5hsruw - productivity commission

TRANSCRIPT

,QWHUQDWLRQDO�/LQHU&DUJR�6KLSSLQJ��$

5HYLHZ�RI�3DUW�;�RI�WKH7UDGH�3UDFWLFHV�$FW����� ,QTXLU\�5HSRUW

�������5HSRUW�1R������������6HSWHPEHU�����

Commonwealth of Australia 1999

ISBN 1 74037 030 9

This work is subject to copyright. Apart from any use as permitted under theCopyright Act 1968, the work may be reproduced in whole or in part for study ortraining purposes, subject to the inclusion of an acknowledgment of the source.Reproduction for commercial use or sale requires prior written permission fromAusInfo. Requests and inquiries concerning reproduction and rights should beaddressed to the Manager, Legislative Services, AusInfo, GPO Box 1920, Canberra,ACT, 2601.

Publications Inquiries:Media and PublicationsProductivity CommissionLocked Bag 2Collins Street EastMelbourne VIC 8003

Tel: (03) 9653 2244Fax: (03) 9653 2303Email: [email protected]

General Inquiries:Tel: (03) 9653 2100 or (02) 6240 3200

An appropriate citation for this paper is:

Productivity Commission 1999, International Liner Cargo Shipping: A Review ofPart X of the Trade Practices Act 1974, Report no. 9, AusInfo, Canberra.

The Productivity Commission

The Productivity Commission, an independent Commonwealth agency, is theGovernment’s principal review and advisory body on microeconomic policy andregulation. It conducts public inquiries and research into a broad range of economicand social issues affecting the welfare of Australians.

The Commission’s independence is underpinned by an Act of Parliament. Itsprocesses and outputs are open to public scrutiny and are driven by concern for thewellbeing of the community as a whole.

Information on the Productivity Commission, its publications and its current workprogram can be found on the World Wide Web at www.pc.gov.au or by contactingMedia and Publications on (03) 9653 2244.

0HOERXUQH�2IILFH

/HYHO��������&ROOLQV�6WUHHW0HOERXUQH��9,&������

/RFNHG�%DJ���&ROOLQV�6WUHHW�(DVW0HOERXUQH��9,&������

7HOHSKRQH ������������)DFVLPLOH ������������

&DQEHUUD�2IILFH

7HOHSKRQH ������������

15 September 1999

The Honourable Rod Kemp MPAssistant TreasurerParliament HouseCANBERRA ACT 2600

Dear Assistant Treasurer

In accordance with Section 11 of the Productivity Commission Act 1998, we have pleasurein submitting to you the report on the inquiry into International Liner Cargo Shipping: AReview of Part X of the Trade Practices Act 1974.

Yours sincerely

Dr Neil ByronPresiding Commissioner

Dr Robin StewardsonAssociate Commissioner

TERMS OFREFERENCE

V

Terms of reference

I, ROD KEMP, Assistant Treasurer, pursuant to Parts 2 and 3 of the ProductivityCommission Act 1998 and in accordance with the Government’s Legislation ReviewSchedule, refer Part X of the Trade Practices Act 1974 and associated regulations to theProductivity Commission for inquiry and report within six months of receipt of thisreference. The Commission is to hold hearings for the purpose of the inquiry.

Background

2. Part X of the Trade Practices Act 1974 is the regulatory regime for internationalliner cargo shipping operations in Australia. It describes the conditions under whichinternational liner cargo shipping operators are permitted to form conferences to providejoint liner shipping services for Australian exporters and importers.

Scope of Inquiry

3. The Commission is to report on the appropriate arrangements for regulation ofinternational cargo shipping services, taking into account the following objectives:

a) legislation/regulation should be retained only if the benefits to thecommunity as a whole outweigh the costs; and if the objectives of thelegislation/regulation cannot be achieved more efficiently through othermeans, including non-legislative approaches;

b) regard should be had to the effects on: the access of Australian exportersto competitively priced international liner cargo shipping services that areof adequate frequency and reliability; public welfare and equity; economicand regional development; consumer interests; the competitiveness ofbusiness including small business; and efficient resource allocation; and

c) the Government’s commitment to accelerate and strengthen themicro-economic reform process, including through improving thecompetitiveness of markets, particularly those which provideinfrastructure services, in order to improve Australia’s economicperformance and living standards.

4. In making assessments in relation to matters in paragraph (3), the Commission isto have regard to the analytical requirements for regulation assessment by theCommonwealth, including those set out in the Competition Principles Agreement. Thereport of the Commission should:

VI TERMS OFREFERENCE

a) identify the rationale for Part X, quantifying issues as far as reasonablypractical;

b) assess whether Part X satisfies the rationale identified in (a);

c) identify if, and to what extent, Part X restricts competition;

d) identify relevant alternatives to Part X, including the authorisationprocesses in Part VII of the Trade Practices Act 1974 and non-legislativeapproaches, and the extent to which these would achieve the rationaleidentified in (a);

e) analyse and, as far as reasonably practical, quantify the benefits, costs,impacts (including with respect to predictability of outcome on thestandards of shipping services provided), and cost effectiveness of Part Xand the alternatives identified in (d);

f) identify the liner cargo shipping regimes of Australia’s major tradingpartners and determine the compatibility of the alternatives identified in(d), and Part X, with those regimes;

g) identify the different groups likely to be affected by Part X andalternatives identified in (d);

h) list the individuals and groups consulted during the review and outlinetheir views;

i) determine a preferred option for regulation, if any, in light of objectivesset out in paragraph (3); and

j) examine possible mechanisms for increasing the overall efficiency ofPart X.

5. In undertaking this review, the Commission is to advertise nationally, consult withkey interest groups and affected parties, and publish a report.

6. The Government will consider the Commission’s recommendations and its responsewill be announced as soon as possible after the receipt of the Commission’s report.

ROD KEMP12 MARCH 1999

CONTENTS VII

Contents

Terms of reference V

Abbreviations and explanations XI

Glossary XVI

Key messages XVIII

Overview XIX

Recommendations and findings XXXIX

1 Introduction 1

1.1 Australia’s liner cargo shipping task 1

1.2 Liner shipping conferences 2

1.3 Background to the current inquiry 3

1.4 Scope of this inquiry and the Commission’s approach 5

1.5 Conduct of the inquiry 6

2 Trends in liner shipping 9

2.1 Global liner shipping market 9

2.2 Australian liner shipping market 18

3 Assessing regulation 31

3.1 Identifying the national interest 31

3.2 Role of conferences 33

3.3 Evaluation criteria 36

4 Current regulation of international liner shipping 41

4.1 Regulation of conferences in Australia 41

4.2 Objectives and key provisions of Part X 43

4.3 Rationale for current regulation 50

4.4 International regulation 51

VIII CONTENTS

4.5 International agreements 60

5 Performance of liner shipping 65

5.1 Services to Australian shippers 65

5.2 Case studies 75

6 Evaluation of Part X 87

6.1 Performance of Part X 87

6.2 Other criteria 94

6.3 Conclusion 113

7 Alternative approaches 115

7.1 Reform options 115

7.2 Authorisation 115

7.3 Block authorisation 136

7.4 Industry codes 137

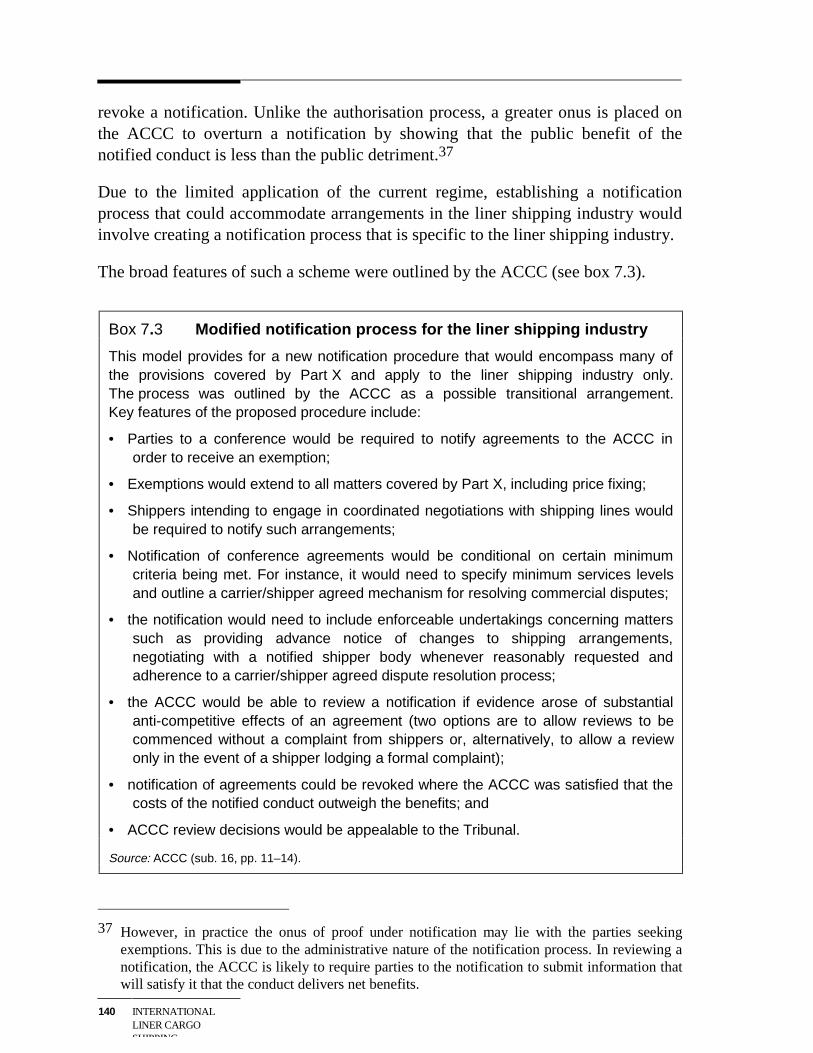

7.5 Notification 139

7.6 Conclusion 142

8 Modifications to Part X 145

8.1 Terminal handling charges 145

8.2 Intermodal or ‘door-to-door’ rates 149

8.3 Safeguards for importers 152

8.4 Regulation of discussion agreements 156

8.5 Open versus closed conferences 159

8.6 Declaration of a carrier with substantial market power 161

8.7 Discrimination between shippers 162

8.8 Australian flag shipping 164

8.9 Penalties and dispute settlement 165

8.10 Variations to the registration process 169

8.11 Funding for APSA 170

8.12 A separate shipping Act? 172

9 Appropriate regulation: the Commission’s assessment 175

A Public consultation A.1

A.1 List of submissions A.1

A.2 List of visits A.2

CONTENTS IX

A.3 Position paper public hearings - participants A.3

A.4 Participants’ views A.4

B Economic issues B.1

B.1 Role of conferences and other cooperative arrangements B.1

B.2 Shipping services and the public interest B.10

B.3 Countervailing power B.12

C Australia’s sea-freight task C.1

C.1 Liner trade by commodity group C.2

C.2 Conference trade by commodity group C.4

C.3 Liner trade by trade region C.5

C.4 Conference trade by trade region C.9

C.5 Transhipment C.12

C.6 Landbridging C.15

D Evaluation of liner shipping services to Australia D.1

D.1 Service D.2

D.2 Freight rates D.20

E Container shipping cost model E.1

F Foreign shipping legislation F.1

G Case studies G.1

G.1 Australia–South-East Asia G.1

G.2 Australia–North and East Asia G.8

G.3 Australia–Europe G.16

G.4 Australia–North America G.25

References

X CONTENTS

ABBREVIATIONS ANDEXPLANATIONS

XI

Abbreviations and explanations

Abbreviations

AAA Australia–Asia Alliance Container Consortium

AAX Asia–Australia Express Container Consortium

ABC ABC Container Line

ABS Australian Bureau of Statistics

ACA Australian Consumers’ Association

ACCC Australian Competition and Consumer Commission

ACCI Australian Chamber of Commerce and Industry

ACCLA Australia–Canada Container Line Association

ACS Australian Customs Service

ACT Australian Competition Tribunal

AELA Australia to Europe Liner Association

ANLCL ANL Container Line

ANSCON Australia Northbound Shipping Conference

ANZDL Australia–New Zealand Direct Line

ANZECS Australia–New Zealand-Europe Container Service

AOTA Australia Oversea Transport Association

APL APL Lines

APSA Australian Peak Shippers’ Association

XII ABBREVIATIONS ANDEXPLANATIONS

ASA Australia–South Asia Container Consortium

ATPR Australian Trade Practices Report

AUSCLA Australia–United States Container Line Association

BAF Bunker adjustment factor

BTCE Bureau of Transport and Communications Economics

BTE Bureau of Transport Economics

CAF Currency adjustment factor

CGM Compagnie Generale Maritime

cif Cost insurance freight

CMA Compagnie Maritime D’Affretement

CP CP Ships

CPA Competition Principles Agreement

DCN Daily Commercial News

DTRS Department of Transport and Regional Services

EDI Electronic data interchange

fob Free on board

FMC Federal Maritime Commission (United States)

GATS General Agreement on Trade in Services

H&M Hull and machinery

IAC Industries Assistance Commission

IC Industry Commission

ICSD International Cargo Statistics Database

IMTL International Marine Transport Line

ABBREVIATIONS ANDEXPLANATIONS

XIII

LCSA Liner Cargo Shipping Authority

LLDCN Lloyd’s List Daily Commercial News

LSS Liner Shipping Services

MISC Malaysia International Shipping Corporation

MSC Mediterranean Shipping Company

MTC Maritime Transport Committee (United States)

NACON North American Conference

NCP National Competition Policy

NEC National Electricity Code

NEM National Electricity Market

NOL Neptune Orient Lines Ltd

NVOCC Non-vessel operating common carrier

OECD Organisation for Economic Cooperation and Development

PC Productivity Commission

pers. comm. Personal communication

P&I Protection and indemnity

P&O The Peninsular and Oriental Steam Navigation Company

PSA Prices Surveillance Authority

PSC Port service charges

R&M Repair and maintenance

ro-ro Roll-on roll-off (vessel)

TEU Twenty foot equivalent unit

TFG Trade Facilitation Group

XIV ABBREVIATIONS ANDEXPLANATIONS

THC Terminal handling charge

TPA Trade Practices Act 1974

TPC Trade Practices Commission

trans. Transcript

sub. Submission

UASC United Arab Shipping Company

UNCTAD United Nations Conference on Trade and Development

WTO World Trade Organisation

Explanations

Billion The convention used for a billion is a thousand million (109).

Findings Findings in the body of the report are paragraphs high-lighted using italics, as this is.

Recommendations Recommendations in the body of the report are high-lighted using bold italics with an outside border, as thisis.

GLOSSARY XV

Glossary

Australian flagshipping operator

An operator who is an Australian citizen or a bodycorporate incorporated by or under Commonwealth, Stateor Territory Law who provides shipping services,employing a ship that is registered in Australia.

Accord An agreement or arrangement between conference andnon-conference carriers on a trade route, resulting fromdiscussions on matters of mutual interest such as capacityand freight rates.

Bunkeradjustment factor(BAF)

An adjustment in freight rates for fluctuations in bunker(fuel) prices.

Carrier shipping line

Cartel An association of competitors that, by agreement, limitsthe degree of competition that would otherwise prevail inthe buying or selling of goods or services by members ofthe cartel.

Comity The courtesy by which a nation allows another’s laws tobe recognised within its territory.

Conference Defined in Part X as an unincorporated association of twoor more ocean carriers carrying on two or more businesseseach of which includes, or is proposed to include, theprovision of liner cargo shipping services. Conferencesmay either be ‘open’ or ‘closed’.

open conference — involves a legal entitlement for anyline to become a conference member, subject to thatshipping line satisfying conference requirements.

closed conference — where the entry of new shippinglines must be approved by existing conference members.

XVI GLOSSARY

Consortium A joint venture by members of a conference signifying ahigher degree of cooperation in service arrangements suchas the sharing of vessels under a shipping pool.

Currencyadjustment factor(CAF)

Factor applied to freight rates to adjust for fluctuations inthe exchange rate(s).

Designated peakshipper body

An association representing the interests of Australianexporters generally for the purposes of negotiations underPart X of the Trade Practices Act 1974, and so designatedby the Minister.

Designatedsecondary shipperbody

The association, designated by the Minister for thepurpose of negotiations under Part X, representing theinterests of all or any of the following:

• Australian shippers in a particular trade;

• Australian shippers of particular kinds of goods;

• shippers in a particular part of Australia;

• producers of goods of a kind exported, or proposed tobe exported, from Australia.

Discussionagreement

An agreement between conference and non-conferencelines to reach a non-binding consensus over, for example,the charging of common freight rates and a variety ofservice arrangements.

Extra-territorial Outside Australia’s territorial jurisdiction.

Intermodal Transport involving transfer between two or more modesto exploit the comparative advantages of each mode.

Landbridging The movement of containerised cargo between sea portsby road and rail rather than sea, thus enabling moreefficient utilisation of containerships.

Liner service A service prearranged on a particular trade route.

NVOCC non-vessel operating common carrier (term used in the USShipping Act of 1984).

GLOSSARY XVII

Port servicecharge

A land-based charge for statutory port costs that is passedon to the shipper by the shipping line.

Reefer refrigerated container

Ro-ro roll-on roll-off vessel

Shipper The party on whose account goods are consigned (ashipper can be an importer or an exporter, but the ‘shipperbody’ provisions in Part X relate solely to exporters).

Stevedoring The loading and unloading of ships’ cargoes. Generally,stevedoring of container vessels is carried out at acontainer terminal but general cargo wharves may beused.

Twenty footequivalent unit(TEU)

The standard ISO container measures 20 feet by 8 feet by8 feet.

Terminal handlingcharge (THC)

Container port charge levied by container lines for theservice of moving a container from a ship to a positionwithin the container terminal, enabling clearance from theport.

Transhipment Transfer of cargo from one ship to another at anintermediate port between the port of origin and port ofdestination.

XVIII KEY MESSAGES

Key messages

• As an importer of liner cargo shipping services, Australia’s national interest isserved by obtaining liner shipping services that meet shippers’ diverse needs at thelowest-possible price.

• Because transport costs and service levels directly affect their competitiveness,Australian exporters and importers have a direct interest in obtaining thebest-possible deal from foreign liner carriers. Thus pursuit of their self interest inrelation to liner shipping also serves the national interest.

• Conferences — groupings of liner carriers which coordinate services on individualtrade routes — can be an efficient way of meeting an important part of shippers’diverse demands (in terms of frequency, reliability etc). But any form of marketcooperation increases the potential for market power.

• The tension between the benefits and potential costs of conference arrangementshas led to special treatment of conferences worldwide. Part X of the TPA is anindustry-specific, legislated industry code which exempts conferences from somegeneral provisions of the TPA, provided they meet certain obligations to Australianexporters and they do not misuse any market power. Exporters also are allowed toform collective buying groups to enhance their negotiating power, backed up byregulatory intervention as they see fit.

• The current regulatory approach has promoted the national interest because Part Xallows the efficiencies of conference arrangements while letting competition fromnon-conference lines and the countervailing power of Australian exporters constraintheir potential market power.

• Repeal of Part X in favour of a potentially more interventionist approach under thegeneral (authorisation) provisions in Part VII of the TPA, is unlikely to deliver greaternet national benefits. Scope for successful intervention appears limited and,moreover, the general provisions of the TPA are likely to involve greateradministrative and compliance costs than Part X.

• While a Part X-type outcome for regulation of liner shipping could, in principle, bereplicated under Part VII (especially if block authorisation were allowed) or under aspecial notification procedure, there can be no certainty that these alternativeswould, in practice, meet the criteria as well as Part X does. Nor could they beintroduced at negligible transitional cost.

• The ultimate test for any regulation or legislation is whether it promotes the nationalinterest and does so more efficiently than alternatives. Part X passes this test.

KEY MESSAGES XIX

OVERVIEW XIX

Overview

The Commonwealth Government has asked the ProductivityCommission to review Part X of the Trade Practices Act1974 (TPA) and report on the appropriate arrangements forregulation of international liner cargo shipping services.Part X describes the conditions under which internationalliner shipping operators are permitted to cooperate as‘conferences’ to provide coordinated shipping services toAustralian exporters and importers.

This inquiry stems from the Commonwealth, State andTerritory Governments agreement of April 1995 — theCompetition Principles Agreement (CPA) under the NationalCompetition Policy. Under the CPA, Commonwealth andState Governments agreed to review all legislation whichrestricts competition, by the year 2000.

In making its assessment, the Commission is required to takeinto account three objectives:

(a) legislation/regulation should be retained only if thebenefits to the community as a whole outweigh thecosts; and if the objectives … cannot be achieved moreefficiently by other means [emphasis added];

(b) regard should be had to the effects on: the access ofAustralian exporters to competitively pricedinternational liner cargo shipping services that are ofadequate frequency and reliability; public welfare andequity; economic and regional development; consumerinterests; the competitiveness of business includingsmall business; and efficient resource allocation; and

(c) the Government’s commitment to accelerate andstrengthen the micro-economic reform process,including through the competitiveness of markets,particularly those which provide infrastructureservices …

This inquiry concernsregulation ofinternational linercargo shipping …

… it stems from theNational CompetitionPolicy legislativereview program.

Regulation should beretained only if thebenefits exceed thecosts and there is nobetter option.

XX OVERVIEW

Background

International shipping is an essential intermediate serviceinput for Australia’s merchandise trade. Around 79 per centof merchandise exports and 71 per cent of merchandiseimports (by value) were transported by sea in 1997-98.

Liner services are provided by container (includingrefrigerated container), roll-on roll-off (ro-ro) andconventional and multi-purpose ships, which operate regular,scheduled services to set timetables. In 1997-98, linerservices carried 4 per cent of the volume and 48 per cent ofthe value of Australia’s seaborne exports, and 23 per cent ofthe volume and 74 per cent of the value of Australia’sseaborne imports. Bulk shipping services carried theremainder.

Conferences, or groupings of liner shipping operators whichcoordinate services, account for more than half of linerservices on major global routes. It is estimated that in themid-1990s, conferences accounted for around 60 per cent oftotal global liner capacity. On Australian trades, conferencescurrently carry more than 50 per cent of liner exports andmore than 60 per cent of liner imports by value. However,conference shares in terms of both the volume and value ofliner cargoes have fallen since the early 1980s.Non-conference operators providing direct or transhipmentservices (that is, where containers change ships at anintermediate port) serve the remainder of the market.

Australian liner trades are described as ‘long’ and ‘thin’, aproduct of Australia’s relative isolation and the size of itseconomy. Australia is not located on the major round-the-world or northern hemisphere east–west trade routes — itsmajor trade routes run north–south. Ranked 15th in the worldin terms of container movements, the Australian coastal andinternational liner trade amounted to 2.74 million twenty footcontainer equivalents (TEU) or only 1.67 per cent of theestimated world container cargo for 1997.

Shipping is essentialfor Australia’sinternational trade.

Liner ships mainlycarry containerisedcargo and provideregular, scheduledservices.

Liner conferencescarry more than halfof Australia’s linercargo by value.

Australia is notlocated on majoreast–west shippingroutes and its linertrade volumes aresmall by worldstandards …

OVERVIEW XXI

Figure 1 Trends in Australian liner tradea

0

2

4

6

8

10

12

14

16

18

20

1988-89 1990-91 1992-93 1994-95 1996-97year

volu

me

(mill

ion

to

nn

es)

0

5

10

15

20

25

30

35

40

45

50

valu

e ($

bill

ion

) export tonnage

import tonnage

export value

import value

a A series break exists in mid-1994.

Figure 2 Conference shares of the value ofAustralia’s liner exports: key trades

20

30

40

50

60

70

80

90

1989-90 1991-92 1993-94 1995-96 1997-98

Co

nfe

ren

ce s

har

e (%

)

Japan/North Asia

South East Asia

East Asia

Europe

North America

Total

XXII OVERVIEW

Australia’s major liner exports are commodities (meat,cereals and dairy products), whereas imports are largelymanufactured goods (machinery, vehicles and chemicals).Many export cargoes require refrigeration, whereas importsgenerally do not. Not only do export tonnages exceed importtonnages, but Australia’s exports tend to be heavier per unitof volume than its imports. These differences createimbalances in container requirements between inward andoutward legs.

Major trade partners for Australian liner exports and importsare East Asia, Europe, Japan and North Asia, New Zealand,North America, and South-East Asia.

Trends in liner shipping markets

Global and Australian liner shipping markets have changedsignificantly since Part X was last reviewed in 1993,continuing a process of change initiated by containerisationin the 1960s. In line with many other industries, linershipping is becoming more concentrated via mergers andacquisitions, while average vessel size continues to grow ascarriers attempt to capture scale economies. Rationalisationis being driven by technological change and intensecompetition in most trades which has seen freight rates fallsignificantly in real terms and profitability decline.

The trend towards greater industry concentration via mergersand acquisitions does not appear to have reducedcompetition. On the contrary, it appears the expansion ofglobal shipping companies has increased competition onindividual routes — Asian lines have entered the NorthAtlantic trade, east–west lines are entering north–southmarkets and the feeder services of large carriers (especiallytranshippers) are competing with traditional regional lines.Thus conferences compete with each other, withtranshipment operators, and with independent directoperators.

… while differencesbetween imports andexports createimbalances incontainerrequirements.

International linershipping isexperiencing rapidchange …

… competition hasintensified.

OVERVIEW XXIII

Australia’s national interest

Australia relies almost entirely on foreign shipping lines forinternational liner cargo shipping services — liner cargoshipping therefore is an essential imported service.

In general, a reduction in the (inward or outward) cost ofliner shipping to Australia for a given quality of service, orimproved service for a given cost, will increase Australiannational income. This is achieved by reducing the cost ofimports to Australian consumers and users of importableinputs, and by making Australian exports more competitivein world markets.

Exporters benefit directly from lower (effective) shippingcosts in terms of the price they receive for their exportsand/or increased export sales. Importers are able to sell moregoods at lower prices to Australian customers. Therefore theinterests of Australian shippers (that is, exporters andimporters) in obtaining more efficient shipping servicesbroadly coincide with the national interest and, at least in thiscontext, serve as a good proxy for that community-wideinterest.

It is difficult to conceive of a situation, in practice, whereAustralian exporters and importers will not have an interestin obtaining a better deal from liner carriers, or where pursuitof that interest will not translate into national gains.

Role of shipping conferences

Liner shipping is characterised by a range of economies ofscale and scope suggesting that low-cost supply is likely torequire some form of industry integration and henceconcentration or cooperation. In principle, this could beachieved by a relatively small number of large globaloperators.

Australia relies onforeign liner services.

Lower shipping costsincrease nationalincome and promotethe nationalinterest …

… and Australianshippers broadlyrepresent the nationalinterest.

Low-cost provision ofliner shipping is likelyto involve industryconcentration …

XXIV OVERVIEW

However, in practice, conferences have been the preferredform of integration in liner shipping markets for over100 years. Conferences provide a looser form of cooperationthan a merged company and usually are trade specific (andmay even be limited to one direction on each route). Theymay engage in joint price setting, capacity rationalisation,revenue and/or cost pooling arrangements, discriminatorypricing structures, and customer loyalty agreements.

In contrast to bulk shipping where each vessel carries onecommodity on a charter basis, demand for liner shipping isdiverse. The costs of coordinating these diverse demandsvirtually rule out ship chartering as an efficient form ofservice delivery. On the other hand, the supply of regular,scheduled liner services provides a means of reducingtransactions costs so that shippers with diverse demands areable to access liner shipping services.

Lower costs of provision of such services require the variouseconomies of scale and scope to be captured. A singleshipping line may be loath to commit several large vessels(and incur correspondingly large fixed costs) in order toprovide a comprehensive, regular, scheduled service wheredemand is uncertain and where that uncertainty isexacerbated by the possibility of rivals encroaching on thetrade.

Cooperation with potential rivals offers a way of reducinguncertainty, although not eliminating it as liner shipping iscontestable. A lower risk premium will mean that largerships can be utilised and filled to optimal capacity (thuscapturing economies of vessel size), while a large conferencefleet may generate additional economies while providing thecoordinated, frequent scheduling valued by shippers. In thisway, conferences can provide an efficient mode of servicedelivery.

… and conferenceshave been thepreferred form ofcooperation for morethan a century.

Conferences canpromote low-costsupply of regularshipping services …

OVERVIEW XXV

Box 1 What is a liner shipping conference?

In conventional usage, a ‘conference’ is an unincorporated association between two ormore companies coordinating services on a specific trade route (either return orone-way). Members seek to rationalise their shipping schedules, arrange the vesselcapacity deployed on that route, and to set a common price to charge their customers(‘shippers’) as a device to coordinate services and minimise commercial risks. Theymay pool their revenues and costs. They may be ‘open’ (any shipping line can join orleave the conference at short notice) or ‘closed’ (membership is by invitation only).

Under Part X of the TPA, a conference is defined as any two or more companiesoffering shipping services. This therefore includes, in addition to the customary use ofthe term, consortia, alliances, slot charters, non-vessel operating common carriers(NVOCCs) and discussion agreements (in which the conference and one or morenon-conference lines discuss (but do not enter binding agreements on) schedules, portcoverage, prices and capacity management).

Not only do all major trading countries permit conferences to operate in carryingcargoes to and from their ports, but each has a system of blanket exemption orimmunity from its national competition or anti-monopoly legislation.

At the same time, however, conference structures (like acompany merger) may give shipping operators a degree ofmarket power.

The key to the impact of conferences in practice is whetherthey face effective competition or, at least, potential effectivecompetition. Given such competition, conferences will beconstrained to charge prices that do not yield excess profitsand to operate efficiently over the long run.

Conferences and competition

By definition, conferences constrain competition betweenmember lines. But it is highly unlikely that, if conferences(and other cooperative arrangements which are covered byPart X) were prohibited, equivalent levels of (coordinated)service would (or could) be provided by all formerconference members operating individually on each trade. Itis more likely that, if conferences were proscribed, carrierswould merge, thus internalising the conference, or that somelines currently operating within a conference would exit thetrade, allowing remaining providers to expand and take a

… but may giveconference membersmarket power.

The key is whetherconferences faceeffective competition.

The alternative toconferences is notperfect competitionbut other forms ofcooperation.

XXVI OVERVIEW

larger share of the trade. In other words, the economics ofliner shipping are such that there will be market cooperationand concentration in some form in order to provide theservice currently provided by conferences.

In assessing the extent of competition, the Commission hasexamined a range of indicators.

Conference shares of major inward and outward trades havedeclined over the 1990s, though some trades andcommodities have moved against this trend. Conferencescarried 64 per cent of Australia’s liner imports by value in1997-98 (compared with 73 per cent in 1989-90) and56 per cent of liner exports by value in 1997-98 (comparedwith 73 per cent in 1989-90). On very thin trades (forexample, East India–Australia) conference shares currentlyexceed 70 per cent but have exhibited considerable volatilityfrom year to year.

Overall, however, there is no trade route into or out ofAustralia in which a conference has a monopoly or close to amonopoly — in other words, shippers always have a choice(see figure 3 which illustrates available liner services on theAustralia–Europe trade). Increasing trade shares for non-conference operators reflect an improvement in the quality ofnon-conference services. This improvement has been drivenby the emergence of several large global operators in the1980s and 1990s which provide direct or transhipmentservices to Australia, usually (though not invariably)choosing to operate outside the conference system — forexample, Evergreen Lines, Maersk, COSCO, Hanjin, Fescoand MSC. This development appears consistent with amarket that is dynamic and competitive.

There are other indicators that suggest that Australia’s linertrades are contestable and subject to competitive forces.There have been numerous entries and exits on Australiantrades during the 1990s, though mergers and takeoversappear to account for major changes in carrier line-up. Thecomparatively poor profitability of many liner carriers, bothon Australian trades and globally, including conferencemembers, also is not suggestive of excess profits.

Conference shareshave declined overthe 1990s …

… reflecting theincrease in choiceavailable to shippers.

Entries and exits onAustralian trades alsosuggest freedom ofentry ...

OVERVIEW XXVII

Figure 3 Australia–Europe trade: services availablein 1999

Commercial incentives applying to potential new entrantsapply equally to individual conference members. Demand bylarge shippers for individual service contracts has reducedthe practice of common rate setting, though common ratescontinue to apply for some types of cargo.

The potential for conferences to exercise market power alsoappears to have been constrained to some degree bycountervailing power exercised by Australian exporters. Forexample, evidence from shippers suggests that scope forcollective rate negotiation, and the requirements for shippingoperators to negotiate minimum service levels and provideinformation to shippers, have bolstered their negotiatingposition. At the same time, individual large shippersincreasingly appear to be negotiating directly with shippinglines to their mutual advantage.

… and conferencemembers alsocompete against eachother.

Australian exportersalso have been able toexert somenegotiating clout.

IndependentServices

AUSTRALIA

SINGAPORE(and other Asian ports)

Direct Conference Service

EUROPE

Direct IndependentService

TradeFacilitation

Group

Independent Services

Conference Service

XXVIII OVERVIEW

Freight rates for conference and non-conference linershipping services on most major Australian trade routes havedeclined steadily and significantly in nominal and real termssince the early 1990s, continuing a trend evident since thelate 1970s. Many participants in this inquiry claimed thatfreight rates are historically low on major trade routes (seefigure 4). While freight rate movements do not of themselvesindicate the state of market competition, it appears thataggressive competition has been a driving force.

Participants also have claimed that service levels to Australiahave improved in recent years. Evidence gathered by theCommission relating to service reliability, capacity,frequency, port coverage and transit times generally supportsthis assessment.

While the quality of service provided by non-conferenceoperators has improved since the 1993 Brazil Review,conferences as a whole continue to offer a better qualityservice than individual non-conference lines in terms of theiroverall frequency of services, reefer and dry capacity andport coverage. The difference between conference and non-conference freight rates has narrowed, though conferenceservices typically continue to attract a premium reflecting thehigher level of service provided.

While these and other indicators examined by theCommission are partial and therefore imperfect, the range ofevidence available to the Commission consistently suggeststhat conferences are subject to effective competition fromindependent operators. Australian shippers claim that theyenjoy a wide range of choice regarding service levels andprices, with conferences, on the whole, providing higherquality services. The shipping market in this respect is likemany others where a range of differentiated services andgoods is available from a variety of production units.

Freight rates havecontinued to fallsteadily over the1990s …

… while service levelsoverall haveimproved.

Competition in linershipping markets isintense, withconferences providingone of a number ofservice types.

OVERVIEW XXIX

Figure 4 Trends in freight rates in key northboundtrades

0

20

40

60

80

100

120

140

160

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Year

Ind

ex

Europe

SE Asia

Japan/Korea

CPI

Appropriate regulation

Although market forces appear to have ensured goodoutcomes for Australian shippers, there are two main reasonsfor regulation of conferences. First, several conferencepractices constitute prima facie breaches of Part IV of theTPA. Therefore, if conferences are to operate at all, theyrequire some form of exemption or authorisation. Second,and more fundamentally, as an importer of liner shippingservices, it is in Australia’s interests to exercisecountervailing power appropriately. This may be facilitatedby legislation or regulation.

The ultimate objective of any regulation must be to enhancethe national interest. For this inquiry the national interest iscongruent with the interest of Australian shippers inobtaining appropriate quality service at the best-possibleprice.

Regulation maypromote Australia’scountervailingpower …

XXX OVERVIEW

If it is accepted that conferences and other cooperativestructures which characterise liner shipping services canpromote efficiency and service levels, an appropriateregulatory regime will be one that allows such arrangementsbut which, at the same time, ensures that the efficiency gainsand lower costs made possible by such arrangements areshared with Australian shippers and, through them, theAustralian public.

To this end, and drawing on the terms of reference for thisinquiry and accepted guidelines for good regulation, theCommission considers that a desirable regulatory regimewill:

• allow a variety of market arrangements that generateefficient outcomes for Australian shippers;

• minimise adverse impacts on competition;

• promote Australia’s bargaining power and provideeffective constraints against abuses of market power byconferences;

• involve minimal regulation to achieve desired outcomes;

• be compatible with international regulatory regimes (thatis, be workable and enforceable);

• promote predictable outcomes for Australian shippers (inthe sense of predictable standards of shipping servicesprovided); and

• involve low compliance and administration costs, and betransparent and flexible.

An appropriate regulatory regime also will need to be able toadapt to future developments in international liner shippingmarkets — including the possibility of a reduction incompetition — and introduction of new technologies.

… and thus helpensure benefits ofconferences arepassed on.

Good regulation willnot impedecompetition, will becompatible withoverseas regulationand promotecommercialoutcomes …

… and be able toadapt to futuredevelopments.

OVERVIEW XXXI

Some participants suggested that the decision regardingappropriate regulation should take into account possibledevelopments in the WTO regarding international rules forliner shipping. However, a global framework is unlikely tobe agreed in the next few years and, consequently, theCommission does not consider that the choice of regulatoryarrangement should be based on possible developments inthe WTO.

Regulatory options

There are two major alternative approaches to regulation ofinternational liner shipping — that currently embodied inPart X of the TPA, and application of the general provisionsof the TPA, including Part VII authorisation provisions.

Other options include an industry-specific notificationprocedure, block authorisation or an industry code.

Part X

Part X allows individual shipping firms to enter intocooperative arrangements that otherwise would contravenecertain sections of the TPA. To this end, Part X providesregistered liner cargo shipping conference agreements (verybroadly defined) with exemptions from section 45 and, withthe exception of third-line forcing, section 47 of the TPA.These exemptions allow conferences to set joint freight rates,pool earnings and costs, rationalise capacity and restrict newentrants to the agreement (but not the market). Loyaltyagreements with customers also are permitted.

Though the exemptions from the TPA allow shipping lines toenter into conferences and similar arrangements (whichprima facie restrict competition), it does not compel them todo so. Nor does it constrain liner carriers from entering themarket and operating outside the conference, as is the casefor most other legislation deemed to restrict competition. Inthis sense, Part X could be described as taking a permissivestance towards production of liner shipping services.

Part X or Part VII ofthe TPA are the twomajor regulatoryoptions.

Part X exempts linerconferences fromsome provisions of theTPA …

… but does notcompel formation ofconferences orprotect them fromexternal competition.

XXXII OVERVIEW

However, Part X does not take a permissive approach to theeffects of cooperative arrangements on Australian exporters.Indeed, the overriding objective of Part X is to promote theinterests of Australian exporters (and thus the nationalinterest). Specifically, Part X attempts to promote thenegotiating strength (countervailing power) of Australianexporters by:

• allowing (but not requiring) them to form buying groupsand requiring outward conferences to negotiate with andto provide information to these groups;

• providing for ACCC investigations of breaches of Part Xby shipping lines (with scope for full or partialderegistration of conference agreements); and

• not exempting liner shipping operators from applicationof section 46 of the TPA (which prohibits misuse ofmarket power).

While Part X does not contain an explicit ‘public interest’test, in effect, the public interest is monitored and promotedby exporters who have a vested interest in ensuring theyobtain the best-possible outcomes. Exporters can requestintervention by the regulators — the Minister and the ACCC— at any time they consider that conferences have breachedtheir obligations under Part X, including the requirement thatshipping services are ‘economic and efficient’. The ACCCalso can take independent action under section 46 of the TPAbut it has never exercised this option. It also should be notedthat Part X has been subject to regular formal scrutiny toassess whether it serves the national interest — in addition tothe current public inquiry, it has been reviewed in 1977,1986 and 1993.

Part X attempts toensure that Australianshippers benefit fromcost savings ofconferences bybolstering theirnegotiating power.

Part X does notcontain an explicitpublic interest test butthe public interest isupheld by shippers.

OVERVIEW XXXIII

Part VII

The general provisions of the TPA prohibit certain actionssuch as joint price-setting. If Part X were repealed, thegeneral provisions of the TPA would apply to liner shipping.Conferences and other cooperative arrangements in linershipping would need to be authorised under Part VII, almostcertainly on a case-by-case basis, and demonstrate, ex ante,that they would operate in the ‘public interest’. To satisfy theACCC that the public interest would be served, it is possiblethat conferences would be required to give price or otherundertakings (to negotiate with shippers, for example). Whileauthorisation usually is given for a set period, it can berevoked if the ACCC considers that circumstances havechanged ‘materially’.

Other options

Notification as it currently operates is a procedure that allowsnotification to the ACCC of conduct that may breachsection 47 of the TPA. Notification provides immunity fromprosecution unless the ACCC decides to review and revokethe notification. To accommodate liner shipping conferences,the TPA would require industry-specific amendment toextend the range of notifiable conduct. In practice, anotification procedure could follow either the Part X or thecase-by-case authorisation models.

An industry code might operate in a similar fashion to Part Xbut probably would be subject to (possibly block)authorisation under Part VII. An authorised industry codealso might codify behaviour to a greater extent than Part X.As with a notification procedure, block authorisation wouldrequire amendment of the TPA which could be industry-specific or available to industry generally.

Under the generalprovisions of the TPA,conferences would beillegal unlessauthorised …

… conferences wouldhave to demonstratenet public benefits ona case-by-case basis.

Other options includenotification and anindustry code.

XXXIV OVERVIEW

The Commission’s assessment

In assessing the regulatory regime most likely to deliver thebest outcomes for Australians generally and shippersspecifically, the Commission has taken into account anumber of factors relevant to liner shipping (see box 2).

The regulatory approach embodied in Part X is tailored tothese market characteristics. Part X essentially operates as anindustry code, where the market operates relatively free ofday-to-day, third-party intervention. Regulators take actionin the event that Australian shippers are dissatisfied with thebehaviour or performance of conferences. Evidence availableto the Commission suggests that this approach has beensuccessful, promoting commercial relationships and disputeresolution and facilitating good service and price outcomesfor Australian exporters. Moreover, it has done so atcomparatively low administrative cost and has not causedinternational jurisdictional conflicts.

That said, however, Part X has been criticised by someparticipants because it does not impose an explicit ‘publicinterest’ test, its range of sanctions against market power islimited to full or partial deregistration of the conference,importers do not receive the same rights as exporters, and thescope of some of the exemptions from the TPA is notprecise. A general criticism is that Part X may be toopermissive in relation to the formation and conduct ofconferences and discussion agreements and that applicationof the general provisions of the TPA could produce betterprice and quality outcomes for Australian exporters andimporters.

The Commission has explored in some detail howauthorisation and other options might operate with respect toliner shipping but any discussion necessarily is hypothetical.

Part X is a tailoredregulatory regimewhich has promotedshippers’ interests …

… though it has beencriticised for beingtoo permissive.

OVERVIEW XXXV

Box 2 Features of liner shipping

• Shippers’ interests in relation to shipping services coincide with the public interestand shippers as profit-maximisers generally will have a strong incentive to obtainthe best-possible service for the lowest-possible price (failure to do so typically willmean lower sales and/or producer prices);

• Australia relies almost entirely on foreign liner services. If participation in theAustralian shipping market became relatively costly, foreign carriers (whose assetsare highly mobile) could reduce their commitment to Australian trades or evendiscontinue the conference service;

• Evidence of substantial production economies in liner shipping coupled with theneed for regular, coordinated services suggests that cooperation in some formwould characterise the industry even if conferences were proscribed;

• Consistent evidence of effective competition in liner shipping markets and lowbarriers to entry in liner trades suggest that market forces provide, and will continueto provide, effective regulation of conference market power; and

• All countries with which Australia trades currently not only allow the formation ofconferences but also provide general, automatic exemptions from competition law.There is no indication that this situation will change in the foreseeable future.

As noted above, a key difference between Part X andauthorisation (Part VII) is that the authorisation mechanismprovides greater scope for direct third-party intervention on‘public interest’ grounds. Some participants regard this as amajor advantage of authorisation. The Commission agreesthat promotion of the public interest is paramount. But isthird-party intervention likely to enhance that interest? Ifcompetitive forces in liner shipping trades were weak, thecase for stricter regulation would be strengthened.

However, given the degree of market competition (andmarket contestability) and the fact that the public interestcoincides with the interest of shippers, it is not clear thatscope for discretionary third-party intervention is necessaryor even desirable. The national interest is vigilantlyrepresented by the shippers themselves, coupled withapparently effective self-regulation by the market. Thesuggestion that precisely because there is intensecompetition, conferences could be removed at little cost, isnot accepted by the Commission. If conferences survive

Part VII is likely toinvolve more directintervention thanPart X …

… but suchintervention may notbe necessary ordesirable in thisindustry where therisk of market failureappears low.

XXXVI OVERVIEW

competition they must be producing a valued serviceefficiently.

There also are serious doubts as to whether Australia couldenforce its competition laws in the event that authorisationwere not granted. Administrative and compliance costs alsowould appear to be significantly higher under authorisation.

It is feasible that the authorisation process could function in asimilar manner to Part X. Protection of shippers could beachieved by authorising agreements between shipping linessubject to conditions (such as negotiating minimum servicelevels with a shipper body, and providing advance notice ofchanges in price and service levels). Carriers also could optto give the ACCC undertakings regarding protection forshippers. Indeed, the Commission is of the view that, werePart X to be repealed, eventually a Part X-type regime (thatis, conditional industry-wide block exemption) would re-emerge. The transitional process could be uncertain,protracted and costly, however, and probably would requirelegislative amendment to allow block authorisation. Indeed,the approach of Part X appears antithetical to the approach ofPart VII as the latter currently operates.

The Commission notes the argument that liner shippingshould not be treated differently from other Australianindustries. The Commission is not persuaded by thisargument principally because:

• international liner shipping is an imported service forAustralia. If Australia, as a comparatively small user ofinternational liner shipping, were to imposecomparatively onerous regulatory requirements on (someof) these imports, reducing the profitability of Australiantrades relative to other trades, service levels coulddecline. Doubtless other forms of service would expandto fill the gap in the market, but it is difficult to see whythis would promote the national interest if conferenceshad been providing a service valued by shippers andproviding that service efficiently;

Though Part VIIcould work in asimilar way to Part X,their approaches arefundamentallydifferent.

Part VII has theadvantage ofuniformity, but thisshould not beconsidered an end initself.

OVERVIEW XXXVII

• while it is desirable that no industry or sector of theeconomy is given special favours which may result inresource misallocation, inefficiency or undesirableincome transfers, virtually all liner shipping to and fromAustralia is provided by foreign carriers who use veryfew Australian resources. The major potential forresource misallocation is if Australian shippers cannotaccess adequate quality liner shipping at competitiverates; and

• uniformity of regulation is not an end in itself — theultimate objective must be a regulatory regime which bestserves the national interest.

Moreover, and of overriding importance in this case, theCommission’s terms of reference direct that the legislationshould be retained if, having passed the test of benefitsoutweighing costs, its object cannot be achieved moreefficiently by other means.

The Commission also has considered other options includingnotification, a block authorisation and an industry code. Withnotification, or with an industry code (unless it had blockauthorisation), there would be an additional level ofuncertainty — that is, the uncertainty of not knowingwhether, in practice, it would be administered in a mannersimilar to Part X, or similar to Part VII authorisation. In theevent of the latter type of application, the advantages anddisadvantages of a Part VII authorisation, as alreadydiscussed, would apply.

Even if the Part X-type approach could be replicated in anindustry code or notification procedure, at the very leasttransitional costs would be incurred for no apparent gain.Moreover, liner shipping, in effect, would continue to receivethe special treatment that most proponents of change regardas a major reason for repealing Part X.

Other options alsowould involve greateruncertainty andtransitional costs.

XXXVIII OVERVIEW

Unlike other legislation deemed to restrict competition,Part X does not give liner conferences a protected monopoly.Rather it applies competition principles in an unusual way,albeit a way designed to ensure that the interests ofAustralian shippers, and the community overall, areprotected. The Commission’s conclusion as to appropriateregulation for this industry is based on an assessment of thepast and present operation of liner shipping markets and alsohow they are likely to develop.

For these reasons, on balance, the Commission considers thatthe regulatory approach encapsulated in Part X is likely toproduce better outcomes for Australian shippers, and henceconsumers and the community at large, than Part VII of theTPA, or available alternatives, and do so more efficiently.

That said, the operation of Part X could be improvedsomewhat, by amendments which clarify the scope of theexemptions from the TPA with regard to land-basedactivities and which extend the range of sanctions availableto the Minister in the event of a breach of an undertaking bya conference. The Commission has set out the appropriateamendments in its recommendations.

Part X appliescompetitionprinciples, albeit inan unusual way.

On balance Part X islikely to producebetter outcomes forAustralian shippersthan other options ...

… but its operationcould be improved atthe margin.

RECOMMENDATIONSAND FINDINGS

XXXIX

Recommendations and findings

The Commission has been asked to report on appropriate regulation forinternational liner cargo shipping taking into account, inter alia, the objectivethat regulation/legislation should be retained only if the benefits exceed the coststo the community and if alternatives cannot achieve the objectives of theregulation/legislation more efficiently.

The Commission concludes that, given competition and market contestability, thebenefits to Australian shippers (and hence the community overall) of allowingconferences and other cooperative arrangements to operate exceed any costs.

Moreover, given the fact that the interests of Australian shippers are aligned withthe national interest, and that they will vigilantly represent their interests, theCommission considers that regulation of conferences under Part X is appropriate.

In particular, Part X:

• involves minimal — but adequate — regulation and promotes commercialrelationships and commercial dispute resolution;

• is neutral with respect to market arrangements and has not hindered efficientmarket outcomes or hindered competitive forces in liner shipping markets;

• has supported the negotiating position of Australian shippers and assisted inproviding them with predictable service outcomes;

• is compatible with international regulatory regimes; and

• is low cost.

Repeal of Part X and its replacement by the general provisions of the TPA (asthey currently stand and as they have been applied) is unlikely to produceoutcomes as good or better than Part X, or do so more efficiently. While theCommission accepts that, in principle, a Part X-type approach could be appliedwithin the general provisions of the TPA, this may require industry-specificlegislation (a notification procedure) or possibly general amendment of the TPA(block authorisation). However, inevitably uncertainty would remain as towhether these options would be implemented in the manner of the regulationwhich the Commission assesses is appropriate, as embodied in Part X.

XL RECOMMENDATIONSAND FINDINGS

The Commission therefore concludes that the alternatives would not achieve theobjectives of the legislation more efficiently than the current legislation.Accordingly, Part X should be retained.

The Commission also recommends that the situation be re-examined in 2005 toascertain whether the conclusions of this review are substantially altered as aresult of technological or institutional changes in the international liner shippingmarket.

Other recommendations

In addition, the Commission considers that operation of Part X could be improvedby the following amendments:

Clarify that the exemption relating to rate setting extends to land-based chargesthat normally form part of a ‘terminal-to-terminal’ shipping contract (that is, onethat includes not only the ‘blue water’ component but also the sorting and stackingof containers within a container terminal). The Commission favours widening thedefinition of terminal from the present ‘within the limits of the wharf as under theCustoms Act 1901’ to include terminals located within the metropolitan area of portcities.

Confirm existing practice allowing members of shipping conferences to negotiatecollectively with stevedores.

Delete sections 10.14.2 and 10.22.2 which allow the fixing of door-to-door freightrates for outward and inward liner conferences respectively, recognising that thedeletion of these sections will make it necessary for insertion of a clause insections 10.14.1 and 10.22.1 permitting conferences to set terminal-to-terminalrates.

Repeal section 10.05 which prohibits price discrimination in certain circumstances.The Commission considers that the price discrimination provisions of Part X serveno useful purpose and indeed are potentially harmful if they discourage efficientprice discrimination. In addition they would be extremely difficult to implement.

RECOMMENDATION 8.1A

RECOMMENDATION 8.1B

RECOMMENDATION 8.2

RECOMMENDATION 8.3

RECOMMENDATIONSAND FINDINGS

XLI

Add a ‘national interest’ test, similar to that in section 10.67, to apply to anydetermination by the Minister in relation to sections 10.45(a)(v) and 10.53. Thisamendment would ensure that shippers’ interests were taken into account explicitlyin a Ministerial determination as to whether a conference or non-conference carrierwith substantial market power was misusing market power in order to hinder anefficient Australian carrier.

Provide for more effective and flexible enforcement of undertakings. The provisionsof section 87C of the TPA could serve as a useful model.

Findings

The Commission also examined a range of other issues relating to Part X on whichit decided not to recommend amendments to the current legislation:

The issue of whether or not terminal handling charges should be itemisedseparately in the freight charge is a matter for negotiation between shippers andcarriers rather one to be determined within the ambit of Part X.

While accepting the principle that inward shippers should be able to organise inorder to exert countervailing power, the Commission considers that imposingregistration requirements and obligations on inward conferences equivalent tothose imposed on outward conferences would impose some costs, and possibly leadto significant jurisdictional problems, for little benefit. However, the Commissiondoes not consider that importers should be precluded from forming a collectivebuyer group to negotiate Australian THCs if a cost-effective mechanism can bedevised.

RECOMMENDATION 8.4

RECOMMENDATION 8.5

FINDING 8.1

FINDING 8.2

XLII RECOMMENDATIONSAND FINDINGS

Discussion agreements should not be treated differently from other forms ofcooperation among carriers. The Commission has not been able to identify clearbenefits to offset the costs and difficulties (including problems of definition) thatwould be created by not allowing discussion agreements the exemptions currentlyprovided under Part X. Safeguards exist to protect shippers against any exploitivepractices under discussion agreements.

The current Part X approach, which permits (but does not require) carriers to formclosed conferences, offers efficiency gains through the employment of larger vesselsand cooperative vessel scheduling. The Commission considers that sufficientcompetitive pressures exist (notably through internal competitive pressures, theoperation of non-conference carriers, the threat of entry, the operation oftranshipment carriers, and the countervailing power of shippers) to negate anypotential monopoly power of closed conferences.

Division 9 (which relates to declaration of a non-conference carrier withsubstantial market power) should be retained because, if used judiciously, it doesnot appear to impose costs on shippers, while offering them additional defencesagainst misuse of market power by any carrier which might come to dominate aparticular trade.

The processes for registering conference agreements and variations to theseagreements provide important transparency benefits and should be retained.Measures to expedite the registration process are matters for negotiation betweenshippers and conferences, not for regulation.

Funding for APSA should come from the beneficiaries of its activities, namelyAustralian shippers.

Regulations governing international liner shipping should be retained in the TPArather than transferred to a separate shipping Act.

FINDING 8.3

FINDING 8.4

FINDING 8.5

FINDING 8.6

FINDING 8.7

FINDING 8.8

INTRODUCTION 1

1 Introduction

This chapter provides background to this inquiry and the major issues dealt with inthe report. It also outlines how the Commission has approached its task.

1.1 Australia’s liner cargo shipping task

Australia’s demand for shipping services is a derived demand, stemming fromdomestic demand for imports and foreign demand for Australian exports.International shipping therefore is an essential intermediate service input forAustralia’s exports and imports.

Around 79 per cent of merchandise exports and 71 per cent of merchandise imports(by value) were transported by sea in 1997-98. Liner services are provided bycontainer (including refrigerated container), roll-on roll-off (ro-ro), conventionaland multi-purpose vessels, and provide regular, scheduled services to set timetables.Liners tend to carry relatively high value/low volume cargoes (see table 1.1), thoughthey may carry relatively low value bulky cargoes as ballast. In 1997-98, linervessels carried 4 per cent of the volume and 48 per cent of the value of Australia’sseaborne exports, and 23 per cent of the volume and 74 per cent of the value ofAustralia’s seaborne imports. Remaining Australian seaborne trade consists ofcommodities shipped by bulk carriers (for example, grains and minerals) andtankers.

Within the liner trades, shipping conferences (groupings of liner shipping operators— see section 1.2 below) tend to carry more valuable cargoes than non-conferencevessels (see table 1.1). Though conferences remain important, currently carryingmore than 50 per cent of liner exports by value and more than 60 per cent of linerimports, conference shares of both the volume and value of liner trade have fallensince the early 1980s.

2 INTERNATIONALLINER CARGOSHIPPING

Table 1.1 Australian sea freight, 1997-98

Australian exports Australian imports

By value $ billion % of totalby sea

% of linershipping

$ billion % of totalby sea

% of linershipping

Total carried by sea 69.6 – – 64.1 – – Bulk shipping 36.1 52 – 16.8 26 – Liner shipping 33.5 48 – 47.3 74 – — Conference 18.8 27 56 30.1 47 64 — Non-conference 14.8 21 44 17.3 27 36

By weight milliontonnes

% of totalby sea

% of linershipping

milliontonnes

% of totalby sea

% of linershipping

Total carried by sea 427.1 – – 51.7 – – Bulk shipping 408.8 96 – 39.6 77 – Liner shipping 18.2 4.3 – 12.1 23 – — Conference 8.1 1.9 45 6.5 13 54 — Non-conference 10.1 2.4 55 5.5 11 46

Source: Bureau of Transport Economics, International Cargo Statistics Database (accessed April 1999).

1.2 Liner shipping conferences

The principal reason for regulating international liner shipping is the industry’spropensity to form ‘conferences’.1 Conferences are groupings of liner shippingoperators which coordinate the supply of shipping services. Currently there areapproximately 300 conferences operating worldwide. Each conference tends to limitits activities to one leg of a particular route or trade between two or more countries.Most conferences have fewer than ten members, although some have as many asfifty. Some shipping companies choose to join conferences on all or most of theroutes in which they operate. Other companies choose to operate independently inall or most trades.

There is a range of views regarding the rationale for, and effect of, shippingconferences. As outlined in chapter 3 and appendix B, conferences may enhanceefficiency by allowing carriers to capture economies of scale and scope which inturn allow them to provide low-cost, reliable, regular, scheduled services toshippers. On the other hand, conference behaviour may be consistent with theactions of producer cartels and, as such, facilitate monopolistic or oligopolisticpractices and pricing. In practice, conferences may display desirable and undesirablecharacteristics simultaneously.

1 Shipping generally is subject to international regulatory codes on matters such as safety and

pollution. Conference arrangements, however, exist only for (scheduled) liner shipping.

INTRODUCTION 3

This tension between the potential benefits and costs of shipping conferences hasmotivated the special regulatory arrangements which typically apply to conferencesworldwide. Thus most countries allow conferences to operate but attempt either toregulate conference behaviour directly (for example, the United States requiresconferences to be ‘open’ to the entry and exit of members) and/or indirectly, bypromoting the interests of domestic shippers. Australia exempts liner shippingconferences from the application of some provisions of the Trade PracticesAct 1974 (TPA) while, at the same time, imposing certain obligations onconferences to negotiate minimum service levels as well as provide information toAustralian shippers. Australian shippers also are allowed to form buying coalitions.It is this special treatment of international liner shipping within the generalAustralian competition laws which has prompted this inquiry.

1.3 Background to the current inquiry

The Commonwealth Government has asked the Productivity Commission to reviewPart X of the TPA and to report on the appropriate arrangements for regulation ofinternational liner cargo shipping services.

This inquiry stems from the Commonwealth, State and Territory Governments’agreement of April 1995 to extend competition policy — the National CompetitionPolicy. One of the agreements implementing National Competition Policy reforms,the Competition Principles Agreement (CPA), establishes guiding principles forreviewing legislation that restricts competition (see box 1.1). The terms of referencefor this inquiry are drawn from these principles.

There have been three reviews of Part X — in 1977 (the ‘Grigor’ Report), 1986 and1993. Recommendations of the industry taskforce’s Review of Australia’s OverseasLiner Shipping Legislation in 1986 formed the basis for amendments enacted in theTrade Practices (International Liner Cargo Shipping) Amendment Act 1989. Thechanges were designed to encourage a more competitive environment whilstpermitting exporters and importers continued access to liner conference shippingservices.

To this end, the 1989 modifications to Part X:

• reduced the scope of the exemptions conference agreements could obtain fromPart IV of the TPA;

• introduced public registration of outward conference agreements;

• introduced a 30-day notice period for variations to services and freight rates foroutward trades;

4 INTERNATIONALLINER CARGOSHIPPING

• required negotiation of minimum service levels with shippers in outward trades;and

• provided Part IV exemptions for the designated peak shipper body.

Box 1.1 Legislation review requirements

Under the CPA all Australian governments agreed to review and, where appropriate,reform existing legislation that restricts competition by 31 December 2000.

The Commonwealth Government released its review timetable in June 1996. TheLegislation Review Schedule nominated 98 separate reviews, and foreshadowed,amongst others, the review of Part X.

In announcing the Review Schedule, the Commonwealth Government also outlined anumber of requirements for reviews. In particular, the Government stipulated that eachreview is to be approached according to clause 5(1) of the CPA which states that:

The guiding principle is that legislation (including Acts, enactments and Ordinances orregulations) should not restrict competition unless it can be demonstrated that:

a) the benefits of the restriction to the community as a whole outweigh the costs; and

b) the objectives of the legislation can only be achieved by restricting competition.

The CPA also outlines how reviews should be conducted (clause 5(9)). Specifically, areview should:

• clarify the objectives of the legislation;

• identify the nature of the restriction on competition;

• analyse the effect of the restriction on competition and on the economy generally;

• assess and balance the costs and benefits of the restriction; and

• consider alternative means for achieving the same result including non-legislativeapproaches.

The terms of reference for this inquiry are drawn from these broad requirements.

Source: PC (1998c).

An independent review of Part X, known as the Brazil Review, was conductedin 1993. This review recommended that Part X be retained in amended form. Theproposed amendments were designed to strengthen the protection of exporters (thatis, users of outward shipping services), and importers where feasible, and to providea commercially-oriented procedure to deal with disputes. However, no changes weremade to the regulatory regime in response to this review.

As already noted, the current review forms part of the scheduled legislative reviewprocess. Many of the issues covered in previous reports have been re-examined with

INTRODUCTION 5

a view to assessing whether circumstances have changed, or are likely to change,such as to warrant modification of the current regulatory approach to the industry.

1.4 Scope of this inquiry and the Commission’sapproach

The terms of reference stipulate that the legislation (Part X) should be retained onlyif the benefits to the community as a whole outweigh the costs and if the objectivesof the legislation cannot be achieved more efficiently through other means, includingnon-legislative approaches. Accordingly, the Commission has applied this test whenmaking its final assessment.

In assessing costs and benefits, the Commission was asked to take into accountseveral objectives, including access of Australian exporters to competitively-pricedinternational liner cargo shipping services that are of adequate frequency andreliability, public welfare and equity, economic and regional development, thecompetitiveness of business including small business, consumer interests andefficient resource allocation. In conducting the inquiry, as well as referring to thegeneral policy guidelines in the Productivity Commission Act 1998 (see chapter 3,box 3.2), the Commission also was required to have regard to the analyticalrequirements for regulation assessment by the Commonwealth, including those setout in the CPA (box 1.1).

In most legislative reviews under the CPA, the arrangements under review involve aclear restriction on competition. The current inquiry is somewhat unusual in that itreviews an exemption (Part X) to general competition law allowing individualshipping firms to enter into cooperative arrangements that otherwise wouldcontravene that law (unless specifically authorised). Though the exemption allowsshipping lines to enter into conferences and similar arrangements (which reducecompetition between members) it does not require them to do so. Nor does itexplicitly constrain market entry, as is the case for most other legislation deemed torestrict competition.

In this sense, Part X could be described as taking a comparatively permissive stancetowards market structure. However, Part X also puts in place several mechanismsdesigned to ensure that cost savings generated by conferences are shared withAustralian shippers.

The Commission’s approach in this inquiry has been to:

• develop principles for regulation of liner shipping operations, based on: anassessment of the public interest; the role of shipping conferences in service

6 INTERNATIONALLINER CARGOSHIPPING

delivery and their potential beneficial and harmful effects; an appreciation of thenature of liner shipping (especially that it is an international industry); and thefact that Australia relies almost entirely on foreign liner shipping services;

• assess market outcomes under current regulatory arrangements, and how Part Xhas contributed to those outcomes, with a view to establishing strengths andweaknesses of the current approach;

• identify and assess possible alternative mechanisms, most importantly, repeal ofPart X and reversion to the general provisions of the TPA, including the Part VIIauthorisation provisions; and

• recommend the regulatory approach which, on balance, best serves the publicinterest (and which does so most efficiently).

Report structure

Developments in global and Australian liner shipping markets since the 1993 BrazilReview are outlined in chapter 2. Principles for assessing the various regulatoryoptions are developed in chapter 3. Current regulatory arrangements in Australia andoverseas are presented in chapter 4. Chapter 5 contains an evaluation of the qualityand competitiveness of liner shipping to and from Australia. The effectiveness ofPart X is considered in chapter 6. Major regulatory alternatives to Part X areassessed in chapter 7, while possible modifications to the existing Part X arecanvassed in chapter 8. The Commission’s overall assessment is presented inchapter 9.

1.5 Conduct of the inquiry

The terms of reference for this inquiry were received on 12 March 1999. Theinquiry was to be completed within six months — that is, by 12 September 1999.