a guide from our personal financial planning team

TRANSCRIPT

PRACTICAL TAX PLANNING IN 2015A GUIDE fRom oUR PERsoNAL fINANCIAL PLANNING TEAm

Tax planning can be a complex task with a number of strategies to consider, but is more important than ever in today’s tough economic climate. British taxpayers are handing over £4.9bn a year more in tax to Her Majesty’s Revenue & Customs (HMRC) than they need to, according to research undertaken by financial adviser website unbiased.co.uk.

Tax action is an annual campaign undertaken by unbiased.co.uk which focuses on educating consumers on individual areas of tax wastage, highlighting the need for tax planning advice on how to be more tax efficient. It found that wastage has arisen as a result of individuals:

• Not making use of the allowances and reliefs available.

• Not optimising the tax efficiency of their personal financial planning affairs.

Of course, effective tax planning should be undertaken in the context of a coordinated financial strategy. Taking inappropriate investment risks in pursuit of tax savings can lead to regret. However, there are some key actions that can be considered as part of a sensible approach to minimising the impact of tax.

In this guide we review areas where you could reduce your tax bill. It is not a detailed analysis of each opportunity so, if in doubt, you should seek professional advice. The amount of tax saved and over what period will, of course, depend on your personal circumstances.

As ever, if you need any help or advice on the areas covered, please don’t hesitate to get in touch with me or one of our local personal financial planning consultants – you can find our contact details on page 6.

Further information on Tax Action can be obtained by visiting www.unbiased.co.uk/tax-action.

Tim Robson

FPFS, Chartered Financial Planner

TAX yEAR ENDING 5 APRIL 2015

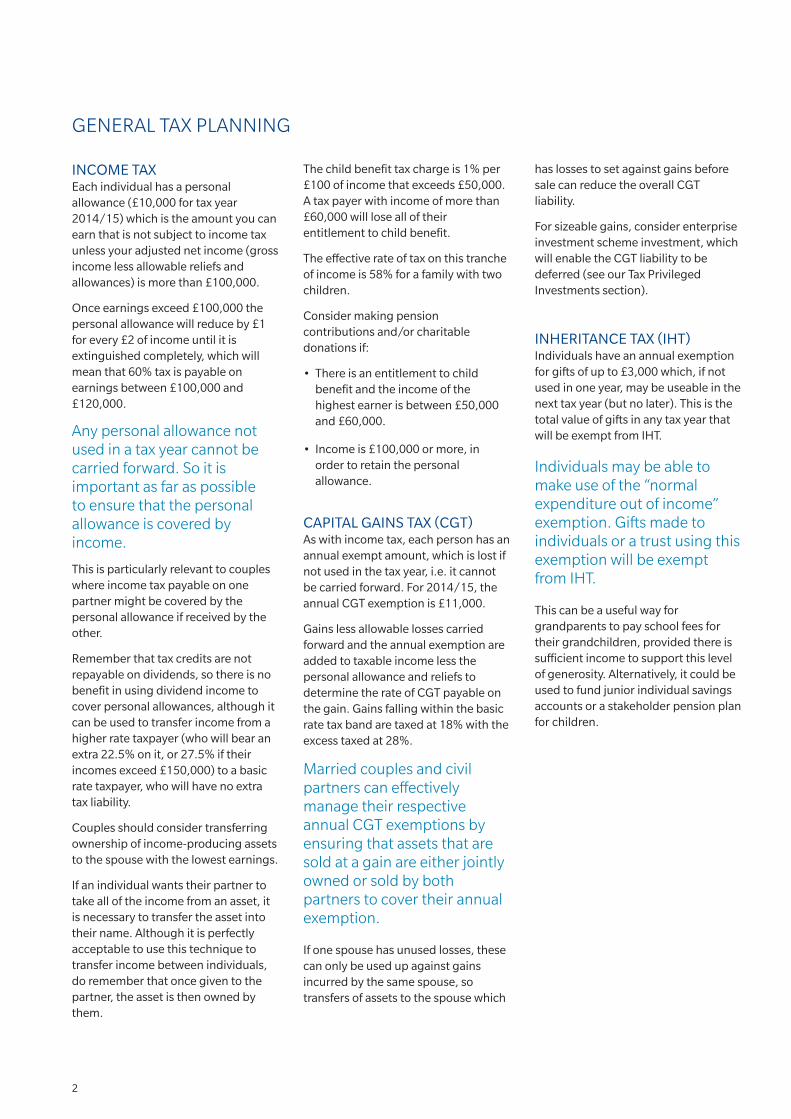

TAX WASTAGE IN NUMBERS...

45% of savers think that they are already paying as little tax as they should.

74% of taxpayers admit they haven’t done anything to reduce their tax waste in the last year.

£165 : The average amount each individual taxpayer is estimated to waste.

Source: Tax Action 2015

1

2

GENERAL TAX PLANNING

INCOME TAXEach individual has a personal allowance (£10,000 for tax year 2014/15) which is the amount you can earn that is not subject to income tax unless your adjusted net income (gross income less allowable reliefs and allowances) is more than £100,000.

Once earnings exceed £100,000 the personal allowance will reduce by £1 for every £2 of income until it is extinguished completely, which will mean that 60% tax is payable on earnings between £100,000 and £120,000.

Any personal allowance not used in a tax year cannot be carried forward. so it is important as far as possible to ensure that the personal allowance is covered by income.

This is particularly relevant to couples where income tax payable on one partner might be covered by the personal allowance if received by the other.

Remember that tax credits are not repayable on dividends, so there is no benefit in using dividend income to cover personal allowances, although it can be used to transfer income from a higher rate taxpayer (who will bear an extra 22.5% on it, or 27.5% if their incomes exceed £150,000) to a basic rate taxpayer, who will have no extra tax liability.

Couples should consider transferring ownership of income-producing assets to the spouse with the lowest earnings.

If an individual wants their partner to take all of the income from an asset, it is necessary to transfer the asset into their name. Although it is perfectly acceptable to use this technique to transfer income between individuals, do remember that once given to the partner, the asset is then owned by them.

The child benefit tax charge is 1% per £100 of income that exceeds £50,000. A tax payer with income of more than £60,000 will lose all of their entitlement to child benefit.

The effective rate of tax on this tranche of income is 58% for a family with two children.

Consider making pension contributions and/or charitable donations if:

• There is an entitlement to child benefit and the income of the highest earner is between £50,000 and £60,000.

• Income is £100,000 or more, in order to retain the personal allowance.

CAPITAl GAINS TAX (CGT)As with income tax, each person has an annual exempt amount, which is lost if not used in the tax year, i.e. it cannot be carried forward. For 2014/15, the annual CGT exemption is £11,000.

Gains less allowable losses carried forward and the annual exemption are added to taxable income less the personal allowance and reliefs to determine the rate of CGT payable on the gain. Gains falling within the basic rate tax band are taxed at 18% with the excess taxed at 28%.

married couples and civil partners can effectively manage their respective annual CGT exemptions by ensuring that assets that are sold at a gain are either jointly owned or sold by both partners to cover their annual exemption.

If one spouse has unused losses, these can only be used up against gains incurred by the same spouse, so transfers of assets to the spouse which

has losses to set against gains before sale can reduce the overall CGT liability.

For sizeable gains, consider enterprise investment scheme investment, which will enable the CGT liability to be deferred (see our Tax Privileged Investments section).

INHERITANCE TAX (IHT)Individuals have an annual exemption for gifts of up to £3,000 which, if not used in one year, may be useable in the next tax year (but no later). This is the total value of gifts in any tax year that will be exempt from IHT.

Individuals may be able to make use of the “normal expenditure out of income” exemption. Gifts made to individuals or a trust using this exemption will be exempt from IHT.

This can be a useful way for grandparents to pay school fees for their grandchildren, provided there is sufficient income to support this level of generosity. Alternatively, it could be used to fund junior individual savings accounts or a stakeholder pension plan for children.

3

TAX PRIvILEGED INvEsTmENTs

INdIvIdUAl SAvINGS ACCOUNTS (ISAS)Individuals have an annual ISA allowance, which is £15,000 for tax year 2014/15. There are also Junior ISAs for children, which have an annual investment limit of £4,000. Investment can be made in cash deposits and stocks and shares.

The amount invested in IsAs does not attract tax relief but the income and gains on the investment are broadly tax free.

Any ISA allowance not used in a tax year cannot be carried forward.

From 1 April 2015 if an ISA holder dies, under the new inheritance ISA rules, their spouse or civil partner will be able to invest an amount equivalent to the value of the deceased’s ISA into their own ISA via an additional allowance.

Over time, a substantial tax protected investment portfolio can be accumulated by making use of the annual ISA exemption.

ENTERPRISE INvESTMENT SCHEMES (EIS) These type of schemes involve investing in the shares of unquoted companies.

Investment in companies not listed on the Stock Exchange that meet the EIS qualifying rules carries high risk. The tax relief is intended to offer some compensation for that risk.

An investor may invest up to £1,000,000 in a tax year in an EIs and obtain a tax reducer of 30% of the amount of investment. This will mean that tax relief is provided via self assessment.

EIS shares are exempt from CGT once they have been held for three years.

CGT on the disposal of other assets can be deferred by reinvesting the proceeds in EIS shares. However, the tax on the original gain will become payable when the EIS investment is sold. dividends are not tax free.

If the shares are disposed of at a loss, the amount of the loss, less any income tax relief given, can be set against income of the year in which they were disposed of, or any income of the previous year, instead of being set off against any capital gains.

All tax reliefs depend on the EIS qualifying conditions being met for three years.

vENTURE CAPITAl TRUSTS (vCTS)vCTs are similar to investment trusts. They are run by fund managers who are usually members of larger investment groups.

Investors can subscribe for, or buy, shares in a vCT, which invests at least 70% of the funds raised in qualifying unquoted trading companies, providing them with funds to help them develop and grow.

An investor may invest up to £200,000 in a tax year in a vCT and obtain a tax reducer of 30% of the amount of investment. This will mean that tax relief is provided via self assessment.

dividends are income tax exempt. vCT shares are exempt from CGT once held for five years.

All tax reliefs depend on the vCT qualifying conditions being met.

4

PENSIONSTax relief and a tax-free growth environment are powerful incentives to make pension contributions.

Additional rate (45% taxpayers) using their full £40,000 annual allowance (ignoring any carry forward) can convert an otherwise £18,000 tax bill into retirement savings.

As the tax year end approaches, we have identified eight good reasons to make pension contributions for this tax year.

1. Obtain tax relief on contributions at your highest marginal rate.

• Individuals who are additional or higher rate tax payers for tax year 2014/15, but are unsure of their income level for tax year 2015/16 can secure tax relief at their highest marginal rate in the current tax year.

• Typically, this is likely to be individuals whose remuneration fluctuates with profit-related bonuses, who are not sure of repeating their performance in subsequent tax years.

• Pensions are most tax-efficient as a tax deferral vehicle where tax relief obtained on contributions is more than tax paid on pension payments/income withdrawals when pension benefits are taken.

• Further employee National Insurance Contribution (NIC) savings can be made if contributions are paid by bonus or salary sacrifice and the pension contribution could be increased if the employer is prepared to pass on all or part of their NIC saving.

2. Immediate access to pension savings for the over 55s.

• The new flexibility for taking pension benefits from defined contribution (dC) pension arrangements from April 2015 will mean that those age 55 or over can have the same access to their pension savings as they do to any other investments.

• With the combination of tax relief and tax-free cash, pensions will generally outperform ISAs on a like-for-like basis for the majority of individuals. Therefore individuals over age 55 should consider maximising pension contributions ahead of saving through other investments.

3. Increase pension fund value prior to accessing the new flexibility.

• Individuals looking to take advantage of the new flexibility for their dC fund value may wish to consider maximising their fund value by making additional pension contributions prior to 5 April 2015. Once the new flexibility is accessed (when the amount drawn down exceeds the maximum tax-free cash allowable) the amount of pension contributions that can be made without any adverse tax consequences will reduce to £10,000.

• Individuals who enter into capped income drawdown and retain it post 6 April 2015, will continue to be entitled to the full annual allowance of £40,000 per tax year for ongoing pension contributions provided the contract is written as one arrangement.

4. Providing for dependants.

• The new death benefit rules for dC pension arrangements will mean that money can be passed on tax efficiently to heirs. There will generally be no inheritance tax (IHT) payable and the fund value can be paid tax free to your nominated beneficiaries on death before age 75.

• Individuals who have sufficient annual allowance and lifetime allowance available could consider moving savings that could potentially be subject to IHT into a dC pension arrangement to shelter assets from IHT, obtain tax relief on the pension contributions and benefit from investment returns that would be broadly tax free.

• Provided the individual is not in serious ill health when the transfer payment is made, the amount contributed to the dC pension arrangement will be immediately outside of their estate for IHT purposes.

5. Don’t miss out on the £50,000 annual allowance for tax year 2011/12, 2012/13 and 2013/14.

• For carry forward purposes an annual allowance of £50,000 will apply for tax years 2011/12, 2012/13 and 2013/14. As each tax year passes, the reduction in the annual allowance to £40,000 from tax year 2014/15 dilutes how much can be paid. Up to £190,000 can be made as pension contributions for tax year 2014/15 without incurring an annual allowance tax charge. By tax year 2017/18, this will reduce to £160,000.

5

A summary of end of tax year planning action points is provided below:

Planning area Action points

Personal allowances Where possible make sure income is covered by personal allowances

Capital gains tax exemption If capital gains have been made consider using the annual capital gains tax exemption

Capital gains tax deferral for

large gains

Capital gains tax on the disposal of other assets can be deferred by reinvesting the proceeds in enterprise investment scheme shares

Annual inheritance tax exemption

make use of the annual inheritance tax exemption

Inheritance tax “normal expenditure out of income” exemption

Consider establishing a regular pattern of gifting out of income to use the inheritance tax “normal expenditure out of income” exemption

ISA allowances subject to affordability, make use of IsA allowances (including junior IsAs)

Income tax reducer investments Consider investing in enterprise investment scheme shares and venture capital trusts

Pension contributions Use any available pension annual allowance

END of TAX yEAR PLANNING ACTIoN PoINTs

6. Use your 2015/16 annual allowance in tax year 2014/15.

• This can be achieved by making the maximum allowable pension contributions in tax year 2014/15 and closing the pension input period (PIP) prior to the end of the tax year. An extra amount of £40,000 could then be paid in tax year 2014/15 for tax year 2015/16 provided the new PIP ends in tax year 2015/16.

• This could be useful for someone who wanted to maximise pension contributions prior to taking pension benefits.

7. Recover your personal allowance.

• For a higher rate tax payer with taxable income of between £100,000 and £120,000, a pension

contribution that reduces taxable income to below £100,000 would achieve an effective top rate of tax of 60%. For higher incomes, or larger contributions, the effective rate will be somewhere between 40% and 60%

8. Avoid the child benefit tax charge.

• Child benefit worth £2,475 to a family with three children is not payable if the taxable income of the highest earner exceeds £60,000. There is no tax charge if the highest earner has income of £50,000 or less. A pension contribution could be made to reduce income to below £50,000 to avoid the tax charge and it could be as simple as redirecting pension contributions paid for the lowest earner.

• The combination of higher rate tax relief on the contribution plus the child benefit tax charge saved can lead to effective rates of tax relief as high as 64% for a family with three children.

6

This guide is for general guidance only and represents our understanding of law and HMRC as at

February 2015. Whilst every care has been taken to ensure the accuracy of editorial content, no

responsibility can be taken for errors or omissions, or for actions taken or not taken as a result of

any statement in this document.

The value of investments can go down as well as up and you may not get back the full amount you

invested. The past is not a guide to future performance. Nothing in this document constitutes

advice or is intended to be read as such and should not form the basis on which investment

decisions are made.

Copyright 2015 Mercer llC. All rights reserved.MMB-ETYP0215

CoNTACT Us

PERsoNAL fINANCIAL PLANNING WITH mERCER mARsH BENEfITs

Mercer Marsh Benefits has a team of expert consultants providing personal financial planning advice and wealth management service to senior executives and other high net worth individuals. This can be paid for through corporate sponsorship or by individuals. Our services are transparent and fee based.

Mercer Marsh Benefits is a service

provided by Mercer ltd which is

authorised and regulated by the Financial

Conduct Authority. Registered in England

and Wales No. 984275. Registered Office:

1 Tower Place West, Tower Place, london,

EC3R 5BU.

Marsh ltd is authorised and regulated by

the Financial Conduct Authority.

Registered in England and Wales No.

1507274. Registered Office: 1 Tower

Place West, Tower Place, london, EC3R

5BU.

lONdON ANd SOUTHTim Robson Email: [email protected]

Tel: 020 7178 5781

Neville Khorshidchehr Email: [email protected] Tel: 020 7178 3446

Stuart Miller Email: [email protected]

Tel: 020 7178 7380

MIdlANdSSteven HilditchEmail: [email protected]

Tel: 0121 644 3768

SCOTlANdAllan Erskine Email: [email protected]

Tel: 0141 222 8563

NORTHMichael Kessler Email: [email protected] Tel: 0113 394 7681

You can also find out more online at: www.uk.mercer.com/

personalfinancialplanning

6