2013 march ernst & yang report german economy

TRANSCRIPT

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 1/8

AustriaBelgium

Cyprus

Estonia

Finland

France

Germany

Greece

Ireland

Italy

Luxembourg

Malta

Netherlands

Portugal

Slovakia

Slovenia

Spain

Ernst & Young Eurozone Forecast Spring edition — March 2013

Eurozone

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 2/8

Outlook for Germany

Ernst & Young Eurozone Forecast — Spring edition March 2013

Published in collaboration with

17 Eurozone countries

Spain

Portugal

France

Ireland

Finland

Estonia

Belgium

Slovakia

Austria

Slovenia

Italy

Greece

Malta

Cyprus

Netherlands

Luxembourg

Germany

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 3/8

1Ernst & Young Eurozone Forecast Spring edition March 2013 | Germany

HighlightsBusiness investment

and exports to drive a

return to growth in the

rst half of 2013

• The combination of sound domestic

fundamentals, a normalizing risk

environment and an improving global

growth backdrop means that we expect

the German economy to return to

growth in the rst half of 2013. Despite

this, we forecast growth of 0.7% in

2013, a little slower than in 2012, but

then the pace is expected to accelerate

to 1.9% in 2014.

• The economy slowed sharply over

the past year and ended 2012 with acontraction of 0.6% in Q4. The slowdown

was focused on business investment

and, to a lesser extent, exports and

consumer spending. Despite slowing,

Germany still outperformed the rest

of the Eurozone in 2012 with growth

of 0.9%. Fear of a further sharp

deterioration in the economic outlook

or another credit crunch caused

businesses to curtail investment in

plant and machinery in 2012.

• Despite its recent weakness, the

economy remains fundamentally sound.

Neither businesses nor households

are particularly highly leveraged,

and corporate prots have reversed

around 95% of the fall seen during

the 2008–09 global nancial crisis.

Corporate borrowing rates and survey

measures of credit constraints are

close to historic lows, and the banking

sector has made good progress in

deleveraging. The German Government

is estimated to have balanced itsbudget in 2012, four years ahead of

schedule.

• These strong fundamentals provide

the foundation for accelerating growth

over the next couple of years, led by

a pickup in business investment. This

prospect is illustrated by the Institute

for Economic Research (Ifo) index,

which, after falling fairly consistently

since March 2011, has risen in each of

the last four months, suggesting that

the economy has passed its low point.

• We believe that the risk environment

is normalizing again after a period inwhich it was difcult for companies to

have high condence in the economic

outlook and risks were skewed to the

downside. This will give companies the

condence needed to start investing

again. The fall in peripheral bond

spreads and the rise in equity prices

and the euro over the last six months

suggest that investors also believe the

balance of risks has shifted.

• Weakness in exports also contributed

to economic contraction at the end

of 2012. Although export order

books have only picked up a little so

far, we expect the export situation to

improve during the course of 2013

as world trade growth accelerates.

The rise in world trade will reect an

anticipated pickup in the US economy

and a reacceleration of emerging

market growth, driven by Asia and

Latin America.

• Last year saw a sharp rise in concern

about unemployment among

consumers. But given our forecast that

the contraction in output will be short

lived, we expect unemployment on

the International Labour Organization

(ILO) measure to decline to 5.4% in

2013 overall. Consequently, as it

becomes clear to consumers that the

risk environment is normalizing, we

expect fear of unemployment to fall

and consumer spending to increase.

As a result, we forecast consumer

spending growth will accelerate from

0.6% in 2012 to 0.8% in 2013 and then

1.2% in 2014.

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 4/8

2 Ernst & Young Eurozone Forecast Spring edition March 2013 | Germany

The combination of solid domestic demand,

a normalizing risk environment and an

improving global growth backdrop means that

we expect the German economy to return to

growth in the rst half of 2013, with GDP

seen rising 0.3% in both Q1 and Q2. Theeconomy ended 2012 on a weak note with

a contraction of 0.6%. As a result, we expect

growth in 2013 to be just 0.7%, before

accelerating to 1.9% in 2014.

Although growth slowed sharply

during 2012 …The economy slowed sharply over the past

year, with growth down from 3.1% in 2011 to

0.9% in 2012, as the Eurozone crisis took its

toll. The pace slowed progressively during

2012, with weakness focused on business

investment and, to a lesser extent, exportsand consumer spending. Despite slowing,

Germany outperformed the rest of the

Eurozone, which contracted by 0.5% in 2012.

… the economy remains

fundamentally soundMoreover, the German economy remains in

good shape. Consequently, we expect growth

to average 1.6% a year in 2014–17, only a little

below the pace of the ve years prior to thenancial crisis. By contrast, we expect the pace

of Eurozone growth to be less than two-thirds

of its pre-crisis average.

The economy is also in pretty robust nancial

health, which provides the foundations for

medium-term growth. Neither businesses nor

households are particularly highly leveraged.

Non-nancial companies have liabilities equal

to 95% of GDP, well below the Eurozone

average of 138%. Households have been

deleveraging since the early 2000s, with the

ratio of household debt to income falling from

115% to 92% at the end of 2012. Consequently,

both companies and households have the

scope to borrow more to fund additional

investment and spending. Surveys show that,

unlike their counterparts in the peripheral

Eurozone economies, German companies that

do not have the internal funds necessary to

fund investment have good access to credit. As

well as corporate balance sheets being sound,prots have reversed around 95% of the fall

they experienced during the 2008–09 global

nancial crisis.

Relatively low debt levels combined with

historically low borrowing rates, at 3.4% for

corporates and 7.8% for households, mean that

the debt-service burden is low. In addition, the

low amount of leverage means that households

and companies do not look particularly

vulnerable to a rise in interest rates. The

banking sector has also made good progress in

deleveraging and the Government is estimated

to have balanced its budget in 2012, four yearsahead of schedule.

Business investment andexports to drive a returnto growth in the rst half

of 2013

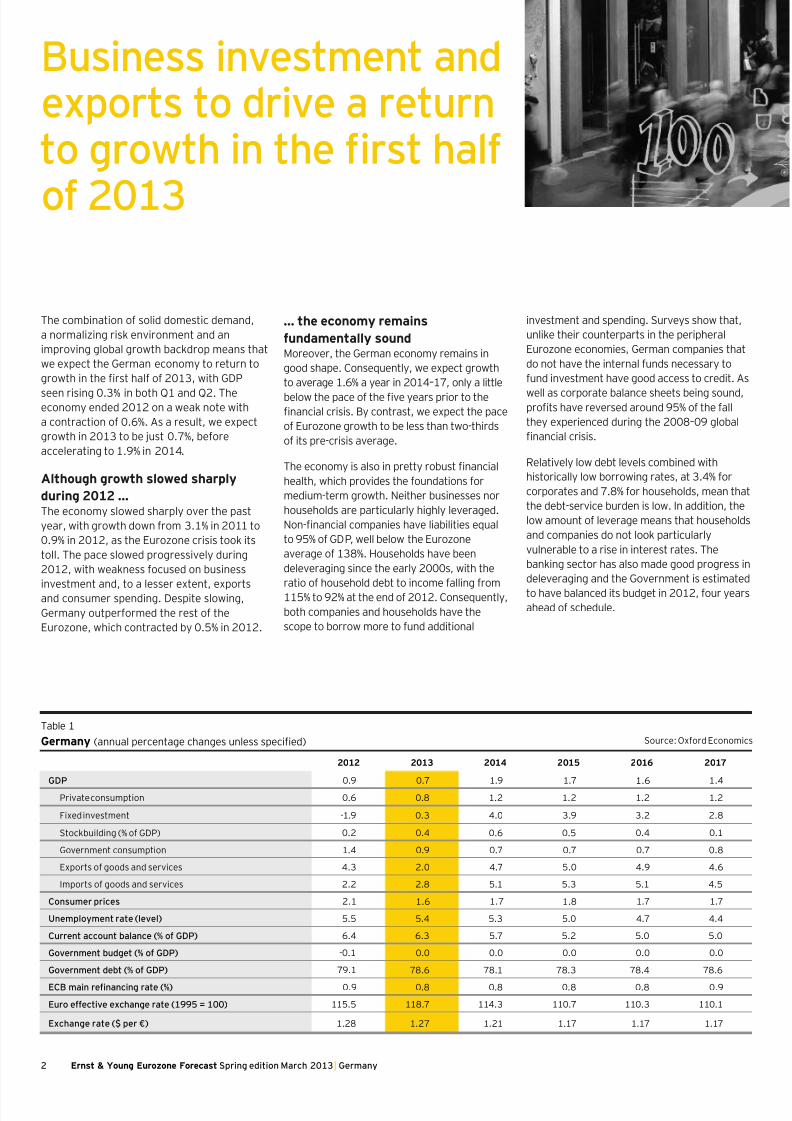

Table 1

Germany (annual percentage changes unless specied)

2012 2013 2014 2015 2016 2017

GDP 0.9 0.7 1.9 1.7 1.6 1.4

Private consumption 0.6 0.8 1.2 1.2 1.2 1.2

Fixed investment -1.9 0.3 4.0 3.9 3.2 2.8

Stockbuilding (% of GDP) 0.2 0.4 0.6 0.5 0.4 0.1

Government consumption 1.4 0.9 0.7 0.7 0.7 0.8

Exports of goods and services 4.3 2.0 4.7 5.0 4.9 4.6

Imports of goods and services 2.2 2.8 5.1 5.3 5.1 4.5

Consumer prices 2.1 1.6 1.7 1.8 1.7 1.7

Unemployment rate (level) 5.5 5.4 5.3 5.0 4.7 4.4

Current account balance (% of GDP) 6.4 6.3 5.7 5.2 5.0 5.0

Government budget (% of GDP) -0.1 0.0 0.0 0.0 0.0 0.0

Government debt (% of GDP) 79.1 78.6 78.1 78.3 78.4 78.6

ECB main renancing rate (%) 0.9 0.8 0.8 0.8 0.8 0.9

Euro effective exchange rate (1995 = 100) 115.5 118.7 114.3 110.7 110.3 110.1

Exchange rate ($ per €) 1.28 1.27 1.21 1.17 1.17 1.17

Source: Oxford Economics

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 5/8

3Ernst & Young Eurozone Forecast Spring edition March 2013 | Germany

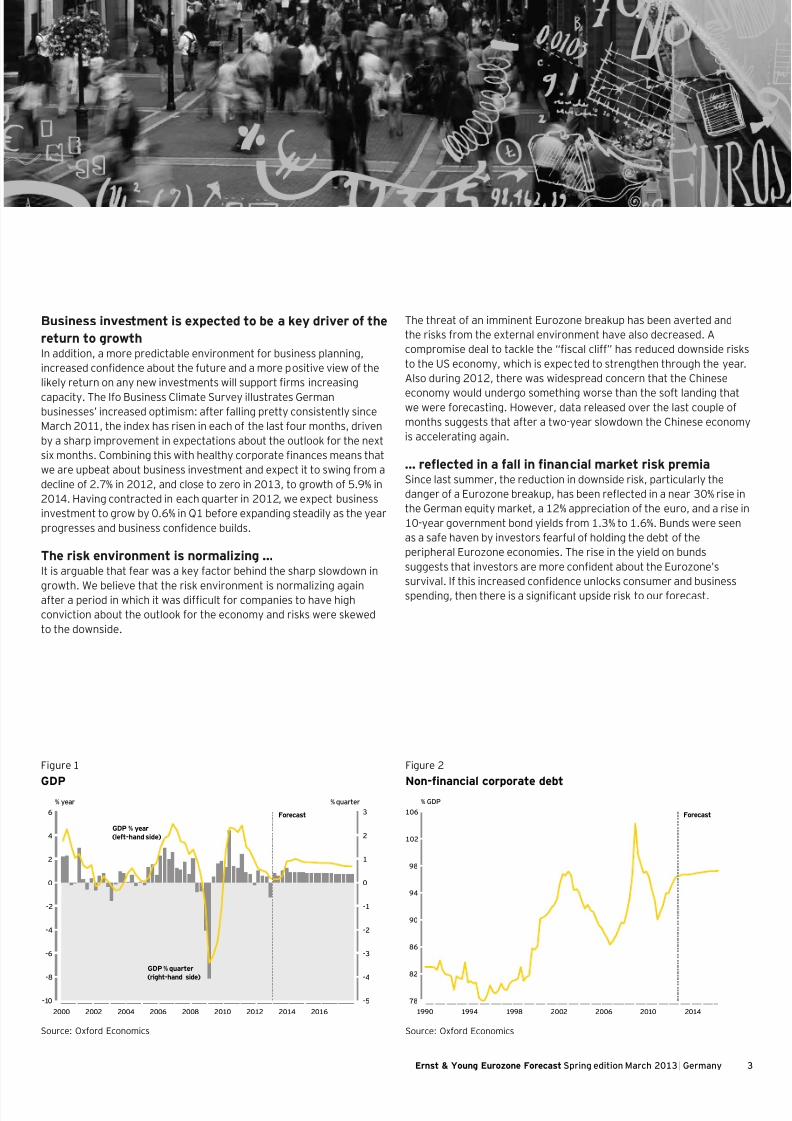

Figure 1

GDP

Figure 2

Non-nancial corporate debt

Source: Oxford Economics Source: Oxford Economics

Business investment is expected to be a key driver of the

return to growthIn addition, a more predictable environment for business planning,

increased condence about the future and a more positive view of the

likely return on any new investments will support rms increasing

capacity. The Ifo Business Climate Survey illustrates Germanbusinesses’ increased optimism: after falling pretty consistently since

March 2011, the index has risen in each of the last four months, driven

by a sharp improvement in expectations about the outlook for the next

six months. Combining this with healthy corporate nances means that

we are upbeat about business investment and expect it to swing from a

decline of 2.7% in 2012, and close to zero in 2013, to growth of 5.9% in

2014. Having contracted in each quarter in 2012, we expect business

investment to grow by 0.6% in Q1 before expanding steadily as the year

progresses and business condence builds.

The risk environment is normalizing …It is arguable that fear was a key factor behind the sharp slowdown in

growth. We believe that the risk environment is normalizing againafter a period in which it was difcult for companies to have high

conviction about the outlook for the economy and risks were skewed

to the downside.

The threat of an imminent Eurozone breakup has been averted and

the risks from the external environment have also decreased. A

compromise deal to tackle the “scal cliff” has reduced downside risks

to the US economy, which is expected to strengthen through the year.

Also during 2012, there was widespread concern that the Chinese

economy would undergo something worse than the soft landing thatwe were forecasting. However, data released over the last couple of

months suggests that after a two-year slowdown the Chinese economy

is accelerating again.

… reected in a fall in nancial market risk premiaSince last summer, the reduction in downside risk, particularly the

danger of a Eurozone breakup, has been reected in a near 30% rise in

the German equity market, a 12% appreciation of the euro, and a rise in

10-year government bond yields from 1.3% to 1.6%. Bunds were seen

as a safe haven by investors fearful of holding the debt of the

peripheral Eurozone economies. The rise in the yield on bunds

suggests that investors are more condent about the Eurozone’s

survival. If this increased condence unlocks consumer and business

spending, then there is a signicant upside risk to our forecast.

% quarter

Forecast

% year

GDP % year

(left-hand side)

GDP % quarter

(right-hand side)

-5

-4

-3

-2

-1

0

1

2

3

-10

-8

-6

-4

-2

0

2

4

6

2000 2002 2004 2006 2008 2010 2012 2014 2016

78

82

86

90

94

98

102

106

1990 1994 1998 2002 2006 2010 2014

% GDP

Forecast

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 6/8

4 Ernst & Young Eurozone Forecast Spring edition March 2013 | Germany

Figure 3

Condence

Figure 4

Unemployment

Source: Haver Analytics Source: Oxford Economics

l

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

74

78

82

86

90

94

98

102

106

110

114

2005 = 100 % Balance

Ifo expectations

(left-hand side)

Consumer confidence

(right-hand side)

2000 2002 2004 2006 2008 2010 2012

4

5

6

7

8

9

10

11

12

%

Forecast

1992 1995 1998 2001 2004 2007 2010 2013 2016

Resilient labor market underpins consumer spending However, our forecast assumes a modest pickup in consumer

spending, as households have typically shown themselves to be

cautious. Although investor sentiment and business condence have

both improved, the best that can be said about consumer condence

is that it may have stopped falling. Given that we do not expect theeconomy to slide into recession, we expect unemployment to stabilize

near current levels, averaging 5.4% on the ILO measure in 2013, down

a little from 2012.

A diminished fear of unemployment, combined with high employment,

strong household balance sheets and above-ination wage growth,

means that we expect consumer spending growth to accelerate from

0.6% in 2012 to 0.8% in 2013 and then 1.2% in 2014. And as it

becomes clear to consumers that the Eurozone is no longer in

imminent danger of breakup and that the risk environment is

normalizing, it is possible that the acceleration in consumer spending

growth could be faster than we are forecasting.

Exports should also recoverWeakness in exports contributed to the contraction in the German

economy at the end of last year. Although export order books have

only picked up a little so far, we expect the situation to improve during

the course of 2013 as world trade growth accelerates on the back of

an anticipated sharp pickup in the US economy and a reacceleration ofemerging market growth. As a result, we expect exports to swing from

contracting by 2% in Q4 2012 to growth of 0.7% in Q1 this year. Export

growth is forecast at 2% in 2013 and then 4.7% in 2014.

Euro appreciation may pose a new risk to the

economic outlookGiven the high proportion of German GDP accounted for by exports,

a further marked appreciation of the euro would pose a new risk to the

economy. However, it is a risk that is much less toxic than fears of a

Eurozone breakup. Businesses are used to dealing with currency

uctuations, having experienced such bouts of appreciation before.

Business investment andexports to drive a returnto growth in the rst half

of 2013

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 7/8

Follow the Eurozone’sprogress online

Please visit www.ey.com/eurozone to:

• View video footage of macroeconomists and Ernst & Young

professionals discussing the future of the Eurozone and

its impact on businesses

• Use our dynamic Eurochart to compare country data over

a ve-year period

• Download and print the Ernst & Young Eurozone Forecast

and forecasts for the 17 member states

Or follow our ongoing commentary on Twitter athttp://twitter.com/EY_Eurozone

7/27/2019 2013 March Ernst & Yang Report German Economy

http://slidepdf.com/reader/full/2013-march-ernst-yang-report-german-economy 8/8

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & Young

Ernst & Young is a global leader in assurance, tax, transaction and

advisory services. Worldwide, our 167,000 people are united by our

shared values and an unwavering commitment to quality. We make a

difference by helping our people, our clients and our wider communities

achieve their potential.

Ernst & Young refers to the global organization of member firms of

Ernst & Young Global Limited, each of which is a separate legal entity.

Ernst & Young Global Limited, a UK company limited by guarantee,

does not provide services to clients. For more information about our

organization, please visit www.ey.com.

© 2013 EYGM Limited.

All Rights Reserved.

EYG no. AU1474

In line with Ernst & Young’s commitment to minimize its impact on

the environment, this document has been printed on paper with ahigh recycled content.

This publication contains information in summary form and is therefore intended for general

guidance only. It is not intended to be a substitute for detailed research or the exercise of

professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young

organization can accept any responsibility for loss occasioned to any person acting or refraining

from action as a result of any material in this publication. On any specific matter, reference should

be made to the appropriate advisor.

ED None

EMEIA MAS 1354.0313

About Oxford Economics

Oxford Economics was founded in 1981 to provide independent

forecasting and analysis tailored to the needs of economists and planners

in government and business. It is now one of the world’s leading providers

of economic analysis, advice and models, with over 300 clients including

international organizations, government departments and central banksaround the world, and a large number of multinational blue-chip

companies across the whole industrial spectrum.

Oxford Economics commands a high degree of professional and technical

expertise, both in its own staff of over 70 professionals based in Oxford,

London, Belfast, Paris, the UAE, Singapore, New York and Philadelphia,

and through its close links with Oxford University and a range of partner

institutions in Europe and the US. Oxford Economics’ services include

forecasting for 190 countries, 85 sectors and over 2,500 cities and

sub-regions in Europe and Asia; economic impact assessments; policy

analysis; and work on the economics of energy and sustainability.

The forecasts presented in this report are based on information obtained from public sources

that we consider to be reliable but we assume no liability for their completeness or accuracy.

The analysis presented in this report is for information purposes only and Oxford Economics does

not warrant that its forecasts, projections, advice and/or recommendations will be accurate orachievable. Oxford Economics will not be liable for the contents of any of the foregoing or for the

reliance by readers on any of the foregoing.