2015 full year results april 2016 - alliance...

TRANSCRIPT

John Dawson – Chief Executive

Andrew Franklin – Chief Financial Officer

2015 Full Year Results

April 2016

2

Highlights

Sales £48.3m (2014: £43.5m)

Hydromol™ continues to demonstrate good growth, year on year of +10% to £6.6m

MacuShield™ acquisition £3.5m sales

Sinclair acquisition £0.8m sales

Pre-tax profits £11.4m* (2014: £10.8m)

Free cash flow £6.3m (2014: £10.3m) after acquisition of £4.7m Sinclair inventory

Net debt : EBITDA at 2.8 times

Sanofi settlement of net £6.3m received in connection with ImmuCyst™

Acquisitions

Transformational acquisition from Sinclair IS in December 2015 - £127.5m

MacuShield Ophthalmology / OTC product in February 2015 - £8.8m

Diclectin™ in-licensed January 2015 - £1.5m

Sinopharm – five child nutrition brands in China in September 2015

Final and full year dividend up 10%

Adjusted EPS 3.69p (2014: 3.36p)

*Before the exceptional and non-underlying items, being primarily

compensation from Sanofi and Sinclair acquisition costs

3

Company Background

and Strategy

4

Background to Alliance

Started in 1998 as a specialty pharma company, using a Buy and Build model

Profitable, cash generative and dividend paying

Strong track record of 31 deals in 17 years building up a portfolio of over 90 products

Balanced portfolio:

Actively managed - organic growth from prescription and consumer products in:

Dermatology

Mother and Child

Ophthalmology

Passively managed - bedrock of sustainable cash flow from core of established niche medicines,

typically with limited competition

Sales mainly in Western Europe, but also in 90+ other countries

Direct presence in UK, Germany, France, Italy, Spain and Ireland

Office in China plus two joint ventures

Other countries via distribution partners

Virtual operating model with manufacturing, warehousing and logistics outsourced

5

Portfolio and Organisation

Promoted areas:

Dermatology

Mother & Child

Ophthalmology

Balance of actively promoted (52%) and passively managed bedrock (48%)

Geographic spread:

50% UK

75% Western Europe

Contender for pan-European opportunities

25% Rest of World

Organisation

Chippenham UK – Group and UK affiliate

Paris – International partnerships management and French affiliate

Other European affiliate offices in Dusseldorf, Milan and Madrid

“Wholly Owned Foreign Enterprise” in Shanghai plus two JVs (Shanghai and Guangzhou)

6

Balanced Portfolio

The bedrock: core portfolio of non-promoted products

48%

Dermatology

32%

Kelo-cote

Hydromol

Flammazine/

Flammacerium

Aloclair

Atopiclair

Lypsyl

Mother & Child

16%

Diclectin,

Kelo-stretch

Forceval/Fushifu,

Suprememil

Ashton & Parsons

Anbesol, Alovex

Syntometrine, MolluDab,

Timodine, Oxyplastine

Ophthalmology

4%

MacuShield

Percentages refer to pro forma sales in the 12 months to December 2015, including share of joint ventures

7

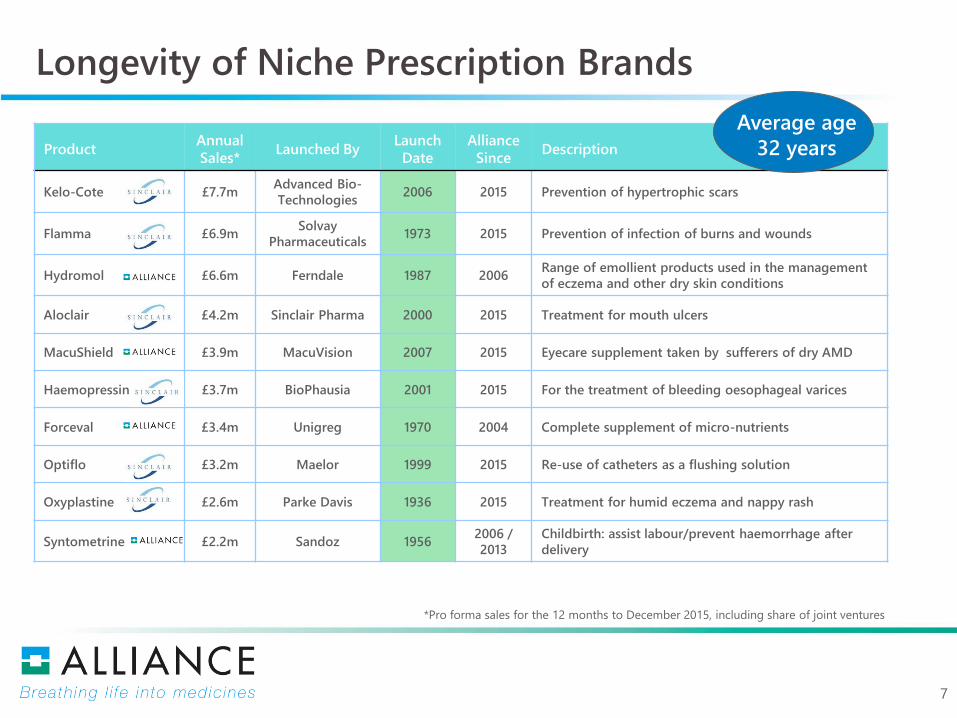

Longevity of Niche Prescription Brands

ProductAnnual

Sales*Launched By

Launch

Date

Alliance

SinceDescription

Kelo-Cote £7.7mAdvanced Bio-

Technologies2006 2015 Prevention of hypertrophic scars

Flamma £6.9mSolvay

Pharmaceuticals1973 2015 Prevention of infection of burns and wounds

Hydromol £6.6m Ferndale 1987 2006Range of emollient products used in the management

of eczema and other dry skin conditions

Aloclair £4.2m Sinclair Pharma 2000 2015 Treatment for mouth ulcers

MacuShield £3.9m MacuVision 2007 2015 Eyecare supplement taken by sufferers of dry AMD

Haemopressin £3.7m BioPhausia 2001 2015 For the treatment of bleeding oesophageal varices

Forceval £3.4m Unigreg 1970 2004 Complete supplement of micro-nutrients

Optiflo £3.2m Maelor 1999 2015 Re-use of catheters as a flushing solution

Oxyplastine £2.6m Parke Davis 1936 2015 Treatment for humid eczema and nappy rash

Syntometrine £2.2m Sandoz 19562006 /

2013

Childbirth: assist labour/prevent haemorrhage after

delivery

Average age

32 years

*Pro forma sales for the 12 months to December 2015, including share of joint ventures

8

Risk Reduction Through Diversity

Kelo-cote9%

Flamma8%

Hydromol7%

Aloclair5%

MacuShield4%

Haemopresin4%

Forceval4%

Optiflo4%

Oxyplastine3%

Syntometrine2%

Other50%

Revenue over 90 products

Pro forma

revenue in the

12 months

ended 31

December 2015,

including share

of joint

ventures

UK51%

France10%

APAC8%

MEA7%

CEE & LATAM

7%

DACH5%

ROI4% Italy

3%

Spain2% JV

2%Others

1%

Geographical split over

100 countries

Pro forma

revenue in the

12 months

ended 31

December 2015,

including share

of joint ventures

9

Buy & Build – Acquisitions Over Past 10 Years

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

C A R A D E R M

Syntometrine

£2.0m

Atarax

Deltacortril

Terracortrill

£1m

Permitabs

£0.8m

Dermamist

£0.26m

Hydromol

£3.3m

Pavacol D

£0.6m

Buccastem

Timodine

£7.5m

Cambridge

£16.4m

Quinoderm

Ceanel

£1.5m

Rizuderm +

5 Products

£2.4m

Anbesol

Ashton &

Parsons

£2.26m

Opus

£8mLypsyl

£1.9m

Syntometrine

(excl. UK)

£7.5m

Irenat

(Germany)Forceval

China

£1.95m

MacuShield

£5.5 - 11.5m

Antimalarials

£4.2m

31 deals in 17 years

Every year since 2006

Sinopharm

Sinclair

£127.5m

Diclectin

£1.5m

10

Sinclair Products Acquisition – December 2015

Largest acquisition to date

£127.5m plus £5m inventory

£39.4m sales to December 2015

£81m (net) equity raised at 41p

£100m new debt facility from Lloyds, RBS and Silicon Valley Bank

£75m drawn down: £56m for acquisition, £19m to close previous facility

Transformational deal

Market cap from £120m* to £237m**; Enterprise Value from £141m to £308m

Approximate doubling of sales, profits, people

Delivers pan-EU5 footprint to facilitate future opportunities

Strengthens China business and provides a base in SE Asia

Provides potential territories for original Alliance brands

*16th December 2015

**6th April 2016

11

Other Deals in 2015

MacuShield: £8.8m – February 2015

2015 sales £3.5m +13% (Pro-forma sales £3.9m)

90% UK & Ireland – significant international potential

Sinopharm: September 2015

Five child nutrition brands add to Mother & Child franchise in China

£1.5m sales in 12 months to March 2015

Diclectin in-licensing for UK: £1.5m – January 2015

In registration – launch expected H1 2017

Will be UK’s only licensed product for nausea and vomiting of pregnancy

Been on Canadian market for over 30 years

US approval by FDA two years ago – sales running at $160m pa

12

Hydromol – Range of emollients for remission of eczema

2015 sales £6.6m; largest territory UK

Kelo-cote™ – Scar reduction

2015 sales £7.7m; largest territory China

Flammazine™ / Flammacerium™ – Anti-infective for burns

2015 sales £6.9m; largest territory France

Aloclair™ – Oral lesions

2015 sales £4.2m; largest territory Italy

Atopiclair™ – Atopic eczema

2015 sales £1.7m; largest territory SE Asia

Papulex™ – Acne

2015 sales £1.5m; largest territory SE Asia

Dermatology – £28m / 32% of Sales

13

Mother & Child – £15m / 16% of Sales

Fushifu™ (Forceval™) – micronutrient support in pregnancy2015 sales £0.9m (60% share) / China

Diclectin – nausea and vomiting of pregnancyIn registration (expected approval H1 2017) / UK

Kelo-stretch™ – avoidance/reduction of stretchmarks2015 sales £1.5m / largest territory SE Asia

Syntometrine™ – prevention of post-partum haemorrhage2015 sales £2.2m / largest territory UK

Suprememil™ – infant formula milk2015 sales £0.4m (20% share) / China

Ashton & Parsons Infants’ Powders™ – calming relief from teething2015 sales £1.5m / UK

Anbesol™ – pain relief for teething2015 sales £1.5m / UK

Timodine™ – infected nappy rash2015 sales £1.6m / UK

Oxyplastine™ – barrier cream for nappy rash2015 sales £2.3m; largest territory MEA

14

Ophthalmology / MacuShield- Sales in 2015 £3.5m (+13% pa)

Macula is the region at the back of the eye (retina) for central vision

Three carotenoid (macular) pigments found there

Meso-zeaxanthine

Zeaxanthine

Lutein

Macular pigments filter out high energy blue light

Reduce glare (eg night-time driving)

Improve contrast sensitivity (eg sport)

Anti-oxidant and reduce oxidative stress (damage to photo-receptors)

Stabilise or reverse age-related macular degeneration (AMD)

Risk factors: poor diet, smoking, genetics

Largest cause of blindness in the elderly

500,000 registered cases in UK alone

MacuShield supplements dietary macular pigments

Only product containing lutein, zeaxanthine and meso-zeaxanthine (patented)

Promoted scientifically to optometrists / supplied commercially via consumer channels

Territories – EU + CH, N, Russia, E Europe, AUS, NZ, SA (currently 75% sales UK)

15

2015 Results

1616

2015 Full Year Results – Summary

Revenue £48.3m (2014: £43.5m)

Including Sinclair sales of £0.8m

Gross margin rate of 59.4% (2014: 57.5%)

Operating profit £12.5m* (2014: £11.8m**)

Adjusted pre-tax profit £11.4m* (2014: £10.8m**)

Reported pre-tax profit £15.2m (2014: £10.2m)

Adjusted diluted EPS 3.61p* (2014: 3.34p**)

Diluted EPS 4.55p (2014: 3.16p)

Free cash flow £6.3m (2014: £10.3m)

After acquisition of £4.7m Sinclair inventory

Net bank debt £71.5m (2014: £21.1m), with gearing at 2.8 times EBITDA

Final dividend up 10% to 0.734p (2014: 0.667p)

Total dividend up 10% to 1.100p (2014: 1.000p)

*Before the exceptional and non-underlying

items (primarily compensation from Sanofi

and Sinclair acquisition costs)

** Before impairment of Pavacol-D

17

Performance Comparison

£43.5m

£48.3m

40.0

42.0

44.0

46.0

48.0

50.0

2014 2015

£m

Sales

3.16p

4.55p

3.34p3.61p

-

1.00

2.00

3.00

4.00

5.00

2014 2015

Pen

ce

Basic & adjusted diluted EPS

Basic Diluted EPS

Adjusted Diluted EPS

£10.8m

£11.4m

10.4

10.6

10.8

11.0

11.2

11.4

11.6

2014 2015

£m

Underlying PBT

1.00p

1.10p

0.95

1.00

1.05

1.10

1.15

2014 2015

Pen

ce

DPS

18

2015 Sales Movements

2015

£m

2014

£m

Change

£m

MacuShield February 2015 acquisition3.5

0.8

6.6

-

-

6.0

+3.5

+0.8

+0.6

Sinclair Sales December 2015 acquisition

Hydromol Growth of 10%

Forceval Capsules Recover from stock-out 2.1 1.5 +0.6

Other Consumer Growth from promotion 4.1 3.7 +0.4

Fostered Products Handed back in 2014 - 1.6 (1.6)

Nu-Seals Generic competition 1.9 2.5 (0.6)

Quinoderm API unavailable 0.2 0.5 (0.3)

Other 29.1 27.7 +1.4

Group 48.3 43.5 +4.8

Share of China joint ventures 1.3 2.0 (0.7)

Total 49.6 45.5 4.1

19

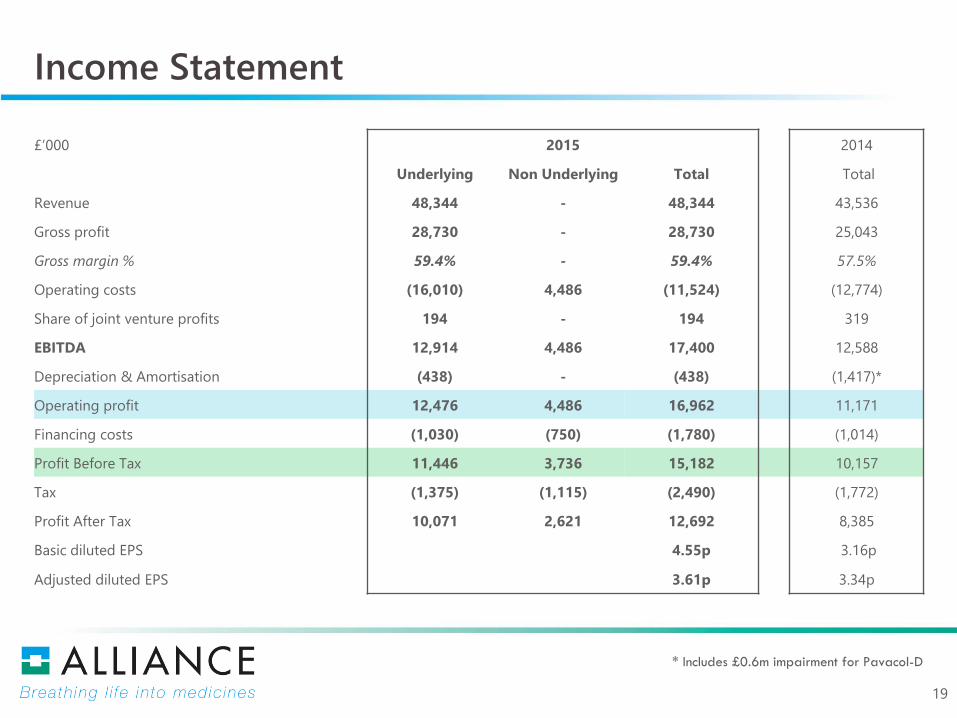

Income Statement

£’000 2015 2014

Underlying Non Underlying Total Total

Revenue 48,344 - 48,344 43,536

Gross profit 28,730 - 28,730 25,043

Gross margin % 59.4% - 59.4% 57.5%

Operating costs (16,010) 4,486 (11,524) (12,774)

Share of joint venture profits 194 - 194 319

EBITDA 12,914 4,486 17,400 12,588

Depreciation & Amortisation (438) - (438) (1,417)*

Operating profit 12,476 4,486 16,962 11,171

Financing costs (1,030) (750) (1,780) (1,014)

Profit Before Tax 11,446 3,736 15,182 10,157

Tax (1,375) (1,115) (2,490) (1,772)

Profit After Tax 10,071 2,621 12,692 8,385

Basic diluted EPS 4.55p 3.16p

Adjusted diluted EPS 3.61p 3.34p

* Includes £0.6m impairment for Pavacol-D

20

Cash Flow

£’m 2015 2014

Operating profit 17.0 11.2

Depreciation and Amortisation 0.4 1.4*

Share options 0.6 0.6

Working capital (8.2) 0.3

Cash flow from trading 9.8 13.5

Financing costs (1.0) (1.0)

Capital expenditure (0.6) (0.2)

Tax paid (1.9) (2.0)

Free cash flow 6.3 10.3

Acquisitions (133.9) (3.8)

Equity raised (net of issue costs) 81.0 -

(Payment)/receipt of borrowings (net of fees) 51.3 (1.7)

Dividend (2.6) (2.4)

Net movement in cash and cash equivalents 2.1 2.4

* Includes £0.6m impairment of Pavacol-D

21

Balance Sheet

£’m Dec 15 Dec 14 Change

Intangibles: Product licences 259.9 88.9 +171.0

Joint ventures 2.9 2.7 +0.2

Inventories 12.9 5.9 +7.0

Trade and other receivables 11.6 8.3 +3.3

Trade and other payables (13.9) (6.9) (7.0)

Taxes (current and deferred) (39.4) (7.1) (32.3)

Other net assets (0.1) 0.1 (0.2)

Net cash / overdraft 3.2 1.0 +2.2

Bank loans (74.7) (22.1) (52.6)

Net bank debt (71.5) (21.1) (50.4)

Equity 162.4 70.8 +91.6

22

Summary

23

Summary

2015 was a good year for the original Alliance business:

Sales £48.3m (+11.0%)

New growth area with MacuShield in AMD

In-licensing of Diclectin for nausea and vomiting of pregnancy

Underlying PBT £11.4m (+5.5%)

Underlying EPS 3.61p (+8.1%)

Dividend raised by 10% to 1.1p for the full year

The transformational Sinclair acquisition facilitates the buy and build strategy

Approximate doubling of sales, profits, people

Strengthens Alliance’s Dermatology offering

Strengthens Alliance’s Mother and Child offering

A 50/50 portfolio balance between growth and bedrock products is maintained

Delivers pan-EU5 footprint to facilitate future opportunities (75% of sales)

Strengthens China business and provides a base in SE Asia

Provides new potential territories for original Alliance brands

Greater financial scale opens up potentially larger M&A opportunities in the future

24

Appendices

24

25

Top 20 Investors: 1 March 2016

Holder / Fund Manager No. of Shares % Holding

Director & Related 62,182,788 13.28%

MVM Life Science Partners 55,561,900 11.87%

Aviva Investors Global Services 44,982,748 9.61%

Artemis Fund Managers Ltd 37,583,219 8.03%

Nigel Wray 37,376,510 7.98%

Slater Investments 33,947,038 7.25%

Fidelity Management & Research 33,513,321 7.16%

River & Mercantile Asset Management 24,000,000 5.13%

Hargreave Hale 11,994,159 2.56%

Franklin Templeton Investments 11,750,000 2.51%

Brown Shipley Asset Management 11,599,706 2.48%

LGT Capital Management 9,890,832 2.11%

Brown Brothers Harriman & Co 8,120,455 1.73%

BlackRock Investment Management (UK) 7,930,847 1.69%

Henderson Global Investors 6,796,204 1.45%

Cavendish Asset Management 5,994,000 1.28%

Smith & Williamson Investment 4,740,694 1.01%

Threadneedle Asset Management 4,214,732 0.90%

Redmayne Bentley Stockbrokers 3,774,849 0.81%

Barclays Wealth Management (UK) 3,199,286 0.68%

Total No of Share Owners: 934 No of Shares in Issue: 468,304,266

26

Board Members

John Dawson – Chief Executive Officer

Tony Booley – Executive Director

Andrew Franklin – Chief Financial Officer Peter Butterfield – Chief Commercial Officer

Andrew Smith – Chairman

Thomas Casdagli – Non-Executive Director

Pharmacist, MSc Finance; > 40yrs’ sector

experience, founder of Alliance

Director – International

BSc Physiology, MBA, Chartered Marketer;

30yrs’ sector experience, with Alliance since 1998

Former UK Commercial Director of Cambridge

Laboratories Ltd, graduated in Pharmacology from

University of Edinburgh

Senior positions held at SmithKline Beecham

Pharmaceuticals, Diversified Health Systems Europe,

Cerebrus plc and Parexel International

Partner in MVM Life Science Partners, Chartered

Accountant, graduated from Oxford in Molecular and

Cellular Biochemistry, joined March 2009

David Cook – Non-Executive Director

CFO and Chief Business Officer at Biotie Therapies

Inc. Chartered Accountant, graduated in

Chemistry from Oxford. Joined Alliance April 2014

Nigel Clifford – Non-Executive Director

CEO of Ordnance Survey. Previously held senior

positions at Procserve Holdings, Micro Focus Int plc,

Nokia, Symbian Software. Graduated in Geography from

the University of Cambridge

Former General Manager – European Tax and Accounting

at Panasonic. Prior to that, Finance Director of Genzyme

Therapeutics Ltd and 12 years pharmaceutical experience

in senior financial positions at Wyeth.

27

Senior Team Members

Janice Timberlake – Chief Human

Resources Officer

Fellow of CIPD with over 20 years of experience

in HR roles. Previous senior roles in My Travel

plc and National Environment Research Council.

NED and Trustee of Plymouth Marine

Laboratory Ltd, BSc Hons in Geography from

Hull University. Joined in 2011.

Dan Thomas – Chief Corporate

Development Officer

Since joining in 2006, has led Alliance’s M&A

and licensing activity, completing over 14 deals.

Has worked in Canada, Germany and France.

He holds a first class honours degree in Applied

Biochemistry from Brunel University. In 2011

Dan won the PLG/Astra Zeneca BD Executive of

the Year award.

Stephen Kidner – Chief Scientific &

Operations Officer

Sarah Robinson – Company Secretary

Over 23 years’ experience in pharma

development, manufacturing and supply chain

management gained with Wyeth and

Mundipharma International. BSc in Chemistry

from University of Wales, Swansea, MSc in

Pharmaceutics from Manchester and an MBA

from The Open University. Joined in 2013.

Over 20 years’ experience in the health and

financial services sectors, including Company

Secretary at the Financial Times and Investors

Chronicle jointly for 7 years. Has worked in

Asia, the UK and the USA. A Chartered

Secretary with an MBA from Southampton

University. Joined in 2010.

28

Product Portfolio

29

Product Portfolio

30

Product Portfolio

31

Product Portfolio

32

Product Portfolio

33

Product Portfolio

34

Product Portfolio

35

Product Portfolio

36

Product Portfolio