©2014 cengage learning. all rights reserved. may not be scanned, copied or duplicated, or posted to...

TRANSCRIPT

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Financial Statement Analysis

Chapter 9

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Learning Objectives

After studying this chapter, you should be able to:

• Describe basic financial statement analytical methods

• Use financial statement analysis to assess the liquidity and solvency of a business

• Use financial statement analysis to assess the profitability of a business

• Describe the contents of corporate annual reports

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Describe basic financial statement analytical methods

Learning Objective 1

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Horizontal Analysis

• The percentage analysis of increases and decreases in related items in _______ financial statements

• Each item on the most recent statement is compared with the related item on one or more earlier statements in terms of the following:1. Amount of increase or decrease

2. Percent of increase or decrease

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Horizontal Analysis

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Vertical Analysis

• A percentage analysis used to show the relationship of each component to a total within _______ statement

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Benefits of Analysis

• Horizontal and vertical analysis are useful in assessing _______ and ______ in financial conditions and operations of a business

• ____________ is useful for comparing one company with another or with industry averages

• ____________ is made easier with common-sized financial statements

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Common-Sized Income Statement

• All items are expressed as ________ with no dollar amounts shown:

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Use financial statement analysis to assess the liquidity and solvency of a business

Learning Objective 2

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Liquidity and Solvency

• _______ – the ability of a business to convert assets into cash

• _______ – the ability of a business to pay its debts

Liquidity, solvency, and _______are interrelated!

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Solvency Analysis

• Normally assessed by examining __________ relationships, using the following major analyses:• Current position analysis• Accounts receivable analysis• Inventory analysis• Ratio of fixed assets to long-term liabilities• Ratio of liabilities to stockholders’ equity• Number of times interest charges are earned

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

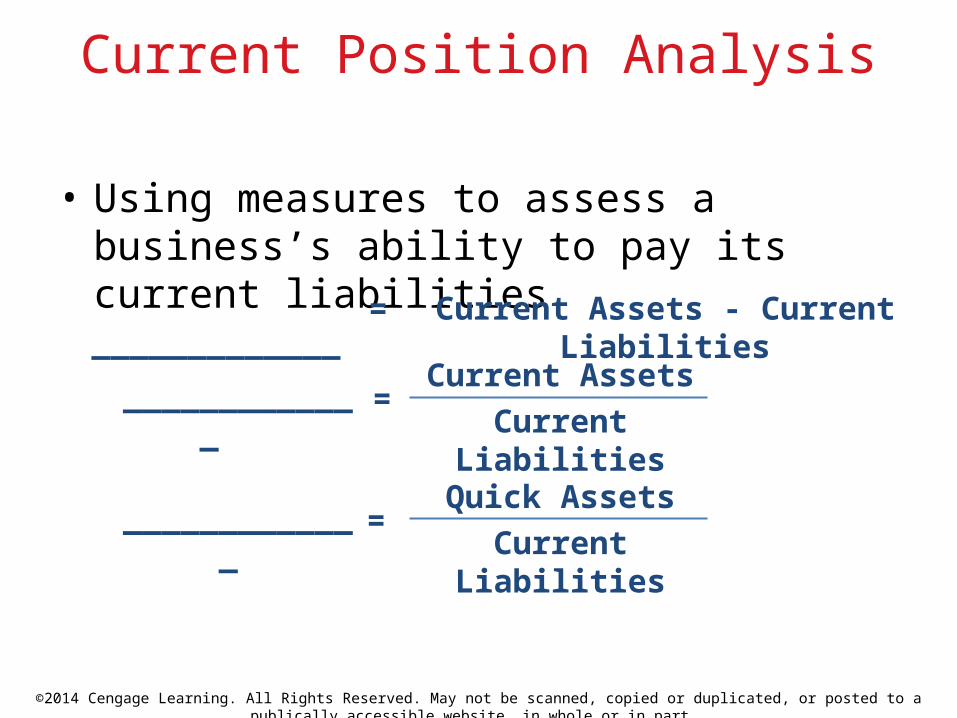

Current Position Analysis

• Using measures to assess a business’s ability to pay its current liabilities

_____________ Current Assets - Current Liabilities=

_____________

Current Assets

Current Liabilities=

_____________ Quick Assets

Current Liabilities=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Working Capital _____________ - ______________=

Working Capital

• To illustrate, the working capital for Mooney Company for 20Y6 and 20Y5 is computed below:

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Current Ratio

• To illustrate, the working capital for Mooney Company for 20Y6 and 20Y5 is computed below:

Current Ratio ______________

______________=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

$280,500 ÷ $210,000 =

Quick Assets$280,500

Quick Assets$160,000

Quick Ratio:

$160,000 ÷ $210,000 = 1.3

0.77

Mooney

Wendt

Quick Ratio

Quick Ratio ______________

______________=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Accounts Receivable Analysis

• Measures efficiency of ________• Reflects ________

Accounts Receivable Turnover

Number of Days’ Sales in Receivables

_________________________________

_____________________________/____

=

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Accounts Receivable Turnover

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Number of Days’ Sales in Receivables

=Number of Days’ Sales in

Receivables

______________

________________

Average Daily Sales __________ / ___=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Inventory Analysis

• Measures inventory efficiency• Avoid tying up funds in _______• Avoid obsolescence

• Reflects liquidity

Inventory Turnover ________________________________

Number of Days’ Sales in Inventory

________________

__________/___

=

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Inventory Turnover

Inventory Turnover ____________________________

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Number of Days’ Sales in Inventory

Number of Days’ Sales in Inventory

____________________

_____________________=

Average Daily Cost of Goods Sold

_________________ _______________=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

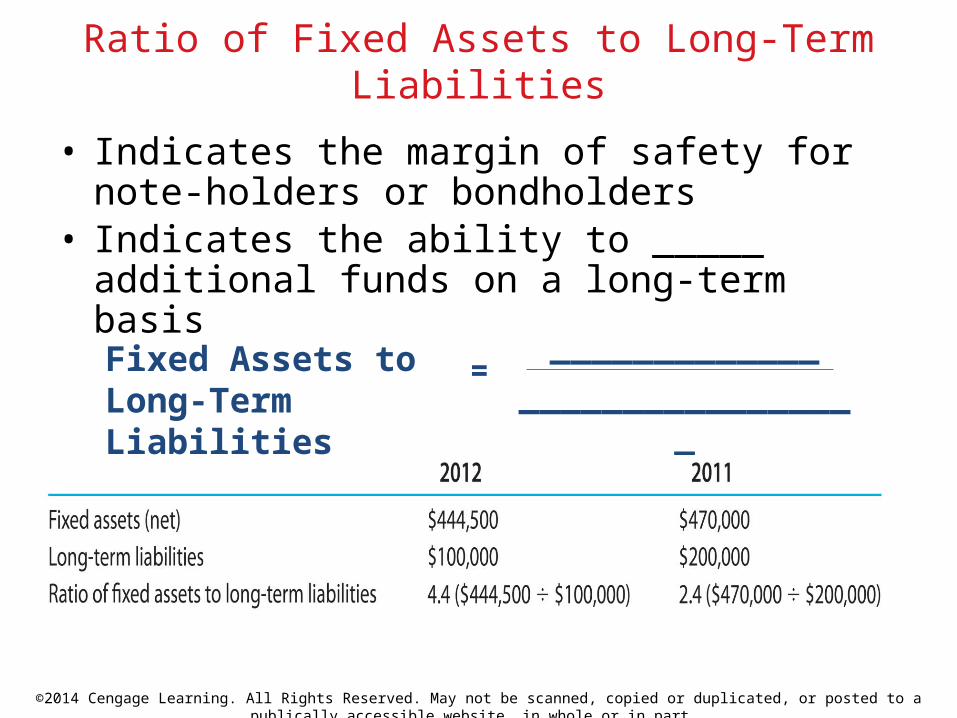

Ratio of Fixed Assets to Long-Term Liabilities

• Indicates the margin of safety for note-holders or bondholders

• Indicates the ability to _____ additional funds on a long-term basis

Fixed Assets to Long-Term Liabilities

_____________

_________________=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Ratio of Liabilities to Stockholders’ Equity

• Indicates the margin of safety for ______• Indicates the ability to withstand adverse

business conditions

Liabilities to Stockholders’ Equity

___________________________________

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Number of Times Interest Charges Earned

• Indicates the general financial strength of the business

• Indicates the ability to withstand adverse business conditions

Times Interest Charges Earned

______________ + ________________________________

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Use financial statement analysis to assess the profitability of a business

Learning Objective 3

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Profitability Analysis

• Normally assessed by examining the income statement and balance sheet resources, using the following major analyses:• Ratio of net sales to assets• Rate earned on total assets• Rate earned on stockholders’ equity• Rate earned on common stockholders’ equity• Earnings per share on common stock• Price-earnings ratio• Dividends per share• Dividend yield

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

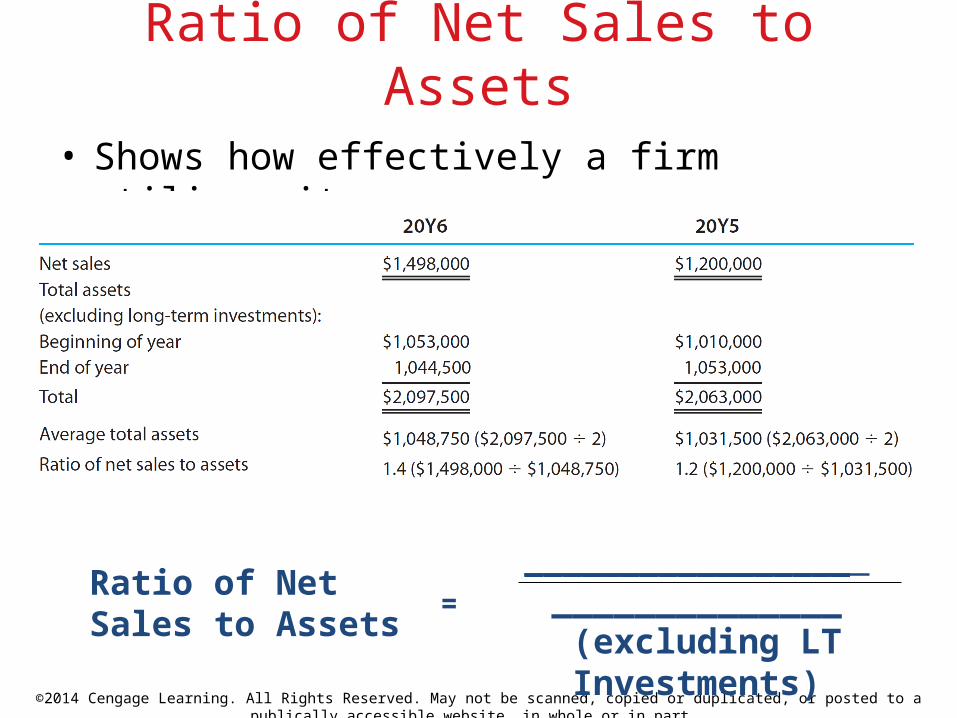

Ratio of Net Sales to Assets

• Shows how effectively a firm utilizes its ______

_________________ ______________

(excluding LT Investments)

Ratio of Net Sales to Assets

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Rate Earned on Total Assets

• Measures the profitability of ________ without considering how the assets are financed

________ + __________ _________________

Rate Earned on Total Assets

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Rate Earned on Stockholders’ Equity

• Emphasizes the rate of income earned on the amount invested by the __________

________________ _____________________

Rate Earned on Stockholders’ Equity

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Leverage

• The effect of leverage for 20Y6 is 3.1% which compares favorably with the 2.7% leverage for 20Y5

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

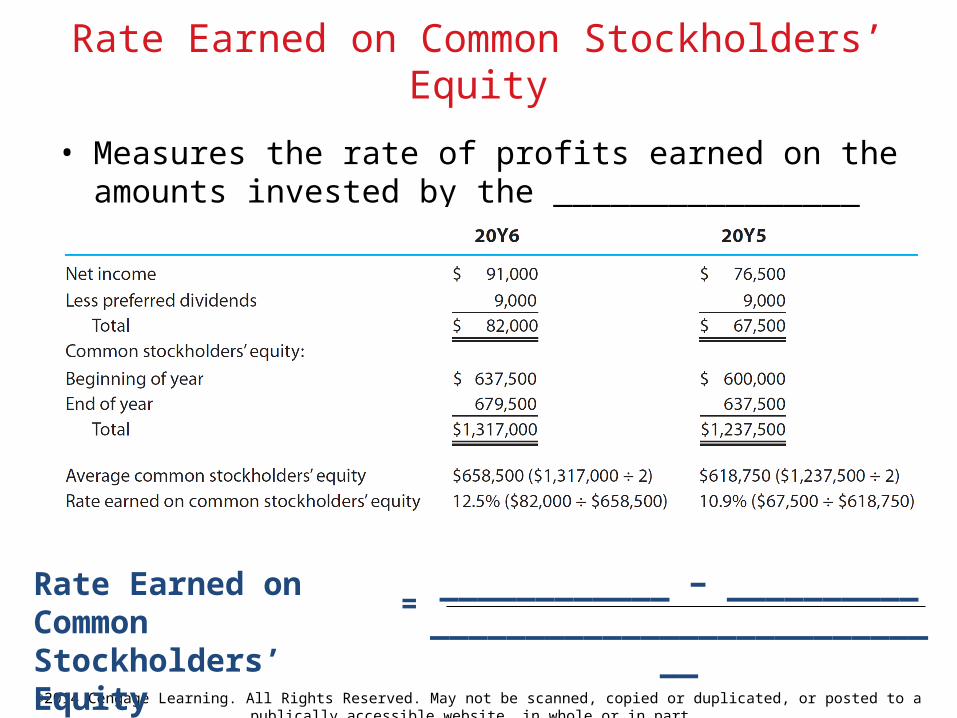

Rate Earned on Common Stockholders’ Equity

• Measures the rate of profits earned on the amounts invested by the ________________

____________ − ______________________________________

Rate Earned on Common Stockholders’ Equity

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Earnings Per Share on Common Stock

• The income earned for each share of _________

____________ − ______________________________________

Earnings per Share on Common Stock

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Price-Earnings Ratio

• Price-earnings (P/E) ratio on common stock measures a firm’s future _________ prospects

________________________________________________________________

P/E Ratio =

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Dividends per Share

Dividends per Share ____________________________________________

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Dividend Yield

• Dividend yield shows the rate of return to common stockholders in terms of cash dividends

Dividend Yield _____________________________________ _____________________________________

=

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Describe the contents of corporate annual reports

Learning Objective 4

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Corporate Annual Reports

• Summarize operating activities for the past year and plans for the future

• Many variations in the order and form, but all include:• Management’s _______ and ________• Report on __________• Report on ______ of the financial statements

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Management Discussion and Analysis (MD&A)

• Provides critical information in interpreting the ____________ and assessing the future of the company

• Includes an analysis about __________ and financial condition

• Discusses management’s _______ about future performance

• Discusses significant _____ exposure• Management’s assessment of the company’s

_________ and the availability of capital to the company

• Any “___________” arrangements such as leases not included directly in the financial statements

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

Independent Auditors’ Report

• Publicly traded companies must get an independent opinion on the fairness of the ________________

• The ______________________ (CPA) firm that conducts the audit renders an opinion, called the Report of Independent Registered Public Accounting Firm, on the fairness of the statements

• This opinion must be included in the ____________ along with an opinion on the accuracy of management’s internal control assertion

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publically accessible website, in whole or in part.

End of Chapter 9