4. confirmation of minutes from previous … · confirmation of minutes from previous ... australia...

TRANSCRIPT

Audit Committee - Minutes of meeting held 5 February 2015 Page

1

MINUTES OF THE MEETING OF THE AUDIT COMMITTEE OF THE BAROSSA COUNCIL

held in the Committee Room, 43-51 Tanunda Road, Nuriootpa, on Thursday 5 February 2015 commencing at 12:00 noon.

1. WELCOME

Mr Peter Brass welcomed everyone to the meeting, extending a particular welcome to the new members. The new members of the Committee Cr Scotty Milne and Tanya Johnston provided a brief introduction to the Committee..

2. PRESENT

Mr Peter Brass, Mr James Heuzenroeder, Ms Tanya Johnston, Cr Angas, Cr Milne, Cr Miller (present 12.05pm onwards)

Invited Staff Members Mr Martin McCarthy, Chief Executive Officer Ms Jo Thomas, Director Corporate & Community Services Mr Mark Lague, Manager Financial Services Ms Vicky Rohrlach, Senior Accountant Mr Alan Jackson, Risk Manager Ms Nicole Rudd, Internal Controls Compliance Officer Ms Susie Roehr, Executive Assistant, Director Corporate & Community Services

3. APOLOGIES Nil 4. CONFIRMATION OF MINUTES FROM PREVIOUS MEETING MOVED Mr Heuzenroeder that the Minutes of the Audit Committee Meeting held 29 October 2014, as circulated, be confirmed as a true and correct record of the proceedings of the meeting. Seconded Cr Angas CARRIED 5. BUSINESS ARISING FROM PREVIOUS MINUTES Included in the agenda. 6. CONSENSUS AGENDA 6.1 REPORTS FOR INFORMATION The meeting discussed item 6.1.1 – Amended Terms of Reference. A few minor amendments were proposed. Document to be updated and distributed to Audit Committee members to ensure proposed amendments are incorporated correctly. Terms of reference will then need to be presented to Council for approval. MOVED Cr Angas that the amended Audit Committees Terms of Reference be noted and changes incorporated for approval by Council. Seconded Cr Miller CARRIED

Audit Committee - Minutes of meeting held 5 February 2015 Page

2

6.2 CORRESPONDENCE

The meeting discussed each item. MOVED Mr Heuzenroeder that Correspondence Items 6.2.1 to 6.2.3 be received. Seconded Ms Johnston CARRIED 7.1 DEBATE AGENDA - REPORTS 7.1.1 DRAFT AUDIT COMMITTEE 2015 WORKPLAN INTRODUCTION The Draft Audit Committee Workplan for 2015 was provided for members. MOVED Cr Miller that the Audit Committee approves the draft Audit Committee Workplan for 2015. Seconded Mr Heuzenroeder CARRIED

COMMENT The draft Workplan has been formulated based on a model workplan developed by the Local Government Association. A well-functioning Audit Committee and an appropriate and robust internal audit program (as outlined in the draft Workplan), significantly reduces the likelihood of the need for Efficiency and Economy Audits as prescribed in Section 130A of the Local Government Act 1999. The Workplan has been prepared to include all proposed reports, policy reviews, compliance reviews, etc for 2015. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 – Section 126 FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Adoption and adherence to an annual Workplan is a risk management tool. COMMUNITY CONSULTATION Not required under legislation or Council’s Public Consultation Policy. ACTIONS: • The Chair requested divisional Managers present their risk profiles at a future

meeting(s). The Chief Executive to present risk profile information at November /December meeting.

• September/October – in camera meeting with the external and internal auditor be noted. Workplan to be updated accordingly.

7.1.2 REVIEW OF INVESTMENTS

Audit Committee - Minutes of meeting held 5 February 2015 Page

3

In respect of the graph showing Investment Performance verses Benchmark, Members questioned how the Local Government Finance Authority Weighted Average Fixed Interest Rate could fall below the Official Reserve Bank of Australia Cash Rate as depicted in the graph. Officers to provide clarification. INTRODUCTION Pursuant to Section 140 of the Local Government Act 1999, and in accordance with Council’s Investment Policy, Council must undertake an annual performance review of its investments. MOVED Cr Angas that the report on Council’s 2014 Investments be received and noted. Seconded Cr Miller CARRIED

COMMENT During 2014, Reserve Bank interest rates have remained at 2.50%. All investments made during 2014 were held with the Local Government Finance Authority of South Australia (LGFA) or Council’s National Australia Bank (NAB) investment account and are based on the following key factors: Interest rate consistently similar or slightly higher than rates quoted from other

financial institutions. Council staff compared rates between LGFA, National Australia Bank, Bank SA, AMP, Westpac and Commonwealth Bank.

Annual bonus distribution to Councils based on debenture loan/investment

holdings ($47,158 bonus received in 2014/15); Annual contribution to the Local Government Research and Development fund;

Ease of making transactions.

The National Australia Bank ‘investment’ account has a higher interest rate than Council’s operating account and money is automatically transferred overnight whenever the operating account balance is more than $50,000. This maximises interest earnings on a daily basis. The current interest rate as at 31 December 2014 for this account is 3%. Where funds are significantly higher than required for upcoming payments, funds are transferred to the LGFA for deposit of between 0 and 120+ days investment, as per previous practice and dependant on cash flow requirements. These factors are considered consistent with the criteria outlined in Council’s Investment Policy.

Audit Committee - Minutes of meeting held 5 February 2015 Page

4

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

%

INVESTMENT PERFORMANCE VS BENCHMARKJANUARY TO DECEMBER 2014

Official Cash Rate

LGFA Weighted Average Fixed Interest Rate

LGFA Weighted Average Variable Interest Rate

NAB Weighted Average Variable Interest Rate

0

2,000

4,000

6,000

8,000

10,000

12,000

$ INTEREST EARNED JANUARY TO DECEMBER 2014

LGFA Variable Investments LGFA Fixed Investments NAB Investment Account

The weighted average interest rate (fixed and variable) on Council’s investments during 2014 compared to the official Reserve Bank of Australia cash rate, is outlined in the graph below:

Monthly interest earned for 2014 is shown in the following graph:

The level of funds invested during the year is presented in the graph below. The graph excludes Council’s separate operating bank account which was maintained at minimum working capital levels in accordance with the Policy.

Audit Committee - Minutes of meeting held 5 February 2015 Page

5

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

$ LEVEL OF FUNDS INVESTED JANUARY TO DECEMBER 2014

LGFA Investments NAB Investment Account

Council’s total investments as at 31 December 2014 are outlined in the table below: Variable

Interest Rate

$’000

< 1 year Fixed $’000

> 1 year < 5 years

$’000

> 5 years $’000

Non-interest bearing

$’000

TOTAL $’000

LGFA

5,374

1,244

0

0

0

6,618

NAB Investment A/c

772

0

0

0

0

772

TOTAL

6,146

1,244

0

0

0

7,390

LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Section 140 of the Local Government Act 1999 Council Policy Investment Policy Council Strategic Plan Strategy 4.1: Responsibility FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS The review of Council investments monitors performance in this area. COMMUNITY CONSULTATION Community consultation is not required for the operational management of investments. ACTIONS: • Follow up explanation on the Investment Performance verses Benchmark graph

comparing the average interest rate on Council’s investments via Local Government Finance Authority during 2014 compared to the official Reserve Bank of Australia

Audit Committee - Minutes of meeting held 5 February 2015 Page

6

cash rate to be provided to members. Future examination of the Policy to be undertaken to see how it is calculated.

7.1.3 TREASURY MANAGEMENT REVIEW INTRODUCTION Pursuant to Section 140 of the Local Government Act 1999, and in accordance with Council’s Treasury Management Policy, Council must undertake an annual performance review of its Treasury Management activities. MOVED Cr Milne hat the report on Council’s 2014 Treasury Management activities be received and noted. Seconded Mr Heuzenroeder CARRIED

COMMENT The key principles within Council’s Treasury Management Policy are as follows: Council will:

• Maintain target ranges for its Net Financial Liabilities ratio;

• Generally only borrow funds when it needs cash and not specifically for particular projects;

• Not retain and quarantine money for particular future purposes unless required

by legislation or agreement with other parties;

• Apply any funds that are not immediately required to meet approved expenditure (including funds that are required to be expended for specific purposes but are not required to be kept in separate bank accounts) to reduce its level of borrowings or to defer and/or reduce the level of new borrowings that would otherwise be required.

Comments regarding the 2014 performance with regard to the above principles are outlined below: (a) Net Financial Liabilities Ratio Council’s policy regarding its net financial liabilities is that they shall not exceed 100% of total operating revenue (adopted February 2010). As at 30 June 2014, Council’s net financial liabilities represented 43% of total operating revenue, and it is projected to increase to 50% as at 30 June 2015. Accordingly, Council is currently operating within its policy threshold. (b) Loan Borrowings Council’s policy relative to loan borrowings states that the use of internal reserves be considered prior to consideration of external loan borrowings. New borrowings for 2014 included $515,000 (Debenture 108) and $125,000 (Debenture 109). Both of these loans were for community group loans (Barossa Valley Hockey Association and Tanunda Tennis Club Inc/Tanunda Netball Club Inc and will be repaid to Council in half yearly repayments.

Audit Committee - Minutes of meeting held 5 February 2015 Page

7

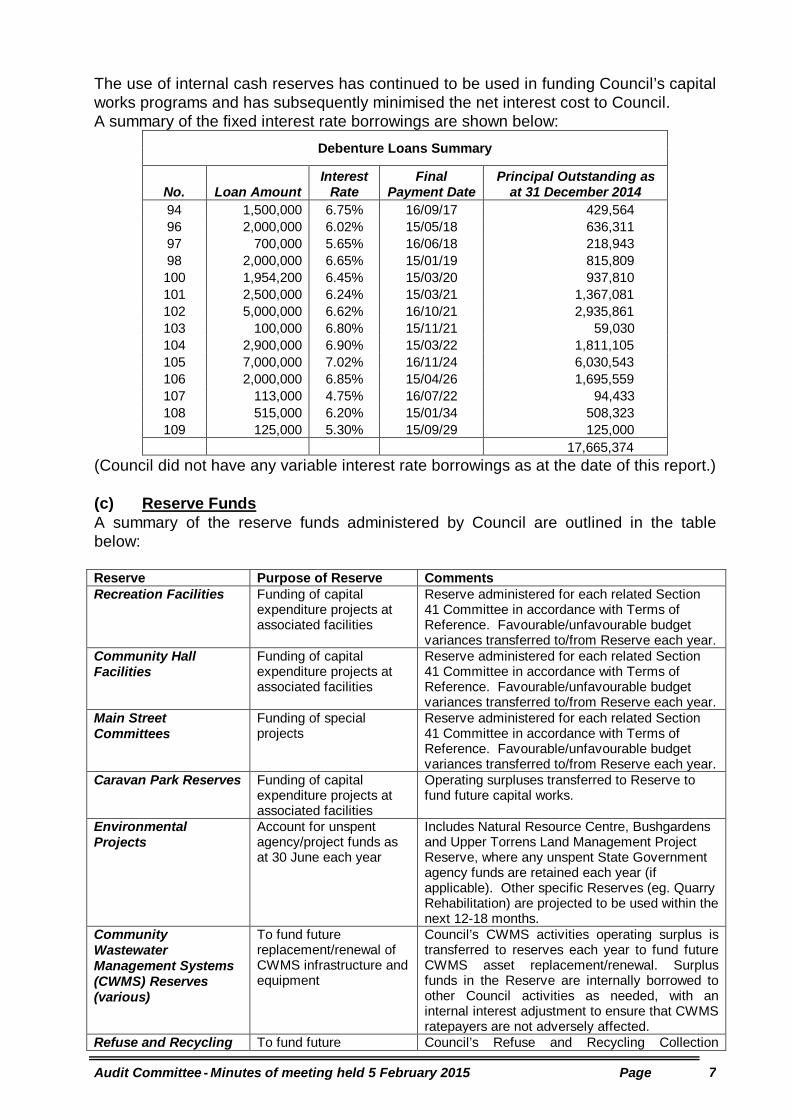

The use of internal cash reserves has continued to be used in funding Council’s capital works programs and has subsequently minimised the net interest cost to Council. A summary of the fixed interest rate borrowings are shown below:

Debenture Loans Summary

No. Loan Amount Interest

Rate Final

Payment Date Principal Outstanding as

at 31 December 2014 94 1,500,000 6.75% 16/09/17 429,564 96 2,000,000 6.02% 15/05/18 636,311 97 700,000 5.65% 16/06/18 218,943 98 2,000,000 6.65% 15/01/19 815,809 100 1,954,200 6.45% 15/03/20 937,810 101 2,500,000 6.24% 15/03/21 1,367,081 102 5,000,000 6.62% 16/10/21 2,935,861 103 100,000 6.80% 15/11/21 59,030 104 2,900,000 6.90% 15/03/22 1,811,105 105 7,000,000 7.02% 16/11/24 6,030,543 106 2,000,000 6.85% 15/04/26 1,695,559 107 113,000 4.75% 16/07/22 94,433 108 515,000 6.20% 15/01/34 508,323 109 125,000 5.30% 15/09/29 125,000

17,665,374 (Council did not have any variable interest rate borrowings as at the date of this report.) (c) Reserve Funds A summary of the reserve funds administered by Council are outlined in the table below: Reserve Purpose of Reserve Comments Recreation Facilities Funding of capital

expenditure projects at associated facilities

Reserve administered for each related Section 41 Committee in accordance with Terms of Reference. Favourable/unfavourable budget variances transferred to/from Reserve each year.

Community Hall Facilities

Funding of capital expenditure projects at associated facilities

Reserve administered for each related Section 41 Committee in accordance with Terms of Reference. Favourable/unfavourable budget variances transferred to/from Reserve each year.

Main Street Committees

Funding of special projects

Reserve administered for each related Section 41 Committee in accordance with Terms of Reference. Favourable/unfavourable budget variances transferred to/from Reserve each year.

Caravan Park Reserves Funding of capital expenditure projects at associated facilities

Operating surpluses transferred to Reserve to fund future capital works.

Environmental Projects

Account for unspent agency/project funds as at 30 June each year

Includes Natural Resource Centre, Bushgardens and Upper Torrens Land Management Project Reserve, where any unspent State Government agency funds are retained each year (if applicable). Other specific Reserves (eg. Quarry Rehabilitation) are projected to be used within the next 12-18 months.

Community Wastewater Management Systems (CWMS) Reserves (various)

To fund future replacement/renewal of CWMS infrastructure and equipment

Council’s CWMS activities operating surplus is transferred to reserves each year to fund future CWMS asset replacement/renewal. Surplus funds in the Reserve are internally borrowed to other Council activities as needed, with an internal interest adjustment to ensure that CWMS ratepayers are not adversely affected.

Refuse and Recycling To fund future Council’s Refuse and Recycling Collection

Audit Committee - Minutes of meeting held 5 February 2015 Page

8

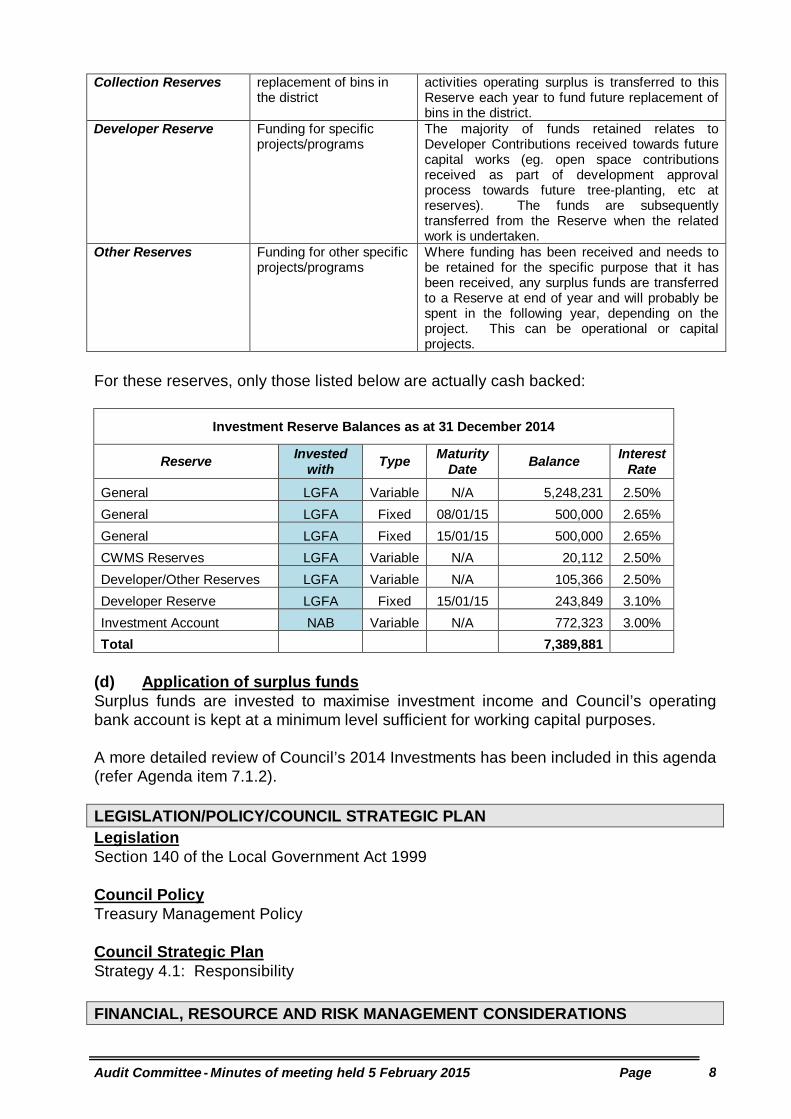

Collection Reserves replacement of bins in the district

activities operating surplus is transferred to this Reserve each year to fund future replacement of bins in the district.

Developer Reserve Funding for specific projects/programs

The majority of funds retained relates to Developer Contributions received towards future capital works (eg. open space contributions received as part of development approval process towards future tree-planting, etc at reserves). The funds are subsequently transferred from the Reserve when the related work is undertaken.

Other Reserves Funding for other specific projects/programs

Where funding has been received and needs to be retained for the specific purpose that it has been received, any surplus funds are transferred to a Reserve at end of year and will probably be spent in the following year, depending on the project. This can be operational or capital projects.

For these reserves, only those listed below are actually cash backed:

Investment Reserve Balances as at 31 December 2014

Reserve Invested with Type Maturity

Date Balance Interest Rate

General LGFA Variable N/A 5,248,231 2.50% General LGFA Fixed 08/01/15 500,000 2.65% General LGFA Fixed 15/01/15 500,000 2.65% CWMS Reserves LGFA Variable N/A 20,112 2.50% Developer/Other Reserves LGFA Variable N/A 105,366 2.50% Developer Reserve LGFA Fixed 15/01/15 243,849 3.10% Investment Account NAB Variable N/A 772,323 3.00% Total 7,389,881

(d) Application of surplus funds Surplus funds are invested to maximise investment income and Council’s operating bank account is kept at a minimum level sufficient for working capital purposes. A more detailed review of Council’s 2014 Investments has been included in this agenda (refer Agenda item 7.1.2). LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Section 140 of the Local Government Act 1999 Council Policy Treasury Management Policy Council Strategic Plan Strategy 4.1: Responsibility

FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS

Audit Committee - Minutes of meeting held 5 February 2015 Page

9

The review of Council’s Treasury Management activities monitors our performance in this area. COMMUNITY CONSULTATION Community consultation is not required for operational Treasury Management. 7.1.4 2015/16 AUDIT COMMITTEE BUDGET INTRODUCTION The Audit Committee considered a draft 2015/16 budget for the Committee’s operations. MOVED Cr Angas That: (1) the draft 2015/16 Audit Committee budget be endorsed for consideration by Council during the budget deliberations; (2) the 2015/16 sitting fee of $550 (excl GST) per meeting for the Independent Chairman of the Audit Committee be endorsed for consideration by Council; (3) the 2015/16 sitting fee of $350 (excl GST) per meeting for the Independent Members of the Audit Committee be endorsed for consideration by Council; and (4) the 2015/16 Consultant budget $3,000 and Training budget $1,000 be endorsed

for consideration by Council. Seconded Cr Milne CARRIED

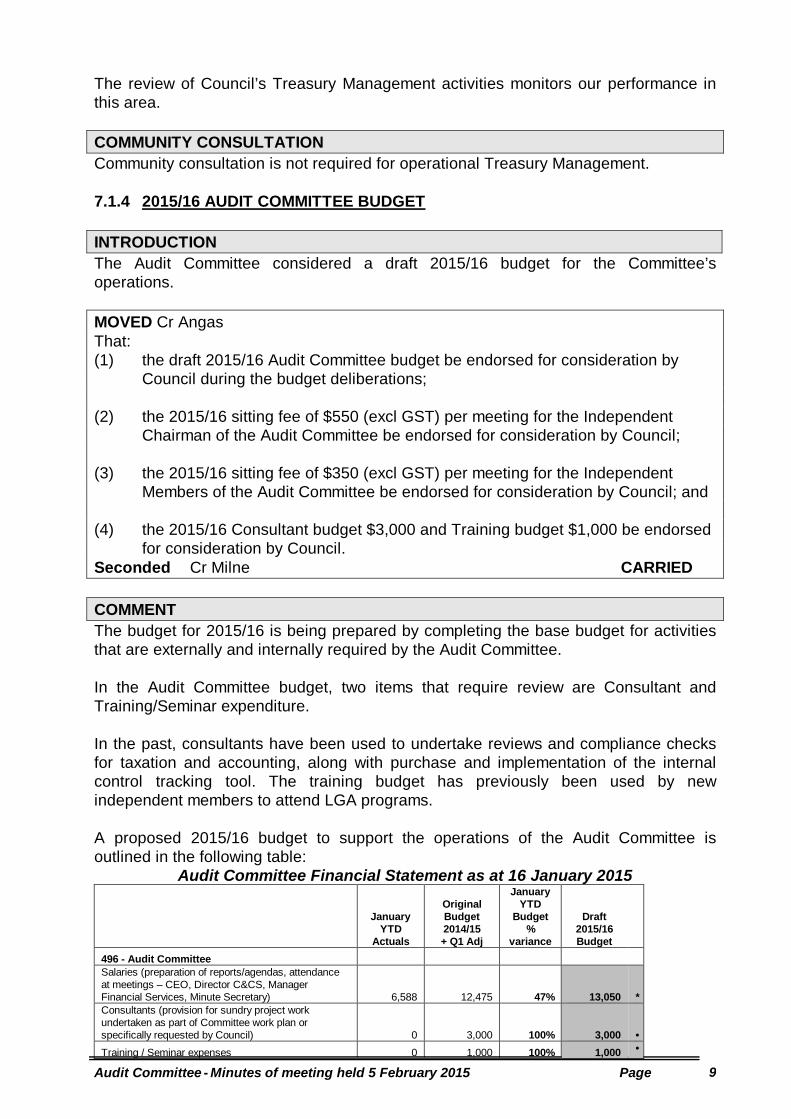

COMMENT The budget for 2015/16 is being prepared by completing the base budget for activities that are externally and internally required by the Audit Committee. In the Audit Committee budget, two items that require review are Consultant and Training/Seminar expenditure. In the past, consultants have been used to undertake reviews and compliance checks for taxation and accounting, along with purchase and implementation of the internal control tracking tool. The training budget has previously been used by new independent members to attend LGA programs. A proposed 2015/16 budget to support the operations of the Audit Committee is outlined in the following table:

Audit Committee Financial Statement as at 16 January 2015

January YTD

Actuals

Original Budget 2014/15 + Q1 Adj

January YTD

Budget %

variance

Draft 2015/16 Budget

496 - Audit Committee

Salaries (preparation of reports/agendas, attendance at meetings – CEO, Director C&CS, Manager Financial Services, Minute Secretary) 6,588 12,475 47% 13,050

*

Consultants (provision for sundry project work undertaken as part of Committee work plan or specifically requested by Council) 0 3,000 100% 3,000

•

Training / Seminar expenses 0 1,000 100% 1,000 •

Audit Committee - Minutes of meeting held 5 February 2015 Page

10

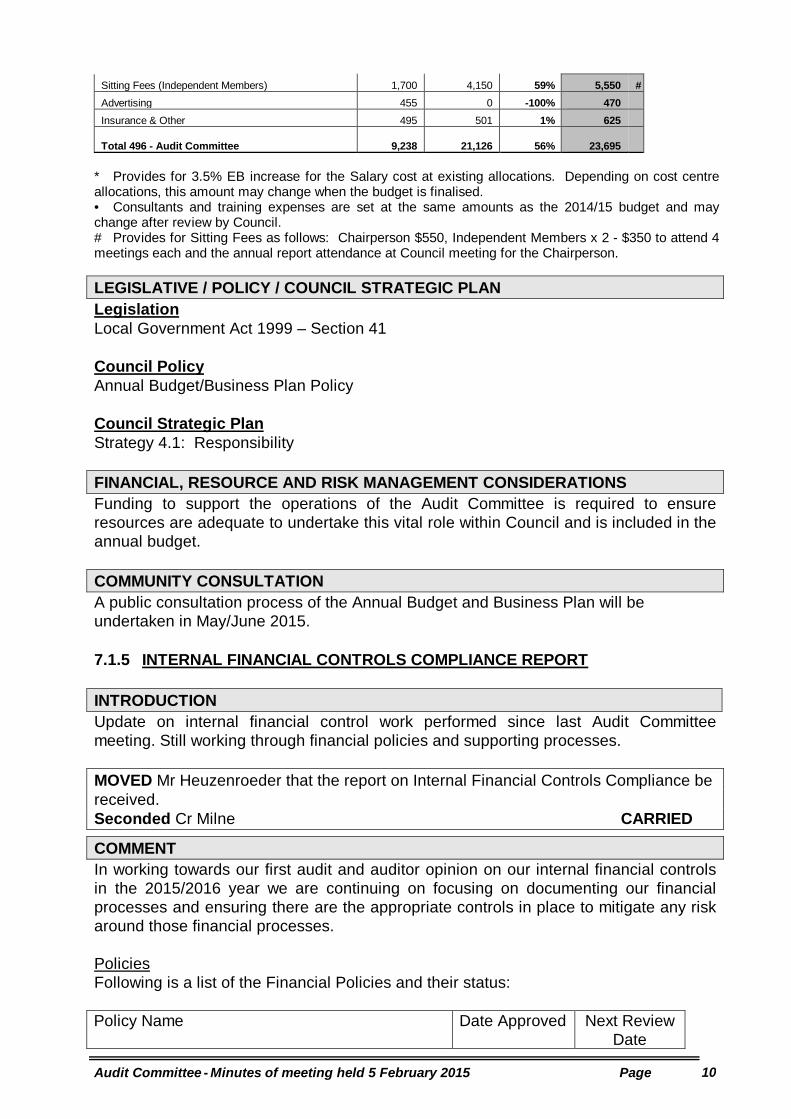

Sitting Fees (Independent Members) 1,700 4,150 59% 5,550 # Advertising 455 0 -100% 470 Insurance & Other 495 501 1% 625

Total 496 - Audit Committee 9,238 21,126

56% 23,695

* Provides for 3.5% EB increase for the Salary cost at existing allocations. Depending on cost centre allocations, this amount may change when the budget is finalised. • Consultants and training expenses are set at the same amounts as the 2014/15 budget and may change after review by Council. # Provides for Sitting Fees as follows: Chairperson $550, Independent Members x 2 - $350 to attend 4 meetings each and the annual report attendance at Council meeting for the Chairperson. LEGISLATIVE / POLICY / COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 – Section 41 Council Policy Annual Budget/Business Plan Policy Council Strategic Plan Strategy 4.1: Responsibility FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Funding to support the operations of the Audit Committee is required to ensure resources are adequate to undertake this vital role within Council and is included in the annual budget. COMMUNITY CONSULTATION A public consultation process of the Annual Budget and Business Plan will be undertaken in May/June 2015. 7.1.5 INTERNAL FINANCIAL CONTROLS COMPLIANCE REPORT INTRODUCTION Update on internal financial control work performed since last Audit Committee meeting. Still working through financial policies and supporting processes. MOVED Mr Heuzenroeder that the report on Internal Financial Controls Compliance be received. Seconded Cr Milne CARRIED

COMMENT In working towards our first audit and auditor opinion on our internal financial controls in the 2015/2016 year we are continuing on focusing on documenting our financial processes and ensuring there are the appropriate controls in place to mitigate any risk around those financial processes. Policies Following is a list of the Financial Policies and their status: Policy Name Date Approved Next Review

Date

Audit Committee - Minutes of meeting held 5 February 2015 Page

11

Asset Accounting Policy 27/6/13 1/6/16 Budget and Business Plan and Review Policy 10/9/14 10/9/17 Community Assistance Scheme Policy 16/10/12 1/6/15 Debt Recovery Policy New Policy Disposal of Land and Other Assets Policy 10/9/14 10/9/18 Funding Policy 20/10/09 31/10/12 Investment Policy 15/6/10 1/5/12 Procurement Policy 24/6/14 30/6/16 Prudential Management Policy 15/7/14 15/7/17 Rates Hardship Policy 21/6/11 31/10/12 Remission and Postponement of Fines / Interest Policy New Policy Strategic Rating Policy 17/2/09 30/6/12 Treasury Management Policy 20/10/09 31/10/12 Those policies which are in bold are under current review or are new policies being worked on. These will be forwarded to the Audit Committee as they become available. ControlTrack As reported previously, we have completed our first self-assessment cycle (2013 – Internal Controls First Assessment) of the ‘core’ controls which are contained in the ‘Better Practice Model’. We have tested 194 core controls in our first assessment cycle in which 121 action plans were developed to enhance those controls. Our second self-assessment cycle (2014 – Internal Control Assessment) has commenced, and the results from that cycle will be compared to the initial one with the results again being reported back to the Audit Committee. We have now opted to have our own ‘individual control library’ within ControlTrack instead of staying with the standard ‘shared library’. This will give us the flexibility to tailor the current risks and controls or add additional ones to suit our own operations. We are also looking to extend the use of ControlTrack to the broader Council risk management. Officers are meeting with ControlTrack in early February to initiate the library separation and expand on the organisational risk side of the tool. Risk Assessments The assessment of any financial risks are now being carried out in ControlTrack. Within ControlTrack there is the ability to track the inherent, target and residual risk assessments for each risk. These risks are then mitigated by the controls which are self-assessed within the ControlTrack system. The inherent risk is completed to indicate the severity of the risk should there be no controls in place. The target risk assessment is completed to indicate where we would like to be – should all appropriate controls be in place and effective. During the ‘review’ phase of the Control Self-Assessment Cycle the residual risk assessment is completed indicating the level of risk Council is exposed to with the effectiveness of the controls that are in place.

Audit Committee - Minutes of meeting held 5 February 2015 Page

12

LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 – Section 125, 126, 129 (1) (b) Local Government Financial Management (Regulations) 2011, 14(e) Council Strategic Plan Governance and Organisation – Strategy 4.1 : Responsibility. Governance and Organisation – Strategy 4.3 : Systems FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS The regular monitoring and review of Council’s financial internal controls and risk assessments will significantly facilitate the on-going safeguarding of Council assets. The control and review of risks is a core officer function and responsibility. The introduction of the new system supports officers by providing a consistent framework and process. COMMUNITY CONSULTATION Not required under legislation or Council’s Public Consultation Policy. ACTIONS: • Outstanding policies to be presented at the next Audit Committee meeting for review • Officers to provide a demonstration of how Control Track works at the next Audit

Committee meeting.. 7.1.6 REVIEW DRAFT BUDGET 2015-16 AND ANNUAL REVIEW LONG TERM FINANCIAL PLAN INDEXATION AND ASSUMPTIONS INTRODUCTION As per the 2015-16 Annual Budget/Business Plan timetable endorsed by Council in January 2015, the Audit Committee needs to consider and provide comment on the indexation and assumptions for the Annual Budget & Business Plan (AB&BP) 2015-16 and Long Term Financial Plan (LTFP) 2015-16 to 2024-25. MOVED Cr Miller that the Audit Committee notes the indexation and assumptions for the Annual Budget & Business Plan 2015-16 and Long Term Financial Plan (LTFP) 2015-16 to 2024-25. Seconded Mr Heuzenroeder CARRIED Overview The review of indexing and assumptions for the Annual Budget & Business Plan 2015-16 and Long Term Financial Plan (LTFP) 2015-16 to 2024-25 will be considered by Council at the information briefing Workshop on 4 February 2015. This process enables Council to take a long term view and ‘set the big picture’ before starting the annual budget process. A copy of the Council Workshop presentation and background reading papers were provided to the Audit Committee. Key Assumptions & Enhancements

Audit Committee - Minutes of meeting held 5 February 2015 Page

13

Each annual review process provides an opportunity to introduce new assumptions or enhance the information base as required, using the existing indexation and assumptions. The main assumptions and indexation being considered during this early stage of budget preparation is the income and expenditure indexation. As included in the presentation paper, Council reviews the proposed rate increase and the indexation application to operational expenditure. The LGPI (Local Government Price Index) is used as a base for the plan(s) and considering local needs and requirements to meet service levels, including external influences such as service contracts where fuel prices and employment costs may vary the service cost. The Local Government Price Index (LGPI) increase for 12 months to 30 June 2014 was 2.3% 30 September 2014 was 2.0%; (noting the Adelaide CPI for the 31 December period was 1.7%). Income Rate increases to fund and ensure service level provision is maintained in line with revised sustainability requirements. The adopted General Rate Revenue indexation rates in the LTFP from last year were split in previous years into Residential and Non-residential rates. From next year both the Residential and Non-residential rate revenue were budgeted to increase at 4.50% in 2015-16, 5% in 2016-17, 4.5% for two years then 3.5% per annum thereafter. The adopted Waste Service Rate Revenue indexation rates in the LTFP from last year was budgeted to increase at 5.0% in 2015-16, 6.5% in 2016-17 and 2017-18, 6.0% in 2018-19 then 4.5% for the next 3 years and then 4.0% and the last year at 3.5%. The adopted Community Wastewater Management Systems Service Rate Revenue indexation rates in the LTFP from last year was budgeted to increase at 2.0% in 2015-16, 2.5% in 2016-17, 3.5% in 2017-18 and then 4.0% per annum thereafter. A review of the service charge is underway following requirements from ESCOSA to now include cost of Capital into the annual operating cost. Other income indexation has a base increase of 2.0%. Expenditure Operating expenditure indexation will be assessed individually for internal and external factors as follows:

• employee costs at the enterprise bargaining agreements scheduled to increase at 3.5%;

• Contractors and materials have a base increase of 2.0%; the default indexation for expenditure;

• selected operating costs have been isolated as increases to these are unique eg. power 6%, water 2%, insurance TBA%, waste collection TBA% all plus changes to service provision, ie. increased number of services provided or usage

Audit Committee - Minutes of meeting held 5 February 2015 Page

14

Long term plans for Capital expenditure will be reassessed; ensuring funding is allocated for renewal and replacement assets along with an allowance for new discretionary projects. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 – Section 122 Council Policy Annual Budget/Business Plan Policy Council Strategic Plan Strategy 4.1: Responsibility FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Long-term financial planning is an iterative process - it occurs on a regular basis and experience suggests that it will take many attempts to ‘get it right’. As new information is included in the planning process – from the latest advice on interest rates to information from the community on expected service standards – the plans are discussed, reviewed and fine-tuned. Each annual review process provides an opportunity to introduce new assumptions or enhance the information base as required. COMMUNITY CONSULTATION A public consultation process of the Annual Budget and Business Plan will be undertaken in May/June 2015. 7.1.7 PROGRESS REPORT – RISK MANAGEMENT MOVED Mr Heuzenroeder that the progress report on risk management be received. Seconded Cr Miller CARRIED Risk Management Framework The draft Risk Policy is still in its consultation period. Current work on risk facets including land use agreements, insurance requirement reviews and procurement which are all currently adding to the Risk Management Framework. ControlTrack Council has now purchased an extension of the “ControlTrack” Program currently used by the Finance team. Council’s broader Strategic and Organisational risks are to be identified in ControlTrack and a set of controls developed to mitigate those risks. Meeting set for February will start the import of The Barossa Council risk data, including internal controls, control owners and reviewers, into the new system. This will be achieved by separating the Council’s control library from the shared SALGFMG control library and setting up additional sets of control activities. Mutual Liability Claims

Audit Committee - Minutes of meeting held 5 February 2015 Page

15

The status hearing for the McCrystal Claim, that names The Barossa Council as the third defendant in a negligence claim, was set down for January 15th 2015 but has now been postponed to March 12th at the second defendant’s request. WorkCover has now issued a separate summons against the Council as the third defendant in the same case, stating “The third defendant, its servants or agents, were negligent and/or in breach of duty of care”. The WorkCover proceedings will be stayed for 6 months to await the negotiations of the McCrystal primary action. Emergency Planning The Council’s Emergency Plan and Sub - Plans for the Nuriootpa Office, Works Depots, Libraries, Tanunda Gallery, Bushgardens and Barossa Visitor Centre are now ready for implementation. The first emergency drills are scheduled for the Tanunda and Williamstown depots in February. The Emergency Planning Committee have now finalised the purchase of six hand held two way UHF radios for use in emergency response at the Nuriootpa Office. These radios are the same make and model purchased by the Depots for use in emergency response and event management, so they can also act as back up units whilst Nuriootpa Office is closed. Business Continuity Plan After several extensions of the review period, to allow for the completion of outstanding business impact assessments, the majority of these documents have now been received. Work is now underway on compiling and updating Council’s Business Continuity Plan (BCP) and the subordinate Business Unit Recovery Sub Plans. External Audits and Rebates This year’s LGAMLS Risk Review will be undertaken in the next several months. Some of the areas that require work to close out last year’s corrective actions include Tree Management Policy and Guideline development and further implementation of the Volunteer Management Framework across the Organisation. WHS Plan and WHS Management System With the finalisation of the current group of WHS Management System documents a new schedule has been developed for further processes identified through recent task risk assessments. The new processes are progressing with the Vehicle and Driver Safety Process being worked on in conjunction with the Councils Vehicle Policy. The Asbestos Management Process is now in its early draft stage with discussions being held with Council’s Manager - Asset & Infrastructure around the development of an Asbestos Management Plan and relocating the current Asbestos Register into council’s asset management program “Conquest”. The recently reviewed Training and Professional Development Policy and Training Request and Needs Analysis Process are through the consultation phase and have now been signed off by CMT. ACTIONS: • Draft Risk Management Framework to be put on the agenda for next Audit

Committee meeting

Audit Committee - Minutes of meeting held 5 February 2015 Page

16

8. OTHER

8.1 AUDIT COMMITTEE ACTION TRACKING MOVED Cr Angas that the progress report on risk management be received. Seconded Cr Milne CARRIED 9. ANY OTHER BUSINESS Nil. 10. NEXT MEETING To be advised. 11. CLOSURE There being no further business, Mr Brass closed the meeting at 1:40 pm.

Confirmed:

Chairman: ...................................... Date: .............................

AUDIT COMMITTEE

REPORTS FOR INFORMATION

24 JUNE 2015 CONSENSUS AGENDA 6.1 REPORTS FOR INFORMATION 6.1.1 REVIEW OF DELEGATIONS

Annual Review The Barossa Council’s Delegations Register (“the Register”) is reviewed: (1) annually in accordance with Section 44(6) of the Local Government Act

1999 (“the Act”), and (2) by way of best practice quarterly and amended if the Local Government Association’s Quarterly Reviews recommend that amended Instruments of Delegation be immediately adopted.

Please find attached (Attachment 1) an extract of the minutes of the Council meeting held on the 17 March 2015, detailing the various resolutions required by the annual review of delegations. Copies of the Instruments of Delegation where amendments were required, as well as Instruments of Delegation where no changes were made are available to Members of the Audit Committee if requested. Due to the file size they have not been included as a part of this report.

Subsequent Review A more recent review of Council’s by-laws and delegations identified a need to review and update the delegation of Council’s powers and functions afforded in the following by-laws:

• Permits and Penalties By-law 2013 • Moveable Signs By-law 2013 • Roads By-law 2013 • Local Government Land By-law 2013 • Dogs By-law 2013 • Cats By-law 2013 • Nuisances Caused By Building Sites By-law 2013

Please find attached (Attachment 2) an extract of the minutes of the Council meeting held on the 21 April 2015 updating the delegation of Council’s powers and functions relating to these by-laws. RECOMMENDATION: That the minutes be noted.

2015/75

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

Where a referral agency has recommended refusal A land division application which involves more than 20 allotments

Of the 11 applications refused by the Panel in 2012-2014, five were non-complying, one merit residential development and six merit land divisions. Attachment: Amended policy showing the proposed changes. Note: A separate report is being presented to Council regarding the annual review of all delegations. That review has highlighted several changes to delegations to the Panel however they do not relate to the Development Plan Consent Delegation Policy. The changes to the policy will be reflected in sub-delegations by the Chief Executive Officer to staff. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Development Act 1993 Council Strategic Plan 3.5 Planning & Building 4.2 Service 4.3 Systems FINANCIAL AND RISK MANAGEMENT CONSIDERATIONS The ability for staff to refuse certain development applications will create efficiencies and may require fewer meetings of the Development Assessment Panel. The requirement for recommendations to be counter signing by senior management will ensure a legitimate and rigorous process is followed prior to a decision being made to refuse a proposal. COMMUNITY CONSULTATION There is no requirement to undergo consultation in respect to the review of the Development Plan Consent Delegation Policy. 7.3.1.2 ANNUAL REVIEW OF DELEGATIONS

MOVED Cr de Vries

1. Annual Review That the Council has reviewed its delegations for the time being in force, in accordance with Section 44 of the Local Government Act 1999 and has resolved in the terms set out herein with respect to that review.

2. Revocations That having delegated powers and functions to the Chief Executive Officer of the Council on the 18th day of March 2014 under the:

(i) Development Act 1993, Development (Development Plans) Amendment Act 2006 and Development Regulations 2008 (ii) Local Government Act 1999 (iii) Residential Parks Act 2007 (iv) Road Traffic Act 1961 (SA), Road Traffic (Miscellaneous)

Regulations 2014 and Road Traffic (Road Rules – Ancillary and Miscellaneous Provisions) Regulations 2014 the Council hereby revokes this 17th day of March 2015 delegations of those powers and functions under the following Acts set out below made to the Chief Executive Officer of the Council on the 18th day of March 2014:

(i) Development Act 1993, Development (Development Plans) Amendment Act 2006 and Development Regulations 2008:

EXTRACT FROM MINUTES

2015/76

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

the power pursuant to Development Regulation 78(4)(d) for building rules regarding bushfire prone areas

(ii) Local Government Act 1999: - the power pursuant to section 302B regarding

Whistleblowing (iii) Residential Parks Act 2007:

- the entire Instrument of Delegation (iv) Road Traffic Act 1961 (SA), Road Traffic (Miscellaneous)

Regulations 2014 and Road Traffic (Road Rules – Ancillary and Miscellaneous Provisions) Regulations 2014:

- the powers pursuant to Regulation 6B regarding Event Management Plan and Regulation 14 regarding Permit Zones.

3. Delegations under the Local Government Act 1999 The Council, in exercise of the power contained in Section 44 of the Local Government Act 1999, hereby delegates to the person occupying the office of Chief Executive Officer this 17th day of March 2015, the powers and functions under the following Acts set out below subject to any conditions and/or limitations set out below:

(i) Local Government Act 1999: - the power pursuant to section 302B regarding Whistleblowing

(ii) Residential Parks Act 2007: - the entire Instrument of Delegation

(iii) Road Traffic Act 1961 (SA), Road Traffic (Miscellaneous) Regulations 2014 and Road Traffic (Road Rules – Ancillary and Miscellaneous Provisions) Regulations 2014: - the powers pursuant to Regulation 6 regarding Event Management Plan and Regulation 17 regarding Permit Zones.

4. Delegations under the Development Act 1993

4.1 The Council, in exercise of the power contained in Section 20 and 34(23) of the Development Act 1993 hereby delegates to the person occupying the office of Chief Executive Officer this 17th day of March 2015, the powers and functions under the Development Regulations 2008 set out below subject to any conditions and/or limitations set out below:

- Regulation 47A regarding Minor Variation of Development Authorisation

- Regulation 76D(4a) regarding Swimming Pool Safety

4.2 The Council, in exercise of the power contained in Section 20 and 34(23) of the Development Act 1993 hereby delegates to the Development Assessment Panel this 17th day of March 2015, the powers and functions under the Development Act 1993, and Development Regulations 2008 set out below subject to any conditions and/or limitations set out below:

- Section 34(1a) of the Development Act regarding provision of report to the Development Assessment Commission

EXTRACT FROM MINUTES

2015/77

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

Regulation 74 of the Development Regulations regarding determination of Development Assessment Commission as a Relevant Authority.

5. Authorisations for financial signatories 5.1 To reflect changes in staff members’ roles, Council hereby updates the signatory authorisations as listed on the Authorised Financial Signatory Schedule (which is in Attachment 1 at Appendix 23 and is distributed under separate cover).

5.2 That the Chief Executive Officer may review, alter or add financial signatories from time to time.

6. Instruments of Delegation That the Instruments of Delegation as set out at Attachment 1 of this Report dated 17th day of March 2015 under the:

Development Act 1993, Development (Development Plans) Amendment Act 2006 and Development Regulations 2008 Local Government Act 1999 Residential Parks Act 2007 Road Traffic Act 1961 (SA), Road Traffic (Miscellaneous) Regulations 2014 and Road Traffic (Road Rules – Ancillary and Miscellaneous Provisions) Regulations 2014 Authorised Financial Signatories Schedule

be amended in accordance with this resolution. Seconded Cr Harms CARRIED 2014-18/196 INTRODUCTION The Barossa Council’s Delegations Register (“the Register”) is reviewed: (1) annually in accordance with Section 44(6) of the Local Government Act 1999 (“the Act”), and (2) by way of best practice quarterly and amended if the Local Government Association’s Quarterly Reviews recommend that amended Instruments of Delegation be immediately adopted. For the purposes of this review, the Register is divided into two groups of Instruments of Delegation: Attachment 1 contains those Instruments of Delegation in which there have been legislative amendments and which require Council approval to delegate to the Chief Executive Officer. A summary of all amendments is in the Comments section below, and also appear by way of track changes throughout the Attachment. Attachment 2 contains those Instruments of Delegation in which there are no proposed changes, but are provided for Elected Members’ review and information. Both attachments form part of this report, but due to their size they are provided by separate cover and entitled “7.3.1.2 Attachments: Annual Review of Delegations”. Elected Members will note that the Instruments of Delegation in the Register contain both delegations and sub-delegations. The annual review of delegations before Council today deals only with the Council’s delegations. The Chief Executive Officer’s sub-delegations will be reviewed by him in a separate process. COMMENT Background to Delegations

EXTRACT FROM MINUTES

2015/78

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

Council decision-making occurs in one of two ways, when it:

sits formally as the Elected Body at a formally constituted Council meeting; and uses delegations.

Council may only exercise those powers and functions which are conferred on it by legislation. The ways in which Council may exercise its powers and functions are:

when the Council itself exercises the power/function; and where the legislation enables it, a power or function may be delegated pursuant to an Instrument

of Delegation and exercised in the name of a delegate.

Used well, delegations can greatly assist Council by enabling the Elected Body to progress with the strategic/policy element of local government and leave the day-to-day operations and administration of the Council to the staff who have the relevant expertise and experience to deal with such matters thus improving effectiveness and efficiency.

Delegations can range from signing contracts which commit the Council to significant expenditure (in line with approved budgets) to approving development applications and issuing enforcement notices. Accordingly, it is essential to good governance that the Council fully and carefully considers the delegations it proposes to make and demonstrates it has turned its mind to the issue. Process Improvement for Delegations

Council’s past process for the annual Delegations Review was to review, revoke and reissue all the Instruments of Delegation that comprise the Delegations Register, in order to show that the Elected Body had considered each power it delegated to its Chief Executive Officer and others. This process was in accordance with the LGA’s recommendations for transparency, but was beyond what was required in the Act, which called simply to “review”. The administration of the Register has become burdensome due to:

the increasing number of Instruments of Delegation, and the practice of reviewing, revoking and reissuing all Instruments, which then also requires a

review, revoke and reissue of the all sub-delegations to over 70 officers.

Legal advice supports a change in process to further improve administrative efficiency and it is that the Elected Body:

continue to annually review the entire Register in accordance with Section 44(6) of the Act; and only revoke and adopt changes to the relevant power if there was an amendment to the

Instrument of Delegation, which has occurred either due to a legislative change, or if the Elected Body revoked an existing delegation. This means the entire Instrument does not have to be revoked and reissued.

Dates of delegation for each power would continue to be recorded in the Register for transparency and accountability.

Summary of Amendments in Attachment 1

Local Government Act 1999 (Attachment 1 – Appendix 13) Page 85: updated reference to Local Government (General) Regulations 2013 in accordance with legislative amendment.

Road Traffic Act 1961 (Attachment 1 – Appendix 17) Pages 4-5: updated references to Road Traffic (Miscellaneous) Regulations 2014 and minor renumbering in accordance with legislative amendment.

Development Act and Regulations (Attachment 1 – Appendix 18) Page 58: inclusion of new Regulation 81A regarding “minor variation of development

authorisation” – due to legislative addition Page 62: inclusion of new Regulation 94A regarding swimming pool safety – due to legislative addition

Page 63: removal of Regulation 95 regarding Building Rules Bushfire Prone Areas – due to legislative amendment

Development Act and Regulations- to the Development Assessment Panel (Attachment 1 - Appendix 18A)

For certain development proposals the Development Assessment Commission will be the relevant authority, either by default (e.g. crown development or electricity infrastructure) by regulation (e.g. certain land divisions in the Mount Lofty Ranges Watershed) or by special

EXTRACT FROM MINUTES

2015/79

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

declaration (e.g. where the Minister believes Council has a conflict of interest or the Coordinator-General declares certain projects of $3 million or more as being of State significance). In such situations Council is given opportunity to provide comments on the application to the Commission.

Currently the Development Assessment Panel only has delegation to provide comment to the

Commission in respect to crown development or electricity infrastructure, but not for other proposals. While the Chief Executive Officer has delegation which he has sub-delegated to various officers, from time to time proposals are received which delegated officers believe should be presented to the Development Assessment Panel for their independent view.

Pages 2 and 7 – inclusion of powers at sections 11.2 and 74 allows the Panel to provide the Commission with comment on relevant proposals when necessary.

Residential Parks Act 2007 (Attachment 1 – Appendix 22)

This Instrument has been subject to comprehensive review and updated legal advice. Delegations of powers or functions have been retained. Specific references to delegation of statutory duties under the Residential Parks Act 2007 have been removed as they are legal obligations distinct from the operation of a particular function. A tracked changes copy is available upon request, a clean copy is attached. Page 12 - a delegation in respect of requesting reasons from the Tribunal under section 123 of the Residential Parks Act was added.

Authorised Financial Signatories (Attachment 1 – Appendix 23)

Names updated to incorporate changes in staff roles. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 Section 44 of the Local Government Act 1999 (the LG Act) provides that:

‘A council may delegate a power or function vested or conferred under this or another Act.’

Various powers cannot be delegated, for example the power to declare a rate – see Section 40(3). In reliance on the above power, the Council is able to delegate many of its powers and functions under many pieces of legislation.

Section 44(2) of the LG Act provides that:

‘A delegation may be – (a) to a council committee; (b) to a subsidiary of the council; or (c) to an employee of the council; or (d) to the employee of the Council for the time being occupying a particular office or position; or (e) to an authorised person.’ The Council may only delegate to those persons listed in Section 44(2) of the LG Act. It is noted that the Council may not delegate a power or function to an elected member including the Mayor.

An ‘authorised person’ means a person appointed by the Council as an authorised person under the LG Act. It is noted elected members may not be appointed authorised persons under the LG Act.

Development Act 1993 Section 20 of the Development Act 1993 (the DAct) provides that: ‘(1) The Minister, the Advisory Committee, the Development Assessment Commission or another authority established under this Act, or a council, may delegate a power or function vested or conferred under this Act. (2) A delegation:

(a) may be made: (i) to a particular person or body; or (ii) to the person for the time being occupying a particular office or position; or (iii) to a subsidiary established under the Local Government Act 1999; and

EXTRACT FROM MINUTES

2015/80

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

(b) must in prescribed circumstances be made to a committee or subcommittee of the Advisory Committee or Development Assessment Commission established by the regulations; and (c) may be made subject to conditions and limitations specified in the instrument of appointment; and (d) subject to any other provision of this Act or the regulations, is revocable at will and does not derogate from the power of the delegator to act in a matter; and (e) in the case of a delegation by the Advisory Committee, the Development Assessment Commission or another authority under this Act – may continue despite a vacancy in the membership of the body. (3) A power or function delegated under this section may, if the instrument of delegation so provides, be further delegated. (4) Subject to subsection (7), a delegate must not act in any matter pursuant to the delegation in which the delegate has a direct or indirect private interest.’

Development Plan Consent – Section 34(23) There is a specific requirement on the Council to delegate its power to determine whether or not to grant development plan consent under the DAct as follows: ‘(23) A council must delegate its powers and functions as a relevant authority with respect to determining whether or not to grant development plan consent under this Act to - (a) its council development assessment panel; or (b) a person for the time being occupying a particular office or position but not including a person who is a member of the council); or (c) a regional development assessment panel (if such a delegation is consistent with the extent to which the panel may act under the provisions of the regulations constituting the panel and in addition to the operation of subsection (1)(ab)). (24) A council may, in connection with the operation of subsection (23) - (a) make a series of delegations according to classes of development; and (b) vary any delegation from time to time, but a council cannot at any time (c) act in its own right in a matter that is subject to delegation under that subsection; or (d) give a direction with respect to the exercise or performance of a power or function under the delegation.

(26) A power or function delegated under subsection (23) may be further delegated (and any such further delegation may be made subject to specified conditions and limitations, is revocable at will and will not derogate from the power of the panel or person making the delegation to act in any matter). (27) A council must - (a) establish a policy relating to the basis upon which it will make the various delegations required by subsection (23); and (b) ensure that a copy of that policy is available - (i) for inspection at the principal office of the council during ordinary office hours; and (ii) for inspection on the Internet.’ Sub-delegation Section 44(4) LG Act relates to sub-delegation and provides that: ‘(4) A delegation - (a) is subject to conditions and limitations determined by the council or specified by the regulations; and (b) if made to the chief executive officer authorises the sub-delegation of the delegated power or function unless the council directs otherwise and if made to anyone else authorises the sub-delegation of the delegated power or function with the approval of the council; and (c) is revocable at will and does not prevent the council from acting in a matter.’

EXTRACT FROM MINUTES

2015/81

The Barossa Council Minutes of Council Meeting held on Tuesday 17 March 2015

Strategic Plan: 4. Governance and Organisation – 4.3 Systems: We are committed to ensuring the Systems and Processes of Council support the organisation in delivering the best possible services to our community in an open and transparent manner. FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Failure to conduct an annual review will result in non-compliance with legislation, as an annual review (once in every financial year) is required under section 44(6) of the Local Government Act 1999. The risk of having ineffective or invalid delegations is minimised as the delegations being considered have been recommended by Norman Waterhouse Lawyers (which prepared the Instruments for the LGA) and Wallmans Lawyers which prepared the Residential Parks Act 2007 Instrument. It is imperative that delegations are validly made as consequences of ineffective or invalid delegations include:

the exercise of power may fail – ie the decision made may be liable to being overturned by a court

the cost of a successful challenge to a decision made without lawful delegation will likely be borne by the Council

where the unlawful exercise of the power has caused loss or damage the Council may be liable for such loss or damage.

COMMUNITY CONSULTATION There is no legislative requirement to consult the community in this situation, nor, in officers’ opinions, do the particular circumstances require it as the delegations themselves are based on prescribed LGA templates where there is no option for amendment through community feedback. For transparency, the community has access to the delegations register on Council’s website so is made aware of the powers of the CEO as delegated by the Council, and also the powers of officers as sub-delegated by the CEO. 7.3.2 FINANCE - DEBATE 7.3.2.1 MONTHLY FINANCE REPORT (AS AT 28 FEBRUARY 2015) B411 MOVED Cr Boothby that the Monthly Finance Report as at 28 February 2015 be received and noted. Seconded Cr Miller CARRIED 2014-18/197 INTRODUCTION The Monthly Finance Report (as at 28 February 2015) was provided with the agenda for this meeting. COMMENT The Uniform Presentation of Financials report provides information as to the financial position of Council, including notes on material financial trends and transactions. The report has been prepared comparing actuals to the Original 2014/15 Budget and incorporating the adopted Revised Budgets for September and December 2014. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Local Government (Financial Management) Regulations 2011 - Reg 9(1)(b) LGA Information paper no. 25 – Monitoring Council Budget Performance FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS To enable Council to make effective and strategic financial decisions, a regular up to date high level financial report is provided.

EXTRACT FROM MINUTES

2015/108

The Barossa Council Minutes of Council Meeting held on Tuesday 21 April 2015

The Board is now seeking Council approval to pay a Remuneration Fee to Independent members of the NCPA Audit Committee. Pending approval of the proposed Remuneration Fee, the Board will continue to seek to appoint Independent Members. It is understood that a previous Independent Member of the NCPA Audit Committee has now indicated an interest again serving on the Committee. Upon request of the NCPA the unsuccessful nominees for the Independent Member positions on Council’s Audit Committee have been contacted by Council Officers and the contact details of those who expressed an interest in the independent member positions on the NCPA Audit Committee have been forwarded to the Board for consideration. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999, Local Government (Financial Management) Regulations 2011 Policy Charter Nuriootpa Centennial Park Authority Council Strategic Plan 1.3 Recreation 2.1 Tourism 2.2 Business and industry FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Financial Costs associated with the operation of NCPA;s Audit Committee will be included within NCPA’s 2015/2016 draft budget. Resource As per Clause 38.2.1 of the NCPA Charter, a senior officer(s) of the Council designated by the Chief Executive Officer of the Council will attend Audit Committee meetings in a non-voting capacity – the Director Corporate and Community Services has been appointed in this role. Risk Management The NCPA is legislatively required to have an Audit Committee under Schedule 2 Clause 13(4) of the Local Government Act. COMMUNITY CONSULTATION None required. 7.3.1.4 DELEGATED POWERS UNDER BY-LAWS B2743 MOVED Cr Boothby that: (1) In exercise of the powers contained in Section 44 of the Local Government Act 1999 the powers and functions under the following by-laws and specified in the proposed Instruments of Delegation contained in the annexure to this report marked Attachment 2, are hereby delegated this 21st day of April 2015 by Council to the person occupying the office of the Chief Executive Officer (and anyone acting in that position), subject to the conditions or limitations (if any) specified in the proposed Instruments of Delegation: Permits and Penalties By-law 2013 Moveable Signs By-law 2013

EXTRACT OF MINUTES

2015/109

The Barossa Council Minutes of Council Meeting held on Tuesday 21 April 2015

Roads By-law 2013 Local Government Land By-law 2013 Dogs By-law 2013 Cats By-law 2013 Nuisances Caused By Building Sites By-law 2013 (2) In accordance with sections 44 and 101 of the Local Government Act 1999, the

Chief Executive Officer is authorised to sub-delegate these powers and functions to an officer or officers of Council as the Chief Executive Officer sees fit, provided that any sub-delegation shall be subject to the same conditions and limitations (if any) as are specified in the proposed Instruments of Delegation.

Seconded Cr Hurn CARRIED 2014-18/230 INTRODUCTION On 17 December 2013, The Barossa Council endorsed a suite of seven by-laws which came into effect on 9 May 2014. A recent review of Council’s by-laws and delegations has identified a need to review and update the delegation of Council’s powers and functions afforded in these by-laws. COMMENT Council has had by-laws in place for many years as they provide a valuable tool to assist officers in regulating and resolving a range of matters at a local level which may otherwise be unable to be dealt with through existing primary legislation. At Council’s 17 December 2013 meeting, the following seven by-laws were approved in accordance with the Local Government Act 1999 (‘the Act’). By-Law #1 Permits and Penalties Purpose: A by-law to repeal by-laws, provide for a permit system and continuing penalties in Council by-laws and to clarify the construction of such by-laws. By-Law #2 Moveable Signs Purpose: To protect visual amenity and public safety on roads and footpaths by setting standards for moveable signs and regulating their placement in a manner which recognises the advertising needs of businesses to maximise economic viability. By-Law #3 Roads Purpose For the management, control and regulation of activities on roads in the Council’s area. By-Law #4 Local Government Land Purpose For the management and regulation of the use and access to local government land vested in or under the control of the Council, including the prohibition and regulation of particular activities on local government land. By-Law #5 Dogs Purpose For the Management and control of dogs within the Council’s area and to limit the number of dogs kept in premises. By-Law #6 Cats Purpose To limit the number of cats that can be kept on premises and to provide for the control and management of cats in the Council’s area.

EXTRACT OF MINUTES

2015/110

The Barossa Council Minutes of Council Meeting held on Tuesday 21 April 2015

By-Law #7 Nuisance Caused by Building Sites Purpose To prevent and suppress certain kinds of nuisance caused by rubbish escaping from land on which building work is being undertaken. These by-laws were Gazetted on 9 January 2014 and in accordance with section 249(5) of the Local Government Act 1999 (“the Act”), came into operation four months later on 9 May 2014. Opportunity now presents to appropriately empower the Chief Executive Officer who will sub-delegate to relevant officers to assist them in accordance with their day-to-day duties. Without this delegation, such matters would otherwise need to be presented to Council for approval. LEGISLATION/POLICY/COUNCIL STRATEGIC PLAN Legislation Local Government Act 1999 The Barossa Council By-laws 2013 By-Law #1 Permits and Penalties By-Law #2 Moveable Signs By-Law #3 Roads By-Law #4 Local Government Land By-Law #5 Dogs By-Law #6 Cats By-Law #7 Nuisance Caused by Building Sites FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Financial There are no additional financial implications of these delegations as the officers nominated would exercise the powers and functions as part of their regular duties. Resource There are no additional resource implications. In fact, the delegation of these powers will reduce the time required for the Elected Body to otherwise have to deal with issues arising under the By-laws. Risk Management Risk is managed by ensuring the delegates are aware of their powers through Instruments of Sub-delegation. COMMUNITY CONSULTATION There is no legislative requirement to consult the community in this situation, nor, in officers’ opinions, do the particular circumstances require it as the powers that are available to the delegate are limited within the By-laws themselves. For transparency, the Delegations Register is a public document through which the public can be made aware of the names, powers and functions of the delegates should they wish. 7.3.2 DEBATE AGENDA - FINANCE 7.3.2.1 MONTHLY FINANCE REPORT (AS AT 31 MARCH 2015) B411 MOVED Cr Miller that the Monthly Finance Report as at 31 March 2015 be received and noted. Seconded Cr Seager CARRIED 2014-18/231

EXTRACT OF MINUTES

AUDIT COMMITTEE

REPORTS FOR INFORMATION

24 JUNE 2015 6.1.2 RISK MANAGEMENT REPORT Risk Management Framework Example risk appetite statements have been presented at the June 11th Council Workshop. Development of a Risk Implementation Flowchart has provided an educational tool to help inform management and staff of how risk management impacts on Council operations. The corporate risk register has been migrated to the new council intranet site and workflow testing is now underway. Review of the risk register by Directorate has started. Corporate and Community Services has started the sorting of risk Types and Categories. ControlTrack The ControlTrack project has been progressing with linkages to the LGA Better Practice Model Study and alignment of risk categories and business practices to the developing risk register and draft risk process. Work planned to be carried out with ControlTrack for February this year did not occur due to a hold up with the new ControlTrack IT platform being developed. The library of controls and risks relating to the existing Internal Financial Control data for Barossa Council within ControlTrack has now been separated from the ‘shared’ library. This enables us to add and change existing controls and risks outside the set ‘shared’ library. No further setup of additional sets of control activities and risks has been undertaken as yet and this is being delayed now until the release of the updated ControlTrack platform (anticipated by mid-August 2015). Mutual Liability Claims The 2015 review of Mutual Liability Claims has seen a continuing reduction in the total number of claims against Council. To account for the Statute of Limitations on claims, the report runs over a five year period with a total of 76 claims in this period with 12 claims still unresolved. There has been a steady decline in claim numbers since 2012 (19) to 2015 (6) which may be a reflection on improved proactivity from Councils Works & Engineering Directorate in particular. LGAMLS - Risk Review 2015 The 2015 Risk Review has been completed this month with an unofficial result of 92% compliance. Areas of concern included: Councils Tree and Vegetation Management Framework and requirements for Business Continuity Plan testing scenarios to be undertaken (see Business Continuity Plan below). Emergency Planning The 2015 emergency drill has been successfully completed for the Tanunda Depot with several issues being identified during the fire scenario. Emergency shut off switches required for the fuel store and audibility of the emergency alarm were two requirements to be actioned.

Business Continuity Plan (BCP) After several extensions of the review period, to allow for the completion of outstanding business impact assessments, all impact assessment documents have now been returned. Work is now underway on compiling and updating BCP and the subordinate Business Unit Recovery Sub Plans and instigating a meeting with members of the Business Continuity Working Party. Scenario testing (as per LGAMLS risk review gaps) will need to be scheduled as part of the process. External Audits and Rebates The 2015 LGRWCS Rebate and KPI audit results were the best results achieved by Council to Date with 100% rebate score coming from the results of the 2014 KPI Audit and WorkCover Review combination. WHS Plan and Risk Management System With the finalisation of the current group of WHS Management System documents a new schedule has been developed for further processes identified through recent task risk assessments. The new processes are progressing with the Vehicle and Driver Safety Process being finalised in conjunction with the Councils Vehicle Policy and Councils Safe Site Policy moving into the Consultation phase. The 2015 KPI Action Plan has been submitted to LGAWCS for approval. This Plan will be the backbone of the 2015 KPI audit which will be used to determine the 2016 KPI rebate. The 2015/2017 WHS Plan and this year’s KPI Action plan have been written around the Standards 4 & 5 of the Performance Standards for Self Insurers (PSSI) being S4 Measurement and Evaluation and S5 Management Systems Review and Improvement. Barossa is the first regional council to reach this level of review. RECOMMENDATION: That the report be noted.

AUDIT COMMITTEE

REPORTS FOR INFORMATION

24 JUNE 2015 6.1.3 STRATEGIC PROJECTS FRAMEWORK The attached report is provided as an update on progress against targets and timeframes agreed following review and updating of the framework in January 2015. Both quantitative and qualitative updates have been provided for key projects spanning 2013/14-2014/15. RECOMMENDATION: That report be noted.

The Barossa Council

Strategic Projects Framework

Progress Report - 19 June 2015

Contents

INTRODUCTION .................................................................................................................. 2

FOCUS AREA 1 – MAINTAINING A CONSTRUCTIVE CULTURE ................................................... 2

FOCUS AREA 2 – BUDGET SAVINGS & EFFICIENCIES ................................................................ 4

FOCUS AREA 3 – RISK MANAGEMENT AND WORK HEALTH SAFETY .......................................... 8

FOCUS AREA 4 – BUILDING ORGANISATIONAL & COMMUNITY CAPACITY & EFFICIENCY .......... 10

FOCUS AREA 5 – SUSTAINABILITY ....................................................................................... 13

FOCUS AREA 6 – CORPORATE PLANNING ............................................................................ 16

FOCUS AREA 7 – ORGANISATIONAL IMPROVEMENT (BUSINESS EXCELLENCE) ......................... 17

FOCUS AREA 8 – PERFORMANCE MEASUREMENT & REPORTING ........................................... 20

INTRODUCTION The following report is provided as an update on progress against agreed targets and timeframes for Stage 1 (January 2013 – December 2015) and Stage 2 (January 2015 – June 2016) deliverables as detailed in the updated Strategic Projects Framework approved in January 2015. FOCUS AREA 1 – MAINTAINING A CONSTRUCTIVE CULTURE

Objectives

• Continue to develop our organisational culture by addressing relevant factors of organisational, team and individual behaviours and impacts to:

o Encourage the setting and achieving of goals o Enjoy work and produce high quality services o Support people and be open to new ideas and o Be friendly, open and sensitive.

• Generate improved staff morale and organisation culture. • Encourage flexibility within the workplace and assist in driving efficiency improvements in all

strategies outlined. Performance Results Measure Target Result Comment % shift in the culture survey results to an organisation of progressively improving achievement and self-actualising styles of operation.

10 percentile shift upward

Normed data

18 percentile shift in both

syles

(normed data

Trending above expectations by 8 percentile points.

% of constructive styles above 50th percentile.

100% 50% Two of the four constructive styles are above the 50th percentile, with the other two styles approaching the 45th percentile

% of defensive styles at or below the 49th percentile.

100% 100% All defensive styles are below the 49th percentile

Performance Outputs and Outcomes Project Status Description

Culture and Organisation Action Plan Change Champion: Chief Executive Officer Project Coordinator: Manager, Organisational Development

Phase 1 – COMPLETE Phase 2 – IN PROGRESS

The organisational culture was measured for the second time in August 2014. Results indicate partial achievement of the KPI, in that all ‘defensive’ styles are below the 50th percentile, and half of the ‘constructive’ styles above the 50th percentile. Marked movement have been made toward the 50th percentile in the remaining ‘constructive’ styles. Several actions from the initial Culture Improvement Plan have been initiated and continue: • Life Styles Inventory (LSI) support

sessions for managers are running in the Organisational Management Group meetings. Discussion includes behaviour types and development of understanding and practical application of the information provided.

• LSI opportunities are available to other members of the organisation other than OMG.

• Organisational Management Group (OMG) continues to meet fortnightly to support strategic and operational decision making and culture change agenda

• People Management Group (PMG) continues to meet quarterly for individual and group development.

• Organisational Action Plan and Team Action Plans as a result of the 2014 OCI/OEI have been developed and deployed.

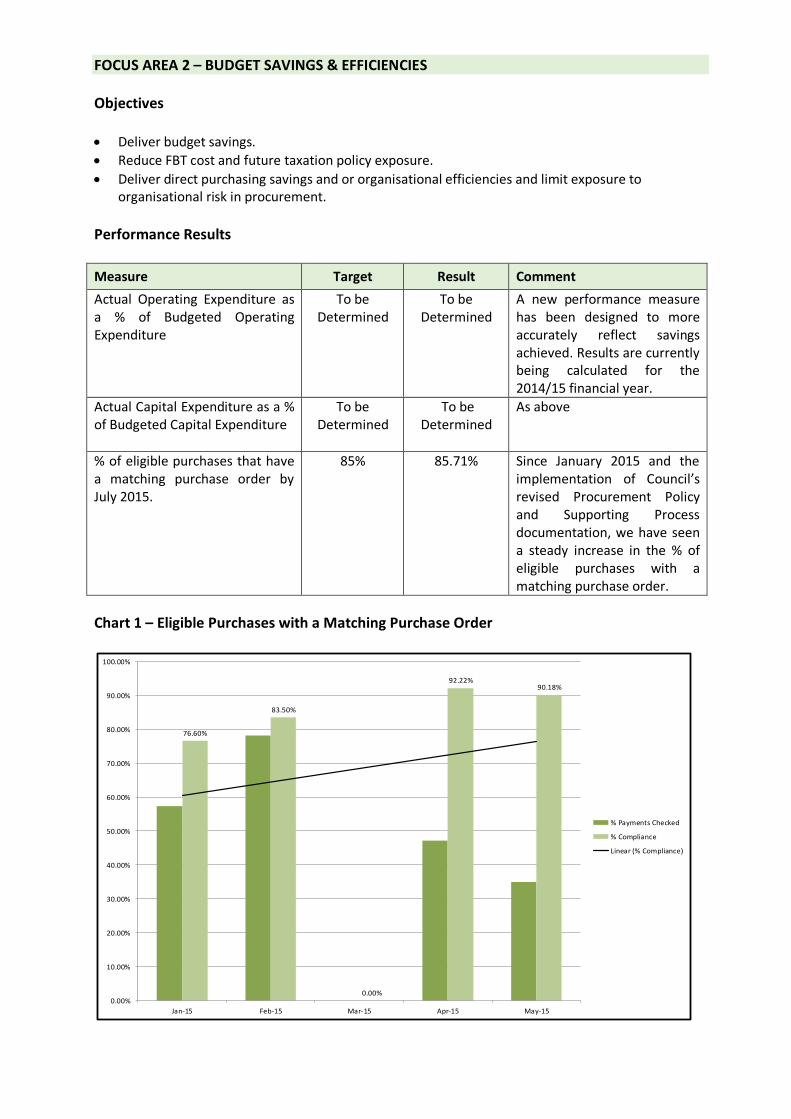

FOCUS AREA 2 – BUDGET SAVINGS & EFFICIENCIES Objectives • Deliver budget savings. • Reduce FBT cost and future taxation policy exposure. • Deliver direct purchasing savings and or organisational efficiencies and limit exposure to

organisational risk in procurement. Performance Results Measure Target Result Comment Actual Operating Expenditure as a % of Budgeted Operating Expenditure

To be Determined

To be Determined

A new performance measure has been designed to more accurately reflect savings achieved. Results are currently being calculated for the 2014/15 financial year.

Actual Capital Expenditure as a % of Budgeted Capital Expenditure

To be Determined

To be Determined

As above

% of eligible purchases that have a matching purchase order by July 2015.

85% 85.71%

Since January 2015 and the implementation of Council’s revised Procurement Policy and Supporting Process documentation, we have seen a steady increase in the % of eligible purchases with a matching purchase order.

Chart 1 – Eligible Purchases with a Matching Purchase Order

76.60%

83.50%

0.00%

92.22%90.18%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Jan-15 Feb-15 Mar-15 Apr-15 May-15

% Payments Checked

% Compliance

Linear (% Compliance)

Performance Outputs and Outcomes Project Status Description

Budget Improvement Strategy (Zero Based Budgeting, Cost Recovery, Budget Knowledge) Change Champion: Director, Corporate and Community Services Project Coordinator: Manager Financial Services

IN PROGRESS

• Approved budget for 2013/14

developed using zero based budgeting for around 40% of account lines / budget areas.

• The approved budget for 2014/15 completed zero based budgeting for 40% of residual cost centres not completed last year.

• The draft budget 2015/16 completed many of the remaining areas for the zero based budgeting.

• Budget managers reviewed business plans and updated information as required to reflect zero based cost centre activities. A major review was undertaken for the March quarter.

• In September 2014 Council adopted a Disposal of Land or Other Assets Policy and Budget and Business Plan and Review Policy providing detailed principle based guidance to staff in meeting legislative requirements for the Strategic Management Plan, the Annual Business Plan, Council’s Budget and the Long Term Financial Plan.

Contracting/Procurement Strategy Change Champion: Chief Executive Officer Project Coordinator: Manager Strategic Projects

IN PROGRESS

The Barossa Council – Internal Procurement Project • Revised Council Procurement Policy

was approved by Council in June 2014.

• Procurement Planning, Sourcing and Selection Process; Purchasing Process; and Contract and Contractor Management Process approved by CMT in January 2015.

• Tender, Contract and Contractor Registers implemented in SharePoint – currently 72 Suppliers and 49 Contracts entered in the system.

• The above registers are supported by automatic workflows to alert Contract Superintendents when Contractors mandatory documentation such as licences, insurance and induction checklists are due for renewal or contracts are

approaching their expiry. • It is anticipated that the use of the

electronic contract and contractor management systems will reduce duplication of effort in pre-qualifying and inducting suppliers and increase the sharing of information regarding the performance of our suppliers.

• Sharepoint information site launched for procurement in February 2015 as a central one-stop-shop for all information, policies, processes, advice, templates and registers associated with procurement to be presented in a user friendly, intuitive format.

• Mandatory Procurement Framework Awareness Training delivered to all staff in February 2015 – 8 sessions delivered across multiple locations.

• Procurement Framework Awareness introduced as a mandatory requirement within all staff inductions.

The Barossa Regional Procurement Group Initiative • MOU between The Barossa Council,

Light Regional Council, Mid Murray Council, The Town of Gawler and District Council of Mallala signed in September 2014.

• Barossa Regional Procurement Group Project Plan and Resource Sharing Proposal approved by all 5 Councils in December 2014.

• Joint Stationery contract implemented with all 5 Councils in December 2014 – savings estimated for Barossa Council at 18% or $2,899 p.a.

• Resource Sharing Agreement Signed between all 5 Councils in January 2015.

• Regional Procurement Project Officer recruited and commenced in March 2015.

• Standard suite of regional documents (including request for tender, contracts, tender evaluation and tender planning, CEO reporting framework) developed.

• Regional Forward Procurement Plan developed in March 2015.

• Regional Procurement email address

and preliminary branding established. • First joint Request for Tender for

Building Maintenance Services released on 1 April 2015 and closed on 15 May 2015 – was advertised throughout regional papers, on Council websites and via direct mail out to existing suppliers across the Councils. 46 Tenders were received and are currently being evaluated for development of a panel of suppliers.

• Audit Services Tender released via SA Tenders on 19 May 2015 and scheduled to close on 3 June 2015

• Road Reseal and Line Marking Tenders to be released via SA Tenders by 5 June 2015.

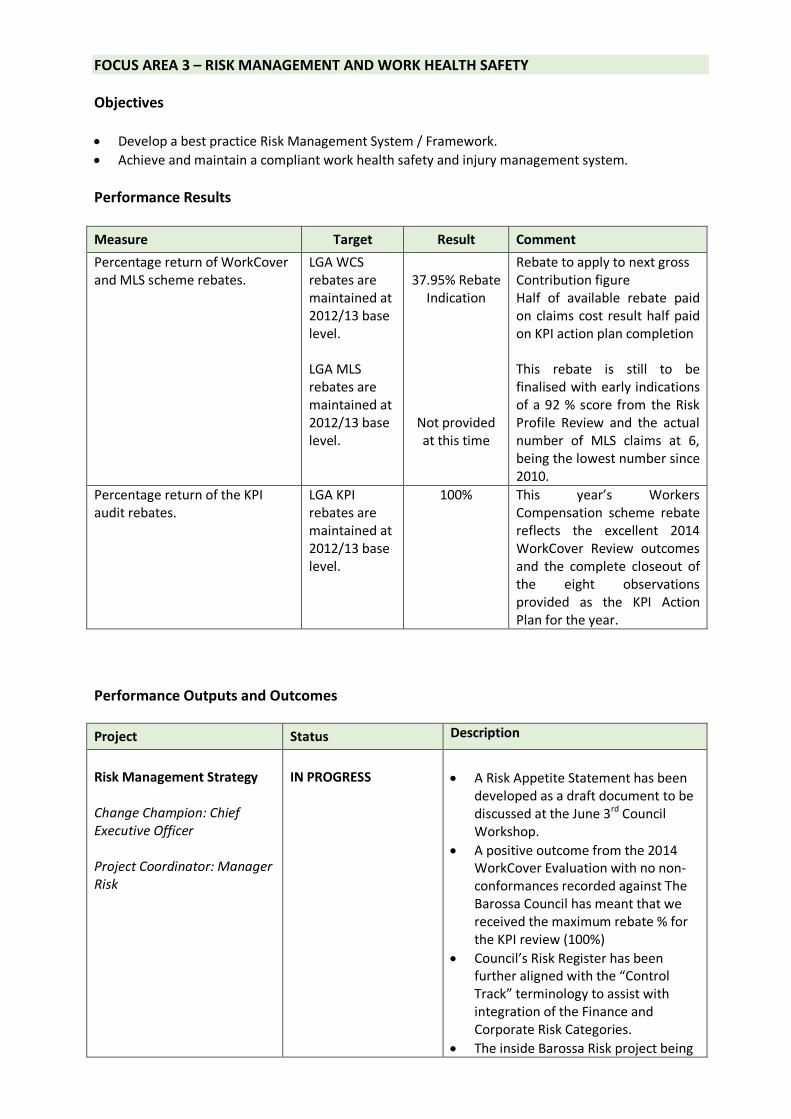

FOCUS AREA 3 – RISK MANAGEMENT AND WORK HEALTH SAFETY Objectives • Develop a best practice Risk Management System / Framework. • Achieve and maintain a compliant work health safety and injury management system. Performance Results Measure Target Result Comment Percentage return of WorkCover and MLS scheme rebates.

LGA WCS rebates are maintained at 2012/13 base level. LGA MLS rebates are maintained at 2012/13 base level.

37.95% Rebate

Indication

Not provided at this time

Rebate to apply to next gross Contribution figure Half of available rebate paid on claims cost result half paid on KPI action plan completion This rebate is still to be finalised with early indications of a 92 % score from the Risk Profile Review and the actual number of MLS claims at 6, being the lowest number since 2010.

Percentage return of the KPI audit rebates.

LGA KPI rebates are maintained at 2012/13 base level.