20171sm46d1l3jt643nn5k1s8l2e-wpengine.netdna-ssl.com/.../2018/03/...report.pdf · students from the...

TRANSCRIPT

annual REPORT &GROuP FInanCIal STaTEMEnTS

2017

VALUE DISTRIBUTION STATEMENT

2017 2016

P’000’s P’000’s

VALUE ADDED

REVEnUE 269,986 210,822 Other income 2,955 17,965 Finance income 344 733 Release of impairement in associate 1,204 - Operating expenditure (106,503) (90,787)VALUE cREAtED 167,986 138,733 Resource royalties, lease rentals, licences & other fees 15,282

16,077

ADjUstED VALUE ADDED 183,268 154,810

VALUE DIstRIBUtED

to EmPLoyEEs

Net salaries, wages and other benefits 52,237 42,705

to PRoVIDERs of cAPItAL

Dividends 35,776 31,304 Finance cost 136 82

35,912 31,386

to GoVERnmEnt

Taxation 22,719 19,220 VAT 19,636 14,064 PAYE 6,899 4,368 Resource royalties, lease rentals, licences & other fees 15,282 16,077

64,536 53,729

REtAInED foR ExPAnsIon AnD GRowth

Depreciation and amortisation 23,000 15,661 Deferred tax (1,061) 375 Retained profit for the year 28,280 25,018

50,219 41,054

ADjUstED VALUE ADDED 202,904 168,874

sUmmARy

Government 32% 32%Employees 26% 25%Providers of capital 18% 19%Retained for expansion and growth 24% 24%

100% 100%

VALUE DIstRIBUtED 2017

GoVERnmEnt

24%

EmPLoyEEs

PRoVIDERs of cAPItAL

REtAInED foR ExPAnsIon &

GRowth

18%

26%32%

VALUE DIstRIBUtED 2016

24%19%

25%32%

GoVERnmEnt EmPLoyEEs

PRoVIDERs of cAPItAL

REtAInED foR ExPAnsIon &

GRowth

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

1

Corporate Information 2Group Structure 3Chief Executive Officer’s Report 4Corporate Social Responsibility Statement 6Directors’ Report 8Corporate Governance 10Report of the Independent Auditors 13Statements of Comprehensive Income 18 Statements of Financial Position 19Statements of Changes in Equity 20Statements of Cash Flow 22Summary of Significant Accounting Policies 23Financial Risk Management 37Critical Accounting Estimates and Assumptions 42Notes to the Financial Statements 45Shareholders Information 65Notice of Annual General Meeting 66Proxy Form 67Notes 68

CONTENTS

Incorporated In Botswana:Company number: 4543Date of incorporation: 31 May 1983

company secretary:R Gerrard P O Box 32Kasane

transfer secretarIes:DPS Consulting Services (Proprietary) LimitedPlot 50371, Fairground Office ParkGaborone

regIstered offIce:Plot 50371Fairground Office ParkGaborone

Independent audItors:PricewaterhouseCoopersGaborone

Bankers:Bank Gaborone LimitedFirst National Bank of Botswana LimitedBank Windhoek Limited – NamibiaFirst Rand Bank Limited – South Africa

nature of BusIness

chobe Holdings Limited owns and operates through its wholly owned subsidiaries, eleven

eco-tourism lodges and camps on leased land in northern Botswana and the caprivi strip

in namibia with a combined capacity of 310 beds under the brands of desert & delta safaris

and ker & downey Botswana. safari air, a wholly owned air charter operator provides air

transport services to the group’s camps and lodges. desert & delta safaris (sa) (pty) Ltd,

another wholly owned subsidiary operating in south africa, provides reservation services to

the group. In the current year, the group acquired an air maintenance operation from a third

party which is operated through north west air (pty) Ltd.

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

2

CORPORATE INFORMATION

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

3

100% 100% 100% 100% 100% 100% 100% 100% 100% 66.66% 100%

dormant subsidiaries and associates- Xugana Air (Pty) Ltd – 100% held by The Bookings Company (Pty) Ltd- BVP Ltd – 25% held by Ker and Downey Botswana (Pty) Ltd- Chobe Dairies (Pty) Ltd – 50% held by Chobe Farms (Pty) Ltd

t Incorporated in Namibia tt Incorporated in South Africa All other companies incorporated in Botswana

desert and deLta

safarIs (sa) (pty) Ltd tt

VensteLL (pty) Ltd

cHoBe game Lodge

(pty) ltd

ker & downey

Botswana (pty) Ltd

cHoBe farms

(pty) Ltd

cHoBe propertIes

(pty) Ltd

cHoBe eXpLoratIons

(pty) Ltd

caprIVI fLy fIsHIng safarIs

(pty) Ltd t

tHe BookIngs company (pty) ltd

desert and deLta

safarIs (pty) Ltd

nortH west aIr (pty) Ltd

kanana Ventures (pty) Ltd

okutI safarIs

(pty) Ltd

moremI safarIs

(pty) ltdLL tau

(pty) LtdLLoyds

camp (pty) Ltd

100% 100%

100% 100% 100%

GROUP STRUCTURE

Basis of preparation

The audited financial statements for the year ended 28th February 2017 have been prepared based on ac-counting policies which comply with International Financial Reporting Standards (“IFRS”). The ac-counting policies applied are consistent with those of the annual financial statements for the year ended 29th February 2016, as described in those annual fi-nancial statements.

financial results

During the period under review occupancy in-creased by 4% when compared to the same period in the prior year. This is considered satisfactory in light of continued uncertainty in the world econo-my, cheaper alternative destinations in the region and reduced capacity as a consequence of continu-ing lodge renovations and refurbishments.

A significant increase in revenue was recorded as a result of the aforementioned increase in bed nights sold, favourable exchange rates in our peak season and a marginal increase in achieved bed night rates in US Dollar terms as well as the contribution from the newly acquired, wholly owned, aircraft mainte-nance organisation.

Other operating income comprises mainly foreign exchange gains. The Botswana Pula remained fairly stable during the reporting period resulting in only modest foreign exchange gains when compared with the operating gains of the prior year.

P1.2m was received as a final settlement for the dis-posal of associate Lianshulu Lodge (Pty) Ltd, a Na-mibian company in which Chobe Holdings Ltd held a 44% interest.

CHIEF EXECUTIVE OFFICER'S REPORT

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

4

profit after tax increases by

14%

Increase in revenue28%Costs contained at inflationary levels

Capital expenditure of

P30.9 MILLION

financed from internally generated cashflows

cash & cash equivalent of

P91.3 MILLIONnegligible debt maintained

acquired an aircraft maintenance operation for a consideration of

P18.4 MILLIONfinanced from internally generated cashflows

HIgHLIgHts

Increase in occupancy levels4%

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

5

An operating cost increase of 20% is considered satisfactory in light of increased volumes of business and current inflation levels.

The Group spent, from internally generated cash flows P30.9 million, on the purchase of additional equipment and significantly improving existing buildings and equipment. A further P 18.4 million was used to acquire an air maintenance operation.

As previously announced, the Group, on 1st March 2016, acquired the Maun aircraft maintenance operation of Air Charter Botswana (Pty) Ltd. The fair value of assets acquired which was determined through a valuation was recorded through North West Air (Pty) Ltd, a 100% subsidiary of Chobe Holdings Ltd. The operation has made a positive contribution to the Group’s bottom line for the reporting period. It is anticipated that the financial contribution from this acquisition will be fully realised in the forthcoming financial year once the entity has been fully integrated into the Group.

Your directors approved a phantom share scheme during the year ended 28th February 2013 which allows the Group’s employees to participate in the dividend distributions of the Group. The scheme allows all qualifying staff to share equally in a bonus which is calculated to be equal to the value of dividends attaching to three million shares in the Company. A total of P1,200,000 was distributed amongst qualifying employees during the year ended 28th February 2017.

Leases

In December 2013, two of the Group’s subsidiaries submitted tenders for the lease, utilisation and management of Camp Okavango and Shinde Camp for non-consumptive tourism purposes.

After considerable delay both leases were signed subsequent to the financial year end. The initial period for both leases is fifteen years from March 2015.

future outlook

Political uncertainty associated with the new administration in the United States and other geo political events in the northern hemisphere has added volatility to the US Dollar, the Group’s main

revenue trading currency. A loss in value of the US Dollar would have a negative impact on the Group’s profitability.

The Ministry of Environment, Natural Resource Conservation and Tourism, through Botswana Tourism Organisation, has and continues to internationally expose Botswana as a destination of choice. These efforts are anticipated to result in more tourists visiting our country in general and the Group’s lodges in particular.

The Group continues to invest considerable resources to improve its marketing strategies, product offerings and cost controls. These initiatives are anticipated to translate into satisfactory results for the forthcoming financial year.

The Group’s strong cash position provides us with the opportunity to take advantage of any expansion opportunities that may arise.

dividends

In keeping with the Company’s dividend distribution policy and the solvency requirements of the Companies Act, 2003, your Directors have declared a dividend of 50 thebe per share, payable to shareholders registered at the close of business on 16th June 2017 for payment on 30th June 2017.

unclaimed dividends

The Directors wish to bring to the notice of shareholders that there are certain amounts of unclaimed dividends in the Company’s records. Shareholders are reminded to contact the Transfer Secretaries to claim their outstanding dividends.

By order of the Board of Directors

J m gibson ceo & deputy chairman18th may 2017

CHIEF EXECUTIVE OFFICER'S REPORT [COnTInUEd]

CORPORATE SOCIAL RESPONSIBILITY STATEMENT

1. overview

Chobe group policy is that funding for Cor-porate Social Responsibility (CSR) programs comes from group treasury and is accounted for at subsidiary company level. Primary areas of support are the areas in which the group operates i.e. North West, Chobe and Central Districts focusing on community involvement, environmental action and economic growth.

2. key initiatives in the year ended 28 february 2017

2.1 education and trainingAs part of government’s ‘adopt-a-school’ policy the company supports the follow-ing schools:

2.1.1 tshodilo Junior secondary schoolUniforms, stationery and bags were provided to twenty students. A further twenty students were treated to a weekend getaway at Leroo La Tau Lodge to experience the reality of tourism and conser-vation at the same level as full pay-ing customers.

2.1.2 kumaga primary schoolStudents from the school were taken on game activities to appre-ciate Botswana’s wildlife experi-ence. Financial assistance was also provided to the school to assist in various areas such as trophies to students that achieved a pass mark of over 75%, carear fair and provi-son for PSLE revision books which contributed to the school posting the best PSLE results in the Boteti region.

2.1.3 Liswaani Junior secondary schoolThe school was provided with books and other materials required for Science and Mathematics. Prizes to best performing students were also given in addition to re-pairing and refurbishing desks.

Two students are also sponsored on a full bursary basis to study International Hos-pitality Management degree courses of-fered by the Botswana Accountancy Col-lege. This number will increase to three from next year.

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

6

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

7

In 2006 Chobe Game Lodge developed a relationship with the Botswana National Youth Council which resulted in the youth of the Chobe District being trained in the Food and Beverage departments at Chobe Game Lodge. Close to 200 young men and women have been trained since incep-tion of the program with over 50 being employed by Chobe Game Lodge on a full time basis.

2.2 sports

The group provided financial sponsor-ship to Chobe United Football Club and Sankoyo Bush Bucks Football Club.

2.3 arts and culture

2.3.1 shorobe Basket co-operativeThis ongoing initiative is part of a broader focus on crafts whereby rural craft producers are supported to become production units and visitor centres while establishing a social and commercial enterprise.

2.3.2 Independence day celebrationsFinancial support in aid of Botswa-na’s Independence Day celebra-tions at Kumaga Village, Kasane, Kazungula and Lesoma was pro-vided.

2.4 welfare

2.4.1 tshodilo stimulation centreThis initiative ensures that about thirty children receive a regular wholesome lunch and also pro-vides the centre with much needed equipment.

2.4.2 Bana Ba Letsatsi (BBL)BBL supports around 100 vulner-able and orphaned children in Maun. The group is one of the ma-jor financial sponsors of BBL.

2.4.3 Lady khama charitable trustThe trust benefitted from financial sponsorship.

2.4.4 sos children’s villagesBi-annual financial sponsorship was provided to SOS Children’s vil-lages.

2.4.5 Vulnerable women in chobe districtThe project’s aim is to provide an opportunity to vulnerable women to operate a salon. The group as-sisted these women by paying rent for their business premises.

2.4.6 women against rapeSecurity is paramount for the wom-en and children who take refuge at the shelter. The group contributed to security upgrades at the shelter.

2.5 conservation

The group participates in the rhino relo-cation program through the provision of funds for darting and monitoring rhino movements in the Makgadikgadi Pans National Park.

A donation towards auction prizes at the annual Kalahari Conservation Society dinner dance was made.

The UNDP Sustainable Land Manage-ment Program in partnership with the University of Botswana created the Peter Smith University of Botswana (PSUB) Herbarium Project. This project aims to create a digital database to provide easy access to facts that will allow further in-vestigation of the botanical history of Northern Botswana. The group provided financial support to the project.

CORPORATE SOCIAL RESPOnSIBILITY STATEMEnT [COnTInUEd]

The Board of Directors has pleasure in submitting its report to the shareholders together with the au-dited financial statements for the year ended 28 Feb-ruary 2017.

nature of Business

The Group’s principal business is the ownership and operation of photographic safari operations and as-sociated support businesses.

directors’ responsibility for the financial statements and annual report

In preparing the accompanying financial state-ments, International Financial Reporting Stan-dards have been used and applied consistently, and reasonable and prudent judgements and estimates have been made. The Board approves any changes in accounting policies and the effects thereof are

fully explained in the annual financial statements. The financial statements incorporate full and re-sponsible disclosure in line with the stated account-ing philosophy of the Group.

The directors have reviewed the group’s budget and cash flow forecast for the year to 28 February 2018. On the basis of this review, and in light of the cur-rent financial position, the directors are satisfied that Chobe Holdings Limited is a going concern and have continued to adopt the going concern basis in preparing the financial statements. The group’s ex-ternal auditors, PricewaterhouseCoopers, have au-dited the financial statements and their report ap-pears on page 13 to 17.

The board recognises and acknowledges its respon-sibility for the Group’s systems of internal financial control as reflected in the Corporate Governance statement on pages 10 to 11.

DIRECTORS' REPORT

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

8

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

9

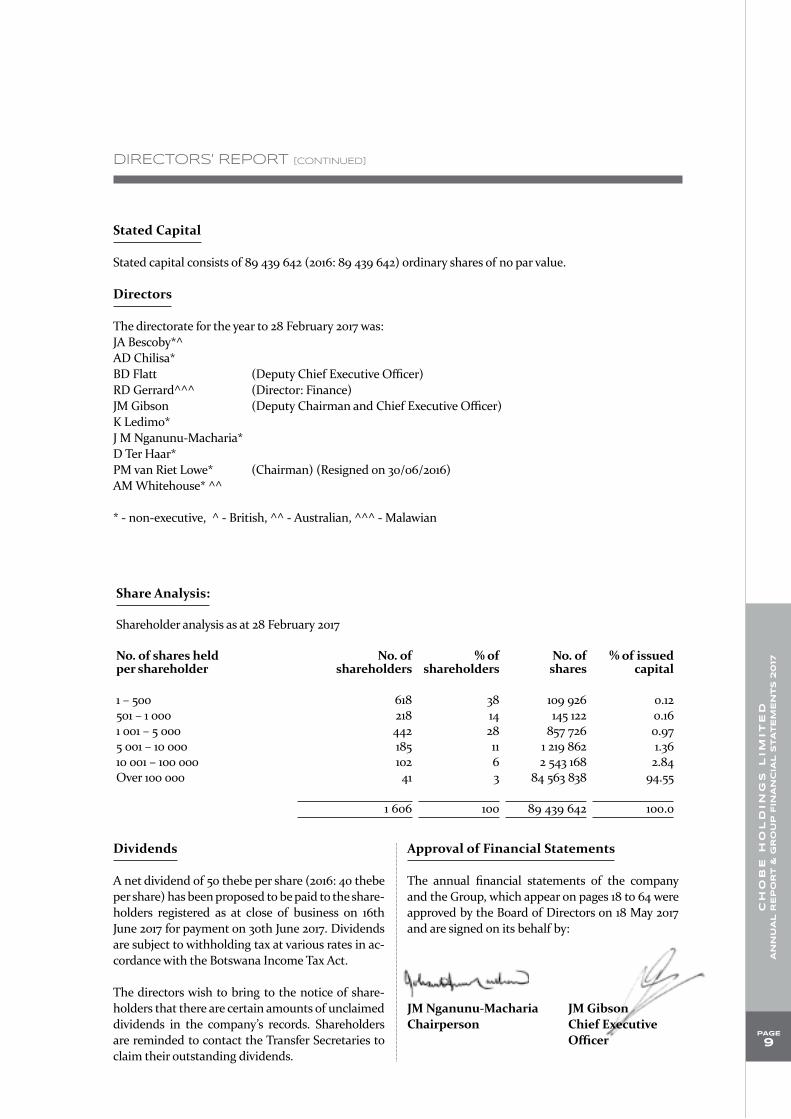

share analysis:

Shareholder analysis as at 28 February 2017

no. of shares heldper shareholder

no. of shareholders

% ofshareholders

no. ofshares

% of issuedcapital

1 – 500 618 38 109 926 0.12501 – 1 000 218 14 145 122 0.161 001 – 5 000 442 28 857 726 0.975 001 – 10 000 185 11 1 219 862 1.3610 001 – 100 000 102 6 2 543 168 2.84Over 100 000 41 3 84 563 838 94.55

1 606 100 89 439 642 100.0

dividends

A net dividend of 50 thebe per share (2016: 40 thebe per share) has been proposed to be paid to the share-holders registered as at close of business on 16th June 2017 for payment on 30th June 2017. Dividends are subject to withholding tax at various rates in ac-cordance with the Botswana Income Tax Act.

The directors wish to bring to the notice of share-holders that there are certain amounts of unclaimed dividends in the company’s records. Shareholders are reminded to contact the Transfer Secretaries to claim their outstanding dividends.

approval of financial statements

The annual financial statements of the company and the Group, which appear on pages 18 to 64 were approved by the Board of Directors on 18 May 2017 and are signed on its behalf by:

Jm nganunu-macharia Jm gibsonChairperson Chief Executive Officer

dIRECTORS' REPORT [COnTInUEd]

stated capital

Stated capital consists of 89 439 642 (2016: 89 439 642) ordinary shares of no par value.

directors

The directorate for the year to 28 February 2017 was:JA Bescoby*^AD Chilisa* BD Flatt (Deputy Chief Executive Officer)RD Gerrard^^^ (Director: Finance)JM Gibson (Deputy Chairman and Chief Executive Officer)K Ledimo* J M Nganunu-Macharia* D Ter Haar* PM van Riet Lowe* (Chairman) (Resigned on 30/06/2016)AM Whitehouse* ^^

* - non-executive, ^ - British, ^^ - Australian, ^^^ - Malawian

Corporate governance is the process by which com-panies are directed, controlled and risk managed. Directors of the Board are responsible for the gov-ernance of the Group whereas the shareholders’ role is to appoint the directors and the external auditors.

The concept of corporate governance has grown internationally in recent years by the adoption of principles outlined in reports, such as the King III Report in South Africa and the Cadbury Report and Turnbull Report in the United Kingdom. These re-ports have as a common goal the promotion of high-est standards of corporate governance by providing recommendations and principles in line with best practice. Chobe Holdings Limited strives to imple-ment good corporate governance, adopting relevant aspects of the above reports where practical.

the Board of directors

The Board is responsible for overseeing the activities of the Group. The Board recognises the need to con-duct the business of the Group with integrity and in accordance with generally accepted corporate prac-tices and endorses the internationally developing principles of corporate governance. It is responsible for maintaining systems of internal control, which provides reasonable assurance of effective and ef-ficient operations, internal financial control, and compliance with laws and regulations. The Board is responsible for the preparation and integrity of the annual financial statements and related financial information contained in this annual report. The financial statements are prepared in accordance with International Financial Reporting Standards and they incorporate full and responsible disclosure

to ensure that the information contained therein is both relevant and reliable.

The Board comprises executive and non-executive directors. The chairman of the Board is an indepen-dent non-executive director. The role of non-execu-tive directors is to bring independent judgement to board deliberations and decisions. The directors are appointed for specified terms and their re-appoint-ment is not automatic. Directors have extensive business experience enabling them to apply their knowledge to the functions required.

The board meets regularly throughout the year. It has a formal schedule of matters referred to it for decision. The board otherwise delegates specific responsibilities to directors. However, it remains responsible for the overall activities of the group, including the implementation of corporate strategy.

The Board met four times during the year. The re-muneration of the board members, for their services as non-executive directors, was as follows:

2017 p

2016 p

PM van Riet Lowe 39 583 80 000

JA Bescoby 85 000 70 000

AD Chilisa 85 000 70 000

K Ledimo 80 000 65 000

D Ter Haar 80 000 65 000

JM Nganunu-Macharia 80 000 65 000

AM Whitehouse 80 000 65 000

529 583 480 000

CORPORATE GOVERNANCE

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

10

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

11

Remuneration for management services of executive directors is set out in note 25 of the financial state-ments. financial control

The directors ensure that adequate systems of inter-nal financial control are developed so that the Group can give reasonable assurance with regard to:

• the completeness and accuracy of the accounting records;

• the integrity and reliability of the published financial statements;

• the ability of the company and the Group to continue as a going concern;

• the safeguarding of assets.

audit and finance committee

The Board Audit and Finance Committee comprises the Chief Executive Officer, and two non-executive directors. The committee’s major functions are the thorough and detailed review of financial state-ments, internal controls and related audit matters through the independent judgement and contribu-tion of non-executive board members. In addition, the committee safeguards the credibility, transpar-ency and objectivity of external financial reporting.

The committee meets with management, including the company secretary, and the external auditors. The committee reviews the financial statements and shareholders’ reports, monitors the appropriateness of accounting policies and the effectiveness of inter-nal control systems. The committee also considers the findings of the external auditors.

The following directors were members of the Audit and Finance Committee during the year:

* JA Bescoby (Chairman)* D Ter Haar JM Gibson (Chief Executive Officer)

* - non-executive The committee met three times during the year.

financial statements and annual report

The responsibility for the preparation of the finan-cial statements is that of the company’s directors. The financial statements are prepared in accor-dance with generally accepted accounting practices, consistently applied, and in accordance with the requirements of the Botswana Companies Act and International Financial Reporting Standards. Rea-sonable judgement and estimates support the infor-mation contained in the financial statements.

The Board is responsible for the integrity, objectivity and reliability of the annual report. The directors believe that the financial statements fairly represent the financial position of the company and the Group as at the end of the financial year and the result of their operations, changes in equity and cash flow in-formation for the year then ended.

company secretary and professional advice

All directors have unlimited access to the services of the company secretary, who is responsible to the Board for ensuring proper procedures are followed.

All directors are entitled to seek independent pro-fessional advice concerning the affairs of the com-pany and the Group, at the company’s expense.

External Auditors

The external auditors are responsible for the inde-pendent review and the expression of an opinion on the reasonableness of the financial statements based on their audit.

Jm nganunu-macharia Jm gibsonChairperson Chief Executive Officer

CORPORATE GOVERnAnCE [COnTInUEd]

ANNUAL FINANCIAL STATEMENTSFOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

12

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

13

Page 13

PricewaterhouseCoopers, Plot 50371, Fairground Office Park, Gaborone, P O Box 294, Gaborone, Botswana, T: (267) 395 2011, F: (267) 397 3901, www.pwc.com/bw Country Senior Partner: B D Phirie Partners: R Binedell, A S Edirisinghe, L Mahesan, R van Schalkwyk, S K K Wijesena

INDEPENDENT AUDITOR’S REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED

Report on the audit of the consolidated and separate financial statements

Our opinion In our opinion, the consolidated and separate financial statements give a true and fair view of the consolidated and separate financial position of Chobe Holdings Limited (the “Company”) and its subsidiaries (together the “Group”) as at 28 February 2017, and of its consolidated and separate financial performance and its consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards (“IFRS”). What we have audited Chobe Holdings Limited’s consolidated and separate financial statements set out on pages 18 to 64

comprise: ● the consolidated and separate statements of financial position as at 28 February 2017;

● the consolidated and separate statements of comprehensive income for the year then ended;

● the consolidated and separate statements of changes in equity for the year then ended;

● the consolidated and separate statements of cash flows for the year then ended; and

● notes to the financial statements, which include a summary of significant accounting policies.

Basis for opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated and separate financial statements section of our report. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Independence We are independent of the Group in accordance with the Botswana Institute of Chartered Accountants Code of Ethics (the “BICA Code”) and the ethical requirements that are relevant to our audit of financial statements in Botswana. We have fulfilled our other ethical responsibilities in accordance with these requirements and the BICA Code. The BICA Code is consistent with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (Parts A and B).

Our audit approach

Overview

Overall group materiality ● Overall group materiality: P 4,300,000, which represents 5% of the

consolidated profit before tax for the year.

Group audit scope ● Our engagement comprises of the statutory audit of the Company’s

consolidated financial statements for the year ended 28 February 2017. ● Based on our assessment, full scope audits were performed at the Company

and all significant operating subsidiaries of the Company, which could individually or in aggregate have a material impact on the consolidated financial statements.

Key Audit Matters ● Impairment of goodwill

INDEPENDENT AUDITORS REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED

PAGE

14

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

Page 14

As part of designing our audit, we determined materiality and assessed the risks of material misstatement in the consolidated and separate financial statements. In particular, we considered where the directors made subjective judgements; for example, in respect of significant accounting estimates that involved making assumptions and considering future events that are inherently uncertain. As in all of our audits, we also addressed the risk of management override of internal controls, including among other matters, consideration of whether there was evidence of bias that represented a risk of material misstatement due to fraud. Materiality The scope of our audit was influenced by our application of materiality. An audit is designed to obtain reasonable assurance whether the financial statements are free from material misstatement. Misstatements may arise due to fraud or error. They are considered material if individually or in aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the consolidated financial statements. Based on our professional judgement, we determined certain quantitative thresholds for materiality, including the overall group materiality for the consolidated financial statements as a whole as set out in the table below. These, together with qualitative considerations, helped us to determine the scope of our audit and the nature, timing and extent of our audit procedures and to evaluate the effect of misstatements, both individually and in aggregate on the financial statements as a whole.

Overall group materiality

P 4 300 000

How we determined it 5% of profit before tax

Rationale for the materiality benchmark applied

We chose profit before tax as the benchmark because, in our view, it is the benchmark against which the performance of the Group is most commonly measured by users, and is a generally accepted benchmark. We chose 5% which is consistent with quantitative materiality thresholds used for profit-oriented companies in this sector.

How we tailored our group audit scope We tailored the scope of our audit in order to perform sufficient work to enable us to provide an opinion on the consolidated financial statements as a whole, taking into account the structure of the Group, the accounting processes and controls, and the industry in which the Group operates. In doing so, full scope audits were performed at the Company and all significant operating subsidiaries of the Company (that is, all subsidiaries that engage in tourism related activities and the air maintenance operation) which could individually or in aggregate have a material impact on the consolidated financial statements. Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated and separate financial statements of the current period. These matters were addressed in the context of our audit of the consolidated and separate financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. We communicate the key audit matter that relates to the audit of the consolidated financial statements of the current period in the table below. We have determined that there are no key audit matters to communicate in our report with regard to the audit of the separate financial statements of the Company of the current period.

INDEPENDENT AUDITORS REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED (CONTINUED)

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

15

Page 15

Key audit matter How our audit addressed the key audit matter

Impairment of goodwill

The Group carries out an impairment review of goodwill at least annually or whenever there is an impairment indicator in accordance with IFRS.

This was considered a matter of most significance to our audit due to the magnitude of the carrying value of the goodwill balance (P35 million as at 28 February 2017) and because the directors’ assessment of ‘value in use’ of the Group’s Cash Generating Units (“CGUs”) involves significant judgement about the future cash flows of the business and with respect to the discount rates applied to present value those cash flow forecasts.

Goodwill arose when the Group assumed control over specific tourism concessions and as a result of the acquisition of an air maintenance operation in the current year, which resulted in an additional goodwill of P4.7Mn. The Group determined the cash generating units attributable to goodwill to be the relevant concessions and businesses which generate independent separately identifiable cash flows.

The Group determines the recoverable amount of each CGU at the higher of fair value less cost of disposal and value in use of the relevant cash generating unit. In this instance, the recoverable amount was determined based on value in use, by using the discounted cash flow model.

In carrying out its assessment, for the purposes of cash flow forecasts, the Group projects future cash flows based on approved budgets. These budgets are prepared annually and assume a zero growth rate for future cash flows with the expectation of maintaining the occupancy rates (where applicable) as forecast for the initial year.

For concessions identified as CGUs, cash inflows are projected in United States Dollars (“USD”) as this is the primary currency in which the group generates the majority of its revenues. Cash outflows are projected in Botswana Pula (“BWP”). These cash flows are discounted using applicable discount rates and converted at the prevailing spot rate for USD cash flows. For the aircraft maintenance operation, all cash flows are projected in Pula. Based on calculations carried out by the Group, there was headroom between the carrying values of goodwill and the calculated net present values of the CGUs. On this basis, the Group did not recognise any impairment.

The disclosure associated with goodwill impairment assessment is set out in the financial statements in the following notes:

● Critical accounting estimates and judgements, Impairment of goodwill (Page 43)

● Note 9 Goodwill (page 49 )

The recorded goodwill is attributed to five CGUs namely Desert & Delta Safaris (Pty) Ltd, Camp Kanana, Camp Okuti and Camp Shindi (all part of Ker & Downey Botswana (Pty) Ltd) and Northwest Air (Pty) Ltd.

Our work included the following procedures: ● We tested the reliability of budgets and

forecasts by comparing the actual results against the historical budgets and forecasts;

● We tested whether the budgets and forecasts utilised to support the recovery of goodwill were approved by those charged with governance; were consistent with confirmed business plans; and were consistent with our understanding of the economic developments in Botswana as these may impact on the budgets and forecasts; and

● We tested the mathematical accuracy of the impairment assessment

We found that historical results were consistent with the historically budgeted results and that the annual budgets were subject to oversight and were consistent with the Board approved budgets. We also found that the impairment assessment was mathematically accurate.

For the five CGUs we challenged the key inputs and assumptions the Group used in the forecasts of net cash flows as follows:

● Growth rates and occupancy rates (where applicable) were assessed by understanding the basis and comparing these against historical trends and economic forecasts used in preparing these budgets; and

● Discount rates for both USD and BWP cash

flows were compared to our independently determined risk adjusted discount rate.

We found the inputs and assumptions to be in line with our expectations.

We carried out calculations on the impairment assessments to determine the degree by which the key assumptions would need to change in order to trigger an impairment. We discussed the outcomes of these sensitivity analyses with the Group and considered the likelihood of such changes occurring, and accepted that key assumptions used by the Group fell within a reasonable range of likely outcomes.

INDEPENDENT AUDITORS REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED (CONTINUED)

PAGE

16

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

Page 16 Other information

The directors are responsible for the other information. The other information comprises the Chief Executive Officers’ Report, the Directors’ Report, Group Structure and Corporate Governance Report, which we obtained prior to the date of this auditor’s report, and value distribution statement, which is expected to be made available to us after that date. The other information does not include the consolidated and separate financial statements and our auditor’s report thereon.

Our opinion on the consolidated and separate financial statements does not cover the other information and we do not and will not express an audit opinion or any form of assurance conclusion thereon.

In connection with our audit of the consolidated and separate financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the consolidated and separate financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed on the other information that we obtained prior to the date of this auditor’s report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of the directors for the consolidated and separate financial statements

The directors are responsible for the preparation of the consolidated and separate financial statements that give a true and fair view in accordance with International Financial Reporting Standards and for such internal control as the directors determine is necessary to enable the preparation of consolidated and separate financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated and separate financial statements, the directors are responsible for assessing the Group and the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the Group and/or the Company or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities for the audit of the consolidated and separate financial statements

Our objectives are to obtain reasonable assurance about whether the consolidated and separate financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated and separate financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

● Identify and assess the risks of material misstatement of the consolidated and separate financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

● Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s and the Company’s internal control.

● Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the directors.

INDEPENDENT AUDITORS REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED (CONTINUED)

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

PAGE

17

INDEPENDENT AUDITORS REPORT TO THE SHAREHOLDERS OF CHOBE HOLDINGS LIMITED (CONTINUED)

Page 17

● Conclude on the appropriateness of the directors’ use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s and the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated and separate financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group and / or Company to cease to continue as a going concern.

● Evaluate the overall presentation, structure and content of the consolidated and separate financial statements, including the disclosures, and whether the consolidated and separate financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

● Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide the directors with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the directors, we determine those matters that were of most significance in the audit of the consolidated and separate financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Individual practicing member: Rudi Binedell 26 May 2017 Membership no: 20040091 Gaborone

PAGE

18

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

STATEMENTS OF COMPREHENSIVE INCOME

group company

notesnotes

2017 p '000s

2016 p '000s

2017 p '000s

2016 p '000s

Revenue 1 269,986 210,822 - - Other operating income 2,955 17,965 38,677 33,842 Cost of inventories consumed / sold (42,211) (25,583) - - Employee benefit expenses 4 (59,136) (47,073) - - Depreciation and amortisation 8, 10 (23,000) (15,661) - - Release of impairment in associate 1,204 - 1,204 - Other operating expenses 2 (64,292) (65,204) (1,362) (1,207)

Operating profit 85,506 75,266 38,519 32,635

Finance income 3 344 733 499 78 Finance cost 3 (136) (82) (267) (222)

Profit before income tax expense 85,714 75,917 38,751 32,491 Income tax expense 5 (21,658) (19,595) (2,901) (2,538)

profit for the year 64,056 56,322 35,850 29,953

other comprehensive incomeItems that may be subsequently reclassified to profit or lossCurrency translation differences 792 (820) - -

Other comprehensive income for the year 792 (820) - -

total comprehensive income for the year 64,848 55,502 35,850 29,953

profit attributable to:Owners of the parent 63,937 56,187 Non-controlling interest 119 135

64,056 56,322

total comprehensive income attributable to:Owners of the parent 64,729 55,367 Non-controlling interest 119 135

64,848 55,502

Earnings per share attributable to the equity holders of the company during the year.

Basic and diluted earnings per share (thebe)(note 6) 71.62 62.97

PAGE

19

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

STATEMENTS OF FINANCIAL POSITION

group company

notes2017

p '000s 2016

p '000s 2017

p '000s2016

p '000s

assetsnon-current assetsProperty, plant and equipment 8 148,590 130,120 - - Goodwill 9 35,085 30,336 - - Intangible assets 10 51,224 51,985 - - Investment in associate 11 - - - - Investments in subsidiaries 12 - - 111,999 111,982 Deferred income tax assets 17 3,834 2,519 - -

238,733 214,960 111,999 111,982

current assetsInventories 13 9,867 3,997 - - Trade and other receivables 14 9,955 8,610 18 77 Current income tax receivable 4,388 2,539 186 138 Cash and cash equivalents 15 91,283 83,299 565 118

115,493 98,445 769 333

total assets 354,226 313,405 112,768 112,315

eQuIty Stated capital 16 102,899 102,899 102,899 102,899 Foreign currency translation reserve (730) (1,522) - - Retained earnings 165,236 137,075 8,252 8,178

267,405 238,452 111,151 111,077 Non-controlling interest 677 558 - -

total equity 268,082 239,010 111,151 111,077

LIaBILItIesnon-current liabilitiesDeferred income tax liabilities 17 23,161 22,187 - - Deferred lease obligations 22 8,678 6,613 - -

31,839 28,800 - -

current liabilitiesBorrowings 18 259 259 - - Current income tax payable 619 2,483 - - Advance travel receipts 19 22,831 18,278 - -

Trade and other payables 20 30,596 24,575 1,617 1,238

54,305 45,595 1,617 1,238

Total liabilities 86,144 74,395 1,617 1,238

total equity and liabilities 354,226 313,405 112,768 112,315

PAGE

20

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

STATEMENTS OF CHANGES IN EQUITY

attributable to equityholders of the company

non controlling

interest total group

stated capital p '000s

retained earnings

p '000s

foreign currency

translation reserve p '000s p '000s p '000s

year ended 29 february 2016Balance at 1 March 2015 102,899 112,192 (702) 423 214,812

Profit for the year - 56,187 - 135 56,322

other comprehensive income

Currency translation differences - - (820) - (820)

transactions with owners

Dividends paid - (31,304) - - (31,304)

Balance at 29 february 2016 102,899 137,075 (1,522) 558 239,010

year ended 28 february 2017Balance at 1 March 2016 102,899 137,075 (1,522) 558 239,010

Profit for the year - 63,937 - 119 64,056

other comprehensive income

Currency translation differences - - 792 - 792

transactions with ownersDividends paid - (35,776) - - (35,776)

Balance at 28 february 2017 102,899 165,236 (730) 677 268,082

PAGE

21

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

STATEMENTS OF CHANGES IN EQUITY (CONTINUED)

company stated capital p '000s

retained earnings

p '000s total

p '000s

year ended 29 february 2016Balance at 1 March 2015 102,899 9,529 112,428

Profit for the year - 29,953 29,953

transactions with owners

Dividends paid - (31,304) (31,304)

Balance at 29 february 2016 102,899 8,178 111,077

year ended 28 february 2017Balance at 1 March 2016 102,899 8,178 111,077

Profit for the year - 35,850 35,850

transactions with owners

Dividends paid - (35,776) (35,776)

Balance at 28 february 2017 102,899 8,252 111,151

PAGE

22

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

STATEMENTS OF CASH FLOW

group company 2017

p '000s 2016

p '000s 2017

p '000s 2016

p '000s

operating activities:Cash generated from operations (note 21) 117,288 95,388 34,852 29,888 Interest paid (note 3) (136) (82) (267) (222)Income tax (paid)/refund received (26,431) (17,662) (48) 89 Cash generated from operating activities 90,721 77,644 34,537 29,755

Investing activities:Purchase of property, plant and equipment (“PPE”) (note 8) (30,880) (41,498) - - Acquisition of air maintenance operation (note 24) (18,418) - - - Proceeds from disposal of associate investment 1,204 - 1,204 - Proceeds on sale of PPE 789 2,868 - - Decrease/(increase) in loans to subsidiaries - - (17) 1,240 Interest received (note 3) 344 733 499 78 Net cash (used in)/generated from investing activities (46,961) (37,897) 1,686 1,318

financing activities:Repayment of borrowings - (88) - - Dividends paid (35,776) (31,304) (35,776) (31,304)Net cash used in financing activities (35,776) (31,392) (35,776) (31,304)

Net increase/ (decrease) in cash and cashequivalents 7,984 8,355 447 (231)

movement in cash and cash equivalents At beginning of year 83,299 74,944 118 349 Increase/ (decrease) in the year 7,984 8,355 447 (231)At end of year 91,283 83,299 565 118

represented by:Cash and cash equivalents (note 15) 91,283 83,299 565 118

PAGE

23

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies applied in the prepara-tion of these group and company financial statements are set out below. These policies have been consistently ap-plied to all the years presented, unless otherwise stated.

The group consolidated financial statements were autho-rised for issue by the Board of Directors.

1. Basis of preparation

The financial statements have been prepared in ac-cordance with International Financial Reporting Standards (“IFRS”). The financial statements have been prepared under the historical cost convention. Amounts are rounded to the nearest thousands.

The preparation of financial statements in conform-ity with IFRS requires the use of certain critical ac-counting estimates. It also requires management to exercise its judgement in the process of applying the group’s accounting policies. The areas involving a higher degree of judgement or complexity, or ar-eas where assumptions and estimates are significant to the group financial statements are disclosed in a separate section of the financial statements.

The entity’s owners do not have the power to amend the financial statements after issue.

a) International financial reporting standards and amendments issued but not effective for 28 February 2017 year-end:

Amendment to IAS 7 – Cash flow statements (Effective date 1 January 2017)

In January 2016, the International Accounting Standards Board (IASB) issued an amendment to IAS 7 introducing an additional disclosure that will enable users of financial statements to evaluate changes in liabilities arising from fi-nancing activities.

The amendment responds to requests from investors for information that helps them bet-ter understand changes in an entity’s debt. The amendment will affect every entity preparing IFRS financial statements. However, the infor-mation required should be readily available. Preparers should consider how best to present the additional information to explain the chang-

es in liabilities arising from financing activities. The amendment is not expected to significantly impact the group.

IFRS 15 – Revenue from contracts with customers. (Effective date 1 January 2018)

The FASB and IASB issued their long awaited converged standard on revenue recognition on 29 May 2014. It is a single, comprehensive rev-enue recognition model for all contracts with customers to achieve greater consistency in the recognition and presentation of revenue. Rev-enue is recognised based on the satisfaction of performance obligations, which occurs when control of good or service transfers to a cus-tomer.

The group is yet to completely assess the impact of the standard. However, preliminary indica-tions are that the standard will not significantly impact the group’s current recognition and measurement policy.

IFRS 9 – Financial Instruments (2009 &2010)• Financial liabilities• Derecognition of financial instruments• Financial assets• General hedge accounting

This IFRS is part of the IASB’s project to replace IAS 39. IFRS 9 addresses classification and measurement of financial assets and replaces the multiple classification and measurement models in IAS 39 with a single model that has only two classification categories: amortised cost and fair value. The standard is not expected to significantly impact the group annual finan-cial statements but the group is yet to assess the impact to stand alone subsidiary financial state-ments.

IFRS 16 – Leases. (Effective date 1 January 2019)

After ten years of joint drafting by the IASB and FASB they decided that lessees should be re-quired to recognise assets and liabilities arising from all leases (with limited exceptions) on the balance sheet. Lessor accounting has not sub-stantially changed in the new standard.

PAGE

24

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

The model reflects that, at the start of a lease, the lessee obtains the right to use an asset for a period of time and has an obligation to pay for that right. In response to concerns expressed about the cost and complexity to apply the re-quirements to large volumes of small assets, the IASB decided not to require a lessee to recog-nise assets and liabilities for short-term leases (less than 12 months), and leases for which the underlying asset is of low value (such as laptops and office furniture).

A lessee measures lease liabilities at the present value of future lease payments. A lessee meas-ures lease assets, initially at the same amount as lease liabilities, and also includes costs directly related to entering into the lease. Lease assets are amortised in a similar way to other assets such as property, plant and equipment. This ap-proach will result in a more faithful represen-tation of a lessee’s assets and liabilities and, to-gether with enhanced disclosures, will provide greater transparency of a lessee’s financial lever-age and capital employed.

One of the implications of the new standard is that there will be a change to key financial ratios derived from a lessee’s assets and liabilities (for example, leverage and performance ratios).

IFRS 16 – Leases. (Effective date 1 January 2019) (continued)

IFRS 16 supersedes IAS 17, ‘Leases’, IFRIC 4, ‘De-termining whether an Arrangement contains a Lease’, SIC 15, ‘Operating Leases – Incentives’

and SIC 27, ‘Evaluating the Substance of Trans-actions Involving the Legal Form of a Lease’. The group is yet to assess the impact of the standard to its financial position and performance.

Amendment to IAS 12 – Income taxes (Effective date 1 January 2017)

The amendments were issued to clarify the re-quirements for recognising deferred tax assets on unrealised losses. The amendments clarify the accounting for deferred tax where an asset is measured at fair value and that fair value is below the asset’s tax base. They also clarify cer-tain other aspects of accounting for deferred tax assets. The amendment is not expected to sig-nificantly impact the group.

IFRIC 22 - Foreign currency transactions and advance consideration - (Effective date 1 January 2018)

This IFRIC addresses foreign currency trans-actions or parts of transactions where there is consideration that is denominated or priced in a foreign currency. The interpretation provides guidance for when a single payment/receipt is made as well as for situations where multiple payment/receipts are made. The guidance aims to reduce diversity in practice. The group is yet to assess the impact of the interpretation.

b) early adoption of standards

The group did not early adopt any new or amended standards in the current year.

1. Basis of preparation [continued]

PAGE

25

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

2. consolidation

The group financial statements incorporate the fi-nancial statements of Chobe Holdings Limited and all its subsidiaries and associate for the year ended 28 February 2017.

(a) subsidiaries

Subsidiaries are all entities (including struc-tured entities) over which the group has control. The group controls an entity when the group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully consolidat-ed from the date on which control is transferred to the group and are de-consolidated from the date that control ceases.

The group applies the acquisition method to ac-count for business combinations. The consider-ation transferred for the acquisition of a subsid-iary is the fair value of the assets transferred, the liabilities incurred to the former owners of the acquiree and the equity interests issued by the Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement and fair value of any pre-existing equity interest in the subsidiary.

Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. On an acquisi-tion-by-acquisition basis, the group recognises any non-controlling interest in the acquiree ei-ther at fair value or at the non-controlling inter-est’s proportionate share of recognised amount of acquiree’s identifiable net assets.

Acquisition-related costs are expensed as in-curred.

Where settlement of any part of cash considera-tion is deferred, the amounts payable in the fu-ture are discounted to their present value as at the date of the exchange. The discount rate used is the entity’s incremental borrowing rate, being the rate at which a similar borrowing could be obtained from an independent financier under comparable terms and conditions.

Contingent consideration is classified either as equity or a financial liability. Amounts classi-fied as a financial liability are subsequently re-measured to fair value with changes in fair value recognised in profit or loss.

If the business combination is achieved in stag-es, the acquisition date carrying value of the acquirer’s previously held equity interest in the acquiree is re-measured to fair value at the ac-quisition date; any gains or losses arising from such re-measurement are recognised in profit or loss.

Inter-company transactions, balances and un-realised gains on transactions between group companies are eliminated. Unrealised losses are also eliminated. When necessary, amounts reported by subsidiaries have been adjusted to conform with the group’s accounting policies.

(b) changes in ownership interests in subsidiaries without change of control

Transactions with non-controlling interests that do not result in loss of control are accounted for as equity transactions – that is, as transactions with the owners in their capacity as owners. The difference between fair value of any considera-tion paid and the relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity. Gains or losses on disposals to non-controlling interests are also recorded in equity.

PAGE

26

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(c) disposal of subsidiaries

When the group ceases to have control any re-tained interest in the entity is re-measured to its fair value at the date when control is lost, with the change in carrying amount recognised in profit or loss. The fair value is the initial car-rying amount for the purposes of subsequently accounting for the retained interest as an as-sociate, joint venture or financial asset. In ad-dition, any amounts previously recognised in other comprehensive income in respect of that entity are accounted for as if the group had di-rectly disposed of the related assets or liabili-ties. This may mean that amountspreviously recognised in other comprehensive income are reclassified to profit or loss.

(d) associates

Associates are all entities over which the group has significant influence but not control, gener-ally accompanying a shareholding of between 20% and 50% of the voting rights. Investments in associates are accounted for using the equity method of accounting.

Under the equity method, the investment is initially recognised at cost, and the carrying amount is increased or decreased to recognise the investor’s share of the profit or loss of the in-vestee after the date of acquisition. The group’s investment in associates includes goodwill identified on acquisition.

If the ownership interest in an associate is re-duced but significant influence is retained, only a proportionate share of the amounts previous-ly recognised in other comprehensive income is reclassified to profit or loss where appropriate.

The group’s share of post-acquisition profit or loss is recognised in the income statement, and its share of post-acquisition movements in oth-er comprehensive income is recognised in other comprehensive income with a corresponding adjustment to the carrying amount of the in-vestment. When the group’s share of losses in an associate equals or exceeds its interest in the associate, including any other unsecured re-ceivables, the group does not recognise further losses, unless it has incurred legal or construc-tive obligations or made payments on behalf of the associate.

The group determines at each reporting date whether there is any objective evidence that the investment in the associate is impaired. If this is the case, the group calculates the amount of impairment as the difference between the re-coverable amount of the associate and its carry-ing value and recognises the amount to ‘share of profit/(loss) of associates in the income state-ment.

Profits and losses resulting from upstream and downstream transactions between the group and its associate are recognised in the group’s financial statements only to the extent of unre-lated investor’s interests in the associates. Un-realised losses are eliminated unless the trans-action provides evidence of an impairment of the asset transferred. Accounting policies of associates have been changed where necessary to ensure consistency with the policies adopted by the group.

When the group ceases to equity account for an investment because of loss of significant influ-ence, any retained interest in the entity is meas-ured to its fair value with the change in carrying amount recognised in profit or loss. This fair

2. consolidation [continued]

PAGE

27

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

value becomes the initial carrying amount for the purposes of subsequently accounting for the retained interest as an associate or financial as-set. In addition, any amounts previously recog-nised in other comprehensive income in respect of that entity are accounted for as if the group had directly disposed of the related assets or lia-bilities. This may mean that amounts previously recognised in other comprehensive income are reclassified to profit or loss.

If the ownership interest in an associate is re-duced but significant influence is retained only a proportionate share of the amount’s previously recognised in other comprehensive income are reclassified to profit or loss where appropriate.

The group’s shareholding in Lianshulu Lodge (Proprietary) Limited was disposed in the cur-rent year.

(e) Investment in subsidiaries

The company accounts for investments in sub-sidiaries at cost, which includes transaction costs, less accumulated impairment losses.

Investments in subsidiaries are assessed for impairment when indicators of impairment are identified. Such impairment indicators in-clude, but are not limited to, for example:

• Sustained deterioration in financial results of operations and / or financial position of a subsidiary;

• Changes in the operating environment of a subsidiary, including regulatory and eco-nomic changes, market entry by new com-petitors and

• Inability of a subsidiary to obtain finance required to sustain or expand operations.

Where impairment indicators are identified, the recoverable value of the subsidiary is meas-ured at the lower of realisable value through sale less costs to sell, and value in use. Value in use is the present value of future cash flows expected to be derived from the subsidiary.Where the recoverable value of a subsidiary is below the carrying amount, the carrying amount is reduced to the recoverable value through an impairment loss charged to the statement of comprehensive income.

Once an impairment loss has been recognised, the company assesses at each year-end date whether there is an indication that the impair-ment loss previously recognised no longer exists or has decreased. If this is the case, the recover-able value of the subsidiary is remeasured and the impairment loss reversed or partially re-versed as may be the case.

The group’s financial statements include the fi-nancial statements of Chobe Holdings Limited and its following subsidiaries, whose financial year ends are all 28 February:

Caprivi Fly Fishing Safaris (Pty) Ltd - 100% Chobe Farms (Pty) Ltd - 662/3% Chobe Game Lodge (Pty) Ltd - 100% Chobe Properties (Pty) Ltd - 100% Desert and Delta Safaris (Pty) Ltd - 100% Desert and Delta Safaris (SA) (Pty) Ltd - 100% Ker and Downey Botswana (Pty) Ltd - 100% L. L. Tau (Pty) Ltd - 100%Lloyds Camp (Pty) Ltd - 100%The Bookings Company (Pty) Ltd - 100% Venstell (Pty) Ltd - 100% Moremi Safaris (Pty) Ltd - 100%Kanana Ventures (Pty) Ltd - 100%Okuti Safaris (Pty) Ltd - 100%North West Air (Pty) Ltd - 100%

2. consolidation [continued]

PAGE

28

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3. foreign currency translation

functional and presentation currency

Items included in the financial statements of each of the group’s entities are measured using the currency of the primary economic environment in which the entity operates (‘the functional currency’). The consolidated financial statements are presented in Botswana Pula, which is the Chobe Holding Limited’s functional and presentation currency.

transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settle-ment of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are rec-ognised in the statement of comprehensive income.

Foreign exchange gains and losses that relate to bor-rowings and cash and cash equivalents are presented in the income statement within ‘finance income or costs’. All other foreign exchange gains and losses are presented in the income statement within ‘Other operating income’.

group companies

The results and financial position of all the group en-tities (none of which has the currency of a hyperin-flationary economy) that have a functional currency different from the presentation currency are trans-lated into the presentation currency as follows:

(i) assets and liabilities for each statement of financial position presented are translated at the closing rate at the reporting date;

(ii) income and expenses for each statement of comprehensive income are translated at average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the dates of the transactions); and

(iii) all resulting exchange differences are rec-ognised in other comprehensive income.

On consolidation, exchange differences arising from the translation of the net investment in foreign oper-ations, and of borrowings and other currency instru-ments designated as hedges of such investments, are taken to other comprehensive income. When a foreign operation is sold, exchange differences that were recorded in other comprehensive income are recognised in the statement of comprehensive in-come as part of the gain or loss on sale.

Goodwill and fair value adjustments arising on the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at the closing rate. Exchange differences arising are rec-ognised in other comprehensive income.

PAGE

29

FOR THE YEAR ENDED 28 FEBRUARY 2017

CH

OB

E H

OL

DIN

GS

LIM

ITE

DA

NN

UA

L R

EP

OR

T &

GR

OU

P F

INA

NC

IAL

STA

TE

ME

NT

S 2

017

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

4. property, plant and equipment

Property, plant and equipment is stated at historical cost less depreciation. Historical cost includes ex-penditure that is directly attributable to the acquisi-tion of the items.

Subsequent costs are included in the asset’s carry-ing amount or recognised as a separate asset, as ap-propriate, only when it is probable that future eco-nomic benefits associated with the item will flow to the group and the cost of the item can be measured reliably. The carrying amount of the replaced part is derecognised.

Depreciation is recorded by a charge to statement of comprehensive income and computed on a straight line basis to allocate their cost to their residual values over their estimated useful lives, as follows:

Aircraft 6.7% Aircraft engine and propellers number of

hours flownLeasehold improvements over the period

of the leaseFurniture and fittings 10% - 15% Machinery and equipment 15% - 25% Motor vehicles and motor boats 12.5% - 25%

The assets’ residual values and useful lives are re-viewed, and adjusted if appropriate, at each report-ing date.

Where the carrying amount of an asset is greater than its estimated recoverable amount, it is written down immediately to its recoverable amount.

The group adopts a policy of expensing individual assets with a value less than P 20 000.

Gains and losses on disposal of property, plant and equipment are determined by comparing the pro-ceeds with the carrying amount and are taken into account in determining operating profit.

Repairs and maintenance are charged to the state-ment of comprehensive income during the financial period in which they are incurred. The cost of major renovations is included in the carrying amount of the asset when it is probable that future economic benefits in excess of the originally assessed standard of performance of the existing asset will flow to the group. Major renovations are depreciated over the remaining useful life of the related asset.

5. goodwill