3q15 analysts’ briefing -...

TRANSCRIPT

3Q15 Analysts’ Briefing

26 November 2015 ICON OFFSHORE BERHAD

Level 12A, East Wing, The Icon

No. 1, Jalan 1/86F, Off Jalan Tun Razak

55000 Kuala Lumpur, Malaysia

www.iconoffshore.com.my

Disclosure Statement

2

The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell

or the solicitation of an offer or invitation to purchase any securities (“Securities”) of Icon Offshore Berhad (“ICON”) in Malaysia,

the United States or any other jurisdiction. This presentation should not, nor should anything contained in it, form the basis of, or

be relied upon in any connection with any contract or commitment whatsoever. This presentation is confidential and is intended

only for the exclusive use of the recipients thereof and may not be reproduced (in whole or in part), retransmitted, summarized or

distributed by them to any other persons without ICON's prior written permission

This presentation contains forward-looking statements that involve risks and uncertainties. Forward-looking statements are based

on certain assumptions and expectations of future events. The future events referred to in these forward-looking statements

involve known and unknown risks, uncertainties and other factors, many of which are beyond ICON's control, which may cause the

actual results to be materially different from those expressed or implied by the forward-looking statements. These forward-looking

statements are based on numerous assumptions regarding ICON's present and future business strategies and the environment in

which ICON operates and are not a guarantee of future performance. Any reference to past performance should not be taken as an

indication of future performance. ICON makes no representation, warranty or prediction that the results anticipated by such

forward-looking statements will be achieved, and such forward-looking statements represent, in each case, only one of many

possible scenarios and should not be viewed as the most likely or standard scenario. You are cautioned not to place undue

reliance on these forward looking statements, which are based on current view of Icon's management on future events.

This presentation has been prepared by ICON. No representation, warranty, express or implied, is made as to, and no reliance

should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation.

Certain data in this presentation was obtained from various external data sources, and ICON has not verified such data with

independent sources. None of ICON or any of its directors, officers, employees, agents or advisers, or any of their respective

affiliates, advisers or representatives, undertake to update, revise or re-affirm the presentation including any forward-looking

statements, whether as a result of new information, future events or otherwise and none of them shall have any liability (in

negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in

connection with this presentation and any liability therefore (including liability for any direct or indirect consequential loss or

damage) is hereby expressly disclaimed and none of them accept any responsibility for any loss or damages howsoever arising,

whether directly or indirectly from any use, reliance or distribution of the presentation, its contents or otherwise arising in

connection with the prospectus.

Icon Offshore at a glance

3

Key Takeaways 33 Vessels - as at 30 Sept 2015

Largest pure-play OSV

provider in Malaysia and one

of the largest in Southeast

Asia in terms of number of

vessels

Diversified and young fleet of

33 vessels with low average

age of 5.5 years for the year

ending 31 December 2015

(FY2015)

Four vessels currently under

construction with targeted

delivery by Q1 2017

Focused on shallow waters

with focus on optimising

utilisation rates, strategic

fleet diversification and fleet

renewal programme

AHT/AHTS 24 vessels

SSV 4 vessels

UV 1 vessel

PSV 2 vessels

AWB 2 vessels

YTD Sept 2015 Revenue

RM201.2 mil

(YTD Sept 2014 Revenue:

RM241.8 mil)

YTD Sept 2015 Average

fleet utilisation

61%

(YTD Sept 2014 Average fleet

utilisation: 79%)

YTD Sept 2015 Adjusted

PAT

RM14.6 mil

(YTD Sept 2014 Adjusted

PAT: RM71.4 mil)

YTD Sept 2015 Adjusted

PAT Margin

7.2%

(YTD Sept 2014 Adjusted PAT

Margin: 29.5%)

3Q15 Highlights

As at 30 September 2015, the Group’s order book stood

at RM714.6 mil

Secure a short-term contract with ExxonMobil Exploration

& Production Malaysia Inc. for the provision of two (2)

AHTSs, namely Icon Zara and Icon Ikhlas

Leveraging on PETRONAS’ initiatives to support MOSVA

members

• According to International Energy Agency, higher oil

output from OPEC and a slowdown in world economic

growth means the crude oil glut will persist through 2016

• A slowdown in oil demand growth stemming from lower

prices faded as economic activity weakened in countries

dependent on commodity revenues

• World oil supply held steady near 99.6 mil barrels/day in

September as a drop in output from the US, and other

producers outside of OPEC, was offset by increased

supply from the cartel itself

• Saudi Arabia is working with OPEC members and

producers from outside the group to stabilise the market

via continued exploration and producing oil and investing

in spare capacity

Industry Trends and Leading Indicators

4

Global outlook remains bearish…

Source: International Energy Agency 2015, Thomson Reuters, Bloomberg article

…with some bright spots in the domestic market

• PETRONAS is striving to support local owner

operators through a review of its licensing

requirements

• A directive was issued, effective from September

2015, eliminating the use of agents for tender

submissions. Preference will be given to members of

the Malaysian OSV Owners Association for the

charter of vessels

• This will help support local owners and stem the

outflow of funds to foreign boat owners, which is

largely in line with CORAL 2.0 program to reduce

costs

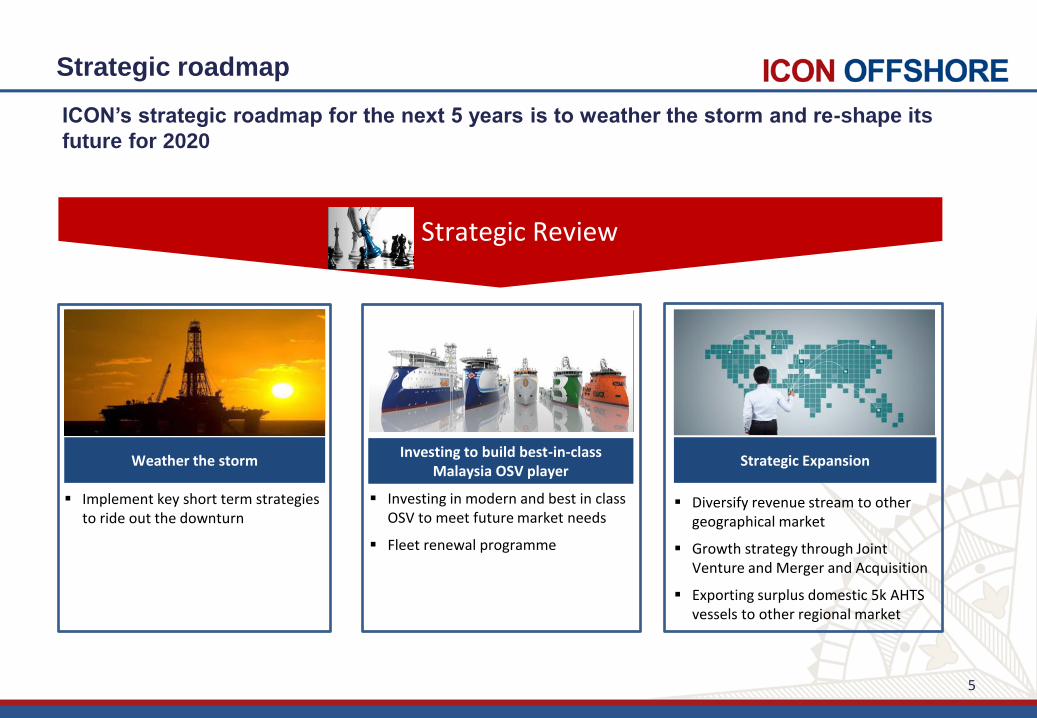

Strategic roadmap

5

Strategic Review

Weather the storm

Implement key short term strategies to ride out the downturn

Investing to build best-in-class Malaysia OSV player

Investing in modern and best in class OSV to meet future market needs

Fleet renewal programme

Strategic Expansion

Diversify revenue stream to other geographical market

Growth strategy through Joint Venture and Merger and Acquisition

Exporting surplus domestic 5k AHTS vessels to other regional market

ICON’s strategic roadmap for the next 5 years is to weather the storm and re-shape its

future for 2020

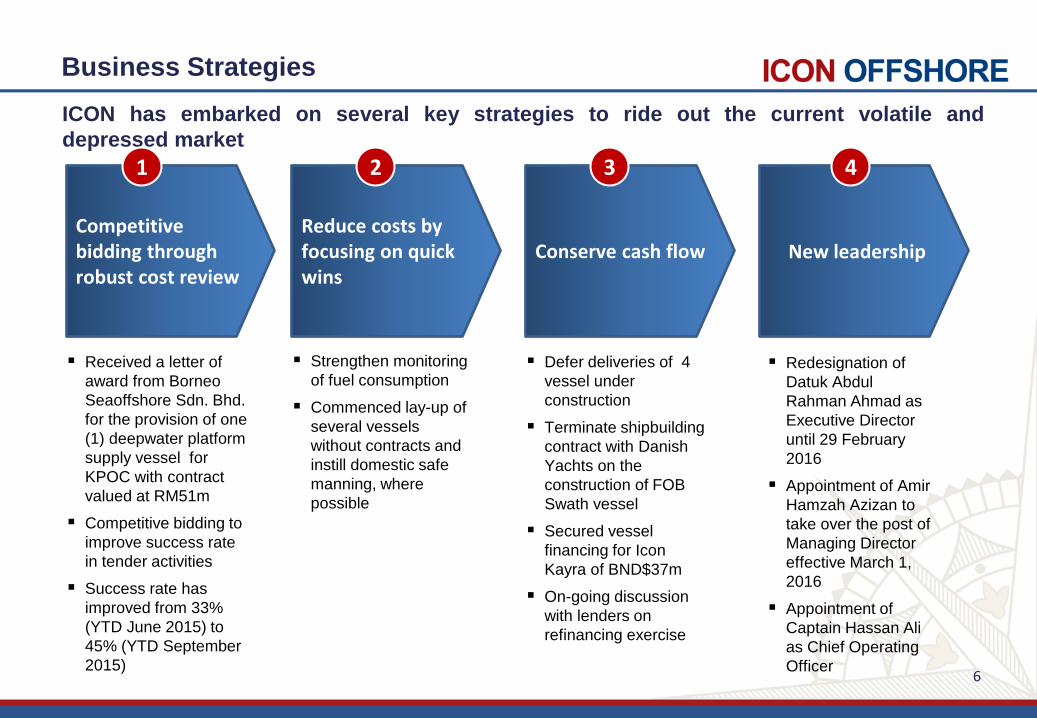

Business Strategies

6

ICON has embarked on several key strategies to ride out the current volatile and

depressed market

Received a letter of

award from Borneo

Seaoffshore Sdn. Bhd.

for the provision of one

(1) deepwater platform

supply vessel for

KPOC with contract

valued at RM51m

Competitive bidding to

improve success rate

in tender activities

Success rate has

improved from 33%

(YTD June 2015) to

45% (YTD September

2015)

Strengthen monitoring

of fuel consumption

Commenced lay-up of

several vessels

without contracts and

instill domestic safe

manning, where

possible

Defer deliveries of 4

vessel under

construction

Terminate shipbuilding

contract with Danish

Yachts on the

construction of FOB

Swath vessel

Secured vessel

financing for Icon

Kayra of BND$37m

On-going discussion

with lenders on

refinancing exercise

Redesignation of

Datuk Abdul

Rahman Ahmad as

Executive Director

until 29 February

2016

Appointment of Amir

Hamzah Azizan to

take over the post of

Managing Director

effective March 1,

2016

Appointment of

Captain Hassan Ali

as Chief Operating

Officer

Competitive bidding through robust cost review

1

Reduce costs by focusing on quick wins

Conserve cash flow New leadership

2 3 4

Operational Highlights

7

Operational Highlights (1/5) – Utilisation

8

Fleet utilisation rate Contracts status

No. of vessels

15

Type of contract

Long-term

18 Spot/available

for charter

%

45%

55%

Utilisation rate trend

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

YTD Q32014 YTD Q42014 YTD Q12015 YTD Q22015 YTD Q32015

Utilisation Rate

Competitive tenders have arrested the decline in utilisation Backed by significant number of vessels with long-term contracts

15 vessels (45%) out of the Group’s total fleet have

remaining tenure on its long-term contracts, of which

constitutes ~91% of the Group’s order book of

RM714.6 mil as at 30 September 2015

AHTS

AHT

SSV

PSV

AWB

Others

YTD Sept 2014 YTD Sept 2015

88%

41%

73%

88%

100%

62%

65%

40%

51%

9%

91%

100%

79% 61%

Operational Highlights (2/5) – Order book

9

Increased bidding activity with focus on the South East Asia region, as well as maintaining

earnings visibility

Charter Contract Tender Success Rate YTD Sept 2015

Healthy order book with several tenders still awaiting results

Total order book stood at RM714.6 mil, of which

RM455.8 mil (63.8%) are firm, RM249.4 mil (34.9%) are

extension options and RM9.4 mil (1.3%) are spot

charters.

Continuous participation in tenders

The Group has average success rate of 45% (2Q 2015:

33%) in our tendering activities.

PETRONAS Carigali

Contracts with reputable oil majors limits credit risks

Order Book

RM' mil 2015 2016 2017 >2017 Total

Firm Charter 54.3 207.3 144.2 50.0 455.8

Option Charter 0.0 7.1 62.5 179.7 249.4

Spot Charter 8.6 0.9 0.0 0.0 9.4

Contract Value 62.9 215.3 206.8 229.7 714.6

Order Book Summary as at 30-Sept 2015

Successful Unsuccessful Total Success Rate Awaiting Results

AHTS 6 5 11 55% 5

AHT 2 4 6 33% 2

SSV 1 0 1 100% 4

PSV 0 3 3 0% 5

UV 0 0 0 0% 1

AWB 1 0 1 0% 0

Total 10 12 22 45% 17

Operational Highlights (3/5) – Contract awards

10

Egypt

Saudi Arabia

Malaysia

India U.A.E

Iraq

Myanmar

Thailand

Vietnam

Brunei

ICON Experience ICON Vessel(s) currently deployed

14 Jul 2015

Received two letters of award from PCSB for the provision of two

anchor handling tug/supply vessels (“Long-term Contracts”), namely

Icon Samudera and Icon Sophia for a period of 2+1 years

The Long-term Contracts is effective from 5 July 2015

The total value of the Long Term Contracts is approximately RM55

mil inclusive of extension period

27 May 2015

Secured second long-term contract through Brunei

JV partner with Brunei Shell Petroleum for the

provision of one (1) Accommodation Work Boat for

a period of 2+1 years, namely Icon Valiant

The contract is valued at approximately RM99 mil

Business Development – Key Significant Contracts YTD September 2015

23 Oct 2015

Received Letter of Award from ExxonMobil Exploration &

Production Malaysia Inc. for the provision two (2) Anchor Handling

Tug/Supply vessels (“Short-term Contract”), namely Icon Zara and

Icon Ikhlas

Icon Zara has commenced its service on 30 Sept 2015 and shall

continue for a period of six (6) months with an option for one (1)

month extension period

Icon Ikhlas has commenced its service on 1 Oct 2015 for a period

of three (3) months

The Short-term Contract is valued at approximately RM7.7 mil

24 Nov 2015

Received a letter of award from Borneo Seaoffshore Sdn. Bhd. for

the provision of one (1) deepwater platform supply vessel for

KPOC

The contract is valued at approximately RM51 million

Contracts awarded after 3Q15

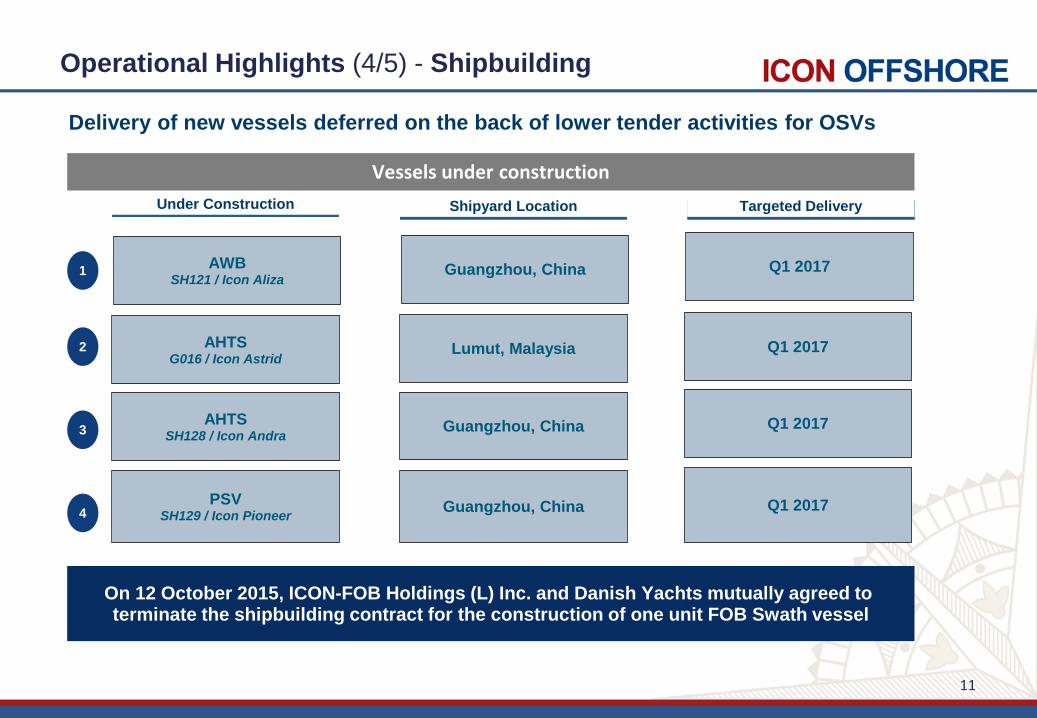

Operational Highlights (4/5) - Shipbuilding

11

Delivery of new vessels deferred on the back of lower tender activities for OSVs

Vessels under construction

AHTS G016 / Icon Astrid

AHTS SH128 / Icon Andra

AWB SH121 / Icon Aliza

PSV SH129 / Icon Pioneer

Lumut, Malaysia

Guangzhou, China

Guangzhou, China

Guangzhou, China

Q1 2017

Q1 2017

Q1 2017

Q1 2017

Under Construction Shipyard Location Targeted Delivery

3

1

2

4

On 12 October 2015, ICON-FOB Holdings (L) Inc. and Danish Yachts mutually agreed to terminate the shipbuilding contract for the construction of one unit FOB Swath vessel

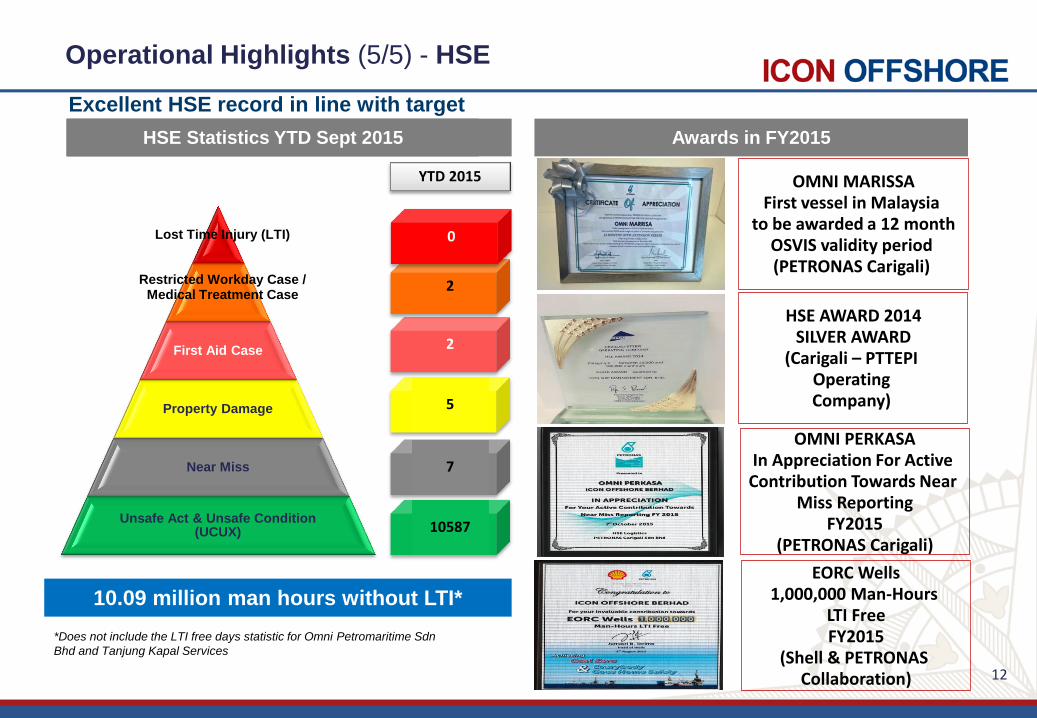

Operational Highlights (5/5) - HSE

12

Excellent HSE record in line with target

Awards in FY2015 HSE Statistics YTD Sept 2015

OMNI MARISSA First vessel in Malaysia

to be awarded a 12 month OSVIS validity period (PETRONAS Carigali)

HSE AWARD 2014 SILVER AWARD

(Carigali – PTTEPI Operating Company)

HSE Statistics YTD Sept 2015

First Aid Case

Property Damage

Near Miss

Unsafe Act & Unsafe Condition (UCUX)

Restricted Workday Case / Medical Treatment Case

Lost Time Injury (LTI)

10587

7

5

2

2

0

YTD 2015

10.09 million man hours without LTI*

*Does not include the LTI free days statistic for Omni Petromaritime Sdn

Bhd and Tanjung Kapal Services

OMNI PERKASA In Appreciation For Active Contribution Towards Near

Miss Reporting FY2015

(PETRONAS Carigali) EORC Wells

1,000,000 Man-Hours LTI Free FY2015

(Shell & PETRONAS Collaboration)

Group Financial Overview

13

241.8201.2

YTD Sept 2014 YTD Sept 2015

Utilisation rates

-16.8%

61%79%

147.8

90.8

YTD Sept 2014 YTD Sept 2015Margin

61.6%

-38.6%

45.1%

71.4

14.6

YTD Sept 2014 YTD Sept 2015Margin

7.2%29.5%

-79.6%

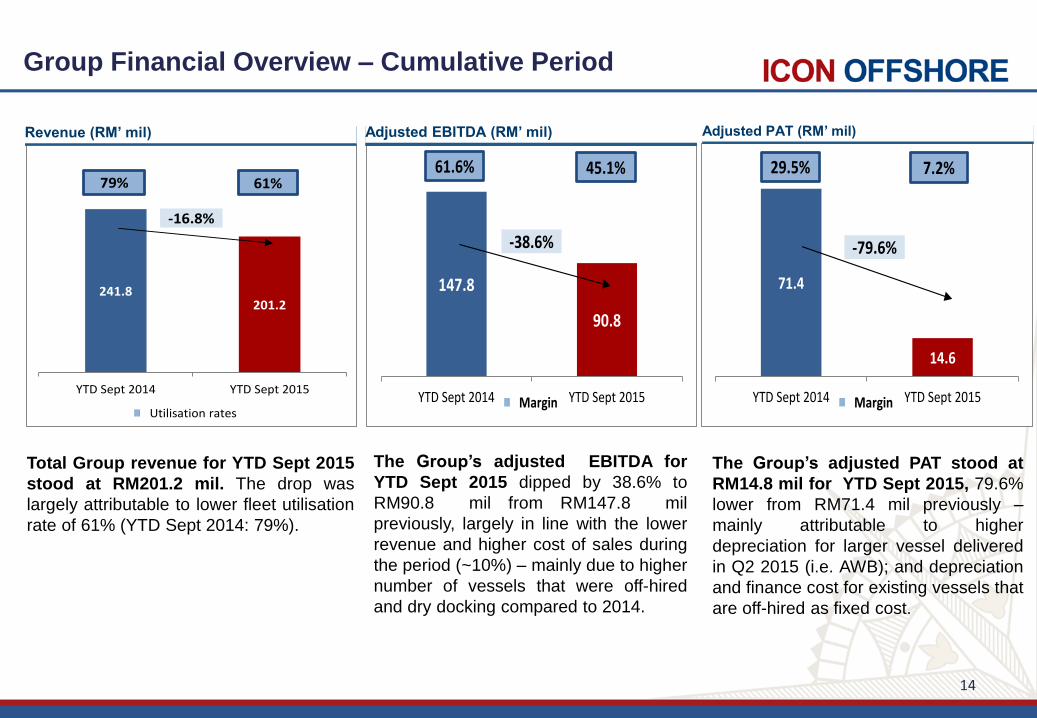

Group Financial Overview – Cumulative Period

14

Revenue (RM’ mil) Adjusted EBITDA (RM’ mil) Adjusted PAT (RM’ mil)

Total Group revenue for YTD Sept 2015

stood at RM201.2 mil. The drop was

largely attributable to lower fleet utilisation

rate of 61% (YTD Sept 2014: 79%).

The Group’s adjusted EBITDA for

YTD Sept 2015 dipped by 38.6% to

RM90.8 mil from RM147.8 mil

previously, largely in line with the lower

revenue and higher cost of sales during

the period (~10%) – mainly due to higher

number of vessels that were off-hired

and dry docking compared to 2014.

The Group’s adjusted PAT stood at

RM14.8 mil for YTD Sept 2015, 79.6%

lower from RM71.4 mil previously –

mainly attributable to higher

depreciation for larger vessel delivered

in Q2 2015 (i.e. AWB); and depreciation

and finance cost for existing vessels that

are off-hired as fixed cost.

79.7

69.1

3Q14 3Q15

-13.4%

20.7

6.1

3Q14 3Q15

-70.5%

8.9%26.0%

Margin

45.1

32.4

3Q14 3Q15

56.5% 46.9%

Margin

-28.2%

Group Financial Overview – Quarter on Quarter

(3Q14 vs 3Q15)

15

3Q15 Group revenue stood at RM69.1

mil versus RM79.7 mil in 3Q14. The

decrease by RM10.6m was primarily

due to lower vessel utilisation rate

during the quarter under review 3Q15.

This is a decrease of 14.2% from 3Q14

of 76.1%

The decrease were mainly due to 4

vessels on scheduled drydock, vessels

that have completed contracts and

vessels on repair/maintenance program

3Q15 adjusted EBITDA recorded at

RM32.4m, mainly lower by RM12.7m

due to the lower revenue as a result

from lower oil and gas activities during

the quarter.

3Q15 adjusted PAT showed a dip which

is mainly attributable to higher

depreciation for larger vessel (i.e. AWB

and PSV) delivered in Q2 2015; as well

as depreciation and finance cost

incurred for existing vessels that are off-

hired as fixed cost.

Revenue (RM’ mil) Adjusted EBITDA (RM’ mil) Adjusted PAT (RM’ mil)

3.3

5.26.1

1Q15 2Q15 3Q15

18.6%

8.9%7.5%

Margin

56.4%

5.2%

27.0

31.5 32.4

1Q15 2Q15 3Q15

Margin

42.5% 46.9%45.9%

2.8%16.7%

63.6 68.6 69.1

1Q15 2Q15 3Q15

0.7%7.8%

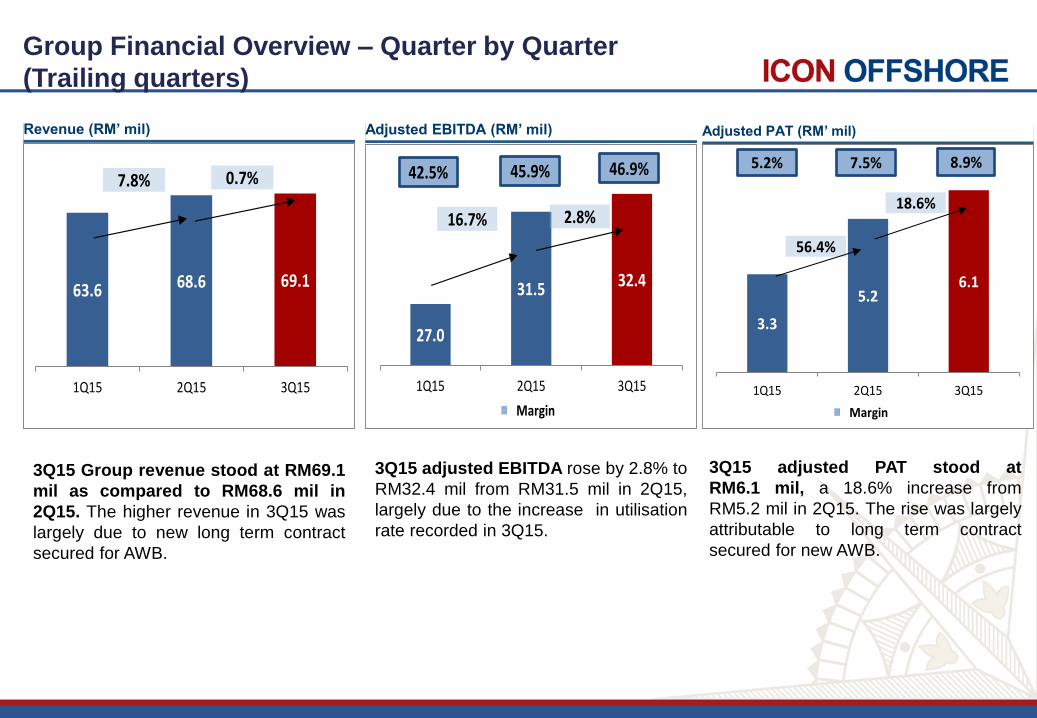

Group Financial Overview – Quarter by Quarter

(Trailing quarters)

16

3Q15 Group revenue stood at RM69.1

mil as compared to RM68.6 mil in

2Q15. The higher revenue in 3Q15 was

largely due to new long term contract

secured for AWB.

3Q15 adjusted EBITDA rose by 2.8% to

RM32.4 mil from RM31.5 mil in 2Q15,

largely due to the increase in utilisation

rate recorded in 3Q15.

3Q15 adjusted PAT stood at

RM6.1 mil, a 18.6% increase from

RM5.2 mil in 2Q15. The rise was largely

attributable to long term contract

secured for new AWB.

Revenue (RM’ mil) Adjusted EBITDA (RM’ mil) Adjusted PAT (RM’ mil)

RM85.5 mil72%

RM33.2 mil28%

75%

25%

RM152.7 mil96%

RM7.1 mil4%

90%

10%

166

924 18

7 6

121

816

3

45

7

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

AHTS AHT SSV PSV AWB Others

YTD Sept 2014 YTD Sept 2015

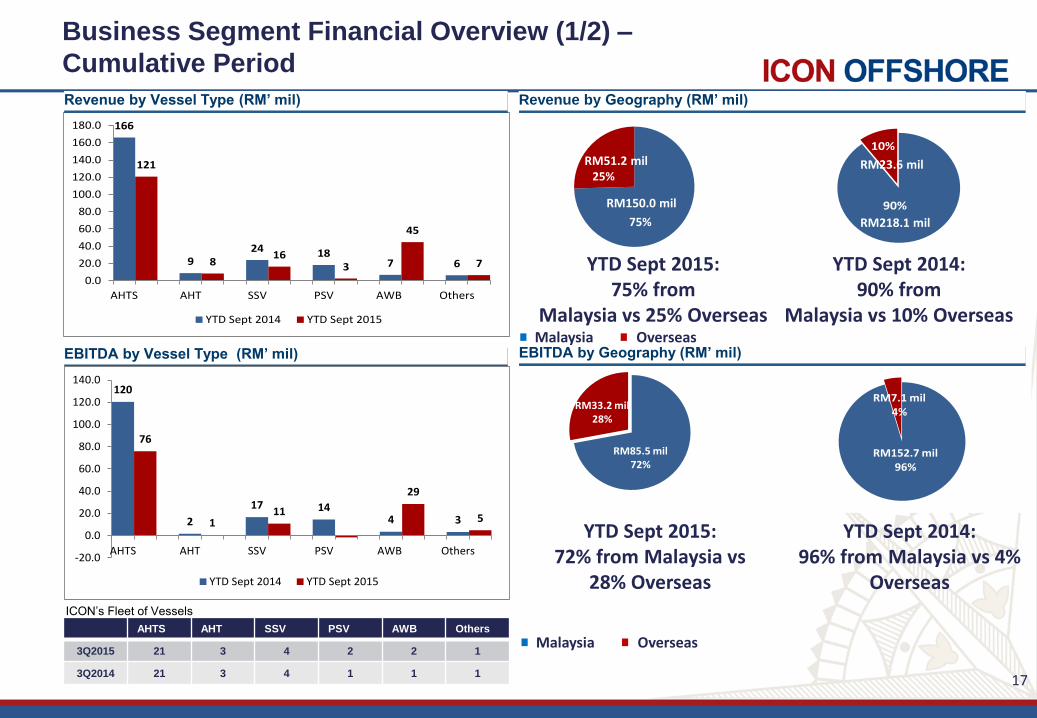

Business Segment Financial Overview (1/2) –

Cumulative Period

17

Revenue by Vessel Type (RM’ mil) Revenue by Geography (RM’ mil)

EBITDA by Geography (RM’ mil) EBITDA by Vessel Type (RM’ mil)

YTD Sept 2015: 72% from Malaysia vs

28% Overseas

YTD Sept 2014: 96% from Malaysia vs 4%

Overseas

RM150.0 mil

RM218.1 mil

RM51.2 mil

YTD Sept 2015: 75% from

Malaysia vs 25% Overseas

YTD Sept 2014: 90% from

Malaysia vs 10% Overseas

RM23.6 mil

120

2

17 144 3

76

111

29

5

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

AHTS AHT SSV PSV AWB Others

YTD Sept 2014 YTD Sept 2015

ICON’s Fleet of Vessels

AHTS AHT SSV PSV AWB Others

3Q2015 21 3 4 2 2 1

3Q2014 21 3 4 1 1 1

Malaysia Overseas

Malaysia Overseas

38

1 25

41

25

14

14

2

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

AHTS AHT SSV PSV AWB Others

Q32014 Q32015

65%

35%

3Q14: 84% from Malaysia vs 16% Overseas

54

4 47 7

4

38

4 6

0

20

2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

AHTS AHT SSV PSV AWB Others

Q32014 Q32015

16%

84%

Business Segment Financial Overview (2/2) –

Quarter on Quarter

18

Revenue by Vessel Type (RM’ mil) Revenue by Geography (RM’ mil)

EBITDA by Vessel Type (RM’ mil) EBITDA by Geography (RM’ mil)

3Q15: 64% from Malaysia vs 36%

Overseas

Malaysia Overseas

3Q14: 90% from Malaysia vs 10%

Overseas

RM67.3 mil RM44.6 mil

3Q15: 65% from Malaysia vs 35% Overseas

RM21.9 mil RM12.5 mil

AHTS AHT SSV PSV AWB Others

3Q2015 21 3 4 2 2 1

3Q2014 21 3 4 1 1 1

ICON’s Fleet of Vessels

RM27.9 mil64%

RM15.6 mil36%

Malaysia Overseas

RM45.2 mil90%

RM5.1 mil10%

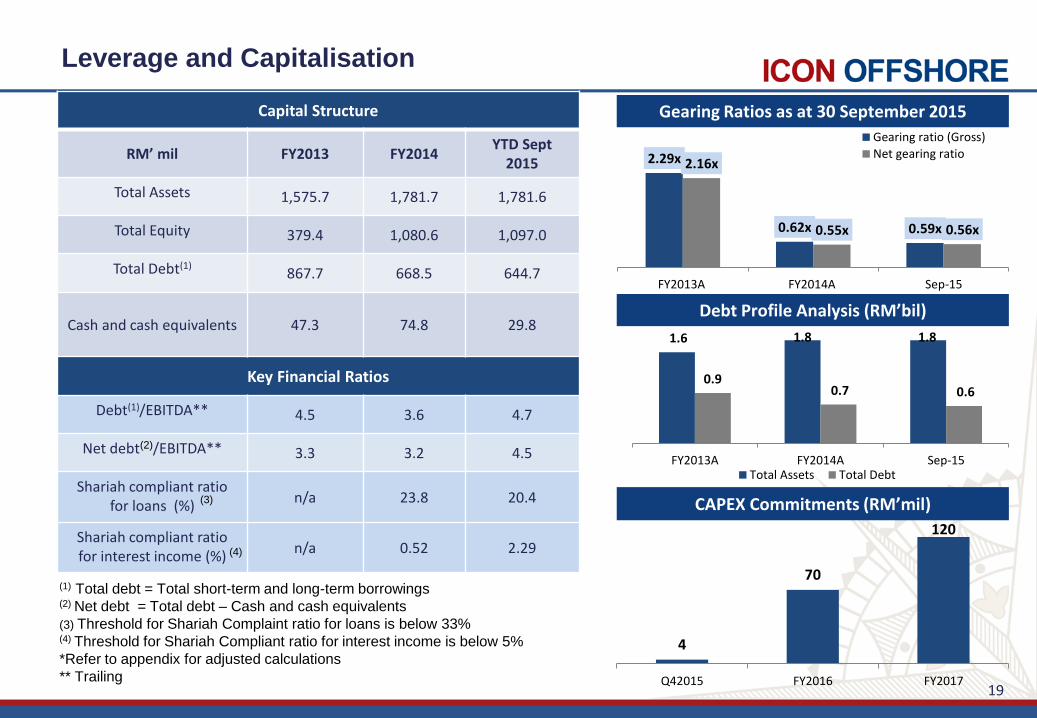

Leverage and Capitalisation

19

Capital Structure

RM’ mil FY2013 FY2014 YTD Sept

2015

Total Assets 1,575.7 1,781.7 1,781.6

Total Equity 379.4 1,080.6 1,097.0

Total Debt(1) 867.7 668.5 644.7

Cash and cash equivalents 47.3 74.8 29.8

Key Financial Ratios

Debt(1)/EBITDA** 4.5 3.6 4.7

Net debt(2)/EBITDA** 3.3 3.2 4.5

Shariah compliant ratio for loans (%)

n/a 23.8 20.4

Shariah compliant ratio for interest income (%)

n/a 0.52 2.29

(1) Total debt = Total short-term and long-term borrowings (2) Net debt = Total debt – Cash and cash equivalents

(3) Threshold for Shariah Complaint ratio for loans is below 33% (4) Threshold for Shariah Compliant ratio for interest income is below 5%

*Refer to appendix for adjusted calculations

** Trailing

Gearing Ratios as at 30 September 2015

Debt Profile Analysis (RM’bil)

CAPEX Commitments (RM’mil) (3)

(4)

2.29x

0.62x 0.59x

2.16x

0.55x 0.56x

FY2013A FY2014A Sep-15

Gearing ratio (Gross)

Net gearing ratio

1.6 1.8 1.8

0.9 0.7 0.6

FY2013A FY2014A Sep-15Total Assets Total Debt

4

70

120

Q42015 FY2016 FY2017

Key takeaways

1 Icon has been taking positive steps to navigate the current

challenging market conditions

We are controlling costs, ensuring operational efficiency, and expanding into new

markets

We have a strong business that is continuing to win contracts

Our team blends decades of domestic, international and industry experience

2 Icon’s positive steps are starting to show results and have an impact

Our adjusted net profit and revenue have all improved on a quarter-by-quarter

basis since the start of the financial year

There is a higher vessel utilisation arising from expansion into the Brunei market

We have a higher tender success rate through a targeted bidding strategy

Our vessels running costs are lower through enhanced operational efficiency –

improved margins

20

1

2

Thank you

21

Appendices

22

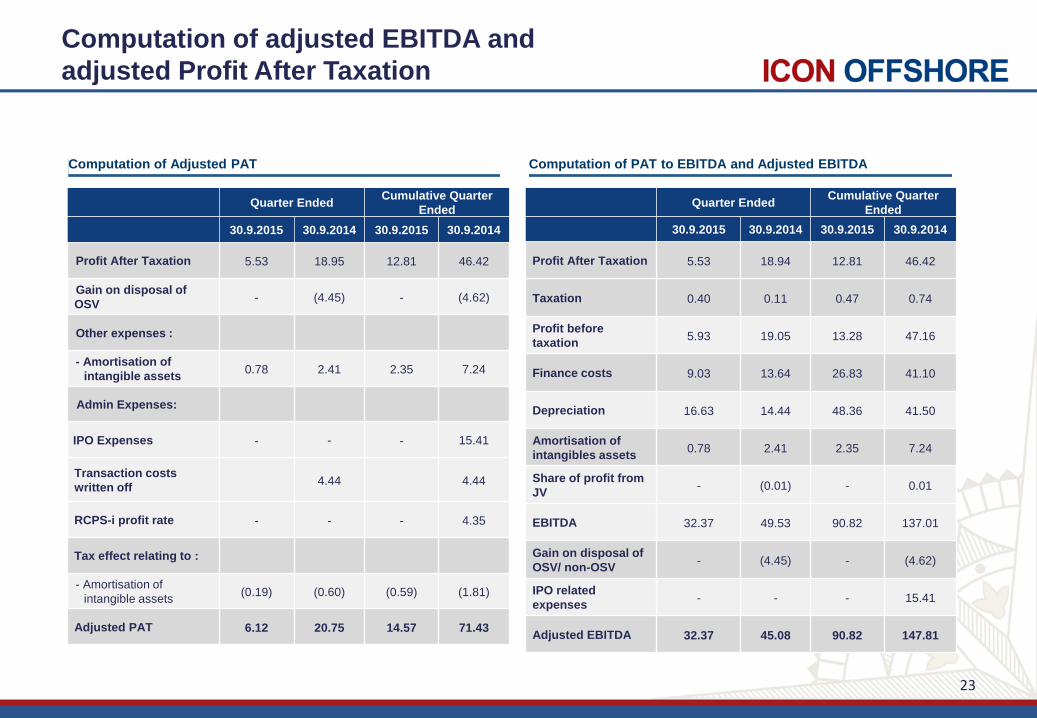

Computation of adjusted EBITDA and

adjusted Profit After Taxation

23

Computation of PAT to EBITDA and Adjusted EBITDA Computation of Adjusted PAT

Quarter Ended

Cumulative Quarter

Ended

30.9.2015 30.9.2014 30.9.2015 30.9.2014

Profit After Taxation 5.53 18.95 12.81 46.42

Gain on disposal of

OSV - (4.45) - (4.62)

Other expenses :

- Amortisation of

intangible assets 0.78 2.41 2.35 7.24

Admin Expenses:

IPO Expenses - - - 15.41

Transaction costs

written off

4.44

4.44

RCPS-i profit rate - - - 4.35

Tax effect relating to :

- Amortisation of

intangible assets (0.19) (0.60) (0.59) (1.81)

Adjusted PAT 6.12 20.75 14.57 71.43

Quarter Ended Cumulative Quarter

Ended

30.9.2015 30.9.2014 30.9.2015 30.9.2014

Profit After Taxation 5.53 18.94 12.81 46.42

Taxation 0.40 0.11 0.47 0.74

Profit before

taxation 5.93 19.05 13.28 47.16

Finance costs 9.03 13.64 26.83 41.10

Depreciation 16.63 14.44 48.36 41.50

Amortisation of

intangibles assets 0.78 2.41 2.35 7.24

Share of profit from

JV - (0.01) - 0.01

EBITDA 32.37 49.53 90.82 137.01

Gain on disposal of

OSV/ non-OSV - (4.45) - (4.62)

IPO related

expenses - - - 15.41

Adjusted EBITDA 32.37 45.08 90.82 147.81