8th annual pricewaterhousecoopers like-kind exchange ... i... · slide 5 8th annual like-kind...

TRANSCRIPT

8th Annual PricewaterhouseCoopersLike-Kind Exchange Conference

Session I: International Financial Reporting StandardsSteve Lilley, PricewaterhouseCoopers

PwC

Certain matters that will be discussed today may represent services that PwC may be prohibited from providing to our audit clients. In those instances, the information is being provided to inform you of options that you may consider as you assess your company's approach to IFRS. Independence rules are complex and we recommend discussing all services with you in advance to ensure all services are designed within the context of the independence rules.

The opinions expressed today are those of the speaker and may or may not represent those of PricewaterhouseCoopers….after listening to the speaker you will understand why…….

Thank you for joining us today.

Agenda

OverviewSummary of response letters to SEC road mapIFRS conversion and implementation approachHow IFRS may impact the processing environment Specific PPE challengesSummary Q&A

Overview

Slide 58th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

The world has chosen IFRS

More than 100 countries require or permit the use of IFRS, or are convertingTop 10 Global Capital Markets

US US GAAPJapan Converting to IFRSUK IFRSFrance IFRSCanada Converting to IFRSGermany IFRSHong Kong IFRSSpain IFRS Switzerland IFRS or US GAAPAustralia IFRS

Countries seeking convergence with the IASB or pursuing adoption of IFRSs

Countries that require or permit IFRSsCountries with no current plan to adopt

Slide 68th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Benefits and first-mover advantages

IFRS: Uniform Global Accounting Language

Reduced cost of financial reporting for global companies

Industry perception of market leadership

Sufficient time to adequately debate strategic first time adoption – in particular with “look back” provision

Streamlined M&A activity

More effective procurement with vendors and customers reporting under IFRS

Improved transparency and comparability for investors and rating agencies

More efficient access to capital for global corporations

Ability to analyze impact on tax-related issues

Ability to understandinteraction with strategic initiatives to generate value from synergies

Ability to secure scarce IFRS knowledge resources and optimize human capital deployment decisions

More room for management’s judgment and truer reflection of economic reality with principles-based GAAP

Slide 78th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Potential US and non-US subsidiary transition timelines

2008 2009 2010 2011 2012 2013 2014

SEC determines mandatory dates and approach

Early US adoption?*

Periods in 1st US financials

Transition date – Opening IFRS balance sheet

Beginning of IFRS mandatory adoption

US preparation

Non-US subsidiary IFRS preparation

* The SEC’s announced preliminary roadmap provided for voluntary early adoption for certain companies beginning in 2009. Given the uncertainties associated with the timing of the finalization of the SEC’s proposed roadmap, early adoption may ultimately not be allowed this early.

Slide 88th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Current proposed timeline for US transition

SEC proposed a roadmap for adoption of IFRS by US issuers• Proposed phased-in mandatory adoption in 2014• Early adoption choice for some as soon as 2009 that meet the following criteria:

- Must be among the top 20 companies in industry- IFRS must be the most used accounting standard- Must obtain a letter of no objection from the SEC

• SEC has established milestones that must be progressed upon by 2011, where they will vote to continue moving to IFRS by 2014 or to change course including:- Improvements to IFRS- Accountability and independent funding of IASCF and IASB- XBRL compatibility- IFRS education and training in the US

Slide 98th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Our view on IFRS in the US

• The SEC’s roadmap outlines a path to voluntary and mandatory adoption of IFRS. Our preliminary views are:- We would prefer the SEC sets a definitive date for transition- We believe achievement of the milestone relating to progress against the

FASB/IASB Memorandum of Understanding should be viewed with flexibility- We do not believe that the alternative requiring ongoing reconciliation from IFRS

to US GAAP during the transition window should be required- We support allowing early adoption for a wider group of registrants

• Globalization will drive a change to IFRS in the US, and the 2014 to 2016 mandatory change dates are reasonable and attainable

• Moving to a single set of robust, transparent global accounting standards is in the best interests of investors globally

Slide 108th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Our view on IFRS in the US

• Establishing a definitive date with minimal milestones as soon as possible is the key to motivating market participants

• Allowing early adoption will be helpful to the US capital markets prior to a mandatory change

• The current convergence model is a challenging pathway for business• Transitioning to IFRS will be at a cost, but the benefits will outweigh the cost

(specific 1st-time adoption exemptions are available to ease the burden of conversion)

• IFRS provides opportunities to reduce complexity and simplify financial reporting- Through implementation of a principles-based framework- By moving to global shared services centers for global financial reporting

• Current capital market conditions have delayed progress

Slide 118th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Principles-based vs. rules-based

• US GAAP is more prescriptive and rules-based, addressing specific industries and types of transactions in many areas

• IFRS allows for more use of reasonable judgment• Fewer rules means more consideration of a transaction’s economics• Footnote disclosures increase in importance to allow

comparability between companies

US GAAP25,000 pages

IFRS2,500 pages

IFRS:• Standards

- IFRS- IAS

• Interpretations- IFRIC- SIC

• Framework

US GAAP:• Standards:

- SFAS- APB- ARB

• Interpretations - FSP- EITF- FIN

• Concepts Statements• Other

- FTB- AICPA

Interpretations- SOP- AICPA Industry

Guides, SABs, DIGs, etc.

Slide 128th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

US GAAP vs. IFRS typical differences

Transition Exceptions/Elections Upon Adoption

Business Combinations Minority InterestEquity/Debt Derivatives and HedgingConsolidation Share based paymentsEmployee benefit plans Revenue RecognitionImpairment PP&ER&D Provisions and ContingenciesLIFO

Slide 138th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Effort & impact – potential IFRS to US GAAP differences

RestructuringInventory

Treasury stock

Foreign exchange

Implementation Effort/Complexity

Fina

ncia

l Sta

tem

ent I

mpa

ct

Low HighLow

High

Stock basedcomp

Segment reporting

Development costs

Business combinations

Property, plant and equipment

Revenue recognition

Derivatives and hedging

Investments

d

OCI

d

Taxes

EPS Pensions

Leasing

Receivables

Impairment

Goodwill and intangibles

Debt

Consolidation

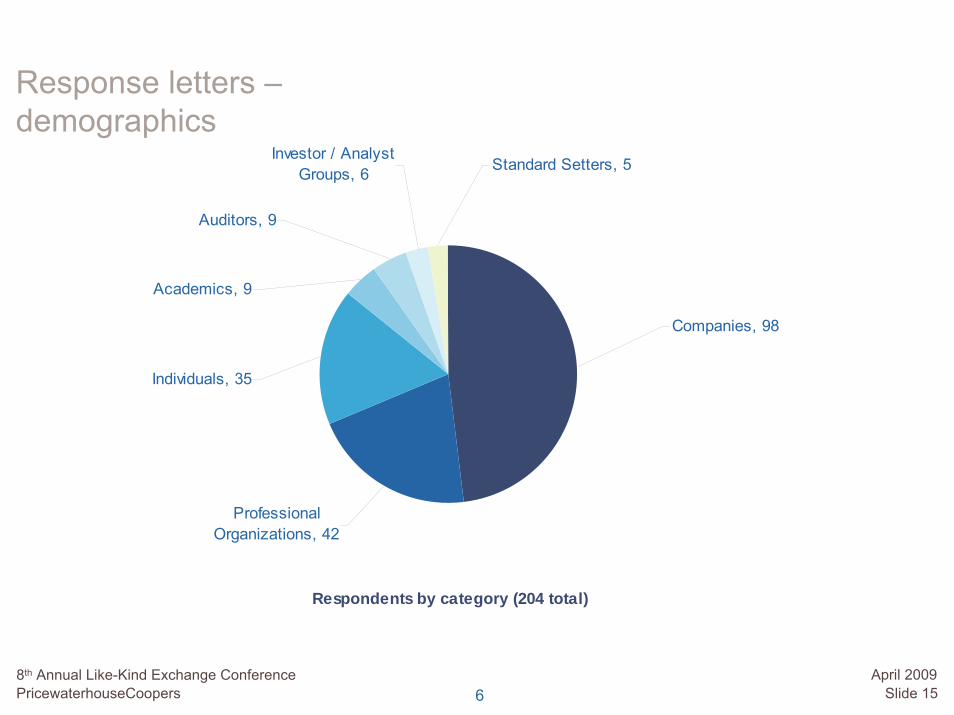

Summary of response letters to SEC road map

Slide 158th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Respondents by category (204 total)

Auditors, 9

Investor / Analyst Groups, 6 Standard Setters, 5

Academics, 9

Individuals, 35

Professional Organizations, 42

Companies, 98

Response letters –demographics

6

Slide 168th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –demographics

7

Domestic vs. International respondents (204)

179

25

0 50 100 150 200

Domestic

International

Number of responses

Slide 178th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –demographics

8

Respondents by Fortune 1000 designation (98)

32

34

5

13

10

4

0 5 10 15 20 25 30 35 40

1 - 100

101 - 500

501 - 1000

1000+

FPI

Private

Number of responses

Slide 188th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –demographics

9

Respondents with industry affiliation (112)

3

33

20

19

16

14

7

0 5 10 15 20 25 30 35

Financial Services

Energy & Mining

Consumer & Retail

Industrial / Contracting

Technology & Comm.

Healthcare & Pharma.

Entertainment & Media

Number of responses

Slide 198th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –key points

• Four key themes from response letters:

- Support for moving to a single set of global accounting standards

- Views varied on the path to IFRS, but many asked for more time

- Independence and accountability of the IASB is important

- The change to IFRS proposed by the Roadmap will have a much wider impact than expected

• SEC may begin to clarify direction later in 2009 or early 2010

• Companies should follow a measured approach to preparing for IFRS

5

Slide 208th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –themes – single set of accounting standards

• The goal of a single set of global accounting standards was supported by 84% of respondents

- IFRS has potential, but many believe it needs improvement

- Joint projects between IASB and FASB

• Desire for more industry guidance

• IFRS – not US GAAP – only viable option

10

Slide 218th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –themes – path to single set of accounting standards

• Three broad approaches to IFRS:

- Full convergence of IFRS and US GAAP (43%)

- Partial convergence coupled with a mandatory adoption date (24%)

- Decide now on a mandatory adoption date (28%)

• Fortune 1000

- Fortune 100 companies evenly divided among the three approaches

- Remaining Fortune 1000 companies support (66%) full convergence

• Consumer & Retail, Aerospace & Defense, and Utilities generally supported the full convergence approach

11

Slide 228th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Response letters –next steps - SEC

• Near-term focus is on financial crisis and regulation

• Expect increased activity later in 2009 or into 2010

- Address G20 commitments

• SEC will have to choose

- How much convergence actually takes place before a mandatory date is established?

- How will the transition be effected?

- What is the final timeline?

17

IFRS conversion and implementation approach

Slide 248th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

IFRS conversion – alternative approaches

Description Large scale, simultaneous/sequential conversion effort for the entire Company. One time effort with company-wide assessment of implications

Effort Substantial effort across organization, maximum disruption to businessResources Large number of IFRS skilled staff required (incremental hiring/outsourced). Typical resource mix of

65/35% (internal/external) Comments Too robust given existing workload; significant upfront costs; least efficient; does not take advantage of anticipated SEC

timeline; increased risk of error on adoption; minimizes knowledge transfer & staff development

Effort Low effort at start up; significant, ad hoc effort and disruption to business at reporting datesResources Additional resources required at critical stages. Typical resource mix of 55/45% (internal/external) at critical stagesComments Higher risk scenario; manually intensive; minimizes differences; centralized effort to comply; reactive to peers;

substantial future effort to realign organization to realize benefits

Effort High effort in phase; low effort out of phase. Effort level and business disruption dictated by management’s schedule and alignment with other Company initiatives

Resources Resources to be added at management discretion; Typical resource mix of 80/20% (internal/external)Comments Effective, efficient implementation method; affords time to properly embed IFRS and make judgments; maximizes

knowledge transfer and staff development

Description Increases top side adjustments to US GAAP consolidated F/S at reporting periods

Description Implemented in stages at management discretion (i.e. pilot basis)

“Wait & See”

“Big Bang”

“Staged Phases”

Slide 258th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Getting started – progressive approach to phase 1 assessmentW

ork

activ

ities

Del

iver

able

Pros

and

con

s

Option 1* – “Raising awareness and staying in control”

Option 2* – “Developing a clearer view of the way forward”

Option 3* – “Being fully prepared to begin detailed conversion work”

Benchmarking and focused workshops, followed by additional high-level analysis and meetings on:• Technical issues• International dimensions• Tax, systems and wider business issues• Ongoing systems or other major business

projects (to assess interdependencies)

Option 1 PLUS:• Additional workshops and analysis on key

areas (e.g., disclosures).• Survey overseas business units• Begin awareness training at the center• Detailed analysis of conversion results

and experience of non-US comparable companies

Option 2 PLUS:• Additional workshops and analysis on key

business and technical areas (e.g., systems, commercial issues).

• Begin more substantive interaction with key business units’ IFRS activities

• Project planning and governance considerations.

• High-level report for senior management, the Audit Committee, or the Board of Directors.

• More detailed report with company and industry-specific information for use by company decision makers.

• Project plan for conversion activities.

Pros: • Decision-useful, strategic information• Begins building company awareness• Quick and cost efficientCons:• High level• Brings an element of process inefficiency,

due to necessity of re-starting process later

Pros:• Decision-useful, detailed information• Increased buy-in to change at the centerCons:• More time and cost (although the

investment will have to be made at some point)

• Some remaining process inefficiency

Pros:• Thorough understanding of potential

impact on the group• Project plan, allowing flexibility on timing

of next stepsCons:• Cost and time investment (although the

investment will have to be made at some point)

*In practice, each approach will be tailored to meet your specific needs (e.g., technical topics will be tailored for your industry). Please see Appendix 1 for a detailed outline of the work to be performed for each option.

Slide 268th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

TransitionIFRS methodology

US GAAP IFRSProject management, communication, knowledge transfer

Phase 1• Preliminary study

Phase 2• Project set-up• Component

evaluation and issues resolution

• Initial conversion

Phase 3• Integrate change:

Go-live and embedding

Assess impact and determine strategy

Establish IFRS policies and prepare initial IFRS financial results

Embed IFRS as the primary financial language

Slide 278th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

IFRS – not just debits and creditsA conversion is a business transformation and encompasses changes to processes and systems, as well as numbers.

Changing People• Communication

- Internal- External

• Training:- At different levels- Not only Finance people

Changing NumbersAddition of another GAAP and/or change in primary GAAP• Accounting policies determination; Chart of Accounts review, Opening Balance Sheet,….

Changing Processes• Existing processes to be enhanced:

- Not adequate with volume- As alternative to system change

• New processes created• Budgeting & forecasting• Internal controls revisited

Changing Systems• Data availability and system

requirements• New systems components: data

warehouse, calculation engine• Re-alignment of management

information systems• Multi-GAAP solutions• Primary GAAP changeover

Changing Business• Performance management to be embedded across :

- Performance measure/KPIs- Management accounts - Remunerations/bonuses - Budgeting/forecasting- Financial and Business impact analysis: debt covenants- Different valuations

Slide 288th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Tangible benefits for US companies

• Opportunity to enhance financial reporting processes…a fresh start• Potential for reduced cost of compliance

- Centralized IFRS policies and shared services department- Potential to simplify statutory reporting process

• Increased flexibility in capital-raising initiatives• Improved global comparability of financial results• Fewer rules and exceptions simplifies financial reporting• Potentially reduce the risk of reporting errors• Allow for the broader use of professional judgment• Increase a company's ability to move personnel among countries

Slide 298th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Key challenges in an IFRS implementation

• Underestimation of time required- Project management essential

• Not enough focus on correlative effects- Investor relations and market communications- Contracts and agreements- Tax related issues- Bonus and compensation plans- Effects on IT systems

• Lost opportunities- Too many workarounds- IT not used as effectively as it could have been

Slide 308th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

• Establish a clear vision and plan at the start• Establish the tone at the top and set up the right governance structure and clear

decision-making powers.• Plan and execute appropriately considering impacts across the business.• Don’t “outsource” the conversion process – grow your own resources.• Develop a conversion plan that takes into account peaks and valleys of activity (e.g.

quarterly reporting).• Consider how IFRS will impact KPIs and your internal and external

communication strategy.• Take steps early to communicate with and influence regulators, tax authorities and other

stakeholders around the impact and acceptance of IFRS.• Become knowledgeable with the standard-setting process, as IFRS will continue to evolve

during implementation.• Make the most of opportunities for other project efficiencies (e.g. faster close process).• Consider opportunities for reporting rationalization/streamlining (e.g. multi-GAAP reporting,

tax balances).• Implement at the business unit level using a top-down and bottom-up approach, with

business units involved earlier rather than later, as the impact can be profound.

IFRS – lessons learned from 100 countries

Slide 318th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Conversion costs and benefits of IFRS –the value of a preliminary study• Having the benefit of a realistic implementation timeline without the pressure of

mandatory adoption deadlines• There are still numerous differences between IFRS and US GAAP• IFRS resources are scarce and companies should begin to increase

IFRS knowledge• Potential for reduced cost of compliance• Potential to reduce operational risk and enhance the quality of financial reporting• Market considerations• Benchmarking with Peers• Audit Committees/Boards are starting to ask about IFRS; some are starting to

assess the impact now• Take advantage of any finance transformation initiatives or SAP Implementations/

Upgrades for ERP/consolidation systems to consider the implications of adopting IFRS

Slide 328th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Key IFRS drivers

Key motivator Actions takenCompany with significant international revenues motivated by analysts’ questions and a need to invigorate top management

Undertake a diagnostic focusing on understanding the key technical differences. Accounting, corporate development, systems and tax focus.

Desire to better understand status of local foreign adoptions and their accounting policy selections. Interest in exploring cost reduction opportunities through one GAAP reporting and shared services centers.

Design an electronic survey to identify past, current and future local adoptions, as well as state of readiness and opportunities for knowledge sharing.

Company with subsidiaries that are required to adopt IFRS by 2011 (e.g., Canada, Brazil, South Korea, Japan)

Corporate and subsidiary accounting and finance personnel working to develop common approach to education and conversion. Corporate to monitor and provide input on subsidiary adoption. Results in trained corporate personnel for future potential US statutory changes.

Worldwide SAP implementation requiring need to identify impact of dual GAAP reporting and options for ultimate adoption of IFRS as primary accounting language

Tailor “non-leading ledgers” to accommodate IFRS as part of SAP implementation on a country by country basis.

Interest in raising internal awareness level of IFRS. Provide training to finance, accounting, tax, actuarial and other users of financial information.

How IFRS may impact the processing environment

Slide 348th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Challenges that may arise with transitioning to IFRSThe transition, conversion, and implementation to IFRS should be viewed like any other new business requirement and the resulting transformational initiative to embed the requirement into the business. Like other business transformation events, management needs to consider the degree, complexity, and nature of implementing the new requirements:

STRATEGY:Lead Peers, “Wait & See”, “Big Bang Implementation”, Phase in Approach

ORAGANIZATION:Training, Roles & Responsibilities, etc.

PROCESS:Business Practices, Supporting Business Procedures, etc

TECHNOLOGY:Consolidations, Transactional Processing, Supporting Systems, etc.

GOVERNANCE:Business Policies, Compliance Rules, Controls, Management / Supervisory Oversight, Documentation

IFRS Requirements

Company Specific Accounting Changes

New Business and Accounting Policies

New Business Processes & Practices

TechnologyEnablement

People & O

rganization Change

Business R

equirements

Slide 358th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Illustrative Example –relative impact of IFRS on the processing environment

Key Accounting Topics Business Processing Technical Environment

Financial Consolidation & Reporting

Development Costs, including IPR&D

Revenue Recognition

Inventories

Property, Plant & Equipment

Intangible Assets

Provisions & Contingencies

Expense Recognition

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Lower HigherModerate

Rule of Thumb: ∆ Transactional Process Related Change∆ Analytical / Valuation Change∆ Presentation / Disclosure Change∆ Policy Change

Lower

HigherRelative Degree of: ∆ Change/Impact∆ Cost∆ Time to Complete∆ Complexity

Slide 368th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

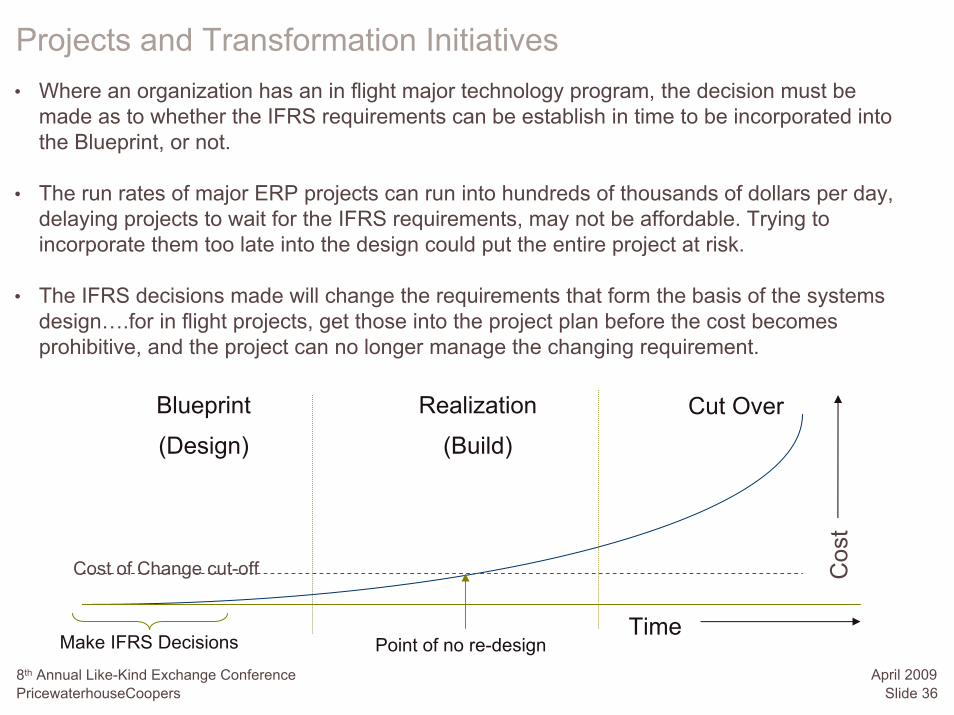

Projects and Transformation Initiatives

Time

Cos

t

Blueprint

(Design)

Realization

(Build)Cut Over

Point of no re-design

Cost of Change cut-off

Make IFRS Decisions

• Where an organization has an in flight major technology program, the decision must be made as to whether the IFRS requirements can be establish in time to be incorporated into the Blueprint, or not.

• The run rates of major ERP projects can run into hundreds of thousands of dollars per day, delaying projects to wait for the IFRS requirements, may not be affordable. Trying to incorporate them too late into the design could put the entire project at risk.

• The IFRS decisions made will change the requirements that form the basis of the systems design….for in flight projects, get those into the project plan before the cost becomes prohibitive, and the project can no longer manage the changing requirement.

Slide 378th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

TransitionIFRS methodology

Many of our ERP clients have a global ERP solution, and so changes made locally can have an impact globally.

Pre-Go Live Post Go LiveUS GAAP IFRS US GAAP IFRS

US Only Companies Primary Secondary Primary Blank Canvas to look at how to adopt IRFS

Global Companies (US Based)

Primary Secondary Secondary Primary One standard must apply…US might drive standard that impacts overseas businesses

Global Companies (US Operations)

Secondary Primary Secondary Primary One standard must apply…US adoption may be driven from overseas parent

Slide 388th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Consider the timing of ERP initiatives and IFRS conversion

ERP Initiatives -- Potential Timelines

Upgrades

Strategy

Functional

NewImplementations 2 to 5 Year Implementation Plan

IFRSConversionProjects

ERP Transaction Source Systems IFRS Ready

Financial Reporting Systems Ready

How long to get the ERP sourcesystem and the FinancialReporting systems IFRS ready?

Technical

(3 to 6 months)

(3 to 12 months)

(1 to 2 years)

Anticipated IFRS Conversion and Implementation Timeline

Early US adoption?1

USpreparation

SEC determines mandatory dates and approach

Periods in 1st US financials

Transition date – Opening IFRS balance sheet

Beginning of IFRS mandatory adoption

Non-US subsidiary IFRS preparation

2008 2009 2010 2011 2012 2013 2014

Slide 398th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

ERP steady state IFRS planning (example)

Res

ourc

e R

equi

rem

ents

Time

Existing Projects in the Sustainment Organizations Multi-Year Plan

Upgrades Add Modules New Consolidation System Archiving

2012 2013201120102009

Global Adoption of IFRS

• With early identification of the business requirements, both in the US and Globally of IFRS, the people, process and technology impacts can be quantified

• This will take some additional resources and costs upfront, but will be no where near the cost of an 11th hour attempt to get the systems to support IFRS

• Getting IFRS and an IFRS Blueprint into the governance and change control process will allow the global introduction of IFRS country by country without major system disruption, and will allow the pain points for a particular organization to be managed over time.

Planned resources with limited lead time to IFRS embedding

Planned resources with good lead time to IFRS embedding

Current planned resources supporting identified projects

Current Steady State

Key

Slide 408th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

How IFRS may impact the ERP processing environment

Key themes and take-aways:

What Can Change: IFRS should be viewed as a new business requirement and management should evaluate what could be impacted just like any other transformation project that supports a business initiative

Degree of Change: IFRS requirements that need to be addressed or need to be considered at the business transaction level, will most likely, have more impact on the ERP environment than those requirements that do not need to consider, address, or tie-out to the transaction level. In addition, management action plans for meeting the IFRS requirements will dictate how much has to be changed.

Current Initiatives: Look at current ERP projects and related transformation initiatives – consider timing in conjunction with both IFRS conversion time requirements and new IFRS conversion / readiness projects

Specific PPE challenges

Slide 428th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

PP&E – challenges

• Consistency of accounting policies• Cost of significant components must be separately identified and depreciated to

their residual values over their useful lives. Identifying significant components can be a complex process for very large, advanced plants.

• Data management considerations given the number of potential components that may require separate identification and measurement.

• PPE must me assessed for qualitative indicators each reporting periods and must have process in place to record and reverse impairments if necessary.

• Identification of constructive obligations for asset retirement obligations; therefore additional reviews would be necessary.

• Additional judgment of classification of lease agreements.

Slide 438th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

PP&E challenges in an IFRS conversion

• Adjustments to PP&E can occur in many areas, including:- Componentization- Impairment- Technology

• First time adoption of IFRS provides transitional opportunities that companies should consider

Slide 448th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Componentization

• How significant of an issue is componentization?

- Accounting for PP&E in smaller components can require a manual effort to disaggregate existing PP&E data into smaller components

- Systems might be challenged by increase in data requirements

• To assess the issue, companies should:

- Review current US GAAP policies to assess whether PP&E can be further componentized

- Review gain / loss information on disposal / replacement of PP&E

- Consider whether stat-to-GAAP adjustments exist for statutory locations reporting under IFRS

Slide 458th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Impairments

• Both IFRS and US GAAP test PP&E for impairment when there is an indicator

• IFRS and US GAAP test PP&E at similar levels

• US GAAP uses a two step impairment model:

- Step 1 – compare PP&E / asset group carrying amount to undiscounted future cash flows

- Step 2 – If step 1 failed, write PP&E down to its fair value

• IFRS uses a single step model to measure impairment losses:

- Comparison of the carrying amount to its recoverable amount

- Recoverable amount is the higher of fair value less costs to sell and value in use.

Slide 468th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

PP&E – technology impact

• Potential process and technology impact would be related to componentization as it would need additional data elements for different depreciable life categories to support additional depreciation calculations.

• New processes and changes to the fixed asset sub-ledger may be needed to capture, process and record fixed asset data at a more granular level.

• Modifications to systems may result in interface and mapping changes, changes to the chart of accounts, changes to reporting packs and financial reporting tools and modifications to account for documentation and archiving.

Slide 478th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

First time adoption considerations

• As a general principle, IFRS 1 required the opening balance sheet be presented as if the company had always applied IFRS.

• This requires retrospective application of IFRS policies, including those relating to PP&E

• However, IFRS 1 provide an optional exemption relating to PP&E:

- An entity may elect to measure an item of PP&E to its fair value at the transition date

- This amount becomes deemed cost at that date

- Exemption is available on an asset by asset determination

Slide 488th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

First time adoption considerations

• Applying fair value as deemed cost requires strategic consideration:

- Will the fair value adjustments affect cash management strategies

- Are distributable reserves affected?

- Are there cast tax implications?

- How will future financial performance be affected?

Slide 498th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

PP&E – initial measurement of components

Approaches to the Componentization Challenge faced by companies:

• Regulatory Approach

- Depreciation studies, Cost recovery method and Regulatory components.

• Fair Value Allocation Approach

- Use of relative fair value to allocate gross book value to significant components.

• Capex Forecasting Approach

- Use of capital expenditures forecast to identify significant components.

• Third party Valuation Approach

- Appointing and working with a third party to perform the componentization exercise.

Summary

Slide 518th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

In summary

Market & Internal challenges PwC supporting your needs• IFRS is gaining momentum in the US and its

eventual adoption is inevitable• Easier access to the capital markets outside

the US • Stakeholders are requesting IFRS information

and want to understand the impact of differences between US GAAP and IFRS

• Global competitors are already applying IFRS• IFRS resources in the US are scarce• Time and effort to convert from US GAAP to

IFRS is not a small task• ERP upgrade plans defined long in advance and

difficult to rescope once underway

• Experience performing thousands of conversions worldwide

• Flexible, tailored and phased approach to IFRS conversions with proprietary tools enhanced over the past 10 years

• Use of a integrated resource team to drive conversions

• Early identification and resolution of issues • Professionals that bring a financial, operational,

tax and ERP technical expertise to the table• Control of process and outcome maintained by

effective project management

Slide 528th Annual Like-Kind Exchange ConferencePricewaterhouseCoopers

April 2009

Next steps - companies

• Approach IFRS in a thoughtful, strategic manner

• Perform assessment – identify what makes sense to start now…and what doesn’t

• Invest only in the most significant areas of IFRS-related impact

• Follow developments in the joint IASB and FASB projects

• Incorporate IFRS in key business planning activities

• Corporate oversight relating to subsidiaries adopting IFRS

© 2008 PricewaterhouseCoopers LLP. All rights reserved. "PricewaterhouseCoopers" refers to PricewaterhouseCoopers LLP or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity. PwC