2017 gasb update - gasb 75 is coming! (and...

TRANSCRIPT

1

2017 GASB Update - GASB 75 is Coming! (And Beyond…)

June 20, 2017

2

3

• GASB 72 – Fair value• GASB 73 – Certain pensions not administered

through a trust• GASB 76 – GAAP hierarchy• GASB 79 – External investment pools

Recent GASB Activity - Past

4

• GASB 74 – OPEB reporting for plans• GASB 77 – Tax abatement disclosures• GASB 78 – Certain multiple-employer defined

benefit pension plans• GASB 80 – Blending requirements for certain

component units• GASB 82 – Pension issues• Implementation Guide No. 2016-1

Recent GASB Activity - Present

5

• GASB 75 – OPEB reporting for employers (2018)

• GASB 81 – Irrevocable split-interest agreements (2018)

• GASB 83 – Asset retirement obligations (2019)• GASB 84 – Fiduciary activities (2020)• GASB 85 – Omnibus (2018)• GASB 86 – Debt Extinguishment (2018)

Recent GASB Activity - Future

6

A Brief Recap

7

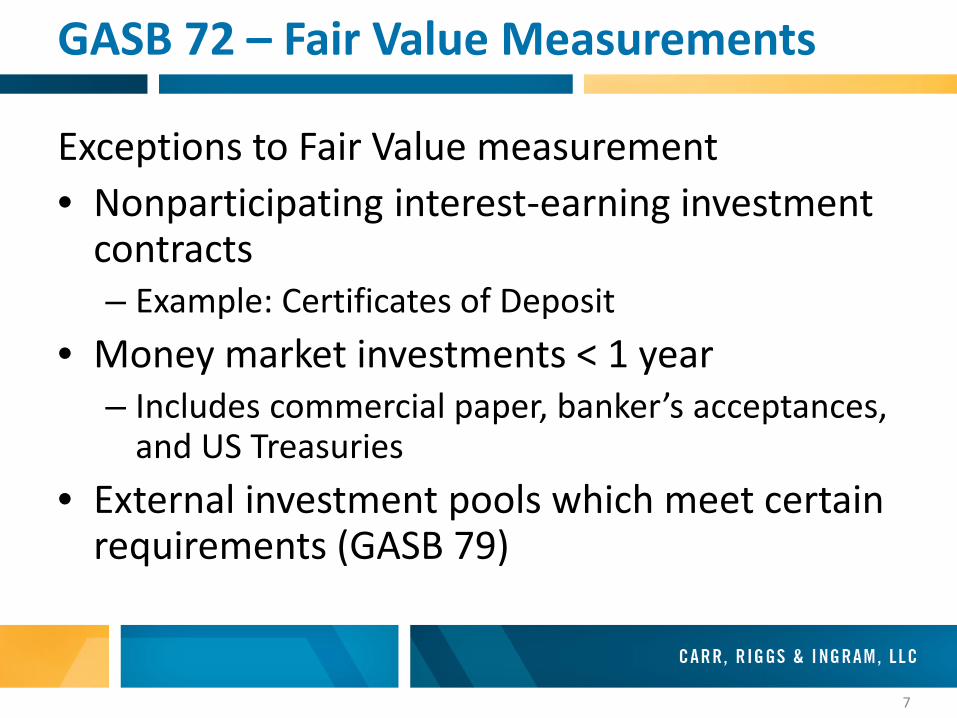

Exceptions to Fair Value measurement• Nonparticipating interest-earning investment

contracts– Example: Certificates of Deposit

• Money market investments < 1 year– Includes commercial paper, banker’s acceptances,

and US Treasuries• External investment pools which meet certain

requirements (GASB 79)

GASB 72 – Fair Value Measurements

8

GASB 73 – More Pensions

Effective – Years beginning after 6/15/2016 AND Years beginning after 6/15/2015

9

Accounting and Financial Reporting For Pensions and Related Assets That Are Not

Within The Scope of GASB 68, and Amendments to Certain Provisions of GASB 67

and 68

GASB 73 – More Pensions

10

• Impacts pensions WITHOUT a trust• If the employer does not have a “special

funding situation” – should record an obligation for the Total Pension Liability

• Discount rate to use – yield or index rate for 20-year, tax-exempt GO municipal bonds with average rating of AA/Aa or better

GASB 73 – More Pensions

11

• Assets accumulated for the payment of pension obligations that are NOT administered through a trust should NOT be accounted for as “pension plan assets”

• Required disclosures – similar to requirements of GASB 67 and 68 in the notes and RSI

GASB 73 – More Pensions

12

GASB 79 – External Investment Pools

Effective – years beginning after June

15, 2015 except provisions on portfolio quality, custodial credit risk & shadow pricing which are effective for years after December

15, 2015

13

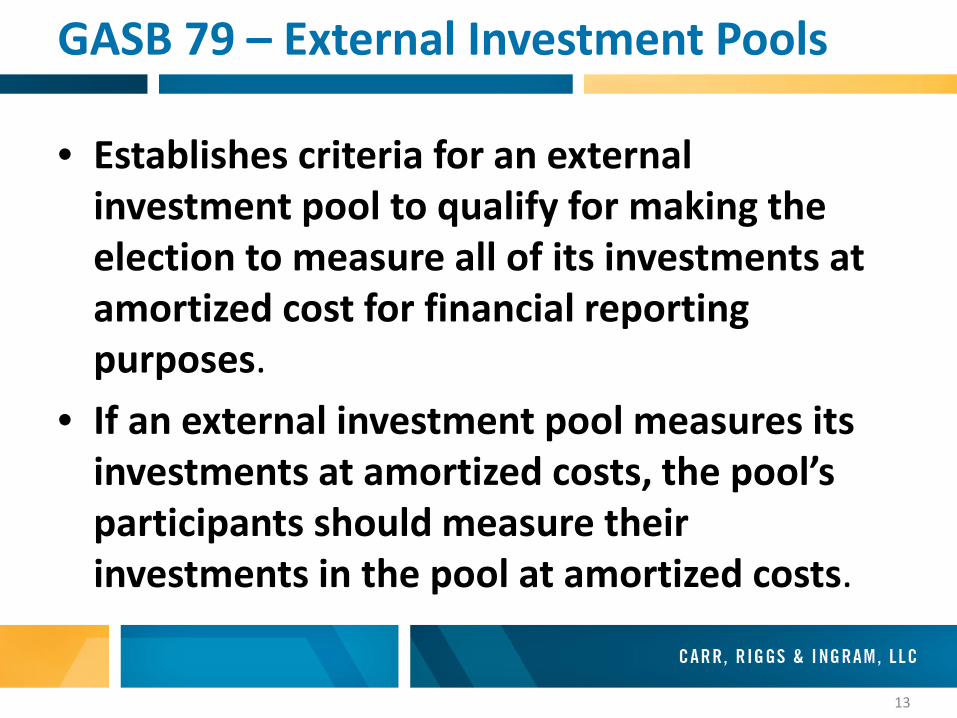

• Establishes criteria for an external investment pool to qualify for making the election to measure all of its investments at amortized cost for financial reporting purposes.

• If an external investment pool measures its investments at amortized costs, the pool’s participants should measure their investments in the pool at amortized costs.

GASB 79 – External Investment Pools

14

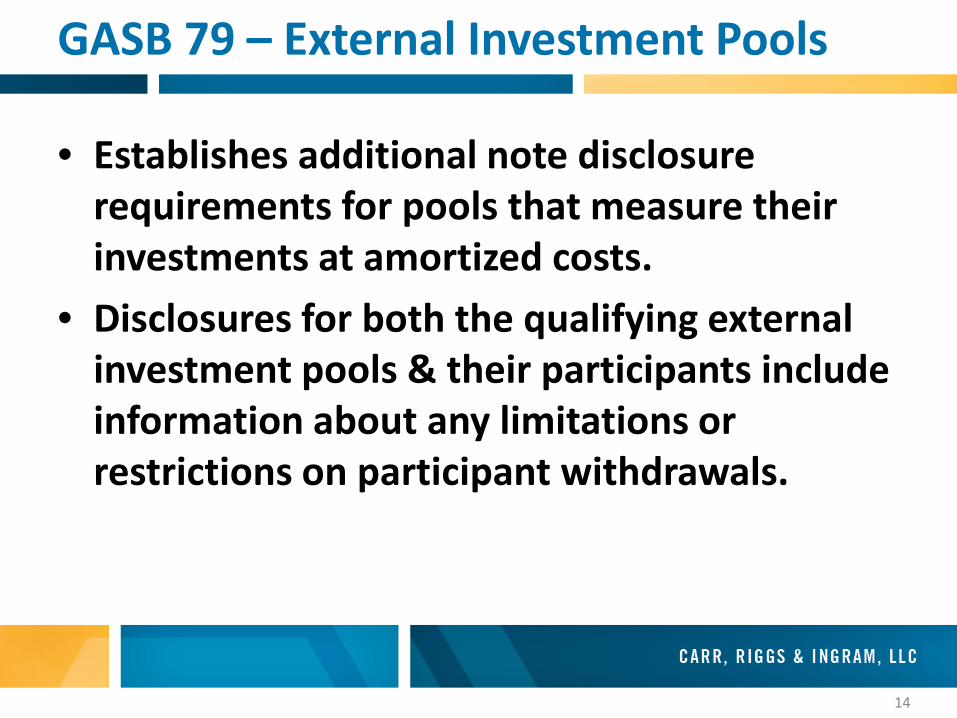

• Establishes additional note disclosure requirements for pools that measure their investments at amortized costs.

• Disclosures for both the qualifying external investment pools & their participants include information about any limitations or restrictions on participant withdrawals.

GASB 79 – External Investment Pools

15

GASB 74 and 75 - OPEB

16

GASB 74 and 75 - OPEB

17

• 74 – Financial Reporting For Post-Employment Benefit Plans Other Than Pension PlansEffective – years beginning after June 15, 2016

• 75 – Accounting and Financial Reporting For Post-Employment Benefits Other Than PensionsEffective – years beginning after June 15, 2017

GASB 74 and 75 - OPEB

18

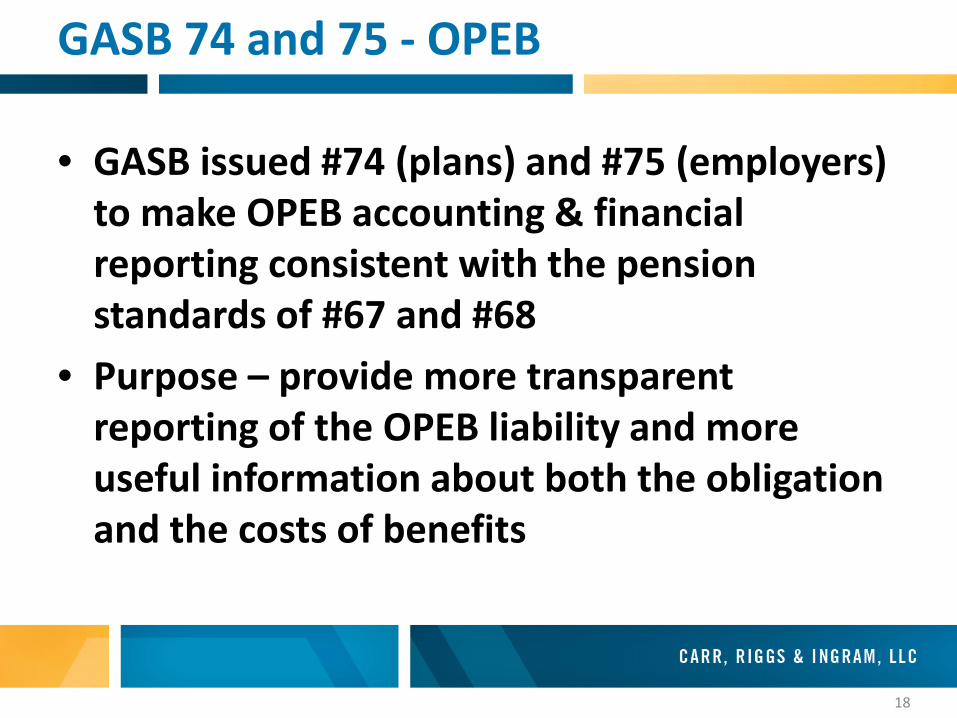

• GASB issued #74 (plans) and #75 (employers) to make OPEB accounting & financial reporting consistent with the pension standards of #67 and #68

• Purpose – provide more transparent reporting of the OPEB liability and more useful information about both the obligation and the costs of benefits

GASB 74 and 75 - OPEB

19

Plan and Asset Reporting

Scope – defined benefit and defined contribution OPEB plans administered through trusts that meet specified criteria

GASB 74 - OPEB

20

Also addresses assets that are accumulated for providing OPEB benefits that are NOT

administered through trusts that meet the criteria

• Assets are reported as assets in the employer’s governmental/proprietary funds

• Assets that are held for other governments –reported in an agency fund

GASB 74 - OPEB

21

• Not many changes from GASB 43 as far as financial statement recognition is concerned

• RSI and disclosure changes are primarily to reflect changes in the measurement of defined benefit liabilities of employers

GASB 74 - OPEB

22

Scope and Applicability to Employers:

Same definition of OPEB as used in GASB 45(all post-employment healthcare benefits and other benefits that are not provided through a pension plan)

GASB 75 - OPEB

23

Liability – based on the total OPEB liability –the portion of actuarial present value of projected benefit payments that is attributable to past periods of employee service

GASB 75 - OPEB

24

• Is OPEB administered through a trust that meets specified criteria?

• If yes, recognize the net OPEB liability (total OPEB liability minus OPEB plan fiduciary net position)

• If no, recognize the total OPEB liability

GASB 75 - OPEB

25

• Measurement date –• The employer’s liability to employees is

measured as of a date no earlier than the end of the employer’s prior fiscal year and no later than the employer’s current fiscal year

• Based on an actuarial valuation obtained at least biennially no more than 30 months and 1 day earlier than the employer’s most recent fiscal year-end

GASB 75 - OPEB

26

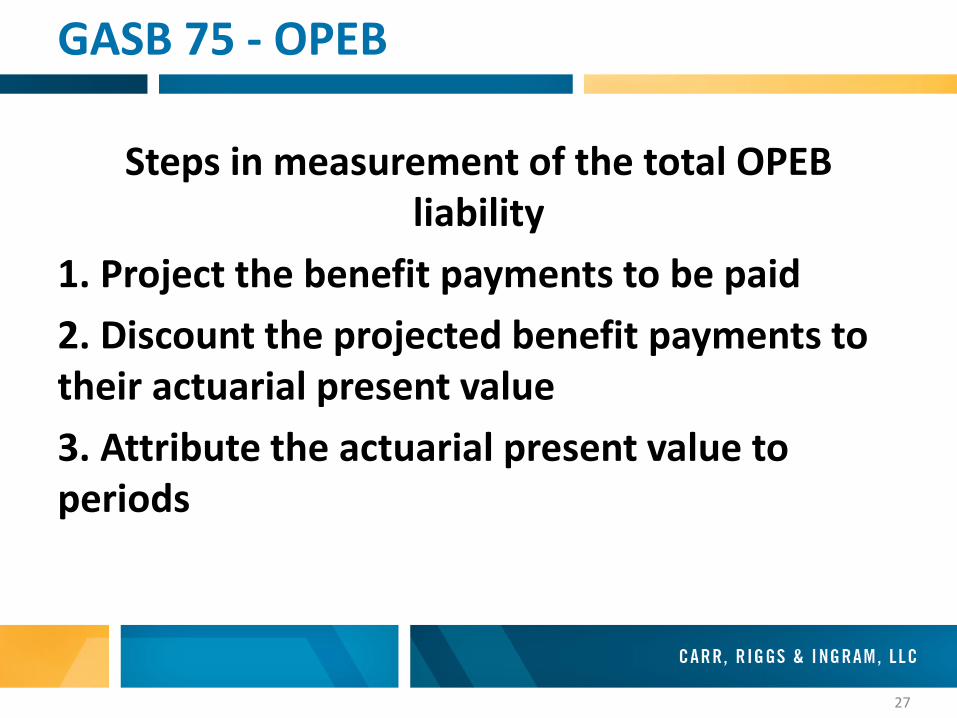

27

Steps in measurement of the total OPEB liability

1. Project the benefit payments to be paid2. Discount the projected benefit payments to their actuarial present value3. Attribute the actuarial present value to periods

GASB 75 - OPEB

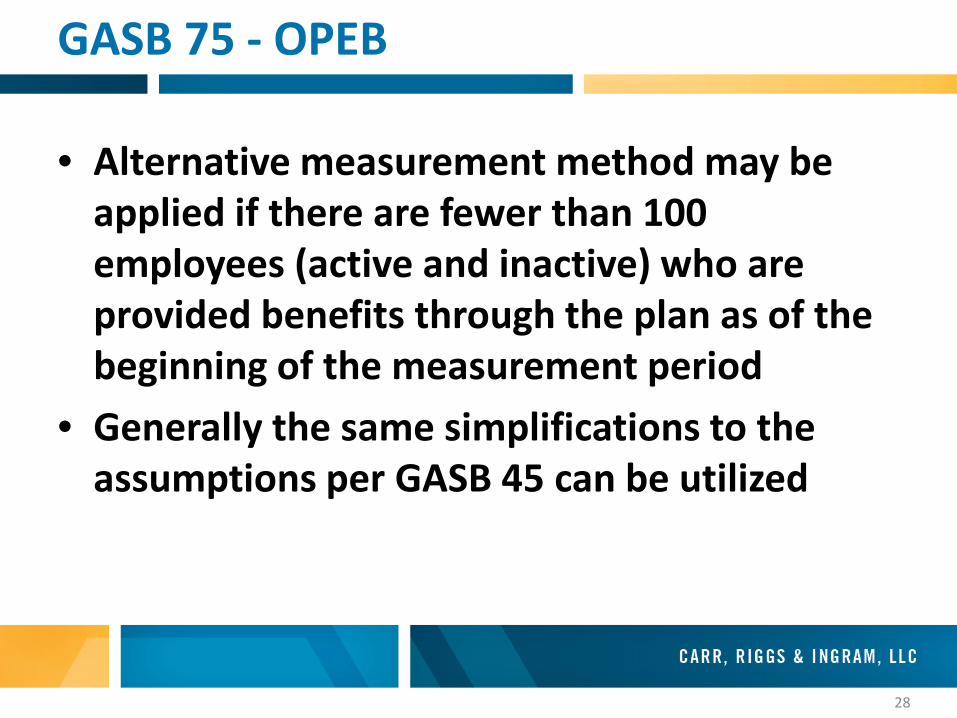

28

• Alternative measurement method may be applied if there are fewer than 100 employees (active and inactive) who are provided benefits through the plan as of the beginning of the measurement period

• Generally the same simplifications to the assumptions per GASB 45 can be utilized

GASB 75 - OPEB

29

Changes in the OPEB liability – Will record most changes in the liability for the current financial reporting period as immediate OPEB expense –except:1. Changes in the total OPEB liability:

a. Differences between expected and actual experience related to economic and demographic factors in the measurement of the total OPEB liability

b. Changes of assumptions in the measurement of the total OPEB liability

GASB 75 - OPEB

30

2. For OPEB administered through a trust in which specified criteria are met:a. Difference between projected and actual

earnings on plan investmentsb. Employer contributions

GASB 75 - OPEB

31

Cost-sharing employers:• Recognize proportionate share of collective

net OPEB liability, OPEB expense, and deferred outflows/inflows related to OPEB

GASB 75 - OPEB

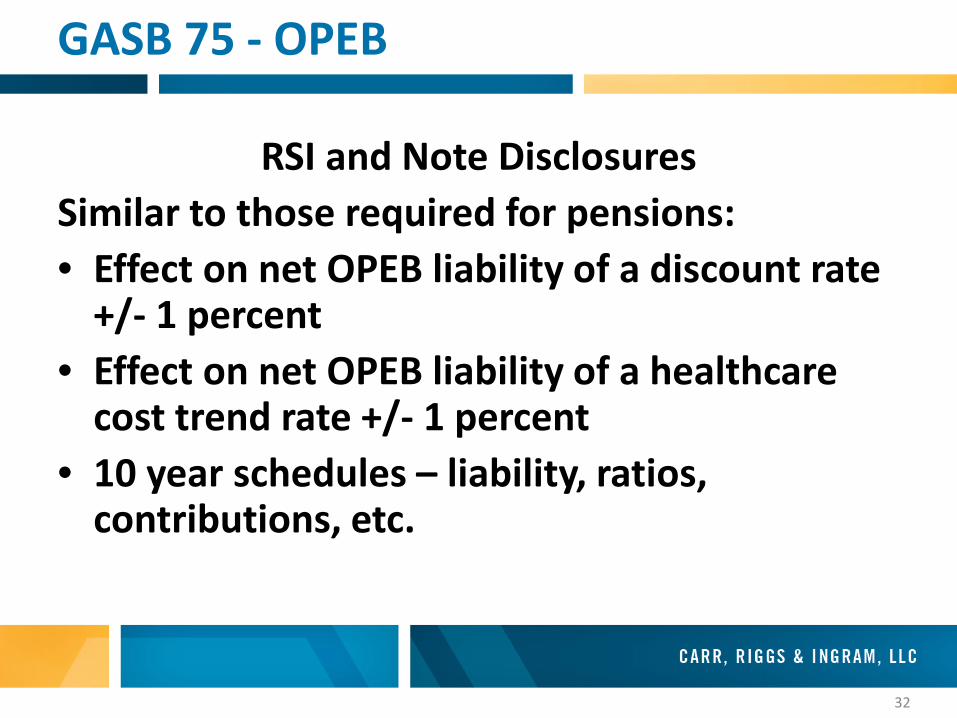

32

RSI and Note DisclosuresSimilar to those required for pensions:• Effect on net OPEB liability of a discount rate

+/- 1 percent• Effect on net OPEB liability of a healthcare

cost trend rate +/- 1 percent• 10 year schedules – liability, ratios,

contributions, etc.

GASB 75 - OPEB

33

Sensitivity of the net OPEB liability to changes in the discount rate. The following presents the net OPEB liability of the school districts, as well as what the school districts’ net OPEB liability would be if it were calculated using a discount rate that is 1-percentage-point lower (6.5 percent) or 1-percentage-point higher (8.5 percent) than the current discount rate:

GASB 75 - OPEB

34

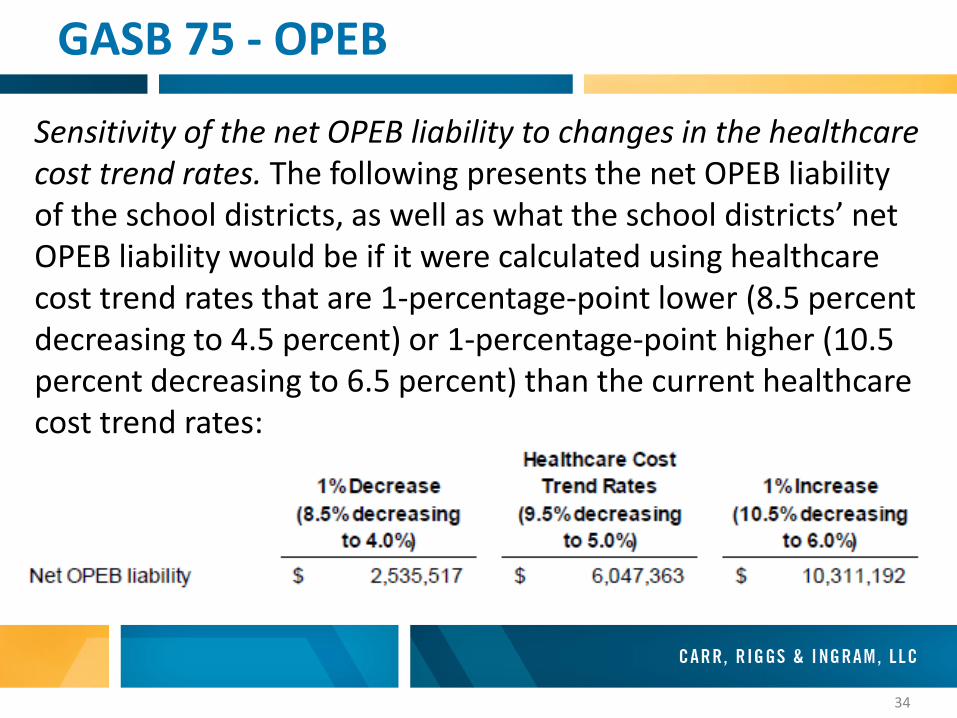

Sensitivity of the net OPEB liability to changes in the healthcare cost trend rates. The following presents the net OPEB liability of the school districts, as well as what the school districts’ net OPEB liability would be if it were calculated using healthcare cost trend rates that are 1-percentage-point lower (8.5 percent decreasing to 4.5 percent) or 1-percentage-point higher (10.5 percent decreasing to 6.5 percent) than the current healthcare cost trend rates:

GASB 75 - OPEB

35

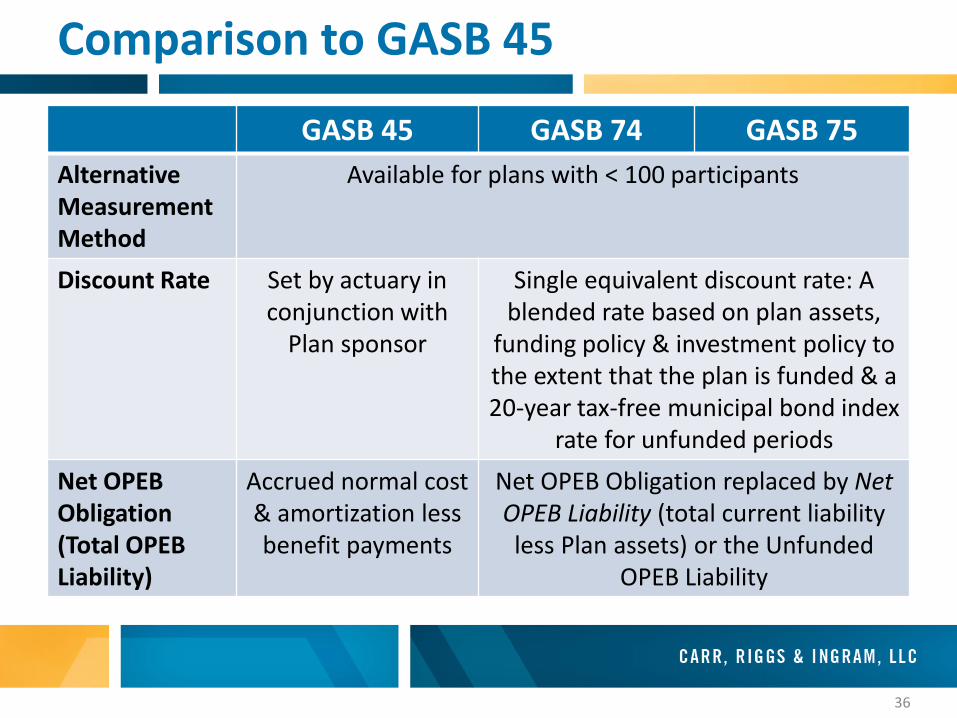

GASB 45 GASB 74 GASB 75Actuarial Cost Method

Multiple Permissible Actual Cost

Methods

Entry Age Normal Cost Method Required

Valuation Date Not more than 24 months prior to the

beginning of the biennial or triennial

valuation cycle

No more than 24 months prior to fiscal year-end

No more than 30 months & 1 day

prior to fiscal year-end

Valuation Frequency

Biennial for employers with >

200 covered participantsTriennial for

employers < 200 participants

Once every 2 years regardless of size

Comparison to GASB 45

36

GASB 45 GASB 74 GASB 75Alternative MeasurementMethod

Available for plans with < 100 participants

Discount Rate Set by actuary in conjunction with

Plan sponsor

Single equivalent discount rate: A blended rate based on plan assets,

funding policy & investment policy to the extent that the plan is funded & a 20-year tax-free municipal bond index

rate for unfunded periodsNet OPEB Obligation (Total OPEB Liability)

Accrued normal cost & amortization less benefit payments

Net OPEB Obligation replaced by Net OPEB Liability (total current liability less Plan assets) or the Unfunded

OPEB Liability

Comparison to GASB 45

37

GASB 45 GASB 74 GASB 75Recognition of Changes in Liability

Changes amortized in gains/losses over a period of 30 years

or less

Investment gains & losses arerecognized – or phased in – over 5

years while changes in liability due to experience & assumption changes are amortized over the average remaining

lifetime of the populationImplicit Subsidy

Community rated plans not required

to recognize an implicit subsidy

All Plan type must recognize an implicit subsidy

Comparison to GASB 45

38

39

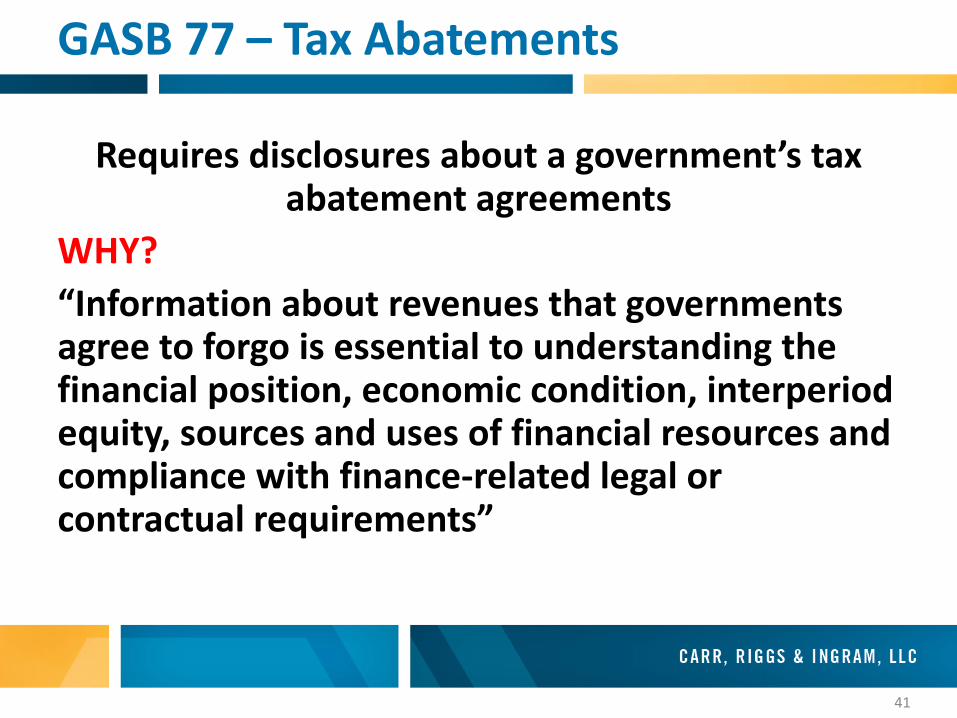

GASB 77 – Tax Abatements

40

GASB 77 – Tax Abatements

Tax Abatement Disclosures

Effective – years beginning after

December 15, 2015

41

Requires disclosures about a government’s tax abatement agreements

WHY?“Information about revenues that governments agree to forgo is essential to understanding the financial position, economic condition, interperiod equity, sources and uses of financial resources and compliance with finance-related legal or contractual requirements”

GASB 77 – Tax Abatements

42

Emphasis is on the substance of the arrangement meeting the definition in GASB 77, not on its name or form

Does not include all transactions that reduce tax revenues – some actions can cause a reduction in taxes but are not abatements

GASB 77 – Tax Abatements

43

Applies only to arrangements that meet this definition:

A reduction in tax revenues that results from an agreement between one or more governments and an individual or entity in which:(a) One or more governments promise to forgo

tax revenues to which they are otherwise entitled ---AND

GASB 77 – Tax Abatements

44

(b) the individual or entity promises to take a specific action after the agreement has been entered into that contributes to economic development or otherwise benefits the governments or the citizens of those governments

GASB 77 – Tax Abatements

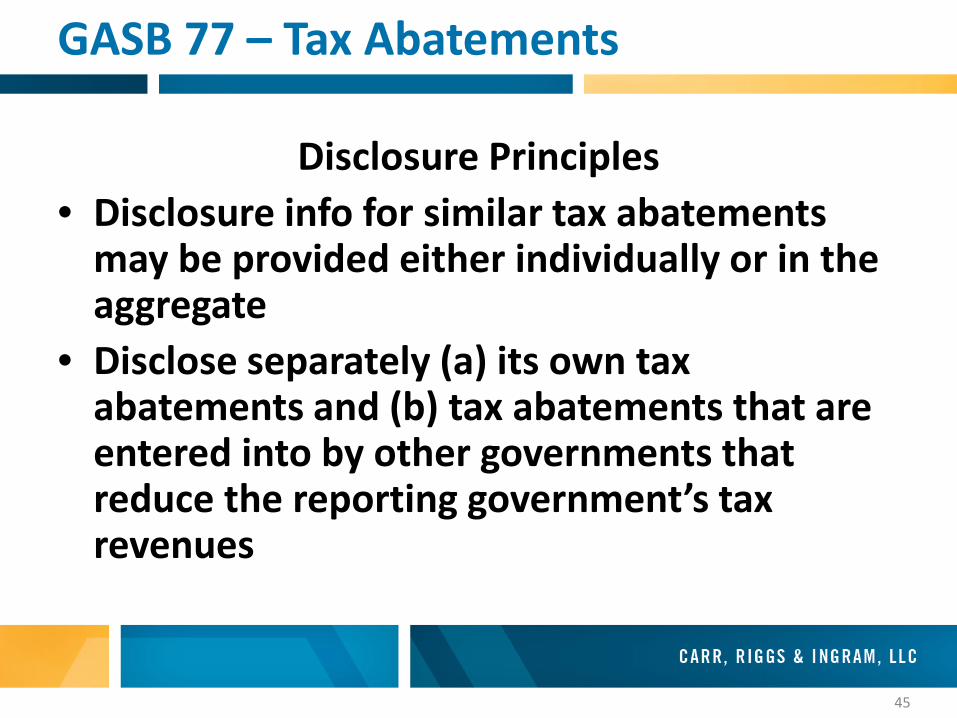

45

Disclosure Principles• Disclosure info for similar tax abatements

may be provided either individually or in the aggregate

• Disclose separately (a) its own tax abatements and (b) tax abatements that are entered into by other governments that reduce the reporting government’s tax revenues

GASB 77 – Tax Abatements

46

• Must disclose own tax abatements by major program

• Disclose those of other governments by the government and the specific tax that was abated

• May disclose individual abatements above the quantitative threshold established by the government

GASB 77 – Tax Abatements

47

• Disclosure commences in the period in which a tax abatement agreement is entered into and continues until the tax abatement expires, unless otherwise specified

GASB 77 – Tax Abatements

48

NOTE (X): Tax Abatements

The County enters into property tax abatement agreements with local businesses under the State Economic Development Opportunity Act of 20X1. Under the Act, localities may grant property tax abatements of up to 40 percent of a business’ property tax bill for the purpose of attracting or retaining businesses within their jurisdictions. The abatements may be granted to any business located within or promising to relocate to the County.

GASB 77 – Tax Abatements

49

Note (X): Tax AbatementFor the fiscal year ended September 30, 20X7, the County abated property taxes totaling $347,620 under this program, including the following tax abatement agreements that each exceeded 10 percent of the total amount abated:A 40 percent property tax abatement to a grocery store chain for purchasing and opening a store in an empty storefront in the business district. The abatement amounted to $97,500.A 40 percent property tax reduction for a local restaurant increasing the size of its restaurant and catering facility and increasing employment. The abatement amounted to $38,750.

GASB 77 – Tax Abatements

50

Brief Descriptive Info Government’s Own

Abatements

Other Government’s Abatements

Name of program X

Purpose of program X

Name of government X

Tax being abated X X

Authority to abate taxes X

Eligibility criteria X

Abatement mechanism X

Recapture provisions X

Types of recipient commitments X

GASB 77 – Tax Abatements

51

Other Disclosures Government’s Own Abatements

Other Government’s Abatements

Dollar amount of taxes abated X X

Amounts received or receivable from other governments associated with the abated taxes

X X

Other commitments by the government

X

Quantitative threshold for individual disclosure

X X

Information omitted (if any) due to legal prohibitions

X X

GASB 77 – Tax Abatements

52

Other GASB Pronouncements

53

GASB 78 – Multiple Employer Pensions

Pensions Provided through Certain

Multiple Employer Defined Benefit Pension Plans

Effective – years beginning after

December 15, 2015

54

• Excludes certain plans from the scope of #68• Cost-sharing multiple employer defined benefit

plans that are:a. not a state or local governmental planb. used to provide benefits to both

governmental and non-governmental employers, and

c. plans with no predominant gov’t employer

GASB 78 – Multiple Employer Pensions

55

GASB 80 – Blending Component Units

Blending Requirements for

Certain Component Units

Effective – years beginning after June

15, 2016

56

• Requires blending of a component unit incorporated as a not-for-profit corporation in which the primary government is the sole corporate member, as identified in the component unit’s articles of incorporation or bylaws.

• Does not alter GASB #39

GASB 80 – Blended Component Units

57

GASB 82 – Pension Issues

An Amendment of GASB Statements No.

67, 68 & 73

Effective – years beginning after June

15, 2016

58

• Addresses issues regarding:a. presentation of covered payroll – defines

covered payroll as the payroll on which contributions to a pension plan are based & ratios that use that measure– Previously, covered payroll was the payroll of

employees that are provided with pensions through the plan

GASB 82 – Pension Issues

59

• Addresses issues regarding:b. selection of assumptions and treatment of

deviations from Actuarial Standard of Practice– Deviations are not considered to be in

conformity with GASB

GASB 82 – Pension Issues

60

• Addresses issues regarding:c. classification of payments made by

employers to satisfy employee contribution requirements as plan member contributions

– Requires employer’s expense/ expenditures for these contributions be recognized in the period assessed

– Recognized as compensation other than pension (not pension expense)

GASB 82 – Pension Issues

61

62

For the Future…

63

GASB 81 – Split-Interest Agreements

Irrevocable Split-Interest Agreements

Effective – years beginning after

December 15, 2016

64

• Giving agreements used by donors to provide resources to two or more beneficiaries, including governments

• Created through trusts or other legally enforceable agreements

• Donor transfers resources to an intermediary to hold & administer for the benefit of the government & at least 1 other beneficiary.

GASB 81 – Split-Interest Agreements

65

• Requires that a government records assets, liabilities & deferred inflows at the agreement inception

• Revenue is recognized when the resources become applicable to the reporting period

• Standard should be applied retroactively

GASB 81 – Split-Interest Agreements

66

GASB 83 – Asset Retirements Obligations

Certain Asset Retirement Obligations

Effective – years beginning after June

15, 2018

67

• ARO – a legally enforceable liability associated with the retirement of a tangible capital asset.

• Establishes criteria for determining the timing, pattern of recognition & corresponding deferred outflows for ARO’s.

• Recognition occurs when liability is both incurred & reasonably estimable.

GASB 83 – Asset Retirement Obligations

68

• Laws & regulations may require governments to take specific actions to retire certain capital assets, like sewage treatment plants.– May also result from contracts or court

judgements

• Internal events include the occurrence of contamination or placing into operation an asset that is required to be retired

GASB 83 – Asset Retirement Obligations

69

• ARO is based on best estimate of the current value of outlays to be incurred– Should include probability weighting of all

potential outcomes– Alternative measure if probability weighting is

not financially feasible• Deferred outflows reduced & recognized as

outflows in a systematic manner over the life of the capital asset.

GASB 83 – Asset Retirement Obligations

70

GASB 84 – Fiduciary Activities

Fiduciary Activities

Effective – years beginning after

December 15, 2018

71

• Focus is on:– Whether a government is controlling the assets

of the fiduciary activity; and– The beneficiaries with whom a fiduciary

relationship exists

• Establishes the criteria on which a fund should be reported as a fiduciary fund

GASB 84 – Fiduciary Activities

72

• Four fiduciary funds:– Pension (and OPEB) trust funds– Investment trust funds– Private-purpose trust funds– Custodial funds

• Liability recognized in the fiduciary fund when an event has occurred that requires the government to disburse fiduciary resources.

GASB 84 – Fiduciary Activities

73

• Three words… School Internal Funds

GASB 84 – Fiduciary Activities

74

GASB 85 – Omnibus 2017

Omnibus 2017

Effective – years beginning after June

15, 2017

75

• Addresses a variety of practice issues identified during the implementation & application of certain GASB statements– Blending a component unit in which the primary

government is a business-type activity with a single column for FS presentation

– Reporting amounts previously reported as goodwill

– Classifying real estate held by insurance entities

GASB 85 – Omnibus 2017

76

– Measuring certain investments at amortized cost– Timing of measurement of pension or OPEB

liabilities for entities using the current financial resources measurement focus

– Recognizing on-behalf payments for pensions or OPEB

– Presenting payroll-related measures in RSI– Classifying employer paid member contributions

for OPEB

GASB 85 – Omnibus 2017

77

– Simplifying certain aspects of alternative measurement method for OPEB

– Accounting & financial reporting for OPEB provided through certain multiple-employer defined benefit OPEB plans.

GASB 85 – Omnibus 2017

78

GASB Technical Agenda

www.gasb.org

What Lies Ahead??

79

GASB Technical Agenda Overview

Technical Agenda Current Stage TimingConceptual Framework: Recognition PV Redeliberations Jan 2017 –

Mar 2018

Financial Reporting Model –Reexamination of Statements 34, 35, 37, 41 & 46 and Interpretation 6

Invitation to Comment Redeliberations

Jan 2017 –May 2018

Leases – Reexamination of NCGA Statement 5 & GASB Statement 13

Final Pronouncement Q2 2017

Revenue & Expense Recognition Initial Deliberations

80

GASB Technical Agenda Overview

Technical Agenda Current Stage TimingCapitalization of Interest Cost Added to AgendaCertain Debt Extinguishments Final Pronouncement Q2 2017Debt Disclosures – Including DirectBorrowing

Initial Deliberations

Equity Interest Ownership Issues Initial DeliberationsImplementation Guidance – Update Final Pronouncement Q2 2017Implementation Guide for Statements 74 & 75 on Other Postemployment Benefits

Final Pronouncement Q2 2017

81

Brief note – Financial Reporting Model Reexamination

Major criticism of governmental financial reports – that they are not available on a timely basis.GASB will be looking for appropriate changes to the model that could positively impact the timeliness of reports.

GASB Technical Agenda Overview

82

Questions?