2015 - greater bank limited · greater building society ltd. abn 88 087 651 956. afsl/australian...

TRANSCRIPT

2015Annual Report

Contents

Chairman’s Report 01

CEO’s Report 03

Our Community 05

The Greater Charitable Foundation 09

Financial Statements 30 June 2015 11

Head Off ice: 103 Tudor Street Hamilton NSW 2303 PO Box 173 Hamilton NSW 2303 P 1300 651 400 F 02 4921 9112

Greater Building Society Ltd. ABN 88 087 651 956. AFSL/Australian Credit Licence No. 237476.

Annual Report | 2014-15Greater Building Society 0201

Chairman’s ReportI am pleased to report another strong year of performance for the Greater Building Society.

As The Greater is a customer owned financial banking organisation, the role of the Board is to protect and enhance long-term value for customers. The Board and Management have been developing a new strategy to deliver upon our mantra of customer first. The strategy is built around five broad pillars:

• Sustainably grow our customer base in target markets,

• Improve organisational efficiency,

• Proactively manage regulatory change and risk,

• Strengthen business capabilities (people, processes and systems), and

• Commit to corporate social responsibility.

This strategy is designed to ensure that The Greater continues to remain relevant and sustainably grow in a rapidly changing and highly competitive environment. While the strategy is still being implemented, our new CEO and his team are already embracing change. The CEO’s report details a number of specific achievements this year.

Our strong financial performance is good news for customers and the community. It allows The Greater to invest in the changes required for IT, core banking, products and systems to be able to offer customers even better products and services. It also allows us to continue to support the communities in which we operate through sponsorships as well as funds to The Greater Charitable Foundation. The Greater’s Capital Adequacy Ratio is again growing to exceed regulator requirements and ensure continued strength and stability.

We want to continue our history of strong financial performance, value for customers, outstanding service and support for the community while positioning The Greater to be more nimble. Being nimble is important for us to be able to anticipate and respond to customers’ changing needs as well as changes to the industry and regulatory environment.

Corporate Governance and Risk Management

The Greater has a proud history of good governance and risk management. We manage risks consistent with the best interests of customers and the long term, sound financial performance of the business.

The Board and Management have continued to strengthen their governance and risk management consistent with Prudential Standard CPS 220 Risk Management.

The Risk and Audit committees of the Board are now separate to allow a greater focus on both important aspects of the business and a demonstration of its commitment to risk management principles.

The Greater employs risk-based decision-making and oversight across all operations. The Board sets the tone from the top to ensure a sound risk culture is maintained and communicated via The Greater’s business strategy, risk appetite, understanding of risk and capabilities, as well as how risk management behaviours are encouraged and rewarded.

The Greater’s comprehensive, three lines of defence structure and Risk Management Framework are incorporated explicitly into all Greater policies. The framework allows us to identify, analyse and manage the current and emerging risks within the business. The Board is actively monitoring its risk profile to ensure that activities undertaken to achieve strategic objectives are within risk appetite.

Through the Board committees, a Chief Risk Officer (CRO) and external support, we ensure oversight of the risk profile and risk management as well as independent reporting lines to appropriately escalate issues.

Board performance

The Board and each of its committees have a charter to guide roles and responsibilities in compliance with APRA’s CPS 510 Governance and CPS 520 Fit and Proper.

Board members continue to undertake ongoing professional development activities and regularly attend Australian Institute of Company Directors events and forums to enhance their role as Directors. In addition, the Board engages external consultants to assist it with an annual review of Board performance.

Support for community

One benefit for customers banking with the customer owned Greater is that profits are invested back into improved services as well as support for their community.

The Board again provided $1.2M to The Greater Charitable Foundation this year. Those funds are being used by The Greater Charitable Foundation to provide grants to a number of outstanding charities that are making a real difference to the lives of families and a stronger community.

The future – a name change

The Board is committed to driving change to ensure The Greater remains relevant and viable to provide much needed competition to the major banks for the benefit of customers. An important change we must make is to our name. The term building society does not adequately reflect the services we provide and is not well understood, particularly by younger people.

Changing our name to Greater Bank better reflects what we do – which is to provide a comprehensive range of banking services. If the name change is approved at the AGM we will remain a mutual (customer owned). The only major change existing customers will see is more people joining them to experience our award-winning service and greater value products and services, making us even stronger and better able to offer even more value to customers and the community.

Thank you to my fellow Directors, Management and employees for their contribution to The Greater’s excellent results. I also thank them for their support for the need to change to continue to put customers first.

Wayne Russell Chairman

Greater Board Members; Front L to R: Malcolm McDonald, Jayne Drinkwater, Wayne Russell; Middle L to R: Roger Cracknell, Scott Robinson; Back: Russell Ware

Chairman, Wayne Russell

Annual Report | 2014-15Greater Building Society 0403

This is my first report as CEO and I am pleased to report this financial year has been an excellent one. Below is an overview of achievements made against the five pillars of our new strategic approach.

Sustainably grow our customer base

Against the trend of many peers we welcomed more customers to The Greater, particularly in 2015. This stems from the work we started this year to better understand what customers are looking for in terms of our branding, distribution and service capabilities.

Providing outstanding customer service has always been at the centre of our success. This was recognised when we took out a national Roy Morgan Customer Satisfaction Award for the second year running with ratings as high as 97%.

Offering the best customer experience and attracting more customers comes down to more than friendly, expert employees. We reviewed our product features, and continue to review our pricing, to ensure our products are sharp and fit for purpose. Two of our loans received accolades in the Mozo Experts Choice Awards and Australian Lending Awards. We introduced a new low fee, high interest youth savings account that is proving very popular.

Our Straightforward Banking campaign positions The Greater as a financial institution that offers customers simple, honest banking. We are straightforward but also increasingly sophisticated in our product and service offering.

The Greater is a leader among customer owned financial institutions in digital banking and use of social media. This year we introduced a new, plain English, customer centric website that is seamless across all platforms. Digital banking improvements included enhanced mobile banking apps with four-digit PINs for faster login, account balances available directly after login, on the go set up of new payees and billers, as well as the Australian first of Direct Debit SMS alerts.

Improve organisational efficiency

Our solid profit result demonstrates we are a strong, well-managed, efficient financial institution.

Our group profit of $34.95M is up 11% on last year and comprehensive income is up 17% to $36.4M. This result reflects continued focus on cost reduction as well as doing things simpler and smarter. We’ve also started to see some very good asset growth, particularly over the last eight months of the year. At the end of the year, total assets were $5.4 billion, up 6.2%.

Loan growth was modest at just over 2.2% – a sound result given the competitive environment. Importantly, lending growth strengthened in the second half of the year with net loan approval numbers at their highest since 2011. We consciously grew deposits (up 6.2%), which puts us in good stead as we continue to drive stronger lending.

Proactively manage regulatory change and risk

With the rapid changes taking place in banking, failure to manage risk and regulation effectively represents one of our greatest strategic concerns. Our achievements are detailed elsewhere in this report but we have continued to increase resources and focus on our risk management.

Strengthen business capabilities

To sustainably grow our customer base we need to continue to develop the right business capabilities. Our focus is on developing our key people, processes and system assets. We started to recruit new members of our Executive team as an important first step.

On the people front, it was pleasing to see almost 100 employees graduate with nationally accredited qualifications from our business school. This training gives employees the skills and knowledge to be experts when serving customers, as well as better leaders and team members to improve our business.

We continue to make changes to better measure and reward outstanding performance. Congratulations to our long serving North Coast Lending Manager, Michael Clement, on being named Employee of the Year and to mid North Coast Lending Manager, Mick Herb, for taking out the Ian Nelmes Award for Outstanding Service. We also had two Greater employees recognised nationally as emerging leaders within the customer owned banking sector – Ben Picton and Emma Avery. This combination of existing, new and emerging talent is key to our success.

Creating a diverse and flexible workplace is critical to attracting the best people. The Greater was named Workplace Flexibility Champion at the Hunter Diversity Awards and was also a finalist for flexible workplaces in the national HR Awards.

We made some realignments to our branch network to ensure we have branches in the right locations to meet the needs of customers. Our commitment to the Gold Coast was reaffirmed with a new Robina Branch.

That branch will serve as a concept branch to test enhancements in service such as concierge services and greater use of technology for a better banking experience.

Our ‘lending simple’, omni-channel and other business improvement programs are also delivering back and front end changes to processes to truly put our customers first.

Commit to corporate social responsibility

In the coming years we’ll continue to integrate CSR into our business strategy to promote innovation and business sustainability. We strive to operate our business in an ethical way and minimise our impact on the environment. CSR is about creating value for our business and the communities in which we operate, which includes risk management and giving back to the community.

Our customer owned structure means our focus is on customers and community rather than shareholders. Through The Greater’s many sponsorships, other business and community support and its funding of The Greater Charitable Foundation (see pages 9 and 10), we are improving the regions in which we operate and the lives of local people.

The future is exciting

Looking forward, the outlook remains challenging. Economic uncertainty surrounds our national and regional economies and competition from established and new disruptive competitors continues to increase. The Greater will respond to these challenges.

I’d like to thank the Board and our employees for their tremendous support and enthusiasm for change. I remain incredibly excited by the opportunities that lie ahead in our business.

Scott Morgan Chief Executive Officer

Greater Executive Committee; Back L to R: Craig Chapman, Scott Morgan, Michael King, Bruce White; Front L to R: Marie Hanson-Kentwell, Greg Taylor, Matthew Hingston

CEO’s Report

Chief Executive Officer, Scott Morgan

Annual Report | 2014-15Greater Building Society 0605

Our Community

Supporting grassroots sport

Through a number of sporting sponsorships, The Greater has helped people to be healthy and to do their best in their sport, as well as to save for their future.

Grassroots netball

After more than 20 years sponsoring Newcastle grassroots netball, this year The Greater expanded its support of local netball associations across regional NSW and the Gold Coast.

More than 20 netball associations received support to run their weekend games. Thousands of registered players received netball packs with water bottles as well as Life Saver accounts to help women and girls to save for their future.

New support for Hunter Academy of Sport

At the request of the Hunter Academy of Sport, The Greater has this year supported the Academy’s netball squad as well as helped it host the Festival of Sport netball competition involving academies from across NSW. The Greater is continuing to support the Academy’s annual awards night. The support is designed to help more athletes and their families.

The $2,000 Greater Building Society Olympic Scholarships were awarded to 10 athletes striving to represent Australia at upcoming Olympic and Paralympic Games.

The Greater has awarded these scholarships for 22 years, providing more than $360,000 to support more than 100 athletes over this time.

The Greater Fun Run Series

The Greater is encouraging people to have fun and get active with its new sponsorship of nine Athletics NSW fun runs across NSW in 2015 known as The Greater Fun Run Series.

The Greater supported the Hunter Track Classic for the fifth year and the event attracted some of Australia’s best athletes. The Hunter’s Fastest Kid races, also supported by The Greater, gave talented young athletes a chance to shine. Six winners were presented with Life Saver accounts.

Central Coast Carols drives young people

Young people doing it tough on the Central Coast were given a helping hand to learn to drive using the proceeds from the Mingara Christmas Under the Stars.

The Greater sponsored the event for the second year. Mingara and The Greater presented The Salvation Army’s Oasis Youth Centre, at Wyong, with $20,207 to purchase a car for its Drive for Life Program. More than 16,000 local residents attended the Carols event to enjoy some Christmas cheer and to make the donation possible.

Supporting those helping others

Skills for New England youth

At-risk young people living in the New England region have gained valuable skills in agriculture because of a $110,000 donation to Armidale-based charity, BackTrack.

The funding enabled the recruitment of a full-time AgLads Program Co-ordinator, Paul Dawson. It also assisted with program-related costs and allowed researchers at the University of New England to begin to evaluate the program.

These young people work on local training farms. The aim is to give them an opportunity to reconnect with their education and training, to become work- ready, find jobs, lead happy and productive lives and participate fully in the community. The program also helps local farmers overcome skill shortages. The funding came from the $1.5 million The Greater committed to spend in the New England region over 10 years when it merged with Armidale Building Society.

Junior Surfing Development Program

The next wave of up and coming surfers have a better chance of realising their dream of becoming pro surfers, thanks to The Greater’s support of the Merewether Surf Board Club’s new Junior Development Program. The program provides young surfers with support and advice to increase access to the sport and competitions. It encourages surf awareness, skills development and having fun. The Greater also helped the young surfers learn to save for their future with Life Saver accounts and a financial fitness seminar.

Presentation of cheque to BackTrackThis year The Greater expanded its support of local netball associations

Annual Report | 2014-15Greater Building Society 0807

Other organisations to benefit from Greater support

• Central Coast Academy of Sport

• Newcastle and Hunter Rugby Union

• The Newcastle Italian Film Festival (raising funds for motor neurone disease research)

• Hunter Young Professionals

• Property Council Hunter Chapter events

• Rotary (Newcastle Red Lantern Walk)

• Cystic Fibrosis NSW

• Regional Development Australia

• Armidale New England Enterprising Business Women’s Breakfasts and Enterprising Woman of the Year Award

• Hunter Business Award for Customer Satisfaction (under 20 employees) – won by Pepper Tree Wines in August 2014

• Junior Spirit Obstacle race in Forster

• Hunter District Cycling Club

• Big Day In – IT careers conference for young students

• Newcastle Art Prize – Society of Artists

Our Community continued

Supporting those helping others

KidzWish Giving Tree for Love and Laughter

The Greater has joined forces with Illawarra charity, KidzWish Foundation, to improve the lives of sick and disadvantaged children and their families. The Greater funded the construction of a new KidzWish Giving Tree at Stockland Shellharbour. The mural has space for personalised fundraising leaves, which people can buy from a Greater branch. The aim is to raise an additional $35,000 on top of $25,000 already donated by The Greater for KidzWish’s Love and Laughter Appeals Program. The funds raised will be distributed back to Illawarra children and their families in the form of grants to purchase equipment or services to improve their general health and independence.

Keeping Youth Off The Streets

A new partnership between The Greater and Father Chris Riley’s Youth Off The Streets was established to raise vital funds for programs that keep young people out of crisis and away from danger.

In a first for both organisations, The Greater will donate $2 to Youth Off The Streets for every Life Saver Account opened until $10,000 is raised.

The money raised will go toward outreach and educational programs that help disadvantaged young people in regional NSW.

The launch of The Giving Tree Wall with Shellharbour Branch Manager, Brendan White

Father Chris Riley in the Youth Off The Streets and Life Saver campaign

Annual Report | 2014-15Greater Building Society 1009

The Greater Charitable Foundation

Over the last 12 months, The Greater Charitable Foundation provided funding to nine organisations to support practical initiatives that are making a significant difference to the lives of families and communities across New South Wales and Queensland.

The Greater Charitable Foundation is funded from the profits of the Greater Building Society. Since its inception in 2011, The Greater Charitable Foundation has allocated more than $4 million to 12 different organisations, including $1.2 million this financial year.

In January, three partners received a welcome boost, sharing in $155,000 of additional, one-off funding. Autism Spectrum Australia (Aspect), Starlight Children’s Foundation and Cerebral Palsy Alliance were granted the funds to allow them to continue existing projects to help improve the lives of local people.

Below is a list of the partners supported by The Greater Charitable Foundation throughout 2014/15.

Autism Spectrum Australia (Aspect) – helping families of children with autism through the provision of early intervention services.

Camp Quality – reducing the stress and anxiety that children experience whilst hospitalised through the implementation of a Child Life Therapy Program at the John Hunter Children’s Hospital.

Cerebral Palsy Alliance – mentoring youth living with cerebral palsy to help coach and challenge them to build on their strengths, develop new skills and become job-ready.

Hunter Institute of Mental Health – developing a new set of resources and interventions promoting resilience, mental health and well-being for children with chronic illness and their families.

Hunter Medical Research Institute (HMRI) – supporting medical research into stroke treatment and rehabilitation.

KidzWish Foundation – mobile speech therapy service for children in the Illawarra Region, providing them with long-lasting speech and language enrichment.

Starlight Children’s Foundation Australia – transforming the hospital experience for kids and families in regional and remote areas and granting wishes for seriously ill children.

Youth Off The Streets – tailored early-intervention and education programs for disadvantaged children and young people in the Hunter Valley.

YWCA NSW – helping young people in the Northern Rivers reach their educational and social potential by providing employment and training opportunities.

Volunteering

A key platform of The Greater Charitable Foundation is the involvement of Greater employees with funded partners through volunteering or pro bono assistance. In the last 12 months, 280 Greater employees have volunteered, with many volunteering more than once and for more than one charity.

During National Volunteer Week 2015 (11–17 May), The Greater Charitable Foundation announced its inaugural Employee Volunteer of the Year Award. The award recognises Greater employees who go above and beyond in their efforts to give back to their community.

The winner of the inaugural award was Lending Communications Facilitator, Debbie Mace. This year Debbie volunteered with four of The Greater Charitable Foundation’s charity partners. Debbie also completed a Certificate IV in Community Services and has commenced a Community Services Diploma. Runners-up for the award were Information Security Manager, Jeremy Andreani, and Greenhills Branch Manager, Carolin Mackaway.

The Greater Charitable Foundation also introduced ‘Volunteering Vlogs’ to give a behind-the-scenes insight into what a Greater employee experiences when volunteering with a charity partner.

It was exciting to be part of a program that gives very ill children some relief from their usual day-to-day hospital routine. What a wonderful way to show these children that people care for them besides their families. The Captains should be commended for the work they do and the way in which they interact with children of all ages. Any time spent making a child’s time in hospital more enjoyable is a very meaningful way of assisting the great job already performed by the Captains.

Greater employee after volunteering at the Starlight Express Room as part of The Greater Charitable Foundation’s support of Starlight Children’s Foundation

Anne Long, CEO, The Greater Charitable Foundation; Employee Volunteer of the Year Award winner Debbie Mace and Scott Morgan, CEO, Greater Building Society

Armidale Branch Manager, Wendy Ng, visiting Armidale Hospital with the Starlight Captains

Annual Report | 2014-15Greater Building Society 1211

ContentsFinancial Statements 30 June 2015

Directors’ Report

The Directors have much pleasure in presenting their report on the consolidated financial statements consisting of the Greater Building Society Ltd (the Society) ABN 88 087 651 956 and the entities it controlled at the end of, or during, the year ended 30 June 2015.

DIRECTORSThe following persons held office as Directors for the whole of the financial year and up until the date of this report.

W M Russell B.Comm, CA, GAICD, MIIA (Aust)

Mr Russell joined the Board in April 2011. He has extensive experience in providing auditing and assurance services, having worked as an audit and assurance partner at PricewaterhouseCoopers for 20 years. He is currently a partner at accountancy firm Pitcher Partners. Mr Russell is involved in a number of industry associations and is a member of the Executive and past President of the Australian Financial Institutions Auditors Association. Mr Russell has been the Chairman of the Board since his appointment on 29 November 2011.

Special Responsibilities: Member of the Board Audit Committee, Member of the Board Risk Committee, Member of the Remuneration Committee, Member of the M&A Strategy Committee and Chairman of the Succession Planning Committee.

D S Robinson B.Surveying (Hons), MAICD

Mr Robinson joined the Board in October 2007 and has over 30 years’ experience in surveying, town planning and land development. He is the Managing Director of ADW Johnson, a leading Hunter based consultancy in surveying, town planning, engineering and land development. Mr Robinson has also previously worked as a part-time teacher at TAFE and was a Junior Officer in the Royal Australian Navy.

Special Responsibilities: Deputy Chairman of the Board, Member of the M&A Strategy Committee and Member of the Succession Planning Committee.

W R Ware LL.M. (Hons), FAICD

Mr Ware joined the Board in February 2009. He practised law for 14 years until 1987 when he became a professional Company Director and Business Consultant. He has served on the boards of a number of public companies in diverse industries for over 27 years. He is a co-owner and Director of Rosedale Gardens Retirement Living, a retirement village at Cooranbong, south of Newcastle.

Special Responsibilities: Chairman of the Remuneration Committee and Member of the Succession Planning Committee.

M L McDonald B Ec. FCA, GAICD

Mr McDonald joined the Board in May 2009. He has practised as a Chartered Accountant for over 30 years and was a Partner in the Newcastle Offices of Touché Ross & Co and KPMG Peat Marwick until his resignation in 1994. He has since that date and until recently practised on his own account. He is a Trustee of the Anglican Diocese of Newcastle and has considerable involvement in the Not for Profit sector at Board and Committee level.

Special Responsibilities: Chairman of the Board Audit Committee and Board Risk Committee, Member of the Succession Planning Committee and Member of the Remuneration Committee.

V J Drinkwater B Ec. MBA (With merit), GAICD, CAHRI

Mrs Drinkwater joined the Board in October 2010. She has extensive experience as a Senior Executive in operations, customer service, IT and marketing. Mrs Drinkwater was previously employed as Interim CEO New Zealand, Chief Marketing Officer and Chief Operating Officer at nib health funds limited. She is also a Trustee of the Anglican Diocese of Newcastle.

Special Responsibilities: Member of the Remuneration Committee, Member of the Succession Planning Committee, Member of the Board Audit Committee and Member of the Board Risk Committee.

Directors’ Report 12

Auditor’s Independence Declaration 16

Directors’ Declaration 19

Statement of Comprehensive Income 20

Balance Sheet 21

Statement of Changes in Equity 22

Statement of Cash Flows 23

Notes to and Forming Part of the Financial Statements 24

Annual Report | 2014-15Greater Building Society 1413

R J Cracknell CPA, FAICD

Mr Cracknell joined the Board in May 2011. He was Chief Executive of ABS Building Society from 1973 until April 2011 and has over 40 years’ experience in the Building Society Industry. He has held various executive positions with the Australian Permanent Building Societies (NSW Division) and was a Councillor of AAPBS (National). Mr Cracknell was a partner in the accountancy firm of Jones, Cracknell & Starr for over 40 years.

Special Responsibilities: Member of the Board Audit Committee, Member of the Board Risk Committee, Member of the Succession Planning Committee and Chairman of the M&A Strategy Committee.

COMPANY SECRETARIES

Mr G J Taylor and Ms A C Saltos were appointed as the Company Secretaries on 10 October 2014 replacing Mr B E Mackie. Mr Taylor is the incumbent Chief Financial Officer with responsibilities for all financial reporting and governance, treasury and legal operations for the Society. Mr Taylor joined the Greater Building Society in 1979.

Ms Saltos is a Senior Corporate Lawyer within the Society with over 14 years’ experience in corporate legal practice. Ms Saltos commenced with the Greater Building Society in 2013.

CORPORATE OBJECTIVESThe Society will ensure its long term financial viability by achieving the following short and long term objectives:

• Sustainably grow our customer base in target markets,

• Improve organisational efficiency,

• Proactively manage regulatory change,

• Strengthen business capabilities (people, process and systems), and

• Commit to corporate social responsibility.

The current strategies in place to achieve these objectives are to maintain a distribution network that supports the increasing needs of customers, to provide a range of products and services to meet the demands of members, to continue to provide a superior service level, and to enhance the member experience at all points of contact. Furthermore, internal strategies are in place to ensure the Society provides a challenging and enjoyable workplace, continues to build capacity and knowledge with good corporate governance and is an employer of choice.

The Society measures its performance using a range of financial and non-financial indicators. The main financial indicators are interest margins, cost to income ratio, return on assets, profit per employee, loan portfolio growth and deposit portfolio growth, while non-financial indicators include number of products and services per member, staff and member satisfaction.

PRINCIPAL ACTIVITIESThe principal activity during the year of the consolidated entity comprising the Greater Building Society Ltd and the controlled entities consisted of the provision of financial services to members in the form of taking deposits and providing financial accommodation. Those activities enhanced the financial position of the Society and provided the platform to enable the Society to improve the quality of its distribution channels and expand the range of products and services available to members.

RESULTS OF THE CONSOLIDATED ENTITY

2015 2014

$’000 $’000

Profit after income tax expense 34,950 31,361

Less profit attributable to outside equity interests - (255)

Profit attributable to members of the Greater Building Society Ltd 34,950 31,106

REVIEW OF OPERATIONSA review of operations of the consolidated entity is contained in the Chairman’s and Chief Executive Officer’s Reports.

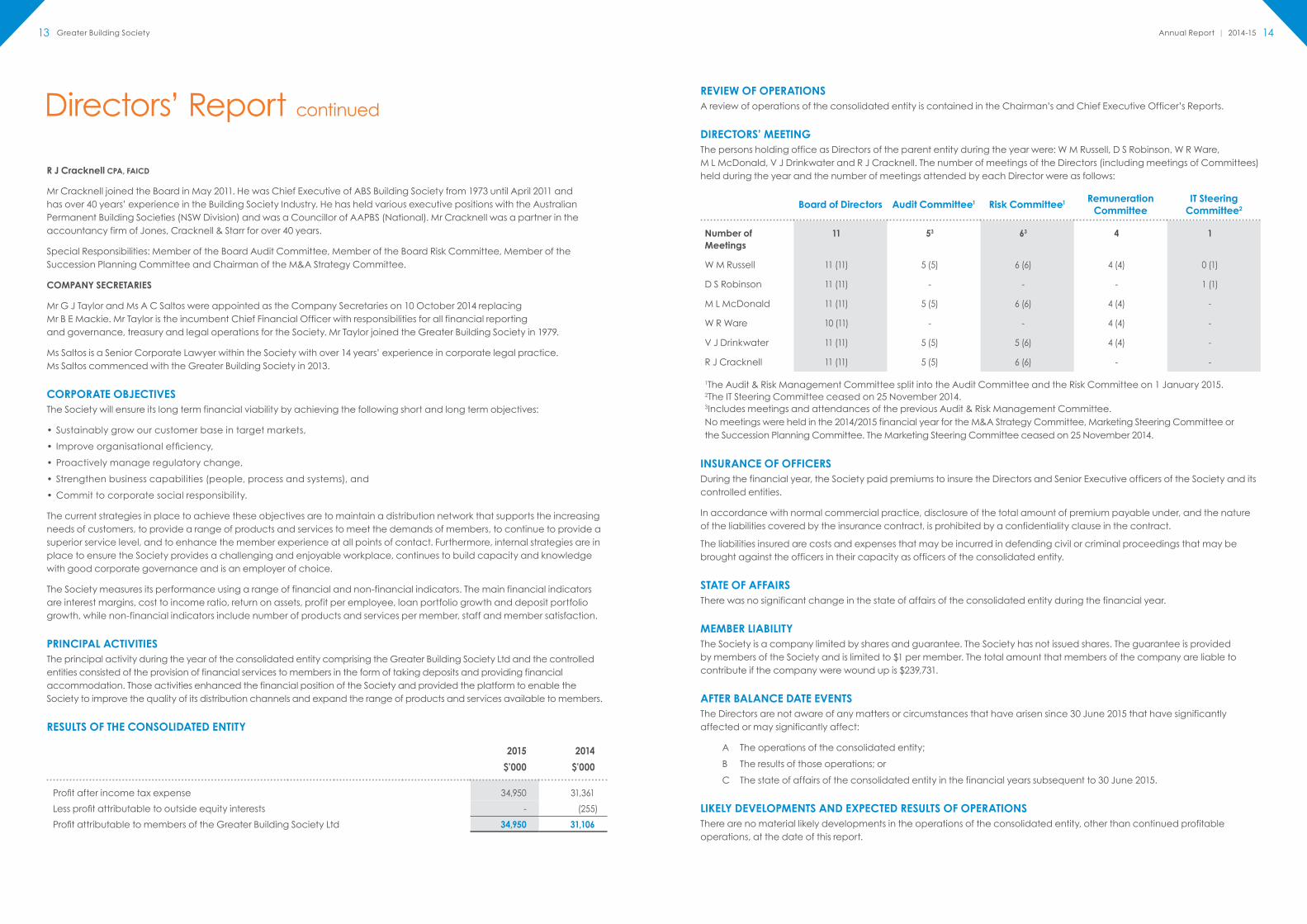

DIRECTORS’ MEETINGThe persons holding office as Directors of the parent entity during the year were: W M Russell, D S Robinson, W R Ware, M L McDonald, V J Drinkwater and R J Cracknell. The number of meetings of the Directors (including meetings of Committees) held during the year and the number of meetings attended by each Director were as follows:

Board of Directors Audit Committee1 Risk Committee1 Remuneration Committee

IT Steering Committee2

Number of Meetings

11 53 63 4 1

W M Russell 11 (11) 5 (5) 6 (6) 4 (4) 0 (1)

D S Robinson 11 (11) - - - 1 (1)

M L McDonald 11 (11) 5 (5) 6 (6) 4 (4) -

W R Ware 10 (11) - - 4 (4) -

V J Drinkwater 11 (11) 5 (5) 5 (6) 4 (4) -

R J Cracknell 11 (11) 5 (5) 6 (6) - -

1The Audit & Risk Management Committee split into the Audit Committee and the Risk Committee on 1 January 2015.2The IT Steering Committee ceased on 25 November 2014.3Includes meetings and attendances of the previous Audit & Risk Management Committee.No meetings were held in the 2014/2015 financial year for the M&A Strategy Committee, Marketing Steering Committee or the Succession Planning Committee. The Marketing Steering Committee ceased on 25 November 2014.

INSURANCE OF OFFICERSDuring the financial year, the Society paid premiums to insure the Directors and Senior Executive officers of the Society and its controlled entities.

In accordance with normal commercial practice, disclosure of the total amount of premium payable under, and the nature of the liabilities covered by the insurance contract, is prohibited by a confidentiality clause in the contract.

The liabilities insured are costs and expenses that may be incurred in defending civil or criminal proceedings that may be brought against the officers in their capacity as officers of the consolidated entity.

STATE OF AFFAIRSThere was no significant change in the state of affairs of the consolidated entity during the financial year.

MEMBER LIABILITYThe Society is a company limited by shares and guarantee. The Society has not issued shares. The guarantee is provided by members of the Society and is limited to $1 per member. The total amount that members of the company are liable to contribute if the company were wound up is $239,731.

AFTER BALANCE DATE EVENTSThe Directors are not aware of any matters or circumstances that have arisen since 30 June 2015 that have significantly affected or may significantly affect:

A The operations of the consolidated entity;

B The results of those operations; or

C The state of affairs of the consolidated entity in the financial years subsequent to 30 June 2015.

LIKELY DEVELOPMENTS AND EXPECTED RESULTS OF OPERATIONSThere are no material likely developments in the operations of the consolidated entity, other than continued profitable operations, at the date of this report.

Directors’ Report continued

Annual Report | 2014-15Greater Building Society 1615

PROCEEDINGS ON BEHALF OF THE COMPANYNo person has applied to the Court under Section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Society, or to intervene in any proceedings to which the Society is a party, for the purpose of taking responsibility on behalf of the Society for all or part of those proceedings.

No proceedings have been brought or intervened in on behalf of the Society with leave of the Court under Section 237 of the Corporations Act 2001.

ENVIRONMENTAL REGULATIONThe Society or its controlled entities are not subject to any significant environmental regulation.

AUDITOR’S INDEPENDENCE DECLARATIONA copy of the auditor’s independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 16.

ROUNDING OF AMOUNTSThe amounts in the financial statements have been rounded to the nearest thousand dollars under the option available to the Society under ASIC Class Order 98/100. The Society is an entity to which the Class Order applies.

AUDITORPricewaterhouseCoopers Australia continues in office in accordance with section 327 of the Corporations Act 2001. Details of the amounts paid or payable to the auditor (PricewaterhouseCoopers Australia) for audit and non-audit services provided during the year are disclosed in Note 27.

W M Russell Chairman

Signed at Hamilton this 22nd day of September 2015 in accordance with a resolution of the Directors.

Directors’ Report continued

Annual Report | 2014-15Greater Building Society 1817

Annual Report | 2014-15Greater Building Society 2019

Directors’ Declaration Statement of Comprehensive IncomeIn the Directors’ opinion:

A The financial statements and notes set out on pages 20 to 61 are in accordance with the Corporations Act 2001, including:

i) Complying with Accounting Standards, the Corporations Regulations 2001 and other mandatory professional reporting requirements; and

ii) Giving a true and fair view of the Society’s and consolidated entity’s financial position as at 30 June 2015 and of their performance, as represented by the results of their operations, changes in equity and their cash flows, for the financial year ended on that date; and

B There are reasonable grounds to believe that the Society will be able to pay its debts as and when they become due and payable; and

C Note 1(A) confirms that the financial statements also comply with International Financial Reporting Standards as issued by the International Accounting Standards Board.

This declaration is made in accordance with a resolution of the Directors.

W M Russell Chairman

Signed at Hamilton this 22nd day of September 2015.

for the year ended 30 June 2015

CONSOLIDATED SOCIETY

Notes 2015 2014 2015 2014

$’000 $’000 $’000 $’000

Interest revenue 2 259,260 264,079 274,821 276,862

Interest expense 3 (132,289) (139,775) (148,507) (154,388)

Net interest income 126,971 124,304 126,314 122,474

Non-interest income 4 25,030 23,830 25,374 22,223

152,001 148,134 151,688 144,697

Non-interest expense 5 (102,361) (104,039) (102,310) (100,615)

PROFIT BEFORE INCOME TAX 49,640 44,095 49,378 44,082

Income tax expense 6 (14,690) (12,734) (14,651) (13,129)

PROFIT FOR THE YEAR 34,950 31,361 34,727 30,953

PROFIT ATTRIBUTABLE TO

Members of the Greater Building Society Ltd 34,950 31,106 34,727 30,953

Non-controlling interests 25 - 255 - -

34,950 31,361 34,727 30,953

OTHER COMPREHENSIVE INCOME

Items that may be reclassified to profit or loss

Cash flow hedges 23 (966) (1,137) (966) (1,137)

Income tax relating to these items 23 290 341 290 341

Items that will not be reclassified to profit or loss

Revaluation of land and buildings 23 2,970 404 2,954 314

Income tax relating to these items 23 (891) (121) (886) (94)

Fair value assets through other comprehensive income

23 46 293 46 293

Income tax relating to these items 23 (14) (88) (14) (88)

Total other comprehensive income 1,435 (308) 1,424 (371)

TOTAL COMPREHENSIVE INCOME 36,385 31,053 36,151 30,582

TOTAL COMPREHENSIVE INCOME ATTRIBUTABLE TO

Members of the Greater Building Society Ltd 36,385 30,798 36,151 30,582

Non-controlling interests 25 - 255 - -

36,385 31,053 36,151 30,582

The above Statement of Comprehensive Income should be read in conjunction with the accompanying notes.

Annual Report | 2014-15Greater Building Society 2221

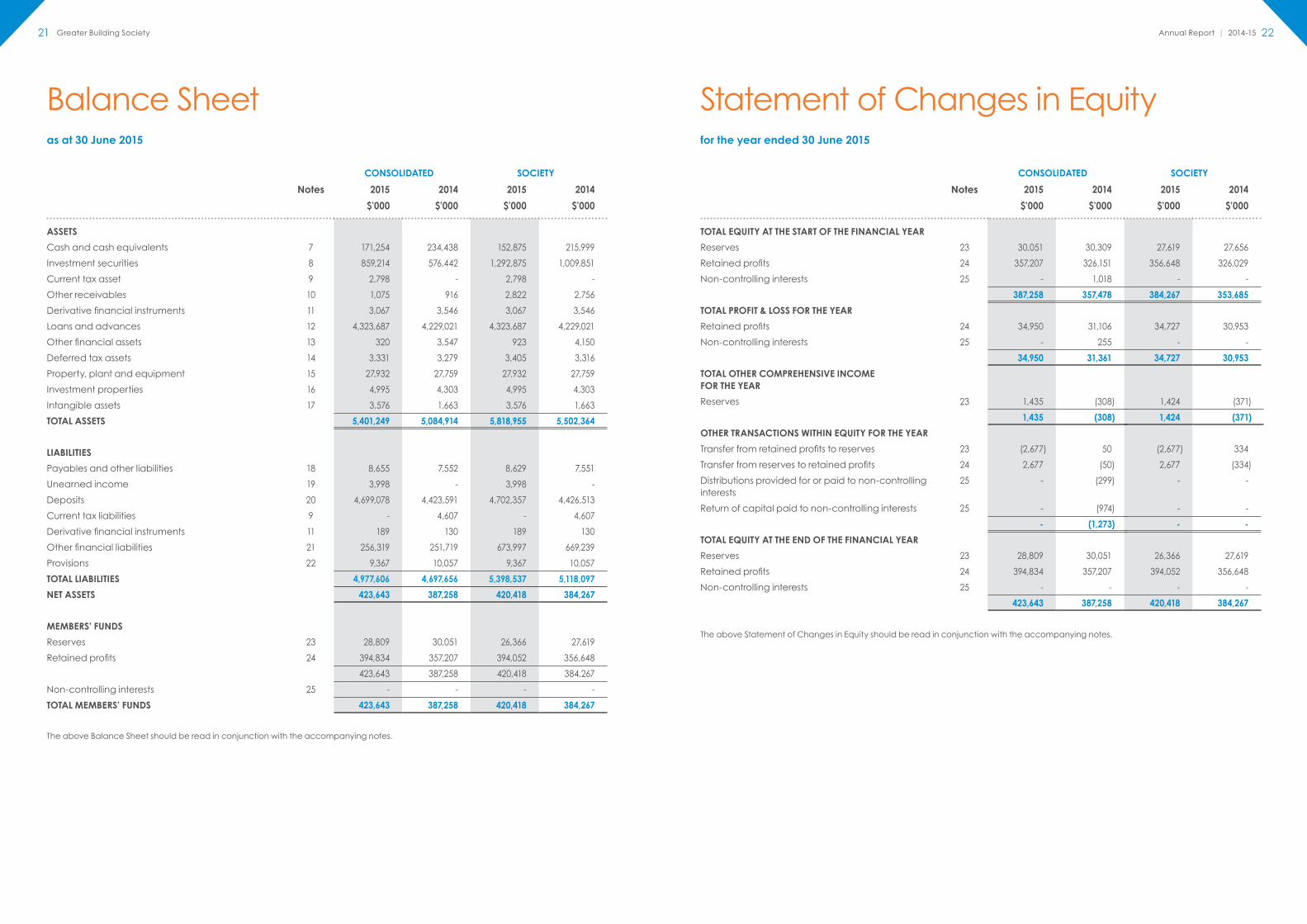

as at 30 June 2015

CONSOLIDATED SOCIETY

Notes 2015 2014 2015 2014

$’000 $’000 $’000 $’000

ASSETS

Cash and cash equivalents 7 171,254 234,438 152,875 215,999

Investment securities 8 859,214 576,442 1,292,875 1,009,851

Current tax asset 9 2,798 - 2,798 -

Other receivables 10 1,075 916 2,822 2,756

Derivative financial instruments 11 3,067 3,546 3,067 3,546

Loans and advances 12 4,323,687 4,229,021 4,323,687 4,229,021

Other financial assets 13 320 3,547 923 4,150

Deferred tax assets 14 3,331 3,279 3,405 3,316

Property, plant and equipment 15 27,932 27,759 27,932 27,759

Investment properties 16 4,995 4,303 4,995 4,303

Intangible assets 17 3,576 1,663 3,576 1,663

TOTAL ASSETS 5,401,249 5,084,914 5,818,955 5,502,364

LIABILITIES

Payables and other liabilities 18 8,655 7,552 8,629 7,551

Unearned income 19 3,998 - 3,998 -

Deposits 20 4,699,078 4,423,591 4,702,357 4,426,513

Current tax liabilities 9 - 4,607 - 4,607

Derivative financial instruments 11 189 130 189 130

Other financial liabilities 21 256,319 251,719 673,997 669,239

Provisions 22 9,367 10,057 9,367 10,057

TOTAL LIABILITIES 4,977,606 4,697,656 5,398,537 5,118,097

NET ASSETS 423,643 387,258 420,418 384,267

MEMBERS’ FUNDS

Reserves 23 28,809 30,051 26,366 27,619

Retained profits 24 394,834 357,207 394,052 356,648

423,643 387,258 420,418 384,267

Non-controlling interests 25 - - - -

TOTAL MEMBERS’ FUNDS 423,643 387,258 420,418 384,267

The above Balance Sheet should be read in conjunction with the accompanying notes.

for the year ended 30 June 2015

CONSOLIDATED SOCIETY

Notes 2015 2014 2015 2014

$’000 $’000 $’000 $’000

TOTAL EQUITY AT THE START OF THE FINANCIAL YEAR

Reserves 23 30,051 30,309 27,619 27,656

Retained profits 24 357,207 326,151 356,648 326,029

Non-controlling interests 25 - 1,018 - -

387,258 357,478 384,267 353,685

TOTAL PROFIT & LOSS FOR THE YEAR

Retained profits 24 34,950 31,106 34,727 30,953

Non-controlling interests 25 - 255 - -

34,950 31,361 34,727 30,953

TOTAL OTHER COMPREHENSIVE INCOME FOR THE YEAR

Reserves 23 1,435 (308) 1,424 (371)

1,435 (308) 1,424 (371)

OTHER TRANSACTIONS WITHIN EQUITY FOR THE YEAR

Transfer from retained profits to reserves 23 (2,677) 50 (2,677) 334

Transfer from reserves to retained profits 24 2,677 (50) 2,677 (334)

Distributions provided for or paid to non-controlling interests

25 - (299) - -

Return of capital paid to non-controlling interests 25 - (974) - -

- (1,273) - -

TOTAL EQUITY AT THE END OF THE FINANCIAL YEAR

Reserves 23 28,809 30,051 26,366 27,619

Retained profits 24 394,834 357,207 394,052 356,648

Non-controlling interests 25 - - - -

423,643 387,258 420,418 384,267

The above Statement of Changes in Equity should be read in conjunction with the accompanying notes.

Statement of Changes in EquityBalance Sheet

Annual Report | 2014-15Greater Building Society 2423

for the year ended 30 June 2015

CONSOLIDATED SOCIETY

Notes 2015 2014 2015 2014

$’000 $’000 $’000 $’000Inflows/

(Outflows)Inflows/

(Outflows)Inflows/

(Outflows)Inflows/

(Outflows)

CASH FLOWS FROM OPERATING ACTIVITIES

Interest received 257,740 264,504 273,294 277,289

Fees and commissions received 24,707 18,141 24,707 18,141

Other income received 528 3,379 825 1,245

Interest paid (134,185) (139,825) (150,987) (156,102)

Operating expenses paid (97,641) (99,041) (97,633) (99,685)

Income taxes paid (22,763) (11,202) (22,763) (11,202)

Net advances and repayments in loans and advances (94,769) (43,548) (94,026) (35,404)

Net placements and redemptions in investment securities (276,059) (20,091) (276,305) (11,161)

Net acceptances and payments in deposits 278,022 238,973 278,369 237,280

NET CASH PROVIDED BY OPERATING ACTIVITIES 30 (64,420) 211,290 (64,519) 220,401

CASH FLOWS FROM INVESTING ACTIVITIES

Net purchases and sales in other financial assets and liabilities

(189) 8 (189) 2,650

Payments for property, plant and equipment (3,720) (3,966) (3,720) (3,953)

Proceeds from sale of property, plant and equipment 592 709 592 709

Dividends and distributions received - 17 - 521

CASH FLOWS FROM INVESTING ACTIVITIES (3,317) (3,232) (3,317) (73)

CASH FLOWS FROM FINANCING ACTIVITIES

Net issue/(repayment) of commercial notes 4,553 (132,957) 4,712 (157,912)

Distributions paid - (882) - -

NET CASH PROVIDED BY FINANCING ACTIVITIES 4,553 (133,839) 4,712 (157,912)

Net increase/(decrease) in cash held (63,184) 74,219 (63,124) 62,416

CASH AT THE BEGINNING OF THE FINANCIAL YEAR 234,438 160,219 215,999 153,583

CASH AT THE END OF THE FINANCIAL YEAR 7 171,254 234,438 152,875 215,999

The above Statement of Cash Flows should be read in conjunction with the accompanying notes.

for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A Basis of Preparation

The financial report includes separate financial statements for the Greater Building Society Ltd as an individual entity (i.e. the Society) and the consolidated entity consisting of the Society and all its subsidiaries.

The financial statements of the Society and the consolidated entity are general purpose financial reports prepared in accordance with provisions of Australian Accounting Standards and the Corporations Act 2001 in Australia. The Society’s and consolidated entity’s financial statements also comply with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). The Greater Building Society Ltd is a for-profit entity for the purposes of preparing financial statements.

The financial statements of the Society and the consolidated entity are prepared under the historical cost convention, as modified by the revaluation of certain financial assets and liabilities (including derivative instruments) at fair value, certain classes of property and investment property.

All amounts are expressed in Australian dollar currency.

Notes containing prior year comparatives may have been restated to provide the user with additional details. Such changes do not alter the total balance as previously disclosed.

The significant accounting policies adopted in the preparation of these financial statements and that of the previous financial year are set out below. These policies have been consistently applied to all periods presented, unless otherwise stated.

i) Criticalaccountestimatesandsignificantjudgements

The preparation of the financial statements requires the use of certain critical accounting estimates. It also requires Management to exercise judgement in the process of applying the accounting policies. The notes of the financial statements set out the areas involving a higher degree of judgement or complexity, or areas where assumptions are significant to the Society and its consolidated entity financial statements. The most significant of these are:

• impairment losses on loans and advances,

• consolidation of special purpose entities, and

• fair valuation estimates.

Estimates and judgements are continually evaluated and are based on historical experience and other factors, including reasonable expectations of future events. Management believes the estimates used in preparing the financial statements are reasonable. Actual results in the future may differ from those reported.

ii) New accounting standards and interpretations

Certain new accounting standards and interpretations have been published that are not mandatory for 30 June 2015 reporting periods. The consolidated entity’s assessment of the impact of these new standards and interpretations is set out below.

Revenue from contracts with customers (effective 1 January 2017)

The IASB has issued a new standard for the recognition of revenue. This will replace IAS18, which covers contracts for goods and services and IAS11 which covers construction contracts. The new standard is based on the principle that revenue is recognised when control of a good or service transfers to a customer, so the notion of control replaces the existing notion of risks and rewards. While the consolidated entity does not expect the new standard to have an impact on how revenue is recognised, it is yet to perform a detailed assessment.

B Consolidation

i) Controlled entities

The consolidated financial statements comprise the financial statements of the Society and its controlled entities (together, ‘the consolidated entity’). The consolidated entity controls an entity when the consolidated entity is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power to direct the activities of the entity. The effects of all transactions between entities in the consolidated entity have been eliminated in full. Non-controlling interest in the results and equity of controlled entities, where the Society owns less than 100% of the issued capital, are shown separately in the consolidated statement of comprehensive income, statement of changes of equity and balance sheet.

Statement of Cash Flows Notes to and Forming Part of the Financial Statements

Annual Report | 2014-15Greater Building Society 2625

Where control of an entity was obtained during the financial period, its results have been included in the consolidated statement of comprehensive income from the date on which control commenced. Where control of an entity ceased during the financial period, its results are included for that part of the financial period during which control existed.

Investments in subsidiaries are accounted for by the Society at cost.

ii) Business combinations

The acquisition method of accounting is used to account for all business combinations. The consideration transferred for the acquisition of a subsidiary comprises the fair values of the assets transferred, the liabilities incurred and the equity interests issued by the group. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are, with limited exceptions, measured initially at their fair values at the acquisition date.

Acquisition-related transaction costs are expensed as incurred.

The excess of the consideration transferred, the amount of any non-controlling interest in the acquiree and the acquisition date fair value of any previous equity interest in the acquired entity, over the fair value of the net identifiable assets acquired is recorded as goodwill. If those amounts are less than the fair value of the net identifiable assets of the subsidiary acquired, the difference is recognised directly in profit or loss as a bargain purchase.

Contingent consideration is classified either as equity or a financial liability. Amounts classified as a financial liability are subsequently remeasured to fair value with changes in fair value recognised in profit or loss.

iii) Securitisation

Securitised positions are held through a number of Special Purpose Entities (‘SPEs’). These securitised positions allow the Society to access funding. The Society does not consolidate an SPE it does not control. Where it can sometimes be difficult to determine whether the Society does control the SPE, it makes judgements about its exposure to the variable returns of the entity and its ability to affect those returns. The Society has consolidated its SPEs. Accordingly, their underlying assets, liabilities, revenues and expenses are reported in the Society’s consolidated balance sheet and statement of comprehensive income.

C Segment Reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision maker. The chief operating decision maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the Chief Executive Officer. All operating segments are less than the quantitative threshold required for separate disclosure.

D Revenue Recognition

i) Interest revenue

Interest income arising from loans and held to maturity investment securities is brought to account using the effective interest rate method. Incremental fees and transaction costs associated with the origination of loans and held to maturity investment securities which are an integral part of the effective interest rate are deferred and recognised in the statement of comprehensive income on a yield basis over the expected life of the financial instrument.

The effective interest rate is that rate that exactly discounts estimated future cash flows throughout the life of the financial instrument.

The balance outstanding of the deferred origination income and expense is recognised in the balance sheet as an adjustment to the carrying amount of the loans and held to maturity investment securities outstanding.

ii) Other revenue

Other income, commission and fee income is recognised in the statement of comprehensive income as revenue on an accruals basis when the service has been provided or incurred.

E Income Tax

The consolidated entity has adopted the balance sheet liability method of tax-effect accounting which focuses on the tax effect of transactions and other events that affect amounts recognised in either the balance sheet or a tax-based balance sheet.

Deferred tax assets and liabilities are recognised for temporary differences, except where the deferred tax asset/liability arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss.

Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is probable that the future taxable amounts will be available to utilise those temporary differences and losses.

Current and deferred tax balances attributable to amounts recognised directly in equity are also recognised directly in equity.

The Society and certain wholly owned Australian controlled entities implemented the tax consolidation legislation as of 1 July 2002. The Australian Taxation Office has been notified of the decision. As a consequence, those entities are taxed as a single entity and the deferred tax assets and liabilities of those entities are set off in the consolidated financial statements.

Tax funding and sharing agreements between the Society and certain wholly owned Australian controlled entities, known as ‘group member entities’, apply from 1 July 2013. Broadly, group member entities are required to calculate their notional tax liability as if they were standalone taxpayers before transferring their tax liability to the head entity. Such transfers will be effected on intercompany account. The Society has responsibility for settling the consolidated entity’s income tax liability with the ATO.

F Financial Assets

The consolidated entity has elected to apply AASB 9 Financial Instruments and AASB2009-11 Amendments to Australian Accounting Standards arising from AASB 9 from 1 July 2010, because the new accounting standards provide more reliable and relevant information for users to assess the amounts, timing and uncertainty of future cash flows.

All financial assets are initially recognised at fair value plus, in the case of financial assets and liabilities not classified as at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset.

Financial assets are then classified as either a debt or equity financial asset, which in turn determines their subsequent accounting measurement. The categories and measurement treatments are:

i) Debt Financial Asset

A debt financial asset is classified as at amortised cost only if both of the following criteria are met:

• the asset is held within a business model with the objective to collect the contractual cash flows, and

• the contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal outstanding.

The nature of any derivatives embedded in the debt financial asset are considered in determining whether the cash flows of the asset are solely payment of principal and interest on the principal outstanding and are not accounted for separately.

A gain or loss on a debt financial asset that is subsequently measured at amortised cost and is not part of a hedging relationship is recognised in profit or loss when the financial asset is derecognised or impaired and through the amortisation process using the effective interest rate method.

If either of the two criteria above are not met, the debt financial asset is classified as at fair value through profit or loss.

A gain or loss on a debt financial asset that is subsequently measured at fair value and is not part of a hedging relationship is recognised in profit or loss and presented net in the income statement within other income or other expenses in the period in which it arises.

ii) Equity Financial Asset

All equity financial assets are measured at fair value.

Equity financial assets that are held for trading are measured at fair value through profit or loss. Changes in the fair value of financial assets at fair value through profit or loss are recognised in other income or other expenses in the income statement as applicable. Interest income from these financial assets is included in the net gains/(losses). Dividend income is presented as other revenue.

For all other equity financial assets (i.e. equity financial assets other than held for trading) the consolidated entity can make an irrevocable election at initial recognition of each equity financial asset to recognise changes in fair value through other comprehensive income (OCI) rather than through profit or loss.

Where Management has elected to present fair value gains and losses on equity financial assets in other comprehensive income, there is no subsequent reclassification of fair value gains and losses to profit or loss. Gains and losses arising from subsequent changes in fair value for equity financial assets nominated as fair value through other comprehensive income are recognised directly in the financial asset at fair value through other comprehensive income reserve in equity, until the asset is derecognised, at which time the cumulative gain or loss will be transferred to retained profits. Dividends from equity financial assets continue to be recognised in profit or loss as other revenue when the right to receive payments is established and as long as they represent a return on investment.

Notes to and Forming Part of the Financial Statementsfor the year ended 30 June 2015

Annual Report | 2014-15Greater Building Society 2827

Equity financial assets are measured at fair value. Fair values of quoted equity financial assets in active markets are based on current bid prices. If the relevant market is not considered active (or the securities are unlisted), the consolidated entity establishes fair value by using valuation techniques, including recent arm’s length transactions, discounted cash flow analysis, option pricing models and other valuation techniques commonly used by market participants. Where equity financial assets cannot be reliably valued they are recorded at cost.

G Cash and Cash Equivalents

Cash and cash equivalents includes cash on hand and deposits at call and other short-term, highly liquid investments with original maturities of three months or less that are readily convertible to cash and are subject to an insignificant risk of changes in value.

H Investment Securities

i) Asset recognition

Investment securities are classified as debt financial assets and are measured at amortised cost using the effective interest rate method. Amortised cost is calculated by taking into account any discount or premium on acquisition, over the period to maturity. Any gains or losses from investments are recognised in profit and loss when the investments are derecognised, on impairment, as well as through the amortisation process.

ii) Revenue recognition

Interest income arising from investment securities is recognised in the statement of comprehensive income using the effective interest rate method (refer Note 1D).

iii) Investments in associates

Associates are those entities over which the consolidated entity exercises significant influence, but not control. Investments in associates are accounted for in the financial statements using the equity accounting method. Under this method, the consolidated entity’s share of the post acquisition profits or losses of associates is recognised in the consolidated statement of comprehensive income, and its share of post acquisition movements in reserves is recognised in consolidated reserves. The cumulative post acquisition movements are adjusted against the carrying amount of the investment.

Investments in associates are accounted for by the Society at cost.

I Loans and Advances

i) Asset recognition

Loans and advances are classified as loans and receivable assets and are recognised when cash is advanced to members. They are carried at amortised cost using the effective interest rate method (refer Note 1F).

ii) Revenue recognition

Interest income arising from loans is brought to account using the effective interest rate method (refer Note 1D).

Loan fees received and transaction costs directly attributable to the acquisition of the loan are deferred and included as an adjustment to the interest revenue of the loan on a yield basis over the expected life of the loan using the effective interest rate method. The deferred revenues and costs are included in the balance sheet as part of the value of the loans and advances outstanding.

Other loan fees, commissions and other service fees provided in relation to services are recognised as profit and loss as other income on an accruals basis.

iii) Loan impairment

All loan assets are subject to regular review and assessment for possible impairment. Allowances for impairment losses on loans are based on an incurred loss model, which recognises an allowance where there is objective evidence of impairment.

Specific allowances are raised for losses that may be incurred for loans that are known to be impaired. Estimated losses on these loans are measured at the difference between the loans carrying amount and the present value of the estimated cash flows discounted at the loans effective interest rate.

Where individual loans are found to not be impaired they are grouped together with loans of similar credit risk characteristics and then assessed collectively for impairment. Any loan that has been individually assessed and considered impaired is excluded from the collective assessment.

Loans that are collectively assessed for impairment are estimated on the basis of historical loss experience adjusted for any current conditions that may have impacted on the historical loss experience.

A credit loss reserve is maintained in equity to cover credit risks inherent in the loan portfolio. Movement in the credit loss reserve is recognised as an appropriation of retained profits (refer Note 1S).

iv) Restructured loans

A restructured loan is a non-commercial facility where the original contractual terms have been modified to provide concessional changes for reasons relating to financial difficulties of the borrower. Where the loan after restructuring remains doubtful and it is not well secured the loan shall be subject to impairment. Loans will only be recognised as restructured once the customer has formally agreed to the new terms.

v) Assets acquired through enforcement of security

Assets acquired through enforcement of security are assets acquired in full or partial settlement of a loan or similar facility through enforcement of security arrangements.

vi) Bad debts written off

Bad debts are written off as identified by Management and the Board of Directors when it is reasonable to expect that the recovery of the debt is unlikely.

Bad debts will be written off directly to profit and loss in the period in which they are identified. Bad debts can be written off directly against the allowance for impaired losses only to the extent that the allowance balance includes a specific allowance in respect of the debt being written off.

J Plant, Property and Equipment

i) Asset recognition

Land and buildings are initially recognised at cost and then subsequently carried at fair value less accumulated depreciation.

Plant and equipment are initially recognised at cost and then subsequently carried at cost less accumulated depreciation and less any impairment adjustment. Assets are reviewed for impairment annually.

Cost includes expenditure directly attributable to the acquisition of the asset.

Items of equipment, furniture and fittings and other small assets, which cost less than $1,000, are expensed at the time of purchase.

ii) Revaluations

Land and buildings are carried at fair value at the date of the revaluation less any subsequent accumulated depreciation of buildings and accumulated impairment losses.

Increases in the carrying amounts arising on revaluation of land and buildings are recognised, net of tax, in other comprehensive income and accumulated in the property revaluation surplus reserve in equity. To the extent that the increase reverses a decrease previously recognised in profit or loss, the increase is first recognised in profit or loss. Decreases that reverse previous increases of the same asset are first recognised in other comprehensive income to the extent of the remaining surplus attributable to the asset; all other decreases are charged to profit or loss. Any accumulated depreciation as at the revaluation date is eliminated against the gross carrying amount of the asset and the net amount is restated to the revalued amount of the asset. Upon disposal, any revaluation surplus reserve relating to the particular asset being disposed is transferred to retained profits.

The balances in the asset revaluation surplus reserve for each particular asset are net of any potential capital gains tax liability.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the item) is included in profit and loss in the year the item is derecognised.

Notes to and Forming Part of the Financial Statementsfor the year ended 30 June 2015

Annual Report | 2014-15Greater Building Society 3029

Fair value is determined by reference to market-based evidence, which is the amount that the assets could be exchanged between a knowledgeable willing buyer and a knowledgeable willing seller in an arm’s length transaction as at the valuation date. Annual assessments of the fair value are made by the Directors, supplemented by independent valuations performed every three years (or more often if circumstances require) ensuring that the carrying amount does not differ materially from the asset’s fair value at the balance sheet date.

iii) Depreciation

Depreciation is calculated so as to write off the net cost or revalued amount of each item of property, plant and equipment (excluding land) over its expected useful life. Additions are depreciated from the date of acquisition.

The consolidated entity uses the following rates and methods of depreciation:

Rate Method

Buildings 2.5% straight line

Office Furniture 25% reducing balance

Office Equipment 25% reducing balance

Motor Vehicles 30% reducing balance

Computer Hardware 40% reducing balance

Cash Dispensing Units 15% straight line

Leasehold improvements are amortised over the shorter of the unexpired period of the lease or the useful life of the leasehold improvements on a prime cost basis.

Useful lives and residual values are reviewed annually and reassessed in light of commercial and technological developments. If an asset’s carrying value is greater than its recoverable amount due to a useful life, residual value or impairment adjustment, the carrying amount is written down immediately to its recoverable amount. Adjustments arising from such restatements and on disposal of fixed assets are recognised in profit and loss.

For taxation purposes, the consolidated entity adopts an effective life for the asset as determined by Taxation Rulings made public by the Commissioner of Taxation. The consolidated entity generally uses the reducing balance method of depreciation for tax purposes.

K Investment Properties

Investment properties are initially recognised at cost and then subsequently carried at fair value. Cost includes expenditure directly attributable to the acquisition of the asset.

Fair value is determined by reference to market-based evidence, which is the amount that the assets could be exchanged between a knowledgeable willing buyer and a knowledgeable willing seller in an arm’s length transaction as at the valuation date. Annual assessments of the fair value are made by the Directors, supplemented by independent valuations performed every three years (or more often if circumstances require) ensuring that the carrying amount does not differ materially from the asset’s fair value at the balance sheet date.

Changes in fair values for investment properties are recognised directly in profit and loss.

Where the property is used by the consolidated entity for its own occupation the property is classified as plant, property and equipment.

L Inventory

No expenditure is treated as an asset where it has no realisable value or it is insignificant in size and nature. Items such as printed internal forms, advertising brochures, etc. are not treated as inventory.

All inventories are stated at the lower of cost and net realisable value.

M Intangible Assets

i) Goodwill

Goodwill represents the excess of the cost of an acquisition over the fair value of the consolidated entity’s share of the net identifiable assets of the acquired entity at the date of acquisition. Goodwill on acquisitions of controlled entities is included in intangible assets. Goodwill on acquisitions of associates is included in the carrying value of investments in associates. Goodwill is not amortised but tested for impairment annually, or more frequently if events indicate that it might be impaired. In this event, it is carried at cost less accumulated impairment losses.

ii) Computer software

Costs directly incurred in acquiring computer software, plus costs incurred in developing major products or systems that will contribute to future period financial benefits through revenue generation and/or cost reductions are capitalised to computer software and amortised over the estimated useful life. Costs incurred on research and software maintenance are expensed as incurred.

The consolidated entity uses the following rates and methods of depreciation:

Rate / Life Method

Major System or Product Development 3 to 7 years straight line

Computer Software 40% reducing balance

N Members’ Deposits

Members’ deposits are measured at amortised cost using the effective interest rate method (refer Note 1F).

Interest on deposits is brought to account using the effective interest rate method (refer Note 1D).

O Financial Liabilities

Financial liabilities are measured at amortised cost using the effective interest rate method (refer Note 1D) except for derivatives, financial liabilities designated as at fair value through profit and loss, and in other limited circumstances as allowed under AASB 9 Financial Instruments which are subsequently measured at fair value through profit and loss. All the consolidated entity’s financial liabilities except for derivatives are classified at amortised cost.

P Provisions

The consolidated entity makes provision where it has a present legal or constructive obligation as a result of past events and it is probable that an outflow of resources will be required to settle the obligation.

A provision for promotion and reward scheme costs is recognised when the present obligations arise. The provision is measured as the amount unpaid at the balance date discounted by an estimated rate of non-usage.

Q Derivative InstrumentsThe consolidated entity uses derivative financial instruments to hedge its exposure to interest rate risks arising from operational, financing and investment activities. In accordance with its treasury management policy, the consolidated entity does not hold or issue derivative financial instruments for trading purposes.

All derivatives, including those used for balance sheet hedging purposes, are recognised on the balance sheet at fair value and are disclosed as an asset where they have a positive fair value at balance date or as a liability where the fair value at balance date is negative (refer Note 1F).

Derivatives are initially recognised at fair value on the date a derivative contract is entered into and subsequently remeasured to their fair value at balance date. Fair values for interest rate swaps is the estimated amount that the Society would receive or pay to terminate the swap at the balance date, taking into account current interest rates and the credit worthiness of the swap counterparties. Movements in the carrying amounts of derivatives are recognised in profit and loss, unless the derivative is designated as a hedge and meets the requirements for hedge accounting.

i) Cash flow hedges

For a derivative designated as hedging a cash flow exposure arising from a recognised asset or liability (or a highly probable forecast transaction), the gain or loss on the derivative associated with the effective portion of the hedge is initially recognised in equity in the cash flow hedge reserve and reclassified into the statement of other comprehensive income when the hedged item is brought to account. The gain or loss relating to the ineffective portion of the hedge is recognised immediately in profit and loss.

Notes to and Forming Part of the Financial Statementsfor the year ended 30 June 2015

Annual Report | 2014-15Greater Building Society 3231

CONSOLIDATED SOCIETY

2015 2014 2015 2014

$’000 $’000 $’000 $’000

2. INTEREST REVENUE

Cash and cash equivalents 6,054 7,597 5,454 6,875

Investment securities 29,875 24,920 46,036 38,376

Loans and advances 223,331 231,562 223,331 231,611

259,260 264,079 274,821 276,862

3. INTEREST EXPENSE

Deposits 122,920 128,978 122,943 129,023

Other financial liabilities 9,369 10,797 25,564 25,365

132,289 139,775 148,507 154,388

4. NON-INTEREST INCOME

Commission 4,744 3,684 4,744 3,684

Dividend revenue (including revenue on wind-up of wholly owned subsidiary)

- 17 - 17

Fee income 16,125 14,428 16,125 14,428

Impaired losses recovered 23 16 23 16

Net gain on revaluation of investment properties 660 2 660 2

Net gain on revaluation of land and buildings 124 16 140 106

Net gain on disposal of investment securities 2,771 2,215 2,771 2,215

Net gain on disposal of property, plant and equipment

96 197 96 197

Rental revenue 267 250 267 250

Sales revenue from sale of inventory - 2,348 - -

Trust distributions - - - 504

Other revenue 220 657 548 804

25,030 23,830 25,374 22,223

5. NON-INTEREST EXPENSE

Amortisation of computer software 582 676 582 676

Cost of inventory sold - 1,541 - -

Depreciation – buildings 361 359 361 359

Depreciation – leasehold improvements 1,512 1,524 1,512 1,524

Depreciation – plant and equipment 1,565 1,886 1,565 1,886

Employee related expense 53,226 52,335 53,226 52,335

Net loss on disposal of other financial assets - 10 - 10

Net loss on disposal of property, plant and equipment 180 84 180 84

Operating rental expense 9,855 9,578 9,855 9,578

Payment system processing costs 8,006 7,107 8,004 7,105

Other general and administration expenses 27,074 28,939 27,025 27,058

102,361 104,039 102,310 100,615

ii) Fair value hedges

For a derivative designated as hedging a fair value exposure arising from a recognised asset or liability (or a firm commitment), the gain or loss on the derivative is recognised in profit and loss together with any changes in the fair value of the hedged asset or liability that are attributable to the hedged risk.

R Employee Entitlements

i) Wages and salaries and annual leave

Liabilities for wages and salaries, annual leave and sick leave are recognised and are measured at the amounts expected to be paid when the liabilities are settled.

ii) Long service leave

A liability for long service leave is recognised and is measured as the present value of expected future payments to be made in respect of services provided by employees up to the balance date using the projected unit credit method. Consideration is given to expected future wage and salary levels, experience of employee departures and periods of service. Expected future payments are discounted using market yields on national government guaranteed securities with terms to maturity that match, as closely as possible, the estimated future cash outflows.

iii) Superannuation

Contributions are made by the consolidated entity to an employee’s superannuation fund and are charged as expenses when incurred. The consolidated entity has no legal obligation to cover any shortfall in the funds’ liability to provide benefits to employees on retirement.

iv) On-costs

On-costs associated with employees, including payroll tax, are recognised as liabilities and expenses when the employment to which they relate has occurred.

S Reserves

With effect from 1 July 2005 the Society has established a reserve for credit losses to cover credit risks inherent but not yet incurred in the loan portfolio (refer Note 1I (iii)). Movement in the credit loss reserve is recognised as an appropriation of retained profits.

T Goods and Services Tax

Where capital or expense acquisitions relate to input taxed activities, goods and services tax is generally non-recoverable from taxation authorities. Accordingly, where the amount of goods and services tax incurred is not recoverable, the tax is recognised as part of the cost of acquisition of an asset or as part of an item of expense.

For the purposes of the statement of cash flows, receipts and payments from operations are inclusive of goods and services tax.

U Impairment