a proposed city of stonecrest, georgia a fiscal feasibility analysis december, 2013

DESCRIPTION

A feasibility study for the proposed City of Stonecrest, in Dekalb County, Georgia. Prepared by the Carl Vinson Institute of Government Studies, University of Georgia.TRANSCRIPT

Assessing Budget Reduction Alternatives for the Georgia Veterinary Diagnostic Laboratory System

TableofContents

ExecutiveSummary...................................................................................................................................................1

Introduction..................................................................................................................................................................2

Revenues.........................................................................................................................................................................4

Expenditures...............................................................................................................................................................16

AppendixA...................................................................................................................................................................33

AppendixB...................................................................................................................................................................34

AppendixC...................................................................................................................................................................37

AppendixD..................................................................................................................................................................39

AppendixE...................................................................................................................................................................40

AppendixF...................................................................................................................................................................42

AppendixG...................................................................................................................................................................49

AppendixH..................................................................................................................................................................52

AppendixI....................................................................................................................................................................53

Tables

Table1:SummaryofEstimatedRevenuesandEstimatedExpenditures..........................................2

Table2:StudyAreaRevenueEstimates...........................................................................................................4

Table3:PropertyValuesinStudyAreaandUnincorporatedDeKalb.................................................7

Table4:2010PopulationfiguresforStudyAreaandUnincorporatedDeKalb..............................9

Table5:2010DemographicProfileofStudyAreaandPrimaryComparisonCities...................17

Table6:SummaryofExpenditureEstimates...............................................................................................18

Table7:StudyAreaParkAmenities.................................................................................................................24

1

ExecutiveSummary

Over the last several years, theCarl Vinson Institute ofGovernment has conducted a

numberoffeasibilitystudiesforproposedincorporations.Thosestudies,likethisone,have

been designed to provide the groups and legislators that have commissioned them an

opportunity to investigate the potential fiscal feasibility of an area being considered for

municipal incorporation. Essentially what the study seeks to determine is whether the

services sought to be provided by a hypothetical city along with the necessary

administrative apparatus can be adequately funded by the revenues that would be

available. The House of Representatives Governmental Affairs Committee of the Georgia

General Assembly has required by committee rule that bills proposing incorporation be

introducedinthefirstyearofabiennialsession,andthatafeasibilitystudybeconducted

before they can be considered in the second year and has named the Institute of

Governmentasoneofthetwouniversityinstitutionsqualifiedtoconductthestudy.

Todetermineavailablerevenues,wehavelookedattheamountsofrevenuebeingpaid

to the county government currently providing services to the area under study and any

revenue streams uniquely available tomunicipalities such as franchise fees orHOST tax

distributions. To determine the likely operational expenses associated with providing

parks, police, public works, planning and zoning, basic administrative costs, as well as

capital costs associated with those services and administration, we looked at two

comparisongovernmentsinthemetropolitanAtlantaarea,DunwoodyandSmyrna.

It is important to note the limitations of these types of studies. They cannot predict

everypossiblevariablethatmayoccurinthefuturewithapotentialimpactonthecostsof

government.Additionally,thestudyisnotintendedtobeamodelbudgetforanewcity.A

newlyelectedcitycouncilwillendeavortorepresenttheirconstituenciesandwillhavea

setofprioritiesthatmayimpactbothtaxingandspendingpatterns.

Weareconfidenthowever, that lookingatcurrentlyavailablerevenuesandanalyzing

comparablemunicipalgovernmentspendingthatourstudyreflectsarealisticassessment

of likely fiscal feasibility. Based on our analysis, we find that likely currently available

2

revenues fall short of likely expenditures for the services identified to be provided, and

thereforehaveconcludedthatacitycomprisedoftheStonecreststudyareaisnotfiscally

feasiblewithoutsignificantrevenueenhancement.

Table1:SummaryofEstimatedRevenuesandEstimatedExpenditures

StudyArea PerCapita

AnnualOperatingExpenses $35,667,177.57 $433.88

AnnualCapitalExpenses $9,476,847.55 $115.28

TotalAnnualExpenses $45,144,025.11 $549.16

TotalAnnualRevenues $31,081,838.00 $378.10

TotalAnnualRevenueslessMotorVehicleTax

$29,885,668.00 $363.55

AmountofRevenuelessMotorVehicleTaxexceedingExpenses

($15,258,357.11) ($185.61)

Introduction

TheStonecrestCityAlliance(hereinafter“SCA”)andStateSenatorRonaldRamsey,

Sr. engaged the Carl Vinson Institute of Government to study an area within

unincorporated DeKalb County in order to aid their consideration of the area’s possible

incorporation.Stonecrest,orthe“studyarea,”asitisreferredtointhisreport,iscomprised

of 37.94 square miles1 and is situated in southeast DeKalb County. The study area is

borderedtothenorthbyGwinnettCounty,totheeastbyRockdaleCounty,andtothesouth

by both Rockdale andHenry Counties. The study area’swestern boundary runs roughly

alongalinestretchingfromCountyLineRoadalongtheHenryCountyborderinthesouth

to Rockbridge Road along the Gwinnett County border in the north. The study area is

separatedfromexistingcitiesinDeKalbCountybyunincorporatedportionsofthecounty

1AsdeterminedthroughGISmapping.

3

andcompletelysurroundstheexistingcityofLithonia.SeeAppendixAforamapofthestudy

area.

This report provides estimates of revenues and expenditures a potential City of

Stonecrest, if incorporated, could anticipate inproviding certainmunicipal services for a

single fiscal year. The revenue estimates are primarily based upon actual revenues

collectedfortheunincorporatedareabyDeKalbCountyinfiscalyear(FY)2012aswellas

projections for franchise fees, the Homestead Option Sales Tax, and the Community

DevelopmentBlockGrant.Expenditureestimatesareprimarilybasedoncostsforservices

in the cities of Smyrna and Dunwoody. For each city that was used to establish costs

estimates, CVIOG faculty examined its budget documents and conducted interviewswith

citystafftoinquireastotheproperallocationofcertaincostsandtoclarifyfiguresandline

itemsreportedintheirbudgets.

ThecitiesofSmyrnaandDunwoodywereselectedattheoutsetofthestudytobe

usedastheprimarycomparisonsforexpenditurepurposes.Thesecitiesaresimilarinsize

tothestudyareaandarelocatedinmetropolitanAtlanta.Oneofthecitiesisfairlynewin

thatDunwoodywasincorporatedonDecember1,2008.Thefiscalyearsof2011and2012

wereusedfromeachcitytoestimatecosts,becausetheyconstitutedthebestavailabledata

duringthetimethestudywasconducted.Formostofthattime,Dunwoodycontractedwith

threedifferentprivate sector serviceproviders inorder toprovide city services. Smyrna

provides municipal services through its own directly employed city staff. Both cities

directlyemploytheirownpolicepersonnel.

Estimatesgiveninthisreportarebasedontaxleviesandservicelevelsforacitynot

yetcreated;and, thus, theyshouldnotbeviewedascertainties.While it isourhopethat

thisreportassistswiththepublicconsiderationofapotentialmunicipal incorporation, it

shouldnotbeconstruedtoconstituteapositioneitherfororagainsttheestablishmentofa

CityofStonecrestbytheCarlVinsonInstituteofGovernment(CVIOG).

4

I. Revenues

The revenue estimates outlined below include all major revenue sources a city

representingthestudyareawouldhavecollectedhaditexistedin2012andassessedtaxes

andfeesatratessimilartoDeKalbCountyinthatsameyear.Incalculatingtheseestimates,

weappliedmetricsusedinpriorresearchthatwereacceptedbystakeholdersinsomeof

themost recent incorporation studies. Thus, this report uses similar revenue estimation

methodologiesasthoseprovidedinbothGeorgiaStateUniversity’s2007report,“TheFiscal

ImpactonDeKalbCountywithPossible IncorporationofDunwoody,Georgia” and theCarl

Vinson Institute’s 2008 report, “Revenue and Expenditure Analysis of a Proposed City of

Dunwoody” to the extent possible. Themethod for determininghowmuch revenuewas

assignedascomingfromthestudyareaisdescribedinTable2.

Table2:StudyAreaRevenueEstimates

RevenueSource DataSource Amount

OccupationTaxesActualsfrom2012Calendaryearfor

Businesslicenses $1,781,792

AlcoholicBeverageExciseTaxes

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $624,491

PersonalPropertyTaxes

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $606,126

Hotel/MotelTaxes

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $430,293

Hotel/MotelTaxes(restrictedtotourism)

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $286,862

BusinessLicense–Police

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $161,857

BusinessLicense–AlcoholicBeverages

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $1,351,124

5

Table2:StudyAreaRevenueEstimates(continued)

RevenueSource DataSource Amount

BankSharesTaxes

RatioofassessedvalueofcommercialpropertyinstudyareatoDeKalb

unincorporatedarea $126,658

Intangible

RatioofassessedvalueofallpropertyinstudyareatoDeKalbunincorporated

area $99,688

DevelopmentFund

Ratioofassessedvalueofresidential&commercialpropertyinstudyareato

unincorporatedarea $567,178

ZoningandVarianceFeesandPermits

Ratioofassessedvalueofresidential&commercialpropertyinstudyareato

unincorporatedarea $12,355

InsurancePremiumsRatioofpopulationinstudyareato

DeKalbunincorporatedarea $4,026,408

Fines&ForfeituresRatioofpopulationinstudyareato

DeKalbunincorporatedarea $3,626,090

StormWaterFund 2013ActualsfromTaxCommissioner $2,543,990

MotorVehiclesTaxes*Ratioofpopulationinstudyareato

DeKalbunincorporatedarea $1,196,170

LawEnforcement‐ConfiscatedMoniesFund

RatioofpopulationinstudyareatoDeKalbunincorporatedarea $281,037

SaleofPrintedMaterial‐Police

RatioofpopulationinstudyareatoDeKalbunincorporatedarea $43,935

HomesteadOptionSalesTaxes(restrictedtocapital)

CalculationpursuanttoO.C.G.A.§48‐8‐104 $2,095,151

StateGrant‐CommunityDevelopmentBlockGrant

Averagerevenuefrom19Georgiacitiespopulationrangebetween30,000‐

94,000from2008‐2011 $628,868

MiscellaneousThisrepresentsanumberofsmallrevenuesources.SeeAppendixB. $36,877

FranchiseFees Regressionwithdatasetof32cities $5,749,374

RealPropertyTaxes 2013ActualsfromTaxCommissioner $3,893,045

6

Table2:StudyAreaRevenueEstimates(continued)

RevenueSource DataSource Amount

RealPropertyTaxes‐Penalties

RatioofPenaltiestoPropertyTaxesinUnincorporatedDeKalb $62,289

StreetLights 2013ActualsfromTaxCommissioner $831,505

SpeedBumps 2013ActualsfromTaxCommissioner $18,675

TotalRevenueEstimate $31,081,838

TotalRevenuelessMotorVehicleTaxes

$29,885,668

ReliesonFY2012dataunlessotherwiseindicated.SeeAppendixCforcountyrevenuedatadetail.

*UnderO.C.G.A.§48‐5C‐1(c)(3)citiesformedonorafterJanuary1,2013willnotreceiveafirststepdistributionoftheLocalTitleAdValoremTaxFeeand,consequently,thissourceofrevenuewilldisappearforthestudyareaoverashortperiodoftimeasresidentsoftheareapurchasenewvehicles.

A. MethodologiesUtilizingRatiosofAssessedRealPropertyValue

AnumberoftaxescurrentlycollectedintheunincorporatedareaofDeKalbCountyare

generatedsolelybycommercialactivity.Inordertoobtainestimatesofhowmuchrevenue

wouldbegeneratedbythesetaxes,acomparisonwasmadebetweentheassessedvalueof

commercial property in the study area and the unincorporated area of the county.

Assuming that the ratio of commercial real property value is a proxy for commercial

activity,thisratiowasappliedagainstactual2012collectionsforseveralrevenuesources

whicharedescribedbelow.Actualcountyrevenuesusedtotabulatethedifferentrevenue

estimationswereprovidedbyDeKalbCounty.Appraisedvaluesfortherealpropertyinthe

studyareawereprovidedbytheDeKalbTaxCommissioner,aswerethetaxdigestvalues

forthecounty’sunincorporatedarea.Todeterminerevenuefromheavyequipmenttaxes,

the same approachwas taken utilizing the ratio for industrial property. SeeAppendixB.

Table3illustratestheratiosofresidential,commercial,industrial,utilityandtotalassessed

propertyvalueofthestudyareatotheunincorporatedareainDeKalbCounty.

7

Table3:2013PropertyValuesinStudyAreaandUnincorporatedDeKalb

StudyArea UnincorporatedDeKalbCounty

PercentStudyAreato

Unincorporated

AVResidentialProp $677,541,552 $6,326,833,769 10.71%

AVCommercialProp $425,189,227 $2,755,000,357 15.43%

AVCom&Res $1,102,730,779 $9,081,834,126 12.14%

AVIndustrialProp $123,611,342 $610,887,609 20.23%

AVUtilityProp $0 $286,113,789 0%

TotalAssessedValue $1,226,342,121 $9,978,835,524 12.29%

OccupationTaxes

Occupationtaxesare leviedonpersonsandentitiesengaged inoccupationsor trades for

profit‐making purposes. DeKalb County levies an occupation tax in the unincorporated

area.

AlcoholicBeverageExciseTaxes

Alcoholic beverage excise taxes are collected on individual retail sales of alcoholic

beverages.

PersonalPropertyTaxes

Personalpropertytaxesareleviedonpersonalpropertyownedbycommercialbusinesses.

Hotel/MotelTaxes

Hotel/moteltaxesarecollectedbasedonapercentageofthenightlyroomratechargedby

hotelswithinthejurisdictionofacityorcountythatleviesthetax.DeKalbCountyleviesa

tax of 5% of the nightly room rate. Pursuant to state law, however, only the revenue

generated by a 3% taxmay be spent for general fund purposes; the remaining revenue

must be spent on activities promoting tourism, generally by contract with a non‐profit.

8

Thus,someofthefundsidentifiedinthetablearerestrictedtothispurpose.SCAverified

thepresenceofatleast9hotelsinthestudyarea.ThesearelistedinAppendixD.

BusinessLicenses‐Police

Thislineitemrepresentsfeesgeneratedbybackgroundchecksthatarerequiredtoobtain

licenses for various locally‐regulated activities (e.g. alcoholic beverage pouring permits,

taxicablicenses,etc.).

AlcoholicBeverageLicenses

InordertosellalcoholicbeveragesinGeorgia,aproprietormusthavebothalocalandstate

licensetoselleitherinpackagesorbythedrink.Locallicensesarerenewedannuallyand

eachyear’srenewalisaccompaniedbypaymentofafee.

BankSharesTaxes

Citiesandcountiesarepermittedto levya taxondepository financial institutionshaving

officeslocatedintheirrespectivejurisdictions.

IntangibleTaxes

Intangibletaxes(recordingtaxes)arecollectedonpropertythatissoldatthetimeitsdeed

is recorded. This number was obtained by applying the ratio of the assessed value of

commercial and residential property in the study area to the assessed value of the

commercialandresidentialpropertyintheunincorporatedspecialtaxdistrictagainstthe

amountofrevenuecollectedbythecountyintheunincorporatedarea.

DevelopmentFund

Thisamount represents fees charged forpermits related todevelopment (e.g., plumbing,

electrical,HVAC,andbuildinginspections).

ZoningandVarianceFeesandPermits

This figure represents fees charged of applicants for zoning changes and variances. This

figurewasobtainedbyapplyingtheratioofassessedvalueofcommercialandresidential

9

property in the study area to the unincorporated area against the revenue generatedby

theseactivitiesintheunincorporatedarea.

B. MethodologiesUtilizingRatiosofPopulationoftheStudyAreatotheUnincorporatedArea

Anumberofrevenuesourcesdependmoredirectlyuponthenumberofindividuals

engagingincertainbehaviorssuchasthepurchaseofinsurance,watchingcabletelevision,

owning a car, and committing traffic offenses. For these revenue sources, assumptions

weremadethatthesebehaviorsarefairlyconstantacrosstheunincorporatedpopulation

of DeKalb County, and thus the ratio of the population of the study area to the entire

unincorporated area was applied to the actual revenues. Table 4 gives the population

figuresforthestudyareaandunincorporatedDeKalbCounty.

Table4:2010PopulationfiguresforStudyAreaandUnincorporatedDeKalb

StudyArea UnincorporatedDeKalbCounty

PercentStudyAreato

Unincorporated

Population 82,205 511,619 16.07%

MedianHouseholdIncome

$44,715 $36,000

PovertyRate 15.5% 17.59%

PopulationfiguresforthestudyareaweresuppliedbytheGeorgiaGeneralAssemblyOfficeofCongressionalandLegislativeReapportionment;otherfiguresforpopulations,medianhouseholdincome,andpovertyratecamefromthe2010CensusandtheAmericanCommunitySurvey,2007‐2011estimatesutilizing2010BlocksandBlockgroupsthatapproximatedthestudyarea.

InsurancePremiumsTax

Insurancepremiumstaxesarecollectedonpolicieswrittenforbothpropertyandcasualty

and life insurancepoliciespurchasedby those insuredwithin the jurisdictionofacityor

unincorporated areas of a county. The figure given above is based on the ratio of the

populationofthestudyareatothepopulationoftheunincorporatedarea.

10

FinesandForfeitures

Traffic offenses and certain misdemeanor offenses may be adjudicated in county level

(recorders) and city level (municipal) courts, and fine revenue from these offenses is

retainedbythelocalgovernmentwithjurisdiction.Anassumptionwasmadethatratesof

pettyoffensesof thisnature takeplaceona fairlyconsistent levelacrossunincorporated

DeKalb,andthepopulationratiowasappliedto2012actualrevenue.

MotorVehicles

Motorvehiclesaresubjecttoanadvaloremtaxleviedontheirassessedvalue.Thefigure

aboveisderivedbyapplyingthepopulationratioandassumescarownershipisconsistent

acrosstheunincorporatedarea.Onagoing‐forwardbasis,thestudyareashouldexpectits

revenuefromthissourcetodecreasesignificantly.O.C.G.A.§48‐5C‐1(c)(3)providesfora

two‐stepdistributionofLocalTitleAdValoremTaxFee(“TAVT”)proceedsonamonthly

basis. Over time, as annual ad valorem taxes phase out, the first step distribution will

gradually increase, eventually comprising the majority of motor vehicle property taxes.

Underthestatutorystructure,citiesformedonorafterJanuary1,2013willnotreceivea

first‐stepdistribution.2

MotorvehiclespurchasedandtitledinGeorgiapriortoMarch1,2013aregenerallysubject

to annual ad valorem taxes pursuant to Chapter 5 of Title 48. Vehicles purchased on or

afterMarch1,2013aresubjecttoTAVTandareexemptfromannualadvaloremtax.Thus,

as Georgia taxpayers purchase newmotor vehicles, the annual ad valorem tax revenue

collectedwilldecreasegraduallyeachyear.3

ThefirststepdistributionofTAVTproceedsiscalculatedbycomparingthe2012annualad

valoremtaxescollectedinagivenmonthtotheamountcollectedinthesamemonthofthe

currentyear.Fora“newcity”whichcollectednoannualadvaloremtaxinagivenmonth

during2012,thereisnofigureorrecordavailableuponwhichtocomparesubsequentyear

annualadvaloremtaxrevenue.Thus,thereductionoffsetamountwillalwaysbezero,and

2GeorgiaDepartmentofRevenueTitleAdValoremTaxFeeLocalDistributionGuidance,October30,2013.3Id.

11

thefirststepdistributiontosuch“new”citywillalsobezero.4TheGeorgiaDepartmentof

RevenueTitleAdValoremTaxFeeLocalDistributionGuidanceletterisincludedinAppendix

E.

LawEnforcement‐ConfiscatedMoniesFund

This fund represents revenues received from money confiscated in drug cases. An

assumptionwasmadethatpoliceseizureofmoneyfromillegaldrugtraffickingwouldbe

proportionatetopopulation.

SaleofPrintedMaterial‐Police

Police departments are able to charge fees for copies of police reports, incident reports,

motorvehicleaccidentreportsandothermiscellaneousmaterials.Itisassumedthatthere

wouldbesomedemandforthesametypesofdocumentsfromamunicipality.

C. HomesteadOptionSalesTax(restrictedtocapital)

The Homestead Option Sales tax is a one cent countywide sales tax originally

enacted to provide for county property tax rollback that is levied on the sales of most

goods. The HOST tax has been amended over time to allow up to twenty percent of its

proceedstobespentoncapitalneedsandtoprovidethatnewlyincorporatedcitiesreceive

aportionof theproceeds fromthecountywide levy touse for theircapitalneeds.Avery

specificformulafoundinO.C.G.A.§48‐8‐104providesforthecalculationoftheamountto

bedistributedtoanewmunicipalitybasedonboththeleveloffundstobespentinagiven

year on capital as determined by the county and the relative size of the residential

homesteadrealpropertytaxdigestsoftheapplicablelocalgovernments.Theintentbehind

thestatutorychangesthatallowcitiesinDeKalbCountytoreceivedistributionsseemsto

reflectadesiretoequalizethebenefitof thetaxrollbacktomunicipaltaxpayersthatpay

property taxes tocities insteadof thecounty forcertainservices.Thus, the “equalization

payments” made to cities under the statute are proportional to the size of the city’s

residentialhomesteaddigest.

4Id.

12

Another variant in the HOST proceeds calculation is the capital factor set by the

county, which determines the amount of the overall proceeds that can be spent by the

county on capital needs. Using themost recent HOST certification from the DeKalb Tax

Commissioner to establish the total homestead digest for the county and each qualified

municipality,acalculationofthe2013HOSTproceedsamountwasappliedagainstacapital

factor of 20%. The homestead tax digest for the study areawas calculated based on tax

informationprovidedbytheDeKalbTaxCommissioner’sOffice.CVIOGcalculatedthetotal

amount of distributions likely due to all qualified municipalities to determine the total

amount of equalization payments. Appendix F contains these calculations using the

spreadsheetutilizedbytheGeorgiaDepartmentofRevenueaswellasthemostrecentcounty

certificationletter.

It should be noted that distributions are made from the previous year’s tax

collections,soanewcitywouldhavetowaittobegincollectingthisdistribution.

Itshouldfurtherbenotedthattheincorporationofanyothercitieswilldecreasethe

amountofHOSTproceedsreceivedbythestudyareacitybyvirtueoftheHOSTcalculation.

The HOST calculation distributes the capital outlay proceeds based on the equalization

calculations. In the event the amount of the capital outlay proceeds exceeds the

equalizationpaymentsduetoeachqualifiedmunicipality,theexcessisamountisdivided

upamongallthequalifiedmunicipalitiesbasedontheirshareofthehomesteaddigestto

the total digest. Thus, additional cities will decrease the amount each existing city is

receivingfromthisexcesscapitaloutlayamount.

Finally,thereisa“tipping”pointafterenoughnewterritoryisincorporatedwhere

the amount due to themunicipalities under the equalization calculationwill exceed the

amountofcapitaloutlayproceedsavailablefordistribution.Atthispoint,HOSTproceeds

willbeallocatedbasedsimplyontheratioofthenethomesteadofeachmunicipalitytothe

totalhomesteaddigest.

13

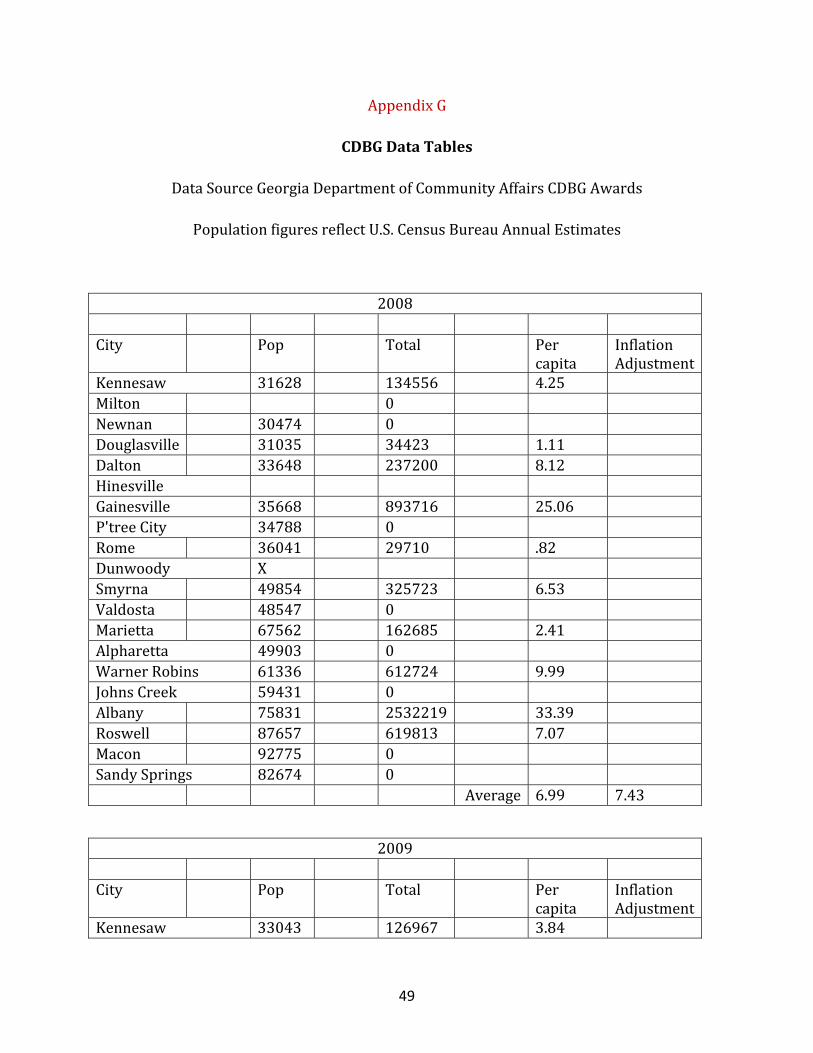

D. CommunityDevelopmentBlockGrant

CommunityDevelopmentBlockGrants(CDBG)areawardedbythefederalandstate

governmentstolocalgovernmentsmeetingcertaincriteria.Toobtainanestimateforwhat

acitycomprisedofthestudyareamightexpecttoreceivefromsuchgrants,fouryearsof

awardsfor19differentGeorgiacitiesranginginpopulationfromapproximately30,000to

96,000wereaveragedintoapercapitaamount,adjustedforinflationandappliedagainst

thepopulationofthestudyarea.ItisalsoworthyofnotethatDunwoodyhasnotreceived

any CDBG funds since their incorporation. The fact that Dunwoody is a new city likely

contributes to this fact. Smyrna,however,has receivedCDBG funds in recentyears.5The

datausedforthesecalculationsisshowninAppendixG.

E. FranchiseFees

Somerevenuesourcesareunique tomunicipal corporations inGeorgia.Franchise

fees are essentially rental compensation by a private utility company for use of a city’s

publicrights‐of‐way.Forestimatingtheelectric,naturalgas,cableandtelephonefranchise

fees,theauthorsutilizedaregressionmodelwithfranchisefeespaidto30citiesinGeorgia

in 2011 and 2 cities in 2010, which was the latest data available. The data was only

available as a total number for franchise fees, and not broken down by type.6 The

regressionoutputisshowninAppendixH.

FranchiseFees‐Cable

Federal and state lawallows cities and counties to enter into franchise agreementswith

cablecompaniestocompensatethelocalgovernmentfortheiruseofthepublicrights‐of‐

way.Thesefeesareusually5%oftherevenuederivedfromcabletelevisionservices.

5http://portal.hud.gov/hudportal/HUD?src=/program_offices/comm_planning/communitydevelopment/programs6GAPowerprovidedanestimatedfranchisefeeamountfromelectriconlyforthestudyareaof$3.30million.

14

FranchiseFees‐Electric

Franchise fees for electric utilities are the result of contracts between municipal

corporations and electric utility providers that occupy a city’s right‐of‐way. These

agreements typically provide that 4%of the gross sales of electric powerwithin a city’s

limitslesssalestaxesandfuelcostsbepaidannuallytothecitytocompensatethecityfor

useandoccupancyofpublicproperty.Thesoleelectricutilityproviderinthestudyareais

GeorgiaPower.PursuanttorecentrulingsbytheGeorgiaPublicServiceCommission,half

of the annual franchise feepaidbyGeorgiaPower tomunicipal corporations is collected

fromtheratebaseofallGeorgiaPowercustomersstatewide(asacostofdoingbusiness)

andtheotherhalf iscollectedasa feesolelyon theelectricbillsofcustomerswithin the

municipalitycollectingthefee.Thus,collectionoftheelectricfranchisefeewouldresultin

anincreaseoflessthan2%intheelectricbillsofcitycustomers.

FranchiseFee‐NaturalGas

AtlantaGasLightistheonlynaturalgasdistributionutilityoccupyingpublicrights‐of‐way

in the study area. Franchise fees paid tomunicipal corporations are paid out of the rate

baseofallAGLcustomersasacostofdoingbusiness.

FranchiseFees‐Phone

Since only landline telephone service requires occupancy of themunicipal right‐of‐way,

movement away from landline service to internet‐based and cell telephony services is

makingthisadiminishingrevenuesourceformunicipalcorporations.

F. RealPropertyTaxes

The figures givenhere represent the amountof realproperty taxesbeingpaidby

studyarearesidentstothecountyfortheservicesbeingprovidedthroughcountyspecial

service tax districts. The actual amount paid in Fiscal Year 2013 by the residents who

would actually live in the study areawasprovidedby theTaxCommissioner’s office. It

shouldbenotedthatbecausestatutorycountyhomesteadexemptionsandtheHomestead

Option Sales Tax credit must be applied to the taxable value of residential homestead

15

property to determine the amount of revenue generated by application of a particular

millagerateincountyspecialdistricts,thisspecificmillageratedoesnotdirectlyequateto

a municipal millage rate. In other words, the method utilized here demonstrates the

amount of property tax revenue being generated in the study area for the county that

wouldbecomeavailabletoamunicipalitythattookovertheprovisionofthosemunicipal

servicescurrentlybeingprovidedbythecounty if theamountofpropertytaxcollections

remainedconstantbutwasinsteadcollectedbyacity.

Recentstatutorychangeshaverequiredthatpoliceservicesbebrokenapartfromtheother

specialservices taxdistrictservicesandbilledasaseparate line item.7The2013millage

rateforthepoliceservicesthatwerepreviouslyincludedinthespecialservicestaxdistrict

is4.25millsandthemillageratefortheremainingunincorporatedspecialservicesis .71

mills. Together, these two millage rates equal 4.96 mills and represent services funded

fromthepreviousunincorporatedspecialtaxdistrict.

Penalties

Theratioofpenaltiestorealpropertytaxes intheunincorporatedareaforcalendaryear

2012wasappliedtothestudyareapropertytaxesprovidedbytheTaxCommissioner.

G. OtherActualsfromTaxCommissioner

StormWaterFee

DeKalbCountycollectsastormwaterutilityfeeinordertodefraythecostsassociatedwith

infrastructure to handle storm water runoff. The fees imposed are designed to be

proportionate to the amount of runoff created by impervious surfaces. The 2012 rates

charged by DeKalb County were $48 per single family residential dwelling annually.

Multipledwellingunitsareeachchargedhalfofthatrateannually,andallotherimproved

propertiesarechargedatarateof$48per3,000squarefeetofimpervioussurface.Asthe

amount of impervious surface in the study area is unknown at this time as well as the

actual collections from the study area, the population ratio was used here as a rough

7 SeeHB607,effectiveMay11,2011.

16

approximationofdevelopmentand,consequently, reflectiveof theamountof impervious

surface.Becausestormwaterutilitiesoperateasanenterprisefundandbecausethefees

collected must be used for storm water utility purposes, this figure was also used to

calculateexpenditures.

StreetLightsandSpeedBumps

StreetlightsandSpeedBumpprogramsalsooperateasenterprisefunds.Theactualsfor

thestudyareawereprovidedbytheTaxCommissionerandthesesamenumberswerealso

usedintheexpenditureanalysis.

II. Expenditures

Theexpenditureestimatesbelowarebasedprimarilyonexpendituresincurredby

comparablegovernmentstoprovideservicessimilartothosecontemplatedtobeprovided

byacitycomprisedofthestudyarea.Incalculatingtheseestimates,CVIOGfirstestablished

twoprimary comparable governments, the cities ofDunwoody and Smyrna. These cities

were selected based on several factors. Dunwoody is new, officially incorporated in

Decemberof2008,whileSmyrnaisanestablishedcity.Bothcitiesarelocatedinthemetro

Atlantaareaandarecloseinpopulationtothestudyarea.Dunwoody,likethestudyarea,is

whollycontainedinsidethelimitsofDeKalbCounty.Smyrna’spopulation,povertyrateand

medianhouseholdincomeareverysimilartothestudyarea,anditslocationinthemetro

Atlanta area makes it a good comparison city. Profile data for the study area and the

comparisoncitiesisgivenbelowinTable5.

17

Table5:2010DemographicProfileofStudyAreaandPrimaryComparisonCities

StudyArea Smyrna Dunwoody

Population 82,205 51,265 46,267

Race‐White 4.26% 46.6% 64.1%

Race‐Black 94.8% 31.6% 12.6%

Race‐Asian .56% 4.9% 11.1%

Race‐Other .38% 16.9% 12.2%

Hispanicethnicity* 2.65% 14.9% 10.3%

MedianIncome $43,715 $55,989 $74,411

Poverty% 15.5% 12.8% 10.4%

*Hispanic is recognized as an ethnicity rather than a race in Census Data. Persons indicating HispanicethnicityarealsocountedasbelongingtoaracialgroupbytheCensus.

PopulationfiguresforthestudyareaweresuppliedbytheGeorgiaGeneralAssemblyOfficeofCongressionalandLegislativeReapportionment;other figures forpopulationsandmedian incomeandpovertyratecamefromthe2010CensusandtheAmericanCommunitySurvey,2007‐2011estimatesutilizing2010BlocksandBlockgroupsthatapproximatedthestudyarea.

Formostofthecostestimatesgiven,thefigureswerederivedbyaveragingtheper

capitacostsofexpendituresmadebythetwocomparisoncitiesforboththefiscalyearsof

2011 and 2012. In some instances, it was not possible to allocate costs to one ormore

departmentsbecauseofthewayacityhadaggregateditscosts.Todeterminehowbestto

interpret the budget and other financial documents of each city, faculty from CVIOG

interviewedtheFinanceDirectorsofbothDunwoodyandSmyrna.Theexplanationforhow

eachestimatewasderivedisincludedbelow.Thesummaryoftheexpendituresisgivenin

Table6below.

Todetermineservicesonwhichtoestimateexpenditures,itwasassumedthatacity

comprised of the study area would provide the services currently provided to the

unincorporated area via the unincorporated special tax districts. This includes police,

parks,roadmaintenance,andstormwater. Itwasalsoassumedthatanewcitywouldbe

responsibleforplanningandzoning;butthatfireandrescue,E‐9‐1‐1,sanitation,andother

18

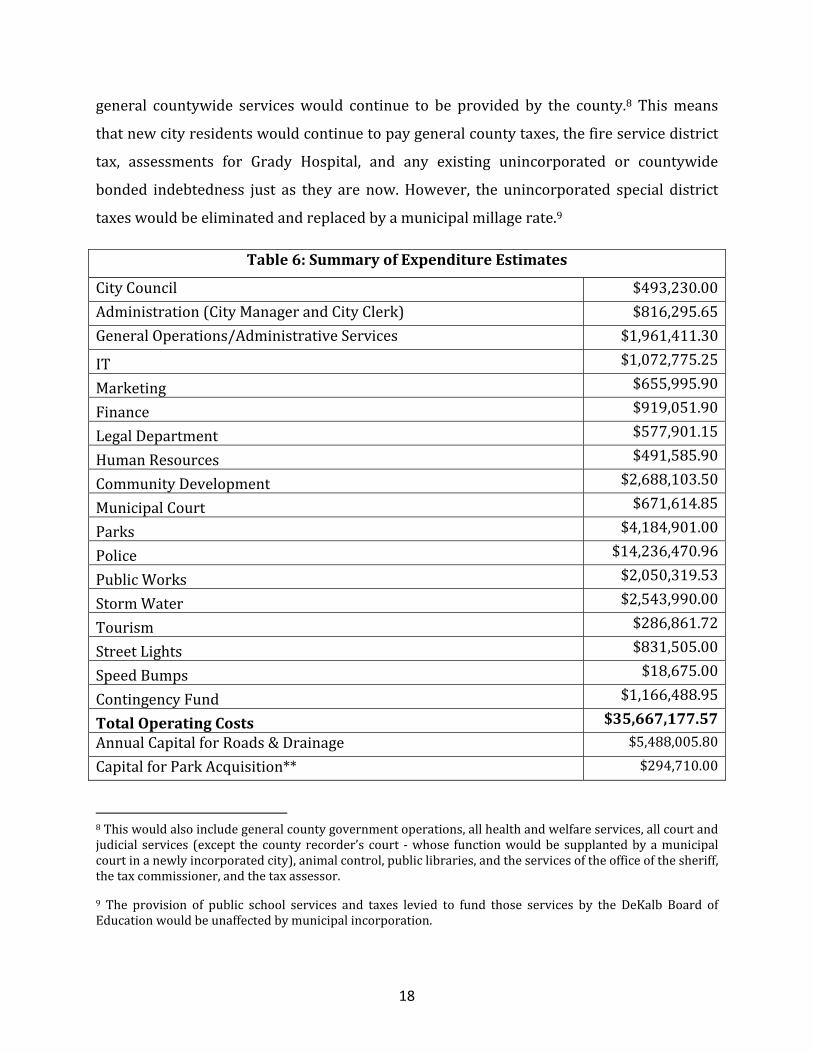

general countywide serviceswould continue to be provided by the county.8 Thismeans

thatnewcityresidentswouldcontinuetopaygeneralcountytaxes,thefireservicedistrict

tax, assessments for Grady Hospital, and any existing unincorporated or countywide

bonded indebtedness just as they are now.However, the unincorporated special district

taxeswouldbeeliminatedandreplacedbyamunicipalmillagerate.9

Table6:SummaryofExpenditureEstimates

CityCouncil $493,230.00

Administration(CityManagerandCityClerk) $816,295.65

GeneralOperations/AdministrativeServices $1,961,411.30

IT $1,072,775.25

Marketing $655,995.90

Finance $919,051.90

LegalDepartment $577,901.15

HumanResources $491,585.90

CommunityDevelopment $2,688,103.50

MunicipalCourt $671,614.85

Parks $4,184,901.00

Police $14,236,470.96

PublicWorks $2,050,319.53

StormWater $2,543,990.00

Tourism $286,861.72

StreetLights $831,505.00

SpeedBumps $18,675.00

ContingencyFund $1,166,488.95

TotalOperatingCosts $35,667,177.57

AnnualCapitalforRoads&Drainage $5,488,005.80

CapitalforParkAcquisition** $294,710.00

8Thiswouldalsoincludegeneralcountygovernmentoperations,allhealthandwelfareservices,allcourtandjudicial services (except thecounty recorder’s court ‐whose functionwouldbe supplantedbyamunicipalcourtinanewlyincorporatedcity),animalcontrol,publiclibraries,andtheservicesoftheofficeofthesheriff,thetaxcommissioner,andthetaxassessor.

9 The provision of public school services and taxes levied to fund those services by the DeKalb Board ofEducationwouldbeunaffectedbymunicipalincorporation.

19

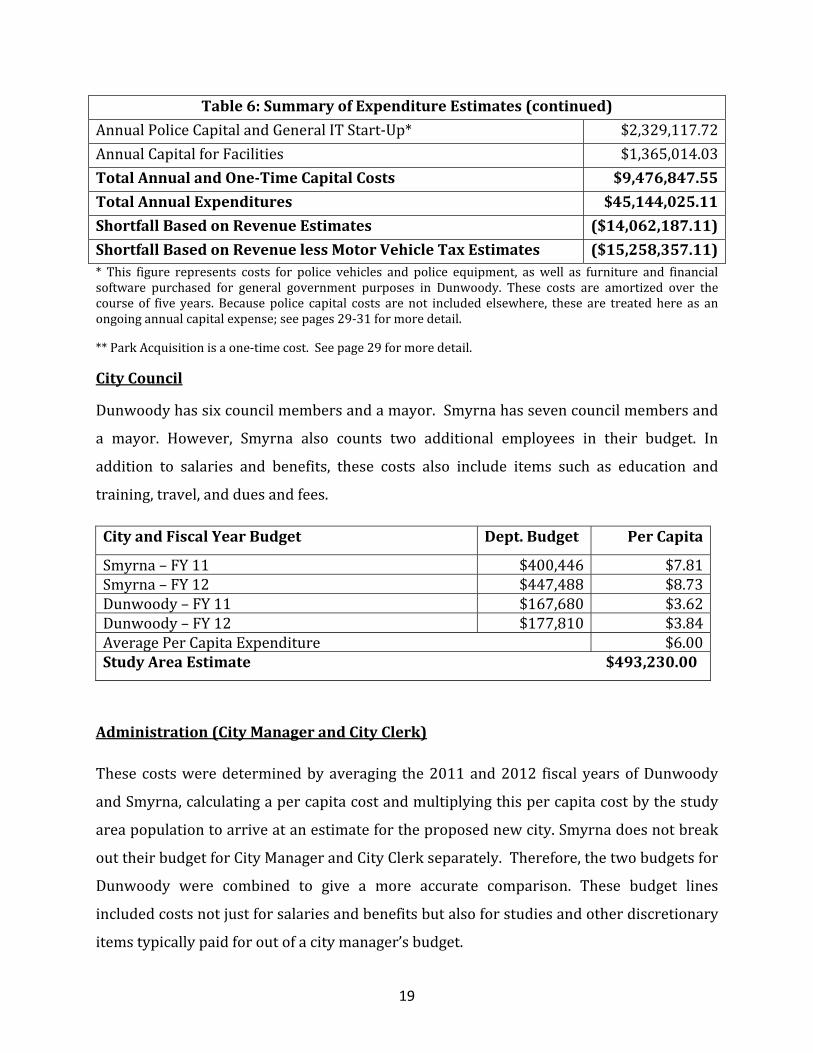

Table6:SummaryofExpenditureEstimates(continued)

AnnualPoliceCapitalandGeneralITStart‐Up* $2,329,117.72

AnnualCapitalforFacilities $1,365,014.03

TotalAnnualandOne‐TimeCapitalCosts $9,476,847.55

TotalAnnualExpenditures $45,144,025.11

ShortfallBasedonRevenueEstimates ($14,062,187.11)

ShortfallBasedonRevenuelessMotorVehicleTaxEstimates ($15,258,357.11)* This figure represents costs for police vehicles and police equipment, aswell as furniture and financialsoftware purchased for general government purposes in Dunwoody. These costs are amortized over thecourse of five years. Because police capital costs arenot included elsewhere, these are treated here as anongoingannualcapitalexpense;seepages29‐31formoredetail.

**ParkAcquisitionisaone‐timecost.Seepage29formoredetail.

CityCouncil

Dunwoodyhassixcouncilmembersandamayor.Smyrnahassevencouncilmembersand

a mayor. However, Smyrna also counts two additional employees in their budget. In

addition to salaries and benefits, these costs also include items such as education and

training,travel,andduesandfees.

CityandFiscalYearBudget Dept.Budget PerCapita

Smyrna–FY11 $400,446 $7.81Smyrna–FY12 $447,488 $8.73Dunwoody–FY11 $167,680 $3.62Dunwoody–FY12 $177,810 $3.84AveragePerCapitaExpenditure $6.00StudyAreaEstimate$493,230.00

Administration(CityManagerandCityClerk)

These costsweredeterminedbyaveraging the2011and2012 fiscal yearsofDunwoody

andSmyrna,calculatingapercapitacostandmultiplyingthispercapitacostbythestudy

areapopulationtoarriveatanestimatefortheproposednewcity.Smyrnadoesnotbreak

outtheirbudgetforCityManagerandCityClerkseparately.Therefore,thetwobudgetsfor

Dunwoody were combined to give a more accurate comparison. These budget lines

includedcostsnotjustforsalariesandbenefitsbutalsoforstudiesandotherdiscretionary

itemstypicallypaidforoutofacitymanager’sbudget.

20

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $550,967 $10.75Smyrna–FY12 $576,560 $11.25Dunwoody–FY11 $378,187 $8.17Dunwoody–FY12 $442,055 $9.55AveragePerCapitaExpenditure $9.93StudyAreaExpenditureEstimate$816,295.65

InformationTechnology

These costsweredeterminedbyaveraging the2011and2012 fiscal yearsofDunwoody

and Smyrna. First year expenses for IT can be expected to be higher than subsequent

years, thusadditionalcapital for ITstartup is included in theGeneralStart‐upportionof

capitalexpenditures,laterinthereport.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $642,654 $12.54Smyrna–FY12 $586,151 $11.43Dunwoody–FY11 $743,696 $16.07Dunwoody–FY12 $561,731 $12.14AveragePerCapitaExpenditure $13.05StudyAreaExpenditureEstimate$1,072,775.25

Marketing

These costsweredeterminedbyaveraging the2011and2012 fiscal yearsofDunwoody

andSmyrna,calculatingapercapitacostandmultiplyingthispercapitacostbythestudy

areapopulationtoarriveatanestimatefortheproposednewcity.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $531,266 $10.36Smyrna–FY12 $549,121 $10.71Dunwoody–FY11 $203,171 $4.39Dunwoody–FY12 $298,907 $6.46AveragePerCapitaExpenditure $7.98StudyAreaExpenditureEstimate$655,995.90

21

GeneralOperations/AdministrativeServices

This figure representsongoingoperational costs.Only the costs fromSmyrnawereused

duetothefactthatDunwoodydoesnotbreakoutthesecostsandtheyaresubsumedinthe

FinancebudgetforDunwoody.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $1,062,156 $20.72Smyrna–FY12 $1,384,332 $27.00AveragePerCapitaExpenditure $23.86StudyAreaExpenditureEstimate$1,961,411.30

Finance

This figure represents all traditional finance functions: accounting, purchasing, contractadministration, risk management, accounting and payroll. Dunwoody was excludedbecausecostscouldnotbeclearlyallocatedtothedepartment.

LegalServices

This figure reflects the per capita average of two fiscal years from both Smyrna and

Dunwoody.Significantlitigationcouldcausethesecoststobehigher,howeverbothcities

experiencedsomelitigationcostsduringthetimeperiodusedtoestimatecosts.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $212,510 $4.15Smyrna–FY12 $200,633 $3.91Dunwoody–FY11 $383,775 $8.29Dunwoody–FY12 $544,098 $11.76AveragePerCapitaExpenditure $7.03StudyAreaExpenditureEstimate$577,901.15

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $640,173 $12.49Smyrna–FY12 $506,611 $9.88AveragePerCapitaExpenditure $11.18StudyAreaExpenditureEstimate$919,051.90

22

HumanResources

This figure reflects the per capita average of two fiscal years from both Smyrna and

Dunwoody.WhiletheHumanResourcesexpensesareassignedtothefinancedepartment

inDunwoody’sbudget,thesecostswereabletobeidentified.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $381,445 $7.44Smyrna–FY12 $358,549 $6.99Dunwoody–FY11 $219,306 $4.74Dunwoody‐FY12 $219,306 $4.74AveragePerCapitaExpenditure $5.98StudyAreaExpenditureEstimate$491,585.90

CommunityDevelopment

This figure includes costs for planning and zoning, building inspections, and code

enforcement.Itrepresentsanaverageoftwofiscalyearsforbothcitiesaveragedpercapita

andappliedtothestudyareapopulation.Dunwoodycontracts fortheseservicesoutand

theDunwoody figures include approximately $1.5million in labor costswhich is higher

thanthecostsacitywouldspendiftheykeptthesefunctionsin‐house,butgivesthemthe

flexibilityofbeingabletobringonpeopleandletthemgo,asneeded.

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $866,261 $16.90Smyrna–FY12 $970,429 $18.93Dunwoody–FY11 $2,099,419 $45.38Dunwoody–FY12 $2,295,250 $49.61AveragePerCapitaExpenditure $32.70StudyAreaExpenditureEstimate$2,688,103.50

MunicipalCourt

This figure represents costs for two fiscal years for each city averaged per capita and

applied to thestudyareapopulation.DunwoodyusesvolunteerBailiffs,generally retired

LawEnforcementOfficers,tohelpkeeptheircostslow.

23

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $513,566 $10.02Smyrna–FY12 $507,318 $9.90Dunwoody–FY11 $258,518 $5.59Dunwoody–FY12 $332,862 $7.19AveragePerCapitaExpenditure $8.17StudyAreaExpenditureEstimate$671,614.85

SubtotalofOverallAdministrativeCosts

Togiveanideaofthebudgetforoveralladministrativecostsforalltheabove‐mentioned

categories,asubtotalisprovided.ThesecostsincludethecostsinDunwoodywhichwere

notabletobeallocatedtoFinanceandGeneralOperations.

CityandFiscalYearBudget Dept.BudgetSmyrna–FY11 $7,030,319Smyrna–FY12 $7,313,997Dunwoody–FY11 $6,074,648Dunwoody–FY12 $7,550,795StudyAreaExpenditureEstimate$10,347,965.40

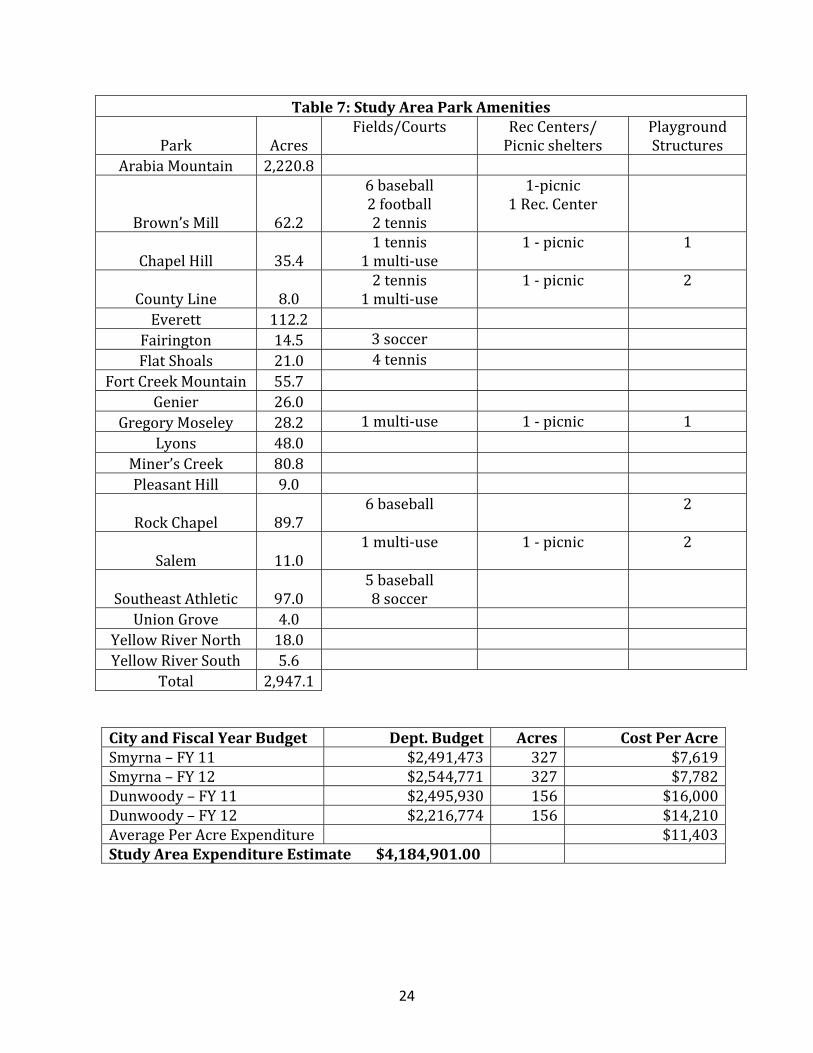

Parks

Inordertocalculateanexpenditureestimateforparkmaintenance,CVIOGcalculatedthe

peracreexpendituremadebythecomparisoncitiesandappliedthisamountto thepark

acreage in thestudyarea.Neitherof thecomparisoncitiesmaintainsa robust recreation

program, relying instead on non‐profits to serve this function, it was assumed a city

comprisedofthestudyareawouldoperatesimilarly.

The study area contains 19 parks that are currently located in unincorporated DeKalb

County. These parks, alongwith amenities, are listed in Table 7. Ten of these parks are

areas which consist primarily of unimproved land or whose only amenities are nature

trails.Thisincludesthe2,000+acreArabiaMountainParkinthesouthernpartofthestudy

area. It was assumed thatmaintenance and operating costs associatedwith passive use

parksarenegligible.Atotalof367acreswereassociatedwithimproved(i.e.non‐passive

use)parksandwereusedasabasisforcalculatingparkmaintenanceexpenses.

24

Table7:StudyAreaParkAmenities

Park AcresFields/Courts RecCenters/

PicnicsheltersPlaygroundStructures

ArabiaMountain 2,220.8

Brown’sMill 62.2

6baseball2football2tennis

1‐picnic1Rec.Center

ChapelHill 35.41tennis

1multi‐use1‐picnic 1

CountyLine 8.02tennis

1multi‐use1‐picnic 2

Everett 112.2 Fairington 14.5 3soccer FlatShoals 21.0 4tennis

FortCreekMountain 55.7 Genier 26.0

GregoryMoseley 28.2 1multi‐use 1‐picnic 1Lyons 48.0

Miner’sCreek 80.8 PleasantHill 9.0

RockChapel 89.76baseball

2

Salem 11.01multi‐use

1‐picnic 2

SoutheastAthletic 97.05baseball8soccer

UnionGrove 4.0 YellowRiverNorth 18.0 YellowRiverSouth 5.6

Total 2,947.1

CityandFiscalYearBudget Dept.Budget Acres CostPerAcreSmyrna–FY11 $2,491,473 327 $7,619Smyrna–FY12 $2,544,771 327 $7,782Dunwoody–FY11 $2,495,930 156 $16,000Dunwoody–FY12 $2,216,774 156 $14,210AveragePerAcreExpenditure $11,403StudyAreaExpenditureEstimate$4,184,901.00

25

Police

Given that police expenditures are such an important part of a city’s budget, the

expenditureswereanalyzedintwodifferentwaystogivethebestestimatepossible.

Inthefirstanalysis,policeoperationalexpendituresforthetwomostrecentfiscalyearsof

SmyrnaandDunwoodywereutilized. To calculate thenumberof officersneeded in the

studyarea,thenumberofofficerspercapitawascalculated.

City PopulationOfficers Personsper

OfficerSmyrna 51,265 91 563Dunwoody 46,267 46 1005

AveragePersonsperOfficer 785StudyArea 82,205 StudyAreaOfficers105

Then the average expense per officer was calculated for Smyrna and Dunwoody. This

averageexpenditurewasappliedtothecalculatednumberofofficersforthestudyareato

arriveatthetotaloperationalexpensesforPoliceinthestudyarea.

CityandFiscalYearBudget Dept.Budget Officers PerOfficerSmyrna–FY11 $8,146,213 91 $80,655.57Smyrna–FY12 $8,084,720 91 $80,046.73Dunwoody–FY11 $5,450,444 46 $118,487.91Dunwoody–FY12 $4,900,735 46 $106,537.72AveragePerOfficerExpenditure $96,431.98 StudyAreaExpenditureEstimate$10,125,357.90

No jail costs are included in this figure, as it was assumed that a new city would not

maintainitsownjailandthatitwouldenjoyasimilararrangementwiththeDeKalbCounty

SheriffasdoesDunwoody.InDunwoody,a10%fineadd‐oniscollectedoncasesthatgoto

municipal court and sent to the county to pay for housing needs for any municipal

prisoners. Municipal prisoners would only be those awaiting adjudication or serving a

sentenceimposedbythecity’smunicipalcourt.Itisworthyofnotethatwithinthesecosts,

26

Dunwoody contributes one person to a cooperative intergovernmental SWAT team, and

employsonefull‐timenarcoticsperson.10

As an alternative to this methodology, the Institute of Government faculty acquired a

datasetofE‐9‐1‐1callsforlawenforcementservicesincalendaryear2012fromtheE‐9‐1‐

1unit of theDeKalbCountyPoliceDepartment.Therewere573,457 calls for service. A

randomnumber generatorwas used to create a random sample of 2,418 addresses. Of

these,2,037weremappedandthenumberofthesewithinthestudyareaidentified.

TotalAnnualServiceCalls 573,547RandomSample 2037CallswithintheStudyArea 269PercentofsampleinStudyArea 13.21%EstimatedAnnualCallsinStudyArea 75,729

The InternationalAssociation of Chiefs of Police (IACP) estimates that, in the absenceof

actualcomplaintcounts,550complaintsorincidentswilloccurforevery1,000residents,

or.55perresident.Usingthisassumption,thestudyareawouldexperience45,213calls.

TotalPopulation 82,205CallsperResident 0.55EstimatedAnnualCallsinStudyArea 45,213

Based on information from the IACP, the national average of time per incident is

approximately45minutes.Further,theIACPindicatesthereisaPoliceActivityWeighting

Scalethatshouldbeappliedtothetimeestimatetoaccountforthetimeneededtohandle

callsinvolvingmoreseriouscrimes.Thus,thecallswereincreasedby25%toaccountfor

thisweighting.

Also,accordingtostudiesconductedbytheIACP,onethirdofanofficer’s timeshouldbe

spenthandlingcalls forservice,onethirdonpreventativepatrol,andtheotheronethird

usedasabuffertimeforaneffectiveandefficientpatrolforce.Inadditiontorespondingto

10 DeKalb Countymaintains use of a police helicopter and other specialized resources thatmight only beavailabletothecityonacostorintergovernmentalagreementbasisuponincorporation.

27

callsforservice,themethodologyalsoaccountsforthetimedemandplacedonofficersas

theyarrestandbookallegedsuspectswithgreaterweightgiventoarrestsformoreserious

crime.11

The number of hours necessary to staff one basic one‐officer patrol unit for one year is

2,920.Thisequatesto8hoursadayfor365days.Sincenooneworkseverysingleday,a

relieffactorwasusedaccountfordaysanofficerwouldbeunavailableduetothingssuch

asdaysoff,sickdays,vacationday,trainingdaysandcourtdays.Thisrelieffactoris1.84.

ItisbasedonareviewofpolicedepartmentpersonnelbenefitsconductedbytheIACP.

Finally, thenumberwas adjusted to account for lawenforcementofficers in supervisory

roles.Thisnumberofofficerswasmultipliedtheperofficerexpenditurescalculatedfrom

theactualsinSmyrnaandDunwoody.

TheWorkloadAnalysisyieldsanumberofofficersconsistentwiththenumberanticipated

usingtheratioofofficerstopopulationmethodologyabove.

WorkloadAnalysis

Analysisassuming.55

callsperResidentAnalysisbasedon

E‐9‐1‐1dataAnnualCalls 75,729 75,729Weightedformoretimeconsumingcalls 94,661 94,661Multipliedby.75ofanhour 47,331 70,996Multipliedby3toaccountfor1/3oftimespentoncalls 141,991.5 212,987.3Dividedby2920toconverttoOfficers 48.6 72.9Multipliedby1.84toaccountfordaysoff 89.5 134.2Inflatedby10%forsupervisors 98.4 147.6Multipliedby$96,431.98/officerStudyAreaExpenditureEstimate

$9,490,980.65 $14,236,470.96

*This figurewasderived froma series of intermediate calculationswhose inputswerenot roundedaftereachindividualstepandwillthereforedifferslightlyfromaresultbasedontheroundedfiguresshowninthetable.

To ensure that police expenditures were not underestimated, the amount of

$14,236,470.97wasusedintheanalysis.Thisisthelargestestimatedpoliceexpense,and

thereforethemostconservativeestimateofpoliceexpenditures.

11http://www.theiacp.org/LinkClick.aspx?fileticket=AKL78d4MBw8%3d&tabid=252

28

PublicWorks

Toestimatecostsforpublicworks,whichwouldprimarilyberoadandbridgerepairand

maintenance,weobtainedthenumberof localroad lanemileswithin thestudyareaand

forthecitiesofDunwoodyandSmyrnathroughuseofGISmappingtechnology.Fiscalyear

expenditures for2011and2012 forbothcitieswerecalculatedper lanemile12and then

averaged.Thatamountwasmultipliedagainstthenumberoflanemilesinthestudyarea.

Dunwoody

CityandFiscalYearBudget Dept.Budget LaneMiles CostperLaneMileSmyrna–FY11 $2,959,416 450 $6,576.48Smyrna–FY12 $2,902,315 450 $6,449.59Dunwoody–FY11 $2,055,155 272.80 $7,533.56Dunwoody–FY12 $1,048,009 272.80 $3,841.68AverageCostPerLaneMile $6,100.33NumberofLaneMilesinstudyarea 336.1StudyAreaExpenditureEstimate$2,050,319.53 StormWater,StreetLightsandSpeedBumps

Stormwaterutilities, street lights, andspeedbumpsareenterprise fundsdesigned tobe

fundedbyafeestructurethatapproximatestheircost.Thus,theestimatedrevenuefigure

for Storm Water, Street Lights, and Speed Bumps has been used as the estimated

expenditureamount.

Tourism

Becauseaportionofthehotel/moteltaxisdedicatedtobespentontourismbystatelaw,

manyjurisdictionstendtousethatportionofthetaxfortheirtourismbudget. Similarly,

theestimatedrevenuefigureforhotel/moteltaxesrestrictedtotourismhasbeenusedas

theestimatedexpenditureamount.

ContingencyFund

These are funds used by cities to cover unforeseen expenditures. Dunwoody has never

useditsContingencyFund.

12GDOTtotallanemileage,2009form499.(Thisassumesthatacitywouldmaintainall“county”roads.)

29

CityandFiscalYearBudget Dept.Budget PerCapitaSmyrna–FY11 $885,598 $17.27Smyrna–FY12 $750,000 $14.63Dunwoody–FY11 $575,000 $12.43Dunwoody–FY12 $575,000 $12.43AveragePerCapitaExpenditure $14.19StudyAreaExpenditureEstimate$1,166,488.95

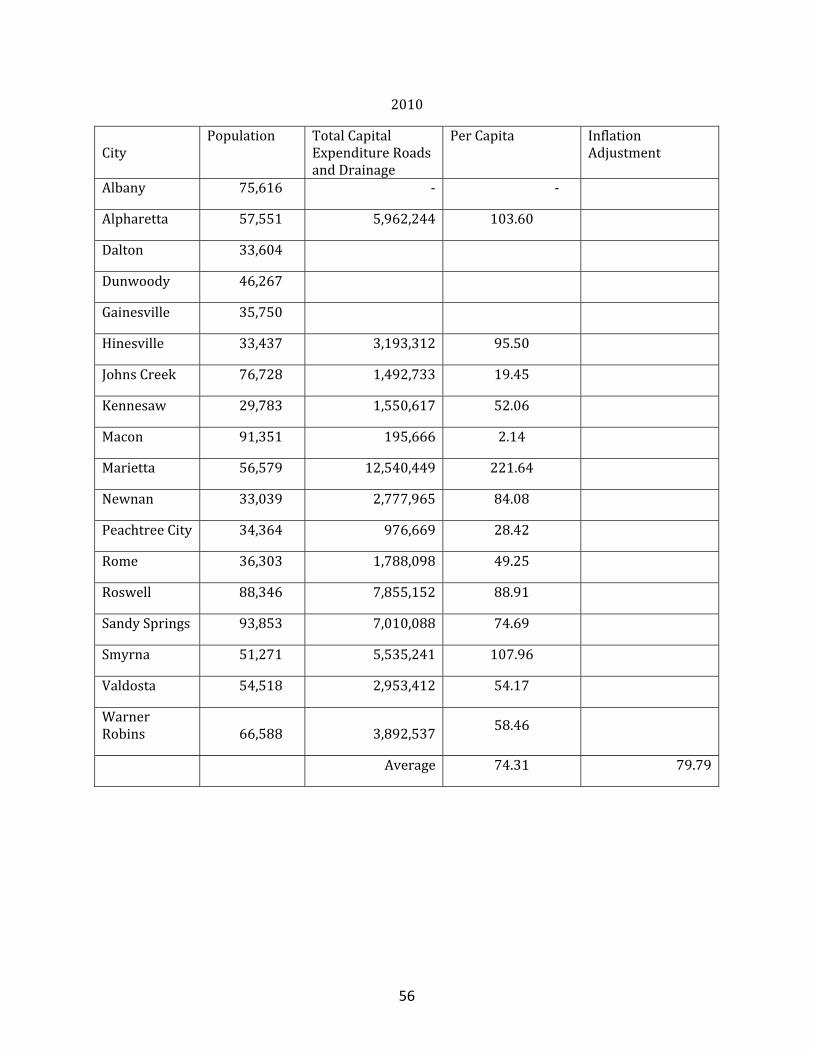

AnnualCapitalforRoadsandDrainage

These costs represent the on‐going capital costs associated withmaintaining roads and

accompanying drainage; i.e., land, equipment, as well as repairs and alterations to fixed

works.Todetermine this figure, capitalexpenditures for roadsanddrainage reported to

the Georgia Department of Community Affairs by 19 cities ranging in population from

31,000 to 92,000 for 2007 ‐2011were averaged per capita. These numberswere then

adjusted for inflation to2013dollarvalues,andthepercapitaaverageof thosenumbers

wasthenappliedagainstthestudyarea’spopulation.SeeAppendixH.Thisfigureexcludes

costs for capital associatedwith services thatwill continue to bemaintained by DeKalb

Countygovernmentlikelibrariesandfirestations,aswellascapitalcostsassociatedwith

city functions assumed to be covered through operational costs. Capital needs for police

services were also excluded from this number as they are accounted for separately as

policecapital.

AnnualCapitalforParkAcquisition

Tothefigureforannualcapitalwasaddedthecostforanewlyincorporatedcitytoacquire

the parks fromDeKalb County as determined by the number of acres and the statutory

formula set forth inO.C.G.A. §36‐31‐11.1,which is$294,710.This statutewaspassed to

resolve an impasse between Dunwoody and DeKalb County, over the costs of park

acquisition,andbyvirtueofitswordingwouldapplyifthestudyareawereincorporated.13

13DCAdatadoesnotsegregatelandacquisitioncostsfromotherparks‐relatedcapitalcosts,consequentlyonlythestatutorily‐derivedparksacquisitioncostfigurewasused.

30

PoliceCapitalandGeneralStart‐Up

Thesecostsrepresentthoseassociatedwithequippingacitypolicedepartmentaswellas

some general non‐police specific city‐wide start‐up costs. Most of these represent costs

associatedwithbeginningtheoperationofapolicedepartmentduetothelargeamountof

equipmentandvehiclesneededtoprovidepoliceservices.Forpurposesofcalculatingthis

figure,itwasassumed,basedontherecentexperiencesofDunwoody,thatlease‐purchase

agreementswould be used to acquire the needed vehicles and equipment pursuant to a

five‐yearleaseataninterestrateof2.25%.14Toarriveatthesecosts,itwasassumedthat

therewouldbe148policeofficersinastudyareacitydepartment,basedontheworkload

analysismethodology.

ComparisonofResidentPopulationtoNumberofPoliceOfficers

Dunwoody Smyrna StudyArea

2010Population 46,267 51,265 82,205

No.ofPoliceOfficers 46 91 148

ResidentsperOfficer 1006 563 555

The total costs of equipping each Dunwoody officerwith a vehicle, computer, furniture,

radio, firearmandotherbasicequipmentwasdeterminedpercapitaandappliedagainst

thenumberofofficersassumedforthestudyareabasedontheWorkloadAnalysistoarrive

atatotalofficerpolicecapitalcostestimate.

14Theuseof2.25%interestratewasbasedondiscussionwiththeGeorgiaMunicipalAssociation.

Averagenumberofresidentsperofficer 784.5

No.ofofficersonapercapitabasis 105

No.ofofficersbasedonWorkloadAnalysis 98(lowest.)–148(highest.)

CityandFiscalYearBudget Budget CostPerOfficerDunwoody‐FY09PoliceStart‐up $2,674,000 $58,130

InflationAdjustedCostperOfficer $63,444NumberofOfficersAssumedforstudyarea=148x$63,444perofficerStudyAreaExpenditureEstimate $9,389,712.00

31

Inadditiontocapitalexpenditures forpolice,anewcitywould likely incursomegeneral

start‐up costs. Dunwoody’s start‐up costs included expenditures for furniture and

software.

CityandFiscalYearBudget Budget PerCapitaDunwoody‐FY09Non‐policeStart‐up $778,000 $16.82InflationAdjustedPerCapitaExpense $18.36StudyAreaExpenditureEstimate $1,502,283.80

Police capital costs andgeneral start‐up costs figuredper capita for the studyareawere

addedtogetherandassumedtobefinancedoverafiveyeartermonsimilartermstothose

usedbyDunwoodytofinancethesesameexpenses.

FacilityLeases

Itisassumedthatthestudyareawillleaseitsfacilities.Toestimatetheexpensethestudy

areawouldincurtoleasefacilityspace,theissuewasanalyzedacoupleofdifferentways.

Dunwoodyleasesthespacethathousestheircityhallandpolicedepartments.Theamount

ofleasedspacepercapitainDunwoodywasusedtocalculatethesquarefootageofleased

spacethatthestudyareacouldexpecttoneedtolease.

CityandFiscalYearBudget LeasedSpaceSq.Ft. PerCapitaSq.Ft.Dunwoody‐FY12 24,785 .54PopulationofStudyAreaStudyAreaEstimateofSquareFootageNeeded 44,391

PoliceCapitalStart‐UpEstimate $9,389,712.00

GeneralStart‐UpCostEstimate $1,509,283.80

TotalStart‐upCostEstimate $10,898,995.80

Amortizedover5yearsat2.25%interest $2,329,117.72

32

Information fromthe2012calendaryearactuals spenton leaseexpensesdividedby the

total leased space in Dunwoody yielded an expense per square foot. This was applied

againsttheestimatedamountofsquarefootageforthestudyarea.

CityandFiscalYearBudget Dept.Budget PerSq.Ft.Dunwoody‐CY12 $422,004 $17.03StudyAreaExpenditureEstimate $755,973.62

Alternatively,thenumberofemployeesinSmyrnawhowereemployedinsimilarfunctions

asthosethestudyareawouldrequire,wascalculatedonapercapitabasis.Thiswasthen

appliedtothepopulationofthestudyareatodeterminethenumberofemployeesneeded

inacitythesizeofthestudyarea.Theamountofsquarefootageperemployeewasthen

calculated.Thiswasdoneforboth125squarefeetperemployeeand225squarefeetper

employee. A surveyof theasking rent for lease space in the studyarea showeda range

withmanyoftheavailableofficebuildingsrunningbetween$14and$18persquarefoot

peryear.

FacilityLeasesNo.ofemployeespercapita .0041Studyareapopulation 82,205Employeesneeded [email protected]./employee 42,[email protected]./employee 75,834

Squarefootage Pricepersq.ft. TotalLeaseExpenseLowend: 42,130 $14.00/sq.ft. $589,821Highend: 75,834 $18.00/sq.ft. $1,365,014.03

Thesummaryanalysisusesthemostexpensiveleaseestimateinordertobeconservative.

Thisnumberwouldincludeallmaintenancecosts,giventhatitisveryconservative.

Appendix A

33

34

AppendixB

MiscellaneousRevenues

The following table provides greater detail for the revenue sources which

individuallyarefairlysmall.

RevenueSource

Methodology StudyAreaEstimate

DataSource

UtilityTaxes

Ratioofassessedvalueofutilitypropertyinstudyareatounincorporatedarea

$0.00

DeKalbRevenueReportbyFundyearthrough

December2012(Unincorporated)

HeavyEquipmentTaxes

Ratioofassessedvalueofindustrialpropertyinstudy

areatoDeKalbunincorporatedarea $43.13

DeKalbRevenueReportbyFundyearthrough

December2012(Unincorporated)

FingerprintingFees

RatioofpopulationinstudyareatoDeKalbunincorporated

area$2,656.87

DeKalbRevenueReportbyFundyearthrough

December2012(Unincorporated)

CopyingFees

RatioofpopulationinstudyareatoentireCounty

$240.91

DeKalbRevenueReportbyFundyearthrough

December2012(Unincorporated)

MotorVehicles–Penalties

Ratioofpenaltiespaidforpropertytaxestoproperty

taxespaidinstudyareatimestotalmotorvehiclestaxes $19,138.72

DeKalbTaxCommissioner

QualifyingFees

3%ofgrossannualsalary/electedofficial

$14,796.90

PursuanttoO.C.G.A.§21‐2‐131

InvestmentIncome

RatioofPopulationinstudyareatounincorporatedarea

$0.00

DeKalbRevenueReportbyFundyearthrough

December2012(Unincorporated)

TotalMiscellaneous $36,876.52

35

UtilityTaxes

Propertyownedbypublicutilitiesisassessedbythestateandalocalmillagerateisapplied

tothatassessment.

HeavyEquipmentTaxes

Taxesareassessedoncertainheavyequipmenttypicallyusedinindustrialenvironments.

Anassumptionwasmadethattheassessedvalueofindustrialpropertyservesasaproxy

for thepresenceof suchequipment.Theratioofassessedvalueof industrialproperty to

the assessed value of industrial property in the unincorporated areawas applied to the

revenuegeneratedfromheavyequipmenttaxesintheunincorporatedarea.

FingerprintingFees

This figurerepresentsrevenuederived fromfeescharged formaking fingerprint sets for

licenseapplicants to those requesting themforprofessional licenseapplicationsorother

reasons.Theratioofpopulationofthestudyareatotheunincorporatedareawasusedto

determinethisamount.

CopyingFees

Governments are allowed to charge small fees per page for copies of documents. Itwas

assumedthataproportionateamountofrequestswouldbemadeofacitycomprisedofthe

studyarea.Here,theavailabledataforcopyingfeesrepresentedfeescollectedonacounty‐

widebasis,sotheratioofpopulationofthestudyareatotheentirecountypopulationwas

used.

MotorVehicles–Penalties

Thisfigurewasobtainedbyapplyingtheratioofpenaltiespaidforrealpropertytaxesto

realproperty taxespaid in thestudyarea times theanticipatedamountofmotorvehicle

taxes. An assumption was made that the ratio of taxpayers that incurred penalties for

failuretotimelypayrealpropertytaxeswouldbethesameformotorvehicletaxes.

36

QualifyingFees

Statelaw,O.C.G.A.§21‐2‐131providesthatmunicipalitiescollectqualifyingfeesforthose

seeking elected office at a rate of 3% of gross annual salary for the elected office being

sought. C4ND asked for an assumption to bemade that this figure be calculated for one

mayorandsixcouncilmembers.Thus,thisfigurewasobtainedbyaveragingthesalariesof

theelectedofficialsinDunwoodyandSmyrna(eachofwhichhavesixcouncilmembersand

onemayor)andthenmultiplyingthataveragedamountbythreepercent.

InvestmentIncome

Normally local governments are able to derive some revenue from interest obtained on

investmentsof fundstypicallymadefor limitedperiodsoftime.Astherewasnorevenue

fromsuch investments in the2012actual revenuedata fromDeKalbCounty,wedidnot

estimateafigure.

37

AppendixC

2012UnincorporatedCountyRevenueFiguresandDataSources

RevenueSource UnincorporatedCounty

RevenueFigure

DataSource

OccupationTaxes 15,207,787 ActualsforCY2012

BeverageExciseTaxes

4,046,370 DeKalbRevenueReportbyFundyearthroughDecember2012

PersonalPropertyTaxes

3,927,373 DeKalbRevenueReportbyFundyearthroughDecember2012

Hotel/MotelTax/

2,788,067 DeKalb2012BudgetBook

Hotel/MotelTax(restricted)

1,858,712 DeKalb2012BudgetBook

BusinessLicense‐Police

1,048,746 DeKalbRevenueReportbyFundyearthroughDecember2012

BusinessLicense‐Beverages

1,266,125 DeKalbRevenueReportbyFundyearthroughDecember2012

BankSharesTax

820,676 DeKalbRevenueReportbyFundyearthroughDecember2012

Intangible

787,909 DeKalbRevenueReportbyFundyearthroughDecember2012

DevelopmentFund4,671,149 DeKalb2012BudgetBook

RevenuefromPermitFees

ZoningandVarianceFeesandPermits

101,751 DeKalbRevenueReportbyFundyearthroughDecember2012

InsurancePremiums

25,059,141 DeKalbRevenueReportbyFundyearthroughDecember2012

Fines&Forfeitures

22,567,688 DeKalbRevenueReportbyFundyearthroughDecember2012

MotorVehicles

7,444,602 DeKalbRevenueReportbyFundyearthroughDecember2012

38

RevenueSource UnincorporatedCounty

RevenueFigure

DataSource

LawEnforcement‐ConfiscatedMoniesFund

1,749,092 DeKalb2012BudgetBook

SaleofPrintedMaterial‐Police

273,440 DeKalbRevenueReportbyFundyearthroughDecember2012

39

AppendixD

HotelsintheStudyArea

1. Microtel Inn and Suites by Wyndham

2980 Evans Mill Rd. Lithonia, GA 30058

2. Fairfield Inns and Suites – Atlanta East

7850 Stonecrest Square Lithonia, GA 30038

3. Hyatt Place – Atlanta East

7900 Mall Ring Road Lithonia, GA 30038

4. Hilton Garden Inn

7890 Mall Ring Road Lithonia, Georgia 30038

5. Economy Lodge

6707 Milwood Lane Lithonia Georgia, 30038

6. Red Roof Inn – Lithonia

5400 Fairington Road Lithonia, GA 30038

7. Super 8 Motel – Decatur

5354 Snapfinger Park Drive Decatur, Georgia 30035

8. Quality Inn and Suites – Decatur

5300 Snapfinger Park Drive Decatur, Georgia 30035

9. Holiday Inn Express and Suites

7846 Stonecrest Square Lithonia, Georgia 3038

Georgia Department of Revenue

Title Ad Valorem Tax Fee

Local Distribution Guidance

October 30, 2013

Summary

Georgia code section 48-5C-1(c)(3) provides for a two-step distribution of Local Title Ad Valorem

Tax Fee (“TAVT”) proceeds on a monthly basis. Over time, as annual ad valorem taxes phase out,

the first step distribution will gradually increase, eventually comprising the majority of motor vehicle

property taxes.

Under the statutory structure, cities formed on or after January 1, 2013 will not receive a first step

distribution. Further, cities formed during 2012 will not receive first step distributions for months

during which no annual ad valorem tax was collected by such cities in 2012.

Shift from Annual Ad Valorem Tax to TAVT

Motor vehicles purchased and titled in Georgia prior to March 1, 2013 are generally subject to annual

ad valorem taxes pursuant to Chapter 5 of Title 48.1 Vehicles purchased on or after March 1, 2013 are

subject to TAVT and are exempt from annual ad valorem tax. Thus, as Georgia taxpayers purchase

new motor vehicles, the annual ad valorem tax revenue collected will decrease gradually each year.

Collection of Annual Ad Valorem Tax and Distribution of TAVT

In the initial years of TAVT, a significant percentage of motor vehicle tax revenue will still derive

from annual ad valorem taxes. Accordingly, it is important to note that both taxes are in effect and

funding local governments at this time. But, because people trade-in or otherwise dispose of their

“annual ad valorem tax vehicles” in exchange for a “TAVT vehicle,” the total amount of annual ad

valorem tax collected by counties and cities will steadily decrease each year.

The first step distribution of TAVT proceeds, distributed on a monthly basis, is designed to offset the

reduction in annual ad valorem taxes collected in subsequent years. This reduction offset amount is

calculated by comparing the 2012 annual ad valorem taxes collected in a given month to the amount

collected in the same month of the current year.2 In other words, the first step distribution is designed

to ensure that a city (or county) is made whole as to the annual ad valorem tax it collected in 2012.

The first step distribution, referred to above as the “reduction offset amount,” is made to four

subcategories within a jurisdiction: (1) the county governing authority, (2) the cities, (3) the county

1 Vehicles purchased between January 1, 2012 and February 28, 2013 are eligible to “opt-in,” in which case those

vehicles are exempt from annual ad valorem tax. O.C.G.A. § 48-5C-1(b)(1)(A). 2 O.C.G.A. § 48-5C-1(c)(3)(A)

Appendix E

40

Page 2 of 2

board of education, and (4) the independent school districts (“Distributees”).3 The second and fourth

distributee categories could have multiple distribution sources because more than one city or

independent school district may exist within a particular county.

The Issue

For a “new” city which collected no annual ad valorem tax in a given month during 2012, there is no

figure or record available upon which to compare subsequent year annual ad valorem tax revenue.

Thus, the reduction offset amount will always be zero, and the first step distribution to such “new” city

will also be zero.

This issue could also affect a city formed during 2012. For example, a city formed in July of 2012

would not have a record of annual ad valorem taxes collected in January through June of 2012. Thus,

no reduction offset amount could be determined for January through June of subsequent years, and

such city would not receive a first step distribution of local TAVT proceeds in those months of future

years.

First Step Distribution Shortfall4

Compounding this issue is the circumstance where the TAVT proceeds available in a current month

are insufficient to fully offset the reduction in annual ad valorem tax proceeds made to the eligible

distributees during the first step distribution.

In this case, a pro rata allocation is made to the eligible distributees. The remaining deficit from the

first step distribution is carried over to the next month. In that next month, the TAVT proceeds are

first used to satisfy the prior month deficit. Only after satisfying the prior month deficit is the next

month’s first step distribution made. Accordingly, in the case of a first step distribution shortfall,

cities formed after January 1, 2013 will not receive any TAVT revenue for that month.

The Second Step Distribution5

The second step distribution is made only if local TAVT proceeds remain after making the first step

distribution. All distributees would be eligible to receive funds, if any remain, in the second step

distribution. The distribution methodology for the second step distribution is set by statute.6

Conclusion

Under the statutory structure of O.C.G.A. § 48-5C-1(c)(3)(A), cities formed on or after January 1,

2013 will not receive a first step distribution. Further, cities formed during 2012 will not receive first

step distributions for months during which no annual ad valorem tax was collected by such cities in

2012.

3 O.C.G.A. § 48-5C-1(c)(3)(A)

4 Id.

5 O.C.G.A. § 48-5C-1(c)(3)(B)

6 See Id.

41

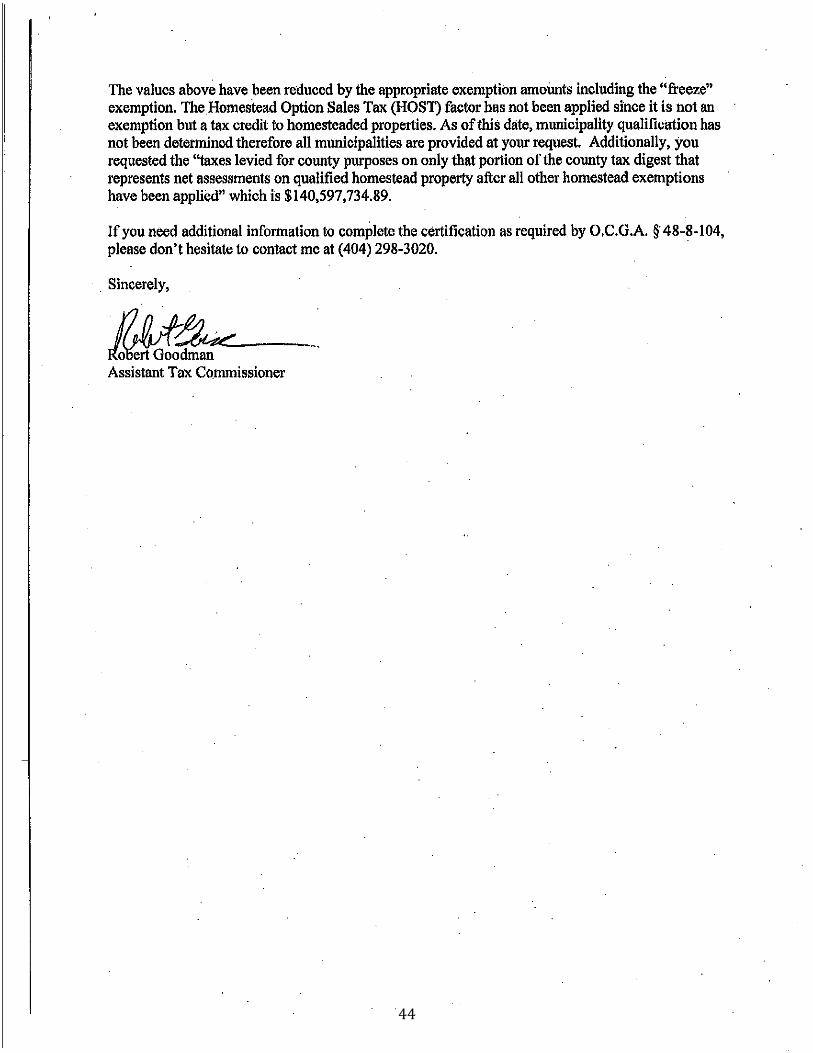

Appendix F HOST Calculations and County Certification Letter

42

43

44

45

46

47

Example from 48-8-104(2) For illustration purposes, a hypothetical example of the (3) In the event the total amount payable in a calendar year to all existing municipalitiescalculation of the equalization amount is provided below. Calculated using Dekalb/Dunwoody as certified by the county pursuant to subparagraph (d)(2)(B) of this Code section plus

Example Example data Actual Calculation the total equalization amount payable to all qualified municipalities in the special district First, calculate the exceeds the capital outlay proceeds calculated based on a maximum capital factor of 0.200, homestead factor in the commissioner shall pay to the governing authority of each qualified municipality a shareaccordance with division of such proceeds calculated as follows:(c)(2)(B)(i) of this Code Amount from county certification letter (A) above plus Equalization amount (J) from left 11,791,776.99$ section as follows: Does this amount exceed Capital outlay proceeds (A) below? NO(A) Capital factor 0.150 0.150 0.200 If yes, continue calculation below. If no, go to (5) belowcertified by county asrequired by subsection (d) (A) Determine the capital outlay proceeds based on a maximum capital factor of 0.200;of this Code section Capital outlay proceeds = Capital factor (A) times Net Sales & Use tax (B) from left 21,661,937.98$ (B) Net amount of sales and $50 million 50,000,000.00$ 108,309,689.91$ (B) Subtract the amount certified by the county as payable to existing municipalities pursuantuse tax collected in the to subparagraph (d)(2)(B) of this Code section;special district pursuant Amount from county certification letter: $0.00to this article for the (C) The remaining amount equals the portion of the capital outlay proceeds that may be usedprevious calendar year (2009) by the commissioner to pay equalization amounts to qualified municipalities. (C) Taxes levied for county $100 million 100,000,000.00$ 140,597,734.89$ Total: 21,661,937.98$ purposes on only that The commissioner shall calculate each qualified municipality's share of such remaining amountportion of the county tax by dividing the net homestead digest for each qualified municipality by the total homesteaddigest that represents net digest for all municipalities.assessments on qualified Net Homestead Digest for municipality from Certification letter: 482,567,151.00$ homestead property after Total Homestead Digest for all municipalities: 7,681,520,997.00$ all other homestead Divide Net Homestead Digest by Total Homestead Digest: 6%exemptions have been applied(D) Calculation of 0.425 0.425 0.616 Total (C) above times calculated percentage above 1,360,842.43$ homestead factor usingfigures above = [(1-0.150)($50 (4) In the event the incorporated county millage rate for a qualified municipality is greater than million/$100 million)] the unincorporated county millage rate, no payment shall be due from the governing authorityNext, calculate the 15.0 mills of the qualified municipality to the governing authority of the county.equalization amount inaccordance with paragraph (1) of this subsection as follows: (5) In the event the amount of capital outlay proceeds exceeds the sum of the equalization (E) Unincorporated county 15.0 mills 15.00 19.29 mills amounts due all qualified municipalities plus the total amount certified under subparagraph (d)(2)(B)millage rate of this Code section as due all existing municipalities, the commissioner shall distribute to each (F)Minus the incorporated Difference: (10.0 mills) (10.00) (14.33) mills qualified municipality a portion of such excess equal to the net homestead digest for such county millage rate for municipality divided by the total homestead digest.qualified municipality "Y" Capital outlay proceeds = Capital factor (A) times Net Sales & Use tax (B) from left 21,661,937.98$ Difference: = 5.0 mills 5.00 4.96 mills Amount from county certification letter (A) above plus Equalization amount (J) from left 11,791,776.99$ (G) Times homestead factor x .425 0.425 x 0.616 Does amount of Capital outlay proceeds exceed amount from (3) above? YES(calculated above) If yes, continue calculation below. If no, go back to (3) above(H) Equals the equalization = 2.125 2.125 3.057 millsmillage: Amount of excess = Capital outlay proceeds minus amount from (3) above 9,870,160.99$ (I) Times net homestead $200 million 200,000,000.00$ 482,567,151.00$ digest for qualified Net Homestead Digest for municipality from Certification letter: 482,567,151.00$ municipality "Y" Total Homestead Digest for county: 7,681,520,997.00$ (J) Equals the equalization $425,000 $425,000.00 1,475,089.62$ Divide Net Homestead Digest by Total Homestead Digest: 6%amount payable to municipality "Y" Total (C) above times calculated percentage above 620,061.50$

6 equal payments of (J) above: 245,848.27$

48

49

AppendixG

CDBGDataTables

DataSourceGeorgiaDepartmentofCommunityAffairsCDBGAwards

PopulationfiguresreflectU.S.CensusBureauAnnualEstimates

2008 City Pop Total Per

capitaInflationAdjustment

Kennesaw 31628 134556 4.25 Milton 0 Newnan 30474 0 Douglasville 31035 34423 1.11 Dalton 33648 237200 8.12 Hinesville Gainesville 35668 893716 25.06 P'treeCity 34788 0 Rome 36041 29710 .82 Dunwoody X Smyrna 49854 325723 6.53 Valdosta 48547 0 Marietta 67562 162685 2.41 Alpharetta 49903 0 WarnerRobins 61336 612724 9.99 JohnsCreek 59431 0 Albany 75831 2532219 33.39 Roswell 87657 619813 7.07 Macon 92775 0 SandySprings 82674 0 Average 6.99 7.43

2009 City Pop Total Per

capitaInflationAdjustment

Kennesaw 33043 126967 3.84

50

Milton Newnan 31587 0 Douglasville 31534 2125 0.07 Dalton 33604 560721 16.69 Hinesville 30705 552306 17.99 Gainesville 35750 207692 5.81 P'treeCity 34784 0 Rome 36031 3900 0.11 Dunwoody 40746 0 Smyrna 50712 670401 13.22 Valdosta 52087 0 Marietta 66953 172303 2.57 Alpharetta 51569 0 WarnerRobins 62500 532237 8.52 JohnsCreek 61794 0 Albany 75616 1013228 13.40 Roswell 87719 1312718 14.97 Macon 92582 0 SandySprings 85625 0 Average 5.18 5.53

2010 City Pop Total Per

capitaInflationAdjustment

Kennesaw 29783 163254 5.48 Milton Newnan 33039 1827754 55.32 Douglasville 30961 0 Dalton Hinesville 33437 976607 29.21 Gainesville P'treeCity 34364 0 Rome 36303 90682 2.50 Dunwoody Smyrna 51271 41242 0.80 Valdosta 54518 0 Marietta 56579 166584 2.94 Alpharetta 57551 0 WarnerRobins 66588 545839 8.20 JohnsCreek 76728 0

51

Albany Roswell 88346 418326 4.74 Macon 91351 4496117 49.22 SandySprings 93853 516114 5.50 Average 11.07 11.63

2011 City Pop Total Per

capitaInflationAdjustment

Kennesaw 30196 139289 4.61 Milton 33711 0 Newnan 33725 176453 5.23 Douglasville 31173 0 Dalton 33313 172275 5.17 Hinesville 34519 406749 11.78 Gainesville P'treeCity 34757 0 Rome 36181 171452 4.74 Dunwoody 46809 0 Smyrna 51982 162197 3.12 Valdosta 56019 0 Marietta Alpharetta 59397 0 WarnerRobins 68500 444389 6.49 JohnsCreek 79192 0 Albany 77683 1617404 20.82 Roswell 91168 1354932 14.86 Macon SandySprings 96856 601319 6.21 Average 5.86 5.98

7.64 4yearinflationadjustedpercapitaaverage

82,205 Studyareapop

$628,868

Total

52

AppendixH

Theregressionmodelwiththehighestexplanatorypowerexpressedfranchisefees

as a function of population, assessed value of commercial property, and had dummy

variables forAugusta, Savannah,Athens‐ClarkeCountyand citieswith apopulationover

100,000.TheadjustedR2forthismodelwas.9979.

RegressionOutput

IndependentVariable

Coefficient Std.Error

t P>t 95%Conf.Interval

Population 56.18269 5.464327 10.28 0.000 44.9287 67.43668

AssessedValueofCommercialProperty

.0026597 .000738 3.60 0.001 .0011397 .0041796

Populationover100,000

3.27e+07 2573598 12.72 0.000 2.74e+07 3.80e+07

Augustadummy

‐2.43e+07 2728944 ‐8.89 0.000 ‐2.99e+07 ‐1.87e+07

Savannahdummy

‐2.99e+07 2356641 ‐12.69 0.000 ‐3.48e+07 ‐2.51e+07

Athens‐ClarkeCountydummy

‐3.24e+07 2628345 ‐12.35 0.000 ‐3.79e+07 ‐2.70e+07

53

AppendixI

CapitalDataTables

DataSourceGeorgiaDepartmentofCommunityAffairsCapitalExpendituresforRoadsandDrainage

PopulationfiguresreflectU.S.CensusBureauAnnualEstimates

2007

CityPopulation TotalCapital

ExpenditureRoadsandDrainage

PerCapita InflationAdjustment