23.07.2012 quantifying the costs of regulatory inefficiency, olin mcgill

TRANSCRIPT

Quantifying the Costs

of Regulatory Inefficiency

July, 2012

Ulaanbaatar, Mongolia

Olin McGill

Business Environment Reform Advisor

Working Documents On Competitiveness And Business Enabling Environment -- Mongolia

Methodology Seminar:

“How much in value

will this project

actually deliver?”

-- Kakha Bendookidze,

State Minister on

Reforms Coordination

The $100 Million Question:

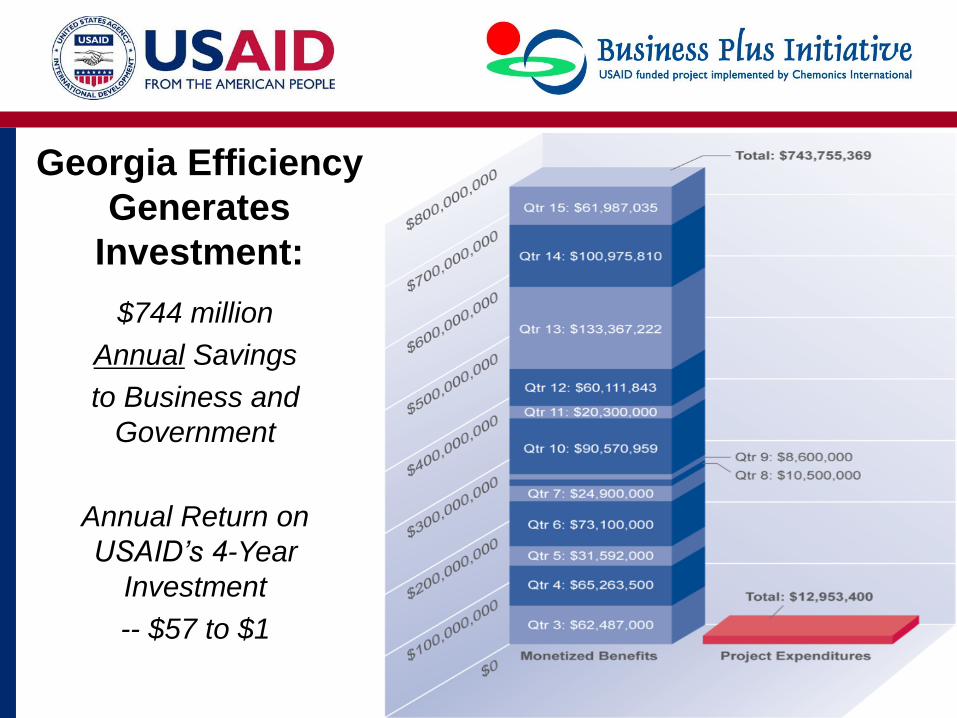

Georgia’s Unprecedented Rise on Doing Business

$744 million

Annual Savings

to Business and

Government

Annual Return on

USAID’s 4-Year

Investment

-- $57 to $1

Georgia Efficiency

Generates

Investment:

• Based on methodology by The Netherlands to quantify

administrative burdens on business.

• Monetizing Benefits v. Quantifying Costs

• Benefits /Costs to business = Costs X Quantity

Costs = financial (fees, bribes(?), etc.) + compliance

Quantity = number of businesses X frequency of

obligations/year

• Benefits/Costs to government = Administrative Savings

Savings = hourly rate of government employees X hours saved

Other = rental space, storage space, retrieval time, etc.

Methodology of calculations

GDT’s Hidden Costs of Storing Paper

Methodology Strengths and Weaknesses

• Strengths:

– Disaggregates impact of USAID assistance on a specific

reform

– Useful order of magnitude estimate of impacts

– Helps generate political will

– Good for prioritizing

• Weaknesses:

– Too time-consuming to capture all impacts

– Relies on inaccurate, incomplete government statistics

– Some things are difficult to measure – electricity privatization

– Apples + Oranges = Fruit (Savings, transfers, fees)

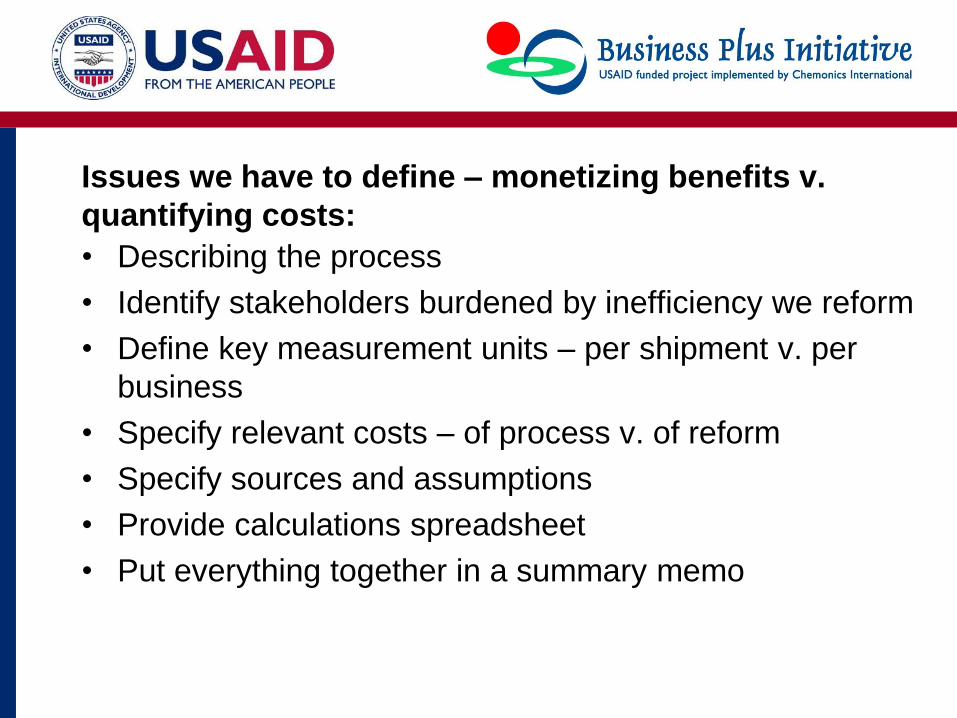

Issues we have to define – monetizing benefits v.

quantifying costs:

• Describing the process

• Identify stakeholders burdened by inefficiency we reform

• Define key measurement units – per shipment v. per

business

• Specify relevant costs – of process v. of reform

• Specify sources and assumptions

• Provide calculations spreadsheet

• Put everything together in a summary memo

Prioritizing Doing Business Reforms

Starting a business

All procedures to open a business

Total days to complete all procedures

Official fees as % of per capita income

Paid-in capital as % of per capita income

Protecting investors

Legal protections provided to minority shareholders

against related-party transactions by company

owners/managers

Dealing with construction permits

All procedures to complete standard building

Total days to complete all procedures

Official fees as % of per capita income

Paying taxes

Total number of payments/reports a year

Total time required to make payments and reports

Total tax rate as % of profits

Getting electricity

All procedures to connect a standard building

Total days to complete all procedures

Official fees as % of per capita income

Trading across borders

All procedures to import and export

Total days to complete all procedures

Official fees for all procedures

Registering property

All procedures to transfer property

Total days to complete all procedures

Official fees as % of property value

Enforcing contracts

All procedures from filing to enforcement

Total days to complete all procedures

Total costs of lawyers, court, enforcement

Getting credit

Effectiveness of legal regime for secured lending

and protecting borrowers and lenders

Availability of credit information

Resolving insolvency

The time and cost required to resolve bankruptcy

Where Georgia started:

3-day line to cross border

Lower transit costs increased Georgia’s trade

Process 2006

# Trucks

Days

Saved Cost per Day Savings

Import 42,000 1 $288 $ 12.096 million

Export 17,000 1 $288 $ 4.896 million

Transit 40,000 2 $288 $ 23.040 million

Annual Benefit

2006 $ 39.992 million

2008 +$133.367 million

Increased Trade Volume 2006-08 333 percent growth

Number of Days to Export

54

13

0

10

20

30

40

50

60

2005 Year 2006 Year

Number of days to import

52

15

0

10

20

30

40

50

60

2005 Year 2006 Year

Georgia Traders’ Reduced time to clear goods …

… Increases velocity of capital:

365 / 52 = 7 turns a year

365 / 15 = 24 turns a year

Georgia Customs Streamlining – Opportunity Costs

• 15% = average annual opportunity cost

• 0.04% = average daily opportunity cost

• Import: 37 days (52-15) X 0.04% X $2.491 billion

= $36.8 million

• Export: 41 days (54-13) X 0.04% X $866.7 million

= $14.2 million

Totals: $51 million opportunity costs

+$40 million trucking savings

=$91 million total savings

Increase in imports/exports

Exports increased by 21.6 % Imports increased by 56.8 %

$524 Million

$638 Million

$0

$100

$200

$300

$400

$500

$600

$700

In USD

Millions

Export in

January-August 2005

Export in

January-August 2006

Total Exports

$1.4

Billion

$2.25

5 Billion

$0

$500

$1,000

$1,500

$2,000

$2,500

Import in

January-August 2005

Import in

January-August 2006

Total ImportsIn USD

Millions

Now only 15 minutes at border

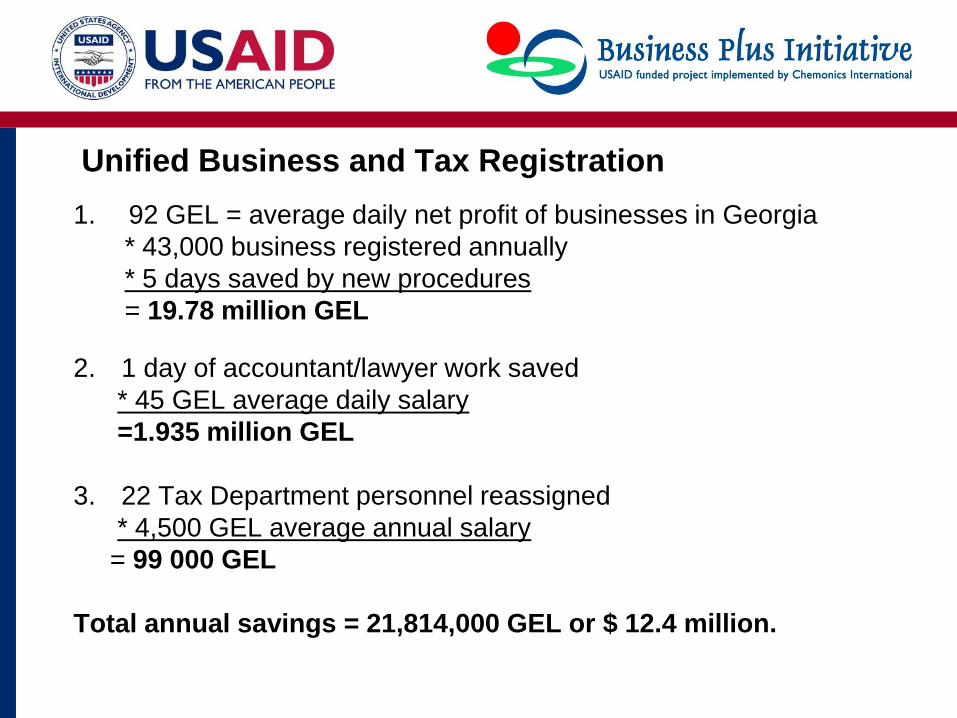

Unified Business and Tax Registration

1. 92 GEL = average daily net profit of businesses in Georgia

* 43,000 business registered annually

* 5 days saved by new procedures

= 19.78 million GEL

2. 1 day of accountant/lawyer work saved

* 45 GEL average daily salary

=1.935 million GEL

3. 22 Tax Department personnel reassigned

* 4,500 GEL average annual salary

= 99 000 GEL

Total annual savings = 21,814,000 GEL or $ 12.4 million.

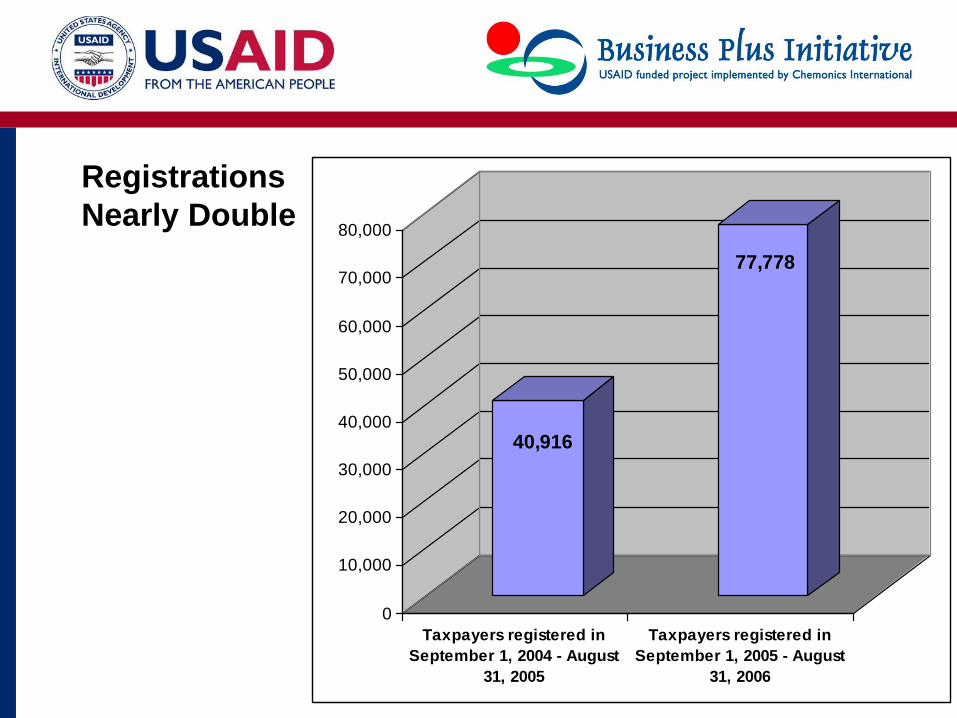

Registrations

Nearly Double

40,916

77,778

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Taxpayers registered in

September 1, 2004 - August

31, 2005

Taxpayers registered in

September 1, 2005 - August

31, 2006

Simplified Registration of Individual Taxpayers

1. 11 GEL = average daily salary

* 78,000 annual individual registrations

* 1 day saved by new procedures

= 858,000 GEL

2. 5 GEL notary fee eliminated

* 78,000 annual individual registrations

= 390,000 GEL

3. 0.50 needed to serve each applicant

* 78,000 annual applications

* 18 GEL average Tax Department employee salary

= 88,000 GEL

Total annual savings = 1.336 million GEL or $763,500 USD.

Registrations

Increase 4X

7,114

28,077

0

5000

10000

15000

20000

25000

30000

Natural Persons registered in April, May, June (25 days) of 2006

Natural Persons registered in July, August, September (25 days) of 2006

Exhibit 14: Reductions in Payments, Time, and Costs Allocated by Reform

Reform Agency Tax Comment Payments Time Costs (billion

MNT)

Totals by Reform

Payments Time Costs

E-

Signature

GDT

VAT Eliminates filing 12

paper reports -12 -34.5 -1,8

-32 -102.6 -15,3

Corporate Income

Tax

Eliminates filing 12

paper reports -4 -22.0 -4,6

MOF Quarterly Financial

Reporting

Eliminates filing 4

paper reports -4 -24.2 -5,3

SID Social Insurance Eliminates filing 12

paper reports -12 -21.9 -3,6

Exhibit 14: Reductions in Payments, Time, and Costs Allocated by Reform

Reform Agency Tax Comment Payments Time Costs (billion

MNT)

Totals by Reform

Paymen

ts Time Costs

True E-

Filing

GDT

VAT

Reduces Payments count

from 12 to 1; Reduces time

and cost to calculate, prepare,

pay, and submit report.

-11 -86.4 -4,5

-36.0 -275.8 -43,6

Corporate

Income Tax

Reduces Payments count

from 12 to 1; Reduces time

and cost to calculate, prepare,

pay, and submit e-report.

-11 -21.0 -4,4

MOF

Quarterly

Financial

Reporting

Reduces Payments count

from 4 to 1; Reduces time

and cost to calculate, prepare,

pay, and submit e-report.

-3 -129.5 -28,3

SID Social Insurance

Reduces Payments count

from 4 to 1; Reduces time

and cost to calculate, prepare,

pay, and submit e-report.

-11 -38.9 -6,4

Exhibit 14: Reductions in Payments, Time, and Costs Allocated by Reform

Reform Agency Tax Comment Payments Time

Costs

(billion

MNT)

Totals by Reform

Payments Time Costs

Combine

Employee

Withholding

and Social

Insurance

GDT &

SID

Social Insurance +

Employee

Withholding

Combining social

insurance and employee

withholding eliminate

all burdens with one tax.

Calculations Employee

withholding eliminated

because times involved

are greater.

-24 -78.4 -13 -24 -78.4 -13

Make Vehicle

Tax Annual GDT Vehicle Tax

Switch from quarterly to

annual eliminates 3

payments -3 N/A N/A -3 N/A N/A

TOTALS BEFORE REFORM 101 592.8 93,5

SAVINGS FROM REFORMS -95 -456.8 -71,9

TOTALS AFTER REFORMS 6 136.0 21,5

Reforming Mongolia’s High Cost of Paying Taxes

Tax or Mandatory

Contribution

Payments Total Hours per Firm Total Annual Cost for All

Firms (Billion MNT)

Before

Reform

After

Reform

Before

Reform

After

Reform

Before

Reform

After

Reform

Annual

Savings

Employer paid- Social

insurance contributions 24 1 80.4 19.6 13.2 3.2 10

Value added tax (VAT) 24 1 163.1 42.2 8.5 2.2 6.3

Quarterly Financial

Reports to MOF 8 1 215.8 62.1 47.3 13.6 33.7

Corporate income tax 16 1 55.1 12.1 11.5 2.5 9.0

Employee Withholding** 24 0 78.4 0.0 13.0 0 13.0

Property Tax 1 1 N/A N/A N/A N/A N/A

Vehicle Tax 4 1 N/A N/A N/A N/A N/A

BPI Totals 101 6 592.8 136.0 93.5 21.5 72

GDT Calculates savings for CIT e-filers

• 5 hours to file paper returns (to and from office)

• X 3,405 MNT average hourly wage of an accountant MNT

(monthly 600,000 MNT) = 17,025 MNT ($13)

• + 6 km average round trip to tax office X 700 MNT taxi per km

= 4,200 MNT

• + 8 MNT per return X 8 pages each return = 64 MNT

• = 21,289 MNT ($16.25) per return

• X 4 time per year = 85,156 MNT ($65) per taxpayer per year

• X 55,331 CIT electronic filers per year

• = 4.7 billion MNT ($3.6 million) per year savings

Test Case: Paper work Cripples Mongolia Meat Exporters:

Agency Purpose Required Documents

Mongolian Taxation Agency To certify meat exporter doesn’t owe taxes - Copy of State Registration Certificate

MNCCI Certificate of Origin

- Copy of State Registration Certificate

- Copy of Sales Contract

- Invoice

- Packing list

GASI and the Central

Laboratory test results

- Copy of Certificate of Origin

- Copy of State Registration Certificate

- Copy of Sales Contract

- Application form

GASI Conformity Certificate

- Copy of State Registration Certificate

- Certification of Origin

- Test Results

- Invoice

- Application form

NARTAM & Railway Admin. CMR transport documentation - Copy of Sales Contract

- Copy of State Registration Certificate

MCGA customs clearance

- Sale of Goods Contract

- Copy of State Registration Certificate

- Conformity Certificate

- CMR

- Certification of Origin

- Taxation Certificate

- Export Certificate