérations et accords connexes à la restructuration)? Veuillez fournir

des commentaires sur la nécessité ou non de l’élaboration d’indications sur les questions

dont l’énoncé de principes ne traite pas.

Les questions non couvertes, pour lesquelles les membres aimeraient obtenir des indications

supplémentaires, sont expliquées à la question 2 et portent sur les contreparties subséquentes, la

clarification des notions de contreparties et de compensations, ainsi que l’identification des entités

visées par les propositions.

7. Pouvez-vous indiquer les incidences de l’application des principes proposés dans le

présent énoncé de principes sur la comptabilisation des opérations et sur l’information

financière dans le secteur public?

Les membres sont d’avis que l’application des principes proposés n’aurait pas d’incidence importante

sur leur pratique, car la majorité des opérations visées sont traitées par d’autres chapitres du Manuel

du secteur public ou concernent des opérations de restructuration avec des entités sous contrôle

commun ou apparentés.

8. Seriez-vous intéressé à participer à un groupe de travail ou à un comité consultatif si le

CCSP décidait d’en former un?

Oui, des membres se sont montrés intéressés à participer à un groupe de travail ou à un comité

consultatif, dans la mesure où les opérations entre entités apparentées et les opérations sous

contrôle commun sont analysées.

Click here to submit

Response Questionnaire

To be considered, comments must be received by

May 17, 2013

Restructurings

Statement of Principles

PSAB welcomes comments on all aspects of the Statement of Principles.

This form is not intended to constrain your response. Each text box will accommodate your full comments.

You are able to save and forward this form to others in your organization for review prior to submission.

Name: Armand Capisciolto, National Accounting Standards Partner

Organization: BDO Canada LLP

E-mail: [email protected]

General comments:

1. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on those issues.

We beleive there is a need to address accounting and reporting issues of a restructuring entity. These transactions are not uncommon and during certain periods of time they are frequent. Currently there is diversity in practice.

2. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition?

We agree that the definition a restructuring transaction is practical and workable. Examples of past transactions with application of this definition that we have seen as a firm are amalgamations of school boards and local governments.

3. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring?

We agree that carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring.

4. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5?

No, we do not agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring is recognized. The accounting for these transactions should not be determined based on legal form, but instead should be based on the substance of the transaction. We prefer the accounting treatment for the newly formed entity and believe that the restructuring transaction for both newly formed entities and existing entities should go through equity and not profit and loss.

5. Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required?

We agree information about the restructuring entities and transferred operations prior to the restructuring date should be encouraged but not required.

6. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed.

At this time we do not have any specific examples.

7. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting?

The problem with current public sector reporting is that there is no guidance on how to account for these type of transactions. As a result, there is diversity in practice and we have seen situations in the past where people have applied accounting similar to what is proposed in this statement of principles and situations where the accounting applied has been different, such as continuity of interest accounting.

8. Would you be interested in participating in a task force or advisory group should PSAB decide to form one?

We would always be interested in having someone from our firm participate in such a group.

Click here to submit

Cliquez ici pour soumettre

Formulaire de réponse Pour être pris en considération,

les commentaires devront être reçus

le 17 mai 2013 au plus tard.

Restructurations

Énoncé de principesLe CCSP invite les intéressés à formuler des commentaires sur tous les aspects des principes proposés dans l'énoncé

de principes.

Ce formulaire ne vise pas à restreindre votre réponse. Chaque boîte de texte acceptera l'intégralité

de vos commentaires. Vous pouvez sauvegarder le formulaire et l'envoyer, pour examen, à d'autres personnes de votre

organisation avant de le soumettre.

Nom : André Miville CPA, CA, directeur général de la pratique professionnelle et Vicky Lizotte CPA, CA, directrice de la Normalisation

Organisation : Contrôleur des Finances - Québec

Courriel : [email protected] et [email protected]

Commentaires généraux :

D'un point de vue général, nous sommes en accord avec le projet du CCSP de publier des recommandations visant à encadrer les restructurations du secteur public. Toutefois, nous sommes d’avis qu’étant donné que les restructurations entre entités sous contrôle commun sont beaucoup plus fréquentes, celles-ci devraient être priorisées. Autre commentaire : L'assertion du paragraphe .27 à l'effet que « Les apports d'actifs ou les prises en charge de passifs sont, en substance, des cadeaux et sont comptabilisés conformément aux indications du chapitre SP 3410, PAIEMENTS DE TRANSFERT » n'est pas exacte. Seuls ceux provenant d'un gouvernement doivent être comptabilisés conformément au chapitre SP 3410. Lorsqu'ils ne proviennent pas d'un gouvernement, c'est le chapitre SP 3100 ACTIFS ET REVENUS AFFECTÉS qui s'applique.

1. Estimez-vous qu'il est nécessaire de se pencher sur les questions de comptabilité et d'information qui se posent aux entités en restructuration? Dans l'affirmative, veuillez indiquer les questions qui devraient être abordées et les raisons pour lesquelles il conviendrait de fournir des indications à leur égard.

Le projet du CCSP sur les restructurations, tel que présenté, nous semble moins utile étant donné que les restructurations entre entités sous contrôle commun sont exclues du champ d’applications. Nous croyons qu'il devrait traiter de ces dernières puisqu'il s'agit des opérations les plus courantes. Les gouvernements procèdent fréquemment à de telles restructurations et l'absence de norme sur le sujet peut entraîner des divergences dans le traitement de ces opérations entre les juridictions, mais aussi à l’intérieur du même périmètre comptable. Cela peut également amener des divergences d’opinions entre les préparateurs et leur auditeur.

2. La définition d'une opération de restructuration est-elle pratique et applicable? Dans l'affirmative, pouvez-vous fournir des exemples d'opérations passées auxquelles s'appliquerait cette définition?

Selon nous, la définition d'une opération de restructuration couvre bien les divers types de restructurations auxquels le gouvernement peut procéder. Nous n'avons pas eu connaissance de restructuration qui entrerait dans le champ d'application du projet sur les restructurations proposé par le CCSP, à l’exception des fusions de municipalités qui ont eu lieu il y a plusieurs années. Toutefois, au cours de l'exercice 2011-2012, le gouvernement du Québec a procédé à la restructuration de plusieurs organismes et fonds sous contrôle commun. Ces restructurations ont notamment été effectuées dans le but d'alléger et de rationaliser les structures de l'État et d'offrir des services plus efficients et mieux organisés aux citoyens du Québec. Voici certaines des restructurations d'entités sous contrôle commun effectuées par le gouvernement du Québec en 2011-2012 : - Fusion de la Corporation d'hébergement du Québec et de la Société immobilière du Québec; - Abolition du Fonds du service aérien gouvernemental et transfert de ses responsabilités (ainsi que ses actifs et passifs) au Centre de services partagés du Québec; - Création de l'Agence du revenu du Québec qui est substituée au ministère du Revenu; - Abolition de l’Immobilière SHQ et intégration de ses activités à la Société d’habitation du Québec.

3. Estimez-vous que l'utilisation de la valeur comptable est appropriée aux fins de l'évaluation initiale des actifs et des passifs transférés lors d'une restructuration?

Nous sommes d’avis qu’il est approprié que l'entité restructurée comptabilise les actifs et passifs transférés à la valeur comptable. Cette comptabilisation permet de présenter la substance de l'opération puisque les actifs et les passifs transférés sont utilisés principalement de la même façon avant et après l'opération de restructuration. Ainsi, il ne serait pas approprié d'en modifier la valeur. Toutefois, nous sommes en désaccord avec la création d'une nouvelle méthode de comptabilisation des regroupements d'entreprises. La littérature comptable comporte une méthode appropriée pour la comptabilisation de ces opérations, soit la méthode de la continuité des intérêts communs. Cette méthode permet de présenter adéquatement la substance des opérations de restructuration dans le secteur public et c'est d'ailleurs la méthode habituellement utilisée comme mentionnée dans l’énoncé de principe. De plus, le CCSP y précise également que l'un des résultats visés par la publication d'un nouveau chapitre sur les restructurations est la comparabilité des entités restructurées et des autres entités du secteur public qui n'ont pas subi de restructuration. Nous croyons que ce résultat serait atteint de façon plus efficace avec la méthode de la continuité des intérêts communs. En effet, selon cette méthode, les données antérieures de l'entité restructurée seraient retraitées comme si elle avait toujours existé en tant qu'entité unique. Il serait donc plus facile de voir l'évolution de ses résultats ainsi que de son actif net au cours des exercices et de les comparer avec d'autres entités.

4. Selon vous, le fait que l'entité restructurée soit une entité nouvellement constituée ou une entité existante devrait-il déterminer la façon de comptabiliser l'opération de restructuration, ainsi que les autres exigences de présentation et d'information, tel qu'il est indiqué dans le Tableau 5?

Non. Il ne serait pas approprié d'utiliser des traitements différents pour des opérations similaires. Les restructurations sont différentes des acquisitions notamment par le fait qu'il n'existe pas d'acquéreur. Puisqu'il n'y a pas d'acquéreur, la création ou non d'une nouvelle entité n'a aucun impact. Nous sommes d’avis que cela induirait les utilisateurs des états financiers enerreur que de traiter différemment les opérations de restructuration où une entité existante en englobe une autre de celles où ces deux mêmes entités se regroupent pour en former une nouvelle. De plus, la possibilité de deux traitements, soit de passer aux résultats ou directement à l’excédent ou déficit cumulé, pourrait entraîner des manipulations au niveau des

opérations de restructuration afin de présenter les résultats souhaités. Par ailleurs, le traitement proposé pour les entités restructurées existantes nous semble inapproprié puisqu'il ne permet pas d'atteindre l'un des résultats visés par la publication d'une nouvelle norme, soit la comparabilité des entités restructurées et des autres entités du secteur public qui n'ont pas subi de restructuration. De par le traitement proposé, les entités restructurées existantes auraient des revenus ou des charges surévalués en raison de la restructuration.

5. Êtes-vous d'accord pour que la communication d'informations sur la situation des entités en restructuration, ou des activités transférées, avant la date de restructuration soit encouragée mais non exigée?

Non, nous sommes d’avis que cette information devrait être exigée. Ainsi, les utilisateurs des états financiers auront en leur possession l’ensemble de l’information visant la restructuration, mais aussi cela permettra de quantifier l’impact de la restructuration sur l’entité restructurée.

6. Pouvez-vous fournir des exemples de questions découlant de restructurations ou qui y sont liées, qu'elles soient couvertes ou non dans le présent énoncé de principes (par exemple, les compensations, et les opérations et accords connexes à la restructuration)? Veuillez fournir des commentaires sur la nécessité ou non de l'élaboration d'indications sur les questions dont l'énoncé de principes ne traite pas.

- Comme mentionné précédemment, il est important que la norme traite de la comptabilisation des opérations de restructuration d'entité sous contrôle commun. - Les termes compensations et contrepartie devraient être définis. Dans le tableau 1, il est indiqué que lorsqu'il y a compensation substantielle sans contrepartie importante c'est une restructuration. Toutefois, au paragraphe 71, on indique qu'il peut y avoir une compensation importante dans une opération de restructuration. Quelle est la différence entre une contrepartie importante et une compensation importante? De plus, quelle est la différence entre une contrepartie importante et une compensation substantielle? - Qu'arrive-t-il lorsque la contrepartie est égale à la valeur comptable des actifs et passifs transférés? Considérez-vous qu’il s’agit d'une acquisition ou d'une restructuration au sens de l’énoncé de principe? - Il serait intéressant que la norme indique le traitement à appliquer par l'entité en restructuration lorsque seulement une partie d'entité est transférée. - Le champ d'application de la norme devrait être précisé. i) Est-ce que la norme s'appliquerait seulement aux restructurations entre entités du secteur public non apparentées ou s'appliquerait- elle également à une opération de restructuration dont l'entité en restructuration n'est pas contrôlée par un gouvernement? ii) Est-ce que la norme s'appliquerait aux restructurations dont l'entité en restructuration est une entreprise publique?

7. Pouvez-vous indiquer les incidences de l'application des principes proposés dans le présent énoncé de principes sur la comptabilisation des opérations et sur l'information financière dans le secteur public?

Nous sommes d’avis qu'il est important de retraiter les données antérieures afin de s’assurer d’avoir une information de qualité dans les états financiers. Ces derniers permettent notamment aux utilisateurs d'évaluer la reddition de comptes du gouvernement relativement à sa gestion des ressources publiques et de ses activités financières. Les restructurations sont souvent effectuées dans une optique d'efficience et d'économie; la présentation des résultats avant et après la restructuration permet aux utilisateurs de déterminer si ce but a été atteint. De plus, le retraitement des états financiers contribue à leur comparabilité. Il s'agit d'une qualité de l'information utile aux utilisateurs des états financiers, car cela permet de dégager des tendances et relever des écarts. À ce sujet, le Manuel de comptabilité de l'ICCA pour le secteur public indique que « Pour que les comparaisons soient significatives, les résultats

prévus et les résultats antérieurs doivent être présentés de la même manière et pour le même ensemble d'activités que les résultats réels de l'exercice. »

8. Seriez-vous intéressé à participer à un groupe de travail ou à un comité consultatif si le CCSP décidait d'en former un?

À évaluer

Cliquez ici pour soumettre

Cliquez ici pour soumettre

Formulaire de réponse Pour être pris en considération,

les commentaires devront être reçus

le 17 mai 2013 au plus tard.

Restructurations

Énoncé de principesLe CCSP invite les intéressés à formuler des commentaires sur tous les aspects des principes proposés dans l'énoncé

de principes.

Ce formulaire ne vise pas à restreindre votre réponse. Chaque boîte de texte acceptera l'intégralité

de vos commentaires. Vous pouvez sauvegarder le formulaire et l'envoyer, pour examen, à d'autres personnes de votre

organisation avant de le soumettre.

Nom : Nancy Klein

Organisation : Ministère des Affaires municipales, des Régions et de l'Occupation du territoire

Courriel : [email protected]

Commentaires généraux :

Nous questionnons la pertinence de partager les entités participant à une restructuration entre entité en restructuration et entité restructurée. Il serait plus simple de considérer qu’il y a d’une part une entité qui cède des actifs et passifs avec les programmes ou les activités afférentes (le cédant) et d’autre part une entité qui reçoit des actifs et passifs et prend à charge les programmes ou les activités afférentes (le récipiendaire). Selon une approche similaire à celle utilisée pour les paiements de transfert, il s’agirait de définir les règles de constatation, d’évaluation et de présentation qui s’appliquent au cédant d’une part tout autant que les règles de constatation, d’évaluation et de présentation qui s’appliquent au récipiendaire d’autre part. Les règles applicables au cédant méritent mieux que la simple mention au paragraphe 29. Une norme sur la restructuration doit viser également les deux entités impliquées. Dans le cadre d’une restructuration, autant l’entité qui cède que celle qui reçoit en sort restructurée. Dans le cas d’un échange à deux sens comme mentionné au paragraphe 48, une même entité pourrait devoir suivre les règles applicables au cédant pour ce qu’elle cède et les règles applicables au récipiendaire pour ce qu’elle reçoit, sans chercher à définir si elle constitue l’entité en restructuration ou l’entité restructurée.

1. Estimez-vous qu'il est nécessaire de se pencher sur les questions de comptabilité et d'information qui se posent aux entités en restructuration? Dans l'affirmative, veuillez indiquer les questions qui devraient être abordées et les raisons pour lesquelles il conviendrait de fournir des indications à leur égard.

Bien que les situations de restructuration ne soient pas des opérations fréquentes dans le milieu municipal, avoir des normes auxquelles se référer lorsque la situation se présente pourrait se révéler utile. Ainsi, le besoin de circonscrire ces opérations et de déterminer la valeur à laquelle ces opérations doivent être effectuées constituent deux points importants

à couvrir. Pour bien circonscrire les opérations de restructuration, il faut s'assurer qu'il n'y ait pas de confusion entre la restructuration et la notion de partenariat. Ainsi, nous recommandons de modifier la dernière phrase du paragraphe 01 comme suit : « … à une autre et les transferts d’actifs et passifs dans le cadre d’ententes de services partagés conclues par des Administrations locales dans une région donnée. »

2. La définition d'une opération de restructuration est-elle pratique et applicable? Dans l'affirmative, pouvez-vous fournir des exemples d'opérations passées auxquelles s'appliquerait cette définition?

La définition d'une opération de restructuration est essentielle. Celle donnée au paragraphe 24 est à notre avis pratique et applicable. Dans le milieu municipal, un exemple de ce type d'opération pourrait être les fusions de municipalités qui ne sont pas de nature courante et fréquente, sauf lors de la vague des fusions survenues en 2002 au Québec. Un autre exemple pourrait-il être le transfert d'infrastructures de loisirs entre une municipalité et une commission scolaire?

3. Estimez-vous que l'utilisation de la valeur comptable est appropriée aux fins de l'évaluation initiale des actifs et des passifs transférés lors d'une restructuration?

À notre avis, bien qu'appropriée, nous croyons que la valeur comptable pourrait dans certains cas être une donnée difficilement accessible pour l'entité qui reçoit les actifs et les passifs. Ces opérations ayant lieu entre des parties non apparentés, plus souvent qu'autrement l'entité ne connaît pas la valeur comptable des actifs et passifs qui lui sont transférés à moins que celle-ci soit mentionnée dans le protocole d'entente.

4. Selon vous, le fait que l'entité restructurée soit une entité nouvellement constituée ou une entité existante devrait-il déterminer la façon de comptabiliser l'opération de restructuration, ainsi que les autres exigences de présentation et d'information, tel qu'il est indiqué dans le Tableau 5?

Nous croyons que les différences suggérées dans la comptabilisation applicable à ces 2 types d'entité (nouvelle et existante) est adéquate. Toutefois, nous questionnons la pertinence et la validité de se baser, comme indiqué aux paragraphes 45 et 46, sur la notion de contrôle pour déterminer si une entité « restructurée » est nouvelle ou existante. En plus de complexifier la norme, cela ne paraît pas justifié selon les fondements des normes pour le secteur public. La comptabilisation devrait plutôt être basée sur l’existence juridique. Toute entité « restructurée » qui existait juridiquement avant la restructuration devrait comptabiliser l’écart entre les actifs et les passifs de la même manière, soit à titre de revenus ou charges de l’exercice. Seule une entité « restructurée » qui commence à exister suite à la restructuration comptabiliserait l’écart dans son excédent (déficit) accumulé de départ. De plus, en faisant intervenir la notion de contrôle, on risque d'amener de la confusion avec les activités de restructuration entre apparentés, ce qui est exclu de la portée de la norme selon le paragraphe 25 c).

5. Êtes-vous d'accord pour que la communication d'informations sur la situation des entités en restructuration, ou des activités transférées, avant la date de restructuration soit encouragée mais non exigée?

Nous sommes en accord pour que la communication de ces informations soit encouragée mais non exigée. Ce devrait être le cas aussi pour l’entité « restructurée ». Pourquoi serait-ce plus important pour une partie impliquée que l’autre? Il y aurait lieu de rendre la présentation d’information facultative pour les deux parties impliquées, mais en insistant sur la notion de significativité pour juger de la pertinence de le faire ou non.

6. Pouvez-vous fournir des exemples de questions découlant de restructurations ou qui y sont liées, qu'elles soient couvertes ou non dans le présent énoncé de principes (par exemple, les compensations, et les opérations et accords connexes à la restructuration)? Veuillez fournir des commentaires sur la nécessité ou non de l'élaboration d'indications sur les questions dont l'énoncé de principes ne traite pas.

À notre avis, il existe une zone grise qui mériterait d'être précisée, à savoir la différence entre une contrepartie importante et une compensation substantielle. Cette différence menant à la comptabilisation de deux opérations différentes, une restructuration ou une acquisition selon le cas, il importe de distinguer clairement les deux termes. À cet égard, dans l'énoncé de principes, les paragraphes 71 à 75 donnent des exemples de ce qui ne constitue pas une compensation. Nous croyons qu'il serait judicieux qu'au sein de ces paragraphes, on fournisse également des exemples de ce qui pourrait constituer une compensation.

7. Pouvez-vous indiquer les incidences de l'application des principes proposés dans le présent énoncé de principes sur la comptabilisation des opérations et sur l'information financière dans le secteur public?

Comme ce type d'opération n'est pas de nature fréquente, les incidences des principes proposés ne sont pas importantes.

8. Seriez-vous intéressé à participer à un groupe de travail ou à un comité consultatif si le CCSP décidait d'en former un?

Nous ne sommes pas disponibles pour participer à un tel groupe de travail.

Cliquez ici pour soumettre

Click here to submit

Response Questionnaire

To be considered, comments must be received by

May 17, 2013

Restructurings

Statement of Principles

PSAB welcomes comments on all aspects of the Statement of Principles.

This form is not intended to constrain your response. Each text box will accommodate your full comments.

You are able to save and forward this form to others in your organization for review prior to submission.

Name: Stuart Barr, Assistant Auditor General

Organization: Office of the Auditor General of Canada

E-mail: [email protected]

General comments:

The Office of the Auditor General of Canada is pleased to provide comments on the PSAB Statement of Principle (SoP) on restructurings. We support PSAB in the development of accounting standards and guidance on public sector restructuring transactions, particularly in light of the current fiscal challenges experienced in Canada. We also look forward to PSAB’s future work to address restructuring transactions among entities under common control as suggested in paragraph 28 of the SoP given these transactions are pervasive throughout the public sector. We acknowledge that there may be fundamental differences between restructuring transactions among related parties and restructuring transaction among unrelated parties that may justify a different accounting treatment. Therefore, before arriving at any conclusion, we believe the issues should be comprehensively considered in both contexts to ensure coherence between the various types of restructuring transactions. Proposed terminology: While we agree with paragraph 19 of the SoP regarding the distinction of restructuring transactions according to their common characteristics and attributes, we question the approach taken in this SoP to avoid using the more traditional terminology, such as combinations, acquisitions and amalgamations. The IPSASB consultation paper, like this SoP, acknowledges that there is a wide range of restructuring activities in the public sector. Also like this SoP (see paragraph 45), IPSASB uses the notion of change in control as the sole criterion for distinguishing the two main types of restructuring activities (acquisitions and amalgamations). Based on our understanding, the key difference between the approaches of the two standard setters regarding the definition of restructuring transactions is the use of different terminology: IPSASB uses traditional terms such as combinations, acquisitions and amalgamations while PSAB proposes to use new terms such as restructuring, existing restructured entity and newly formed restructured entity (paragraphs 22 and 46) as the basis to develop accounting guidance in this area. In our view, the approaches of the two standard setters align in substance because to qualify as restructuring transaction they both require an integrated set of assets/liabilities to be transferred together with related programs or operating responsibilities and they both use the notion of change in control as the key differentiator between the different types of restructuring transactions. It is also not clear how restructuring activities in Canada differ from those found elsewhere in the world and as a result warrant a different terminology. For these reasons the introduction by PSAB of the new terminology is not in our view warranted and has the potential to cause confusion

among users of these standards. We encourage PSAB to align its terminology with that of other public sector standard setters when possible.

1. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on those issues.

Yes, we believe that a new standard on restructuring transactions should also address accounting and reporting issues of a restructured entity, whether the entity will continue or cease to exist, especially when certain circumstances are not already addressed elsewhere in the PSA Handbook. While we agree with paragraph 29 of the SoP that the accounting for restructuring transactions by an entity that continues to exist appears on the surface straightforward, a new standard on restructuring transactions addressing both restructured entity and restructuring entity accounting will in our view be beneficial given the wide range of diversity and complexity of restructuring activities in the public sector. The underlying issue where a restructuring entity ceases to exist is whether the financial statements of the restructuring entity should be prepared on a going concern basis. Strictly interpreted, a restructuring entity that will cease to exist would not meet the going concern assumption in PS 1000.63. While PSAS gives no further guidance on how to prepare financial statements where the going concern assumption is no longer met, other current authoritative sources of GAAP require an entity to consider whether a change in carrying values of assets and liabilities is required (IPSAS 14.22) and others even require a fundamental change in the basis of accounting (IAS 10.15), such as the liquidation basis of accounting. In its June 2012 Consultation Paper (CP) on Public Sector Combinations, the IPSASB explored an alternate view under which the going concern assumption may still remain appropriate since a restructured entity will continue to undertake the same activities and fulfill the responsibilities it has assumed from the restructuring entity. On this basis, the preliminary view put forth by IPSASB was "where combining operations continue to prepare and present general purpose financial statements (GPFSs) using accrual-based IPSASs in the period between the announcement of the amalgamation and the date of the amalgamation, these GPFSs are prepared on a going concern basis where the resulting entity will fulfill the responsibilities of the combining operations" (see IPSASB June 2012 Consultation Paper on Public Sector Combinations, paragraph Preliminary View 9). The IPSASB had an initial discussion in March 2013 on the responses received to the CP and agreed that the draft Exposure Draft should include guidance on both the de-recognition of assets for the transferor and disclosure requirements for combining entities relating to the going concern basis. Given the current lack of guidance in PSAS about how to prepare financial statements for an entity when the going concern assumption is not met and the possibility that applying current authoritative secondary sources of GAAP may lead to inconsistent treatment in restructuring entities' financial statements, we encourage PSAS to address the accounting and reporting issues of a restructuring entity when the going concern assumption is not met.

2. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition?

We have the following comments regarding the definition of a restructuring transaction. Proposed scope out for acquisitions: We question the proposal to exclude from the restructuring definition transfers with significant consideration, and the statement made at paragraph 33 of the SoP that “the key difference between an acquisition and a restructuring is the absence or presence of an exchange of consideration primarily based on the fair value of assets and liabilities transferred”. Irrespective of the relative amount of the compensation involved, the transfer of an integrated set of assets and liabilities together with related programs or operating responsibilities are in our view the two main characteristics reflecting the substance of a restructuring transaction in the public sector. We therefore do not see acquisitions and restructurings to be mutually exclusive. We find the current proposal to segregate acquisitions based on significance of the compensation has

the potential of being confusing to users. A more intuitive approach may be to have a single broader definition of restructuring transactions that would encompass the broad spectrum of acquisitions listed Table 1of the SoP – significant exchange (column 2), substantial but non-exchange (column 3) and nominal (column 4). The new standard would then provide additional guidance on how to distinguish between these types of acquisition transactions and point to PS 2510 and PS 3070 to account for acquisitions with significant consideration. Should PSAB consider adopting this approach, the definition of a restructuring transaction would be simplified to “a transfer of an integrated set of assets and liabilities, together with related program or operating responsibilities”. Transfer of integrated set of assets and liabilities: We agree with PSAS that the transfer of a group of assets and/or liabilities must be accompanied by a related program or operating responsibilities to be classified as a restructuring transaction. The challenge will however be distinguishing between restructuring transactions and government transfers with stipulations. For example, an asset may be transferred with a purpose stipulation that requires the recipient to carry out a particular activity (PS 3410 Glossary). Determining whether transfer terms are stipulations in scope of PS 3410 or whether they constitute operating responsibilities in a restructuring transaction may be an area of significant judgment. We encourage the Board to consider including in the new standard additional guidance to assist with these judgments and encourage consistency in accounting for similar transactions. Non-exchange transactions: The definition of a restructuring transaction scopes out exchange transactions considered to be those involving significant consideration (determined primarily based on the fair value of the individual assets acquired and liabilities assumed). We support this scope exclusion. We however agree with the SoP that the challenge will be determining whether a transfer with substantial compensation is a restructuring or an acquisition to be accounted for using PS 2510 and PS 3070. Reference to the fair value of transferred assets and liabilities can only be useful when such fair value is determinable, which is often not the case. This will be an area of significant judgment and as such, we encourage the Board to consider including in the new standard additional guidance to assist with these judgments and encourage consistency in accounting for similar transactions. The Board will also need to consider consequential amendments to PS 2510 (starting with paragraph 11) which currently defines an acquisition as a transfer of control over net assets in exchange for consideration paid, irrespective of whether such consideration is significant or not when compared to the fair value of the net assets acquired. Joint ventures: The SoP does not deal with the formation of a joint venture. This is in our view appropriate as the accounting joint ventures has already been addressed elsewhere in the PSA Handbook (PS 3060). We however see merit in clarifying this in a new standard on restructurings by explicitly addressing this scope exclusion. Examples of past transactions: We do not have any examples that are within the current scope of the SoP. Examples of past transactions at the federal and territorial levels are primarily among related parties, which we understand will be addressed at a later stage of this project.

3. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring?

When a restructuring entity is newly formed: Yes, we agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring when a restructured entity is newly formed because it most faithfully represents the non-purchase nature of the restructuring transaction and the fact that the restructured entity is the result of two or more restructuring entities combining where none of the restructuring entities gains control of the other entities. Furthermore, carrying amounts,

unlike fair values, allow users to assess the subsequent performance of the restructured entity on the same basis as that used to assess accountability before the restructuring. When the restructured entity is an existing entity: In this scenario, an existing entity takes control over an integrated set of assets and liabilities that it received from one or more unrelated entities. In this case, the use of carrying values is not as obvious as the change in control over the assets and liabilities transferred is changing the fundamental substance of the transaction compared to the scenario above where no change in control occurs. The use of carrying values would also be inconsistent with PS 3410 and PS 3150, which both require that assets contributed in a non-exchange transaction be recorded at fair value at the date of contribution (except in unusual circumstances, where an estimate of fair value cannot be made, a nominal value would be used). The IPSASB is currently dealing with this same issue, and in its June 2012 CP on Public Sector Combinations has sought respondents' views on whether fair value should be applied to all non-related party acquisitions, or whether carrying value would be appropriate in cases where no or nominal consideration is transferred. The IPSASB has not yet finalized its views on this matter. We suggest that a more robust assessment of the merits of the use of either fair values or carry values be made as PSAB moves to the next phase of its project and that the progress of the similar IPSASB project be monitored closely. In the event PSAB continues to support carrying values, it would be beneficial to reconcile this measurement basis with those used in PS 3410 and PS 3150. We also question how practical it will be for an existing entity to obtain access to the carrying values of contributed assets and liabilities in a restructuring transaction when those are contributed by unrelated entities.

4. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5?

Yes we agree with that statement.

5. Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required?

Yes, we agree, given that it provides a balance between the cost of providing information about the restructuring entities and transferred operations prior to restructuring date by the restructured entity and the information needs of users.

6. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed.

We do not have additional examples of issues arising from or related to restructuring that have and have not been addressed in this SoP.

7. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting?

As mentioned in our response to question 2 above, we typically do not encounter examples of restructuring transactions addressed by the SoP, as transactions encountered at the federal or territorial levels are under the ultimate common control of the government. Issuance of a new standard on restructuring transactions will however help address the risk of inconsistent accounting treatment for similar transactions as public sector entities currently refer to different sources of secondary GAAP. For example, some secondary sources of GAAP, such as IFRS3, advocate using the acquisition method (fair values at the date of combination); others, such as FASB’S ASC 805, advocate using predecessor method of accounting (carrying values at the date of combination).

8. Would you be interested in participating in a task force or advisory group should PSAB decide to form one?

The OAG supports PSAB’s standard setting work and currently has many of its staff members participating in PSAB task forces. Should PSAB decide to form a task force or advisory group, the OAG would consider participating if the scope is expanded to include restructurings amongst related parties, given that at the federal level this is how the majority of public sector restructurings take place.

Click here to submit

Raymond Chabot Grant Thornton LLP Suite 2000 National Bank Tower 600 De La Gauchetière Street West Montréal, Québec H3B 4L8 T + 514 878 2691 F + 514 878 2127 www.rcgt.com Grant Thornton LLP 12th Floor 50 Bay Street Toronto, ON M5J 2Z8

T +1 416 366 4240 F +1 416 360 4944 www.GrantThornton.ca

Partnership of Chartered Professional Accountants Member of Grant Thornton International Ltd

May 17, 2013

Mr. Tim Beauchamp Director, Public Sector Accounting Public Sector Accounting Board 277 Wellington Street West Toronto, Ontario M5V 3H2 via: [email protected]

Dear Mr. Beauchamp:

SUBJECT: STATEMENT OF PRINCIPLES – RESTRUCTURINGS (FEBRUARY 2013)

Grant Thornton LLP and Raymond Chabot Grant Thornton LLP would like to thank you for the opportunity to provide comments on the Public Sector Accounting Board’s (PSAB) Statement of Principles (SP), Restructurings.

Please find below our comments related to your specific questions:

1. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on these issues.

Although we support PSAB’s decision to provide guidance regarding restructurings, we believe that these transactions are more likely to happen between related parties or entities under common control or shared control. Therefore, it is disappointing that these transactions are not within the scope of the present SP, the “Related Party Transactions” Exposure Draft or elsewhere in the Handbook as we believe they occur much more frequently than non-related party restructurings. We believe that the transfer of operations between “non-related” parties most often leads to the identification of an acquirer; therefore, these transactions would not fall under the scope of this SP, but under the scope of existing standards.

2

2. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition?

We believe some clarifications are needed in order to understand the concepts of “consideration” and “compensation” that are an integral part of the proposed definition. For example, Table 1 in paragraph .38 addresses the situation of “substantial compensation, but non-exchange consideration”, which is difficult to interpret. Also, a definition or guidance should be provided to define “significant consideration”.

Moreover, situations where compensation would be provided after the restructuring (for example to provide services related to a program or to assume operating responsibilities) should be addressed, in order to determine if these types of compensation should be taken into consideration in analyzing if a transaction falls under the definition of a restructuring transaction.

3. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring?

Given that the scope excludes restructuring transactions between related parties, we believe that in the rare restructuring transactions with non-related parties that it may be difficult to obtain information on the carrying amount of assets and liabilities transferred in such a restructuring. As a result, we question whether the exchange amount should be an appropriate initial measure of such assets and liabilities, especially in the case of a restructuring with little or no consideration.

4. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5?

No, we disagree with this concept. We strongly believe that the form of a restructuring transaction should not take precedence over the appropriate method of accounting. Given the substance of these transactions, we think that all restructuring transactions in which there is a difference between assets and liabilities transferred should give rise to an adjustment in the accumulated surplus or deficit balance, whether or not a new restructured entity is formed.

5. Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required?

Yes, we believe this information should be encouraged.

3

6. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed.

We see a need to clarify whether or not this SP is applicable only to restructurings between public sector entities or if it would also apply to a restructuring involving a “non-public sector” entity.

Also, as explained in our response to question 2, we see a need to clarify the concepts of “consideration” and “compensation” described in the SP.

7. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting?

Given that restructuring transactions between related parties or entities under common control or shared control are excluded from the SP, we believe that the scope of the proposed standard is very limited and we cannot identify any effect of applying the principles proposed in this SP.

8. Would you be interested in participating in a task force or advisory group should PSAB decide to form one?

Given the proposed scope and the fact that restructurings between related parties are excluded from the SP, we would not be interested in participating in a task force or advisory group at this time.

If you wish to discuss our comments or concerns, please contact Melanie Joseph ([email protected], 416-607-2736) or Stéphane Landry ([email protected], 418-647-5008).

Yours sincerely,

Melanie Joseph, CPA, CA Stéphane Landry, CPA auditor, CA Grant Thornton LLP Raymond Chabot Grant Thornton LLP

Finance Comptroller’s Division Comptroller’s Office 715 – 401 York Avenue Winnipeg, Manitoba R3C 0P8 Phone: (204) 945-4919 Fax: 948-3539 E-mail: [email protected]

May 17, 2013 Mr. Tim Beauchamp, Director Public Sector Accounting 277 Wellington Street West Toronto, Ontario M5V 3H2 Dear Mr. Beauchamp:

Re: Exposure Draft: Restructurings Thank you for the opportunity to comment on the Statement of Principles (SOP): Restructurings. The Province of Manitoba (Province) has included responses to the Board’s specific questions in the attachment. The Province has some concerns with the SOP. The scope of the SOP does not currently include restructuring transactions between entities under common control or shared control. However PSAB has indicated in the SOP that restructuring transactions between related parties will be considered after the approval of an exposure draft on related party transactions. Including related parties within the scope of restructuring transactions would create reporting issues for the Province’s Summary Financial Statements (SFS). The recent exposure draft on Amendments to the Introduction includes government components (ministries, departments and funds) as public sector entities. Government components would be related to each other since they are public sector entities under the common control of the government. The Province is concerned that internal reorganizations between departments would be included within the scope of a future standard on restructurings. In accordance with the SOP an existing restructured public sector entity would be required to present prior period information without restatement. This requirement would be in direct contradiction with PS2700.24 which requires that prior period segment data in the SFS be restated if there is a change in segments. Internal government reorganizations often require the Province to restate the segmented reporting for the prior period. Reporting on the Province’s segments under PS2700 is not an equivalent to preparing general purpose financial statements on a government component. However, if entities under common

Page 2 of 4

control are included within the scope of a restructuring standard, there would be an apparent inconsistency between a new standard on restructurings and the current standard for segmented reporting. We appreciate the opportunity to comment on the ED. If you have any questions or concerns related to these comments please contact the undersigned. Yours truly, Betty-Anne Pratt, CA Provincial Comptroller On Behalf of the Province of Manitoba

Page 3 of 4

1. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on those issues. Yes there is immediate need in Manitoba to address accounting and reporting issues of a restructuring entity. The Province has announced that municipalities under a specified population are required to amalgamate with other municipalities within the next few years. Current standards address asset purchases, acquisitions of private sector entities, and transfers. The current standards however do not address situations where the assets, liabilities and responsibilities of a public sector entity are exchanged for little or no compensation. The purchase method is not appropriate for many entity combinations in the public sector.

2. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition? The definition of a restructuring transaction, as described under Principle 1, is practical and workable. In Manitoba, most restructurings would have been between public sector entities within the Province’s government reporting entity (GRE). However in the mid nineties the Province took over the responsibility for social assistance from the local governments. In 2004 the Province took control over Winnipeg Child and Family Services which had operated as a not-for-profit. In recent years there have also been some amalgamations of local governments.

3. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring? The Province agrees that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring. The carrying amount of the assets and liabilities should be adjusted to comply with Public Sector Accounting (PSA) standards and the restructured entity’s accounting policies. The entity’s accounting policies would include whether or not the restructured entity plans to manage its risk or evaluate its performance of the assets and liabilities transferred in a restructuring on a fair value basis.

4. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5? The Province agrees that the appropriate criteria for determining how a restructuring transaction is recognized should be based on the determination of whether this is a newly formed restructured entity or the continuation of an existing entity after a restructuring. It may however be difficult for some restructurings to determine if the restructured entity is newly formed, or the continuation of the entity. The SOP mentions that the continuation of control by an entity’s existing board would support the conclusion the restructured entity is a continuation of the previous entity. PSAB should consider whether further criteria exist for evaluating whether a restructured entity is newly formed or a continuation of the existing entity. Consider the amalgamation of a small

Page 4 of 4

municipality with a large municipality. Based on their sizes the large municipality will have more representation on the new amalgamated council. Based solely on the representation on council, the new amalgamated municipality should be viewed as the continuation of the previous large municipality? But under Provincial legislation the new amalgamated municipality is a new local government while both restructuring municipalities no longer exist under the law.

5. Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required? The Province agrees that the disclosure of information on the restructured entities, and transferred operations prior to restructuring, should be encouraged but not required.

6. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed. There may be situations where two restructuring entities fully amalgamate with equal board representation, but given the differences in size and influence, the amalgamated entity is in substance more of a continuation of the large restructuring entity. The SOP requires more guidance in evaluating whether a restructured entity is newly formed, or a continuation of the restructured entity.

7. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting? If the scope of restructurings is extended to public sector entities under common control, the Province has envisioned some inconsistencies in the preparation of the SFS. If possible, segmented reporting requires the restatement of prior year results for segments that have changed due to internal re-organizations. However for their own financial reporting, the components and government organizations that comprise the segment, may not be required to restate their prior year results if the restructured entity is viewed as a continuation of a restructuring entity.

8. Would you be interested in participating in a task force or advisory group should PSAB decide to form one? Provided a suitable candidate is available, the Province would consider recommending a participant for a task force or advisory group should PSAB decide to form one.

Click here to submit

Response Questionnaire

To be considered, comments must be received by

May 17, 2013

Restructurings

Statement of Principles

PSAB welcomes comments on all aspects of the Statement of Principles.

This form is not intended to constrain your response. Each text box will accommodate your full comments.

You are able to save and forward this form to others in your organization for review prior to submission.

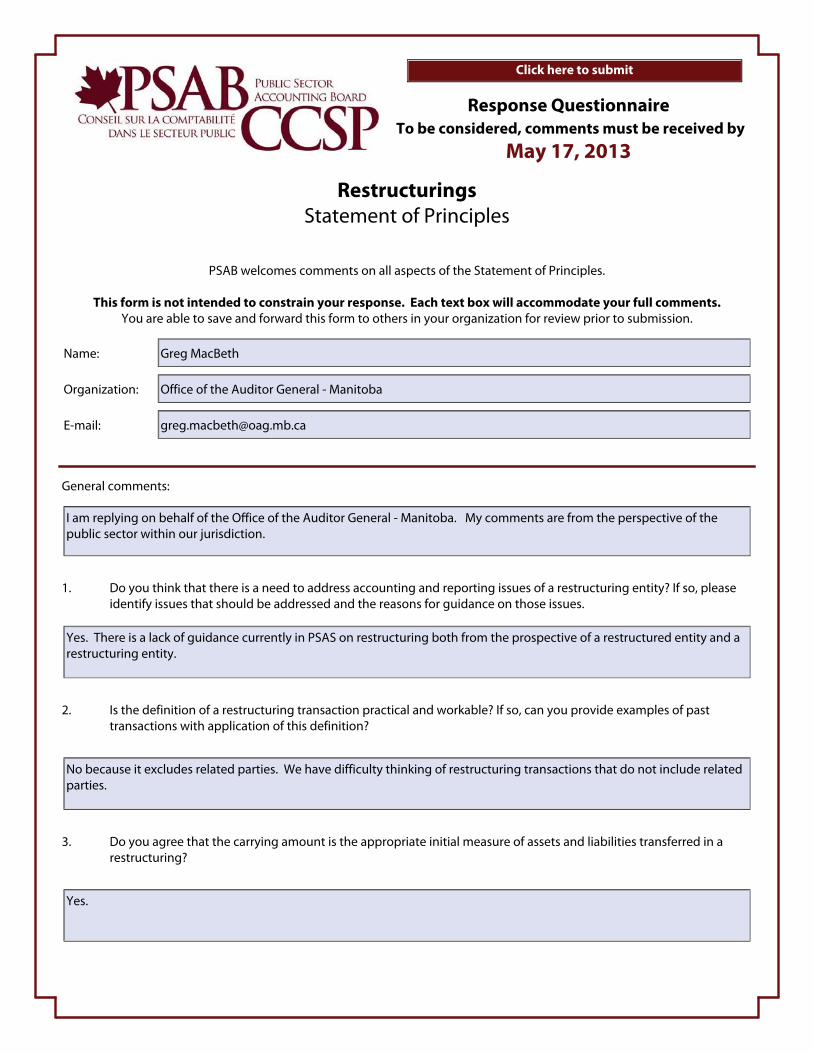

Name: Greg MacBeth

Organization: Office of the Auditor General - Manitoba

E-mail: [email protected]

General comments:

I am replying on behalf of the Office of the Auditor General - Manitoba. My comments are from the perspective of the public sector within our jurisdiction.

1. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on those issues.

Yes. There is a lack of guidance currently in PSAS on restructuring both from the prospective of a restructured entity and a restructuring entity.

2. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition?

No because it excludes related parties. We have difficulty thinking of restructuring transactions that do not include related parties.

3. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring?

Yes.

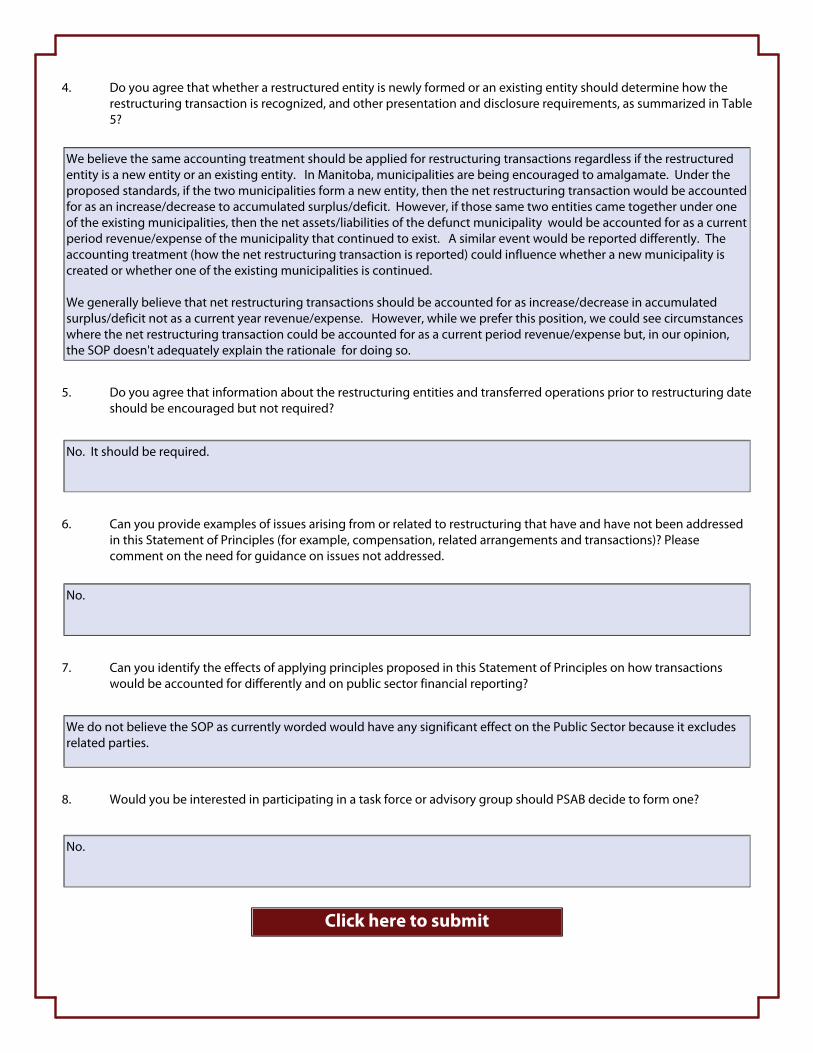

4. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5?

We believe the same accounting treatment should be applied for restructuring transactions regardless if the restructured entity is a new entity or an existing entity. In Manitoba, municipalities are being encouraged to amalgamate. Under the proposed standards, if the two municipalities form a new entity, then the net restructuring transaction would be accounted for as an increase/decrease to accumulated surplus/deficit. However, if those same two entities came together under one of the existing municipalities, then the net assets/liabilities of the defunct municipality would be accounted for as a current period revenue/expense of the municipality that continued to exist. A similar event would be reported differently. The accounting treatment (how the net restructuring transaction is reported) could influence whether a new municipality is created or whether one of the existing municipalities is continued. We generally believe that net restructuring transactions should be accounted for as increase/decrease in accumulated surplus/deficit not as a current year revenue/expense. However, while we prefer this position, we could see circumstances where the net restructuring transaction could be accounted for as a current period revenue/expense but, in our opinion, the SOP doesn't adequately explain the rationale for doing so.

5. Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required?

No. It should be required.

6. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed.

No.

7. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting?

We do not believe the SOP as currently worded would have any significant effect on the Public Sector because it excludes related parties.

8. Would you be interested in participating in a task force or advisory group should PSAB decide to form one?

No.

Click here to submit

Wayne Morgan Office of the Auditor General of Alberta Edmonton, Alberta May 17, 2013 Tim Beauchamp, Director Public Sector Accounting 277 Wellington Street West Toronto, Ontario Dear Mr. Beauchamp, Our response to PSAB Statement of Principles – Restructurings is below. Do you think that there is a need to address accounting and reporting issues of a restructuring entity? If so, please identify issues that should be addressed and the reasons for guidance on those issues. Yes, but the need exists for restructurings involving related parties within a government’s overall reporting entity. It would be helpful to see how such restructurings should be accounted for by related parties, and particularly (considering the proposed amendments to the introduction) for restructurings between government components (where the reporting entities involved are all part of the same legal entity). While the transfer of related assets and liabilities may be covered under a proposed related party standard, there are additional accounting and disclosure / presentation issues that arise from restructurings, including the presentation of meaningful comparative information for the restructured reporting entities. Is the definition of a restructuring transaction practical and workable? If so, can you provide examples of past transactions with application of this definition? The definition would be difficult to apply practically without substantial definition/guidance on what constitutes an “integrated set of assets and liabilities”, “related program or operating responsibilities”, and “significant consideration”. It may be unclear where the application of Government Transfers ends and Restructurings begins. PSAB should also consider guidance on distinguishing restructurings from lease arrangements or arrangements similar to public-private partnerships. Do you agree that the carrying amount is the appropriate initial measure of assets and liabilities transferred in a restructuring?

Carrying amount is the appropriate measurement basis where assets and/or liabilities are transferred between entities that are within the same government reporting entity as the related government has not lost control or responsibility for these assets and liabilities (continuity of interest accounting). However, as described in the recent related party exposure draft, there may be circumstances where the cash flows or service potential for transferred assets may be significantly changed in the restructuring suggesting that fair value would be more appropriate. Do you agree that whether a restructured entity is newly formed or an existing entity should determine how the restructuring transaction is recognized, and other presentation and disclosure requirements, as summarized in Table 5? The proposed accounting appears to depend more on the legal terminology used in the restructuring rather than the de-facto nature of the restructuring. If the merger of two entities into a new entity, or the amalgamation of one into the other with changes to the continuing entity’s governing body, results in identical restructured organizations, why should the accounting be different? Do you agree that information about the restructuring entities and transferred operations prior to restructuring date should be encouraged but not required? The continuity of interest type accounting proposed for restructurings between unrelated parties presumes some continuity of operations (services continue to be delivered, but by a different entity). On that basis, there should be some form of presentation or disclosure of comparative information from before the restructuring. Information about the operations prior to the restructuring date should be encouraged. However, the restructured entity may have difficulty accessing the records of an unrelated restructuring entity to obtain information on prior operations for financial reporting. For restructurings involving related parties within a single government reporting entity, there is no change in the government’s role and responsibilities, only in the composition of component entities providing the services. For such restructurings the presentation of comparative information, as if the restructured entities had always had their post-restructuring responsibilities, may be needed for financial statement users to understand the nature of the restructured entities and how they fit into the larger government reporting entity. This reflects that financial statements of the component units of a government (government components and government organizations) represents a form of segmented information. Can you provide examples of issues arising from or related to restructuring that have and have not been addressed in this Statement of Principles (for example, compensation, related arrangements and transactions)? Please comment on the need for guidance on issues not addressed. As discussed above, there may be difficulty in determining what a restructuring transaction is (as opposed to a regular transfer), or when a restructured entity should be accounted for as a new or existing entity (or if there should be a distinction between these types of restructured entities).

Also, the accounting and presentation/disclosure of restructurings between related parties within a single government reporting entity has not been discussed and may require further guidance than was included in the recent related party transactions exposure draft. Can you identify the effects of applying principles proposed in this Statement of Principles on how transactions would be accounted for differently and on public sector financial reporting? Not clearly. The statement of principles proposes an alternate “continuity of interest” type accounting for restructuring transactions, but is not clear enough in either the definition of what a restructuring transaction or determining whether a restructured entity is, in fact, new or continuing. Would you be interested in participating in a task force or advisory group should PSAB decide to form one? Yes.

Thank you for the opportunity to comment. Sincerely, Wayne Morgan, PhD, CA, CISA

PROVINCIAL AUDITOR •titikilialCWall

May 16, 2013

Mr. Tim Beauchamp, Director Public Sector Accounting The Canadian Institute of Chartered Accountants 277 Wellington Street West TORONTO, ON M5V 3H2

Dear Mr. Beauchamp:

Re: PSAB Statement of Principles— Restructurings