a new decade’s headaches—social networkingiframe.dri.org › dri › course-materials ›...

TRANSCRIPT

A New Decade’s Headaches—Social Networking

Sara M. Thorpe

Gordon & Rees LLP

275 Battery St., 20th Floor San Francisco, California 94111 (415) 986-5900 (415) 986-8054 [fax] [email protected]

Return to course materials table of contents

Sara M. Thorpe is a partner in the San Francisco office of the law firm of Gor-don & Rees LLP. Ms. Thorpe advises insurance company clients on insurance coverage issues and litigates insurance disputes, including bad faith claims. In addition, Ms. Thorpe is a frequent national speaker and actively involved in the DRI’s Insurance Law Committee. At the 2010 DRI Annual Meeting, Ms. Thorpe will be moderating a panel of executives from several insurance compa-nies as they discuss “A New Decade’s Headaches: What Keeps Insurance Execu-tives Awake at Night.”

A New Decade’s Headaches—Social Networking v Thorpe v 439

A New Decade’s Headaches—Social Networking

I. Introduction .............................................................................................................................................. 441

II. Keeping Up with New Ways of Communicating Has Its Benefits—but Can

Also Create New, Different, and Interesting Problems ...................................................................... 441

A. Embracing Innovation ..................................................................................................................... 441

B. The Aches and Pains That Can Follow .......................................................................................... 445

1. Policyholders’ Headaches Spawn New Risks and Products ............................................... 446

III. Conclusion—Take Two Aspirin … ....................................................................................................... 448

Table of Contents

A New Decade’s Headaches—Social Networking v Thorpe v 441

A New Decade’s Headaches—Social Networking

I. IntroductionA good business has interesting problems; a bad business has boring ones. The

idea is to make the problems so interesting that everyone wants to get to work and

deal with them.

There is a host of changes, developments, and problems causing headaches for the insurance

industry. Among them are new governmental regulations, nationalization of insurance, globalization

of insurance, catastrophes (natural and man-made), and economic hardships that place stress on busi-

nesses and limit the resources available to address problems.

This article addresses only one of the challenges—social networking—and only some aspects of

this broad topic. With the insurance industry embracing social networking and its clients’ involvement

in social media, new headaches arise for the insurance industry to address. A brief description of some

of the available tools (for the uninitiated) and examples of how the insurance industry is using them fol-

lows. Then we discuss some of the things insurance companies may worry about because of their use of

these tools, the risks faced by policyholders, and solutions insurance companies have developed.

II. Keeping Up with New Ways of Communicating Has Its Benefits—but Can Also Create New, Different, and Interesting Problems

A. Embracing Innovation

If you look back over your career—whether it spans forty years or only five—it is amazing how

communication has changed. Rotary dial telephones and party lines, telexes, telegrams, and shipping,

have largely been replaced. There are still, and probably will continue to be, billboards, blimps, TV and

radio promos, newspaper and magazine ads, mailings, sponsorships, and pamphlets to get the message

out and converse with others. But every year, there are new methods, technologies, and applications

introduced.

Insurance companies (and, as we discuss below, their customers) have embraced new forms

of technology and social networking to communicate internally, with each other, with agents, and with

customers. This includes use of web sites, YouTube, blogs, Facebook, MySpace, LinkedIn, and Twitter.

The Internet is a global system of interconnected computer networks that now serves billions of

users worldwide. This system connects millions of private, public, academic, business, and governmental

employees and entities. The Internet contains a vast amount of information (as well as misinformation).

Most people are very familiar with web sites, a collection of web pages under a domain name

or address, that provide publicly accessible information. The public sites are on the World Wide Web

(“www”). The domain names most commonly used include: “com” meaning commercial; “net” for net-

work (often associated with organizations involved in networking technologies like Internet service pro-

viders); “org” refers to organization and usually (but not always) refers to noncommercial entities; “edu,”

which is intended for educational institutions; “gov” for governmental entities; and “mil” for military.

Insurance companies use web sites not only to provide information about their companies and

products but to educate and communicate.

442 v DRI Annual Meeting v October 2010

For example, Geico’s web site provides information about insurance products, quotes, and pre-

ventative measures. It also provides the ability to report and track claims. Helpful links and entertaining

items are available to enhance relations with customers.

Likewise, Travelers’ web site supports its brand and provides the viewer with links to informa-

tion, to products and agents and report claims, to payment of bills, and to reviews of Travelers’ other

efforts, including involvement in charitable causes.

YouTube is a video-sharing web site created in 2005, which had been adopted by many users,

including politicians and insurance companies, to get their messages out. Recently Allstate used You-

Tube to promote a campaign relating to its auto insurance business, namely, rallying against texting

while driving.

Blogs are used to comment on all types of topics. Garden State Life Insurance’s blog, “The Life

Insurance Insider” (gardenstatelifeinsurance.blogspot.com) comments on life insurance denials, stud-

ies, underwriting, and purchase of life insurance.

Progressive has a variety of blogs available on its web site. The topics include customer success

stories, disaster response, and a blog that offers the reader a basic understanding of insurance. Below is a

screenshot from its “Understanding Insurance” blog.

A New Decade’s Headaches—Social Networking v Thorpe v 443

E-mail, short for electronic mail, allows users to communicate across the Internet. E-mail has

replaced letter writing, faxes, and even phone calls (and certainly in-person meetings) as a preferred

444 v DRI Annual Meeting v October 2010

means to communicate efficiently with customers and to forward information to other interested par-

ties. It is less formal than letter writing and, as a general rule, less time and attention are paid to the

content, spelling, and the way in which information is communicated. With that can come a host of

problems.

But ask any person under the age of 25, and you will find that e-mail may not be the preferred

way of communicating, at least not outside the office. And that is among the reasons insurance compa-

nies have ventured beyond e-mail.

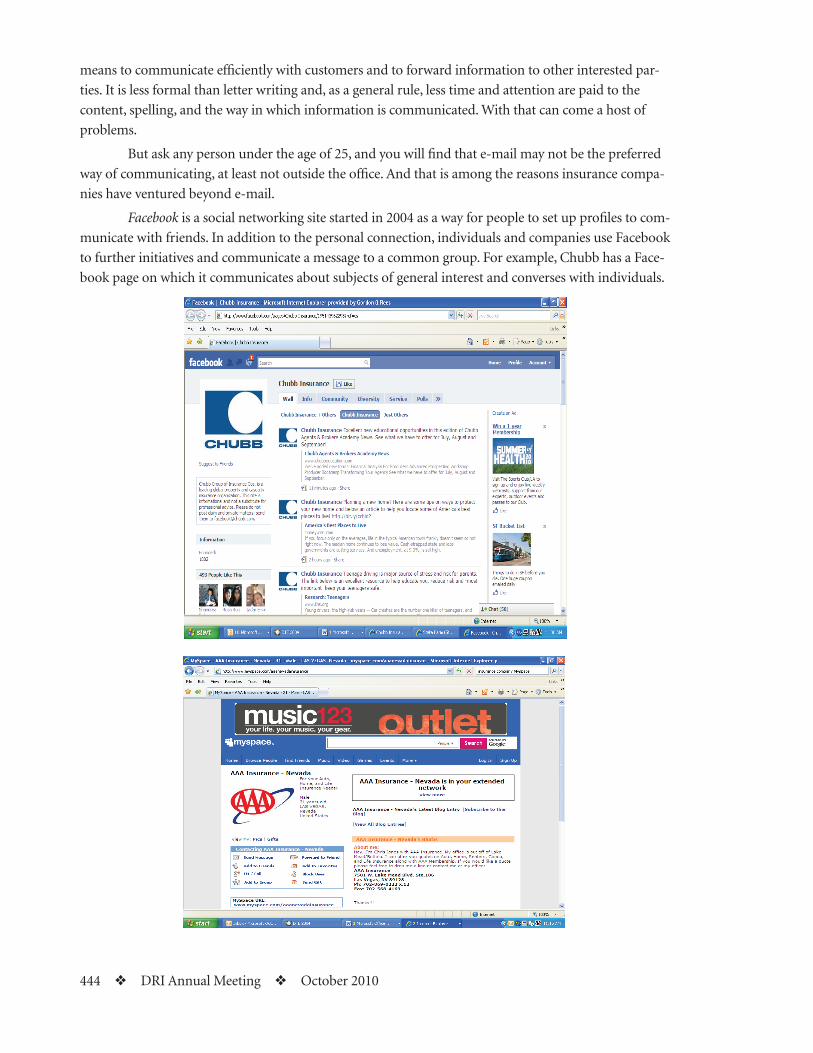

Facebook is a social networking site started in 2004 as a way for people to set up profiles to com-

municate with friends. In addition to the personal connection, individuals and companies use Facebook

to further initiatives and communicate a message to a common group. For example, Chubb has a Face-

book page on which it communicates about subjects of general interest and converses with individuals.

A New Decade’s Headaches—Social Networking v Thorpe v 445

MySpace is another social networking site that allows users to communicate through personal

and group pages.

LinkedIn is a business-oriented social network site that reaches millions of users all around the

world.

Possibly in the category of “TMI” (too much information) is Twitter, which allows users to send

and read other user’s messages called tweets. Tweets are messages of up to 140 characters. Users may

subscribe to another author’s tweets. All users can send and receive tweets via the Twitter web site: www.

twitter.com. State Farm and other insurers are using Twitter as a way of processing customer comments

and communicating about events the company sponsors.

Smartphones, mobile phones with computer capabilities (including Blackberry, Palm, I-Phone,

and others) provide other means of communicating. Text messaging or texting is communicating via

mobile phone. It is unlikely to be a preferred means of communication for the insurance industry

because there is a limit to the amount of information that can be communicated (and therefore more

room for misunderstanding). But it can be a means of sending out short bits of important information

such as deadlines, directions, and links.

Instant messaging refers to real-time direct text-based communication between two or more

people communicating via computer.

Chat rooms are sites on the Internet where people can communicate in real time and take the

pulse of what customers are thinking about particular products and subjects. Examples are Google Talk

and Yahoo! Messenger.

B. The Aches and Pains That Can Follow

Of course, what has to be in the back of one’s mind is whether all this good stuff creates addi-

tional risks and how can it be used against you.

As to the potential for additional risk in doing business, large questions loom on how to com-

ply with existing and future regulations in the insurance area. As one commentary recently pointed out:

446 v DRI Annual Meeting v October 2010

If insurance companies and agents do not use Facebook and Twitter carefully, they may

find themselves not only in violation of insurance laws, but also with an increased risk of

errors and omissions claims.

Susan T. Stead, Social Media Meets Insurance Regulation: Where Are We Headed, National Underwriter,

14 (June 7, 2010).

There are, of course, concerns about how and what the insurance company communicates, be

it providing information of a private nature or erroneous information. Anyone who has litigated insur-

ance cases also knows that even the best-intentioned well-worded communication can be twisted and

turned to the insurance company’s disadvantage.

Using all the information that is out there can create its own risks unless used wisely. For

instance, caution needs to be paid in using public information in investigating claims and allegations of

injury to ensure the source is legitimate, the information accurate, and the data can be substantiated.

In addition, with all this electronic information comes the problem of how to save it, store it,

retrieve it, use it, and defend against it. While in the not-too-distant past it was possible to find most of

what one needed in a physical claim or underwriting file, with perhaps some incomplete historical rec-

ords on how a product had been marketed or what representations were made in the course of issuing

a particular policy, but that is no longer the case. Now, with the use of social networks and electronic

discovery rules in the federal and many state courts, there is the need to keep an enormous amount of

electronic material and then locate specific information if litigation ensues.

A cautionary tale is provided by the Qualcomm-Broadcom discovery debacle played out over

the past couple years. What started as a patent infringement case over the manufacture, sale, and offer

to sell products, evolved into litigation involving many different law firms, costing the parties, firms,

and possibly their insurance companies millions of dollars over a discovery issue. The court initially

sanctioned lawyers and the client for intentionally withholding tens of thousands of documents. The

volume of the discovery was described by the court as requiring review of more than 1.6 million docu-

ments and the production of 22,500 documents (totaling more than 100,000 pages), which included

both hard copy and electronic documents. Qualcomm Inc. v. Broadcom Corp., 2010 WL 1336937, *2

(S.D. Cal. Apr. 2010).

What the court ultimately found to be the problem included this:

[O]utside counsel did not obtain sufficient information from any source to understand

how Qualcomm’s computer system is organized: where emails are stored, how often and

to what location laptops and personal computers are backed up, whether, when and under

what circumstances data from laptops are copied into repositories, what type of informa-

tion is contained within the various databases and repositories, what records are main-

tained regarding the search for, and collection of, documents for litigation, etc.

Id.

Of course, this type of problem only multiplies if, in addition to the sources mentioned by the

court, one adds Facebook, YouTube, and numerous other social networking tools.

1. Policyholders’ Headaches Spawn New Risks and Products

Insurance companies must not only keep up with new methods of communicating to conduct

their own business but must assess the new, different, and increased risks faced by the companies and

people they insure. As businesses incorporate the latest technology, they increase their risks.

A New Decade’s Headaches—Social Networking v Thorpe v 447

The risks—new and old—from social networking can include:

• compliancewithlawsaboutprivacyandnondisclosureobligations

• defamation

• defamationthroughtransmittalofinaccurateinformation

• inadvertentdisclosureofprivateinformation

• criminaldisclosureofinformation(e.g., hacking)

• copyrightinfringement(includingfromtakingcontentfromanothersource)

• patentinfringement

• disparagementofproductorsource

• harassment

The daily headlines (received more often these days via Internet connection and media links

rather than through print media) contain stories about liabilities that can arise through the use of social

networking.

For example, the content of texting and instant messaging is not the only problem in their use:

texting or instant messaging while driving can result in tragedy. Insurers have taken action to reduce

that risk. Allstate Insurance Company is running a campaign via Facebook, YouTube, its web site, and

other means called “X the TXT.” The main information section of its web page describes the goal of the

campaign:

Car crashes are the No. 1 killer of teens. We get it. You want to text all your friends to see

what’s up. But, reaching for a phone while driving increases your risk of crashing by nine

times. So take your thumbs off the cell phone and help keep your friends and family safe.

By joining this page, you’re pledging not to text and drive. Share your thoughts and stories

about texting while driving, or other ideas you have to help X the TXT.

Just as the Web reaches users and viewers all over the world, liability may have no jurisdic-

tional bounds. For instance the Florida Supreme Court ruled recently that a nonresident blogger can

be sued for defaming a Florida-based company on an out-of-state web site, which allegedly accused

the Florida company of criminal activity. Internet Solutions Corp. v. Tabatha Marshall, 2010 Fla. Lexis

943 (2010).

448 v DRI Annual Meeting v October 2010

Liability can pass from the perpetrator to others, depending on what later communicators

do with the offensive message. A California appellate court recently weighed in on the issue of when a

party can be held liable for passing along defamatory information and what constitutes “material con-

tribution” that would impose such liability. See Hung Tan Phan v. Lang Van Pham, 182 Cal. App. 4th 323

(2010).

In addition, innovative approaches can get policyholders in trouble as companies battle over

whose idea it was anyway. An example is the suit brought by Orion for patent infringement of an inter-

active feature in many auto manufacturers’ web sites. One of the patents allegedly infringed was a “build

your own vehicle” feature that allowed users to navigate through a menu to select, for example, col-

ors, engine and transmission types, and options to build a vehicle and obtain the pricing on that vehi-

cle. Hyundai Motors Am. v. National Union Fire Ins. Co., 600 F.3d 1092, 1094 (9th Cir. 2010). While the

allegations were ultimately found meritless, the Ninth Circuit held the insurers had a duty to defend

against the claims under the advertising injury coverage of the policy. Id. at 1104.

New insurance products are being created and marketed to address these new technologies,

products with names like “Social Media Policy,” and “Digital Technology Policy,” and “Multimedia Pol-

icy.” Some of these new products provide coverage for privacy, network security, and media liability.

With them, insurance companies also provide their customers with support to assist in preventing and

responding to data breaches, loss control, suggestions for preventative measures, and additional options

for professional liability coverage.

Not surprisingly, there are also bound to be new limitations on coverage from insurers that

have no intention of picking up these new risks under long-standing insurance products. Just as the last

decade saw the addition to general liability policies of exclusions or sublimits to face new threats of ter-

rorism, mold, silica, and technology-related claims, so will there be a need to further define the scope of

risks attendant on the use of social networking.

III. Conclusion—Take Two Aspirin …If there were no progress, new inventions, or new ways of communicating, there would be no

new ways of being creative and efficient. With the new, there will be challenges. However, if there were

no challenges, no headaches, no calamities, and no unforeseen difficulties, there would be no need for

insurance. There would be no need for creative minds to figure out solutions. So with all that is new

and good (or just interesting), comes the pain but also the opportunity. As we face these innovations,

we need to rely on old advice: take two aspirin. The right response is to understand the problem and

identify the ways to address new innovations and challenges.