a cross-country study on the relationship between ... full_paper_final.pdf · a cross-country study...

TRANSCRIPT

A cross-country study on the relationship

between financial development and earnings management

Masahiro Enomoto*

Kobe University, Kobe, Japan

Fumihiko Kimura†

Tohoku University, Sendai, Japan

Tomoyasu Yamaguchi‡

Tohoku Gakuin University, Sendai, Japan

February 2014

Acknowledgments

The authors gratefully acknowledge the financial support from The Japan Securities Scholarship

Foundation and Ishii Memorial Securities Research Foundation.

* Corresponding author

Research Institute for Economics & Business Administration, Kobe University, 2-1 Rokkodaicho, Nada-ku, Kobe

657-8501, JAPAN. E-mail: [email protected]. Tel: +81-78-803-7031; fax: +81-78-803-7031. † Graduate School of Economics and Management, Tohoku University, 2-2-1 Katahira, Aoba-ku, Sendai 980-8576,

JAPAN. E-mail: [email protected]. Tel: +81-22-217-6282; fax: +81-22-217-6282. ‡ Faculty of Business Administration, Tohoku Gakuin University, 1-3-1 Tsuchitoi, Aoba-ku, Sendai 980-8511,

JAPAN. E-mail: [email protected]. Tel: +81-22-721-3471; fax: +81-22-721-3471.

A cross-country study on the relationship

between financial development and earnings management

Abstract

This paper investigates whether the level of financial development influences earnings

management in an international setting. We deal with accrual-based and real earnings

management. While prior cross-country research on financial accounting treats legal traditions,

outside investor protection, and corporate governance as non-accounting institutions, we focus

on financial development. Financial development is defined as the factors, policies, and

institutions that lead to effective financial intermediation and markets, as well as deep and broad

access to capital and financial services (The World Economic Forum, 2012). Given financial

accounting’s key role of offering information to investors, under the accounting standards of

each country, we propose that there is a link between financial development and the resulting

outcomes from accounting institutions. We examine the relationship between financial

development and both types of earnings management using 54,178 observations in 37 countries

from 2009 to 2012. The results show that a manager is restrained in both types of earnings

management when under a higher level of financial development. We interpret the results as

showing (1) higher quality accounting information is needed in countries with more developed

financial systems, (2) there is a link between financial development and accounting institutions

in each country, and (3) financial development disciplines managers and mitigates their

incentives to manage earnings.

JEL Classification: M41

Key Words: Financial development, Accounting institutions, Earnings management

1

1. Introduction

The purpose of this paper is to investigate whether the level of financial development in a

country influences earnings management in that country. Financial development is closely

related to the spread of financial accounting. We focus on financial development as a crucial

factor of managerial discretion internationally. Our measure for financial development is based

on the World Economic Forum. The scores cover a wide range of institutional factors used in

prior research. The results of this paper provide some evidence that financial development

influences the reporting incentive of a country’s manager in an international setting. In other

words, we show a relationship between accounting institutions and non-accounting institutions.

Leuz and Wysocki (2009) and Wysocki (2011) emphasized new institutional accounting

research that focuses on relationships between accounting and institutional factors. They point

to two critical issues; that accounting institutions are key economic institutions, and that a

linkage between accounting institutions and non-accounting institutions exists. Accounting

institutions include accounting standards, disclosure systems, audits, and so forth.

Non-accounting institutions include legal systems, corporate governance mechanisms, the

existence and enforcement of laws governing investor protection, and disclosure standards

(Wysocki, 2011, 312). Both institutions vary from country to country.

A useful method in new institutional accounting research is cross-country analysis. For

example, Ball, Robin, and Wu (2003) investigate the properties of accounting income in four

countries (Hong Kong, Malaysia, Singapore, and Thailand) and show that “their financial

reporting quality is not higher than under code law, with quality operationalized as timely

recognition of economic income (particularly losses).” As for non-accounting institutions, Leuz,

Nanda, and Wysocki (2003) and Boonlert-U-Thai, Meek, and Nabar (2006) define investor

protection as the power to prevent managers from expropriating minority shareholders and

creditors within the constraints imposed by law. Leuz, Nanda, and Wysocki (2003) examine the

relationships between outside investor protection and earnings management in 31 countries,

from 1990 to 1999, and find that earnings management decreases in countries with stronger

2

investor protection. Boonlert-U-Thai, Meek, and Nabar (2006) also investigate earnings

management in 31 countries, from 1996 to 2002, and they suggest that earnings are smoothed in

countries where investor protection has progressed. Bushman and Piotroski (2006) examine

conservatism in earnings among the countries, and suggest that various institutions, such as

legal systems, ownership structures, and taxation, have an effect on the degree of conservatism.

While prior cross-country research on financial accounting treats legal traditions, outside

investor protection, and corporate governance as non-accounting institutions, we focus on

financial development. Financial development is defined as the factors, policies, and institutions

that lead to effective financial intermediation and markets, as well as deep and broad access to

capital and financial services (The World Economic Forum, 2012). Given financial accounting’s

key role of offering information to investors, under the accounting standards of each country, we

propose that there is a link between financial development and the resulting outcomes from

accounting institutions.

In this paper, we measure financial development based on The Financial Development

Report from the World Economic Forum.1 The report ranks 62 countries according to different

aspects of complex financial systems. These are based on research and data from organizations

such as the World Bank and the IMF including the institutional environment, the business

environment, financial stability, banks, capital markets, overall capital availability, and access.

They are used frequently in research on financial development, and reflect the various aspects of

non-accounting institutions. They are, therefore, suitable measures for our research. In addition,

the scores for rank are updated annually, and those that relate to institutional factors are usually,

in most previous cross-country research, fixed in the sample period. In fact, these scores should

vary with economic circumstances and revisions of laws and regulations. It is, therefore,

appropriate for this study to adopt the scores of the World Economic Forum, and it should be

noted that almost all scores are changing every year. For example, the score relating to the

1 The World Economic Forum is an independent international organization committed to improving the state of the

world by engaging business, political, academic and other leaders of society to shape global, regional and industry

agendas (http://www.weforum.org/).

3

institutional environment in the United Kingdom has risen from 5.54 in 2009 to 6.00 in 2012.

Looking at previous research, we focus on earnings management as an economic

consequence caused by accounting institutions. Earnings management is one of the subjects of

capital market-based accounting research and positive accounting theory, and is a crucial factor

affecting accounting quality (see Dechow, Ge, and Schrand, 2010). Because accounting

information is essential to the development of financial markets and transactions, financial

development brings about the expanded use of accounting information.

This could lead to two patterns in the relationship between earnings management and

financial development. One is that earnings management is more often implemented in

countries with higher financial development, because a growing use of accounting information

produces a greater benefit from earnings management. The other is that earnings management is

restricted in countries with higher financial development, because earnings management is

strictly monitored or more severely punished in some cases. Further, while extensive research

relating to earnings management has covered accrual-based earnings management (AEM), we

focus on real earnings management (REM) that affects a firm’s real activities.

This paper examines the relationship between AEM, REM, and financial development by

using 54,178 observations in 37 countries from 2009 to 2012. The results show that managers

are restrained from using both AEM and REM when under higher financial development. Our

evidence is robust, with the use of multiple financial development scores and the exclusion of

observations from U.S. and Japan and the elimination of firm-years in 2009.

The most important contributions of this paper are as follows. First, we expend on the

earnings management research by investigating the relationship between financial development

and earnings management. Our paper provides the evidence that financial development restrains

earnings management, both AEM and REM, by disciplining a manager’s behavior. The results

suggest that managers in countries with more developed financial systems are required to

provide a higher level of transparency with regard to their financial accounting information. In

other words, financial development leads to increased monitoring, scrutiny, and punishment

4

from outside of the firm and puts pressure on a manager’s ability to manipulate a firm’s real

activities as well as accruals. Although prior research has already shown negative relationships

between AEM and investor protection, there is scant evidence of an association between

earnings management and financial development. We added the REM measures of

Roychowdhury (2006) as a proxy to capture managers’ discretionary behavior at the

international level while Leuz, Nanda, and Wysocki (2003) and Haw, Hu, Hwang, and Wu

(2004) use AEM mainly as a proxy for earnings management. Our results are also in conflict

with Francis, Hasan, and Li (2011) who show that the substitution of REM for AEM in

countries with stronger investor protection is prevalent. This substitution is frequently observed

in prior research that uses data from a single country setting, but it is not found at the

international level in our study.

Second, we refine the global impact of financial development on accounting at a firm level

employing the comprehensive measure of financial development. Further, our score includes

many institutional factors which prior research frequently employ as a critical determinant of

earnings management at the international level. Therefore, this paper contributes to a growing

literature evaluating the factors of international differences in the quality of accounting

information.

The remainder of the paper is organized as follows. Section 2 considers the relationship

between earnings management and financial development. Section 3 delineates the research

design of the study. Section 4 contains the results of the econometric analysis. Section 5

concludes the paper with an extensive discussion of suggestions for future research.

2. Hypothesis development

2.1. Financial development and earnings management

The circumstances surrounding a firm’s financing activities differ from one country to another.

A great deal of cross-country research into financial theory suggests that financial development

is related to economic growth. For example, Beck and Levine (2004) use a dataset of 40

5

countries, from 1976 to 1998, and conclude that fully functional financial systems ease

information and transaction costs and thereby enhance resource allocation and economic growth.

The World Economic Forum (2012, xiii) defines financial development as the factors, policies,

and institutions that lead to effective financial intermediation and markets, as well as deep and

broad access to capital and financial services. It also points out that financial development is

dictated by seven pillars, specifically (1) Institutional environment, (2) Business environment,

(3) Financial stability, (4) Banking financial services, (5) Non-banking financial services, (6)

Financial markets, and (7) Financial access. Each pillar aggregates 12 to 26 indices.2

All pillars have a relationship with financial accounting to a greater or lesser extent. This

paper aims to examine the effect of financial development on financial accounting. However,

three pillars, (2) Business environment, (3) Financial stability, and (7) Financial access,

associate only weakly with financial accounting. Therefore, we have deleted these three pillars

and selected the remaining four from the perspective of the importance of financial accounting.

The definition of the seven pillars and the reason for eliminating the three is described in

Section 3.2.

Next, we discuss the relationship between financial accounting and financial development.

Financial accounting is expected to play an important role in the financial systems of each

country and in the global financial system. The FASB Statement of Financial Accounting

Concepts No. 1 states that financial reporting should provide information that is useful to

present and potential investors in making rational investment decisions (par. 34), and provide

information to help present and potential investors in assessing the amounts, timing, and

uncertainty of prospective cash receipts (par. 37). In addition, the conceptual framework of

International Financial Reporting Standards (IFRS) states that the objective of general purpose

financial reporting is to provide financial information about the reporting entity that is useful to

present and potential equity investors, lenders, and other creditors in making decisions in their

capacity as capital providers. Information that is decision useful to capital providers may also be

2 See The World Economic Forum (2012, 313-383) for details of the indices.

6

useful to other users of financial accounting information who are not capital providers (IASB,

2008, OB2).3

Wysocki (2011, 311) points out that accounting is one institutional mechanism that can help

lower transaction costs, reduce information costs and information asymmetry, lower

coordination costs and improve enforcement of property rights, and that accounting is the

growing body of evidence about which institutions are the primary mechanisms for financial

market development. This suggests that the goal of offering accounting information is to

develop and maintain the financial system in a country. However, in order to achieve this goal,

the accounting information presented by managers is subject to monitoring and scrutiny by

auditors and stakeholders. Managers prepare financial statements under pressure. We, therefore,

argue that higher quality accounting information is required in countries with more developed

financial systems.

The quality of accounting information is affected by earnings management. Earnings

management is defined as the choice by a manager of accounting policies, or real actions that

affect earnings so as to achieve a specific reported earnings objective (Scott, 2011, 423). Some

previous research suggests that the motivation of earnings management is related, to an

appreciable degree, to financing activities and related legal issues. Examples discussed are

raising stock prices in an initial public offering (Teoh, Welch, and Wong, 1998a), secondary

equity offering (Teoh, Welch, and Wong, 1998b), avoiding debt covenant violation (Bikky and

Picheng, 2002), meeting or beating analyst expectations (Bartov, Givoly, and Hayn, 2002), and

the Sarbanes-Oxley Act of 2002 (Cohen, Dey, and Lys, 2008).

Based on the above discussions, there are two scenarios in the relationship between earnings

management and the financial development of each country. One is that higher financial

development is likely to encourage earnings management because managers acquire the benefits

of spreading the use of accounting information about stakeholders. Another is that higher

financial development is likely to constrain earnings management. The reason is that, with

3 Examples of other users of financial accounting information that are not capital providers are regulators, securities

exchanges, analysts, auditors, and so forth.

7

financial development, managers fear monitoring, scrutiny, and punishment from outside of the

firm, and new accounting standards, that narrow their discretion to achieve target income, might

be adopted.4

2.2. The choice between AEM and REM

In this subsection, we explain the two types of earnings management, provide an overview of

previous research into earnings management in an international setting, and develop our

hypotheses. As mentioned in section 1, earnings management is divided into AEM and REM.

AEM alters the accrual process to manage earnings. AEM leads to the reversal of accruals in

subsequent periods, but does not have a direct effect on cash flow.5 Unlike REM, managers are

allowed to implement AEM after the period-end. REM reflects a firm’s real activities and

manages earnings through changing the timing or structure of an operating, investment, or

financial decision. REM may reduce future cash flow due to non-optimal decisions, such as

opportunistically reducing R&D and advertising costs, increasing price discounts, and

overproducing to decrease unit costs.

Prior research shows that there is the relationship between earnings management and

institutional factors in international settings, employing mainly accrual-based measures as a

proxy for earnings management. Leuz, Nanda, and Wysocki (2003) look at 31 countries, from

1990 to 1999, and show that AEM decreases in countries with stronger investor protection.6

Similar findings are also shown in Haw, Hu, Hwang, and Wu (2004) using 31 countries, from

1996 to 1999. Boonlert-U-Thai (2006) investigates the relationship between investor protection

4 The former is that financial development (i.e. non-accounting institution) directly influences the manager’s

incentives to manage earnings. For example, the extent of anti-director rights and/or legal enforcement (Leuz, Nanda,

and Wysocki, 2003; Francis, Hasan, and Li, 2011) and the number of analyst followings in countries with high

financial development (Degeorge, Ding, Jeanjean, and Stolowy, 2013) have been tested. Investor protection by law

and financial intermediation are incorporated into our financial development score (see details in section 3.2.). The

latter is the indirect effect of financial development on earnings management via the changes in accounting

institutions. Barth, Landsman, and Lang (2008) and Ipino and Parbonetti (2011) examine the impact of the adoption

of IFRS on accounting quality. In other words, there are two possible channels where financial development might

impact earnings management. We do not distinguish between the direct and indirect effect, but financial development

probably influences all the examples above. 5 The reversal of accruals is detailed in Dechow, Hutton, Kim, and Sloan (2012). 6 Three of the four measures of earnings management in Leuz, Nanda, and Wysocki (2003) are based on accruals and

can, therefore, be regarded as AEM. Another is loss avoidance.

8

and AEM in 31 countries, from 1996 to 2002, and suggests that earnings are smoothed by

accruals in countries where investor protection has progressed. Francis and Wang (2008) use 49

countries, from 1995 to 2004, and provide evidence that earnings quality improves at firms

audited by brand name auditors in countries with stronger investor protection.7 Generally,

financial development requires stricter investor protection. From the above discussion, we

predict that AEM is decreases with financial development.

Degeorge, Ding, Jeanjean, and Stolowy (2013) use 21 countries, from 1993 to 2002 and find

that analyst following negatively affects AEM in countries with high levels of financial

development. However, it is not clear if financial development has a direct effect on AEM.

Next, we should review the relationship between AEM and REM in an international setting,

but little research has been done on this. Francis, Hasan, and Li (2011) show that REM is

encouraged and AEM is discouraged in countries with stronger legal environments, but they do

not include critical variables relating to financial development8 Enomoto, Kimura, and

Yamaguchi (2013) also investigate the relationship between AEM, REM, and investor

protection. Although they use analyst following as a proxy for financial intermediaries, their

discussion and analysis are based on country data rather than firm-year data.

A manager may choose AEM and/or REM to manage earnings under the prevailing economic

conditions. Many studies have pointed out that managers tend to employ REM rather than AEM

to achieve target income since AEM is more likely to incur the scrutiny of auditors, regulators

and others (Graham, Harvey, and Rajgopal, 2005; Roychowdhury, 2006; Cohen and Zarowin,

2010; Gunny, 2010). Kim, Lei, and Pevzner (2010) also argue that AEM may lead to litigation,

SEC investigation, and criminal liability for managers as well as the scrutiny of auditors. Their

research suggests that AEM may be costly when it is revealed.

Meanwhile, Kothari, Mizik, and Roychowdhury (2012) state that REM is easier to

camouflage as normal activities than AEM. Further, they argue that discretion, relating to

7 We can interpret their finding in relation to AEM, because their evidence is based on abnormal accruals. 8 Ipino and Parbonetti (2011) also show that a substitution between AEM and REM is detected when IFRS becomes

mandatory.

9

operating and investment activities, is inherently given to managers by shareholders. From

surveys and interviews with executives, Graham, Harvey, and Rajgopal (2005) present evidence

suggesting that managers prefer REM because they fear overzealous regulators. Prior research

has argued that managers may prefer REM to avoid the scrutiny and oversight of stakeholders,

in spite of the higher cost to the firm in the future. Graham, Harvey, and Rajgopal (2005) and

Cohen and Zarowin (2010) state that REM that reduces maintenance, advertising costs, and

positive NPV investments may be more costly to firms than AEM as this behavior may not

maximize the future value of the firm. Badertscher (2011) finds that managers compare the

future cost of AEM and REM, and employ REM before AEM.

One purpose of this paper is to clarify whether REM would be employed more in countries

with higher financial development. If financial development heightens the monitoring and

scrutiny of accounting figures, then AEM is less prevalent under high financial development,

and more prevalent under low financial development. Does the manager, then, substitute AEM

with REM, or avoid both AEM and REM in an environment of high financial development? As

mentioned in the previous subsection, accounting information under higher financial

development plays an important role in a range of decision making in financial markets and

firms, as well as in the enforcement of many kinds of laws, regulations, and contracts. Relevant

and reliable accounting information is typically required for investors to take risks and make

decisions.

Accounting standards can, therefore, be regarded as regulations for firms and their revision

can result in managers engaging in discretionary behaviors. Ewert and Wagenhofer (2005)

analytically show that tight accounting standards restrict managers’ discretion to manipulate

accruals, leading them to prefer REM. In addition, Cohen, Dey, and Lys (2008) provide

evidence that managers have shifted away from AEM to REM in the post Sarbanes–Oxley Act

(SOX) period. The passage of SOX can be seen as strengthening regulations, thus increasing the

restraint on employing AEM and leading to an inducement to employ REM. Chi, Lisic, and

Pevzner (2011) provide evidence that managers tend to avoid AEM under higher quality audit

10

conditions, which in turn leads to the employment of REM.

The scrutiny of auditors, therefore, reduces AEM, but increases REM. The research provides

evidence of a substitution between AEM and REM as AEM becomes increasingly constrained.

In fact, Francis, Hasan, and Li (2011) conclude that managers in countries with stronger legal

environment face a higher risk of litigation due to AEM and, therefore, resort to focusing on real

activities. If we assume that financial development can be regarded as a type of institutional

factor, analogous to investor protection, then it may lead managers to reduce AEM and shift to

REM instead.

However, Leuz, Nanda, and Wysocki (2003, 506) mention that “strong and well enforced

outsider rights limit insiders’ acquisition of private control benefits and, consequently, mitigate

insiders’ incentives to manage accounting earnings because they have little to conceal from

outsiders.” The mitigation of managers’ incentives may reduce overall managerial discretionary

behaviors, both AEM and REM. We can infer that as managers are disciplined by strengthening

regulation and investor protections other than the legal system, they will avoid AEM and REM

in the development of financial systems.

Monitoring and scrutiny by stakeholders also discipline managers’ behavior. Wongsunwai

(2013) shows that firms backed by higher quality venture capital do not appear to engage in

both REM and AEM. This means that high quality venture capitalists monitor their portfolio

companies closely and effectively and then behave rationally leading to a constraint of REM. In

other words, sophisticated investors understand the future implications of REM and take into

consideration in decision-making. Kim and Sohn (2013) find that cost of capital positively

relates to REM, when compared with AEM. Based on this evidence, it appears that rational

investors see through the adverse effects on future cash flow of REM. These studies also

suggest that sophisticated market participants monitor managers’ value-destroying behavior and

effectively restrain managers from earnings management by compelling them to keep

stakeholders’ reactions in mind.

What is the effect of financial development on AEM and REM? With higher financial

11

development, more accounting information is required. Financially sophisticated stakeholders

pay close attention to the accounting numbers. Therefore, we hypothesize that managers tend to

avoid AEM where there is higher financial development. For REM, our hypotheses are twofold.

First, if the substitution effect between the two types of earnings management occurs, REM is

restrained in countries with high financial development since AEM becomes more costly.

Second, earnings management, both AEM and REM, reduces with high financial development,

because managers are disciplined by higher financial development. In the next section, we

provide the research design to test the hypotheses.

3. Research Design

3.1. Earnings management measures

3.1.1. Accrual-based earnings management measure

Following previous research (e.g., Warfield, Wild, and Wild, 1995; Becker, DeFond,

Jiambalvo, and Subramanyam, 1998; Cohen, Dey, and Lys, 2008), we use the absolute value of

abnormal accruals as an AEM measure in order to capture both the effects of income-increasing

and income-decreasing AEM. To measure abnormal accruals, we use the cross-sectional

modified Jones (1991) model (see DeFond and Jiambalvo, 1994; Dechow, Sloan, and Sweeney,

1995; Becker, DeFond, Jiambalvo, and Subramanyam, 1998). Specifically, we estimate the

following regression model for each industry-year combination in each country, where industry

is identified by a two-digit SIC code.

ACCijt / Aijt-1 = β0 + β1 (1 / Aijt-1) + β1 ((ΔSijt - ΔARijt) / Aijt -1) + β3 (PPEijt / Aijt -1) + εijt (1)

ACC is accruals that is calculated by net income minus operating cash flow reported in the

statement of cash flow; A is the total assets; ΔS is the change in net sales; ΔAR is the change in

accounts receivable; PPE is the net property, plant, and equipment; the subscripts refer to firm i,

country j, and time t. Abnormal accruals are calculated as the estimated residuals from equation

12

(1), and its absolute value is our proxy for AEM (|A_ACC|).

3.1.2. Real earnings management measures

Following Roychowdhury (2006), Cohen, Dey, and Lys (2008), and Cohen and Zarowin

(2010), we developed the proxy for three methods of REM: (1) sales manipulation, (2) reduction

of discretionary expenses, and (3) overproduction. Sales manipulation is managers' behavior

that tries to increase sales through price discounts or more lenient credit terms. As long as the

margins are positive, the additional sales will increase earnings in the current period. However,

both price discounts and more lenient credit terms lead to lower margins, resulting in lower cash

flow from operations (CFO) and higher production costs compared with the sales.

Reduction of discretionary expenses can also be an earnings management method. Managers

can increase earnings by the reduction of discretionary expenses such as R&D and advertising

costs. Reducing such expenses should lead to low discretionary expenses.

Overproduction is the production of greater than expected demand in order to increase

earnings. If managers engage in overproduction, fixed overhead costs are allocated to a larger

number of units, thereby lowering fixed costs per unit. As long as the decrease in fixed costs per

unit is not offset by any increase in marginal cost per unit, the total cost per unit decreases. As a

result, this decreases the cost of goods sold and increases earnings. However, overproduction

leads to higher production costs and lower CFO than normal production level given the sales,

because of additional production and holding costs.

In summary, sales manipulation and overproduction lead to abnormally high production costs

relative to sales, and abnormally low cash flow from operating activities relative to sales, while

the reduction of discretionary expenditures leads to abnormally low discretionary expenses

(Roychowdhury 2006, 340-341).9

To measure the abnormal level of CFO (A_CFO), discretionary expenses (A_DE), and

production costs (A_PD), we estimate the following regression models. Similar to equation (1),

9 If the firm paid for discretionary expenses in cash, reduction of discretionary expenses could also lead to

abnormally high cash flow (Roychowdhury 2006; Cohen and Zarowin 2008).

13

the regression models are estimated for each industry-year combination in each country, where

industry is identified by a two-digit SIC code.

CFOijt / Aijt-1 = β0 + β1 (1 / Aijt-1) + β2 (Sijt / Aijt-1) + β3 (ΔSijt / Aijt-1) + εijt (2)

DEijt / Aijt-1 = β0 + β1 (1 / Aijt-1) + β2 (Sijt-1 / Aijt-1) + εijt (3)

PDijt / Aijt-1 = β0 + β1 (1 / Aijt-1) + β2 (Sijt / Aijt-1) + β3 (ΔSijt / Aijt-1) + β4 (ΔSijt-1 / Aijt-1) + εijt (4)

CFO represents the operating cash flows reported in the statement of cash flows; DE represents

the selling, general, and administrative expenses; PD represents production costs and is

calculated as the cost of goods sold plus the change in inventory; and S represents the net

sales.10

A_CFO, A_DE, and A_PD are calculated as the estimated residuals from equations (2),

(3), and (4), respectively.

Since the three types of REM described above might be implemented to decrease earnings,

consistent with Francis, Hasan, and Li (2011) and Kim and Sohn (2013), we convert A_CFO,

A_DE, and A_PD to the absolute values and use them as our REM proxies (|A_CFO|, |A_DE|,

and |A_PD|, respectively).11

In addition, we combine these three measures to capture the total

effects of REM. Consistent with Cohen and Zarowin (2010), we multiply A_CFO and A_DE by

negative one, and add them to A_PD in order that higher values indicate greater

income-increasing earnings management. Again, considering the possibility of

income-decreasing REM, we convert the aggregated REM measure to the absolute values and

use it as our fourth REM proxy (|REM|).

10 Following Bartov and Cohen (2009) and Gunny (2010), we use selling, general, and administrative expenses as

discretionary expenses because they frequently include discretionary expenses such as R&D and advertising costs. 11 For example, Francis, Hasan, and Li (2011) point out the possibility of income-decreasing real earnings

management from an income-smoothing perspective. When a firm’s performance is good in the current period,

managers may choose to spend more on R&D, advertising, employee training, etc. These activities have an

income-decreasing effect for the current year but an income-increasing effect for future periods (Francis, Hasan, and

Li, 2011, 9).

14

3.2. Financial development measures

We adopted the financial development score used by the World Economic Forum. The reason

for this is that it takes a comprehensive view when assessing the factors that contribute to the

long-term development of financial systems (The World Economic Forum, 2012, xiii). It also

includes various factors that are used in prior cross-country research on financial accounting,

such as corporate governance, legal and regulatory issues, and contract enforcement. The World

Economic Forum has provided a score and rank for the breadth, depth, and efficiency of 62 of

the world’s leading financial systems and capital markets since 2008. The index analyzes drivers

of financial system development that support economic growth, and thus compares the overall

competitiveness of financial systems (The World Economic Forum, 2012, xiii).

The World Economic Forum (2012, xiii) defines seven pillars as follows. (1) Institutional

environment encompasses financial sector liberalization, corporate governance, legal and

regulatory issues, and contract enforcement. (2) Business environment considers human capital,

taxes, infrastructure, and costs of doing business. (3) Financial stability captures the risk of

currency crises, systemic banking crises, and sovereign debt crises. (4) Banking financial

services measure size, efficiency, and financial information disclosure. (5) Non-banking

financial services include IPO and M&A activity, insurance, and securitization. (6) Financial

markets encompass foreign exchange and derivatives markets and equity and bond market

development. (7) Financial access evaluates commercial and retail access.

A pillar is scaled from one to seven. The financial development score is the average of the

scores relating to the seven pillars. Since all of the pillars cannot be associated with financial

accounting (and resulting earnings management), we extracted the scores from four pillars out

of the seven (Institutional environment, Banking financial services, Non-banking financial

services, and Financial markets) as the factors most closely related to financial accounting.

First, as is demonstrated above the definition of (1) Institutional environment defines overall

financial development as a fundamental structure. This pillar includes the overall laws,

regulations, and supervision of the financial sector, as well as the quality of contract

15

enforcement and corporate governance (The World Economic Forum 2012, 5). Financial

accounting is essential for all of these to work efficiently. Leuz, Nanda, and Wysocki (2003)

claim that strong investor rights and strong legal enforcement discipline managers, making

earnings management appear to be lower.

Next, (4) Banking financial services, (5) Non-banking financial services, and (6) Financial

markets are chosen. It is self-evident that accounting information smooth transactions among

firms and stakeholders within the framework of the pillars. A large number of studies have

looked at earnings management in these areas. We, therefore, focus on the above four pillars in

the main analysis that follows and our financial development score (FD) is the average score of

these.12

Unlike the four pillars, (2) Business environment, (3) Financial stability, and (7) Financial

access can be considered to have an indirect linkage to financial accounting. (3) Financial

stability is excluded because this pillar focuses on the financial crises that affect economic

growth. In a similar vein, (7) Financial access is dropped because it is assumed that greater

access to financial services is associated with the usual proxies for financial development and

resulting economic growth. At first glance (2) Business environment, including taxation policy

and the costs of doing business, seems to relate to financial accounting. However, judging from

the definition of the indices that constitute the pillar, major parts of the index are remotely

related to the necessity for financial accounting. It is, therefore, eliminated from our financial

development score.

The World Economic Forum (2012, 5) divides the seven pillars into three categories:

Financial intermediation; Financial access; and Factors, policies, and institutions. Financial

intermediation includes (4) Banking financial services, (5) Non-banking financial services, and

(6) Financial markets.13

Financial intermediation is defined as the variety, size, depth, and

efficiency of the financial intermediaries and markets that provide financial services. Our

12 In the robustness checks in section 4.3, we test using the original financial development score. 13 Factors, policies, and institutions comprise the Institutional environment, Business environment, and Financial

stability. It is defined as the foundational characteristics that allow the development of financial intermediaries,

markets, instruments, and services.

16

financial development score can, therefore, be interpreted as the financial intermediaries and the

institutional environment supporting them.

3.3. The models to test the hypotheses

To examine the relationship between financial development and earnings management, we

estimate the following regression model.

EMijt = β0 + β1 FDjt + β2 Leverageijt-1 + β3 Sizeijt-1 + β4 MTBijt-1 + β5 ROAijt + β6 NOAijt-1

+ Σ β Year_Fixed_Effect + Σ β Firm_Fixed_Effect + εijt (5)

EM represents the earnings management proxies, that is, either |A_ACC|, |A_CFO|, |A_DE|,

|A_PD| or |REM|; FD is the mean value of four pillars (Institutional environment, Banking

financial Services, Non-banking financial services, and Financial markets) in the financial

development report of the World Economic Forum; Leverage is total debt divided by total

assets; Size is the natural logarithm of the market value of equity; MTB is the market to book

ratio; ROA is the net income divided by lagged total assets; NOA is the net operating assets

divided by sales.14

When the dependent variable is the proxy for AEM (that is |A_ACC|), we predict that the

coefficient of FD has a negative sign. On the other hand, when the dependent variable is the

proxy for REM (that is |A_CFO|, |A_DE|, |A_PD|, or |REM|) the sign of the coefficient of FD

should be negative (positive) if REM is more restrained (engaged) in countries with higher

levels of financial development. In addition to FD, some variables are included to control other

factors likely to affect the earnings management proxies. Leverage is included because previous

research finds that it is related to earnings management measures (e.g., DeFond and Jiambalvo,

1994; Becker, DeFond, Jiambalvo, and Subramanyam, 1998; Roychowdhury, 2006). Following

Gunny (2010), we include SIZE and MTB to control size effects and growth opportunity

14 Following Roychowdhury (2006), we use the values at the beginning of the year for Size and MTB, and use the

values at the end of the year for ROA.

17

respectively. Depending on previous research, showing that earnings management measures are

correlated with firm performance (e.g., Kothari, Leone, and Wasley, 2005; Cohen, Pandit,

Wasley, and Zach, 2011), ROA is included as a control for firm performance. Following Barton

and Simko (2002) and Zang (2012), we include NOA as a proxy for the extent of AEM in

previous periods. Due to the limited flexibility within GAAP and the reversal of accruals, AEM

in previous periods affects managers’ ability to manipulate accruals, with a consequent impact

on REM (Zang, 2012). Finally, according to Degeorge, Ding, Jeanjean, and Stolowy (2013),

Year_Fixed_Effect and Firm_Fixed_Effect are also included in our regression to control industry

effects and year effects.

3.4. Sample Selection

Financial development and relevant data, from 2009 to 2012, are obtained from Global

Note.15

The sample period is chosen because the Financial Development Score (FD), by the

World Economic Forum, is available in Global Note from 2009. The countries in this paper are

based on the 49 in La Porta, Lopez-de-Silanes, Shleifer, and Vishny (1998). Ecuador, New

Zealand, Taiwan, Uruguay, Sri Lanka, and Zimbabwe are dropped, as their FD scores are not

included in the report of the World Economic Forum. Zimbabwe is also eliminated due to its

experience of hyperinflation in the sample period.16

The sample comprises data from Capital IQ, from which we obtained 81,317 pieces of

firm-years data, covering sales and total assets of over 1 million dollars. Next, the data for

financial services firms (2,108 firm-years) are eliminated. To calculate earnings management

measures, we require at least six firm-year observations for each industry-year combination in

each country (13,825 firm-years are excluded). To provide the condition and availability of the

relevant measures that we need, Austria, Colombia, Egypt, Kenya, Portugal, and Venezuela

(8,326 firm-years) are not included in our sample. Using this sample selection process, we

15 Global Note is the website that collects and provides various kinds of international statistics such as Gross

Domestic Product. URL: http://www.globalnote.jp/ (in Japanese). 16 We define hyperinflation as over 100% per year.

18

obtained 54,178 observations from 37 countries.

4. Empirical results

4.1. Descriptive statistics

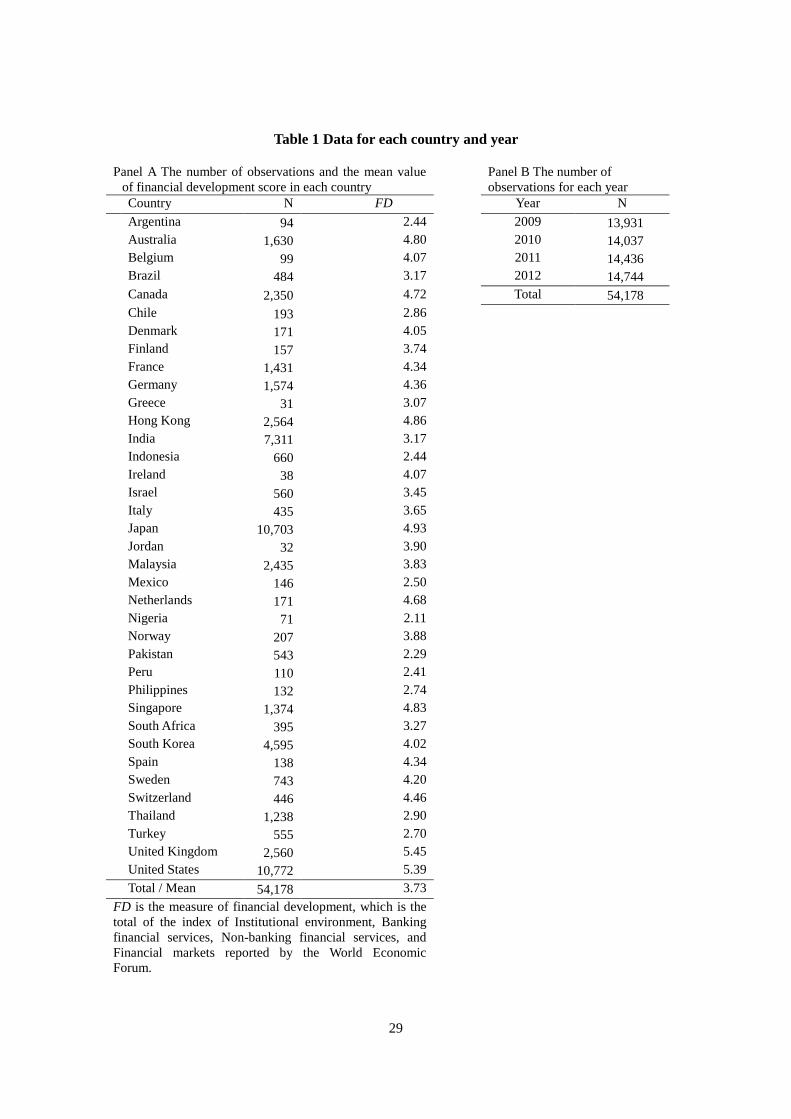

Panel A of Table 1 shows the number of firm-years in 37 countries, and the mean value of FD.

The highest number of firm-years is for the United States. (10,772 observations, 19.8%) and

Japan has a similar number. Observations for the United States and Japan occupy approximately

40% of the total. The lowest number of firm-years is Greece (31 observations).17

The third

column of Panel A reports the mean values of the financial development score (FD). FD is the

mean value of the four pillars i.e., Institutional environment, Banking financial services,

Non-banking financial services, and Financial markets. The United Kingdom has the highest

value, 5.45, in the 37 countries, and the United States is second highest. The lowest score is 2.11

for Nigeria. Only the United Kingdom and the United States have scores exceeding five.18

The

ranking is similar to Beck and Levin (2002) and Degeorge, Ding, Jeanjean, and Stolowy

(2013).19

Panel B is the number of firm-years in the sample period.

[Insert Table 1 here]

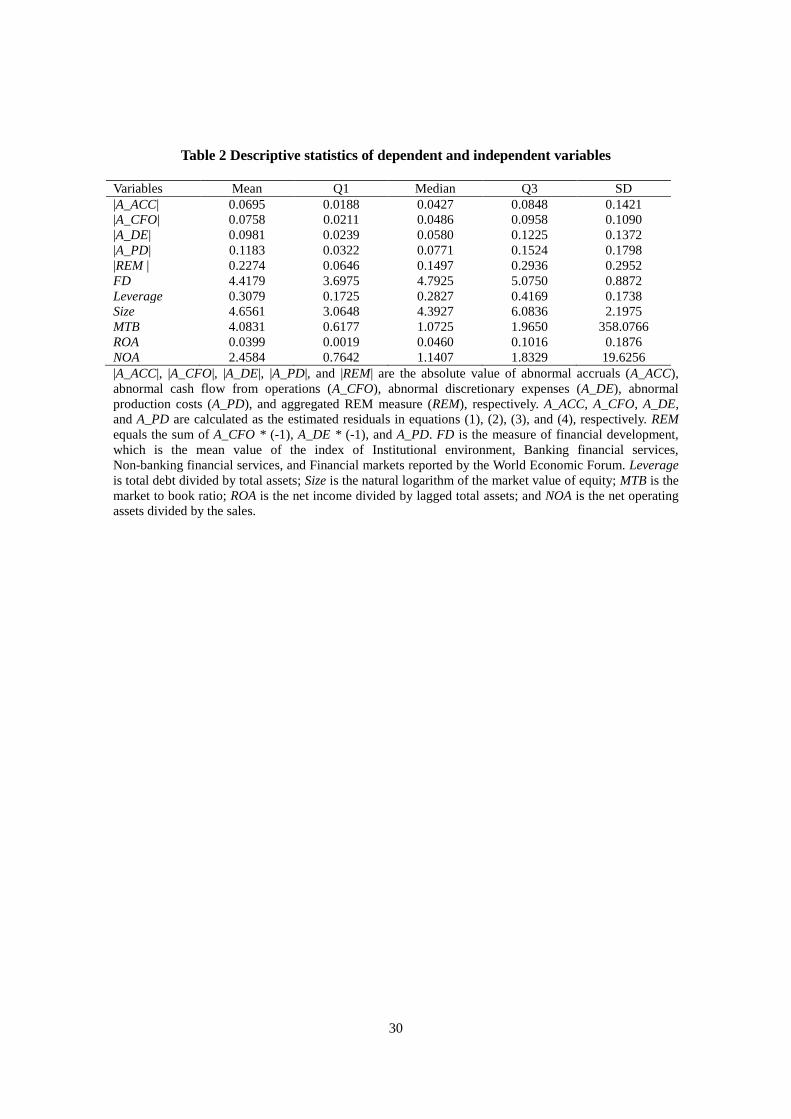

Table 2 shows the descriptive statistics for the dependent and independent variables in

equation (5). The mean values of |A_ACC|, |A_CFO|, |A_DE|, |A_PD|, and |REM| are 6.95%,

7.58%, 9.81%, 11.83%, and 22.74%, respectively. These values are slightly larger than Francis,

Hassan, and Li (2011) and smaller than Kim and Sohn (2013).20

17 The number of firm-years depends on not only the number of listed firms in each country but also the coverage by

Capital IQ. For example, India has more listed firms than Japan. 18 Original financial development scores range from the lowest value of 2.51 for Nigeria to the highest value of 5.17

for the United States, and show the same trends as our financial development score (FD). 19 Beck and Levin (2002) and Degeorge, Ding, Jeanjean, and Stolowy (2013) do not include the United Kingdom in

their sample. 20 These studies used the absolute value of abnormal accrual and three REM measures. The former uses international

data and the latter uses United States data.

19

[Insert Table 2 here]

Table 3 is the correlation matrix. Since a high correlation coefficient is not observed, the

results in the regressions from this section will not be influenced by multicollinearity. FD

negatively associates with |A_ACC|, but positively correlates with |A_CFO|, |A_DE|, |A_PD|,

and |REM|.

[Insert Table 3 here]

4.2. Regression Results

Table 4 reveals evidence of the influences of financial development on managerial behavior.21

Five types of dependent variables in the analyses are provided. Column (1) in Table 4 displays

the regression results of |A_ACC|. The coefficient of FD is significantly negative. This supports

our prediction that AEM is restrained in countries with high financial development. When

regarding financial development as an institutional factor, this result is consistent with Leuz,

Nanda, and Wysocki (2003) and Boonlert-U-Thai, Meek, and Nabar (2006). Financial

development serves as an institutional factor that inclines managers to avoid accrual-based

discretionary behaviors to manage earnings.22

[Insert Table 4 here]

In the regression, where the dependent variable is |A_CFO| (column (2) of Table 4), FD also

has a significant negative coefficient. Where the dependent variables are |A_DE|, |A_PD|, and

|REM| (column (3), (4) and (5) respectively), the coefficients of FD are also significantly

negative. From these results, it follows that financial development leads to REM reducing to

21 We winsorize all dependent and independent variable at the 1 percent and 99 percent levels. 22

Another reason for the small |abACC| of financially developed countries is that it is possible financial

development affects accounting institutions. For example, stakeholders pursuing high accounting quality require

tighter accounting standards in those countries.

20

similar levels as AEM. In economies that are relatively more financially developed, managers

would reduce noise in earnings and avoid the decrease in future revenue caused by earnings

management, fearing that stakeholders would detect these.

Taken together, the results suggest that, as financial development leads stakeholders to focus

on accounting numbers, managers may tend to avoid the costs incurred by earnings management.

These include the scrutiny of auditors and regulators, litigation, a decline in future sales, and

increasing cost of capital. The evidence supports our prediction that both types of earnings

management are restrained (e.g., Wongsunwai, 2013). This is not consistent with prior research

that shows substitution between AEM and REM (e.g. Francis, Hasan, and Li, 2011). Financial

development will discipline managers and mitigate their incentives to engage in earnings

management.

4.3. Additional tests

FD is designed to capture financial development that affects accounting information.

Therefore, FD is composed of the Institutional environment, Banking financial Services,

Non-banking financial services, and Financial markets that are extracted as the factors closely

relating to earnings quality in the original financial development score. However, the original

financial development score has a further three components, in addition to the four mentioned

above. These are Business environment, Financial stability, and Financial access. Hence, we

provide two additional tests.

One is the replacement of FD and another is the decomposition of it. First, FD is extended to

include the three components. We replace FD with the original financial development score,

Original_FD, and re-estimate equation (5). The coefficient of Original_FD in all regressions is

significantly negative (not tabulated) and supports the results of Table 4.

Next, FD is made the simple mean value of four components selected from the seven

indicators of the financial development score. We are concerned with whether FD faithfully

21

represents a true financial development by adding the four components equally.23

Hence, FD is

divided into four components, namely, Institutional_Environment, Banking_Financial_Services,

Non-banking_ Financial_Services, and Financial_Markets. The decomposition of FD makes it

possible to evaluate the effect of each component on earnings management. Equation (6)

includes each component of FD in the place of FD in equation (5).

EMijt = β0 + β1 Institutional_Environmentjt + β2 Banking_Financial_Servicesjt

+ β3 Non-banking_Financial_Servicesjt + β4 Financial_Marketsjt + β5 Leverageijt-1

+ β6 Sizeijt-1 + β7 MTBijt-1 + β8 ROAijt + β9 NOAijt-1 + Σ β Year_Fixed_Effect

+ Σ β Firm_Fixed_Effect + εijt (6)

In column (1) of Table 5, we provide evidence of the effect of each financial development

component. Among them, Non-banking_Financial_Services is negatively associated with the

level of |A_ACC| and the absolute value of the coefficient is the largest. By comparison,

Financial_ Markets has a significant positive value, but does not have a large effect on |A_ACC|.

For the dependent variables of REM, we find that Institutional_Environment and

Financial_Markets negatively affect the REM variable.24

In particular, the significant negative

value of the coefficients of Institutional Environment is not consistent with Francis, Hasan, and

Li (2011).25

23 Original financial development score by the World Economic Forum is also the simple mean value of seven

components. 24 As is well known, the development of a component works for the improvement of other components and entire

financial development. Thus, as there is the issue of interdependency, the findings of Table 5 should be carefully

interpreted. To mitigate any concern, we replace each component with FD. That is, the following regression is

estimated.

EMijt = β0 + β1 Component of FDjt + β2 Leverageijt-1 + β3 Sizeijt-1 + β4 MTBijt-1 + β5 ROAijt + β6 NOAijt-1

+Σ βFirm_Fixed_Effect + εijt-1,

Component of FD = Institutional_Environment, Banking_Financial_Services, Non-banking_Financial_Services, or

Financial_Markets.

Only the estimated coefficients of Non-banking_Financial_Services are similar to Table 5. None of the coefficients

of Institutional_Environment are significant. The coefficients of Banking_Financial_Services are significantly

positive only when the dependent variable is |REM|. In addition, the coefficients of Financial_Markets are consistent

with Table 5 in the regression of |abACC|, |abPD|, and |REM|. 25 As described before, Institutional_Environment includes legal enforcement.

22

[Insert Table 5 here]

Next, we consider the nonlinear relationship between financial development and earnings

management. The growing use of accounting information in the developing stages of financial

development may precede the preparation of relevant regulations. In this case, the ability to

monitor and scrutinize by a stakeholder is relatively immature. In this case, the incentives from

earnings management dominate the constraint. This constraint will dominate incentives in the

developed stage of financial development. To test this relationship, equation (7) adds FD2 in

equation (5). FD2 is the square of FD.

EMijt = β0 + β1 FDjt + β2 FD2jt

+ β3 Leverageijt-1 + β4 Sizeijt-1 + β5 MTBijt-1 + β6 ROAijt + β9 NOAijt-1

+ Σ β Year_Fixed_Effect + Σ β Firm_Fixed_Effect + εijt (7)

In table 6, all coefficients of FD are positive, and those of FD2 are negative. However, for

only |A_ACC| and |A_DE|, coefficients of FD and FD2 are significant with the inflection points

3.94 and 3.23, respectively. These results show that AEM is more prevalent until the FD score

reaches the average point of our sample (see table 1) and become less prevalent after that.

Results from REM tests are less conclusive.

[Insert Table 6 here]

4.4. Robustness checks

For the first robustness test, we re-computed abnormal accruals using the cross-sectional

Jones (1991) model instead. The coefficient of FD in the regression of |A_ACC| is similar to that

observed before (not tabulated).

Next, we employ country-, industry-, and year-fixed effects in place of firm-fixed effects in

23

equation (5).

EMijt = β0 + β1 FDjt + β2 Leverageijt-1 + β3 Sizeijt-1 + β4 MTBijt-1 + β5 ROAijt + β6 NOAijt-1

+ Σ β Year_Fixed_Effect + Σ β Country_Fixed_Effect + Σ β Industry_Fixed_Effect + εijt (8)

While it is suitable that the firm-fixed effects' terms are used to control time invariant factors,

some research includes country-, industry- and year-fixed effects. As shown in Table 7, the

coefficients of FD in all regressions remain significantly negative, which is consistent with

those of Table 4.

[Insert Table 7 here]

In addition, to test the robustness of our findings, we repeat the regressions in the samples,

excluding particular country and year. First, we delete all of the firm-years for the United States

and Japan and re-estimate the models in Table 3. The total observations for the United States

and Japan number 21,475 or 39.6 percent of our sample (see Table 1). It is, therefore, of concern

that the evidence in Table 3 is driven mainly by the data for these two countries. Table 8

displays the estimated coefficients from the sample, excluding the observations for the United

States and Japan. All of the coefficients of FD are negative and significant, and consistent with

those of Table 3. In addition, the results are robust even when we eliminate the observations for

either of these countries.

[Insert Table 8 here]

Second, we deleted all 2009 data in the sample and re-estimated equation (5). This is because

our sample periods include data from periods of financial crisis around the world. The results

are shown in Table 7. The coefficient of FD for |A_ACC| remains significantly negative. For

REM, the coefficients of two of the three dependent variables, |A_DE| and |A_PD|, are similar to

24

Table 3. Thus, our findings are not heavily influenced by financial crises.

[Insert Table 9 here]

5. Conclusion

This paper investigates whether the level of financial development in each country affects

managers’ earnings management by using 54,178 observations from 37 countries in the period

of 2009 to 2012. For earnings management methods, we focus on both AEM and REM. We find

that a negative relationship exists between the levels of financial development in each country

and both types of earnings management. Our results indicate that both AEM and REM are

constrained in countries with high financial development. We interpret this data as showing (1)

higher quality accounting information is needed in countries with more developed financial

systems, (2) there is a link between financial development and accounting institutions in each

country, and (3) financial development disciplines managers and mitigates their incentives to

engage in earnings management.

Previous papers using an international setting show that AEM is restrained in countries with a

high level of investor protection (Leuz, Nanda, and Wysocki 2003). They also show that AEM

and REM are used as substitutes each other, according to the level of the legal system (Francis,

Hasan, and Li, 2011) and the level of outside investor rights (Enomoto, Kimura, and Yamaguchi,

2013). This paper contributes to the earnings management literature by showing that both AEM

and REM are restrained by high levels of financial development in an international setting.

We feel that future study is needed in the following area. First, due to data availability, our

sample period is only 4 years, from 2009 to 2012. To secure more reliable evidence, a test with a

longer sample period is required in the future. Second, we estimated the test models of AEM

and REM separately, even though previous research shows a substitution of AEM and REM. We

recognize the desirability of a simultaneous equations system for the two types of earnings

management, and this remains for future research.

25

Third, we did not clarify the process of linkage between financial development and

accounting institutions. Wysocki (2011, 312) notes the ‘chicken and the egg’ problem of

endogeneity and complementarity between accounting and other institutions, and this problem

would apply to the relationship between financial development and accounting institutions. It is

difficult to determine which comes first, but it is interesting to research this issue.

References

Badertscher, B. A. 2011. Overvaluation and the choice of alternative earnings management

mechanisms. The Accounting Review 86 (5): 1491-1518.

Ball, R., Robin, A., and J. Wu. 2003. Incentives versus standards: properties of accounting

income in four East Asian countries. Journal of Accounting and Economics 36 (1-3):

235-270.

Barth, M.E., W. R. Landsman, and M. H. Lang. 2008. International accounting standards and

accounting quality. Journal of Accounting Research 46 (3):467-498.

Barton, J. and P. J. Simko. 2002. The balance sheet as an earnings management constraint. The

Accounting Review 77 (Supplement): 1-27.

Bartov, E. and D. A. Cohen. 2009. The “numbers game” in the pre-and post-Sarbanes-Oxley

eras. Journal of Accounting, Auditing and Finance 24 (4): 505-534.

Bartov, E., D. Givoly, and C. Hayn. 2002. The rewards to meeting or beating earnings

expectations. Journal of Accounting and Economics 33 (2): 173-204.

Beck, T. and R. Levine. 2002. Industry growth and capital allocation: Does having a market- or

bank-based system matter. Journal of Financial Economics 64 (2): 147-180.

Beck, T. and R. Levine. 2004. Stock markets, banks and growth: Panel evidence. Journal of

Banking and Finance 28 (3): 423-442.

Becker, C. L., M. L. DeFond., J. Jiambalvo, and K. R. Subramanyam. 1998. The effect of audit

quality on earnings management. Contemporary Accounting Research 15 (1): 1-24.

Bikky, J. and L. Picheng. 2002. Earnings management in response to debt covenant violations

26

and debt restructuring. Journal of Accounting, Auditing and Finance 17 (4): 295-324.

Boonlert-U-Thai, K., G. K. Meek, and S. Nabar. 2006. Earnings attributes and

investor-protection: International evidence. The International Journal of Accounting 41 (4):

327-357.

Bushman, R. and J. Piotroski. 2006. Financial reporting incentives for conservative accounting:

The influence of legal and political institutions. Journal of Accounting and Economics 42

(1-2): 107-148.

Chi, W., L. L. Lisic, and M. Pevzner. 2011. Is enhanced audit quality associated with greater

real earnings management? Accounting Horizons 25 (2): 315-335.

Cohen, D. A., A. Dey, and T. Z. Lys. 2008. Real and accrual-based earnings management in the

pre-and post-Sarbanes-Oxley periods. The Accounting Review 83 (3): 757-787.

Cohen, D. A. and P. Zarowin. 2010. Accrual-based and real earnings management activities

around seasoned equity offerings. Journal of Accounting and Economics 50 (1): 2-19.

Dechow, P. M., W. Ge, and C. Schrand. 2010. Understanding earnings quality: A review of the

proxies, their determinants and their consequences. Journal of Accounting and Economics 50

(2-3): 344-401.

Dechow, P. M., A. P. Hutton, J. H. Kim, and R. G. Sloan. 2012. Detecting earnings

management: A new approach. Journal of Accounting Research 50 (2): 275-334.

Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1995. Detecting earnings management. The

Accounting Review 70 (2): 193-225.

DeFond, M. L. and J. Jiambalvo. 1994. Debt covenant violation and manipulation of accruals.

Journal of Accounting and Economics 17 (1-2): 145-176.

Degeorge F., Y. Ding, T. Jeanjean, and H. Stolowy. 2013. Analyst coverage, earnings

management and financial development: An international study. Journal of Accounting and

Public Policy 32 (1): 1-25.

Enomoto, M., F. Kimura, and T. Yamaguchi. 2013. Accrual based and real earnings

management: An international comparison for investor protection. Discussion Paper Series

27

No. DP 2012–13, RIEB Kobe University; Available at SSRN: http://ssrn.com/abstract=

2066797.

Ewert, R. and A. Wagenhofer. 2005. Economic effects of tightening accounting standards to

restrict earnings management. The Accounting Review 80 (4): 1101-1124.

Francis, B., I. Hasan, and L. Li. 2011. A cross-country study of legal environment and real

earnings management. Working paper. Available at SSRN: http://ssrn.com/abstract=

1740036.

Francis, J. R. and D. Wang. 2008. The joint effect of investor protection and Big-4 audits on

earnings quality around the world. Contemporary Accounting Research 25 (1): 157-191.

Gunny, K. 2010. The relation between earnings management using real activities manipulation

and future performance: Evidence from meeting earnings benchmarks. Contemporary

Accounting Research 27 (3): 855-888.

Graham, J. R., C. R. Harvey, and S. Rajgopal. 2005. The economic implications of corporate

financial reporting. Journal of Accounting and Economics 40 (1-3): 3-73.

Haw, I., B. Hu, L. Hwang, and W. Wu. 2004. Ultimate ownership, income management, and

legal and extra-legal institutions. Journal of Accounting Research 42 (2): 423-462.

Ipino., E. and A. Parbonetti. 2011. Mandatory IFRS adoption: the trade-off between accrual and

real-based earnings management. Working Paper. Available at SSRN: http://ssrn.com/

abstract=2039711.

Jones, J. 1991. Earnings management during import relief investigations. Journal of Accounting

Research 29 (2): 193-228.

Kim, B. H., L. Lei, and M. Pevzner. 2011. Debt covenant slack and real earnings management.

Working paper.

Kim, J. B. and B. C. Sohn. 2013. Real earnings management and cost of capital. Journal of

Accounting and Public Policy (forthcoming).

Kothari, S.P., N. Mizik, and S. Roychowdhury. 2012. Managing for the moment: The role of

real activity versus accruals earnings management in SEO valuation. Working paper.

28

Available at SSRN: http://ssrn.com/abstract=1982826.

Leuz, C., D. Nanda, and P. Wysocki. 2003. Earnings management and investor protection: an

international comparison. Journal of Financial Economics 69 (3): 505-527.

Leuz, C. and P. Wysocki. 2009. Economic consequences of financial reporting and disclosure

regulation: a review and suggestions for future research. Working Paper, University of

Chicago and MIT Sloan School of Management. Available at SSRN: http://www.ssrn.com/

abstract=105398.

Scott, W. R. 2011. Financial Accounting Theory 6th edition. Prentice Hall.

Roychowdhury, S. 2006. Earnings management through real activities manipulation. Journal of

Accounting and Economics 42 (3): 335-370.

Teoh, S. H., I. Welch, and T. J. Wong. 1998a. Earnings management and the long-run market

performance of initial public offerings. Journal of Finance 53 (1): 1935-1974.

Teoh, S. H., I. Welch, and T. J. Wong. 1998b. Earnings management and the underperformance

of seasoned equity offerings. Journal of Financial Economics 50 (6): 63-99.

Warfield, T. D., J. J. Wild, and K. L. Wild. 1995. Managerial ownership, accounting choices,

and informativeness of earnings. Journal of Accounting and Economics 20 (1): 61-91.

Wongsunwai, W. 2013. The effect of external monitoring on accrual-based and real earnings

management: evidence from venture-backed initial public offerings. Contemporary

Accounting Research 30 (1): 242-268.

World Economic Forum. 2012. The Financial Development Report 2012. Available at the World

Economic Forum Website: http://www.weforum.org/reports/financial-development-report-

2012.

Wysocki, P. 2011. New institutional accounting and IFRS. Accounting and Business Research

41 (3): 309-328.

Zang, A. 2012. Evidence on the trade-off between real activities manipulation and accrual-based

earnings management. The Accounting Review 87 (2): 675-703.

29

Table 1 Data for each country and year

Panel A The number of observations and the mean value

of financial development score in each country

Panel B The number of

observations for each year

Country N FD Year N

Argentina 94 2.44 2009 13,931

Australia 1,630 4.80 2010 14,037

Belgium 99 4.07 2011 14,436

Brazil 484 3.17 2012 14,744

Canada 2,350 4.72 Total 54,178

Chile 193 2.86

Denmark 171 4.05

Finland 157 3.74

France 1,431 4.34

Germany 1,574 4.36

Greece 31 3.07

Hong Kong 2,564 4.86

India 7,311 3.17

Indonesia 660 2.44

Ireland 38 4.07

Israel 560 3.45

Italy 435 3.65

Japan 10,703 4.93

Jordan 32 3.90

Malaysia 2,435 3.83

Mexico 146 2.50

Netherlands 171 4.68

Nigeria 71 2.11

Norway 207 3.88

Pakistan 543 2.29

Peru 110 2.41

Philippines 132 2.74

Singapore 1,374 4.83

South Africa 395 3.27

South Korea 4,595 4.02

Spain 138 4.34

Sweden 743 4.20

Switzerland 446 4.46

Thailand 1,238 2.90

Turkey 555 2.70

United Kingdom 2,560 5.45

United States 10,772 5.39

Total / Mean 54,178 3.73

FD is the measure of financial development, which is the

total of the index of Institutional environment, Banking

financial services, Non-banking financial services, and

Financial markets reported by the World Economic

Forum.

30

Table 2 Descriptive statistics of dependent and independent variables

Variables Mean Q1 Median Q3 SD

|A_ACC| 0.0695 0.0188 0.0427 0.0848 0.1421

|A_CFO| 0.0758 0.0211 0.0486 0.0958 0.1090

|A_DE| 0.0981 0.0239 0.0580 0.1225 0.1372

|A_PD| 0.1183 0.0322 0.0771 0.1524 0.1798

|REM | 0.2274 0.0646 0.1497 0.2936 0.2952

FD 4.4179 3.6975 4.7925 5.0750 0.8872

Leverage 0.3079 0.1725 0.2827 0.4169 0.1738

Size 4.6561 3.0648 4.3927 6.0836 2.1975

MTB 4.0831 0.6177 1.0725 1.9650 358.0766

ROA 0.0399 0.0019 0.0460 0.1016 0.1876

NOA 2.4584 0.7642 1.1407 1.8329 19.6256

|A_ACC|, |A_CFO|, |A_DE|, |A_PD|, and |REM| are the absolute value of abnormal accruals (A_ACC),

abnormal cash flow from operations (A_CFO), abnormal discretionary expenses (A_DE), abnormal

production costs (A_PD), and aggregated REM measure (REM), respectively. A_ACC, A_CFO, A_DE,

and A_PD are calculated as the estimated residuals in equations (1), (2), (3), and (4), respectively. REM

equals the sum of A_CFO * (-1), A_DE * (-1), and A_PD. FD is the measure of financial development,

which is the mean value of the index of Institutional environment, Banking financial services,

Non-banking financial services, and Financial markets reported by the World Economic Forum. Leverage

is total debt divided by total assets; Size is the natural logarithm of the market value of equity; MTB is the

market to book ratio; ROA is the net income divided by lagged total assets; and NOA is the net operating

assets divided by the sales.

31

Table 3 Correlation matrix of dependent variables and independent variables

|A_ACC| |A_CFO| |A_DE| |A_PD| |REM | FD Leverage Size MTB ROA

|A_CFO| 0.4537

|A_DE| 0.1597 0.2261

|A_PD| 0.1945 0.3045 0.5881

|REM | 0.2256 0.4018 0.7022 0.8828

FD -0.0317 0.0284 0.1637 0.1093 0.1008

Leverage 0.0693 0.0326 0.1100 0.1084 0.1170 -0.1372

Size -0.1775 -0.1272 -0.1004 -0.0765 -0.0891 0.2641 -0.2257

MTB 0.1631 0.2513 0.1998 0.1929 0.2036 0.0916 0.1116 0.2442

ROA -0.1539 -0.1455 -0.0371 0.0469 0.0369 -0.1019 -0.0753 0.2483 -0.0201

NOA 0.0264 0.0204 -0.1332 -0.1117 -0.1075 0.0102 -0.2705 0.0804 0.0155 -0.1694

|A_ACC|, |A_CFO|, |A_DE|, |A_PD| and |REM| is the absolute value of abnormal accruals (A_ACC), abnormal cash flow from operations (A_CFO),

abnormal discretionary expenses (A_DE), abnormal production costs (A_PD), and aggregated REM measure (REM). A_ACC, A_CFO, A_DE, and A_PD

are calculated as the estimated residuals in equation (1), (2), (3), and (4), respectively. REM equals the sum of A_CFO * (-1), A_DE * (-1), and A_PD. FD

is the measures of financial development, which is the mean value of the index of Institutional environment, Banking financial services, Non-banking

financial services, and Financial markets reported by the World Economic Forum. Leverage is the total debt divided by the total assets; Size is the natural

logarithm of the market value of equity; MTB is the market to book ratio; ROA is the net income divided by lagged total assets; NOA is the net operating

assets divided by the sales.

32

Table 4 Financial development score and earnings management

(1) (2) (3) (4) (5)

Variable |A_ACC| |A_CFO| |A_DE| |A_PD| |REM |

Intercept 0.1210*** 0.1396*** 0.1814*** 0.2475*** 0.4341***

(9.4149) (11.4516) (16.7057) (16.6462) (16.2048)

FD -0.0080*** -0.0089*** -0.0129*** -0.0230*** -0.0330***

(-2.7448) (-3.2342) (-5.2553) (-6.8642) (-5.4566)

Leverage 0.0295*** 0.0114*** 0.0053 -0.0193*** -0.0108

(6.3875) (2.6078) (1.3605) (-3.6294) (-1.1217)

Size -0.0065*** -0.0077*** -0.0091*** -0.0089*** -0.0206***

(-8.5825) (-10.7611) (-14.2799) (-10.1821) (-13.0735)

MTB 0.0025*** 0.0032*** 0.0041*** 0.0039*** 0.0085***

(8.5207) (11.6868) (16.6821) (11.7748) (14.0827)

ROA -0.0430*** 0.0135*** 0.0015 0.0852*** 0.1521***

(-9.8886) (3.2880) (0.4108) (16.9630) (16.8176)

NOA -0.0007*** -0.0016*** -0.0012*** -0.0013*** -0.0033***

(-2.8466) (-6.8386) (-5.6881) (-4.7781) (-6.6857)

Year_Fixed_Effects included included included included included

Firm_Fixed_Effects included included included included included

Adjusted R-squared 0.3330 0.4519 0.7766 0.6399 0.6772

Observations 57,148 56,830 57,148 56,830 56,830

The t-statistics are in parentheses. ***, **, and * indicate significance at 1%, 5%, and 10% levels

respectively (two-tailed). The following regressions are estimated:

EMijt = β0 + β1 FDjt + β2 Leverageijt-1 + β3 Sizeijt-1 + β4 MTBijt-1 + β5 ROAijt + β6 NOAijt-1

+ Σ βYear_Fixed_Effect + Σ β Firm_Fixed_Effect + εijt (5)

EM represents the earnings management proxies, that is, |A_ACC|, |A_CFO|, |A_DE|, |A_PD|, or |REM|.

Further, |A_ACC|, |A_CFO|, |A_DE|, |A_PD|, and |REM| are the absolute values of abnormal accruals

(A_ACC), abnormal cash flow from operations (A_CFO), abnormal discretionary expenses (A_DE),

abnormal production costs (A_PD), and aggregated REM measure (REM), respectively. A_ACC, A_CFO,

A_DE, and A_PD are calculated as the estimated residuals in equations (1), (2), (3), and (4), respectively.

REM equals the sum of A_CFO * (-1), A_DE * (-1), and A_PD. FD is the measure of financial

development that is the mean value of the index of Institutional environment, Banking financial services,

Non-banking financial services, and Financial markets reported by the World Economic Forum. Leverage

is total debt divided by total assets; Size is the natural logarithm of the market value of equity; MTB is the

market to book ratio; ROA is the net income divided by lagged total assets; and NOA is the net operating

assets divided by sales.

33

Table 5 The components of financial development score and earnings management

(1) (2) (3) (4) (5)

Variable |A_ACC| |A_CFO| |A_DE| |A_PD| |REM |

Intercept 0.1256*** 0.1683*** 0.2136*** 0.2523*** 0.5110***

(5.0412) (7.0865) (10.1430) (8.7126) (9.7962) Institutional_Environment 0.0021 -0.0116** -0.0139*** -0.0150*** -0.0419***

(0.4405) (-2.5540) (-3.4320) (-2.6900) (-4.1861)

Banking_Financial_

Services

-0.0005 0.0023 -0.0006 0.0041 0.0111**

(-0.2088) (0.9896) (-0.2871) (1.4615) (2.2091)

Non-banking_Financial_

Service

-0.0140*** -0.0018 0.0011 -0.0046** -0.0018

(-7.0801) (-0.9489) (0.6388) (-2.0270) (-0.4416)

Financial_Market 0.0027** -0.0032*** -0.0055*** -0.0078*** -0.0141***

(2.5416) (-3.1495) (-6.0739) (-6.3257) (-6.3611)

Leverage 0.0283*** 0.0115*** 0.0056 -0.0184*** -0.0093

(6.1314) (2.6286) (1.4370) (-3.4591) (-0.9695)

Size -0.0064*** -0.0076*** -0.0090*** -0.0086*** -0.0199***

(-8.4589) (-10.4843) (-14.0556) (-9.7506) (-12.5834)

MTB 0.0025*** 0.0032*** 0.0041*** 0.0039*** 0.0084***

(8.7578) (11.6764) (16.6091) (11.6490) (13.9793)

ROA -0.0427*** 0.0132*** 0.0012 0.0842*** 0.1503***

(-9.8024) (3.2018) (0.3262) (16.7609) (16.6035)

NOA -0.0007*** -0.0015*** -0.0011*** -0.0013*** -0.0033***

(-2.9515) (-6.8044) (-5.6012) (-4.7734) (-6.6269)

Year_Fixed_Effects included included included included included

Firm_Fixed_Effects included included included included included

Adjusted R-squared 0.3338 0.4520 0.7767 0.6400 0.6774

Observations 57,148 56,830 57,148 56,830 56,830

The t-statistics are in parentheses. ***, **, and * indicate significance at 1%, 5%, and 10% levels

respectively (two-tailed). The following regressions are estimated:

EMijt = β0 + β1 Institutional_Environmentjt + β2 Banking_Financial_Servicesjt

+ β3 Non-banking_Financial_Servicejt + β4 Financial_Marketjt + β5 Leverageijt-1 + β6 Sizeijt-1

+ β7 MTBijt-1 + β8 ROAijt + β9 NOAijt-1 + Σ β Year_Fixed_Effects + Σ β Firm_Fixed_Effect + εijt (6)

EM represents the earnings management proxies, that is, |A_ACC|, |A_CFO|, |A_DE|, |A_PD|, or |REM|.

|A_ACC|, |A_CFO|, |A_DE|, |A_PD|, and |REM| are the absolute value of abnormal accruals (A_ACC),

abnormal cash flow from operations (A_CFO), abnormal discretionary expenses (A_DE), abnormal

production costs (A_PD), and aggregated REM measure (REM). A_ACC, A_CFO, A_DE, and A_PD are

calculated as the estimated residuals in equations (1), (2), (3), and (4), respectively. REM equals the sum

of A_CFO * (-1), A_DE * (-1), and A_PD. Institutional_Environment, Banking_Financial_Services,

Non-banking_Financial_Services, and Financial_Markets are the scores for Institutional environment,

Banking financial services, Non-banking financial services, and Financial markets, respectively, reported

by the World Economic Forum. Leverage is total debt divided by total assets; Size is the natural logarithm

of the market value of equity; MTB is the market to book ratio; ROA is the net income divided by lagged

total assets; NOA is the net operating assets divided by sales.

34

Table 6 The nonlinear test results of the relationship between

financial development score and earnings management

(1) (2) (3) (4) (5)

Variable |A_ACC| |A_CFO| |A_DE| |A_PD| |REM |

Intercept 0.0702*** -0.0222 0.0362*** 0.0089 0.0133